Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

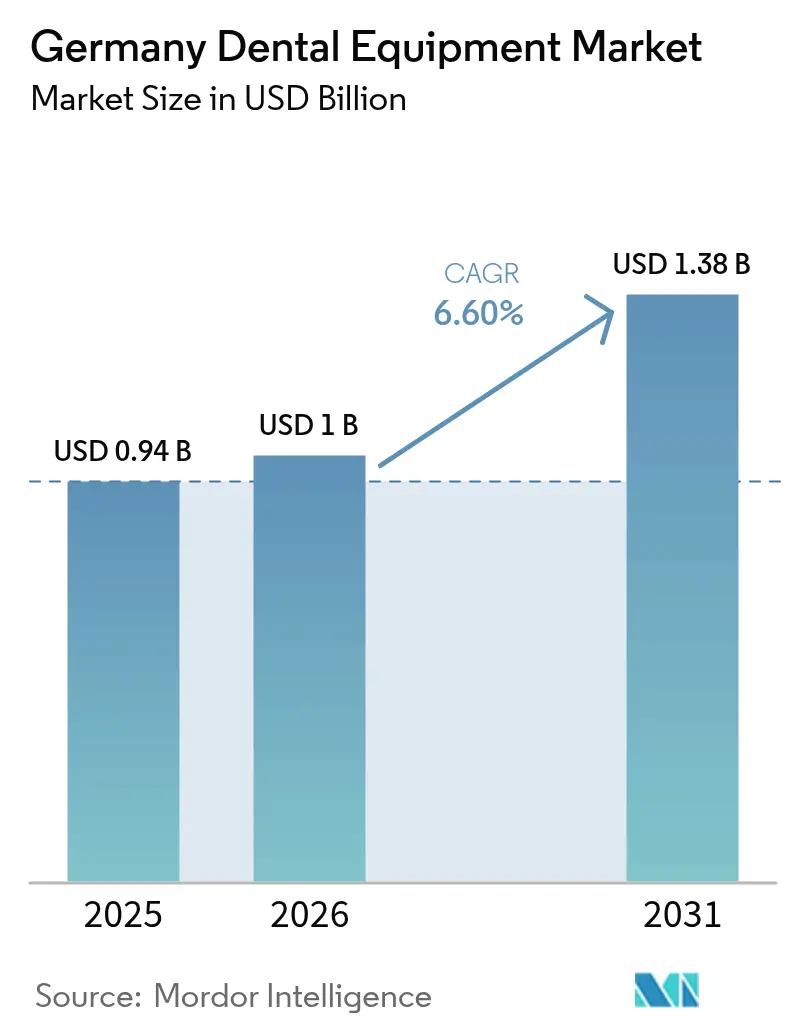

| Base Year Market Size (2025) | USD 0.94 Billion |

| Market Size (2026) | USD 1 Billion |

| Market Size (2031) | USD 1.38 Billion |

| Growth Rate (2026 - 2031) | 6.60% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Dental Equipment Market Analysis by Mordor Intelligence

The German dental equipment market size in 2026 is estimated at USD 1 billion, growing from 2025 value of USD 0.94 billion with 2031 projections showing USD 1.38 billion, growing at 6.60% CAGR over 2026-2031. Demand is accelerating as digital technologies lower chair time, corporate Dental Service Organizations (DSOs) consolidate purchasing power, and an aging population increases restorative treatment volumes. Intraoral scanners, 3D printers, and laser systems are moving from niche to mainstream, while refurbished imports temper average selling prices. Competitive pressure is intensifying: global leaders are bundling cloud-based software with hardware, mid-tier specialists focus on feature depth, and budget suppliers leverage EU secondary markets. Germany’s robust statutory insurance coverage keeps baseline procedure flows predictable, yet limited reimbursement for aesthetic care channels equipment spending toward high-margin private treatments concentrated in metropolitan areas.

Key Report Takeaways

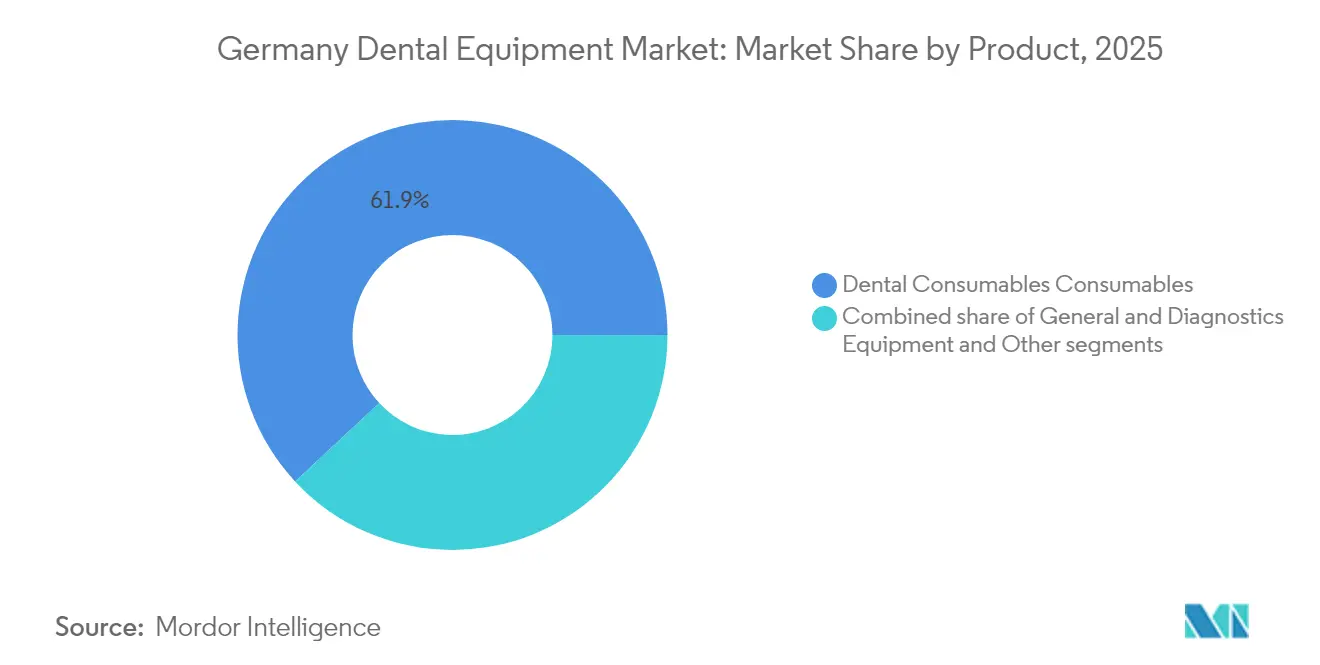

- By product category, dental consumables led with 61.92% revenue share in 2025; general and diagnostics equipment is forecast to expand at a 7.08% CAGR to 2031.

- By treatment type, orthodontic treatment held 31.86% of the German dental equipment market share in 2025; prosthodontics is projected to advance at a 7.29% CAGR through 2031.

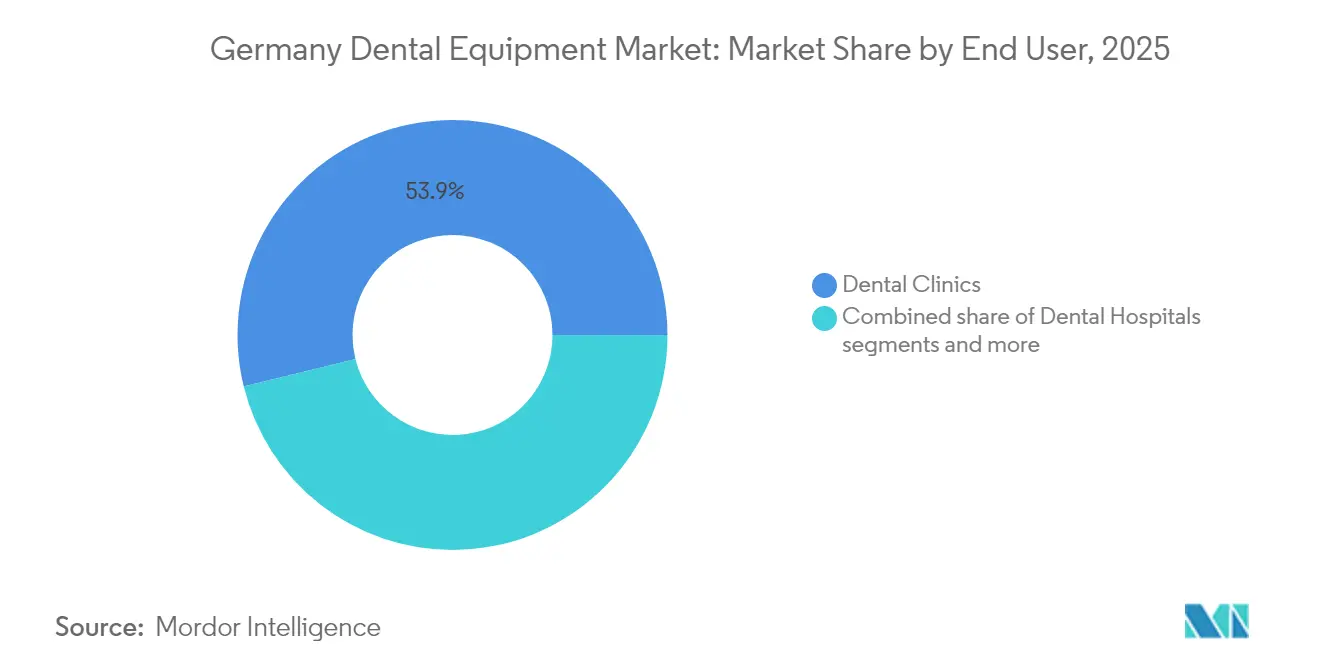

- By end-user, dental clinics commanded 53.85% share of the German dental equipment market size in 2025 and are projected to grow at a 7.62% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Dental Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Uptake of CAD/CAM Systems | +1.6% | National, with early gains in urban centers | Medium term (≈3-4 yrs) |

| Booming Clear Aligner Demand | +1.4% | National, concentrated in metropolitan areas | Short term (≤2 yrs) |

| Increasing Incidences of Dental Diseases | +0.9% | National, higher impact in aging regions | Long term (≥5 yrs) |

| Shift to Laser Periodontal Therapy | +0.7% | Urban centers initially, gradual national adoption | Medium term (≈3-4 yrs) |

| Growing DSO Consolidation | +1.5% | National, with concentration in western Germany | Medium term (≈3-4 yrs) |

| Strong Export Incentives for Made-in-Germany Products | +0.8% | National, with focus on manufacturing regions | Long term (≥5 yrs) |

| Source: Mordor Intelligence | |||

Rapid Uptake of CAD/CAM Systems

German clinics are integrating chairside CAD/CAM ecosystems that pair Primescan 2 scanners with cloud-based DS Core design software, cutting single-visit restoration time in half and reducing lab dependencies. Uptake is most visible in multi-chair urban offices where higher patient throughput justifies capital outlays. DSOs standardize these platforms across networks, enabling centralized training and bulk pricing leverage. As material choices widen—from hybrid ceramics to zirconia blocks—clinicians improve margin capture by bringing milling in-house. Financing models offering five-year 0% plans mitigate cost barriers, yet solo practices in rural regions still postpone adoption, widening the technology gap within the German dental equipment market.

Booming Clear Aligner Demand

German patients pay privately for aesthetic correction, prompting clinics to invest in high-accuracy scanners, treatment-planning AI, and 3D printers for aligner models. Practice marketing pivots toward “invisible dentistry,” and metro offices report case fees 20% above 2022 levels. The resulting equipment upgrade cycle sustains scanner and printing sales while driving recurring revenue from software subscriptions, cementing digital workflows within the German dental equipment market.

Shift to Laser Periodontal Therapy Reducing Surgical Downtime

German clinicians are rapidly incorporating diode, Er:YAG, and Nd:YAG lasers into periodontal protocols because these devices cut tissue with minimal thermal damage, deliver excellent hemostasis, and shorten healing time compared with scalpel surgery. Clinics advertise “no-suture” treatment packages that command 15-20% higher fees, improving payback on laser units priced at USD 25,000-40,000. DSOs are standardising laser platforms across multi-site networks to simplify staff training and leverage bulk-purchase discounts, further accelerating adoption. Regulatory alignment with Germany’s MDR has also become easier because leading manufacturers now ship pre-configured treatment protocols that document energy settings and exposure times, easing compliance audits. Together, these clinical, economic, and regulatory benefits elevate laser periodontal therapy from an optional add-on to a mainstream driver of equipment spending within the German dental equipment market.

Increasing Dental Disease Incidence

Direct spending on oral diseases in Germany hit USD 30.88 billion—8% of global outlays[1]Source: Nityanand Jain, “WHO Global Oral Health Status Report,” onlinelibrary.wiley.com . Caries and periodontal disease prevalence rises with population aging, fueling demand for implant motors, CBCT imaging, and regenerative biomaterials. Preventive awareness initiatives highlight systemic links between periodontitis and diabetes, pushing clinics to expand prophylaxis programs that require ultrasonic scalers and air-polishing units. This epidemiological pressure underpins steady baseline growth even when cosmetic spending fluctuates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-Intensity of Digital Workflows | -1.1% | National, higher impact in rural areas | Short term (≤2 yrs) |

| Price Competition & Limited Reimbursement | -0.8% | National | Medium term (≈3-4 yrs) |

| Stringent MDR Re-certification Costs | -0.6% | National, higher impact on smaller manufacturers | Short term (≤2 yrs) |

| Limited Reimbursement for Aesthetic Procedures | -0.4% | National, concentrated in premium market segments | Medium term (≈3-4 yrs) |

| Source: Mordor Intelligence | |||

Capital-Intensity of Digital Workflows

A full in-office digital chain—scanner, design software, milling unit, and 3D printer—can cost more than USD 162,000. While DSOs amortize this across multiple sites, solo owners face strain, delaying upgrades and lengthening payback periods. Rapid innovation cycles amplify obsolescence fears, making leasing and pay-per-use models attractive yet complex to manage. This funding gap risks widening performance disparities across the German dental equipment market.

Price Competition & Limited Reimbursement

Refurbished units imported from EU neighbors undercut new list prices by up to 40%, appealing to start-ups and budget-conscious practices. Statutory insurance exclusions on cosmetic services cap revenue potential for lasers and high-end CAD/CAM tools focused on anterior aesthetics. Manufacturers respond with modular offerings and subscription software to defend margins, but ASP pressure persists, slowing premium adoption outside major cities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Digital integration accelerates diagnostics dominance

Dental consumables sustained a 61.92% share of the German dental equipment market in 2025 as restorative and implant procedures remained routine. Recurrent demand for bonding agents, impression materials, and biomaterials provides manufacturers with predictable volume, offsetting price erosion. Meanwhile, the general and diagnostics equipment category is projected to grow fastest at 7.08% CAGR through 2031, propelled by demand for radiation-free intraoral cameras like KaVo’s DIAGNOcam Vision Full HD.

Dental chairs now ship with integrated electric motors, touch-screen controls, and IoT sensors that feed maintenance analytics into cloud dashboards. Partnerships such as the 2025 KaVo–A-dec integration enable plug-and-play handpiece connectivity, improving operatory ergonomics. Laser platforms covering diode, Er:YAG, and Nd:YAG wavelengths gain traction for soft-tissue contouring and cavity preparation. Emerging “other devices” lines, including digital shade-matching cameras and sleep-apnea oral appliances, add ancillary revenue streams yet remain sub-5% of the German dental equipment market.

By Treatment: Aesthetic demand reshapes orthodontic and prosthodontic spend

Orthodontics held 31.86% of the German dental equipment market share in 2025 and continues to anchor scanner and software demand. Clear aligner workflows require high-resolution imaging, cloud design, and in-office 3D printing, creating cross-selling opportunities for equipment vendors. Prosthodontics, aided by implant stability metrics and fully guided surgical kits, is forecast to grow at 7.29% CAGR, lifting the German dental equipment market size for implant motors and CBCT units.

Endodontic treatments benefit from motors that combine integrated apex locators with reciprocating file systems like Dentsply Sirona’s X-Smart Pro+. Periodontics leverages diode and Nd:YAG lasers to reduce bacterial load and postoperative pain, fostering patient preference for minimally invasive options. Preventive focus and digital case-acceptance tools stimulate demand for photo-documentation cameras and fluorescence caries-detection devices, broadening the equipment basket purchased per treatment.

By End-User: Clinics spearhead the digital wave

Dental clinics accounted for 53.85% of the German dental equipment market size in 2025 and are projected to lead growth at a 7.62% CAGR. Consolidation under DSOs, exemplified by zahneins’ 80-location network, gives clinics scale to negotiate bundled hardware-software packages. Clinics also pioneer “scan-plan-mill-seat” workflows that align with patient demand for same-day dentistry.

Hospitals, though smaller in number, specify high-end CBCT and surgical navigation systems for complex maxillofacial cases. Academic institutes invest in research-grade printers and AI analytics to validate new restorative protocols, shaping curricula that normalize digital workflows for graduates. Combined, these end-users ensure multi-channel demand diversity within the German dental equipment market.

Geography Analysis

The western Länder—North Rhine-Westphalia and Bavaria—concentrate procedure volume and equipment spend thanks to dense populations and higher disposable income. Munich, Frankfurt, and Berlin clinics routinely deploy chairside milling and diode lasers, shortening restorative cycles and marketing “one-visit” services. Eastern states still lag in scanner penetration but record above-average equipment order growth as EU structural funds support healthcare modernization.

DSO expansion strategies mirror economic clusters: zahneins and Colosseum Dental target commuter belts around Düsseldorf and Hamburg where clinic ownership turnover is rising. Rural practices lean toward refurbished units, sustaining a parallel grey market that satisfies entry-level needs. Manufacturers calibrate channel strategy accordingly, directing premium bundles to urban hubs and modular systems to smaller towns, ensuring broad German dental equipment market coverage.

Cross-border patient flows from Austria and Switzerland into Bavaria bolster implant and aesthetic case volumes, indirectly raising local equipment utilization. Conversely, clinics near Polish and Czech borders face outbound leakage of price-sensitive patients, reinforcing the value proposition of low-maintenance refurbished chairs. Overall, the German dental equipment market exhibits geographic polarization tied to economic vigor and technology adoption speed.

Competitive Landscape

Global majors including Dentsply Sirona and Straumann Group lead through end-to-end digital ecosystems that bundle cloud platforms with scanners and mills;. Mid-sized European brands such as KaVo and Dürr Dental differentiate on ergonomics, imaging clarity, and service networks. Local refurbishers like Ambident thrive on cost-driven segments, extending product lifecycles and pressuring new-unit ASPs.

Strategic activity centers on platform integration and DSO-oriented solutions: Dentsply Sirona’s DS Core Enterprise tailors multi-location data flows, while Straumann’s Enterprise Solutions division supports standardized implant protocols. Partnerships—KaVo with A-dec, Henry Schein with Large Practice Sales—signal an ecosystem race that values workflow stickiness over hardware margins. MDR compliance funnels regulatory costs to smaller manufacturers, raising barriers and nudging the German dental equipment market toward moderate concentration.

Innovation now extends beyond hardware into AI-driven treatment planning and analytics dashboards that predict maintenance needs. Vendors invest in sustainability, exemplified by Dentsply Sirona’s solar-powered Elz site cutting 13.6 tons of CO₂e annually. Competitive intensity therefore hinges on holistic value propositions—clinical efficiency, regulatory support, environmental footprint, and financing flexibility.

Germany Dental Equipment Industry Leaders

Biolase Inc.

GC Corporation

Danaher Corporation (Nobel Biocare)

Dentsply International Inc.

3M

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Planmeca launched the Pro40 and Pro50 S dental units with ergonomic designs, digital integration, improved hygiene, and sustainable solutions.

- November 2024: Dentsply Sirona reported that its German operations contributed significantly to its European performance, with particular strength in digital equipment sales despite overall challenges in the broader European market Dentsply Sirona.

- August 2024: Straumann Group announced the sale of its DrSmile aligner business to Barcelona-based Impress Group, retaining a 20% minority stake in the combined entity while refocusing on business-to-business orthodontics activities in the German market, signaling a strategic shift away from direct-to-consumer clear aligner services

Germany Dental Equipment Market Report Scope

Dental instruments are tools used by dental professionals to provide dental treatment. They include tools to examine, manipulate, treat, restore, and remove teeth and surrounding oral structures.

The Germany Dental Equipment Market is Segmented by Product (General and Diagnostics Equipment (Dental Laser, Radiology Equipment, Dental Chair and Equipment, and Other General and Diagnostic Equipment), Dental Consumables (Dental Biomaterial, Dental Implants, Crowns and Bridges, Other Dental Consumables), and Other Dental Devices), Treatment (Orthodontic, Endodontic, Periodontic, and Prosthodontic), and End-User (Hospital, Clinics, and Other End-Users). The report offers value (in USD million) for the above segments.

By Product

| General and Diagnostics Equipment | Dental Laser | Soft Tissue Lasers |

| Hard Tissue Lasers | ||

| Radiology Equipment | Extra Oral Radiology Equipment | |

| Intra-oral Radiology Equipment | ||

| Dental Chair and Equipment | ||

| Other General and Diagnostic equipment | ||

| Dental Consumables | Dental Biomaterial | |

| Dental Implants | ||

| Crowns and Bridges | ||

| Other Dental Consumables | ||

| Other Dental Devices | ||

By Treatment

| Orthodontic |

| Endodontic |

| Peridontic |

| Prosthodontic |

| Periodontic |

By End User

| Dental Hospitals |

| Dental Clinics |

| Academic & Research Institutes |

| By Product | General and Diagnostics Equipment | Dental Laser | Soft Tissue Lasers |

| Hard Tissue Lasers | |||

| Radiology Equipment | Extra Oral Radiology Equipment | ||

| Intra-oral Radiology Equipment | |||

| Dental Chair and Equipment | |||

| Other General and Diagnostic equipment | |||

| Dental Consumables | Dental Biomaterial | ||

| Dental Implants | |||

| Crowns and Bridges | |||

| Other Dental Consumables | |||

| Other Dental Devices | |||

| By Treatment | Orthodontic | ||

| Endodontic | |||

| Peridontic | |||

| Prosthodontic | |||

| Periodontic | |||

| By End User | Dental Hospitals | ||

| Dental Clinics | |||

| Academic & Research Institutes | |||

Key Questions Answered in the Report

What is the current size of the German dental equipment market?

– The German dental equipment market size was USD 1 billion in 2026 and is projected to reach USD 1.38 billion by 2031.

Which product category leads the market?

– Dental consumables dominate with a 61.92% revenue share, reflecting high procedure volumes for restorative materials.

Why are CAD/CAM systems growing so quickly in Germany?

– Clinics adopt chairside CAD/CAM to cut procedure time by up to 50% and to meet rising demand for same-day restorations, driving a +1.8% impact on CAGR.

How do DSOs influence equipment purchasing?

– Consolidated DSOs negotiate bulk discounts and standardize digital platforms across clinics, accelerating technology penetration.

Page last updated on: