United States Barbeque Grill Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.36 Billion |

| Market Size (2026) | USD 1.41 Billion |

| Market Size (2031) | USD 1.64 Billion |

| Growth Rate (2026 - 2031) | 3.07% CAGR |

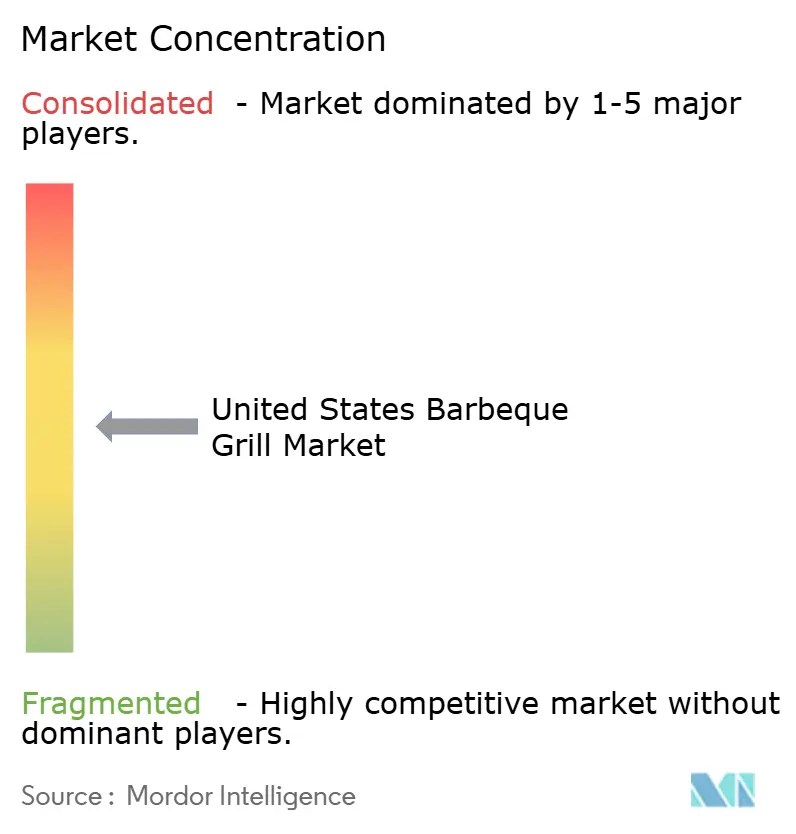

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Barbeque Grill Market Analysis by Mordor Intelligence

The United States barbeque grill market size reached USD 1.36 billion in 2025, is expected to reach USD 1.41 billion in 2026, and is forecast to achieve USD 1.64 billion by 2031 at a 3.07% CAGR. The United States barbeque grill market is shaped by steady demand for outdoor living upgrades, an installed base that supports replacement cycles, and product innovation centered on electric and smart-enabled models. Gas remains the anchor format due to convenience, control, and maintenance simplicity, while electric variants gain from code compliance and electrification policies that narrow the use of open flames in dense urban settings. B2C retail accounts for a clear majority of category sales, helped by omnichannel tactics that blend showroom touch and e-commerce speed with last-mile assembly and installation options. Regionally, usage patterns reflect climate, housing mix, and regulations, which increases the relevance of format-specific assortments and localized marketing in the United States barbeque grill market[1]Spare the Air Program, “Spare the Air Alerts and Wood Burning Rules,” Bay Area Air Quality Management District, sparetheair.org.

Key Report Takeaways

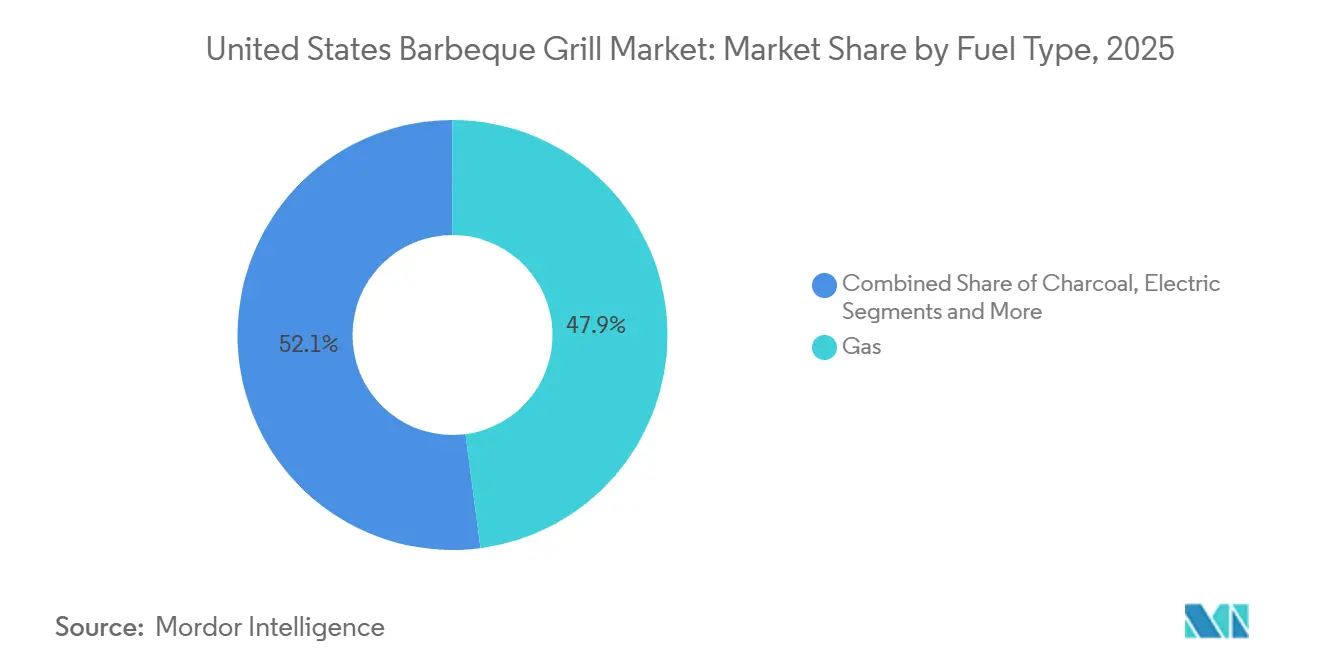

- By fuel type, the United States barbeque grill market was dominated by gas, which captured 47.92% of revenue in 2025, while electric grills are anticipated to register a 4.31% CAGR through 2031.

- By product design, the United States barbeque grill market saw freestanding units account for 41.62% of market share in 2025, whereas portable models are projected to grow at a 3.83% CAGR through 2031.

- From a technology perspective, conventional analog grills represented 79.75% of the 2025 market share in the United States barbeque grill market, while smart/connected variants are forecast to expand at a 4.67% CAGR through 2031.

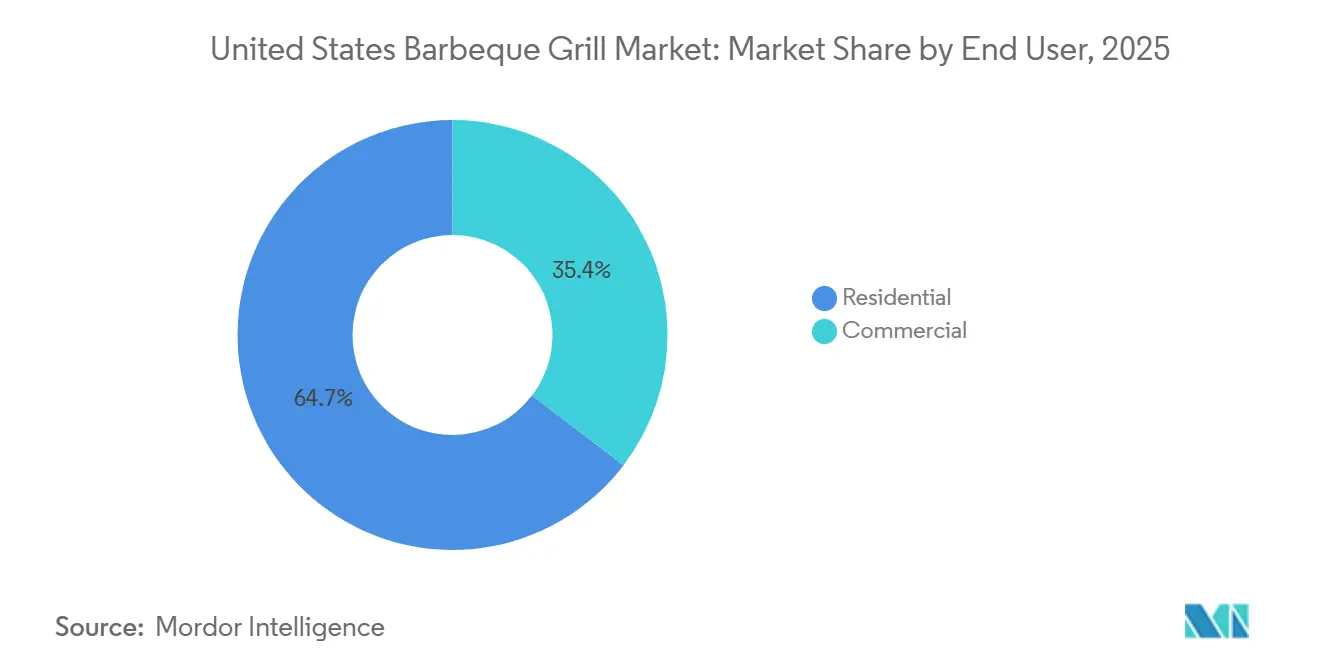

- By end-user segmentation, residential households accounted for 64.65% of the 2025 market share in the United States barbeque grill market, with the commercial segment expected to grow at a 3.64% CAGR by 2031.

- By distribution channels, B2C retail accounted for 66.95% of the total market size in the United States barbeque grill market in 2025, and the segment is projected to grow at a 3.88% CAGR through 2031.

- By geography, the Southeast accounted for 25.05% of the total market size in the United States barbeque grill market in 2025, and the West is on the fastest growth path, boasting a 4.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Barbeque Grill Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High grill ownership and outdoor-living investments sustain demand | +0.8% | National, strongest in Southeast, West, Southwest | Medium term (2-4 years) |

| Gas convenience, control, and low maintenance support leadership | +0.7% | National | Long term (≥ 4 years) |

| Smart/connected features improve outcomes and upgrade rates | +0.5% | Urban cores, affluent suburbs | Short term (≤ 2 years) |

| Omnichannel retail and last-mile assembly expand category reach | +0.4% | National, particularly the suburban Midwest, Southeast | Medium term (2-4 years) |

| Flat-top griddle boom creates second-unit and crossover demand | +0.5% | National, with peak adoption in the Midwest, Southwest | Short term (≤ 2 years) |

| Multifamily communal amenities expand commercial installs | +0.3% | Urban metros | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Grill Ownership and Outdoor-Living Investments Sustain Demand

Household engagement with outdoor cooking remains a structural pillar that supports the United States barbeque grill market even as the category matures. Developers and homeowners have prioritized outdoor kitchens as part of broader lifestyle upgrades, with projects often bundling grills, refrigeration, and shelter features to extend seasonal use. According to statistics from the Hearth, Patio & Barbecue Association, the percentage of U.S. homeowners owning a grill or smoker rose from 64% in 2019 to 80% in 2023, indicating that Americans are still actively grilling outdoors. Younger cohorts demonstrate consistent purchase intent for outdoor categories, while older homeowners allocate larger budgets to premium fixtures, which supports a balanced mix of volume and average selling prices in the United States barbeque grill market. The installed base reinforces an ecosystem of covers, grates, rotisserie kits, and service contracts that help brands preserve engagement between replacement cycles. Overall, the outdoor living focus continues to underpin steady sell-through during peak seasons and supports modest year-round activity through project planning and accessory purchases in the United States barbeque grill market.

Gas Convenience, Control, and Low Maintenance Support Leadership

Gas holds the largest share because it aligns with everyday cooking habits that value quick startup, stable heat zones, and straightforward cleanup. Ubiquitous propane exchange programs and new construction natural gas hookups reduce ownership friction and reinforce weeknight use, which together anchor gas as the default for first-time buyers and upgrades. Ignition reliability and multi-burner control improve outcomes for large gatherings or multi-course meals, which strengthens brand loyalty to established gas platforms in the United States barbeque grill market. Maintenance tasks are simple and familiar for most households, which reduces perceived risk at the point of purchase and favors gas over alternatives that introduce fueling or ash management complexity. State and local policies that support propane or natural gas appliances in select jurisdictions create incremental tailwinds for builders and remodelers who spec gas-ready outdoor kitchens.

Smart/Connected Features Improve Outcomes and Upgrade Rates

Connectivity has moved from early-adopter novelty to an expected feature on mid-range and premium models, with embedded probes, guided workflows, and remote control improving ease of use. Launches such as Weber’s WEBER CONNECT ecosystem and Napoleon’s CES recognized Rogue EQ broaden consumer awareness and set new baselines for feature sets in the United States barbeque grill market. Traeger’s continued deployment of WiFIRE across new lines illustrates how app-based control has become a platform strategy rather than a single SKU experiment. Connected control reduces user error for first-time grillers and busy households, which expands the addressable base beyond enthusiasts who master analog techniques[2]Weber Inc., “Weber Introduces Expanded WEBER CONNECT Smart Grilling Ecosystem,” Business Wire, businesswire.com. As component costs fall and software platforms scale, smart features migrate into lower price bands, which shortens perceived replacement intervals for owners of older analog units in the United States barbeque grill market.

Omnichannel Retail and Last Mile Assembly Expand Category Reach

B2C retail remains the dominant route to market due to a blend of floor displays for tactile evaluation, consultative selling in specialty stores, and the convenience of online ordering. Co-op networks that add premium brands to warehouse and drop-ship programs help thousands of independent dealers offer full assortments, which level the playing field with big-box chains in many local markets. Retailers increasingly bundle delivery, assembly, and gas line connection services to reduce purchase friction for heavier units and built-in installs, which improves conversion and satisfaction. Specialty dealers use live demos and curated assortments to capture higher ticket transactions, while mass merchants scale entry and mid-tier bundles for value-oriented shoppers in the United States barbeque grill market. This omnichannel mix strengthens category resilience by reaching homeowners across budgets, geographies, and service expectations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fire/air-quality restrictions limit charcoal and open-flame use | -0.6% | California Bay Area, Pacific Northwest, Arizona | Long term (≥ 4 years) |

| Raw materials and electronics cost volatility pressure pricing | -0.5% | National | Short term (≤ 2 years) |

| Post-pandemic replacement cycle delays mute near-term sell-in | -0.4% | National, particularly suburban markets | Medium term (2-4 years) |

| Griddle/indoor appliance substitution cannibalizes upgrades | -0.3% | National, concentrated in the Midwest, urban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fire/Air Quality Restrictions Limit Charcoal and Open Flame Use

Many jurisdictions restrict charcoal and open flames during poor air quality periods, which shifts demand toward electric and gas models that comply with local rules. County-level advisories in the Pacific Northwest and Southwest impose additional constraints during high-risk seasons, which change household cooking patterns where yards, balconies, or parks face periodic bans. These conditions create a structural tailwind for electric grills and enclosed systems that can meet emissions expectations, especially in urban cores that favor flameless appliances. Legal uncertainty around municipal gas policies also influences new construction decisions, which can slow commitments to gas-ready amenities in select markets. Enforcement variability across counties adds compliance complexity that brands address through product breadth and localized guidance rather than a single national solution[3]Summit County Government, “Fire Restrictions,” Summit County Government, summitcountyco.gov.

Raw Material and Electronics Cost Volatility Pressure Pricing

Higher tariffs on steel and aluminum since mid-2025 have lifted input costs and pressured margins at manufacturers that rely on imported materials, making selective price adjustments more likely. Companies responded with supply chain shifts and production relocation to reduce exposure to tariff regimes, but these transitions entail near-term tooling and logistics costs that weigh on profitability in the United States barbeque grill market. Electronics parts for connected models remain sensitive to lead times and pricing swings, which can delay launches or constrain inventories for fast-moving SKUs. Brands are managing these pressures to preserve retail relationships, yet sustained inflation in components and materials would likely require broader price actions that test discretionary spending. Procurement teams increasingly balance feature sets with bill-of-materials discipline to protect value propositions while avoiding sudden shifts that disrupt sell-through momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Electric Narrows Gas Leadership Where Codes Favor Flameless Options

Gas grills held a leading 47.92% share in 2025 within the United States barbeque grill market, supported by reliable ignition, stable multi-zone heat, and broad propane access across retail points. Electric grills are the fastest-growing fuel segment with a 4.31% CAGR through 2031, aided by municipal fire codes and electrification preferences that limit open flames on certain balconies and multi-unit properties. As building policies tighten in select cities, electric models gain relevance for urban households that want outdoor cooking without violating rules, which adds new entry points into the United States barbeque grill market. Suppliers increasingly include electric options in mainstream assortments to serve urban and code-sensitive buyers, while maintaining gas as the workhorse for most detached homes. Product strategies emphasize familiar form factors, intuitive temperature control, and accessories that help electric formats approximate searing and capacity performance that consumers expect.

The technology lineup demonstrates this pivot. Weber’s platform investments bring app-assisted control and smart probes to gas and charcoal lines while improving connectivity, which then informs electric design choices for heat management and convenience. Napoleon’s connected electric model earned CES recognition for performance and control features that mirror gas cooktops in a full-size outdoor appliance, which expands the premium ceiling for flameless cooking. Cuisinart’s indoor outdoor electric units cover modest balconies or travel use cases and demonstrate how electric can scale down without losing core utility. Pellet and charcoal formats retain dedicated followings that value smoke flavor and ritual, yet their growth is more sensitive to local burn restrictions, cleanup routines, and storage space than the mainstream gas and electric paths in the United States barbeque grill market. The result is a portfolio dynamic where gas preserves leadership on capability and convenience, and electric claims the growth edge where regulations shape buying criteria in the United States barbeque grill market.

By Product Design: Portability Advances While Freestanding Remains the Installed Base

Freestanding cart grills held a 41.62% share in 2025 and remain the backbone of the United States barbeque grill market due to integrated storage, mobility on casters, and straightforward assembly relative to custom islands. Portable and tabletop designs are growing at a 3.83% CAGR through 2031 as households with smaller patios, travel habits, or tailgating preferences seek compact units that prioritize weight and foldability. These portable formats align with younger households that value flexibility and experiential cooking, and they work well in codes that prohibit large propane cylinders on balconies. Product development focuses on collapsible frames, quick-connect gas fittings, and easy-clean surfaces to reduce friction at setup and teardown. Distribution emphasizes retail portability displays, car trunk fit imagery, and bundle pricing with covers and griddle plates to support immediate use.

Built-in installations target the premium tier, where outdoor kitchens integrate grills, refrigeration, storage, and counters for a cohesive space. Brands such as Lynx and DCS showcase marine-grade materials and high-output burners for reliability and performance under frequent use, which supports longer ownership cycles and service contracts. Although installation costs and permanence keep built-ins to select ZIP codes and new homes, the segment influences innovation that eventually seeps into freestanding lines. Disposable or single-use grills settle into a niche defined by parks and beaches that allow them, but waste diversion goals and landfill restrictions limit expansion. Across formats, the United States barbeque grill market continues to blend convenience, compliance, and performance, with portability serving new occasions and freestanding carts anchoring the core base.

By Technology: Connectivity Commands Premium, While Analog Retains Majority

Analog models held 79.75% share in 2025 in the United States barbeque grill market due to simpler operation, lower prices, and familiarity that appeals to long-time owners. Smart or connected models are the fastest-growing technology segment at a 4.67% CAGR through 2031, led by ecosystems that integrate wireless probes, app guidance, and over-the-air updates. Weber’s 2026 expansion of its connected portfolio and Napoleon’s CES-recognized product validate consumer appetite for guidance, monitoring, and assured results. Traeger’s connected pellet platforms standardize app features across new launches, which helps normalize expectations among mainstream buyers. This technology mix allows brands to pair analog reliability with smart upgrades so households can choose the right balance of price and capability within the United States barbeque grill market.

Adoption drivers include ease of hitting target temperatures, fewer overcooking incidents via notifications, and visual graphs that demystify airflow or pellet feed for novices. Masterbuilt’s connected charcoal unit shows how digital control can be layered over solid fuel platforms to combine flavor and accuracy, while Nexgrill’s connectivity features extend these benefits into accessible price bands. Constraints include home Wi-Fi reliability and comfort with firmware updates, which keeps analog in command for buyers who value turn and cook simplicity in the United States barbeque grill market. As connectivity trickles down to sub-USD 1,000 ranges, the feature premium narrows and upgrade incentives rise, which influences replacement timing more than category entry. Over the forecast horizon, analog’s familiarity remains a moat while connected features scale their share as ecosystems mature and user onboarding improves.

By End User: Residential Anchors Installed Base While Amenities Expand B2B Opportunities

Residential buyers remain the largest installed base, generated 64.7% of 2025 revenue in the United States barbeque grill market, supported by a deep culture of backyard cooking and a multiyear buildout of outdoor living spaces by homeowners. Purchase drivers include convenience for weeknight meals, entertaining capacity for holidays, and accessory ecosystems that refresh an older unit’s capabilities without full replacement. Smart features entice analog owners who want guidance and remote monitoring, while electric formats accommodate code constraints on multifamily balconies and urban patios. Retailers segment assortments by yard size, fuel codes, and service availability, which helps shoppers match format to property type in a way that preserves satisfaction across budgets. As cost pressures flow through to retail tags in connected and premium models, accessory bundles and financing options help smooth demand within the United States barbeque grill market.

Commercial use cases grow as property owners and operators add community grilling stations and outdoor kitchens to differentiate amenities and boost retention. Hospitality and vacation rentals standardize on durable, high-output units that can withstand frequent use, simple training, and weather exposure while minimizing maintenance calls. Specifications often include locking propane storage, clear pictogram controls, and replacement-friendly parts to reduce downtime across multi-site portfolios. Product selections emphasize stainless materials, service network reach, and warranties that match commercial duty cycles, which favors brands that can support national accounts. This amenity arms race keeps a steady stream of B2B projects in planning and installation cycles that complement the consumer-driven seasonality of the United States barbeque grill market.

By Distribution Channel: Retail Omnichannel Blends Showroom Touch with E Commerce Speed

B2C retail channels delivered 66.95% of 2025 sales and continue to advance at a 3.88% CAGR through 2031, reflecting the power of experiential showrooms, well-trained associates, and fast delivery with assembly options. This combination remains the center of gravity for the United States barbeque grill market. Independent hardware and lawn retailers leverage co op buying programs to stock premium assortments and to offer drop ship capabilities that extend their local reach without heavy inventory. E-commerce emphasizes selection breadth, guided content, and reviews, but the category still benefits from physical inspection for lid heft, burner controls, and grate quality on higher ticket units. White glove services and gas line hookup support reduce return rates and accelerate time to first use, which strengthens loyalty and word of mouth in local communities. Assortments by channel reflect budget spread, with mass merchants concentrating on value bundles and specialty dealers scaling connected and premium formats with demonstration events.

B2B and direct channels serve commercial buyers, custom outdoor kitchen fabricators, and hospitality operators that prioritize project management, account coverage, and parts availability over in-store experience. These buyers typically coordinate across multiple properties and schedule deliveries around construction milestones, which makes reliability and service responsiveness critical selection criteria. Brands that balance B2C visibility with B2B program depth increase resilience during seasonal swings and can smooth production by batching commercial runs off-peak for retail. Over time, last-mile assembly, fuel line safety, and service partnerships will remain differentiators as grills get heavier, smarter, and more embedded into outdoor living environments in the United States barbeque grill market. This dual track distribution approach reduces concentration risk and broadens category access across property types and budgets in the United States barbeque grill market.

Geography Analysis

In 2025, the Southeast accounted for 25.05% of total sales. Meanwhile, the West, driven by California's passion for outdoor living and eco-friendly policies favoring gas and electric units, is on the fastest growth path, boasting a 4.03% CAGR through 2031. Warmer regions support more frequent year-round use, creating a larger installed base for gas and built-in formats, while dense coastal cities nudge demand toward electric and compact designs that adhere to building rules. Retailers and brands respond with localized assortments and compliance guidance, especially for municipalities that restrict charcoal or certain fuel connections, to smooth the shopper journey from research to installation. This geographic heterogeneity sustains steady overall growth for the United States barbeque grill market while requiring nuanced merchandising at the metro and county level.

Sun Belt regions, including parts of the Southeast and Southwest, maintain strong baseline usage because outdoor spaces see fewer dormant months, which increases replacement throughput and accessory sales. New home construction in these regions often includes gas-ready patios, which support built-in and larger freestanding placements that emphasize multi-zone burners and storage. Western metros face a mix of strict air quality and wildfire-driven restrictions, which favors electric grills and clean-burning gas formats for urban households while pushing charcoal toward detached properties farther from dense cores. Northern regions with harsher winters show higher seasonality in sell-through, which concentrates promotions in late spring and early summer and pushes dealers to right-size inventory for Q2 peaks in the United States barbeque grill market. Within each region, multiunit housing and HOA rules influence the practical ceiling for fuel types and sizes, which steers selection toward safe, compliant choices.

Local regulation shapes the category’s path in many coastal states. Bay Area Spare the Air alerts curb charcoal use during poor air days, which diminishes the appeal of traditional briquettes during parts of the year and gently nudges demand toward compliant alternatives. Portland’s county advisories and Phoenix area restrictions on open burning create similar dynamics that push households and property managers to consider electric or gas for communal spaces. Mountain counties institute seasonal fire bans at higher wildfire risk, which constrains charcoal even on private property and necessitates flexible assortments for retailers[4]Summit County Government, “Seasonal Fire Bans,” Summit County Government, summitcountyco.gov. As a result, the United States barbeque grill market continues to reflect diverse local norms, and winning strategies tailor inventory, compliance information, and service models to neighborhood-level realities.

Competitive Landscape

Competition in the United States barbeque grill market is balanced across established brands that span entry, mid-range, and premium price tiers, with no single brand able to dictate market outcomes. Leading names emphasize connected features, material quality, and service coverage, while value-oriented offerings compete on feature parity and promotional depth. Portfolio breadth across gas, charcoal, pellet, and electric formats remains a common hedge against regional regulations and shifting consumer preferences. The May 2025 merger of Weber and Blackstone, supported by a sizable equity infusion and long-dated financing, further consolidated capabilities across traditional grills and flat top griddles, and positioned the combined platform to optimize retail footprints and service networks. This move has encouraged rivals to accelerate launches, particularly in connected and electric categories, to protect shelf space and brand mindshare.

Strategy themes include omnichannel expansion, connected feature roadmaps, and supply chain repositioning to manage tariffs and logistics risk. Co op partnerships that add premium grills into warehouse and drop ship programs give thousands of independent dealers more complete assortments and marketing support, enabling them to compete more effectively in local markets. On the product side, Weber’s WEBER CONNECT ecosystem integrates guided cooking and remote control across gas and charcoal lines, building a cross-fuel digital experience that can deepen loyalty. Napoleon’s connected electric model highlights performance targets that push flameless grills into full-size roles, which speaks to an urban and code-sensitive demand pool in the United States barbeque grill market. Pellet leaders continue to strengthen software features and accessories, while charcoal innovators add airflow management and digital monitoring to reduce user error.

Capital structure and portfolio moves signal confidence in premium segments and services. The Weber Blackstone combination reduced pro forma leverage and pushed maturities into the next decade, providing investment headroom for product and channel initiatives. Middleby’s late 2025 sale of a majority stake in its residential kitchen portfolio, including premium outdoor brands, unlocked capital for strategic priorities while maintaining a long-term interest in the category’s upside. Specialty retailers have also pursued targeted acquisitions in modular outdoor kitchens to broaden owned brand offerings and control more of the value chain from design to delivery. Across the board, execution in the United States barbeque grill market hinges on merchandising discipline, feature innovation that feels intuitive, and service models that simplify installation and upkeep for busy households and property managers.

United States Barbeque Grill Industry Leaders

Weber Inc.

Blackstone Products

Traeger, Inc.

Char-Broil (W.C. Bradley Co.)

Pit Boss (Dansons)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Weber expanded the WEBER CONNECT smart grilling ecosystem at CES, adding wireless probes, a smart hub display, and updated connected models across major fuel types.

- December 2025: Middleby sold a 51% stake in its Residential Kitchen Business, including Lynx, to private equity, retaining a 49% interest and receiving cash proceeds to optimize capital structure.

- May 2025: Weber LLC and Blackstone Products finalized their merger, creating a diversified outdoor cooking platform and reducing combined leverage with an equity infusion and extended maturities to 2032.

- January 2025: Traeger launched the Woodridge Series pellet grills with WiFIRE compatibility and a tiered feature set to reach broader price points.

United States Barbeque Grill Market Report Scope

A complete background analysis of the United States barbeque grill market, which includes emerging market trends by segments, significant changes in the market dynamics, key market players, and a market overview, is covered in the report.

The United States Barbeque Grill Market Is Segmented By Product (Gas, Charcoal, And Electric), By Application (Residential, Commercial), And By Distribution Channel (Online Stores, Offline Stores). The Report Offers Market Size And Forecasts For The United States Barbecue Grill Market In Value (USD) For All The Above Segments.

| Gas Grills |

| Charcoal Grills |

| Electric Grills |

| Pellet Grills |

| Hybrid/Alternative Fuel |

| Infrared |

| Built-In |

| Freestanding |

| Portable / Table-top |

| Disposable / Single-use |

| Conventional |

| Smart/Connected |

| Residential |

| Commercial |

| B2B/Direct from the Manufacturers | |

| B2C/Retail | Specialty Stores |

| Home Centers & DIY Stores | |

| Mass Merchandisers | |

| Online | |

| Other Distribution Channels |

| Northeast |

| Midwest |

| Southeast |

| Southwest |

| West |

| By Fuel Type | Gas Grills | |

| Charcoal Grills | ||

| Electric Grills | ||

| Pellet Grills | ||

| Hybrid/Alternative Fuel | ||

| Infrared | ||

| By Product Design | Built-In | |

| Freestanding | ||

| Portable / Table-top | ||

| Disposable / Single-use | ||

| By Technology | Conventional | |

| Smart/Connected | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | B2B/Direct from the Manufacturers | |

| B2C/Retail | Specialty Stores | |

| Home Centers & DIY Stores | ||

| Mass Merchandisers | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | Northeast | |

| Midwest | ||

| Southeast | ||

| Southwest | ||

| West | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the United States barbeque grill market?

The United States barbeque grill market size was USD 1.36 billion in 2025, is expected to reach USD 1.41 billion in 2026, and is forecast to reach USD 1.64 billion by 2031 at a 3.07% CAGR.

Which fuel type leads sales in the United States barbeque grill market?

Gas leads with a 47.92% share in 2025 due to convenience, control, and broad propane availability, while electric is the fastest growing at a 4.31% CAGR through 2031.

How are connected features changing buyer behavior in the United States barbeque grill market?

Smart models add guided cooking, wireless probes, and remote control that reduce user error and encourage upgrades from older analog units, with brand ecosystems from Weber, Napoleon, and Traeger setting the pace.

Which sales channels dominate the United States barbeque grill market?

B2C retail delivers 66.95% of sales and grows at a 3.88% CAGR on the strength of omnichannel experiences, in-store demos, and last-mile assembly that reduce friction.

How do regulations affect demand in the United States barbeque grill market?

Air quality rules often limit charcoal use and open flames during certain periods, which supports demand for gas and electric formats that comply with local restrictions.

What recent moves by leading companies are reshaping competition in the United States barbeque grill market?

The Weber Blackstone merger strengthened a cross-format portfolio with long-dated financing, while connected launches at CES and selective portfolio divestments signal continued investment in premium features and services.

Page last updated on: