GCC Labels And Release Liners Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

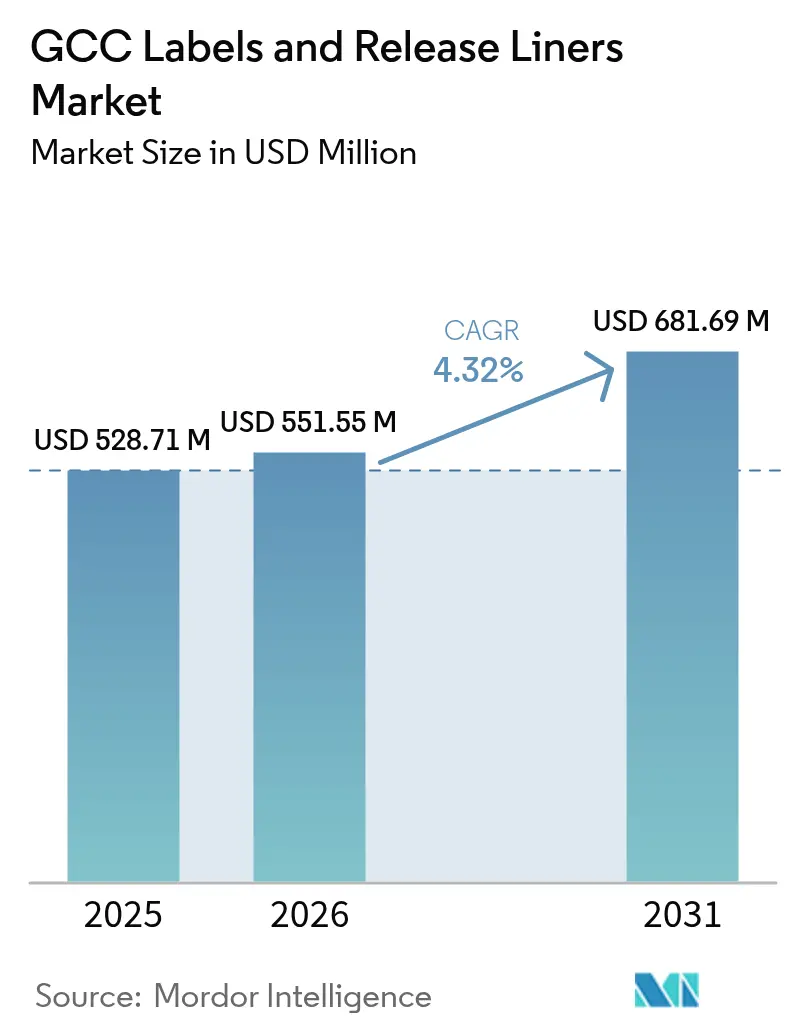

| Base Year Market Size (2025) | USD 528.71 Million |

| Market Size (2026) | USD 551.55 Million |

| Market Size (2031) | USD 681.69 Million |

| Growth Rate (2026 - 2031) | 4.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Labels And Release Liners Market Analysis by Mordor Intelligence

The GCC labels and release liners market size was valued at USD 528.71 million in 2025 and estimated to grow from USD 551.55 million in 2026 to reach USD 681.69 million by 2031, at a CAGR of 4.32% during the forecast period (2026-2031). This expansion aligns with national diversification programs that channel industrial capital into food, beverage, cosmetics, and pharmaceutical lines, all of which require data-rich, multilingual labels. Demand also benefits from fast-growing e-commerce operations that need variable-data shipping labels and from petrochemical investments that secure regional film supply. Technical mandates such as the Gulf health authorities’ 2025 QR-code serialization rules add further volume by increasing the number of labels per unit dose. Against this backdrop, pressure-sensitive constructions remain dominant; however, shrink sleeves, film liners, and digitally printed short runs are posting the fastest gains as converters shift toward premium aesthetics, sustainability, and just-in-time fulfillment. Strategic opportunities, therefore, concentrate on hybrid presses, mono-material films, and turnkey e-labeling platforms that connect QR codes to regulator-hosted instructions.

Key Report Takeaways

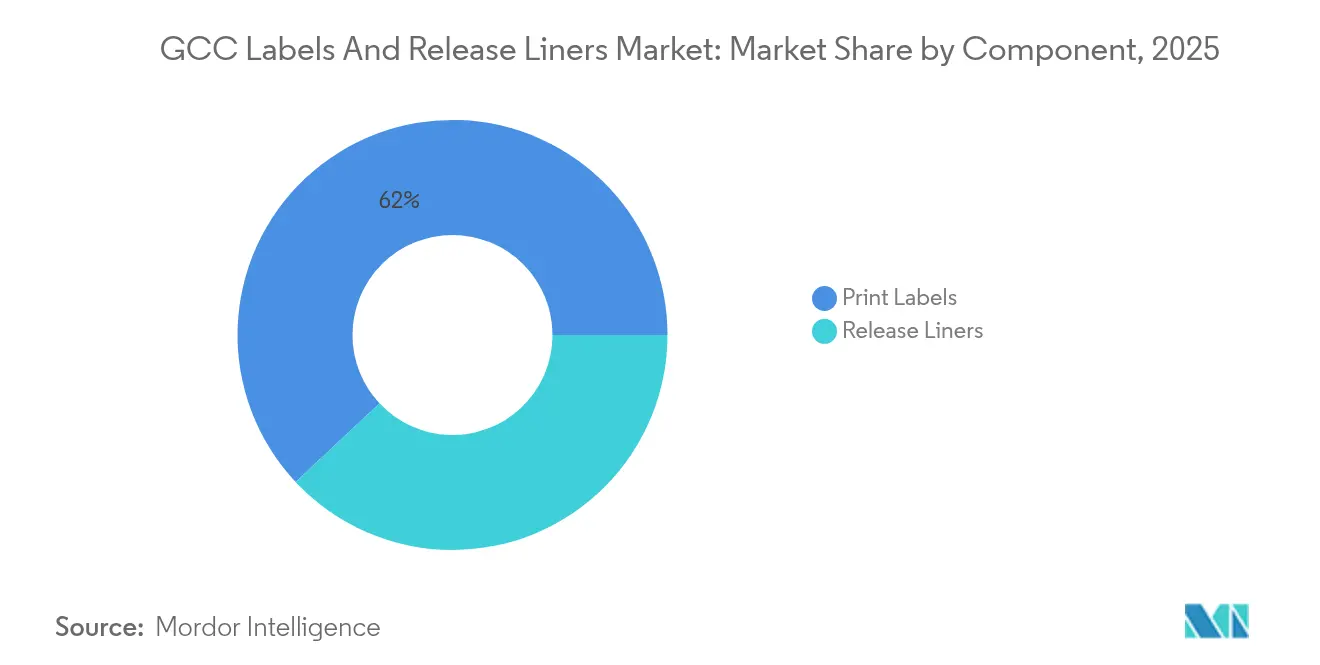

- By component, print labels held 61.98% of the GCC labels and release liners market share in 2025, while release liners are projected to advance at a 5.42% CAGR through 2031.

- By face stock material, paper accounted for 53.92% of the GCC labels and release liners market size in 2025, whereas film liners are expected to expand at a 5.86% CAGR to 2031.

- By print process, flexography led with a 35.21% revenue share in 2025; digital presses are projected to register the highest CAGR at 6.61% through 2031.

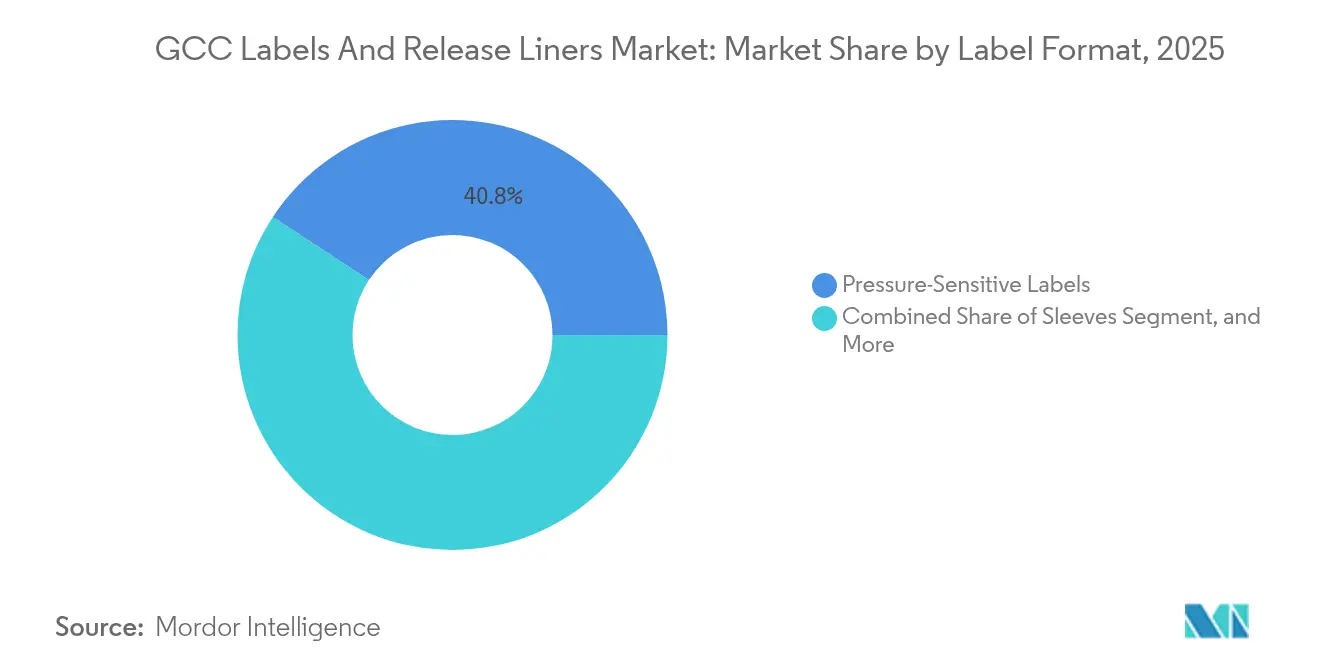

- By label format, pressure-sensitive labels commanded a 40.75% share of the GCC labels and release liners market size in 2025; shrink sleeves are projected to grow at 5.21% annually through 2031.

- By end user, food retained a 28.15% share of the GCC labels and release liners market size in 2025; whereas cosmetics is the fastest-growing segment with a 6.44% CAGR between 2026 and 2031.

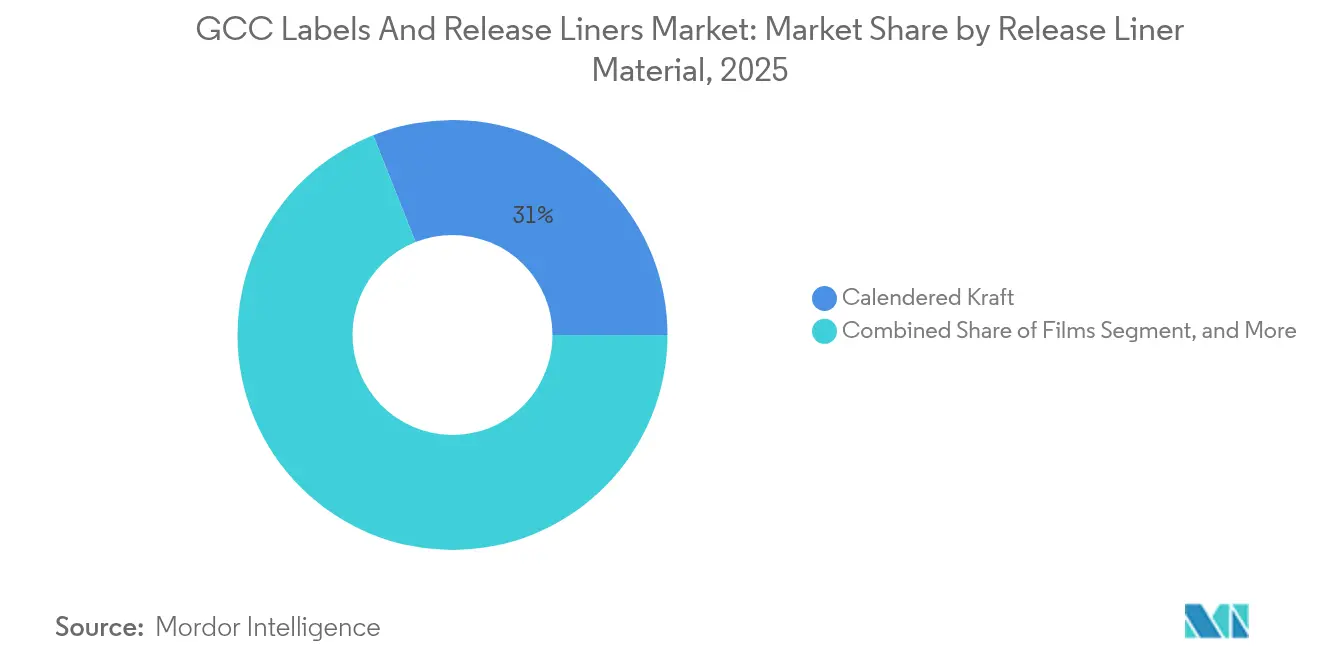

- By release liner material, calendered kraft paper captured a 31.02% share of the GCC labels and release liners market size in 2025; while films are projected to rise at a 5.61% CAGR through 2031.

- By release liner application, labels accounted for 46.21% share of the GCC labels and release liners market size in 2025; medical use cases are projected to record a 6.73% CAGR through 2031.

- By country, Saudi Arabia held 59.97% of the GCC labels and release liners market share in 2025; however, the United Arab Emirates showed the fastest pace at a 6.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Labels And Release Liners Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Growth of Cosmetics, Food and Beverages Sectors | +1.2% | Saudi Arabia, United Arab Emirates, Qatar | Medium term (2-4 years) |

| Expansion of E-Commerce Packaging Demand | +0.9% | United Arab Emirates, Saudi Arabia, Qatar, Bahrain | Short term (≤ 2 years) |

| Rise of Smart Labels for Track-and-Trace | +0.8% | Saudi Arabia, United Arab Emirates | Short term (≤ 2 years) |

| Government Vision-2030 Diversification Initiatives | +1.1% | Saudi Arabia, United Arab Emirates | Long term (≥ 4 years) |

| Surge in Halal-Certified Export Labeling | +0.5% | Saudi Arabia, United Arab Emirates | Medium term (2-4 years) |

| Petrochemical Film Capacity Investments in GCC | +0.7% | Saudi Arabia, United Arab Emirates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of Cosmetics, Food, and Beverages Sectors

Middle East and North Africa beauty sales are on track to reach USD 60 billion by 2025, up from USD 46 billion, which is expected to boost regional demand for premium sleeves, metallic foils, and halal-certified pressure-sensitive labels.[1]PwC Middle East, “MENA Beauty Report,” PWC.COM The Saudi Food and Drug Authority reduced product-registration lead times in 2024, enabling brands such as Asteri to obtain export clearance to 15 markets within six months. Parallel food investments amplify volume: Almarai allocated USD 4.8 billion for new dairy, juice, and bakery lines through 2028, and Nestlé opened a USD 72 million plant in Jeddah in 2025. Dubai Industrial City added AED 350 million (USD 95.3 million) in food-and-beverage capital during 2024, bringing 25 new tenants and millions of square feet under lease. Combined, these expansions ensure dependable throughput for the GCC labels and release liners market, as brands seek multilingual nutrition panels, tamper-evident packaging, and premium shelf appeal.

Expansion of E-Commerce Packaging Demand

Gulf online retail sales are forecast to hit USD 63 billion by 2027, with Saudi Arabia contributing USD 24 billion by 2029.[2]McKinsey and Company, “GCC E-Commerce Growth Forecast,” MCKINSEY.COM E-tailers need durable shipping labels that carry QR codes, order IDs, and personalized messages. Saudi Graphco installed Durst, Xeikon, and Gallus digital presses in 2024, promising a 24-hour turnaround for runs of less than 1,000 units. The United Arab Emirates leverages Al Maktoum International Airport, Jebel Ali Port, and Etihad Rail to consolidate fulfillment, attracting converters that bundle printing, kitting, and customs-compliant labeling under one roof. New customs rules, which expand tariff lines to 13,400 items in 2025, intensify the need for accurate duty declarations on every parcel. These dynamics steer converters toward high-speed digital workflows, reinforcing the growth of the GCC labels and release liners market.

Rise of Smart Labels for Track-and-Trace

Gulf regulators now require QR-coded electronic leaflets for drugs and devices, with the UAE’s Tatmeen platform insisting on unique identifiers for every unit dose.[3]UAE Ministry of Health and Prevention, “Tatmeen Platform,” MOHAP.GOV.AE Converters therefore invest in 2D code verification, secure short-link creation, and high-resolution printing that guarantees 600 dpi readability. RFID use is spreading beyond healthcare: The Landmark Group equipped more than 600 stores with smart tags in 2024, reducing shrinkage and inspiring similar projects in the grocery and apparel sectors. Logistics providers add NFC chips to pallet labels to automate customs clearance, aligning with Saudi Arabia’s goal to rank among the world’s top 25 logistics performers by 2030. These requirements favor film liners that tolerate wide temperature swings and resist moisture, stimulating premium revenue streams within the GCC labels and release liners market.

Government Vision-2030 Diversification Initiatives

Saudi Arabia plans to scale to 36,000 factories by 2035, backed by the USD 100 billion Alat fund for electronics, renewables, and automotive clusters. The UAE’s Make in UAE and Dubai Agenda D33 grant 10-year tax holidays and full foreign ownership, luring over 1,100 tenants to Dubai Industrial City by 2024. Every new facility needs safety labels, asset tags, and supply-chain tracking that conform to GS1 and ISO standards. The Mohammed bin Rashid School of Government noted double-digit improvements in diversification scores for Saudi Arabia and Oman between 2000 and 2022, confirming structural momentum. Converters offering design, print, and compliance services within a single workflow are well-positioned to win long-term contracts, thereby anchoring the growth of the GCC labels and release liners market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Crude-Based Raw Material Prices | -0.6% | Saudi Arabia, United Arab Emirates | Short term (≤ 2 years) |

| Competitive Pressure from Digital Media | -0.3% | United Arab Emirates, Saudi Arabia | Medium term (2-4 years) |

| Import Duties on Adhesives and Chemicals | -0.4% | GCC-wide | Short term (≤ 2 years) |

| Limited Skilled Workforce for Advanced Converting | -0.5% | Saudi Arabia, United Arab Emirates, Qatar | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Crude-Based Raw Material Prices

Saudi Arabia raised petrochemical feedstock prices in 2024, squeezing adhesive and film margins and resulting in a 92.5% profit drop at the National Company for Manufacturing Packaging Materials. Crude oil jumped from USD 70 to USD 90 per barrel during 2024, lifting acrylic adhesive and PET resin costs by up to 20%. Red Sea shipping disruptions added roughly 60% to freight charges and extended transit times by up to 14 days, forcing converters to reassess their global sourcing strategies. Larger players with backward integration, such as Borouge, which will reach 6.6 million tonnes per annum of polymer capacity by 2028, can buffer volatility, but small converters remain exposed. Although anti-dumping duties on Asian film imports may stabilize prices, relief is unlikely before existing inventories clear.

Competitive Pressure from Digital Media

Domino Printing Sciences unveiled a bottle-closure printer in July 2024 that etches QR codes directly onto caps at a rate of 44,000 units per hour, potentially displacing external labels in beverage categories. Consumer electronics brands are embedding NFC chips in cartons to deliver manuals and recycling guides, thereby reducing the need for paper labels. Gulf Print and Pack 2024 showcased AI workflows and direct-to-substrate presses capable of decorating corrugated, metal, and glass substrates, thereby eroding volumes for commodity wet-glue labels. Converters are responding with tamper-evident holograms, temperature-reactive inks, and augmented-reality triggers, but margin pressure persists as some brand owners test labelless packaging.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Release Liners Gain as Medical Serialization Accelerates

Release liners garnered incremental attention in 2025 as pharmaceutical and medical device producers prepared for unit-level serialization. Although print labels represented 61.98% of revenue, liner consumption grew faster because every tamper-evident pharmaceutical label includes a silicone-coated backing. Saudi Arabia’s serialization rules have added millions of blister packs, vials, and syringes to the annual output, each requiring high-grade release liners that can tolerate clean-room handling. Converters with ISO 13485 certification now process 10-15 tonnes of liner per new packaging line, driving steady uptake within the GCC labels and release liners market.

Looking ahead, the shift toward thinner liners and recyclable polypropylene films is set to favor integrated suppliers that control silicone coating, slitting, and die-cutting under one roof. Smaller printers may continue to focus on high-volume food and beverage labels, but margins will lag as commodity prices fluctuate. Strategic investment, therefore, tends to focus on specialty coatings and medical clean-room facilities, where entry barriers are steep, and contract durations are long.

By Face Stock Material: Films Ride Sustainability and Durability Trends

Paper retained a 53.92% share in 2025 due to its printability and cost advantage, while film liners achieved a 5.86% CAGR, driven by their strength in moisture resistance, transparency, and recyclability. SABIC’s TRUCIRCLE resins and Taghleef’s BOPP with recycled content help brand owners meet emerging extended producer responsibility mandates in export markets. Mono-material laminates from Borealis simplify mechanical recycling, a feature prized by the beverage and cosmetics industries seeking circular credentials.

Future demand centers on shrink sleeves, in-mold labels, and logistics tags that are exposed to temperature swings and condensation. Polyethylene films conform to complex bottle shapes in shrink tunnels, while PET films deliver dimensional stability for high-speed die-cutting. The GCC labels and release liners market, therefore, shows a gradual shift away from paper, although paper will remain entrenched in ambient-storage groceries, where tactile appeal and compostable options still resonate with consumers.

By Print Process: Digital Presses Capture Short-Run and Variable-Data Demand

Flexography led with 35.21% revenue in 2025, yet digital presses posted a 6.61% CAGR, propelled by e-commerce, personalization, and mandated QR codes. Saudi Graphco’s Durst and Xeikon lines now turn around orders under 24 hours, shrinking lead times that once discouraged regional fulfillment centers. The latest digital engines run at nearly 40 meters per minute with inline inspection, making them cost-competitive for batches up to 5,000 linear meters.

Gravure holds a niche status for ultra-long shrink-sleeve runs, while offset supports luxury cosmetics that require metallic inks and fine screens. Screen and hot-foil processes serve under 5% of demand, positioning hybrid presses analog color with digital variable heads as the middle-volume solution. As variable-data requirements expand, the digital share of the GCC labels and release liners market is set to climb even faster after 2027.

By Label Format: Sleeves Gain Premium Shelf Presence

Pressure-sensitive formats controlled 40.75% of the value in 2025, due to their application speed and compatibility with legacy filling lines. Shrink sleeves, however, are registering a 5.21% CAGR because beverages and cosmetics value 360-degree graphics and built-in tamper evidence. Pure Ice Cream’s forthcoming Dubai facility highlights this shift, allocating new lines to premium tubs wrapped in full-body sleeves. Wet-glue labels remain the low-cost choice for mass-produced water bottles, but their edge is narrowing as PS adhesives now run at comparable line speeds.

In-mold labeling enables seamless recycling by embedding graphics during the molding process. SABIC has pioneered PP resins that enable the entire container and label to be reintroduced into the polyolefin waste stream, a distinct advantage in the face of looming plastic taxes. Looking forward, converters that master multi-format portfolios will capture growth as brands mix PS, sleeve, and IML solutions across SKU ranges within the GCC labels and release liners market.

By End User Industry: Cosmetics Outpace Food as Fastest-Growing Segment

Food held a 28.15% share in 2025 and continues to produce the largest square-meter volume of labels. Cosmetics, however, is expanding at a rate of 6.44% per year, benefiting from regional beauty spending, export ambitions, and halal certification rules. New cosmetic lines often demand high-definition imagery, tactile varnish, and metallic accents that command premiums over commodity labels. Beverage packaging is enjoying demographic tailwinds, particularly for flavored water and energy drinks that utilize shrink sleeves to stand out on crowded shelves.

Healthcare labels grow steadily thanks to serialization mandates. Avalon Pharma, Acino, and other producers now specify tamper-evident constructions with UV-fluorescent ink and microtext, elevating technical complexity. Industrial end uses such as lubricants, building chemicals, and logistics require solvent-resistant adhesives and durable films, providing a hedge against economic fluctuations in consumer categories.

By Release Liner Material: Films Advance on Silicone-Coating Efficiency

Calendered kraft paper secured a 31.02% share in 2025 due to its low cost and acceptable stiffness in food labels. Film liners, although smaller today, exhibit a 5.61% CAGR as converters utilize thinner gauges that reduce waste and increase press speeds. PET and PP films maintain dimensional stability, enabling precise die-cutting at 200 meters per minute, a must for high-output pharmaceutical lines. Borouge’s agreement to supply 100% recycled polypropylene underscores momentum toward circular alternatives that satisfy multinational sustainability scorecards.

Specialty papers with fluoropolymer coatings or antistatic treatments serve electronics and medical niches where release force tolerance is critical. The investment hurdle for silicone coating on thin films tends to screen out smaller players, intensifying consolidation. As more healthcare and electronics plants start up, films are expected to gain share within the GCC labels and release liners market.

By Release Liner Application: Medical Serialization Drives Fastest Growth

Labels accounted for 46.21% of release-liner tonnage in 2025, reflecting their pervasive use across consumer and industrial products. Medical applications, however, exhibit the fastest growth, at 6.73%, driven by Gulf serialization rules that require the addition of unique identifiers to every blister and vial. Each sterile package often requires a multi-layer label with overt and covert security features, pushing up liner demand.

Tapes find stable demand in construction, automotive, and electronics assembly, where double-sided adhesives bond plastics, metals, and composites. Industrial protective films safeguard glass, metals, and composite panels during fabrication and shipping, a segment likely to grow as new factories emerge under Vision 2030. Graphic films round out demand with vehicle wraps and retail signage that leverage cast-vinyl liners for conformability over complex curves.

Geography Analysis

Saudi Arabia generated 59.97% of GCC labels and release liners revenue in 2025, underpinned by large food and beverage projects and by the National Industrial Development and Logistics Program. Streamlined SFDA approvals help homegrown brands accelerate export, further increasing local print runs. Zahra Al-Waha’s new packaging plant began operations in March 2025, adding domestic capacity even as feedstock price hikes pressure small converters. Logistics corridors at King Abdullah Economic City and the Jeddah land bridge position the Kingdom as a relabeling hub for shipments into Africa and South Asia.

The United Arab Emirates is projected to grow at the fastest rate of 6.58% through 2031. Dubai Industrial City added AED 350 million (USD 95.3 million) of food investments in 2024 and now hosts over 1,100 industrial tenants. Borouge’s polymer expansion to 6.6 million tonnes per annum by 2028 anchors local resin supply, while the Tatmeen platform compels pharmaceutical printers to install verification hardware. Proximity to deep-water ports and freight railroads allows for seamless multimodal logistics, attracting e-commerce packaging clients seeking 24-hour service.

Qatar, Bahrain, Oman, and Kuwait form the remaining slice of market value. Qatar leverages tourism and event-driven demand, while Oman’s Madayn network supports flexible packaging ventures, and Bahrain plans to introduce QR-coded e-PILs by 2025. The region’s new 12-digit customs codes add complexity, benefiting converters who bundle duty declarations with printed packaging. Collectively, smaller Gulf states create niche opportunities focused on halal certification, specialty exports, and cold-chain logistics, all of which rely on compliant labeling.

Competitive Landscape

Multinationals, including Avery Dennison, CCL Industries, UPM Raflatac, 3M, and Brady, anchor the supply chain with adhesives, films, and label stock. Regional converters, such as Sigma Middle East Labels, RAK Labels, and Lawaseq, complement the ecosystem with short lead-time production. PwC logged 475 Middle East mergers and acquisitions in 2024, including five deals above USD 1 billion, signaling a persistent appetite for scale despite the global slowdown. Borouge’s backward integration exemplifies a vertical strategy that secures polymer feedstock and establishes a cost baseline.

Equipment manufacturers are also expanding their regional presence. Rotocon appointed ITM as its GCC distributor in March 2025, and press OEMs opened service hubs in Dubai and Riyadh to cut downtime for digital fleets. Digital disruptors like Saudi Graphco leverage late-stage investments to promise one-day delivery, pulling share from traditional flexo shops. Meanwhile, Domino’s cap printer threatens label volumes in beverages if Gulf bottlers adopt labelless designs.

Quality and compliance now separate leaders from followers. Fewer than 30% of converters hold both ISO 14001 and FSSC 22000 certifications, an opening for well-capitalized entrants. Niche providers that master hybrid printing, recyclable mono-material films, and e-labeling ecosystems can capture high-margin orders, while commodity players face continuous price pressure as resin volatility and labelless technologies converge.

GCC Labels And Release Liners Industry Leaders

Avery Dennison Corporation

Taghleef Industries LLC

3M Company

UPM Raflatac Oy

Brady Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Zahra Al-Waha Trading Company began commercial production at its new printing and packaging facility, completing a multi-year capacity expansion focused on higher-margin label applications.

- March 2025: Rotocon named ITM as its exclusive GCC distribution partner, expanding regional access to the company’s label-converting and finishing equipment portfolio.

- February 2025: Dubai Industrial City confirmed more than AED 350 million (USD 95.3 million) in 2024 food-and-beverage investments and announced additional infrastructure upgrades to support on-site label and packaging converters.

- January 2025: The GCC Integrated Customs Tariff entered into force, introducing 12-digit harmonized codes and expanding tariff lines to 13,400, increasing demand for duty-specific variable-data labels across cross-border trade.

GCC Labels And Release Liners Market Report Scope

The GCC labels and release liners market refers to the industry focused on the production, distribution, and application of labels and release liners across various sectors within the Gulf Cooperation Council (GCC) region. Labels are used for branding, information display, and product identification, while release liners serve as backing materials that facilitate the handling and application of adhesive products.

The GCC labels and release liners market report is segmented by Component (Print Labels, Release Liners), Face Stock Material (Paper, Film Liner, Other Face Stock Materials), Print Process (Offset Lithography, Gravure, Flexography, Digital, Other Print Processes), Label Format (Wet-Glue Labels, Pressure-Sensitive Labels, In-Mold Labels, Sleeves, Other Label Formats), End User Industry (Food, Beverage, Healthcare, Cosmetics, Household, Industrial, Other End User Industries), Release Liner Material (Calendered Kraft, Clay-Coated Paper, Polyolefin-Coated Paper, Films, Other Release Liner Materials), Release Liner Application (Labels, Tapes, Medical, Industrial, Graphic Films/Signage, Other Release Liner Application), and Geography (United Arab Emirates, Saudi Arabia, Qatar, Rest of GCC). The Market Forecasts are Provided in Terms of Value (USD).

| Print Labels |

| Release Liners |

| Paper | |

| Film liner | Biaxially Oriented Polyethylene Terephthalate (BOPP) |

| Polyethylene Terephthalate (PET) | |

| Polyethylene (PE) | |

| Other Face Stock Materials |

| Offset Lithography |

| Gravure |

| Flexography |

| Digital |

| Other Print Processes |

| Wet-Glue Labels |

| Pressure-Sensitive Labels |

| In-Mold Labels |

| Sleeves |

| Other Label Formats |

| Food |

| Beverage |

| Healthcare |

| Cosmetics |

| Household |

| Industrial |

| Other End User Industries |

| Calendered Kraft |

| Clay-Coated Paper |

| Polyolefin-Coated Paper |

| Films |

| Other Release Liner Materials |

| Labels |

| Tapes |

| Medical |

| Industrial |

| Graphic Films/Signage |

| Other Release Liner Application |

| United Arab Emirates |

| Saudi Arabia |

| Qatar |

| Rest of GCC |

| By Component | Print Labels | |

| Release Liners | ||

| By Face Stock Material | Paper | |

| Film liner | Biaxially Oriented Polyethylene Terephthalate (BOPP) | |

| Polyethylene Terephthalate (PET) | ||

| Polyethylene (PE) | ||

| Other Face Stock Materials | ||

| By Print Process | Offset Lithography | |

| Gravure | ||

| Flexography | ||

| Digital | ||

| Other Print Processes | ||

| By Label Format | Wet-Glue Labels | |

| Pressure-Sensitive Labels | ||

| In-Mold Labels | ||

| Sleeves | ||

| Other Label Formats | ||

| By End User Industry | Food | |

| Beverage | ||

| Healthcare | ||

| Cosmetics | ||

| Household | ||

| Industrial | ||

| Other End User Industries | ||

| By Release Liner Material | Calendered Kraft | |

| Clay-Coated Paper | ||

| Polyolefin-Coated Paper | ||

| Films | ||

| Other Release Liner Materials | ||

| By Release Liner Application | Labels | |

| Tapes | ||

| Medical | ||

| Industrial | ||

| Graphic Films/Signage | ||

| Other Release Liner Application | ||

| By Country | United Arab Emirates | |

| Saudi Arabia | ||

| Qatar | ||

| Rest of GCC | ||

Key Questions Answered in the Report

What is the current value of the GCC labels and release liners market?

The market is valued at USD 551.55 million in 2026 and is forecast to reach USD 681.69 million by 2031.

Which segment shows the fastest growth in label formats?

Shrink sleeves grow at 5.21% annually as beverage and cosmetics brands seek 360-degree graphics and tamper evidence.

Why are digital printing presses gaining share in the GCC?

E-commerce and serialization mandates require short runs and variable data, enabling digital presses to achieve 6.61% CAGR through 2031.

How does Saudi Arabia influence regional demand?

Saudi Arabia holds 59.97% of revenue, driven by large food, beverage, and industrial investments under Vision 2030.

What material trend supports sustainability goals?

Film liners made from recyclable polypropylene and PET are expanding at 5.86% CAGR, helped by local resin supply from Borouge and SABIC.

Which driver most boosts market expansion?

Diversification initiatives under Saudi Vision 2030 and the UAE’s Make in UAE program add factories that need compliant industrial and consumer labels.

Page last updated on: