Optical Genome Mapping Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

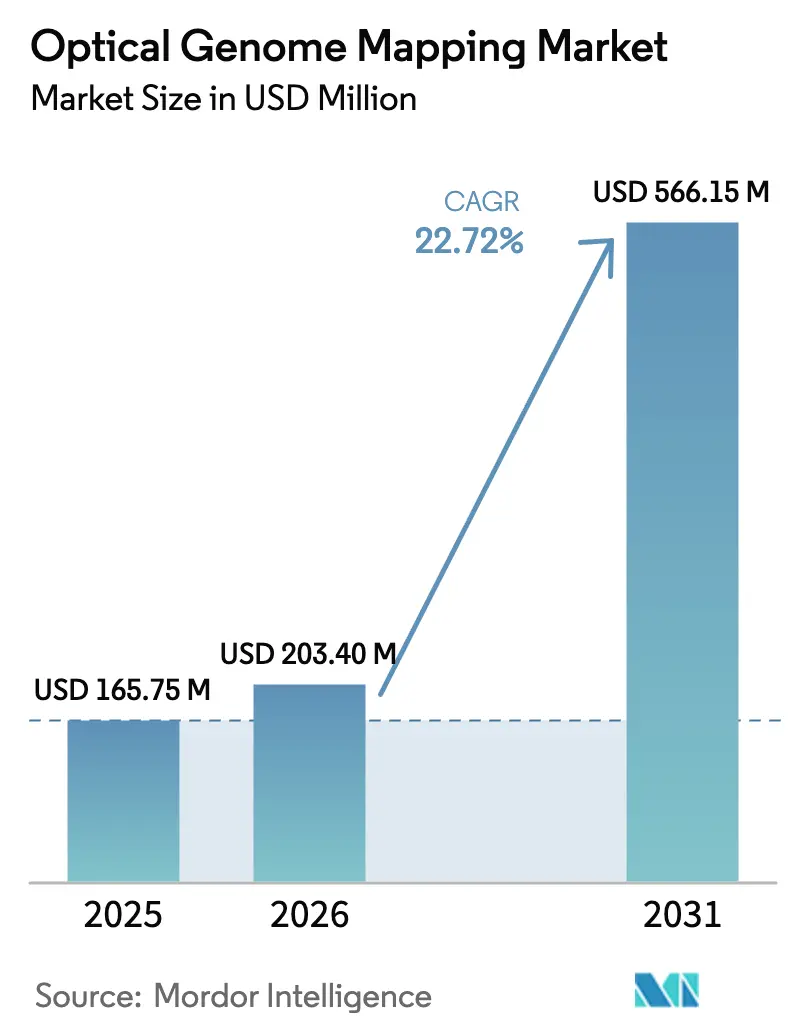

| Market Size (2026) | USD 203.4 Million |

| Market Size (2031) | USD 566.15 Million |

| Growth Rate (2026 - 2031) | 22.72% CAGR |

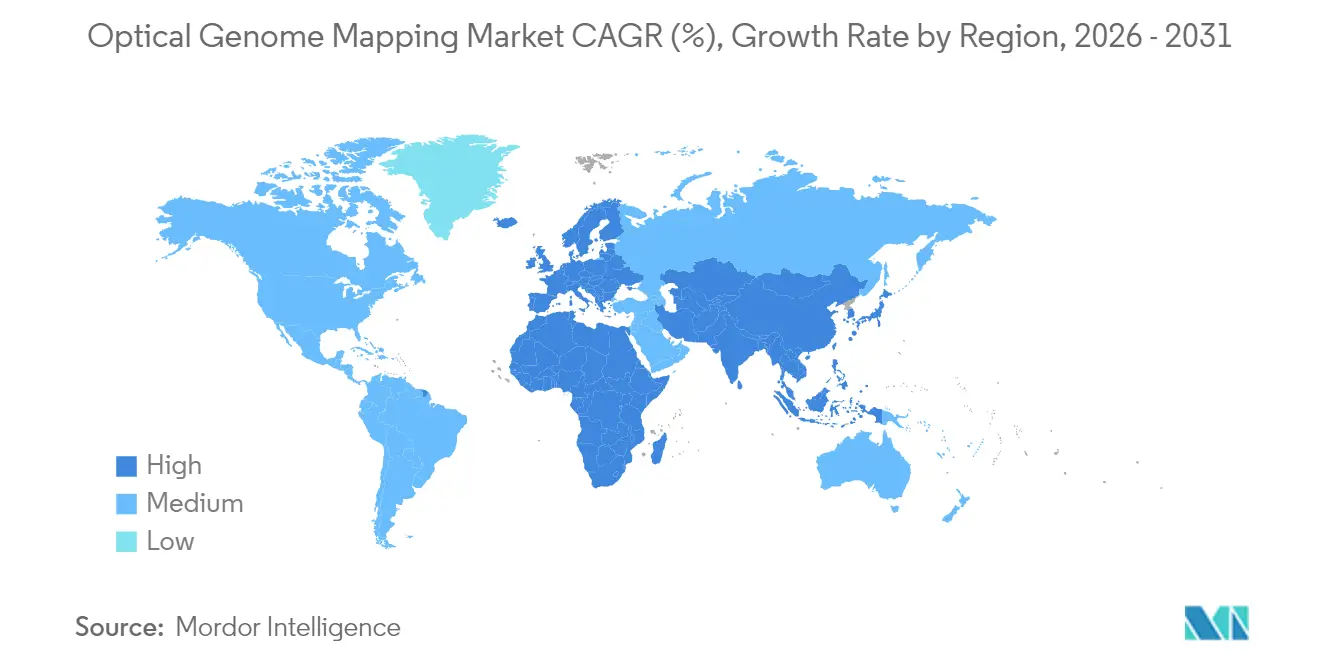

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Optical Genome Mapping Market Analysis by Mordor Intelligence

Optical Genome Mapping Market size in 2026 is estimated at USD 203.4 million, growing from 2025 value of USD 165.75 million with 2031 projections showing USD 566.15 million, growing at 22.72% CAGR over 2026-2031.

This solid trajectory is anchored in the technology’s ability to uncover structural variants that traditional karyotyping and fluorescence in situ hybridization routinely overlook, especially within complex or repetitive genomic regions. Clinicians appreciate that optical genome mapping delivers genome-wide resolution down to 500 base pairs in a single workflow, capturing structural variations, copy-number variants, and chromosomal rearrangements with speed and precision. Instruments constitute the dominant product class, yet escalating consumable usage signals ongoing test-volume expansion as laboratory throughput rises. Oncology remains the largest application area, whereas rare-disease diagnostics are advancing fastest due to the method’s high diagnostic yield in previously unresolved conditions. Robust adoption in biotechnology and pharmaceutical companies co-exists with accelerating uptake in research institutions; the latter reflects mounting academic investment in genomic infrastructure to support precision-medicine programs.

Key Report Takeaways

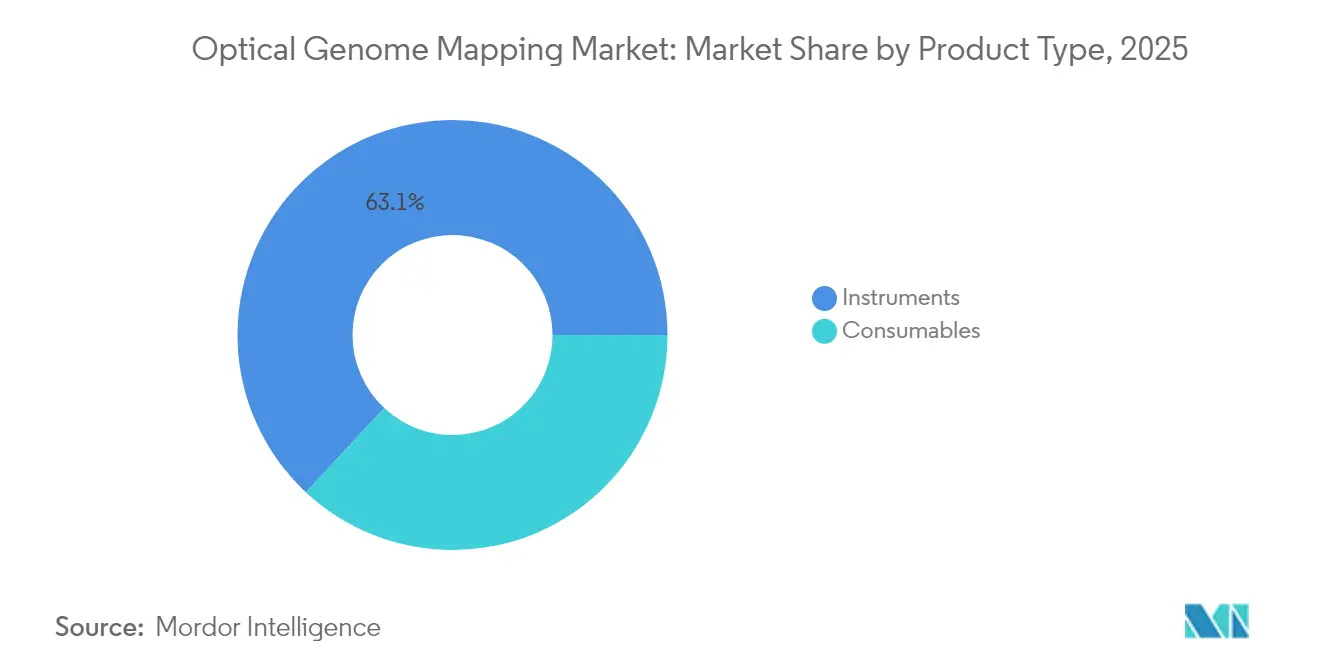

- By product type, instruments led with 63.05% of optical genome mapping market share in 2025; consumables are forecast to grow at a 25.10% CAGR through 2031.

- By application, oncology captured 29.35% revenue share in 2025, while rare-disease and constitutional genetics are projected to expand at a 27.20% CAGR to 2031.

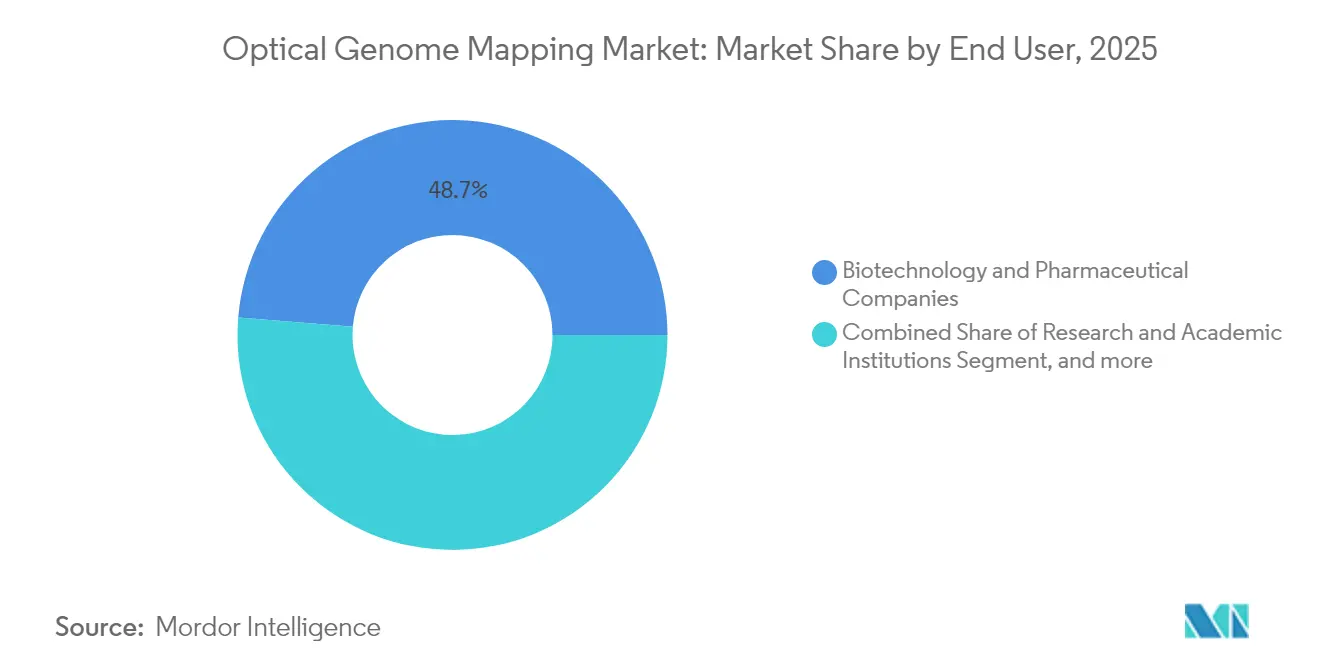

- By end user, biotechnology and pharmaceutical companies held 48.70% share of the optical genome mapping market size in 2025; research and academic institutions record the highest projected CAGR at 23.90% through 2031.

- By geography, North America commanded 41.95% share in 2025, whereas Asia is advancing at a 28.90% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Optical Genome Mapping Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for advanced genomic analysis | +6.2% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Growing prevalence of genetic disorders and cancer | +4.8% | Global, particularly Asia-Pacific emerging markets | Long term (≥ 4 years) |

| Limitations of traditional cytogenetic methods | +3.9% | Global, accelerated in developed markets | Short term (≤ 2 years) |

| Technological advancements in genomics | +3.1% | North America & Europe core, spill-over to Asia | Medium term (2-4 years) |

| Expanding applications in precision medicine | +2.7% | Global, led by North America regulatory framework | Long term (≥ 4 years) |

| Increasing collaborations and investments | +1.8% | Global, concentrated in biotech hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Advanced Genomic Analysis

Health systems acknowledge that legacy cytogenetic techniques can miss up to 40% of clinically relevant structural variants. Optical genome mapping corrects this gap, identifying additional actionable variants in 58% of hematological malignancy cases compared with current standard testing. Laboratories value the single-assay workflow that trims turnaround from weeks to days while boosting diagnostic accuracy. The prospect of Medicare reimbursement under Category I CPT coding underscores financial viability for providers, and the shift toward genomic-first diagnostics in oncology cements sustainable demand growth.

Growing Prevalence of Genetic Disorders and Cancer

Escalating cancer incidence, coupled with recognized genetic heterogeneity, fuels the need for high-resolution structural-variant profiling. Optical genome mapping detects drug-resistance mechanisms invisible to conventional methods, allowing physicians to revise therapies earlier. Rare-disease programs benefit as well; studies show detection of pathogenic variants in 15% of cases that were inconclusive with short-read sequencing.[1]Nature Research, “Optical Genome Mapping in Rare Disease,” nature.comFalling sequencing costs, expanding precision-medicine initiatives, and improved analytics reinforce optical genome mapping’s role across diverse patient cohorts.

Limitations of Traditional Cytogenetic Methods

Standard karyotyping requires dividing cells and offers limited resolution, while fluorescence in situ hybridization interrogates only known targets, leaving balanced translocations and complex rearrangements unnoticed. Optical genome mapping, by analyzing ultra-long DNA molecules without amplification bias, detects events as small as 500 bp across the entire genome.[2]Nature Research, “Optical Genome Mapping in Rare Disease,” nature.com Laboratories replace sequential testing with a single assay, streamlining workflows and reducing cumulative cost.

Technological Advancements in Genomics

Automation and AI-driven analytics now accompany optical genome mapping platforms. Bionano Genomics’ partnership with NVIDIA quadruples data-processing speed, cutting analysis from days to hours.[3]NVIDIA Corporation, “Accelerated Genomic Analysis Collaboration,” nvidia.com Variant-interpretation software such as VIA achieves full reviewer concordance, easing reliance on scarce bioinformatics specialists. These developments lower expertise barriers, enhance throughput, and improve cost-effectiveness, supporting further penetration of the optical genome mapping market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High instrument costs | -2.1% | Global, particularly emerging markets | Short term (≤ 2 years) |

| Requirement for specialized expertise | -1.4% | Global, more pronounced in smaller laboratories | Medium term (2-4 years) |

| Concerns over data interpretation and standardization | -1.2% | Global, critical in clinical diagnostics | Medium term (2-4 years) |

| Regulatory and ethical considerations | -0.8% | North America & Europe primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Instrument Costs

Purchasing a Saphyr or high-throughput Stratys system requires significant capital outlays. Smaller laboratories, particularly in emerging markets, perceive this as a hurdle. Nonetheless, workflow consolidation offsets the burden by lowering per-sample costs and avoiding multiple complementary assays. Leasing and reagent-rental programs plus expanding reimbursement pathways gradually mitigate upfront expense concerns.

Requirement for Specialized Expertise

Comprehensive structural-variant interpretation demands advanced genomic skills beyond traditional cytogenetics curricula. Cloud-based analytics, automated variant calling, and vendor training courses are steadily reducing the expertise gap. As AI-enabled reporting gains traction, optical genome mapping becomes feasible for laboratories of varied size and complexity, supporting sustained adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Consumables Drive Recurring Revenue Growth

The optical genome mapping market size for instruments corresponding to 63.05% of segment revenue in 2025. Consumables, mainly nanochannel array flowcells, recorded the highest momentum and are forecast to climb at a 25.10% CAGR, benefiting from each incremental test run. Flowcell shipments totaled 8,058 units in Q4 2024, indicating healthy utilization across 371 installed systems.

Capital equipment sales hinge on periodic technology cycles. Stratys, launched in January 2024, produces four times the data of earlier systems and processes up to 12 samples concurrently, spurring replacement demand among high-throughput clinical labs. Instrument revenue also accrues from software licenses and maintenance, reinforcing a hybrid model of upfront and recurring streams. The resonance of these dynamics underscores why consumables pace overall growth even as instruments anchor platform stickiness.

By Application: Rare-Disease Diagnostics Emerge as Growth Driver

Oncology delivered 29.35% of optical genome mapping market share in 2025, reflecting entrenched use in hematological malignancies where diagnostic accuracy reaches 98.2% concordance with conventional approaches while unveiling extra clinically actionable variants in 58% of samples. Looking forward, rare-disease and constitutional genetics exhibit the steepest climb at a 27.20% CAGR, buoyed by optical genome mapping’s capacity to identify pathogenic structural variants that short-read sequencing misses.

The optical genome mapping market size for rare-disease diagnostics is projected to double between 2025 and 2030 as family-based studies, neurodevelopmental assessments, and undiagnosed-diseases programs incorporate the technology. Prenatal testing, microbial genomics, and agricultural genomics also expand the total addressable opportunity by extending structural-variant detection to broader research and clinical contexts.

By End User: Research Institutions Accelerate Adoption

Biotechnology and pharmaceutical firms accounted for 48.70% of optical genome mapping market share in 2025, applying the platform to biomarker discovery, target validation, and companion-diagnostic development. Drug developers exploit ultra-long-read data to parse tumor heterogeneity, refine patient stratification, and monitor clonal evolution.

Research and academic institutions represent the fastest-growing cohort at 23.90% CAGR. Government grants, precision-medicine consortia, and philanthropic funding drive purchases as universities establish centralized genomic cores. Clinical laboratories add optical genome mapping to replace sequential cytogenetic arrays, while contract research organizations bundle the technology into multi-omics service portfolios, widening commercial exposure.

Geography Analysis

North America retained leadership in the optical genome mapping market with 41.95% revenue contribution in 2025. Category I CPT codes for hematological malignancy testing and the FDA’s heightened oversight of laboratory-developed tests provide regulatory certainty that favors validated platforms. Academic medical centers and genomic-research enterprises proliferate system placements, and Medicare’s ongoing coverage deliberations could unlock broader hospital adoption.

Asia Pacific is the fastest-growing region, projected at a 28.90% CAGR through 2031. China’s 15-year precision-medicine initiative is sequencing millions of genomes, fostering demand for structural-variant-centric technologies. Japan’s TOP-GEAR program aligns genomic analysis with national cancer-control strategies, and partial insurance coverage for gene-panel testing sets precedent for wider reimbursement. Regional biotechnology clusters collaborate with international vendors to localize manufacturing, training, and support, helping spur adoption beyond tier-one urban centers.

Europe exhibits steady uptake underpinned by public health-care systems, pan-European research consortia, and a mature laboratory network. Latin America and the Middle East are earlier in adoption curves yet show interest through pilot programs and academic partnerships as health-care modernization accelerates.

Competitive Landscape

The optical genome mapping market is moderately consolidated. Bionano Genomics anchors the field with 371 deployed instruments worldwide as of Q4 2024, leveraging a focused R&D roadmap and extensive clinical-validation portfolio. Large genomics vendors such as Illumina, Thermo Fisher Scientific, and Oxford Nanopore Technologies pursue adjacency strategies: they integrate optical genome mapping–style readouts or partner on AI accelerators to expand workflow breadth.

Competitive differentiation revolves around resolution, throughput, automation, and software sophistication. Stratys underscores Bionano’s response to high-volume clinical labs, whereas Illumina’s multi-omics innovations promise complementary read technologies potentially bridging short reads and structural-variant mapping. Thermo Fisher’s acquisition of purification assets illustrates vertical integration aimed at end-to-end sample-to-answer solutions. Start-ups are emerging with cloud-native analytics, streamlined sample prep, and consumption-based pricing, making the optical genome mapping market more accessible to mid-sized laboratories.

Long-term success depends on clinical-utility evidence, seamless bioinformatics, and reimbursement alignment. Vendors that combine automated platforms, AI-guided interpretation, and collaborative research ecosystems are likely to shape market share trajectories through 2030.

Optical Genome Mapping Industry Leaders

Bionano Genomics

OpGen

Nabsys

PerkinElmer, Inc.

Nucleome Informatics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Illumina announced a comprehensive suite of multiomics innovations, including constellation mapped read technology for rare disease detection and a 5-base solution for methylation analysis, with commercialization planned by 2026 to enhance genomic research capabilities and compete with optical genome mapping applications.

- February 2025: Thermo Fisher Scientific announced its acquisition of Solventum's Purification & Filtration business for approximately USD 4.1 billion, expected to enhance bioproduction capabilities and generate USD 125 million in adjusted operating income synergies by year five.

- January 2025: NVIDIA announced partnerships with IQVIA, Illumina, Mayo Clinic, and Arc Institute to advance genomics and drug discovery using AI and accelerated computing, with Illumina utilizing NVIDIA technology for multiomics analysis.

- January 2025: Bionano Genomics reported preliminary Q4 2024 results showing 14% growth in installed base to 371 OGM systems, despite 25% revenue decline due to discontinuation of clinical service products, while achieving commercial release of the Stratys system.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the optical genome mapping market as all dedicated instruments, consumables, workflow-specific software, and associated services that generate high-resolution whole-genome structural-variant maps from ultra-high-molecular-weight DNA across research, clinical, and agricultural settings. According to Mordor Intelligence, revenues are captured at factory gate for new systems and their proprietary reagents.

For clarity, we exclude routine short-read sequencing kits, generic bioinformatics platforms, and revenues from service labs that do not own or operate optical mapping instruments.

Segmentation Overview

- By Product Type

- Instruments

- Consumables

- By Application

- Oncology

- Rare-Disease & Constitutional Genetics

- Prenatal & Reproductive Health

- Microbial & Pathogen Genomics

- Agricultural & Plant Genomics

- By End User

- Biotechnology & Pharmaceutical Companies

- Research & Academic Institutions

- Clinical Diagnostic Laboratories

- Contract Research Organizations

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed laboratory directors, cytogeneticists, and procurement leads across North America, Europe, and Asia Pacific to validate installed-base counts, average selling prices, consumable pull-through ratios, and near-term buying intentions. Follow-up surveys with technology vendors and contract research organizations closed remaining gaps and confirmed learning curve assumptions for consumables.

Desk Research

We began with authoritative public sources such as National Institutes of Health funding tables, European Commission Horizon grant databases, World Health Organization cancer registries, and customs shipment codes covering optical genomic instruments. Company 10-K filings, peer-reviewed articles on PubMed, and insights from the American Society of Human Genetics provided additional context. Subscription assets including D&B Hoovers for company financials and Questel for patent velocity around nanochannel devices helped size peer pipelines. The sources listed illustrate the breadth of secondary inputs, and many other datasets were reviewed to corroborate figures and narrative.

Market-Sizing & Forecasting

A top-down build estimated demand from installed optical genome mapping systems, average runs per instrument, and mean consumables spend. These outputs were cross-checked with selective bottom-up roll-ups from supplier disclosures and channel checks. Key variables include NIH and ERC genomics budgets, annual hematologic oncology sample volumes, system utilization hours, and regional adoption rates within tier-one cytogenetic laboratories. Multivariate regression blended with scenario analysis projects each driver, while ARIMA tests historical uptake trends. The model delivers a market value and a growth rate toward the end of the forecast period. Data voids in emerging regions are bridged through adoption proxies proven in analogous molecular cytogenetics tools.

Data Validation & Update Cycle

Analysts run variance checks against independent series, reconcile anomalies, and escalate outliers for senior review before sign-off. Models refresh annually, with interim updates triggered by material events such as major clinical guideline revisions. A final analyst pass occurs just before release so clients receive the most current view.

Why Mordor's Optical Genome Mapping Baseline Commands Reliability

Published estimates often diverge because providers mix distinct product buckets, apply different currency bases, and refresh at unequal intervals. We find that the way services revenues are bundled or consumable discounts are handled can widen these gaps.

Key gap drivers include the inclusion of generic sequencing consumables by some publishers, optimistic clinical adoption trajectories that overlook regulatory lead times, and linear growth extrapolations from limited 2023 baselines that ignore fresh grant surges already captured in Mordor's scenarios.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 165.75 M (2025) | Mordor Intelligence | - |

| USD 129.30 M (2024) | Global Consultancy A | Narrow geography and static instrument pricing assumptions |

| USD 162.50 M (2024) | Industry Publication B | Counts legacy mapping kits, inflating base volumes |

| USD 160.20 M (2024) | Research Boutique C | Simple CAGR extrapolation without driver validation |

The comparison shows that Mordor's disciplined scope definition, driver-level projections, and yearly refresh cadence provide a balanced baseline that decision-makers can trace to transparent variables and replicate with confidence.

Key Questions Answered in the Report

What is the current size of the optical genome mapping market?

The optical genome mapping market was valued at USD 203.4 million in 2026 and is forecast to reach USD 566.15 million by 2031, growing at a 22.72% CAGR during the forecast period (2026-2031).

Which product segment is expanding fastest?

Consumables are the fastest-growing product segment, advancing at a 25.10% CAGR as laboratories run more tests on the expanding installed base of instruments.

Why are rare-disease diagnostics important for optical genome mapping?

Optical genome mapping identifies pathogenic structural variants that short-read sequencing misses, delivering definitive diagnoses in 15% of previously unresolved rare-disease cases.

Which region shows the highest growth potential?

Asia Pacific leads in growth with a projected 28.90% CAGR through 2031, driven by China’s precision-medicine program and Japan’s TOP-GEAR cancer-genomics initiative.

How does optical genome mapping improve oncology testing?

The technology achieves 98.2% concordance with standard cytogenetic methods while revealing additional actionable variants in 58% of hematological malignancy samples, guiding more precise therapy selection.

What is the main barrier to wider adoption?

High upfront instrument costs remain the primary obstacle, although leasing models, reimbursement progress, and workflow-consolidation savings are steadily lowering this barrier.

Page last updated on: