United Kingdom Barbeque Grill Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

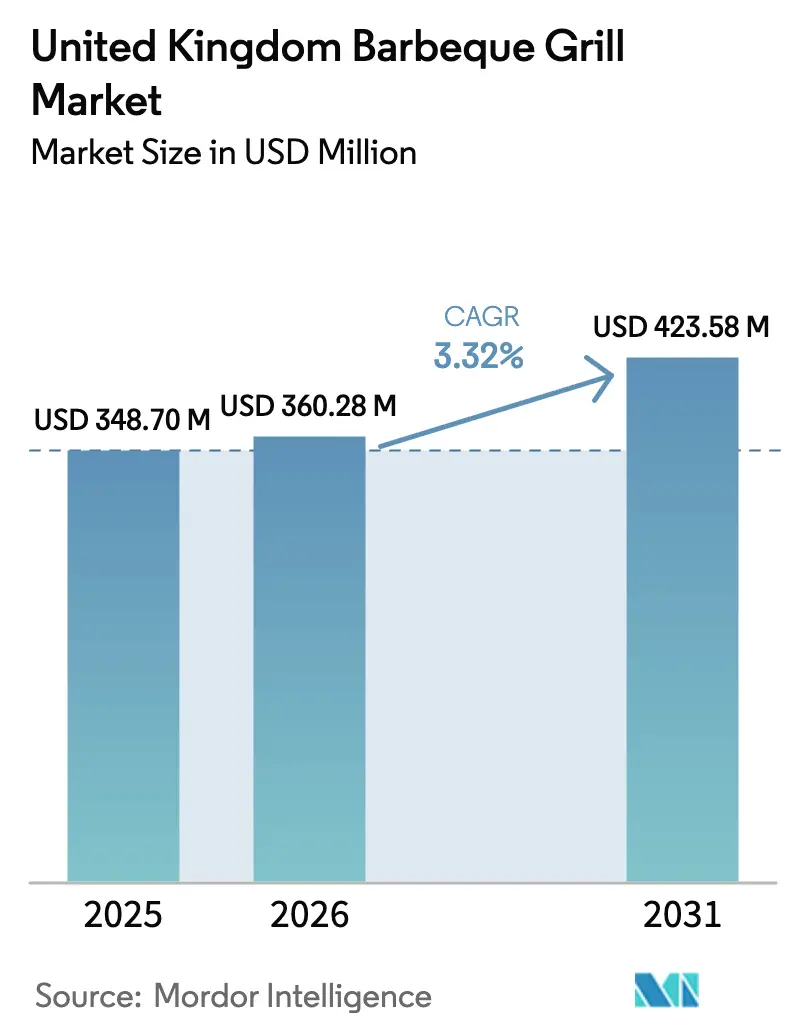

| Base Year Market Size (2025) | USD 348.7 Million |

| Market Size (2026) | USD 360.28 Million |

| Market Size (2031) | USD 423.58 Million |

| Growth Rate (2026 - 2031) | 3.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Barbeque Grill Market Analysis by Mordor Intelligence

The United Kingdom barbeque grill market size in 2026 is estimated at USD 360.28 million, growing from 2025 value of USD 348.7 million with 2031 projections showing USD 423.58 million, growing at 3.32% CAGR over 2026-2031. Demand is buoyed by a 54% surge in BBQ equipment turnover at garden centres as staycation spending reshapes home-improvement priorities, while 127.6 million grilling occasions logged in 2022 validate habitual use despite Britain’s variable weather[1]Source: Staff Writer, “BBQ occasions rise as consumers grill through the rain,” thegrocer.co.uk.. Clean-air legislation is accelerating the switch toward electric and pellet models, encouraging manufacturers to embed IoT controls and hybrid fuel that future-proof portfolios against tighter smoke-control enforcement. Consolidation is stirring Weber’s merger with Blackstone amplifies scale in a moderately fragmented arena while preserving distinct brand voices. Growth resilience is further evidenced by new smart-connected flagships such as the Weber SUMMIT gas grill, whose digital dashboards redefine premium positioning.

Key Report Takeaways

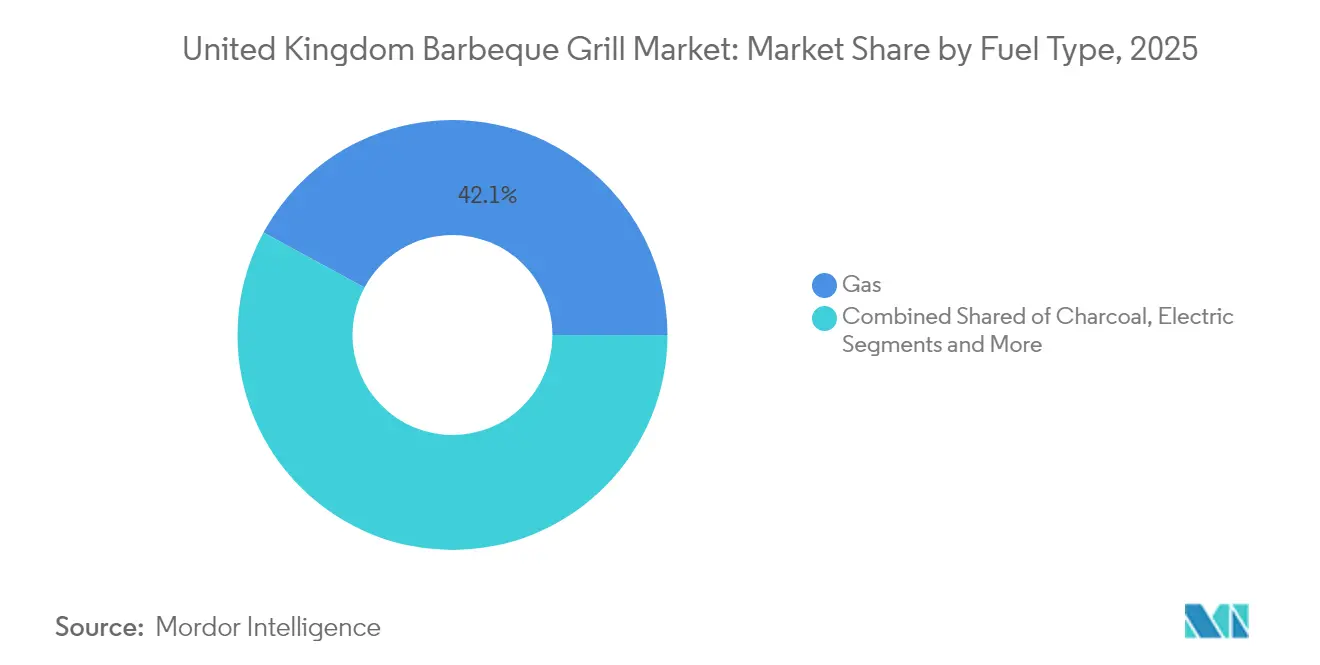

- By fuel type, gas grills led with 42.10% of the United Kingdom barbeque grill market share in 2025, while electric units are forecast to expand at a 4.18% CAGR through 2031.

- By product design, freestanding models secured 47.65% share of the United Kingdom barbeque grill market size in 2025, and portable variants are advancing at a 3.21% CAGR during the same horizon.

- By technology, conventional formats captured 81.85% share in 2025; smart-connected alternatives are poised for a 4.28% CAGR to 2031.

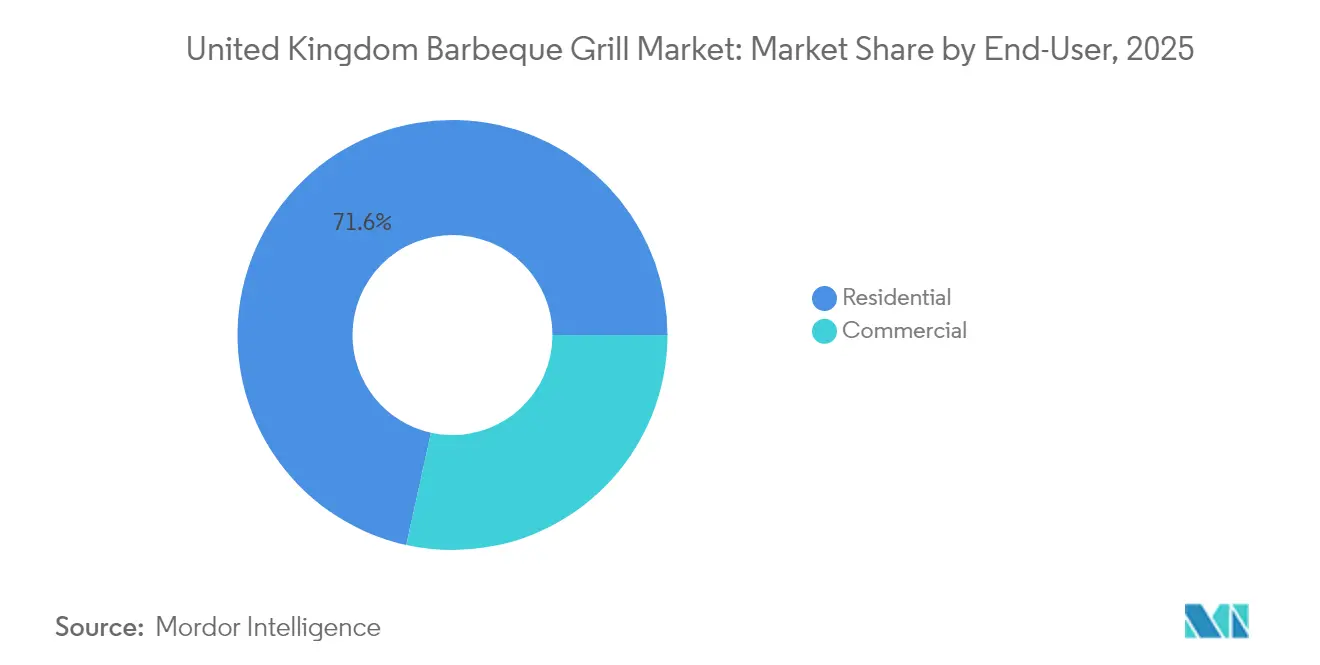

- By end-user, residential buyers accounted for 71.55% of the United Kingdom barbeque grill market size in 2025, whereas commercial demand is recovering at a 3.62% CAGR on the back of hospitality expansion.

- By region, England contributed 28.85% revenue in 2025, whereas Scotland is the fastest-growing geography with a 4.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Barbeque Grill Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing outdoor-dining & staycation trend | +0.5% | National, with stronger influence in England and Scotland | Medium term (2-4 years) |

| Rising disposable income & home-improvement spend | +0.4% | England and Wales primarily, urban centers | Medium term (2-4 years) |

| Product innovation toward hybrid & multi-fuel grills | +0.6% | National, early adoption in metropolitan areas | Long term (≥ 4 years) |

| Expansion of e-commerce retail for BBQ equipment | +0.5% | National, accelerated in Scotland and Northern Ireland | Short term (≤ 2 years) |

| Shift to electric & pellet grills driven by Clean-Air Zones | +0.6% | England urban areas, expanding to Scotland and Wales | Long term (≥ 4 years) |

| Smart-connected (IoT) grill adoption | +0.5% | England and Scotland tech-forward demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Outdoor-Dining & Staycation Trend

The United Kingdom barbeque grill market continues to reap benefits from a shift toward domestic leisure as 26% of consumers remained loyal to barbecuing even during record rainfall and 40% simply moved grills indoors, proving weather resilience[2]Source: Quality Meat Scotland, “Great British BBQ Report 2024,” qms.scot. . London exemplifies the cultural turn, where 18% of residents barbecue monthly, normalizing year-round usage that underpins equipment replacement cycles. Staycation budgets redirect holiday outlays into patio refurbishments, stimulating sales of premium freestanding islands and complementary accessories that anchor the United Kingdom barbeque grill market. Garden centres pivoted from seasonal racks to permanent grill showrooms, leveraging footfall from landscape shoppers to upselling higher-margin smart units. The net effect is a durable structural uplift expected to sustain segmental expansion beyond macro-economic turbulence.

Rising Disposable Income & Home-Improvement Spend

Garden centre turnover reached GBP 5 billion (USD 6.5 billion) in 2024 as households allocated discretionary cash to property enhancements, reaffirming grills as durable assets rather than impulse purchases. Gender analysis shows women scrutinize costs more closely, prompting brands to blend advanced features with affordability to widen penetration. Disposable-income disparities foster tiered demand: England adopts smart infra-red burners, while Scotland and Northern Ireland favor cost-efficient gas carts, yet both cohorts feed the broader United Kingdom barbeque grill market. Manufacturers tailoring SKUs to these income gradients maximize regional conversion.

Product Innovation Toward Hybrid & Multi-Fuel Grills

Hybrid designs gaining traction combine gas, charcoal, pellet, and electric options in one shell, enabling owners to align fuel choice with local smoke rules or flavor goals. Weber’s SUMMIT SmartControl demonstrates the trend, pairing top-down infra-red broiling with remote monitoring that appeals to tech-savvy chefs. Integrated modular prep stations encourage consumers to scale layouts over time, shrinking initial outlays while future-proofing kitchens—an angle pivotal for upselling within the United Kingdom barbeque grill market. Multi-fuel capability also mitigates supply risk amid gas-price swings, reassuring cost-conscious households. Compact blueprints fold multifunctional prowess into footprints suited to balcony constraints, opening hybrid adoption to renters traditionally sidelined in premium segments.

Expansion of E-Commerce Retail for BBQ Equipment

Digital commerce has become a critical lifeline, granting Scottish and Northern Irish buyers equal access to premium lines once limited to England’s showrooms. Garden centres now fuse online catalogues with click-and-collect bays, boosting cross-sell of cover accessories that protect high-end stainless frames from rain damage. Direct-to-consumer disruptors mine browsing data to design bundle promos, locking in recurring pellet subscriptions that steadily enlarge the United Kingdom barbeque grill industry. Augmented-reality view-in-yard apps reduce hesitation for USD 1,000-plus outlays by helping shoppers visualize space impact. Seasonality is managed through online preorder queues that smooth manufacturing loads and minimize retail stockouts, tightening working-capital cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unpredictable UK weather shortens grilling season | -0.3% | National, particularly Scotland and Northern England | Short term (≤ 2 years) |

| Strict smoke-emission & food-safety rules | -0.2% | England urban areas, expanding to other regions | Medium term (2-4 years) |

| Higher steel/aluminium costs post-Brexit | -0.2% | National, affecting all manufacturers | Short term (≤ 2 years) |

| Meal-kit/delivery services limiting at-home grilling | -0.2% | Urban areas, particularly London and Manchester | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Unpredictable UK Weather Shortens Grilling Season

Britain logged its wettest summer on record, eroding spontaneous weekend grilling yet users adapted: 40% relocated cookouts under patio canopies or indoors, cushioning the blow. Manufacturers responded with water-resistant lids, fast-heat burners, and fold-up frames that deploy quickly during dry intervals. Retailers synchronized promotions with meteorological apps, accelerating sales spikes once sunshine was forecasted. Regional variance is stark; Scotland endures longer rain spells and hence favors weather-proof portable units that store neatly in sheds. Resultant CAGR drag is moderate and partially balanced by accessory upsells such as gazebo kits across the United Kingdom barbeque grill market.

Strict Smoke-Emission & Food-Safety Rules

DEFRA-mandated fuel lists constrain charcoal varieties, nudging consumers toward cleaner briquettes or alternate fuels[3]Source: UK Government, “Smoke Control Area Rules,” gov.uk. Compliance certifications inflate R&D budgets as brands integrate catalytic burn chambers and temperature interlocks. Yet first-mover advantage accrues to compliant innovators that lock out lower-spec imports, tilting market share gains to agile domestic makers inside the United Kingdom barbeque grill market. Food-safety codes push probe-port standardization, adding cost but opening premium margins that offset volume softness. Long run, regulatory rigor catalyzes cleaner technology adoption rather than curtailing total demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Gas Dominance with Electric Momentum

Gas retained 42.10% of 2025 revenue as dependable ignition, controllable flames, and affordable LPG cylinders suit Britain’s changeable climate. Electric variants record the fastest 4.18% CAGR because landlords and Clean Air Zones restrict open-flame devices, positioning plug-in formats as the compliance standard for flats. Charcoal holds nostalgic appeal yet cedes share to pellet models that marry hardwood aroma with automated augers, courting connoisseurs seeking hands-off smoking. Hybrid carts incorporating dual burners and storage for briquettes liberate users from single-fuel dependency—an edge in regions where fuel choice fluctuates with local regulation. Smart gas launches like Weber’s SUMMIT fortify gas leadership by layering Wi-Fi precision onto proven burners, ensuring the United Kingdom barbeque grill market remains multi-fuel rather than single fuel dominated.

Electric adoption does face electricity tariff questions, but total-cost parity improves once gas cylinder delivery fees and charcoal waste disposal are counted. Pellet supply chains mature as domestic sawmills divert residues into food-grade pellets, reducing import reliance. Future product roadmaps show infrared electric coils approaching charcoal sear temperatures, likely narrowing performance perception gaps. Consequently, fuel diversification is both a regulatory hedge and consumer empowerment lever that underpins category vibrancy.

By Product Design: Portables Advance on Space Constraints

Freestanding islands still wield 47.65% share, admired for side tables, warming racks, and cabinetry intuitive for suburban gardens. Yet portable grills escalate at 3.21% CAGR amid rising apartment stock and campsite tourism. Foldable legs, 12 kg carry weights, and integrated butane canisters target balcony dwellers in Manchester high-rises and glamping enthusiasts in Welsh hills. Built-in modules populate outdoor kitchens, reflecting property-value confidence among southern English homeowners. Disposable foil pans ebb under green scrutiny, nudging casual users toward reusable tabletop electrics priced below GBP 100 (USD 130).

Brands now market “mobile freestanding” hybrids, full-size cooking decks atop detachable wheelbases, letting owners winter-store units in sheds. Table-height portables featuring clamp-on legs upgrade picnic ergonomics, opening the United Kingdom barbeque grill market to audiences with physical-comfort needs. Materials innovation sees powder-coated steel swapped for aluminium composites, shaving weight and rust-risk simultaneously. In-store planograms shift to showcase portability solutions adjacent to trunk-friendly coolers, feeding impulse purchases as spring bank holiday road-trips approach.

By Technology: Smart Grills Stretch Premium Envelope

Conventional models dominate at 81.85%, yet smart units rocket at 4.28% CAGR, commanding ASPs double their analog peers. Integrated LCDs, probe-guided cook programs, and firmware upgrades eradicate under- or over-done anxieties for novice pit-masters. App alerts nudge cooks to flip steaks, while AI recipe libraries in Beta promise dynamic heat curve adjustments for cut thickness. Resistance persists among older demographics nervous about connectivity complexity, prompting brands to offer manual override knobs alongside digital UIs.

Connectivity challenges, garden Wi-Fi dead zones, are met with dual Bluetooth mesh that hands off to 4G add-on dongles. Lithium battery packs power controllers during patio outages, minimizing cook disruptions. Data captured, usage frequency, temperature logs, feeds CRM engines that upsell grill covers once rainfall predictions spike in the Midlands, enhancing lifetime value inside the United Kingdom barbeque grill market. Component cost deflation suggests smart penetration could surpass 30% by 2030, redefining baseline consumer expectations just as digital thermostats reshaped indoor ovens.

By End-User: Residential Core, Commercial Revival

Residential ownership drove 71.55% of 2025 revenue as pandemic-era patio builds matured into sustained lifestyle routines. Commercial revival at 3.62% CAGR gains steam alongside hospitality rebound, with pubs extending beer gardens through canopy investments and restaurants adding curbside smoker theatrics to entice passers-by. Professional kitchens demand NSF-certified stainless frames, 24-hour duty cycles, and high-BTU infrareds able to speed-sear 400 burgers nightly. Those advancements trickle down to premium homeowner lines, conditioning buyers to expect cast-bronze burners and rotisserie motors once reserved for steakhouses.

Post-Brexit staff shortages motivate operators to adopt smart dashboards that standardize cook profiles across rotating crews, reducing training costs. Residential DIYers embrace similar convenience, purchasing chef-curated pellet blends identical to restaurants. The cross-pollination tightens product-development feedback loops, with consumer color-palette preferences, matte black, forest green, seeping into commercial aesthetics, spawning a cohesive United Kingdom barbeque grill market design language.

By Distribution Channel: Retail Hub, Omni-Channel Future

Brick-and-mortar B2C still accounts for 74.90% because tactile evaluation of lid heft and grate gauge remains critical for GBP 600+ (USD 780) choices. Specialist grill boutiques deploy live-fire demos, aromatic smoke, and chef Q&A to justify premium tags, a science that online videos struggle to replicate. Home-centre aisles link grills to decking timber, fostering bundled checkout tickets that capture holistic backyard budgets. Mass retailers cater to price-sensitive first-time buyers but lack deep expertise, ceding upselling to niche chains.

E-commerce stores compound at double digits within the retail slice, a path smoothed by free pallet deliveries and 12-month 0% finance. Web-native challengers curate limited SKUs but enrich pages with 4K assembly tutorials, taming intimidation among beginners and expanding the United Kingdom barbeque grill industry audience. Click-and-collect appeals to rural counties where courier windows clash with farm schedules. Loyalty apps issue pellet restock reminders timed to estimated depletion rates, embedding annuity revenue streams and driving overall channel profitability.

Geography Analysis

England anchors the United Kingdom barbeque grill market with 28.85% share, propelled by dense population, London’s 18% monthly grill frequency, and mature retail footprints that ensure after-sales parts availability. Disposable income and home equity gains feed luxury outdoor-kitchen installs featuring gas lines, pizza ovens, and smart lighting. Clean-Air Zones in major cities accelerate electric and pellet swaps, making England a bellwether for regulatory responses and subsequent nationwide rollouts. Commercial activity is vibrant as pubs exploit extended terrace licences to offset indoor crowd caps, driving replacement cycles for high-throughput gas rotisseries.

Scotland leads growth at 4.32% CAGR even with harsher weather, as 40% of enthusiasts shift under awnings during rain, demonstrating persistent usage. Tourism along North Coast 500 fuels portable grill rentals among camper-van fleets. Local pride in Scotch Beef propels demand for high-heat searing surfaces, encouraging stores in Inverness and Aberdeen to stock ceramic kamados. E-commerce fills geographic gaps, ensuring Highlands consumers receive the same smart grills as Edinburgh tech adopters. Government climate pledges create grant schemes for low-emission tourism facilities, indirectly boosting pellet install bases.

Wales contributes steady revenue anchored in caravan culture around Snowdonia and Pembrokeshire, where compact butane portables dominate. Rural broadband upgrades promise to lift smart-grill penetration, an area still nascent. Northern Ireland balances agricultural heritage with cross-border price arbitrage, importing Republic-sourced charcoal variants yet adopting British-made electric units for Belfast apartments. Combined, these regions underscore the diverse mosaic that shapes opportunities across the United Kingdom barbeque grill market.

Competitive Landscape

Market structure is moderately fragmented; top five brands capture roughly 45%, leaving room for nimble entrants focusing on eco credentials or IoT differentiation. Weber and Blackstone’s February 2025 merger pools kettle pedigree with griddle innovations, creating a one-stop catalogue spanning smoker cabinets to breakfast stations[4]Source: GTN Xtra Editors, “Weber and Blackstone to Merge Outdoor Cooking Operations,” gtn-xtra.com.. Traeger leverages its pellet forte to launch balcony-compliant Mini Timberline units, bundling subscription pellets that ensure flavor consistency. Napoleon courts steak purists via ceramic infrared SIZZLE ZONE burners that reach 900 °C in 30 seconds, a spec heavily featured in in-store demos.

Start-ups such as Britain-built Everhot tease solar-integrated electric grills pitched to eco estates, while Ooni cross-sells portable pizza ovens alongside modular grill plates, expanding category boundaries. Supply-chain resiliency carries weight: Brexit-induced port delays punish brands lacking local warehousing, granting domestically assembled lines a speed advantage during peak May bank holiday runs. Compliance mastery—securing DEFRA authorised-fuel stamps—serves as moat against low-cost imports, fortifying premium price realization and fueling R&D reinvestment that widens innovation gaps inside the United Kingdom barbeque grill market.

United Kingdom Barbeque Grill Industry Leaders

Weber-Stephen Products LLC

Char-Broil

Napoleon Grills

Landmann

Outback International UK

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Weber and Blackstone Products entered a definitive merger agreement to combine their outdoor-cooking businesses, forming a multi-brand portfolio spanning grills, griddles, and accessories, with Blackstone.

- April 2024: Weber LLC introduced its 2024 line featuring the SUMMIT SmartControl gas grill, SLATE gas griddles, and the compact WEBER TRAVELER, each incorporating remote monitoring, digital ignition, and modular add-ons for kitchen-like versatility.

United Kingdom Barbeque Grill Market Report Scope

A barbecue grill is a piece of equipment that uses heat applied from below to cook food. Barbecue grills can be powered by gas, charcoal, smoke, hybrid, or electricity, depending on the heat source. A complete background analysis of the United Kingdom barbeque grill market, which includes emerging market trends by segments, significant changes in the market dynamics, key market players, and a market overview, is covered in the report.

The United Kingdom Barbeque Grill Market Was Segmented By Product (Gas, Charcoal, And Electric), By Application (Residential, Commercial), And By Distribution Channel (Online Stores, Offline Stores). The Report Offers Market Size And Forecasts For The United Kingdom Barbecue Grill Market In Value (USD) For All The Above Segments.

| Gas Grills |

| Charcoal Grills |

| Electric Grills |

| Pellet Grills |

| Hybrid/Alternative Fuel |

| Infrared |

| Built-In |

| Freestanding |

| Portable / Table-top |

| Disposable / Single-use |

| Conventional |

| Smart/Connected |

| Residential |

| Commercial |

| B2B/Direct from the Manufacturers | |

| B2C/Retail | Specialty Stores |

| Home Centers & DIY Stores | |

| Mass Merchandisers | |

| Online | |

| Other Distribution Channels |

| England |

| Scotland |

| Wales |

| Northern Ireland |

| By Fuel Type | Gas Grills | |

| Charcoal Grills | ||

| Electric Grills | ||

| Pellet Grills | ||

| Hybrid/Alternative Fuel | ||

| Infrared | ||

| By Product Design | Built-In | |

| Freestanding | ||

| Portable / Table-top | ||

| Disposable / Single-use | ||

| By Technology | Conventional | |

| Smart/Connected | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | B2B/Direct from the Manufacturers | |

| B2C/Retail | Specialty Stores | |

| Home Centers & DIY Stores | ||

| Mass Merchandisers | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | England | |

| Scotland | ||

| Wales | ||

| Northern Ireland | ||

Key Questions Answered in the Report

What is the current value of the United Kingdom barbeque grill market?

The sector stands at USD 360.28 million in 2026 and is forecast to hit USD 423.58 million by 2031.

Which fuel category is growing fastest?

Electric grills, expanding at a 4.18% CAGR, outpace all other fuel types thanks to Clean-Air Zone compliance.

How popular are smart-connected grills?

Smart units, though only 18.15% of volume, are growing at a 4.28% CAGR as IoT features become mainstream.

Why is Scotland’s growth higher than other regions?

Strong staycation culture, resilient grilling despite rain, and robust e-commerce access fuel Scotland’s 4.32% CAGR.

How will Clean-Air Zones affect future purchasing?

Emission restrictions will continue to shift demand toward electric and pellet models that meet smoke-control standards.

Page last updated on: