Germany Hearing Aid Retailers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

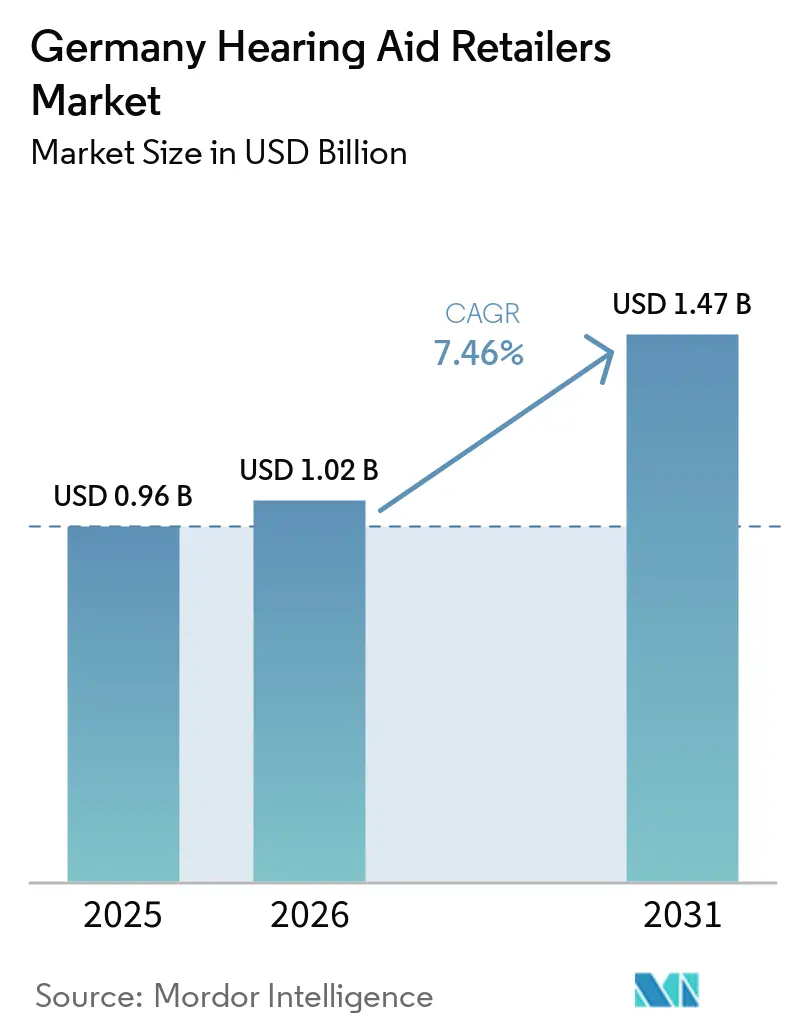

| Base Year Market Size (2025) | USD 0.96 Billion |

| Market Size (2026) | USD 1.02 Billion |

| Market Size (2031) | USD 1.47 Billion |

| Growth Rate (2026 - 2031) | 7.46% CAGR |

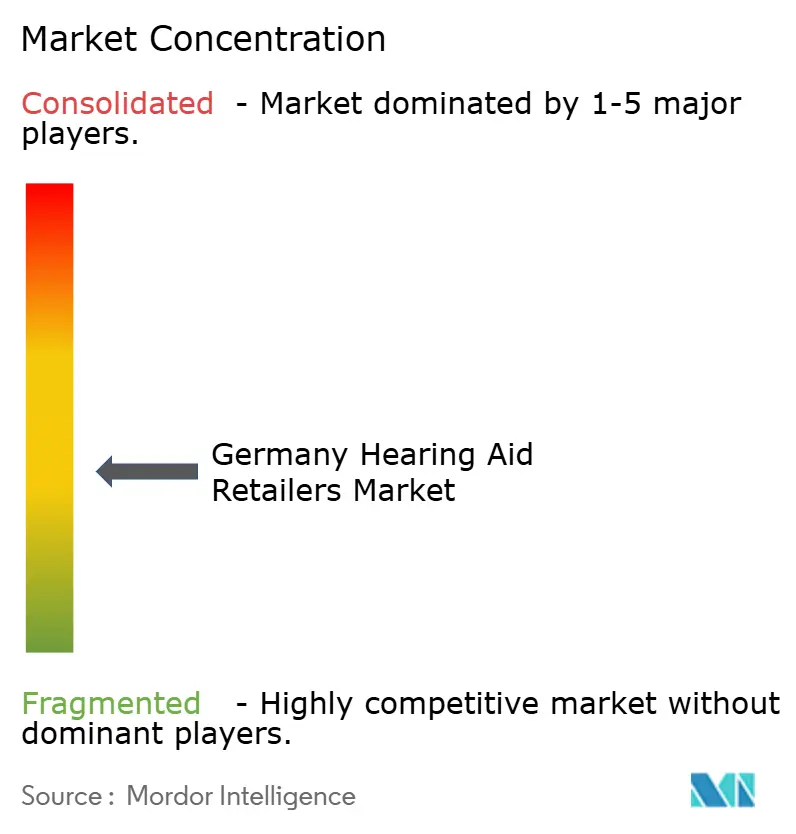

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Hearing Aid Retailers Market Analysis by Mordor Intelligence

The Germany Hearing Aid Retailers Market size is expected to grow from USD 0.96 billion in 2025 to USD 1.02 billion in 2026 and is forecast to reach USD 1.47 billion by 2031 at 7.46% CAGR over 2026-2031.

The Germany hearing aid retailers market is supported by one of Europe’s most structured reimbursement systems, and EuroTrak Germany 2025 shows that 92% of hearing aid users in the country received full or partial support through the statutory GKV pathwa. Demand in the Germany hearing aid retailers market is also being lifted by population aging, because Destatis expects the share of residents aged 67 and older to reach 25% by 2035, up from 20% in 2024. Adoption has improved, but the retail channel still has room to deepen penetration because EuroTrak Germany 2025 reported that hearing aid usage among self-reported hearing-impaired individuals rose to 47% in 2025 from 41.1% in 2022, while a large untreated population remains outside the formal care pathway. Competitive conditions are changing quickly in the Germany hearing aid retailers market as Demant completed the KIND acquisition in December 2025, Amplifon agreed to acquire GN’s hearing business in March 2026, and Fielmann continued to scale its hearing network through its broader optical platform. The main limit on the Germany hearing aid retailers market remains staffing depth, because retailer growth depends not only on demand and reimbursement but also on the availability of qualified hearing care professionals across regional branch networks.

Key Report Takeaways

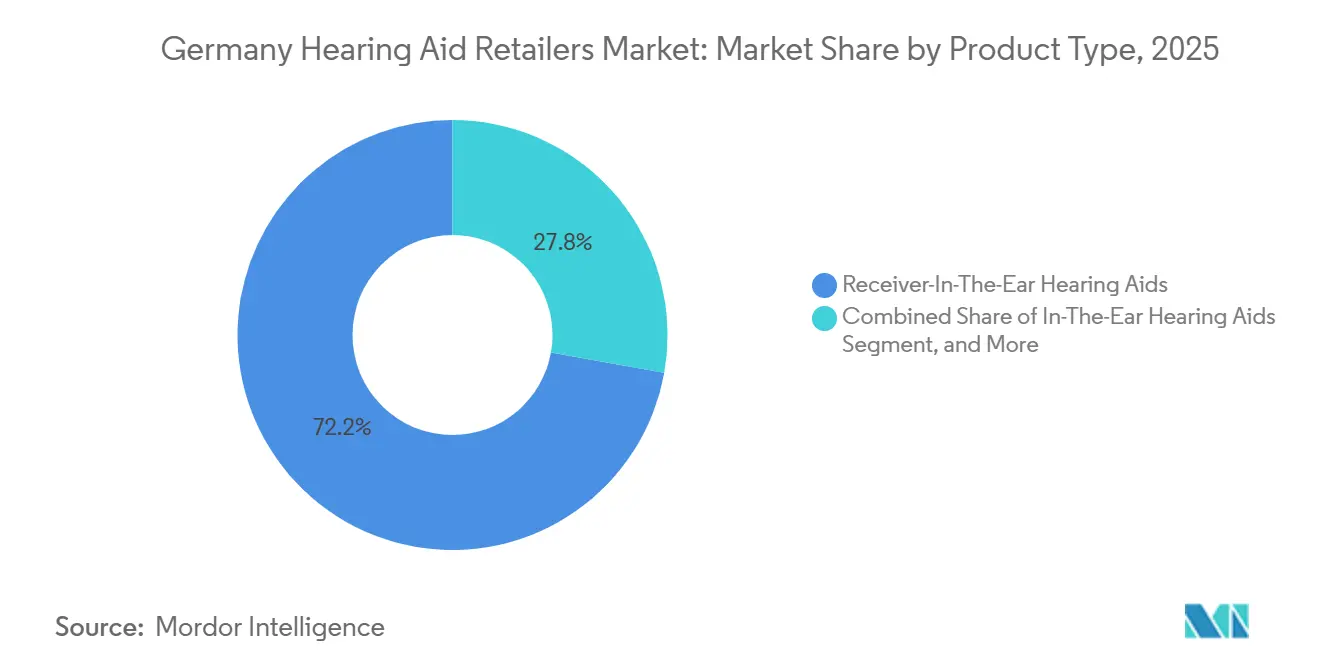

- By product type, receiver-in-the-ear held 72.23% of the Germany hearing aid retailers market share in 2025 and also recorded the fastest projected CAGR at 9.58% through 2031.

- By technology, digital devices accounted for 88.12% of the Germany hearing aid retailers market size in 2025 and remain the fastest-growing technology segment at an 8.85% CAGR through 2031.

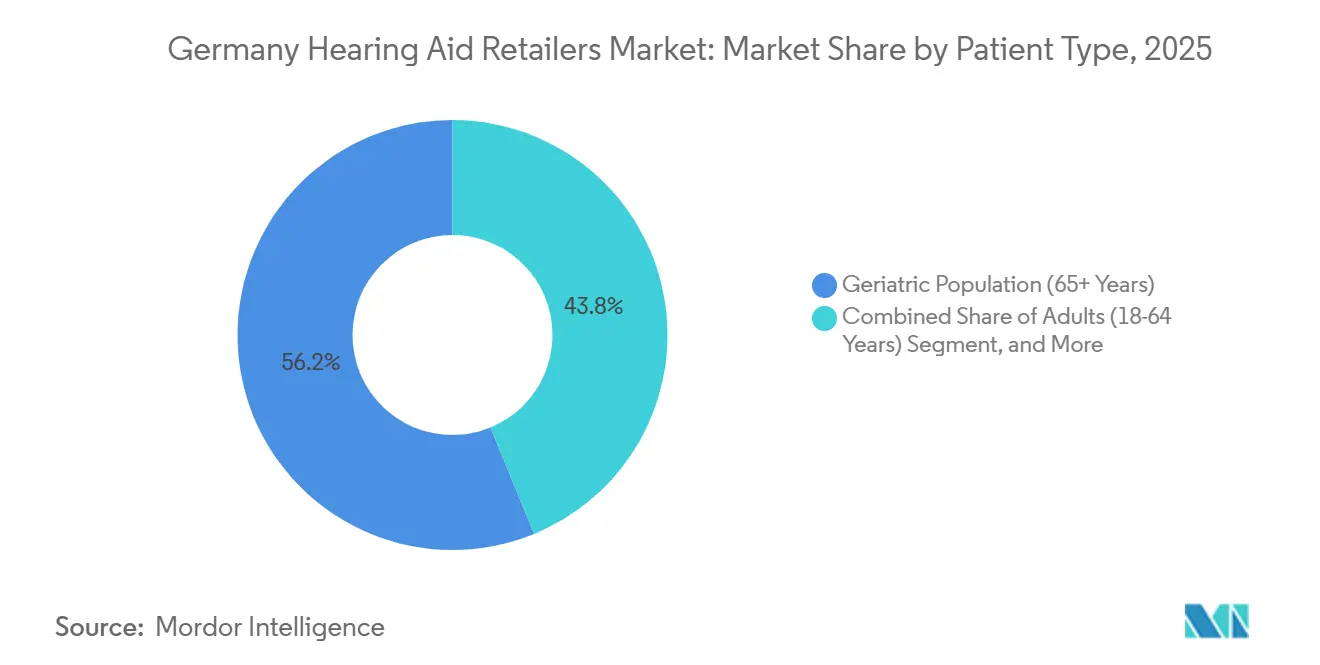

- By patient type, the geriatric segment captured 56.23% of revenue in 2025, while the pediatric segment is forecast to expand at a 10.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Hearing Aid Retailers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population Expands the Hearing-Loss Pool | +2.5% | National, with stronger volume gains in eastern non-city Länder | Long term (≥ 4 years) |

| Statutory Reimbursement Supports First Purchases | +1.5% | National, shaped by §33 SGB V and the updated Hilfsmittel-Richtlinie | Medium term (2-4 years) |

| Bluetooth, App Fitting, and Rechargeability Support Upgrades | +1.2% | National, with premium uptake strongest in major metro areas | Medium term (2-4 years) |

| Omnichannel Retail Improves Trial Conversion | +0.8% | National, with early gains in large cities | Short term (≤ 2 years) |

| Tele-Audiology Reduces Follow-Up Friction | +0.5% | National, strongest in rural and underserved areas | Medium term (2-4 years) |

| Private-Pay Premiumization Lifts Selling Prices | +0.6% | National, concentrated in higher-income consumer groups | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Germany's Aging Population is Expanding the Addressable Hearing-Loss Pool

The Germany hearing aid retailers market is being lifted by a steady increase in older age groups, which are the core population for hearing care demand. Destatis stated in December 2025 that people aged 67 and older will account for 25% of the national population by 2035, compared with 20% in 2024.[1]German Federal Statistical Office, “By 2035, One Quarter of Germany's Population Will Be Aged 67 or Over,” Destatis, destatis.de EuroTrak Germany 2025 also reported that 9.11 million people in Germany describe themselves as hearing impaired, which means the addressable base is already large before the next wave of aging fully arrives. Adoption still sits well below full penetration, so the Germany hearing aid retailers market has room to grow from both first-time users and replacement buyers. That combination keeps aging from being a slow background factor and turns it into a direct retail volume driver through the forecast period.

Statutory Reimbursement Sustains First-Purchase Conversion

The Germany hearing aid retailers market benefits from a medical reimbursement structure that reduces the first-purchase barrier for a large share of users. Germany’s statutory system under §33 SGB V continues to frame hearing aids as a covered medical benefit, while the updated Hilfsmittel-Richtlinie and the June 2025 qualification recommendations tightened quality and documentation expectations for contracted providers.[2]GKV-Spitzenverband, “Hilfsmittel-Richtlinie,” GKV-Spitzenverband, gkv-spitzenverband.de EuroTrak Germany 2025 found that 64% of hearing-impaired non-users did not know about their reimbursement eligibility, which shows that awareness remains a conversion issue rather than pure affordability alone. Retailers that explain eligibility clearly can therefore add volume without waiting for a major shift in household spending patterns. The new compliance burden also favors organized chains and better-documented independents over weaker operators with limited clinical and administrative depth.

Bluetooth, App-Based Fitting, and Rechargeable Devices Are Widening Upgrade Demand

Technology upgrades are creating a more active replacement cycle in the Germany hearing aid retailers market. Oticon launched Zeal in Germany in January 2026 with a nearly invisible in-the-ear design, Bluetooth LE Audio, Auracast connectivity, rechargeability, and same-day fitting, showing how premium features are moving across form factors that previously had a narrower appeal.[3]Oticon, “Oticon Zeal, The World's Most Discreet, Complete Hearing Aid Now Available in the U.S., Canada, and Germany,” Oticon Global, oticon.global That product logic supports retailers because device selection is now tied more closely to connectivity, convenience, and software support over time. Bluetooth and app-based control also keep the customer tied to the retailer after the initial sale through follow-up adjustments and usage support. In the Germany hearing aid retailers market, this makes the premium tier not only more attractive at the point of sale but also more valuable across the life of the device.

Omnichannel Retail Is Improving Conversion from Awareness to Trial

The Germany hearing aid retailers market is moving toward a model where branch consultations, digital booking, and structured follow-up work together instead of competing with each other. Fielmann’s Vision 2035 update shows that the company plans to expand its audiology network from around 450 to more than 700 European locations, using the optical estate as a built-in source of screening traffic and cross-selling opportunities. That matters because awareness does not automatically lead to a store visit, especially among adults who compare options before committing to a fitting. Retailers with stronger digital appointment flows and easier trial management are better placed to turn passive research into branch activity. In the Germany hearing aid retailers market, omnichannel execution is becoming a practical sales tool rather than a branding exercise.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Transparency Compresses Retailer Margins | -0.8% | National, strongest in metro areas with active digital comparison behavior | Short term (≤ 2 years) |

| Skilled Hearing-Care Talent Scarcity Limits Productivity | -0.6% | National, with acute pressure in eastern Länder and rural regions | Long term (≥ 4 years) |

| Digital Comparison Platforms Raise Acquisition Costs | -0.5% | National, concentrated in urban demographics | Short term (≤ 2 years) |

| MDR and Reimbursement Documentation Add Complexity | -0.4% | National, shaped by EU MDR and GKV contracting rules | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Transparency is Compressing Retailer Margins

The Germany hearing aid retailers market faces a clear margin issue even while demand remains healthy. The Bundessozialgericht issued rulings in June 2025 on the conditions under which above-Festbetrag devices qualify for co-funding, and those decisions strengthen the negotiating position of better-informed buyers at the point of sale. That pressure is harder on store-based retailers because their model includes fitting rooms, clinical equipment, audiological labor, and local lease costs that digital-only models do not carry in the same way. Large chains can absorb some of this through scale, procurement leverage, and standardized workflows. Smaller independents in the Germany hearing aid retailers market, therefore, face more pressure on mid-tier pricing than on customer demand itself.

Skilled Hearing-Care Talent Scarcity Limits Branch Productivity

Staffing remains one of the most persistent limits on how fast the Germany hearing aid retailers market can scale. OECD work on Germany’s 2025 labor outlook highlighted strong shortages across health-related occupations, and the Federal Ministry for Economic Affairs has also pointed to sharper skilled-worker gaps in eastern and rural areas. In practice, this means some branches cannot convert all available demand into fittings at the speed the local population would support. Tele-audiology helps with follow-up care, but the initial clinical and reimbursement pathway still depends on qualified people being present in the network. The Germany hearing aid retailers' market, therefore, carries a supply-side limit that is structural rather than temporary.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: RITE Leads, Convergence Reshapes Legacy Formats

Receiver-in-the-ear accounted for 72.23% of the Germany hearing aid retailers market share in 2025 and is projected to grow at a 9.58% CAGR through 2031. That lead reflects a format that works across a wide fitting range and aligns well with rechargeability, Bluetooth connectivity, and easy receiver replacement over time. In the Germany hearing aid retailers market, this makes RITE the main destination for both innovation spending and retailer recommendation patterns. Behind-The-Ear devices still hold an important role for severe-to-profound hearing loss and for pediatric fitting pathways that need durability and adaptability.

In-The-Ear devices are moving back into the premium conversation as their performance gap narrows. Oticon’s Zeal launch in Germany in January 2026 showed that an almost invisible ITE design can now include LE Audio, Auracast, rechargeability, and same-day fitting, which weakens the older tradeoff between discretion and capability. Canal devices remain a narrower specialist format, but they keep relevance for adults who value a more discreet custom fit in daily use. Across the Germany hearing aid retailers industry, the product mix is moving toward formats that combine comfort, connectivity, and long-term service compatibility rather than simply smaller device size.

By Technology: Digital Platform Logic Deepens Structural Advantage

Digital devices held 88.12% of the Germany hearing aid retailers market size in 2025, and this segment is projected to expand at an 8.85% CAGR through 2031. Their lead comes from more than sound processing alone because digital devices now sit inside a broader service model that includes fitting software, app controls, and monitored follow-up. Sinceare, a spin-out linked to Fraunhofer IDMT Oldenburg and Charité Berlin, shows how AI-supported self-fitting can shorten the fitting timeline and reduce clinician chair time in suitable cases. In the Germany hearing aid retailers market, that productivity angle matters because staff availability is a major operating constraint.

Analog devices remain in the channel, but they are now a residual part of the assortment rather than the center of category growth. Their remaining role is strongest in basic low-cost use cases where digital features are less important to the buyer or the care setting. The Germany hearing aid retailers industry is therefore becoming more platform-led, with software support and remote service tools deepening the advantage of digital devices after the initial sale. Retailers that stay brand-agnostic at the service level are better placed to manage switching behavior as device ecosystems become easier for consumers to compare.

By Patient Type: Geriatric Volumes Anchor Revenue, Pediatric Demand Expands Faster

The geriatric segment generated 56.23% of revenue in 2025, making it the largest patient group in the Germany hearing aid retailers market. That weight is supported by a very high prevalence of hearing loss in older cohorts, and the Gutenberg Health Study found that 71.1% of Germans aged 75 to 79 had clinically significant hearing loss. The replacement cycle funded through the statutory system gives this segment a steady revenue base even when product preferences change across device formats. Adults aged 18 to 64 remain less penetrated than their potential suggests, which leaves room for retailers that connect hearing care to work, communication, and daily performance.

The pediatric segment is the fastest-growing group, with a projected 10.52% CAGR through 2031 in the Germany hearing aid retailers market. German registry data show that early intervention remains important, and the German Cochlear Implant Registry reported that 34% of pediatric cochlear implantations occurred before age 2. A BARMER-linked study published in HNO documented a steady flow of hearing device prescriptions among children and adolescents, while the HearAllAges project is expected to support broader pathway development through 2028. This means the Germany hearing aid retailers' market is becoming more balanced across life stages, even though older adults still provide the largest revenue pool.

Geography Analysis

Western non-city Länder form the largest volume base within the Germany hearing aid retailers market because Destatis expects the 67+ population in these states to rise from 12.7 million to 16.3 million by 2039. That demographic scale gives retailers a broad and stable demand base across areas that are less visible than major city clusters but more important in absolute unit potential. The same geography also benefits from the statutory reimbursement system, which keeps entry barriers lower for older first-time users. Major urban centers such as Munich, Hamburg, Frankfurt, and Düsseldorf remain more important for premium mix than for pure volume. Fielmann’s studio expansion strategy fits this pattern because dense urban optical traffic creates efficient hearing screening and referral opportunities inside the same branch network.

Eastern non-city Länder show a different profile in the Germany hearing aid retailers market because aging is already more advanced there than at the national level. Destatis data indicate that 24% of residents in these states were aged 67 and older in 2024, compared with the 20% national average. The demand base is therefore strong, but local staffing shortages make it harder to convert that need into timely fittings and regular follow-up. This is why remote care tools and cooperative operating models have greater practical value in the east than in better-staffed metro markets.

Berlin, Hamburg, and Bremen had 17% of their local populations aged 67 and older in 2024, and Destatis expects this cohort to rise strongly over the long term. These city states support premium retail investment because they combine dense consumer access, strong awareness, and a long runway for aging-led demand growth. Berlin also remains less consolidated than some other parts of the country, which leaves space for both chain expansion and independent multi-brand operators. Across the Germany hearing aid retailers market, regional demand is not the issue, but the balance between local age structure, workforce depth, and premium purchasing behavior shapes how revenue converts from one federal state group to another.

Competitive Landscape

The Germany hearing aid retailers market has moved away from a purely independent structure and now centers on a smaller group of large operators with stronger vertical integration. Demant closed its acquisition of KIND in December 2025 after German antitrust clearance, creating a network of more than 900 clinics in Germany and adding audifon to Demant’s broader hearing care portfolio. That move made scale more important in procurement, contracting, and network management. In March 2026, Amplifon agreed to acquire GN Store Nord’s hearing business, a deal that would combine retail reach with manufacturing and product intellectual property once completed. The Germany hearing aid retailers market therefore, remains fragmented in outlets, but competitive power is shifting toward players that can combine product, service, and distribution at scale.

Sonova’s GEERS brand and Fielmann’s hearing studios remain central members of the first competitive tier. Fielmann reported hearing care sales of around EUR 150 million in 2025 and continues to use its optical network to build hearing customer flow in a way many pure-play operators cannot match. That cross-category model gives Fielmann a structural advantage in awareness generation, appointment conversion, and store economics. In the Germany hearing aid retailers market, this makes branch density important, but it also makes adjacent consumer traffic equally important.

The remaining opportunity is not evenly spread across the country or across patient groups. Working-age adults, underserved rural zones, and pediatric pathways still leave room for differentiated strategies from mid-sized chains and specialized operators. Neuroth is one example of a company trying to stand apart through proprietary product labeling and a stronger focus on clinical equipment quality across its centers. The Germany hearing aid retailers market is thus becoming more concentrated at the top, while still leaving enough room for capable regional players that can meet reimbursement rules, maintain clinical standards, and build local trust.

Germany Hearing Aid Retailers Industry Leaders

AUDILOGIK

auric Management GmbH

HÖREX Hör-Akustik eG

KIND GmbH & Co. KG

OTON Die Hörakustiker

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Amplifon S.p.A. announces a definitive agreement to acquire GN Store Nord's entire hearing business for DKK 17.0 billion, creating a combined entity with approximately EUR 3.3 billion in global revenues across more than 100 countries. The deal is expected to close by end-2026 following regulatory approvals and GN Hearing's operational carve-out, and it targets EUR 60-80 million in run-rate EBITDA synergies by end-2029.

- January 2026: Oticon launches Zeal in Germany, positioning it as the world’s first nearly invisible ITE hearing aid combining second-generation AI sound processing, Bluetooth LE Audio, Auracast connectivity, rechargeability, and a same-day fitting option. The German launch points to rising manufacturer confidence in premium ITE demand within one of Europe’s most established hearing care markets.

- December 2025: Demant closes its EUR 700 million acquisition of KIND Group, Germany’s previously largest independent hearing aid retail chain. The combined Demant footprint in Germany exceeds 900 clinics and expands the group’s global clinic base beyond 4,500.

- November 2025: Germany’s Bundeskartellamt approves the Demant and KIND Group transaction following the divestiture of 3 outlets in the Kassel region. The authority said that possible competition concerns in 15 regional markets did not cross the threshold needed for mandatory prohibition.

Germany Hearing Aid Retailers Market Report Scope

The Germany Hearing Aid Retailers Market includes the network of clinics, audiology centers, and online platforms that distribute and fit hearing devices to consumers.

The Germany Hearing Aid Retailers Market is segmented by product type, technology, and patient demographics. By product type, retailers offer a range of devices, including in‑the‑ear hearing aids, receiver‑in‑the‑ear hearing aids, behind‑the‑ear hearing aids, and canal hearing aids, catering to diverse consumer preferences. By technology, the market is divided into digital and analog solutions, with digital devices dominating due to advanced features and improved sound quality. By patient type, demand is driven across adults (18–64 years), the geriatric population (65+ years) and the pediatric population (0–17 years). The market forecasts are provided in terms of value (USD).

| In-The-Ear Hearing Aids |

| Receiver-In-The-Ear Hearing Aids |

| Behind-The-Ear Hearing Aids |

| Canal Hearing Aids |

| Digital |

| Analog |

| Adults (18-64 Years) |

| Geriatric Population (65+ Years) |

| Pediatric Population (0-17 Years) |

| By Product Type | In-The-Ear Hearing Aids |

| Receiver-In-The-Ear Hearing Aids | |

| Behind-The-Ear Hearing Aids | |

| Canal Hearing Aids | |

| By Technology | Digital |

| Analog | |

| By Patient Type | Adults (18-64 Years) |

| Geriatric Population (65+ Years) | |

| Pediatric Population (0-17 Years) |

Key Questions Answered in the Report

What is the size of hearing aid retail sales in Germany in 2026?

The Germany hearing aid retailers market is valued at USD 1.02 billion in 2026 and is forecast to reach USD 1.47 billion by 2031.

How fast will hearing aid retail demand in Germany grow through 2031?

The market is projected to grow at a 7.46% CAGR from 2026 to 2031, supported by aging demographics, reimbursement access, and premium device upgrades.

Which product format leads sales in Germany?

Receiver-In-The-Ear devices lead the category with a 72.23% share in 2025 and also post the fastest projected growth at 9.58% CAGR through 2031.

Why is statutory reimbursement so important for retailers in Germany?

The GKV pathway keeps first-purchase barriers low, and EuroTrak Germany 2025 shows that 92% of hearing aid users receive full or partial reimbursement support.

Which patient group drives the largest share of revenue?

People aged 65 and above account for 56.23% of revenue in 2025, making older adults the core demand base for the retail channel.

Page last updated on: