Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

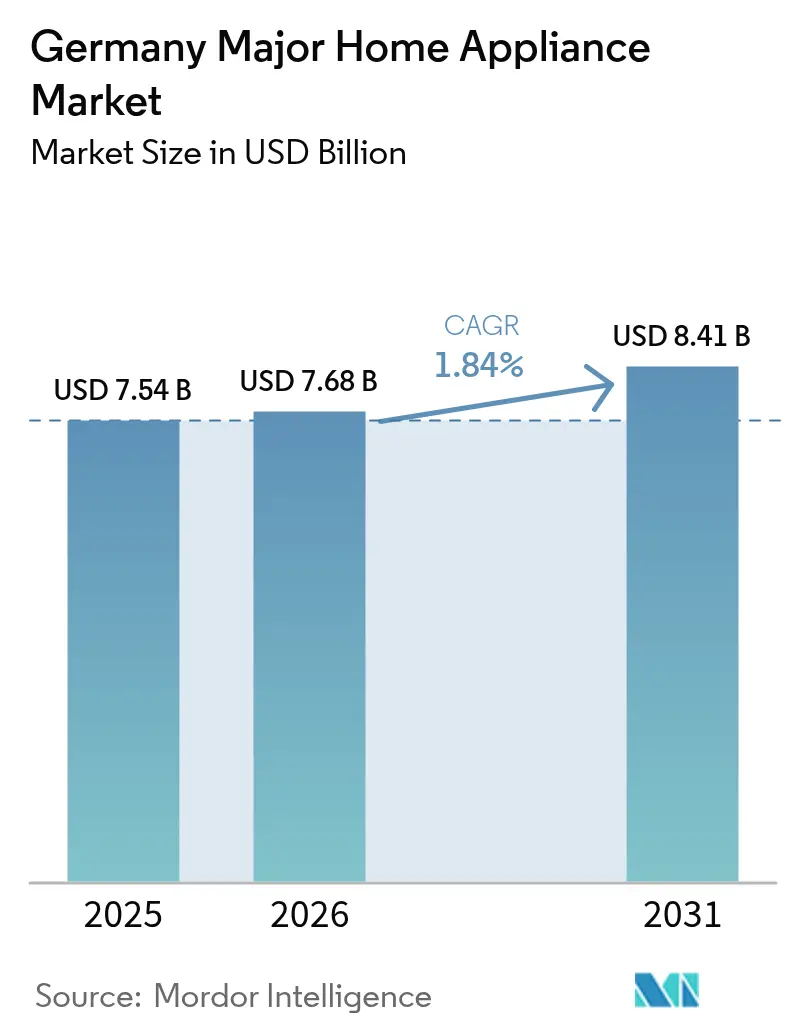

| Base Year Market Size (2025) | USD 7.54 Billion |

| Market Size (2026) | USD 7.68 Billion |

| Market Size (2031) | USD 8.41 Billion |

| Growth Rate (2026 - 2031) | 1.84% CAGR |

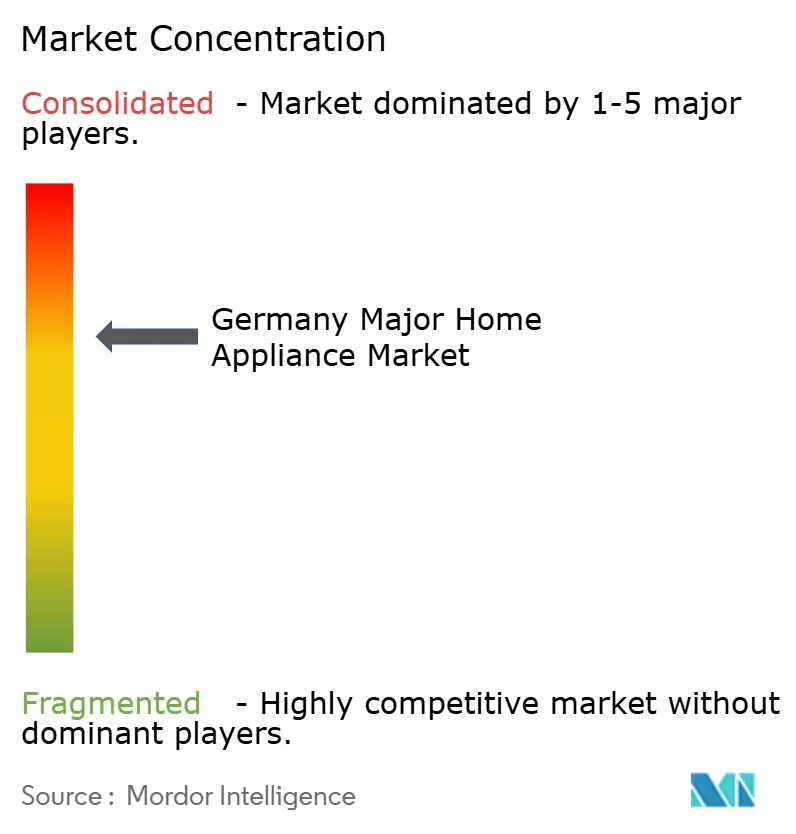

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Major Home Appliance Market Analysis by Mordor Intelligence

Germany major home appliances market size in 2026 is estimated at USD 7.68 billion, growing from 2025 value of USD 7.54 billion with 2031 projections showing USD 8.41 billion, growing at 1.84% CAGR over 2026-2031. The German major home appliances market is mature, yet replacement demand rises because energy-efficiency mandates shorten product life cycles. Government subsidies under KfW and BAFA tilt consumer choices toward A-class models even as raw-material inflation squeezes producer margins. Regulatory pressure, urbanization, and single-resident household growth keep sales volumes steady despite a construction slowdown. Competitive focus, therefore, shifts from unit expansion to software-driven efficiency upgrades, smart-home integration, and space-saving built-in formats. Digital channels complement physical retail, creating a consistent omnichannel journey for shoppers across the German major home appliances market.

Key Report Takeaways

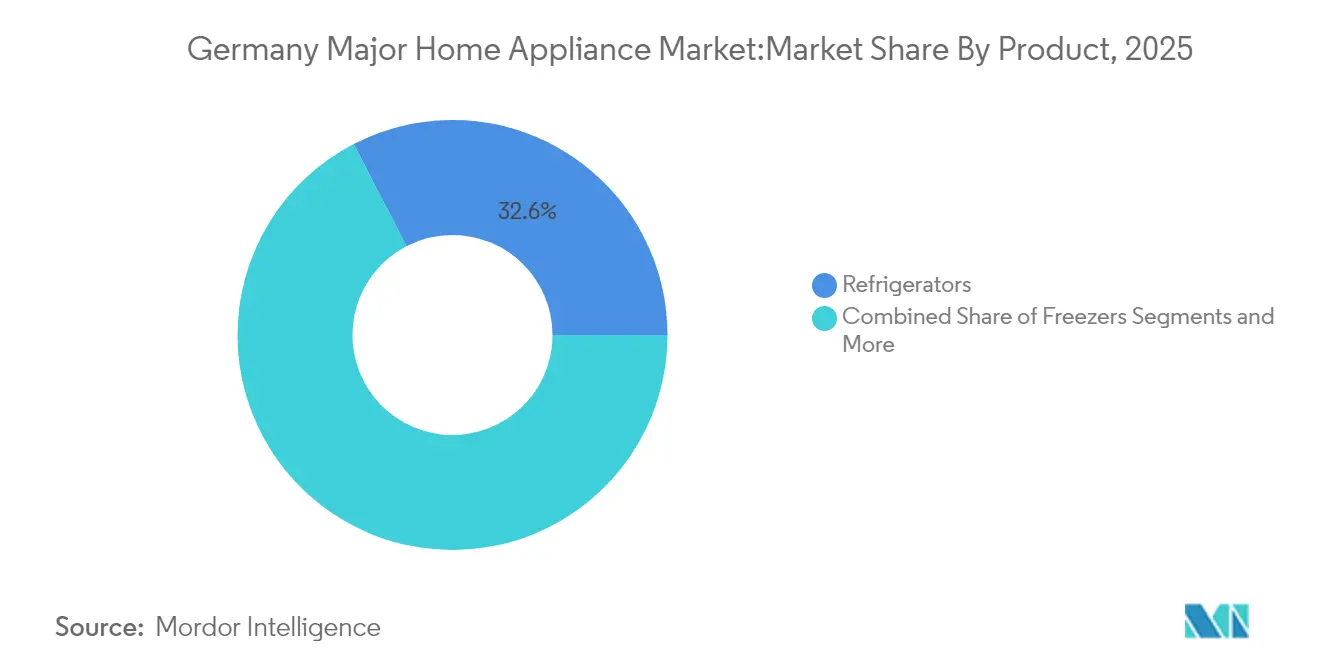

- By product, refrigerators led with 32.60% of the Germany major home appliances market share in 2025, while ovens are projected to grow at a 2.06% CAGR through 2031.

- By distribution channel, multi-brand stores held 34.40% share of the Germany major home appliances market size in 2025, whereas online retail is forecast to expand at a 2.63% CAGR to 2031.

- By region, North Rhine-Westphalia captured 23.70% of the Germany major home appliances market in 2025, and Baden-Württemberg is poised to record the fastest 2.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Major Home Appliance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-efficiency regulations accelerating replacement demand | +0.4% | National, with stronger impact in urban centers | Medium term (2-4 years) |

| Rapid adoption of smart/IoT-enabled appliances | +0.3% | National, led by North Rhine-Westphalia and Bavaria | Long term (≥ 4 years) |

| Built-in formats gaining share in urban kitchens | +0.2% | Urban areas, particularly North Rhine-Westphalia | Medium term (2-4 years) |

| Government subsidies for A-class white goods (KfW/BAFA) | +0.3% | National | Short term (≤ 2 years) |

| Growth of e-commerce pure-play retailers | +0.2% | National | Medium term (2-4 years) |

| Rising single-resident households driving compact SKUs | +0.1% | Urban centers nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy-Efficiency Regulations Accelerating Replacement Demand

The Building Energy Act obliges new heating systems installed from 2025 to source 65% of energy from renewables, and BAFA covers up to 70% of related costs. Replacement, therefore, occurs earlier than technical failure would dictate, particularly for boilers and cooling units whose retrofit bills can reach EUR 30,000 [1]BAFA, “Federal Funding for Efficient Buildings,” bafa.de. Gas prices rose 3.5% in H2 2024, so consumers welcome lower running costs that compliant appliances promise. Brands frame high-efficiency launches as regulatory solutions rather than lifestyle luxuries, realigning purchase priorities within the German major home appliances market.

Rapid Adoption of Smart/IoT-Enabled Appliances

Home-connect ecosystems now link with Amazon Alexa, Google Home, and Matter, letting owners monitor energy usage and schedule predictive maintenance. BSH unveiled a Matter-ready Bosch 100 Series refrigerator at CES 2025, underscoring software’s new value driver. Germany’s AI economy is growing 15% annually, so appliance data integration benefits from a broader digital-skills base. Manufacturers are able to push over-the-air updates and diagnostics, secure repeat engagement, a decisive advantage in the German major home appliances market [2]KfW, “Building Efficiency Subsidy Guideline,” kfw.de.

Built-In Formats Gaining Share in Urban Kitchens

Smaller city apartments reward appliances that disappear behind cabinetry. 2025 kitchen trends favor handle-less fronts, metallic tones, and flush induction cooktops with downdraft ventilation. BSH lifted German built-in sales in 2024 by adjusting its mix toward compact ovens and 45 cm dishwashers. As households invest in premium integrated solutions that free countertop space, average selling prices rise, boosting value more than volume across the German major home appliances market.

Government Subsidies for A-Class White Goods (KfW/BAFA)

The BEG scheme grants up to 45% toward energy-efficient renovations, while KfW’s heating subsidy can add bonuses that raise reimbursement to 70% for single-family homes. These incentives skew demand toward premium energy ratings, pulling orders forward when grant windows open. Mid-tier brands risk displacement if they cannot qualify models quickly, creating sporadic surges followed by lulls tied to federal budget cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw-material and logistics costs post-2024 | -0.3% | National, higher on import-dependent manufacturers | Short term (≤ 2 years) |

| Eco-design & repairability rules raising compliance costs | -0.2% | National | Medium term (2-4 years) |

| Stagnating new-build housing permits 2024-25 | -0.4% | National, heavier in rural/suburban markets | Medium term (2-4 years) |

| Mandatory WEEE collection fees squeezing retail margins | -0.1% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Raw Materials and Logistics Costs Post-2024

Producer prices for durable consumer goods increased 10.8% year over year, while 90% of electrical firms reported supply disruptions [3]ifo Institute, “Supply Bottlenecks Survey 2024,” ifo.de. Brands face a choice between price hikes that may stall volume or absorbing costs that erode profit. Imported compressors, copper, and electronic chips carry freight surcharges, intensifying the squeeze on mid-priced catalogues within the German major home appliances market.

Stagnating New-Build Housing Permits 2024-25

First-quarter 2024 permits dropped 22% to 53,500 units. Single-family approvals plunged 35.6%, erasing a reliable pipeline for built-in kitchens and laundry rooms. Manufacturers pivot toward renovation and retrofit niches, but heightened competition for replacement orders trims growth forecasts for the Germany major home appliances market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Refrigerators Lead While Ovens Accelerate Innovation

Refrigerators generated 32.60% sales in 2025, underpinning the Germany major home appliances market size for cold storage solutions. Near-universal 99.9% household penetration sustains predictable replacement linked to energy re-rating. In contrast, ovens grow at 2.06% CAGR on a smart-cooking wave that turns connectivity into recipe guidance and self-clean cycles. That pace makes ovens the fastest accelerator in the German major home appliances market. High-temperature enamel coatings, air-fry modes, and steam-assist features differentiate premium racks without enlarging footprints, matching urban built-in trends. Washing machines enjoy 96.2% penetration yet confront commoditization, so vendors load soft-sensor algorithms and eco-dose detergent systems to maintain price bands.

Dishwashers, adopted by 74.6% of homes, gain room to move upward as single-person apartments value hygiene and water conservation. Air conditioners, now in 19% of households, see the steepest climb; climate change expands cooling days, so split units and portable ACs move from luxury to necessity. Freezers lose share, squeezed between larger refrigerator freezer drawers and energy-rating mandates that penalize power-hungry standalone chests. In value terms, premium smart features yield higher average transaction prices. The Germany major home appliances market size for ovens alone is projected to grow faster than the overall basket, nudging brand portfolios toward self-steam and voice-controlled ranges. Market entrants that cannot integrate connectivity risk erosion even if their mechanical reliability remains high. Saturated categories rely on replacement frequency shortening under regulation rather than on first-time purchases, reinforcing the strategic weight of after-sales service, firmware updates and warranty extensions.

By Distribution Channel: Multi-Brand Dominance Faces Digital Disruption

Multi-brand chains held 34.40% of 2025 revenue, reflecting shopper preference for side-by-side comparison and bundled installation. Store associates act as de-facto compliance advisors, explaining subsidy paperwork and energy labels. This consultative selling model defends unit value but incurs high fixed costs. Online channels, gaining at 2.63% CAGR, leverage national courier density to promise next-day delivery even for large white goods. Price filters, user reviews and AR sizing tools demystify appliance selection, encouraging shoppers to complete high-ticket orders online. Blended options such as click-and-collect drive 41% of e-commerce baskets, further diluting pure footfall but keeping showroom relevance for tactile evaluation. Exclusive brand outlets curate experience around design studios and chef demonstrations that spotlight smart features in kitchens of the future. Although share is lower, ticket sizes skew premium, helping brands like Miele uphold margin discipline. Marketplace drop-ship sellers and specialty installers address narrow niches, including off-grid refrigerators and aged-care dishwashers. For every channel, end-to-end visibility of stock levels aligns pricing and avoids discount arbitrage. Supply-chain digitization therefore underpins service consistency across the Germany major home appliances market.

Geography Analysis

North Rhine-Westphalia contributed 23.70% of 2025 turnover, anchoring the Germany major home appliances market in its most populous state. Dense urban clusters such as Cologne and Düsseldorf combine high disposable income with apartment renovations that install built-in suites. Regional grant programs complement federal subsidies, magnifying uptake of A-class washers and heat-pump dryers. Manufacturers establish service depots near the Rhine-Ruhr logistics belt to meet same-day repair expectations. Bavaria remains a leading volume generator because Munich households favor premium German brands. High alpine holiday homes also replace equipment more frequently due to rental wear. Miele’s German factories, eight of which lie inside Bavaria and neighboring states, support quick in-market replenishment. Baden-Württemberg, projected at 2.33% CAGR, benefits from its innovation corridors around Stuttgart where tech-savvy consumers adopt IoT appliances early, bolstering smart device density inside the Germany major home appliances market.

Lower Saxony and Hesse keep mid-single-digit shares, balancing metropolitan growth with rural stasis. Northern coastal counties prioritize efficient tumble-dryers suited to wetter climates. Eastern states, grouped in Rest-of-Germany, reveal slower population growth yet display interest in subsidy-driven heat-pump solutions. Single-person households, accounting for more than 41% of the national total, cluster in Berlin and Hamburg, sustaining demand for slimline dishwashers and compact washer-dryers. Cross-state variation in grid tariffs further encourages efficient models, reinforcing federal efficiency rules but allowing localized messaging.Migration flows and urban redevelopment projects influence replacement pacing. Cultural preference for durable German engineering still guides purchase, but yields to software ecosystems when warranties align. Consequently, regional retailers tailor assortments: NRW stores stock broad built-in lines, Bavarian showrooms highlight connectivity, while Baden-Württemberg emphasizes energy dashboards. Despite heterogeneity, subsidy alignment makes energy class A the common baseline across Germany's major home appliances market.

Regulatory Landscape

Germanys major home appliances regulatory environment is anchored in EU ecodesign and energy labeling rules, with national enforcement strengthened in 2026. On June 26, 2026, Germany published the Act on the Modernization of the National Implementation of European Regulations on Ecodesign and Energy Labeling (BGBl. I 2026 Nr. 191), updating the domestic legal basis and replacing the earlier Energieverbrauchsrelevante-Produkte-Gesetz (2008) to align with the new EU Ecodesign for Sustainable Products framework (Regulation (EU) 2024/1781, adopted June 13, 2024). The modernization raises the practical importance of technical documentation, labeling accuracy, and conformity processes for manufacturers and importers selling into Germany.

Market surveillance and compliance checks are mainly carried out by the German Laender authorities, with EU tools such as the Information and Communication System on Market Surveillance (ICSMS) providing support. Alongside ecodesign and labeling, the Product Safety Act (Produktsicherheitsgesetz, ProdSG) remains a core horizontal requirement for safe product placement, reinforcing obligations on product safety, traceability, and corrective actions when issues are identified.

Value Chain Analysis

The Germany major home appliances value chain begins with global and regional sourcing of steel, plastics, compressors, motors, and semiconductors, then moves into design and engineering (including firmware, connectivity modules, and app ecosystems) before assembly and testing at European and German plants. Industry structure is supported by trade bodies such as ZVEI, which represents around 55 manufacturers and more than 80 brands, with over 60 production locations in Europe (more than 20 in Germany) and a meaningful domestic footprint across production and R&D sites.

Downstream, finished goods distribute through multi-brand retail, kitchen and furniture trade channels (important for built-in formats), exclusive brand outlets, and expanding online platforms, while installation, take-back, and after-sales service add value for households. Compliance and sustainability requirements increasingly influence supplier qualification and transparency across tiers, including due-diligence processes under Germanys Supply Chain Due Diligence Act (LkSG). Industry associations and cooperatives such as ZVEI and ProBusiness ElektroHausgeraete e.V. also coordinate positions on standardisation and sustainability, helping medium-sized brands align specifications, marketing, and compliance practices.

Competitive Landscape

Market concentration is moderate as legacy leaders protect brand equity while challengers invest in smart integration. BSH Hausgeräte booked EUR 15.3 billion sales in 2024 and channelled 5.5% of revenue into R&D that produced Matter-compatible refrigerators and AI-diagnostic dishwashers. The strategy reinforces perceived reliability and futureproofing. Miele retained EUR 5.04 billion revenue but announced 2,700 job reductions to release EUR 500 million savings by 2026, signaling cost realignments amid premium cyclicality. Yet its 125th anniversary induction hob launch with antifingerprint glass underlines continued design leadership.

International entrants accelerate acquisition. Midea’s April 2025 purchase of Küppersbusch’s parent company grants the Chinese group heritage German branding and OEM networks. Bosch strengthened its climate-control segment by acquiring Johnson Controls and Hitachi’s HVAC arm, doubling Home Comfort Group revenue to EUR 9 billion and extending heat-pump coverage across the Germany major home appliances market. LG and Microsoft’s AI appliance agent partnership adds cross-industry tech clout that may upset incumbents lacking cloud scale.

Retail groups evolve simultaneously. MediaMarktSaturn grew retail-media income fivefold with Sponsored Brand Ads, monetizing digital shelf visibility. Such ancillary revenues subsidize price matching without eroding margin. Pure-plays refine last-mile delivery, using hub-and-spoke micro-fulfilment in NRW to shorten lead times to six hours. Supply networks integrate reverse logistics for WEEE compliance, a must as repairability regulation tightens. Overall, firms that fuse energy compliance, smart features and omnichannel support retain strategic headroom in the Germany major home appliances market.

Germany Major Home Appliance Industry Leaders

BSH Hausgeräte GmbH

Miele & Cie KG

Whirlpool Corporation

Electrolux AB

Samsung Electronics

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

In a mature, replacement-driven market with high household equipment levels (for example, 2023 penetration around 99.9% for refrigerators and 97.4% for washing machines), growth opportunity centers on trading up rather than first-time adoption. Programs and regulation that reward lower operating costs keep A-class and high-efficiency models at the core of the proposition, while connected features add value through energy monitoring, diagnostics, and software updates integrated into smart-home ecosystems.

Built-in and space-efficient formats also offer an actionable lane, supported by observed category mix shifts: built-in appliances showed a slight upward trend in 2025, with strong gains in electric cookers and cooktops. On the supply side, manufacturers keep funding product and platform refresh cycles, illustrated by BSHs March 2026 disclosure of sustained innovation spending (EUR 847 million in R&D for 2025) and continuation of its investment strategy during 2026. These initiatives translate into more frequent model updates (efficiency, connectivity, and design integration), expanding opportunities for retailers and installers who package appliances with kitchen planning, financing, and compliant take-back services.

Recent Industry Developments

- May 2026: Miele launched the Triflex HX3 cordless vacuum cleaner series, including variants designed for wet cleaning with the Aqua Twister Pro nozzle. The launch broadens Mieles premium cleaning portfolio and supports upsell strategies through feature-led differentiation and accessory ecosystems.

- March 2026: BSH Home Appliances reported 2025 turnover of EUR 15.0 billion and stated it would continue its investment strategy through 2026. The update reinforces the role of R&D and digital capabilities as competitive levers in Germanys replacement-driven major appliance categories.

- June 2024: Reuters reported that Bosch was exploring an offer for Whirlpool, citing sources. Even without a completed transaction, the report highlighted ongoing strategic interest in scale and portfolio consolidation that can influence competitive positioning and partnership dynamics across the appliance supply chain.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market includes major (large) home appliances sold in Germany, covering new refrigerators and freezers, washing machines, tumble dryers, dishwashers, large cooking appliances, and room air-conditioners, across freestanding and built-in formats.

Scope exclusions: Small countertop appliances, consumer electronics, HVAC systems above 12 kW, and aftermarket parts are not counted.

Segmentation Overview

- By Product

- Refrigerators

- Freezers

- Washing Machines

- Dishwashers

- Ovens (Incl. Combi & Microwave)

- Air Conditioners

- Other Major Home Appliances

- By Distribution Channel

- Multi-Brand Stores

- Exclusive Brand Outlets

- Online

- Other Distribution Channels

- By Geography

- North Rhine-Westphalia

- Bavaria

- Baden-Württemberg

- Lower Saxony

- Hesse

- Rest of Germany

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary, build the demand context, and collect consistent time series for appliances and housing-linked drivers. We leaned on public sources such as Destatis, Eurostat, UN Comtrade, the European Commission energy-labeling and ecodesign rules, and Germany customs and trade releases, since these help explain appliance replacement cycles and pricing direction.

We also reviewed company annual reports, investor presentations, retailer and association releases, and reputable business press coverage to cross-check shipment direction, promotion intensity, and category momentum. Where needed, we referenced paid subscriptions for company financials and patent databases to confirm product launches and technology shifts that can move average selling prices. The desk sources named above are illustrative only, and we used additional public and paid references to validate and clarify assumptions.

Primary Interviews and Surveys

Primary work was used to pressure-test the model assumptions that are hard to read from public data alone, especially mix shifts between built-in and freestanding appliances and the role of energy efficiency upgrades in replacement demand. We spoke with stakeholders across manufacturers, distributors, retailers, installers, and service partners, and inputs were balanced across the main regions that influence Germany demand patterns (APAC, EMEA, and the Americas) to avoid over-relying on a single viewpoint.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 12% | |

| Mid tier: 50% | Functional/Unit leaders: 36% | |

| Smaller Players: 14% | Managers: 52% |

Market-Sizing & Forecasting

The model starts from a top-down reconstruction of Germany demand using category-level consumption signals, and then it is checked against selective bottom-up approximations before totals are finalized. In practice, we map major appliance demand to a realistic pool of households and replacement cycles, and then apply price and mix assumptions by category.

Key inputs used in the build (illustrative) include housing stock and household formation trends, replacement timing for core categories like washing machines and refrigerators, built-in versus freestanding mix, energy-efficiency regulation pull-through, and average selling price movement linked to materials and feature upgrades. Where direct volume signals are patchy for a given year, gaps are handled by using proxy indicators such as import and export direction, retailer demand commentary, and channel inventory normalization.

Forecasts are produced using scenario analysis supported by a small set of drivers that interviewees consistently pointed to, such as renovation activity, consumer sentiment for big-ticket purchases, and pricing normalization after promotion-heavy periods. The final forecast path is adjusted only when multiple checks line up, which keeps the outlook explainable and repeatable.

Data Validation & Update Cycle

Totals are validated through triangulation across demand drivers, trade signals, and category-level reasonableness checks, and then unusual jumps are flagged for a second review. We also compare growth rates against independent indicators like housing activity and major appliance replacement momentum, and any mismatch is investigated before sign-off.

The work goes through multi-step analyst review, and interview follow-ups are triggered when pricing, mix, or category definitions look inconsistent across sources. Reports are refreshed annually, with interim updates when material events occur, and a final pass is completed right before delivery so clients receive the most current view.

Mordor Intelligence's Germany Major Home Appliance Market Size Versus Other Published Estimates

Published market sizes can look far apart even when they discuss the same country, because the product boundary and the pricing logic are not always aligned. Differences also show up when one estimate is built from unit-based demand signals and another leans heavily on revenue reports or broad appliance definitions.

By tracking category-level replacement demand and refresh assumptions (ASP movement, built-in share, and room air-conditioner inclusion) in Mordor Intelligence, the number stays tied to major white goods sold as new units in Germany, instead of drifting into small appliances, parts, or wider HVAC revenue.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.54 B (2025) | |

| Industry Association A | USD 8.20 B (2025) | Often rolls small appliances and some accessory revenue into the same basket, and then applies blended pricing that lifts totals versus major appliances only. |

| Trade Journal B | USD 6.90 B (2025) | Tends to use a narrower revenue base focused on shipment value through selected channels, which can miss built-in sales captured through kitchen and renovation routes. |

The spread in the table is mainly explained by scope boundaries and how prices are applied when categories are mixed. When the counted items are kept to major appliances and checked against demand and trade direction, the market total becomes easier to trace and reproduce year to year.

Key Questions Answered in the Report

What is the current value of the Germany major home appliances market?

The market is valued at USD 7.68 billion in 2026 and is on track to reach USD 8.41 billion by 2031.

Which product segment leads sales?

Refrigerators account for 32.60% of 2025 revenue, making them the largest category.

Why are replacement cycles shortening in Germany?

Energy-efficiency legislation and generous KfW and BAFA subsidies encourage households to swap still-functional units for A-class models.

How fast is online appliance retail growing?

Online channels are projected to grow at a 2.63% CAGR through 2031, outpacing physical store expansion.

Which German state buys the most major appliances?

North Rhine-Westphalia holds 23.70% of national turnover owing to its large population and high urban density.

What strategic moves stand out among manufacturers recently?

BSH launched Matter-compatible products, Midea acquired Küppersbusch’s parent, and Bosch doubled its HVAC revenue via the Johnson Controls and Hitachi deal.

Page last updated on: