Barbeque Grill Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.36 Billion |

| Market Size (2031) | USD 8.14 Billion |

| Growth Rate (2026 - 2031) | 5.06% CAGR |

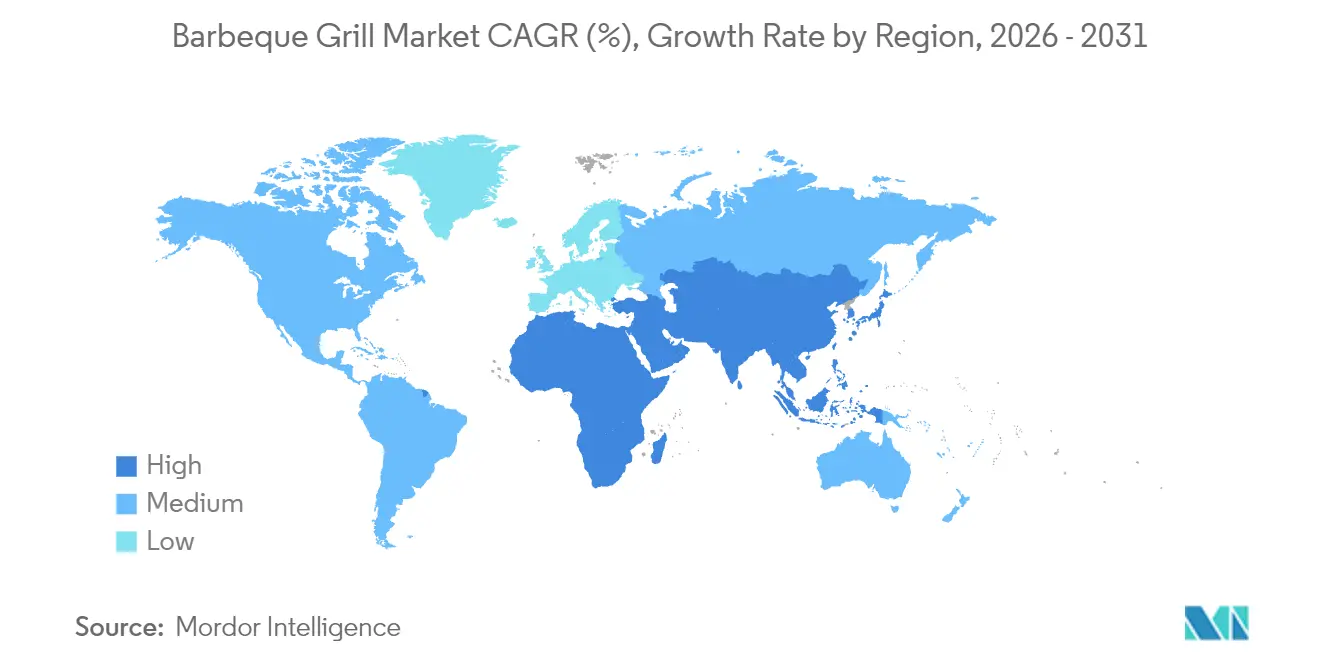

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Barbeque Grill Market Analysis by Mordor Intelligence

The barbeque grill market size was valued at USD 6.05 billion in 2025 and estimated to grow from USD 6.36 billion in 2026 to reach USD 8.14 billion by 2031, at a CAGR of 5.06% during the forecast period (2026-2031). Steady gains stem from the sector’s integration into a wider outdoor recreation economy, which contributed USD 639.5 billion GDP in 2023[1]Source: U.S. Bureau of Economic Analysis, “Outdoor Recreation Satellite Account, 2025,” bea.gov. Consumer enthusiasm for home-centered leisure, coupled with rising disposable incomes in emerging markets, sustains consistent demand for gas and pellet units even as raw-material volatility challenges producer margins. Industry consolidation accelerates after the Weber–Blackstone tie-up, creating a global heavyweight with deep R&D resources and an expansive distribution footprint. In parallel, smart-enabled grills move rapidly from premium novelty to mass-market expectation as IoT connectivity improves precision, convenience, and brand differentiation.

Key Report Takeaways

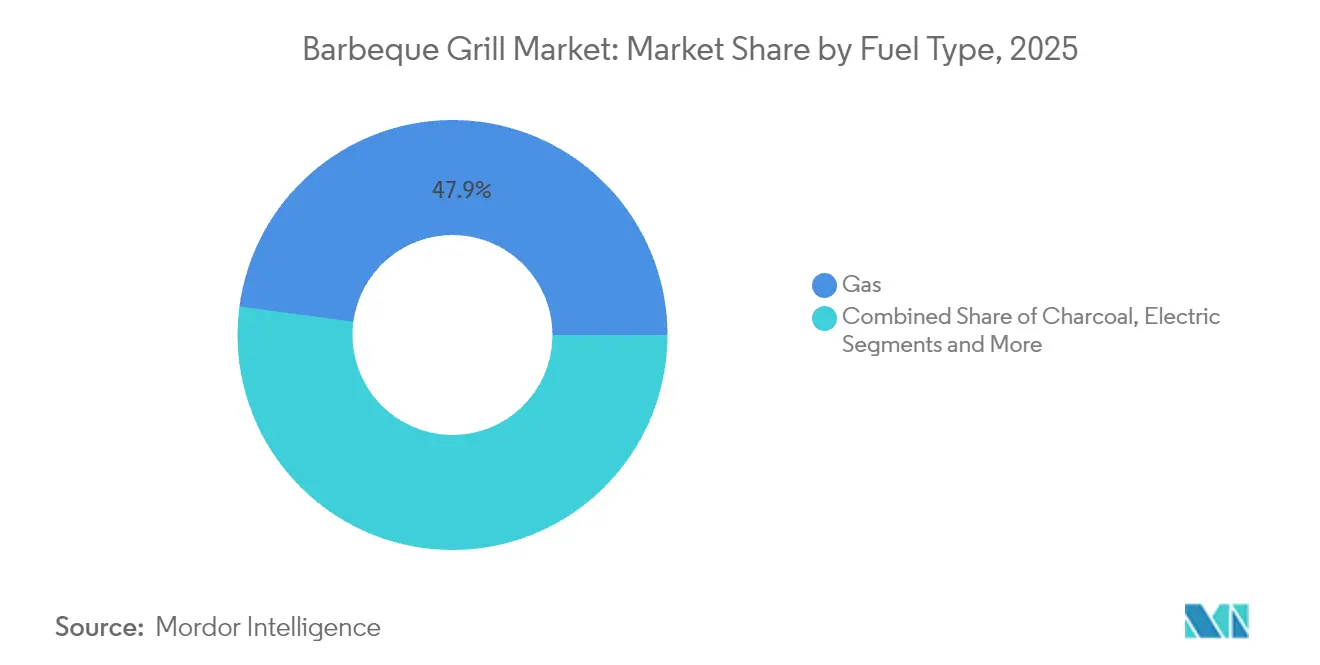

- Gas grills led with 47.88% of barbeque grill market share in 2025, whereas pellet grills are advancing at a 6.54% CAGR through 2031.

- Freestanding formats captured 58.05% of the barbeque grill market in 2025; portable models record the fastest 6.06% CAGR to 2031.

- Conventional technology held an 84.55% share of the barbeque grill market in 2025, yet smart grills are growing at 6.63% CAGR.

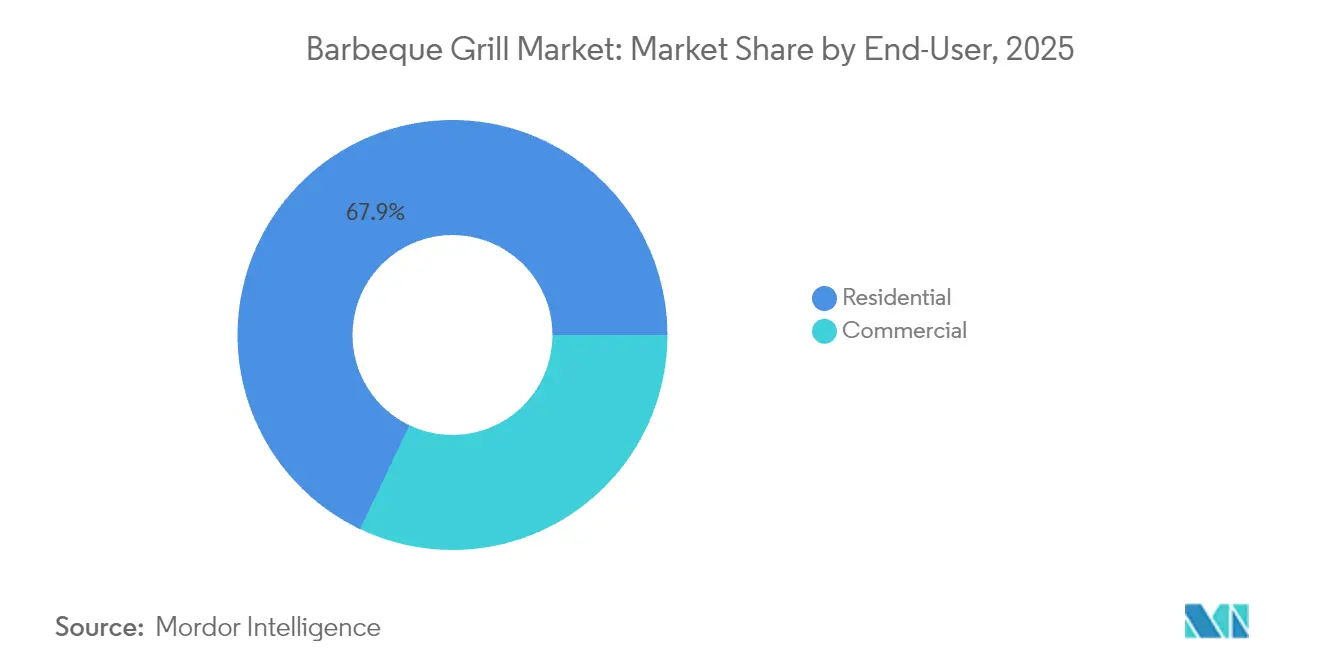

- The residential end user segment accounted for 67.92% of barbeque grill market size in 2025, while commercial installations expand at 5.61% CAGR.

- North America commanded 28.84% of barbeque grill market size in 2025, whereas Asia-Pacific is forecast to post the highest 6.88% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Barbeque Grill Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising popularity of outdoor cooking in developed economies | +1.2% | North America & Europe | Medium term (2-4 years) |

| Increasing availability of multifunctional smart grills | +0.9% | Global, with early adoption in North America | Short term (≤ 2 years) |

| Growing disposable income & urbanization in emerging markets | +1.5% | Asia-Pacific core, spill-over to MEA | Long term (≥ 4 years) |

| Surge in tail-gating culture around e-sports tournaments | +0.3% | North America & Europe | Medium term (2-4 years) |

| Carbon-neutral propane blends spurring gas-grill demand | +0.4% | North America, California leading | Long term (≥ 4 years) |

| Rise of outdoor entertainment spaces in post-pandemic home renovations | +0.8% | Global, concentrated in suburban markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising popularity of outdoor cooking in developed economies

COVID-19 shifted leisure patterns toward outdoor pursuits, drawing 7.1 million additional Americans into recreation in 2020 and fueling an 18.9% jump in the broader outdoor economy by 2021[2]Source: U.S. Census Bureau, “Outdoor Participation Trends,” census.gov. Consumers now view grills as core components of backyard upgrades, often specifying commercial-grade units and multi-zone cook surfaces in new-build plans[3]Source: National Kitchen & Bath Association, “2025 Design Trends,” nkba.org. Flavor experimentation spans Asian, Italian, and Mexican profiles, encouraging purchases of specialty accessories such as woks and planchas. Premium outdoor kitchens leverage stainless steel, granite, and modular cabinetry to deliver year-round functionality even in colder climates. The barbeque grill market thus benefits from a durable lifestyle shift rather than a transitory pandemic spike.

Increasing availability of multifunctional smart grills

Traeger’s WiFIRE platform allows remote temperature control across 2.7 million connected units, illustrating how IoT elevates convenience and food safety. Weber’s 2024 Summit Smart Grill layers touchscreen controls and in-hood sensors that automate searing, roasting, and smoking cycles. Predictive maintenance alerts reduce downtime while app-based recipe libraries deepen brand engagement, keeping consumers within proprietary ecosystems. Mid-tier price points now include Bluetooth probes and voice-assistant integration, widening addressable audiences beyond early adopters. As more households value hassle-free precision, smart functionality becomes a baseline expectation rather than a premium upsell.

Growing disposable income & urbanization in emerging markets

Asia-Pacific’s rapid urban expansion stimulates rooftop and balcony grilling, even in space-constrained apartments where compact electric or portable gas models thrive. Rising middle-class wages turn grills into aspirational lifestyle products rather than utilitarian appliances. Youthful demographics embrace Western techniques yet adapt them to local flavors, buying accessories for skewers, flatbreads, and seafood common in regional cuisines. Developers respond by adding communal barbecue areas to high-rise complexes, embedding outdoor cooking into everyday social rituals. Urban apartment dwellers increasingly invest in compact, electric, and portable grilling solutions that accommodate limited outdoor space while delivering authentic cooking experiences.

Surge in tail-gating culture around e-sports tournaments

E-sports events attract younger, tech-savvy crowds that merge gaming with outdoor gatherings, expanding demand for lightweight, quick-deploy grills. Portable batteries such as EcoFlow’s RIVER 2 Pro enable electric grilling where propane is restricted, ensuring venue compliance. Social-media-friendly aesthetics—bright colors, folding legs, and multi-fuel versatility—resonate with this cohort and magnify word-of-mouth reach. Brands gain visibility by sponsoring tournament tailgates, introducing grilling to consumers previously outside the core audience. The trend opens incremental volume without cannibalizing mainstream suburban sales. The cultural fusion of gaming and grilling creates marketing opportunities for brands to engage with demographics traditionally outside the core grilling market, expanding the total addressable market beyond conventional outdoor cooking enthusiasts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating raw-material (steel & aluminum) prices | -0.8% | Global manufacturing hubs | Short term (≤ 2 years) |

| Seasonality of demand in colder regions | -0.6% | Northern North America & Europe | Medium term (2-4 years) |

| Municipal restrictions on charcoal emissions in cities | -0.4% | Urban centers globally | Long term (≥ 4 years) |

| Supply-chain disruptions & freight-cost volatility | -0.5% | Global, with Asia-Pacific manufacturing impact | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fluctuating raw-material (steel & aluminum) prices

Weber posted a USD 330 million net loss in fiscal 2022 after inflation and currency swings inflated input costs, illustrating margin compression when spot steel rises 15-20% within one quarter. Larger players hedge through multi-year contracts, whereas smaller firms must absorb spikes or raise prices, risking share erosion. Some producers reduce thickness or switch to coated sheet to manage costs, but durability perceptions can suffer. Value-tier items face the harshest impact because price sensitivity limits pass-through latitude. Persistent volatility accelerates consolidation as capitalized manufacturers acquire distressed rivals to secure volume discounts. Premium brands can partially offset material cost increases through value-added features and brand positioning, while value-oriented products face direct margin pressure that may require retail price adjustments or specification reductions.

Seasonality of demand in colder regions

Retail sell-through peaks from April to August, leaving dealers with costly inventory that must be discounted before winter, squeezing gross margins. Production lines confront under-utilization during off-season months, inflating per-unit overhead. While cold-weather ignition systems exist, adoption remains niche because snow and low daylight discourage outdoor cooking. Brands counterbalance by expanding in milder Sun-Belt states and exporting to the Southern Hemisphere to create counter-seasonal revenue. Nevertheless, the barbeque grill market endures cyclical cash-flow swings that complicate working-capital management. Geographic concentration of seasonal demand in key markets like Canada and northern U.S. states limits total addressable market expansion and forces companies to rely heavily on southern and international markets for consistent revenue streams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Gas Dominance Faces Pellet Disruption

Gas grills hold 47.88% of barbeque grill market share in 2025 to push-button ignition and precise flame control, while pellet units account for 6.54% CAGR through 2031 due to wood-fired flavor and digital thermostats. Charcoal models persist among purists but encounter regulatory pressure from particulate limits, restricting urban adoption. Electric and hybrid designs address apartment rules and wildfire bans, broadening household penetration. Traeger’s Woodridge series helped December 2024 sales jump 30%, showcasing pellet appeal among flavor-driven consumers. Manufacturers now bundle multiple fuel options to hedge against regional regulation and taste preferences, supporting category resilience.

Pellet technology narrows performance gaps by introducing sear plates and direct-flame modes that rival gas for high-heat tasks, enhancing perceived versatility. Weber’s Searwood line combines app control with 600 °F searing, positioning pellets as an all-purpose platform. Renewable propane initiatives also sustain gas relevance by offering carbon-neutral options without hardware changes. The barbeque grill market size for gas models will still expand, but at a slower pace, as pellet adoption accelerates among younger buyers valuing flavor and tech convenience. Competitive dynamics thus hinge on balancing legacy gas loyalty with emerging pellet enthusiasm.

By Product Design: Portability Gains Ground

Freestanding units captured 58.05% of the barbeque grill market in 2025 because they balance cooking area, storage, and price. Portable grills, however, record a 6.06% CAGR on the back of tail-gating, camping, and apartment living trends. Built-in configurations flourish inside luxury outdoor kitchens where homeowners desire cohesive aesthetics and integrated utilities, lifting average transaction values beyond USD 5,000. Disposable single-use trays address convenience but face environmental pushback that deters permanent category growth. Consumers increasingly demand modularity, leading brands to design cart-mounted bases that detach into tabletop mode, blurring historical design boundaries.

Urban millennials gravitate toward Weber’s Traveler series, which folds to car-trunk size while retaining 320 sq in of cooking space. Premium homeowners invest in masonry islands featuring gas, charcoal, and pellet bays, illustrating multi-fuel convergence at high price tiers. Product marketers emphasize weight, setup time, and BTU output for portable lines, contrasting with finish, warranty, and customization for built-ins. The barbeque grill market leverages these divergent value propositions to maximize volume and margin across income brackets. Expect continued innovation in collapsible frames and lightweight alloys to satisfy growing mobility demands.

By Technology: Smart Features Drive Innovation

Conventional knobs and analog thermometers still control 84.55% of 2025 shipments, yet smart grills register 6.63% CAGR as connectivity moves mainstream. Early adopters appreciated remote monitoring; today’s buyers also seek auto-shutdown, meat-probe algorithms, and cloud-recipe libraries that prevent overcooking. Traeger’s WiFIRE ecosystem posts only 3.6% U.S. household penetration, indicating vast headroom within the barbeque grill market. Middleby Corp. funnels commercial IoT expertise into residential launches, shortening cook cycles through predictive flame modulation. Voice assistants from Amazon and Google now integrate with grill apps, allowing hands-free temperature tweaks that enrich user experience.

Component costs decline as Wi-Fi modules commoditize, enabling mid-tier SKUs under USD 599 to include smartphone dashboards. Cloud analytics deliver firmware updates that extend appliance life and foster brand attachment long after the initial sale. Security patches and data-privacy assurances become selling points as grills increasingly join smart-home networks. For traditionalists, brands retrofit plug-and-play probe kits so legacy models participate in connected ecosystems, monetizing after-market accessories. The barbeque grill industry therefore transforms from hardware-centric to service-enabled, unlocking recurring revenue streams.

By End-User: Commercial Growth Accelerates

Residential buyers represented 67.92% of barbeque grill market size in 2025, reaffirming backyard cooking as a home-life staple. Commercial venues—restaurants, resorts, and caterers—grow at 5.61% CAGR, drawn by live-fire theatrics that elevate dining ambience. Post-pandemic regulations encourage al-fresco service, prompting eateries to invest in NSF-rated, high-throughput units. Food trucks and pop-up kitchens choose compact, propane-fired models that meet safety codes and deliver consistent output in tight spaces. Cross-over products blur boundaries as residential customers buy commercial-grade stainless steel systems for long-term value and bragging rights.

Urban ordinances restricting smoke push restaurants toward gas or electric grills with catalytic converters, accelerating replacement cycles in dense metros. Hotels market poolside barbecue packages, bundling chef experiences with equipment rentals during peak tourist seasons. Corporate campuses add outdoor cooking stations to attract employees back on site, supporting weekday throughput. Manufacturers tailor SKUs with fold-out shelves, interchangeable grates, and heavy-duty casters to suit high-volume use cases. Consequently, commercial adoption diversifies revenue sources and offsets residential seasonality.

By Distribution Channel: Retail Dominance Strengthens

B2C retail commands 73.12% of 2025 global sales and posts a robust 6.17% CAGR as omnichannel strategies unify online research with store pickup. Tractor Supply’s rollout of Weber products to 500 outlets evidences big-box expansion into rural catchments that traditionally relied on independent dealers. Specialty stores retain relevance by staffing certified grill masters who offer assembly, maintenance, and cooking classes. E-commerce volumes rise due to curbside delivery of large crates, aided by freight partnerships that include lift-gate service and timed scheduling. Direct-to-consumer portals boost margins and harvest user-behavior data for targeted upsells such as rubs and covers.

Mass merchandisers focus on entry-level SKUs during Memorial Day and Prime Day promotions, funneling traffic toward premium lines displayed in end-caps. Virtual showrooms employ augmented reality to visualize built-in islands within customer patios, reducing return risk for big-ticket orders. Loyalty programs bundle accessories and consumables, generating annuity sales beyond the initial hardware purchase. Installation services become a differentiator as more consumers choose complex built-in modules requiring professional hookup. The barbeque grill market consequently rewards retailers that integrate fulfillment, financing, and after-sales support into one seamless journey.

Geography Analysis

North America controlled 28.84% of barbeque grill market size in 2025, propelled by 76 million grill-owning households and a cultural penchant for outdoor gatherings. Southern states permit year-round usage, yet northern zones endure seasonal demand dips despite innovations like insulated fireboxes. Municipal smoke regulations hamper charcoal growth in cities, steering buyers toward gas and pellet alternatives that meet EPA thresholds. Premium adoption continues as suburban homeowners allocate renovation budgets to elaborate outdoor kitchens outfitted with refrigeration, sinks, and smart-enabled grills. Retail partnerships broaden rural reach, sustaining volume even when discretionary spending tightens.

Asia-Pacific delivers the fastest 6.88% CAGR through 2031, fueled by urbanization, rising middle-class incomes, and growing affinity for Western cooking styles blended with regional flavors. Compact electric grills and tabletop gas units cater to limited balcony spaces in megacities such as Shanghai, Mumbai, and Jakarta. Governments encourage communal recreation by adding barbecue pits to public parks, supporting casual social dining. International tourism spreads grilling culture as travelers emulate experiences enjoyed abroad, further stimulating local demand. Currency volatility and trade barriers remain risks, yet multi-plant sourcing within ASEAN reduces supply-chain exposure for global brands.

Europe exhibits steady mid-single-digit expansion as households extend living areas into gardens and terraces post-pandemic. Northern countries normalize winter grilling with double-layer lids and cold-start ignition systems, countering daylight shortages. Mediterranean consumers integrate grills into traditional wood-fired cuisine, preferring ceramic kamado styles for bread and pizza preparation. Stricter emissions frameworks prompt gas and electric substitution in dense urban neighborhoods, though countryside regions continue charcoal traditions. The barbeque grill market benefits from widespread environmental consciousness, spurring interest in renewable propane and sustainably sourced hardwood pellets.

Mordor Intelligence provides coverage of the barbeque grill market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Germany incorporating local coverage and market participation, as required.

Competitive Landscape

The global barbeque grill market remains moderately fragmented; however, consolidation trends intensify following the Weber–Blackstone merger that pools R&D, marketing, and supply-chain muscle under one corporate roof. Traeger dominates the pellet niche with 2.7 million U.S. units sold since 2020, yet that figure equates to only 3.6% household penetration, underscoring vast upside for connected wood-smoke technology. Char-Broil, Napoleon, and Coleman compete on value, leveraging private-label deals with mass merchants to undercut premium rivals. Middleby focuses on commercial crossover, repackaging professional ovens and vent-hood expertise into residential lines that command higher ASPs. New entrants like Spark Grills emphasize charcoal flavor with electric filament ignition, illustrating how innovation continues across fuel categories despite regulatory scrutiny.

Technology serves as the primary differentiator: cloud analytics, AI-driven cook algorithms, and subscription recipe services foster stickier customer relationships than hardware alone. Direct-to-consumer channels deliver higher gross margin, but require robust logistics and after-sales infrastructure to manage big-box packages. ESG narratives gain prominence, with brands publicizing decarbonization roadmaps and recyclable packaging to meet retailer scorecard criteria. As economies of scale favor multiproduct portfolios, niche startups may partner or license IP rather than building full-stack operations. Competitive intensity will likely increase until smart-feature penetration approaches parity with indoor kitchen appliances.

Barbeque Grill Industry Leaders

Weber Inc.

Traeger, Inc.

Napoleon Grills

Char-Broil (W.C. Bradley)

Masterbuilt

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Weber LLC and Blackstone Products agreed to merge, forming a diversified outdoor-cooking platform led by Blackstone CEO Roger Dahle while retaining both brand identities.

- January 2025: Weber unveiled its 2025 collection featuring the re-engineered SPIRIT gas grill with Boost Burner, SMOQUE wood-pellet smoker, and SLATE griddle priced from USD 399 to USD 899.

- January 2025: Weber unveiled its 2025 collection featuring the re-engineered SPIRIT gas grill with Boost Burner, SMOQUE wood-pellet smoker, and SLATE griddle priced from USD 399 to USD 899.

- April 2024: Weber’s 2024 lineup introduced the SUMMIT Smart Gas Grill, SLATE rust-proof griddles, and SEARWOOD pellet grills featuring DirectFlame searing.

Global Barbeque Grill Market Report Scope

A barbecue grill is a type of cooking apparatus where food is cooked using heat that is applied from below. A barbecue grill's heating element can vary, and it can be fueled by gas, electricity, or charcoal. In the report, a full background analysis of the global barbecue grill market is given, including a look at the market as a whole, new trends by segment and regional market, and major changes in market dynamics. The global barbecue grill market is segmented by product type (gas, charcoal, and electric), by application (household and commercial), and by geography (North America, Europe, Asia-Pacific, South America and Latin America, and the Middle East and Africa). The report offers market sizes and forecasts in value (USD) for all the above segments.

| Gas Grills |

| Charcoal Grills |

| Electric Grills |

| Pellet Grills |

| Hybrid/Alternative Fuel |

| Infrared |

| Built-In |

| Freestanding |

| Portable / Table-top |

| Disposable / Single-use |

| Conventional |

| Smart/Connected |

| Residential |

| Commercial |

| B2B/Direct from the Manufacturers | |

| B2C/Retail | Specialty Stores |

| Home Centers & DIY Stores | |

| Mass Merchandisers | |

| Online | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | |

| NORDICS | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Fuel Type | Gas Grills | |

| Charcoal Grills | ||

| Electric Grills | ||

| Pellet Grills | ||

| Hybrid/Alternative Fuel | ||

| Infrared | ||

| By Product Design | Built-In | |

| Freestanding | ||

| Portable / Table-top | ||

| Disposable / Single-use | ||

| By Technology | Conventional | |

| Smart/Connected | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | B2B/Direct from the Manufacturers | |

| B2C/Retail | Specialty Stores | |

| Home Centers & DIY Stores | ||

| Mass Merchandisers | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | ||

| NORDICS | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the global barbeque grill market in 2026?

The barbeque grill market size is USD 6.36 billion in 2026 and is forecast to reach USD 8.14 billion by 2031.

Which fuel type is growing the fastest?

Pellet grills show the highest momentum, expanding at a 6.54% CAGR through 2031 to wood-fire flavor and digital temperature control.

What share do gas grills hold today?

Gas grills hold 47.88% of barbeque grill market share as of 2025, maintaining leadership through convenience and wide availability.

Which region offers the strongest growth outlook?

Asia-Pacific leads with a projected 6.88% CAGR, driven by urbanization, rising incomes, and compact product formats suited to apartment living.

How important is smart technology to future sales?

Smart-enabled units are expected to grow at 6.63% CAGR as connectivity, app control, and predictive cooking features become mainstream.

Page last updated on: