Germany Barbeque Grill Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

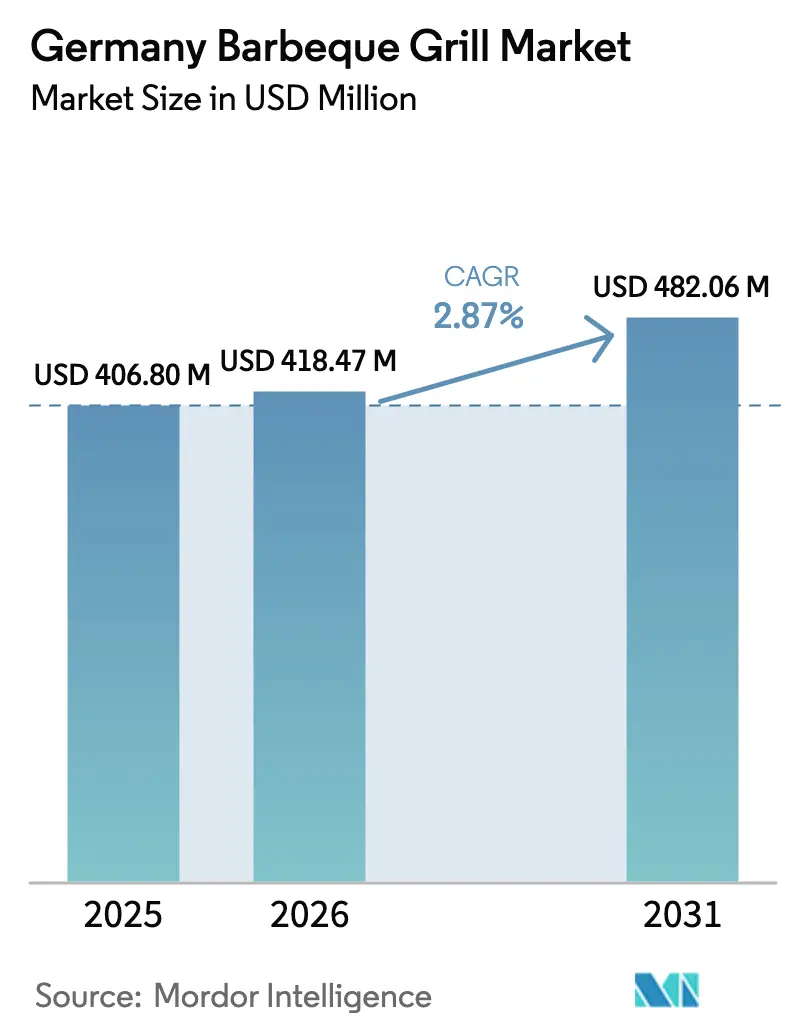

| Base Year Market Size (2025) | USD 406.80 Million |

| Market Size (2026) | USD 418.47 Million |

| Market Size (2031) | USD 482.06 Million |

| Growth Rate (2026 - 2031) | 2.87% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Barbeque Grill Market Analysis by Mordor Intelligence

The Germany barbeque grill market size reached USD 406.8 million in 2025, is expected to reach USD 418.47 million in 2026, and is forecast to achieve USD 482.06 million by 2031 at a 2.87% CAGR. Growth now pivots toward premium feature upgrades, smart connectivity, and balcony-compliant formats that raise average selling prices across core product tiers. Fuel choices are fragmenting as gas retains convenience leadership, while urban regulations and multi-family living steer more households to electric Plug & Cook designs. Design preferences also reflect space constraints, with portable table-top models accelerating even as freestanding units still lead revenue. Technology adoption is shifting toward smart-connected variants as app control and remote monitoring move into mid-tier price bands, supporting a longer-term upgrade cycle across the Germany barbeque grill market.

Key Report Takeaways

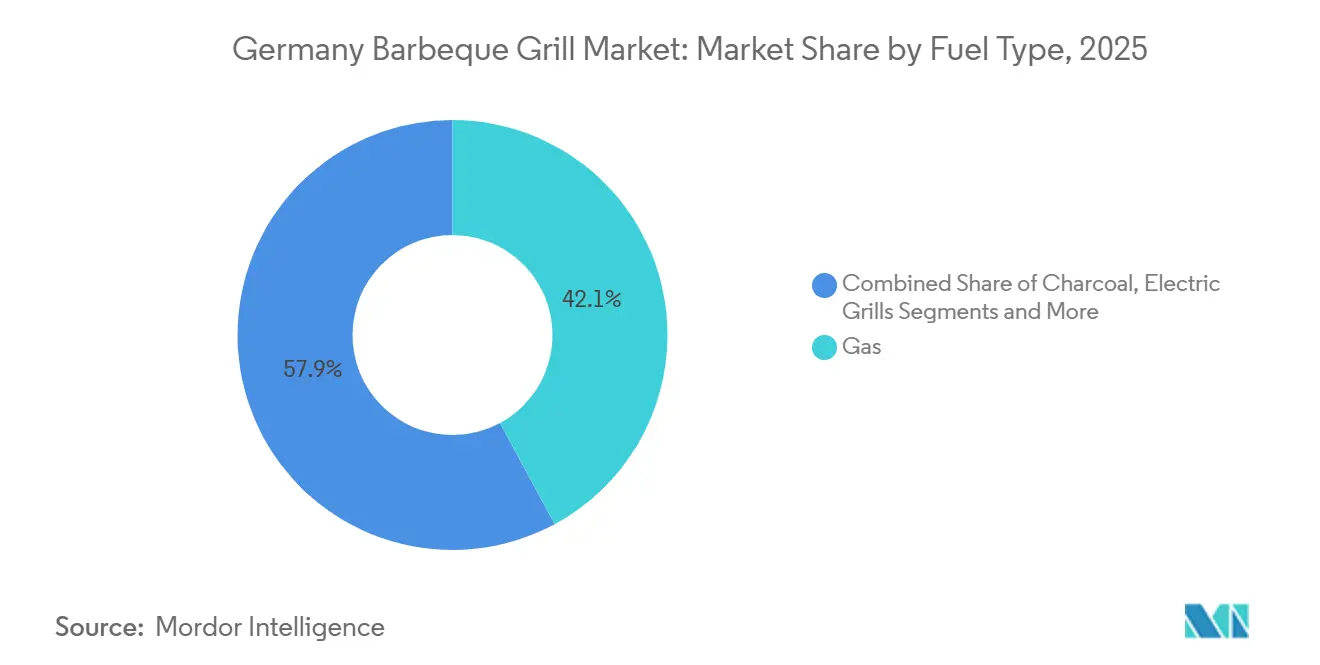

- By fuel type, gas platforms led with 42.12% of the Germany barbeque grill market share in 2025, while electric variants are forecast to expand at a 3.12% CAGR through 2031.

- By product design, freestanding units accounted for 47.85% revenue share in 2025, and portable table-top models are projected to grow at a 3.03% CAGR to 2031.

- By technology, conventional grills represented 78.65% of the Germany barbeque grill market share in 2025, while smart-connected variants carry the highest projected CAGR at 3.13% through 2031.

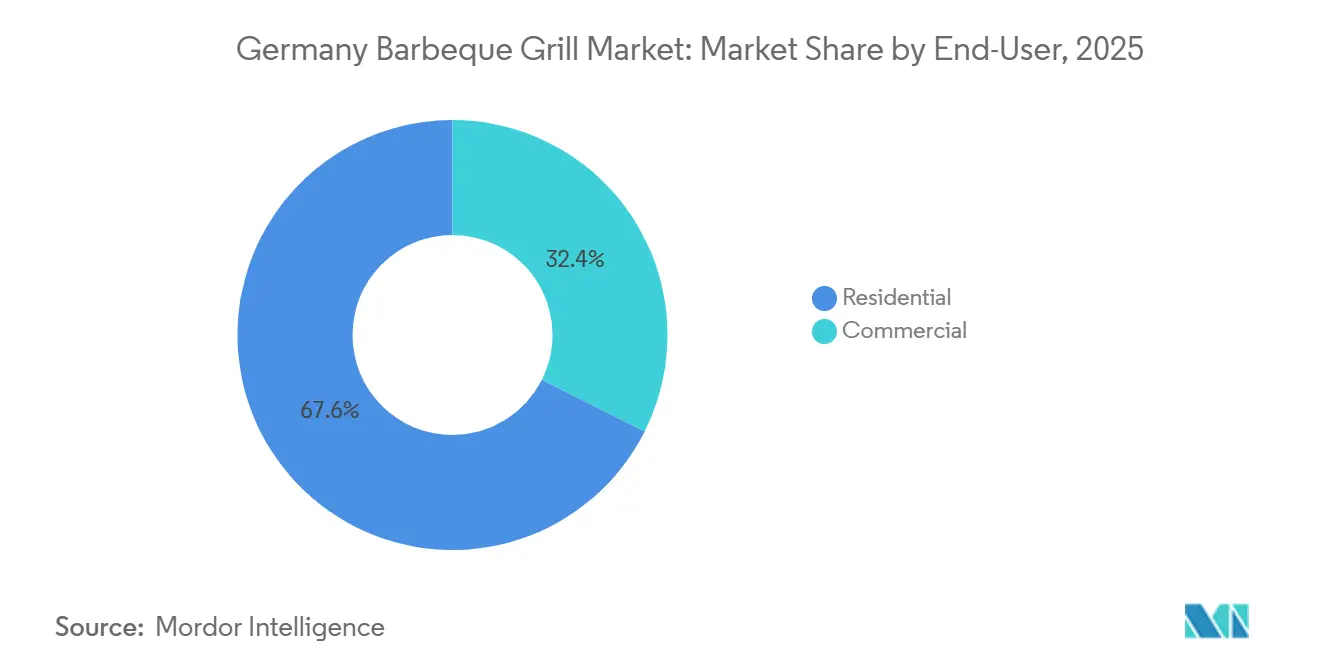

- By end-user, residential households led with 67.60% revenue share in 2025 and are expected to grow at a 2.88% CAGR to 2031.

- By distribution channel, B2C retail held a 70.25% share in 2025, while online-enabled outlets are projected to grow at a 2.97% CAGR through 2031.

- By geography, South Germany commanded 28.75% of 2025 revenue, and North Germany is forecast to record the fastest growth at 3.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with Germany representing one among them. The global report on barbeque grill market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

Germany Barbeque Grill Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cultural grilling tradition | +0.8% | National, most pronounced in Bavaria and Baden-Württemberg | Long term (≥ 4 years) |

| Safety technology advances | +0.4% | National, concentrated in urban centers, requiring TÜV/GS certification | Medium term (2-4 years) |

| Smart home integration | +0.6% | Urban cores in Hamburg, Munich, Berlin, and spillover to North Rhine-Westphalia suburbs | Medium term (2-4 years) |

| BBQ festivals expansion | +0.3% | Regional hotspots such as Stuttgart, Bremen, and Cologne, expanding to secondary cities. | Short term (≤ 2 years) |

| DIY home upgrades | +0.5% | Suburban and exurban areas nationwide with private gardens | Medium term (2-4 years) |

| Smokeless, urban-compliant grills | +0.4% | Dense residential zones in Berlin, Hamburg, and Cologne apply 1. BImSchV standards | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Strong Cultural Tradition of Grilling, Sustaining Steady Demand

Germany’s embedded “Grillen” culture sustains baseline demand as outdoor cooking remains a core leisure activity that extends beyond summer peaks and supports repeat purchases of fuel and accessories across the Germany barbeque grill market. Replacement-driven cycles dominate detached and semi-detached homes, while urban households increasingly adopt compact formats that suit smaller spaces and stricter building rules. Premiumization offsets softer unit volumes as brands bundle accessories, connectivity, and modular side stations, which lifts perceived value and raises average selling prices. New collections use connectivity and accessory ecosystems to justify upgrades, with manufacturers positioning grills as platforms rather than stand-alone appliances. Regional preferences help shape product mixes, with South Germany favoring high-capacity freestanding units and North Germany leaning toward compact balcony-friendly solutions that comply with rental clauses and house rules.

Advances in Grill Safety Technology Are Enhancing Consumer Confidence

Safety upgrades help first-time and urban users overcome concerns around gas leaks, flare-ups, and heat exposure, making onboarding easier in dense residential settings where risk tolerance is lower. Updated GS-mark testing protocols emphasize dimensional accuracy, thermal behavior, and structural rigidity, which signals that certified products can withstand frequent use without premature degradation[1]Editorial Team, “Consumer Product Testing and GS Mark,” TÜV Rheinland, tuv.com . Electric platforms add SafeTouch housing and thermal barriers to keep exterior surfaces cooler while delivering high internal temperatures, broadening appeal among families and multi-unit residences. Firelighter compliance under DIN EN 1860-3 pushes reformulation away from problematic compounds, with DIN CERTCO listing hundreds of valid certifications that guide assortments and support premium positioning for verified products. Retailers and installers increasingly anchor merchandising to TÜV GS and DIN credentials, which standardize the evaluation of competing units and reduce buyer uncertainty at the point of sale. As these controls become expected features, differentiation migrates to build quality, ease of maintenance, and how software layers enhance safe operation across the Germany barbeque grill market.

Increasing Smart Home Integration with Grills

Connected grills are moving from novelty to normal as app control, guided recipes, and remote temperature monitoring simplify cooking and reduce the need for constant oversight during low-and-slow sessions across the Germany barbeque grill market. Enders Colsman advanced patenting activity in 2025 and added Bluetooth probe retrofits to legacy models, enabling budget-friendly upgrades that extend the useful life of installed bases[2]Company Filings, “Enders Colsman AG Patent Publications,” North Data, northdata.de . Ninja’s Woodfire Pro Connect XL introduced AI-assisted temperature management and reminders in Germany, illustrating how software can translate pro-grade results into consumer-friendly workflows. Feature sets that include cloud-linked status, fuel sensors, and predictive alerts appeal to younger families and tech-forward households that already manage lighting, security, and HVAC with apps. Adoption is strongest in large urban cores, with spillovers to suburban high-income districts as prices normalize and reliability improves in the mid-tier.

Growth in DIY Home Improvement Is Fueling Backyard Upgrades

Grills ride the broader upgrade of outdoor living, where patios, pergolas, and garden kitchens shift from occasional-use amenities to daily-use extensions of the home. Built-in gas units integrate into permanent installations and connect to dedicated gas lines, anchoring complete outdoor-kitchen builds that include sinks, refrigeration, and pizza ovens. Modular outdoor systems let homeowners stage investments with configurable worktops and cabinet layouts, widening the addressable base for premium backyard cooking projects. As real wages rise in 2026 and 2027, discretionary budgets for home upgrades strengthen, which aids higher-ticket grills and built-in solutions that align with long-lived renovation cycles. These dynamic supports sustained value-led growth even as overall replacement cycles normalize from pandemic-era peaks, keeping the Germany barbeque grill market positioned for steady upgrades rather than one-off purchases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer budget pressure on premium SKUs | -0.5% | National, acute among households earning below EUR 60,000 annually | Short term (≤ 2 years) |

| Fire bans in forests or parks during droughts | -0.3% | Rural and peri-urban zones, especially eastern areas with low rainfall | Short term (≤ 2 years) |

| Product safety and pollutant scrutiny raise costs | -0.3% | National, amplified in states with stricter enforcement, such as Baden-Württemberg and Bavaria. | Medium term (2-4 years) |

| Consumer concerns over synthetic materials in grills | -0.2% | Eco-conscious urban segments in Hamburg, Freiburg, Munich | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer Budget Pressure on Premium SKUs

Household caution continues to temper high-ticket purchases, which elongates replacement cycles and nudges buyers toward value bundles rather than top-of-line configurations. Promotions, accessory bundles, and mid-tier feature sets provide a bridge for families who want connectivity and performance without committing to flagship prices across the Germany barbeque grill market. Retailers respond with seasonal clearance and deferred financing that align with the spring and summer sales peaks to reduce sticker shock and keep sell-through balanced. These tools protect shelf space for premium models while ensuring that entry and mid ranges remain accessible, which helps stabilize unit volumes in a slow-growth spending environment. As real wage tailwinds gather momentum, premium intent may return, but price sensitivity remains an essential planning assumption in the near term.

Product Safety and Pollutant Scrutiny Raise Costs

Conformance to DIN EN 1860 for charcoal grills and firelighters and DIN EN 498 for gas grills adds testing and documentation steps that raise time to market and cost of goods, especially for smaller brands. TÜV GS-mark certification further expands the test scope to cover construction integrity and thermal behavior, a requirement that many retailers treat as table stakes for listing. Firelighters and fuels also face emissions controls and material restrictions, which push reformulations and certification fees that must be recovered through pricing or scale. The Federal Immission Control framework and municipal-level guidance continue to tighten expectations on particulate emissions, raising compliance complexity for charcoal formats. Together these factors raise development and certification outlays, sharpen the need for rigorous quality systems, and favor vendors that can amortize costs across larger volumes in the Germany barbeque grill market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Electric Platforms Narrow Gas Lead Amid Balcony Bylaws

Gas grills captured 42.12% of the Germany barbeque grill market size in 2025 on the strength of instant ignition, predictable burner control, and weeknight convenience valued by suburban households. Electric models now build momentum as balcony rules and multi-unit housing encourage 220-volt Plug & Cook usage with the added benefit of app control and quick setup times. Electric is forecast to grow at 3.12% to 2031, supported by connected features and compliance advantages that reduce friction for dense urban living. New designs that combine electric heating with wood-smoke flavor, such as AI-assisted control in consumer models, illustrate how software helps replicate charcoal outcomes without open flames. Pellet formats remain a premium niche with steady temperature holds for long cooks, while hybrid and high-heat infrared burners appeal to enthusiasts who want high-sear capability without sacrificing ease of use.

Compliance frameworks shape assortments and channel access across the Germany barbeque grill market. Conformity to DIN EN 1860 for charcoal systems and DIN EN 498 for gas systems, plus TÜV GS-mark testing, remains critical for mass retail listings and reinforces consumer confidence at the point of sale. Charcoal demand still benefits from flavor and tradition, yet municipal emission rules and drought-season restrictions tilt more purchases toward electric formats that minimize particulate output [3]Editorial Team, “Air Pollutants from Grilling and Cleaner Alternatives,” Umweltbundesamt, umweltbundesamt.de. Gas retains a broad base by balancing flavor, power, and convenience, while electric gains through regulatory alignment and connected features that simplify outdoor cooking for newcomers.

By Product Design: Portable Units Gain on Space-Starved Urban Demand

Freestanding grills led revenue in 2025 with a 47.85% share as families sought full-size cooking surfaces, side burners, and rotisserie capacity for entertaining and weekend gatherings. This format remains central in suburban and exurban areas where space permits wheeled carts and larger footprints that support complete meal preparation outdoors. Portable and table-top designs are advancing fastest at a 3.03% CAGR as apartment dwellers prefer fold-flat storage and lighter builds that suit 6 m² balconies and car trunks. Premium portable lines pack robust heating, modular grates, and easy-clean trays into compact footprints, expanding the appeal of outdoor cooking to renters and first-time buyers who grill weekly rather than daily.

Built-in systems consolidate premium intent within the Germany barbeque grill market, especially in renovation and new-build projects that integrate gas lines and modular cabinetry. RÖSLE’s built-in configurations showcase die-cast aluminum combustion chambers, multi-burner layouts, and high-temperature side zones that deliver restaurant-level searing within cohesive outdoor kitchens. Manufacturers increasingly offer modular components that allow staged investments and layout flexibility, reducing upfront cost barriers while preserving upgrade paths. As sustainability considerations shape purchasing choices, reusable compact charcoal systems and durable electric griddles gain share at the expense of low-end disposables, which face both environmental headwinds and retailer delisting.

By Technology: Smart-Connected Variants Chip at Conventional Dominance

Conventional grills account for 78.65% sales in 2025, reflecting buyers who prioritize simple knob-and-burner control, affordability, and durable construction without software layers. This base is strongest among seasonal users who prefer straightforward maintenance and familiar workflows. That said, the value proposition of connectivity is improving at mid-price points, making smart features more accessible to upgraders and new buyers who already manage other household devices by app. Vendors differentiate through cloud-linked controls, fuel sensors, guided recipes, and push notifications that reduce uncertainty during longer cooks, which addresses a key barrier for novices.

Smart-connected grills hold the fastest growth outlook at a 3.13% CAGR to 2031 as software stability improves and interoperability expands across devices and probes. Patent activity continues in burner control, heat distribution, and probe integration, while retrofit accessories help legacy owners add monitoring without replacing entire grills. AI-enabled electric models that automate temperature adjustments and send timely reminders show how software can replicate expert outcomes, pulling more consumers into low-smoke formats that work in multi-family homes. As data privacy expectations remain high, brands position their apps with explicit consent controls and security assurances, which is essential to unlock full adoption within the Germany barbeque grill market.

By End-User: Residential Segment Anchors Growth on At-Home Leisure Surge

Residential households led with 67.60% of 2025 sales and are on track to grow at a 2.88% CAGR through 2031, supported by steady upgrades to patios and outdoor kitchens and a shift toward year-round use in milder regions. Detached and semi-detached homes fuel demand for freestanding gas and charcoal units, while urban apartments lean toward compact electric formats that minimize smoke and comply with building policies. As wage growth improves purchasing power in 2026 and 2027, more households can step into mid-tier and premium SKUs that combine connected control with higher-temperature performance. Accessory ecosystems, from Wi-Fi thermometers to modular side stations, extend lifetime value and provide ongoing reasons to upgrade within the Germany barbeque grill market.

Commercial users comprise the remaining share and prioritize high BTU outputs, corrosion-resistant materials, and durability for extended daily operation in foodservice and events. Specialty catering and venue operators gravitate to robust gas systems with sealed burner boxes and reinforced grates, while balcony-friendly electric solutions appear in boutique hospitality and rooftop settings where open-flame restrictions apply. Extended warranties, bulk purchasing programs, and dedicated service networks matter more to commercial buyers than app features, which keep hardware reliability at the center of specification decisions.

By Distribution Channel: Online Channels Erode Brick-and-Mortar Grip

B2C/ retail channels held 70.25% share in 2025, reflecting the strength of specialty barbecue stores, home centers, and mass merchants that can demonstrate ignition, heat distribution, and accessory fit in person. Specialty retailers use live-cook stations and staff training to increase conversion and defend share against generalist appliance aisles. Category storytelling around safety certifications, smokeless compliance, and app features helps shoppers navigate trade-offs between gas, charcoal, pellet, and electric formats, which increases confidence in higher-ticket purchases. Omnichannel behaviors, like in-store pickup for online orders, reduce last-mile costs for bulky products and let buyers inspect units before final acceptance.

Online-enabled outlets are projected to grow at a 2.97% CAGR through 2031 as consumers blend content discovery with transacting and post-purchase support within a single digital journey. Specialist e-tailers reported strong 2024 momentum driven by recipe content, live chat, and seasonal clearance that align with the seven-month grilling window in Germany. Mobile-first checkout, accessory recommendations, and finance offer lift basket sizes for connected grills, while standardized return policies and clear assembly guidance lower perceived risk and support repeat purchases online.

Geography Analysis

South Germany led with a 28.75% revenue share in 2025 as established outdoor-dining culture, favorable climate, and higher household spending supported premium freestanding gas systems and fully built outdoor kitchens that anchor the Germany barbeque grill market size in the region. Bavaria and Baden-Württemberg house larger lots and garden spaces that accommodate wheeled carts and built-in islands, tightening the link between home renovation and outdoor cooking. Residential projects often pair grills with pizza ovens, sinks, and refrigeration as households shift from seasonal entertainment to year-round use when weather permits. South Germany’s continued tilt toward premium features sustains higher average selling prices and keeps the area central to new-product launches aimed at multi-burner gas and modular kitchen configurations.

North Germany is the fastest-growing region at a 3.36% CAGR through 2031 as urban density and balcony culture favor compact, smokeless solutions that meet house rules and building expectations. Hamburg and Bremen have seen rising interest in fan-assisted charcoal and compact electric units that replicate high-heat searing without open flames, which aligns with apartment living and neighbor considerations. Public guidance that highlights lower pollutant emissions from gas and electric options further nudges choices toward clean formats, reinforcing regional gains for compliant products[4]Editorial Team, “Air Pollutants from Grilling and Cleaner Alternatives,” Umweltbundesamt, umweltbundesamt.de. As newly built multifamily projects emphasize outdoor leisure areas with strict safety provisions, a larger share of purchases flows to electric and connected grills that can operate within posted rules.

Other regions display a balanced mix as metropolitan centers and suburbs diversify product demand across formats. Central corridors with a blend of urban apartments and detached homes show stable growth in both compact electric and freestanding gas as budgets and space permit. Western hubs emphasize mid-tier gas for everyday convenience, while eastern clusters maintain charcoal affinity that is gradually moderated by clean-air messaging and seasonal restrictions that limit open-flame use in sensitive periods. This pattern confirms how climate, housing stock, and rules around emissions define a clear regional map of preferences within the Germany barbeque grill market.

Competitive Landscape

The Germany barbeque grill market shows moderate concentration, with Weber-Stephen, Landmann, Enders Colsman, Napoleon, and Char-Broil together holding an estimated 73% combined Top-5 share in 2025, while long-tail brands and niche specialists compete in focused segments. Weber’s February 2025 merger with Blackstone unites premium gas and electric grills with flat-top griddles and pellet technology, expanding the accessory and software ecosystem that underpins cross-category engagement. Portfolio moves that elevate app stability, firmware updates, and probe ecosystems show how software has become a frontline differentiator alongside heat output and build quality in the Germany barbeque grill market.

Enders Colsman reinforced its innovation posture with multiple 2025 filings and retrofit probes that bring guided cooking to installed bases, a cost-sensitive path to connectivity for owners of conventional models. RÖSLE’s premium outdoor lines with high-temperature side zones and panoramic lids demonstrate how design and materials can support both performance and ease of monitoring in busy family settings. LotusGrill’s fan-assisted smokeless charcoal models stake out compliant use in high-density living, a segment where fast heat-up and minimal smoke drift are decisive. New modular outdoor kitchens from Swiss-origin vendors expand the upgrade canvas, letting retailers merchandise complete backyard solutions rather than individual grills.

Digitization and compliance shape channel strategy as much as hardware specs. Retailers foreground TÜV GS and DIN credentials to streamline consumer choice, while manufacturers direct R&D to cleaner combustion and thermal management to meet emissions expectations. Supply chains continue to regionalize to improve lead times and reduce freight exposure, aided by expanded continental assembly that better supports peak-season demand. As connected ecosystems mature, brands invest in content and community to drive usage frequency, which raises attachment rates for thermometers, griddles, and software-enabled accessories across the Germany barbeque grill market.

Germany Barbeque Grill Industry Leaders

Weber-Stephen Products LLC

Landmann GmbH & Co. KG

Napoleon (Wolf Steel Ltd.)

Char-Broil LLC

Enders Colsman AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: WMF launched the Edition One Plancha and modular outdoor kitchen lineup for Germany, expanding into configurable outdoor cooking systems that integrate with premium cookware.

- March 2025: Outdoorchef unveiled HEAT Outdoor Kitchens with pre-configured modules, rear burners, and customizable worktops for premium backyard installations in Germany.

- February 2025: Weber-Stephen Deutschland GmbH and Blackstone Products finalized a strategic merger that combines gas and electric grills with flat-top griddles and pellet technologies and targets supply chain integration across EMEA to reduce logistics costs.

- January 2025: Weber introduced its 2025 collection led by SPIRIT Boost gas grills, WEBER SMOQUE pellet smokers, and SLATE griddles, positioning connected control and modular add-ons for mainstream buyers.

Germany Barbeque Grill Market Report Scope

A barbecue grill is a piece of equipment that uses heat applied from below to cook food. Barbecue grills can be powered by gas, charcoal, smoke, hybrid, or electricity, depending on the heat source. A complete background analysis of the Germany barbecue grill market, which includes an assessment of the emerging market trends by segments, significant changes in the market dynamics, key major players, and a market overview, is covered in the report.

The Germany Barbecue Grill Market Was Segmented By Product (Gas, Charcoal, And Electric), By Application (Residential, Commercial), And By Distribution Channel (Online Stores, Offline Stores). The Report Offers Market Size And Forecasts For The Germany Barbeque Grill Market In Value (USD) For All The Above Segments.

| Gas Grills |

| Charcoal Grills |

| Electric Grills |

| Pellet Grills |

| Hybrid/Alternative Fuel |

| Infrared |

| Built-In |

| Freestanding |

| Portable / Table-top |

| Disposable / Single-use |

| Conventional |

| Smart/Connected |

| Residential |

| Commercial |

| B2B/Direct from the Manufacturers |

| B2C/Retail – Specialty Stores |

| Home Centers & DIY Stores |

| Mass Merchandisers |

| Online |

| Other Distribution Channels |

| North Germany |

| South Germany |

| East Germany |

| West Germany |

| Central Germany |

| By Fuel Type | Gas Grills |

| Charcoal Grills | |

| Electric Grills | |

| Pellet Grills | |

| Hybrid/Alternative Fuel | |

| Infrared | |

| By Product Design | Built-In |

| Freestanding | |

| Portable / Table-top | |

| Disposable / Single-use | |

| By Technology | Conventional |

| Smart/Connected | |

| By End-User | Residential |

| Commercial | |

| By Distribution Channel | B2B/Direct from the Manufacturers |

| B2C/Retail – Specialty Stores | |

| Home Centers & DIY Stores | |

| Mass Merchandisers | |

| Online | |

| Other Distribution Channels | |

| By Geography | North Germany |

| South Germany | |

| East Germany | |

| West Germany | |

| Central Germany |

Key Questions Answered in the Report

What is the current size and growth outlook for the Germany barbeque grill market?

The Germany barbeque grill market size was USD 418.47 million in 2026 and is projected to reach USD 482.06 million by 2031 at a 2.87% CAGR.

Which fuel type is growing fastest in Germany?

Electric grills are the fastest-growing fuel type, supported by balcony compliance and plug-in convenience, with a 3.12% CAGR projected through 2031.

What product designs are leading and which are rising fastest?

Freestanding units led with 47.85% revenue share in 2025, while portable table-top models are the fastest-growing design at a 3.03% CAGR.

How is technology shaping buyer choices in Germany?

Conventional grills still dominate, but smart-connected models carry the highest projected growth at 3.13% as app control and guided cooking enter mid-tier price points.

Which customer group contributes most to demand?

Residential households generated 67.60% of 2025 sales and are expected to grow at 2.88% through 2031 as outdoor living upgrades continue.

What regions are most influential for growth in Germany?

South Germany held 28.75% of 2025 revenue, while North Germany is the fastest-growing region at a 3.36% CAGR due to urban density and smokeless grill adoption.

Page last updated on: