Hearing Amplifiers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

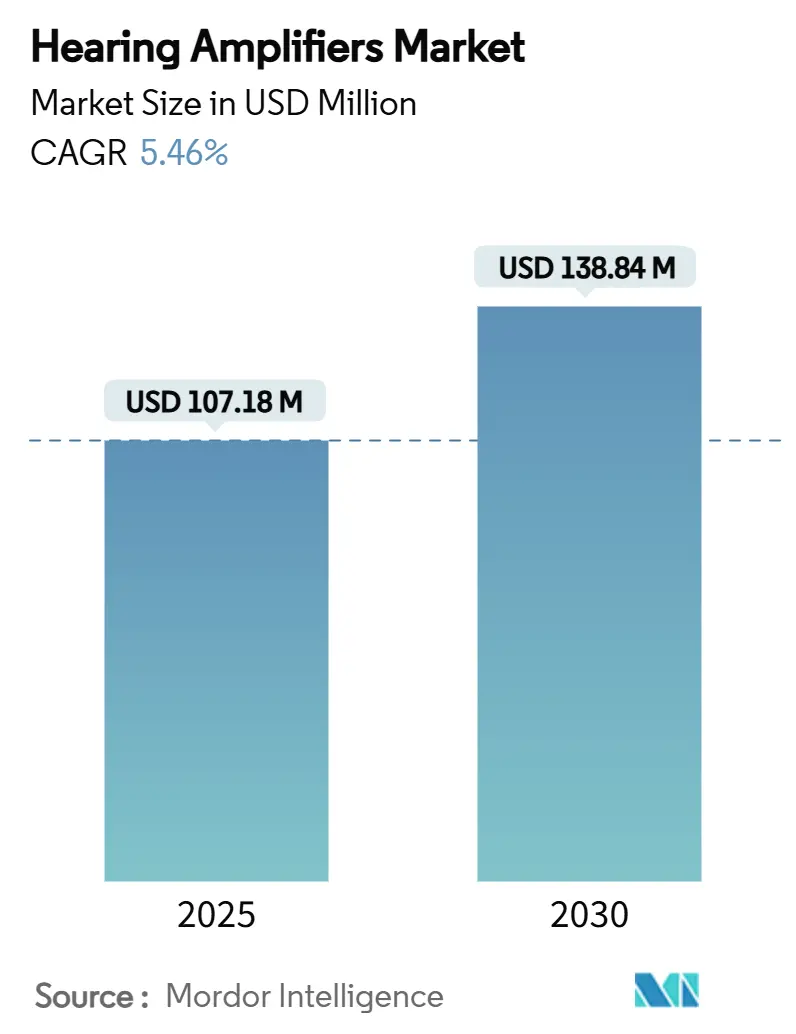

| Market Size (2025) | USD 107.18 Million |

| Market Size (2030) | USD 138.84 Million |

| Growth Rate (2025 - 2030) | 5.46% CAGR |

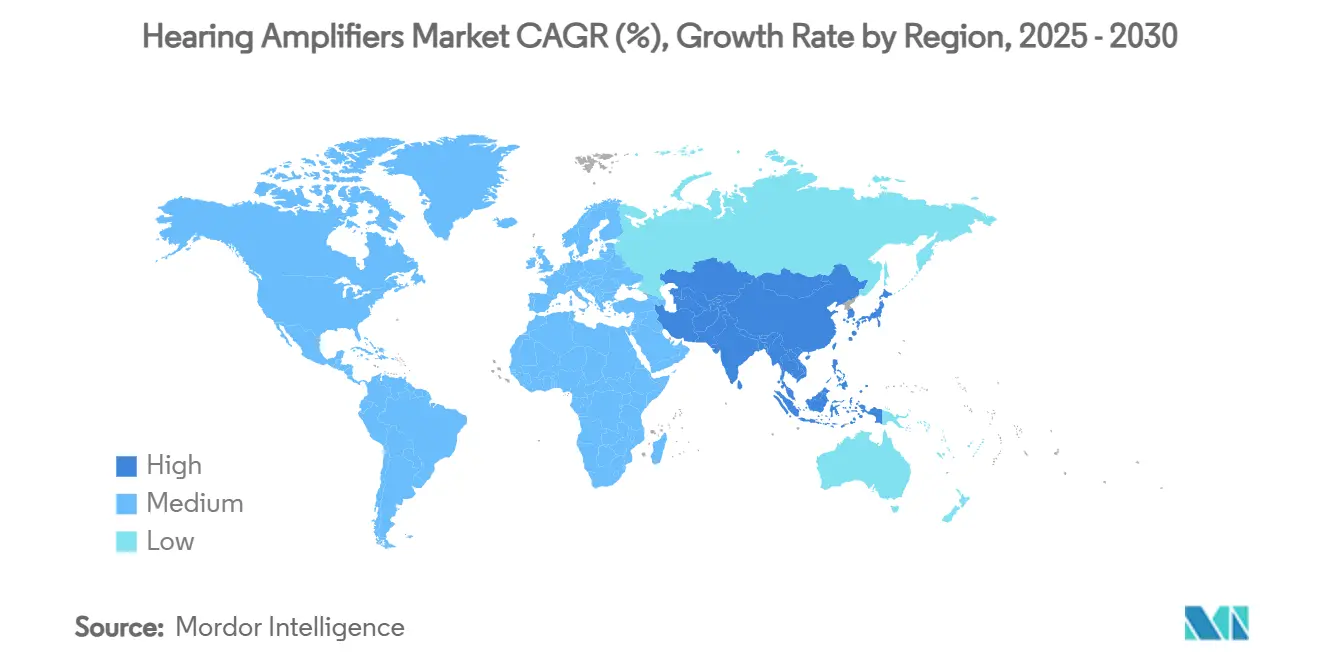

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hearing Amplifiers Market Analysis by Mordor Intelligence

The hearing amplifiers market size stood at USD 107.18 million in 2025 and is forecast to expand to USD 139.84 million by 2030 at a 5.46% CAGR, underscoring steady headway in personal sound-amplification technology and changing consumer access routes. Rising life expectancy, pro-innovation regulation and rapid advances in digital signal processing converge to raise both awareness and adoption. Over-the-counter (OTC) rules in the United States and Japan now allow shoppers to buy amplification products without prescriptions, while Bluetooth LE Audio pushes the devices firmly into the connected-health mainstream. Competitive tactics have shifted toward ecosystem partnerships and miniaturized form factors that remove long-standing stigma, and the hearing amplifiers market is also benefiting from retail audiology chain rollout in populous Asia-Pacific economies. Together, those forces keep pricing pressure contained, support broader distribution and create new revenue lanes for incumbents and entrants alike.

Key Report Takeaways

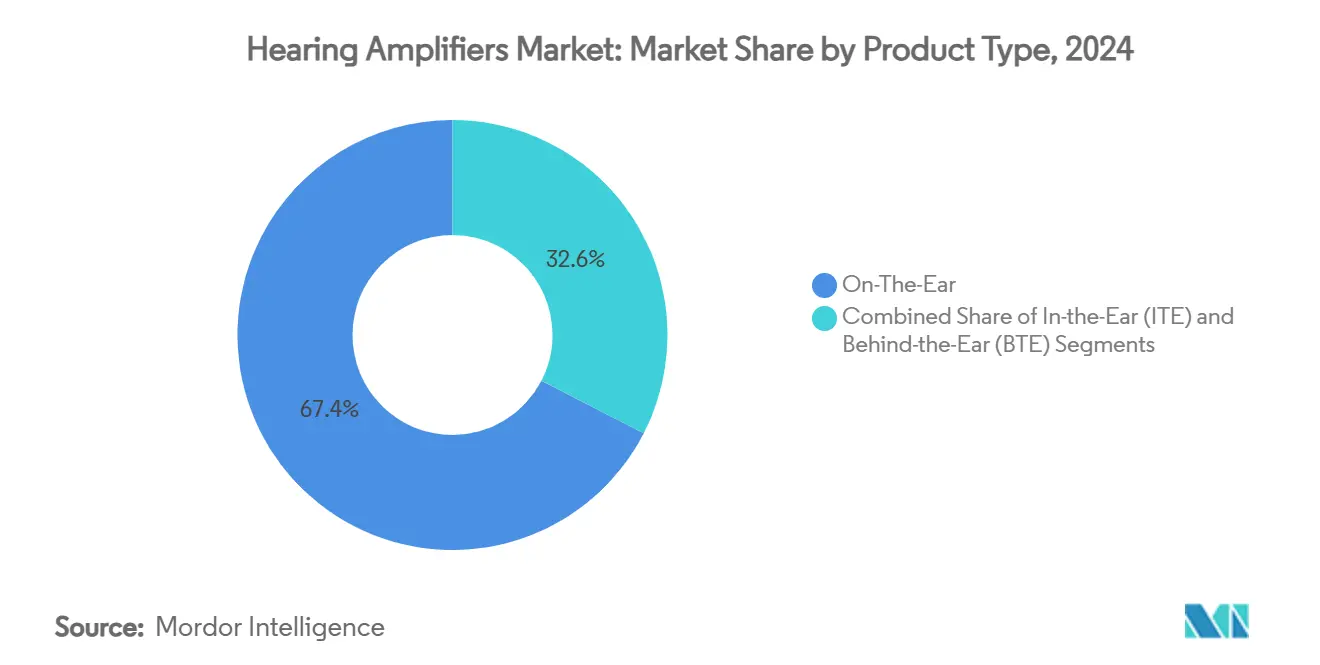

- By product type, on-the-ear devices led with 67.44% revenue share in 2024; in-the-ear solutions are advancing at an 8.89% CAGR through 2030.

- By application, older adults captured 56.78% share of the hearing amplifiers market size in 2024 and pediatrics is projected to rise at an 8.46% CAGR over the same period.

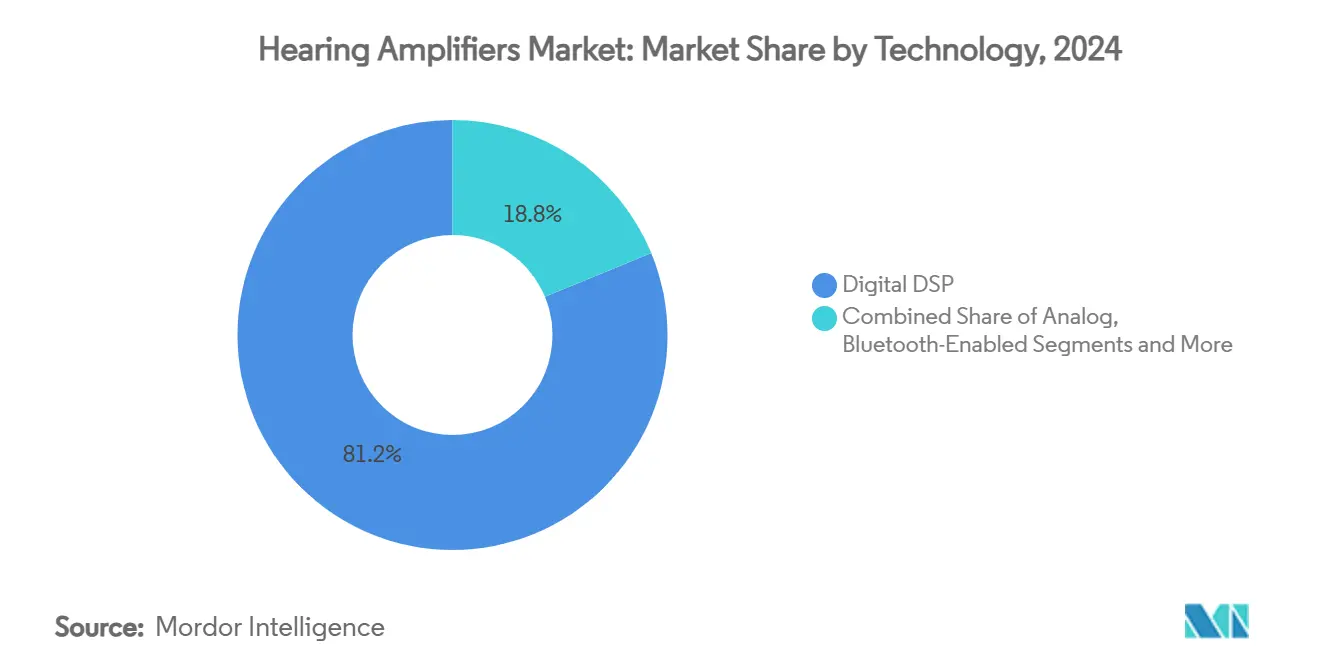

- By technology, digital DSP held 81.23% of the hearing amplifiers market share in 2024, while AI-assisted self-fitting options are moving fastest at a 10.03% CAGR to 2030.

- By sales channel, offline retail accounted for 69.73% share in 2024 and online direct-to-consumer is poised to register a 9.78% CAGR through 2030.

- By region, North America remained the largest revenue contributor at 34.55% in 2024 and Asia-Pacific is forecast to record a 7.67% CAGR to 2030.

Global Hearing Amplifiers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing-world population accelerates mild-to-moderate hearing-loss prevalence | +0.8% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| OTC pathway in US & Japan slashes entry barriers | +0.7% | North America & Japan, expanding into EU | Medium term (2-4 years) |

| Smartphone-centric DSP & Bluetooth-LE Audio integration | +0.5% | Global, led by developed markets | Short term (≤ 2 years) |

| Retail audiology chain expansion in emerging APAC | +0.4% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Voice-first wearables converging with PSAPs | +0.4% | North America & EU early adoption | Medium term (2-4 years) |

| AI-based self-fitting apps cut professional costs | +0.3% | Global, premium market focus | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ageing-world population accelerates mild-to-moderate hearing-loss prevalence

WHO projects that 2.5 billion people will experience some form of hearing loss by 2050. Eighty-three percent of cases occur in individuals older than 50, yet penetration of amplification devices remains below 25% in the 65-plus cohort.[1]World Health Organization, “Deafness and Hearing Loss,” who.int Advancing smartphone literacy among baby boomers removes technical barriers, and clinical studies of nonagenarians report 98% incidence of measurable hearing loss, emphasizing unmet need. Longer life expectancy and changing lifestyle expectations therefore form the largest single demand catalyst for the hearing amplifiers market.

OTC pathway in US & Japan slashes entry barriers

The US Food & Drug Administration’s 2022 rule created the first true OTC class for mild-to-moderate hearing loss devices, and Apple’s AirPods Pro obtained FDA software authorization in September 2024 at a USD 250 price point.[2]U.S. Food and Drug Administration, “FDA Authorizes First Over-the-Counter Hearing Aid Software,” fda.gov Comparable legislation under discussion in Japan signals regulatory harmonization. Controlled trials show 97% of users achieve feedback-free performance with self-fitted OTC devices. Mainstream retail placement dismantles medical-device stigma, widens distribution and compresses average selling prices, fueling additional uptake across the hearing amplifiers market.

Smartphone-centric DSP & Bluetooth-LE Audio integration

Bluetooth LE Audio with Auracast broadcasting lets wearers wirelessly receive sound in airports, theaters and televisions without auxiliary accessories. Starkey and LG enabled Auracast streaming in 2025 OLED TVs. Android’s native support for GN and Oticon aids on flagship smartphones further links amplification to mobile ecosystems. Unified interfaces for calls, media and venue broadcasts reposition devices as everyday connected-health accessories, accelerating demand growth.

Retail audiology chain expansion in emerging APAC

Asia-Pacific retail networks move beyond clinic-only sales. WS Audiology operates with more than 6,000 hearing-care partners in China and posted 30% revenue expansion in 2024. New stores, mobile vans and e-commerce platforms extend reach into rural counties, compress prices and speed uptake. Localization of R&D in Hyderabad supports product tailoring to regional cost structures.[3]WS Audiology, “WS Audiology Strengthens Commitment to Innovation with New R&D Centre of Excellence in Hyderabad,” wsa.com The pattern positions APAC as the fastest-growing geography in the hearing amplifiers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low reimbursement / insurance coverage in most countries | −0.4% | Global, acute in developing markets | Long term (≥ 4 years) |

| High device return rates due to user comfort issues | −0.3% | Global, higher in OTC segments | Short term (≤ 2 years) |

| Growing counterfeit & grey-market devices | −0.3% | Asia-Pacific & other emerging markets | Medium term (2-4 years) |

| Lithium-ion battery disposal concerns | −0.2% | EU leading, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low reimbursement / insurance coverage in most countries

Traditional Medicare does not fund hearing aids, and Medicare Advantage allotments vary from USD 500 to USD 4,000 per ear. Device prices of USD 2,500-8,000 per pair leave many seniors without coverage; only 25% of those with hearing loss currently use amplification. Cash-pay hurdles fragment the addressable base and limit premium prescription growth, moderating the overall hearing amplifiers market trajectory.

High device return rates due to user comfort issues

Users often expect normal hearing restoration yet struggle with background-noise limitations. Qualitative studies highlight frustration with acoustics, fit and sound delays. Deep neural-network noise reduction improves satisfaction but even 5-7 millisecond processing lags can erode auditory phase locking. High return rates create inventory risk for retailers and dent brand loyalty across the hearing amplifiers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Miniaturization strengthens in-the-ear adoption

In 2024, on-the-ear devices captured 67.44% of total revenue, reflecting widespread familiarity, larger batteries and straightforward controls. However, in-the-ear (ITE) units are on track for an 8.89% CAGR because shrinking components allow near-invisible styling that appeals to first-time users. Behind-the-ear models remain indispensable for severe loss categories requiring maximum gain.

Missed social cues and aesthetic apprehension have long dissuaded prospective buyers. ITE advances such as Eargo 8’s Smart Sound Adjust provide 97% feedback-free performance while maintaining barely visible profiles. The new hearing-glasses category, led by FDA-cleared Nuance Audio frames, further lowers stigma. These innovations position ITE and hybrid eyewear to capture incremental share in the hearing amplifiers market size across the forecast horizon.

By Application: Pediatric demand gains ground

Older adults aged 65 plus generated 56.78% of 2024 revenue in line with epidemiological patterns, whereas pediatric fittings are projected for an 8.46% CAGR despite OTC age restrictions. Heightened awareness of speech-development benefits and incremental insurance support drive uptake. Adults 18-64 sit between the two, supported by employer wellness programs recognising occupational noise exposure.

Case studies on bone-conduction solutions such as bilateral Adhear devices show word-recognition gains from 10% to 80% within four weeks for children. Once regulators craft safe OTC pathways for minors, the segment could unlock fresh volume layers for the hearing amplifiers market.

By Technology: AI disrupts legacy DSP

Digital DSP retains 81.23% share today owing to proven speech-clarity gains; yet AI self-fitting tools are rising at a 10.03% CAGR to 2030. Bluetooth-enabled devices occupy middle ground, adding streaming without full autonomy, while analog persists in budget niches.

GN’s ReSound Vivia houses a dedicated deep-neural chip trained on 13.5 million sentences, tailoring amplification in real time. Meta’s contextual-awareness patents foreshadow broader predictive tuning ecosystems. As AI lowers reliance on professional fitting, technology mix will tilt toward intelligent, connected devices, expanding the hearing amplifiers market size for premium features.

By Sales Channel: Online ascendancy challenges clinics

Offline retail—mainly audiology clinics and pharmacies—controlled 69.73% of 2024 volume. OTC deregulation and user-guided apps spur a 9.78% CAGR for online direct-to-consumer sales, luring price-sensitive buyers and digital natives.

Eargo combines website sales with selective storefronts to spread risk, while Amplifon acquired 35 U.S. Miracle-Ear outlets in April 2024 to reinforce physical coverage. Hybrid “click-and-fit” models merging virtual orders and local service are likely to dominate distribution within the hearing amplifiers market.

Geography Analysis

North America accounted for 34.55% of 2024 revenue thanks to OTC regulations, insurance experimentation and a sizeable 65-plus demographic. Europe followed, supported by public health frameworks and early Bluetooth-LE rollouts. Asia-Pacific is set for the quickest climb at 7.67% CAGR through 2030 as chain stores, e-commerce and mobile vans proliferate.

In China, WS Audiology’s network of 6,000 partners combined with 30% annual revenue growth signals robust rural expansion capacity. India benefits from Hyderabad-based R&D that cuts localization time for lower-cost SKUs. Middle East & Africa gain from smartphone penetration that supports Bluetooth-enabled OTC units, while South America inches forward on broader healthcare access initiatives.

Diverging infrastructure maturity shapes the regional mix: established clinic pathways cap incremental upside in developed economies, whereas direct-purchase channels unlock faster gains across emerging nations, ensuring Asia-Pacific remains the hearing amplifiers market’s growth engine.

Competitive Landscape

The hearing amplifiers market shows moderate concentration: the top five vendors hold a combined share in the high-60% range. Sonova, Demant and GN Store Nord commit more than 12% of revenue to R&D but now face price erosion from OTC-focused disruptors. Starkey and WS Audiology captured additional U.S. Veterans Affairs account wins in 2024 as Demant and GN ceded ground.

Competitive advantage pivots on AI, cloud connectivity and fashionable design rather than raw amplification power. Samsung’s patent for object-focused sound capture and Sony’s efforts in personalized head-related transfer functions exhibit the cross-industry innovation race. Consumer electronics newcomers leverage scale efficiencies and brand recognition to compress price tiers, compelling legacy players to accelerate product-refresh cycles.

White-space niches continue to emerge. Voice-first earbuds, smart spectacles and upgradable cochlear implants broaden category boundaries, forcing mid-tier brands to consolidate or specialize. The anticipated outcome is gradual market share realignment but sustained overall expansion for the hearing amplifiers market.

Hearing Amplifiers Industry Leaders

Sonova Holding AG

Demant A/S

GN Store Nord A/S

WS Audiology

Starkey Hearing Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Cochlear Limited introduced the Nucleus Nexa smart cochlear implant system featuring firmware upgrades and the smallest sound processor to date.

- February 2025: EssilorLuxottica obtained FDA clearance for Nuance Audio Glasses, combining directional microphones with fashionable frames.

- January 2025: Ambiq announced Apollo510 microcontroller integration that enables edge-AI speech enhancement for OTC devices, lowering power draw in extended wearables.

Global Hearing Amplifiers Market Report Scope

| In-the-Ear (ITE) |

| On-the-Ear (OTE) |

| Behind-the-Ear (BTE) |

| Older Adults (65+) |

| Adults (18-64) |

| Pediatrics |

| Analog |

| Digital DSP |

| Bluetooth-Enabled |

| AI-Assisted / Self-Fitting |

| Offline Retail (Audiology & Pharmacies) |

| Online / Direct-to-Consumer |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | In-the-Ear (ITE) | |

| On-the-Ear (OTE) | ||

| Behind-the-Ear (BTE) | ||

| By Application | Older Adults (65+) | |

| Adults (18-64) | ||

| Pediatrics | ||

| By Technology | Analog | |

| Digital DSP | ||

| Bluetooth-Enabled | ||

| AI-Assisted / Self-Fitting | ||

| By Sales Channel | Offline Retail (Audiology & Pharmacies) | |

| Online / Direct-to-Consumer | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the global hearing amplifiers market today?

The hearing amplifiers market size reached USD 107.18 million in 2025 and is projected to hit USD 139.84 million by 2030.

Which region will grow fastest between 2025 and 2030?

Asia-Pacific is poised for the highest regional CAGR at 7.67% thanks to retail chain rollouts, e-commerce and demographic trends.

What technology segment is expanding most quickly?

AI-assisted self-fitting solutions are expected to rise at a 10.03% CAGR through 2030, outpacing traditional DSP and Bluetooth-only models.

Why are OTC rules important for future sales?

OTC legislation lowers entry barriers, removes prescription requirements and lets retailers sell devices at consumer-electronics price points, broadening adoption.

Which product form factor is gaining share?

In-the-ear units and hybrid hearing-glasses are growing fastest because miniaturization and aesthetic styling reduce visibility concerns.

What is driving online channel growth?

Self-fitting apps, transparent pricing and shifting buyer preferences are pushing online direct-to-consumer sales toward a 9.78% CAGR through 2030.

Page last updated on: