Gasoline Direct Injection Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

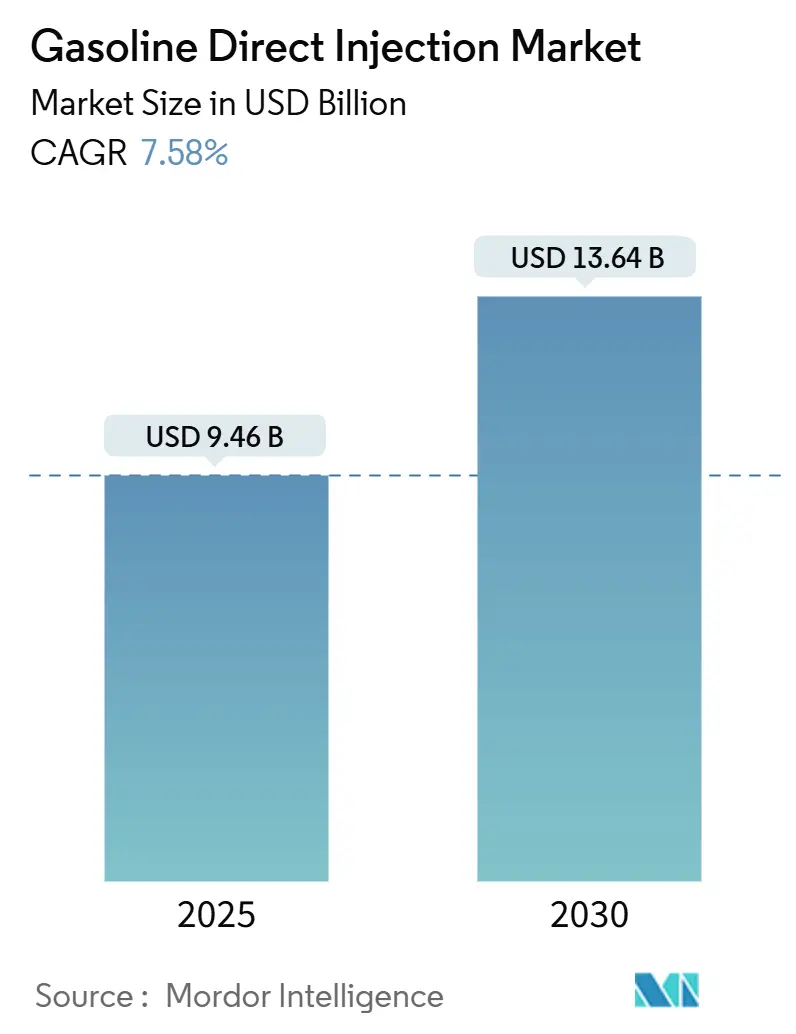

| Market Size (2025) | USD 9.46 Billion |

| Market Size (2030) | USD 13.64 Billion |

| Growth Rate (2025 - 2030) | 7.58% CAGR |

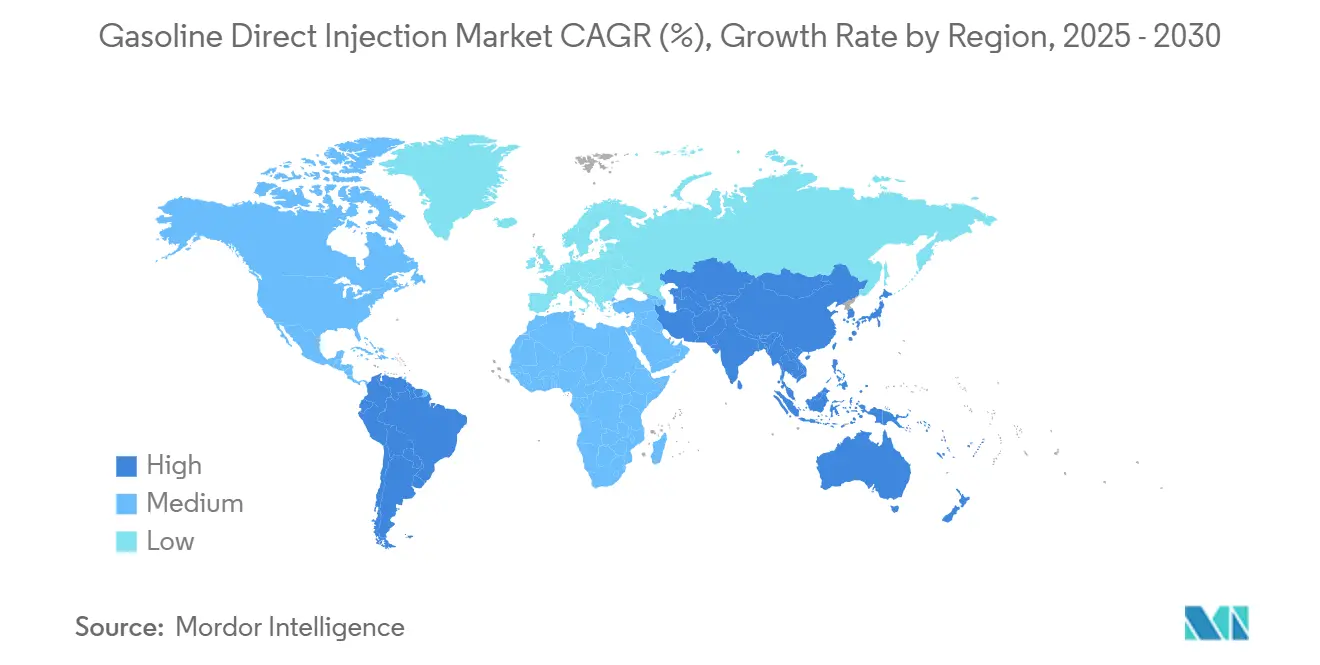

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gasoline Direct Injection Market Analysis by Mordor Intelligence

The Gasoline Direct Injection Market size is estimated at USD 9.46 billion in 2025, and is expected to reach USD 13.64 billion by 2030, at a CAGR of 7.58% during the forecast period (2025-2030). Regulatory pressure remains the single-largest catalyst, as Euro 7, CN7, and BS6 standards compel automakers to adopt high-pressure systems that curb particulate numbers while preserving power through engine downsizing. Continuous innovation in piezo injectors and pressure-sensor integration reinforces this trajectory by improving spray atomization and combustion stability. Asia Pacific’s production scale, led by China’s massive output in 2024, underpins cost competitiveness, accelerating GDI penetration even as regional electrification advances. Meanwhile, SUVs’ popularity challenges extreme downsizing, prompting OEMs to pair larger displacement GDI engines with hybrid modules for balanced performance and emissions compliance. Competitive intensity is high as Bosch, Continental, and DENSO race to embed edge-computing ECUs that enable over-the-air fuel-mapping updates, extending system life-cycle value.

Key Report Takeaways

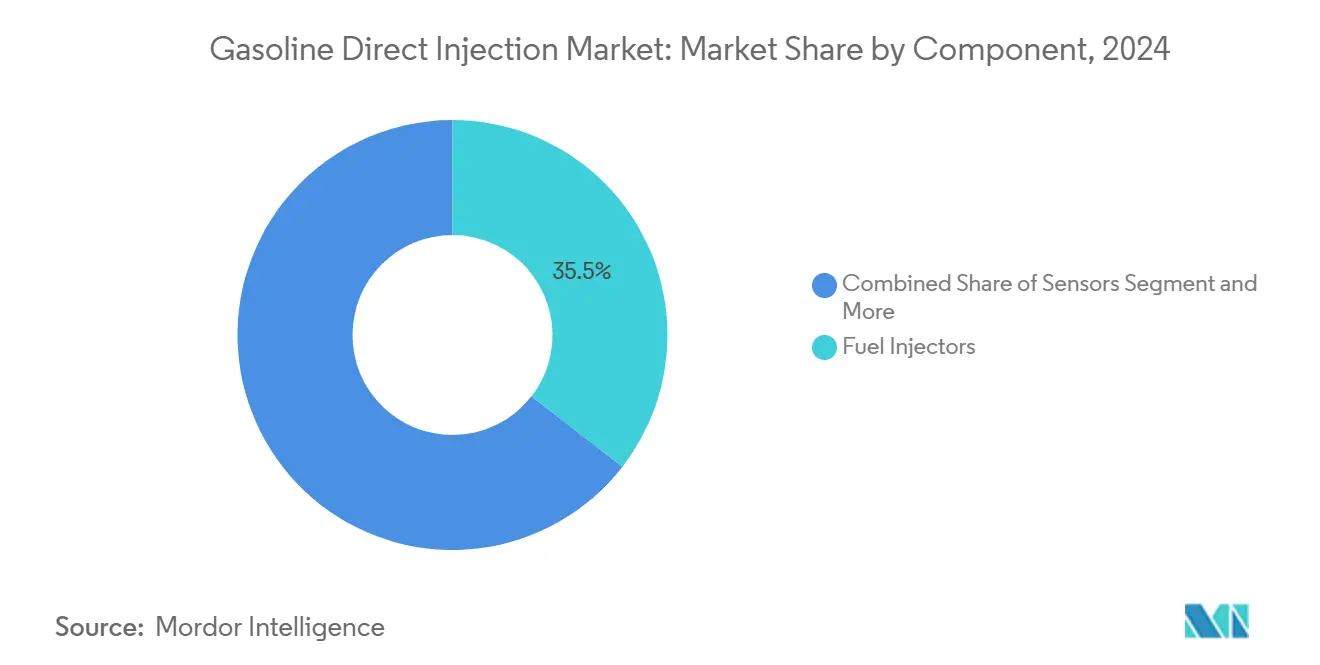

- By component, fuel injectors led with 35.46% of the gasoline direct injection market share in 2024, whereas sensors recorded the fastest 7.61% CAGR through 2030.

- By engine type, inline-4 configurations captured 63.24% of the gasoline direct injection market share in 2024, while inline-3 engines are forecast to grow at a 7.63% CAGR to 2030.

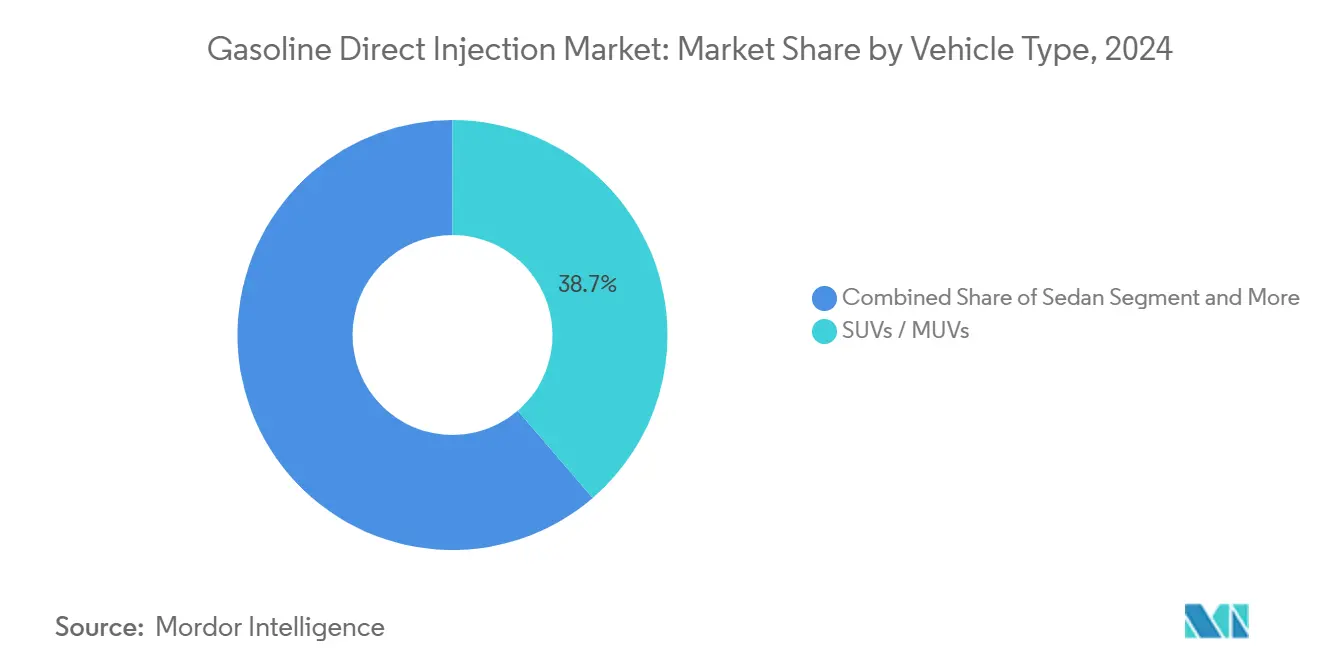

- By vehicle type, SUVs & MUVs commanded 38.71% of the gasoline direct injection market share in 2024 and are advancing at a 7.59% CAGR through 2030.

- By sales channel, OEMs retained 77.63% of the gasoline direct injection market share in 2024, yet the aftermarket is poised for a 7.65% CAGR on rising maintenance demand.

- By region, Asia Pacific held a 38.23% of the gasoline direct injection market share in 2024 and is projected to post a 7.66% CAGR to 2030.

Global Gasoline Direct Injection Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Emission | +2.1% | Global, with EU and China leading | Medium term (2-4 years) |

| OEM Engine Downsizing | +1.8% | North America and EU, expanding to Asia Pacific | Long term (≥ 4 years) |

| Growing Gasoline-Vehicle Production | +1.5% | Asia Pacific core, spill-over to MEA | Short term (≤ 2 years) |

| Integration Of GDI | +1.2% | Global, with early adoption in Japan and EU | Medium term (2-4 years) |

| High-Pressure Injection Systems | +0.7% | Global, technology-driven adoption | Long term (≥ 4 years) |

| Edge-Computing ECUs | +0.3% | North America and EU premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Emission & Fuel-Economy Standards

New particulate-number thresholds PN10 in Euro 7 and similar CN7 clauses force OEMs to redesign combustion chambers, elevate fuel pressures beyond 350 bar, and adopt gasoline particulate filters[1]“Proposal for Euro 7 Standards,” European Commission, europa.EU . Sulfur reductions from 50 ppm to 10 ppm in BS6 fuel enable cleaner injection but mandate onboard diagnostics that heighten electronic complexity. These policies accelerate gasoline direct injection market adoption across all displacement classes and create spill-over demand for pressure sensors, high-strength rails, and software calibration services.

OEM Engine Downsizing & Turbocharging

Due to millisecond-level injection timing accuracy, turbocharged inline-3 and inline-4 engines match or exceed legacy V6 power. Kia’s 2.5-liter T-GDI unit targets a minimal thermal-efficiency gain and one-tenth power lift, illustrating how direct injection supports higher boost without knock. BorgWarner’s electrically actuated wastegates deliver real-time boost control that synchronizes with injector pulses, allowing downsized engines to meet U.S. CAFE targets without sacrificing drivability.

Growing Gasoline-Vehicle Production in Asia Pacific

China produced over 31 million vehicles in 2024, even with a two-fifths NEV penetration, keeping absolute internal combustion output vast and sustaining economies of scale for GDI components. Indian BS6 adoption spurred migration from multi-point to direct injection to meet a quarter NOx cut, while China’s two-fifths export growth spreads Asia Pacific-made injectors worldwide. Domestic champions BYD and Geely hold three-fifths market share at home, catalyzing localized supply chains that trim delivered costs by one-tenth versus imports.

Integration of GDI in Hybrid Powertrains

Toyota’s D-4S engines pair port and direct injection to curb particulate matter by more than half while achieving two-fifths thermal efficiency, proving that GDI complements electric boost[2]“Dynamic Force Engines Technical Guide,” Toyota Motor Corporation, Toyota. Global. Variable compression ratio concepts further raise efficiency to one-fourth over WLTC cycles. Frequent start–stop events in hybrids escalate injector and pump duty cycles, driving demand for durable piezo stacks and self-learning ECUs that recalibrate on the fly.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Electrification | -1.9% | Global, with China and EU leading | Medium term (2-4 years) |

| High Cost | -1.1% | Global, particularly price-sensitive markets | Short term (≤ 2 years) |

| Intake-Valve Carbon Build-Up Warranty Risk | -0.8% | Global, affecting aftermarket demand | Long term (≥ 4 years) |

| Future PN Regulations | -0.5% | EU and regions following Euro standards | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Electrification of Passenger Vehicles

China’s NEV share hit close to half in 2024, buoyed by subsidies up to USD 2,800 per unit, redirecting OEM capital toward battery programs and constraining GDI R&D budgets. Yet combustion engines persist in commercial fleets and price-sensitive segments, tempering the negative impact. Overcapacity plants running at half utilization pressures tier-1s to consolidate or diversify into hybrid-oriented fuel modules.

High Cost & Maintenance Complexity

Piezo injectors cost multiples of electromagnetic designs and require micron-level tolerances. High-pressure pumps exceeding 2,000 psi demand exotic alloys, increasing the bill of materials by minimal relative to port fuel systems. Specialized diagnostic tools and technician training raise total ownership costs, slowing adoption in emerging economies where fuel savings alone may not offset service expenses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Integrated Precision Redefines Performance

Fuel injectors retained a 35.46% of the gasoline direct injection market share in 2024, reflecting their role as gatekeepers of combustion quality. The gasoline direct injection market size for injectors is projected to expand as OEMs raise rail pressures to 350 bar for Euro 7 compliance. Continental’s 40 millionth piezo injector showcases how direct-drive architectures slash response lag, enabling seven-shot strategies that cut soot precursors by one-fifths. Sensors are poised for a 7.61% CAGR through 2030, driven by the need for on-board diagnostics that capture in-cylinder pressure waves and rail-pressure oscillations.

ECUs integrate adaptive algorithms, while high-pressure pumps and rails employ surface-hardened steels to withstand fatigue at 3,000 psi. Bosch’s closed-loop rail solutions maintain ±1 bar stability even during transient load spikes. DENSO’s i-ART platform embeds microprocessors into injector bodies, producing cylinder-specific trim data every combustion cycle.

By Engine Type: Downsizing Spurs Three-Cylinder Momentum

Inline-4 engines held 63.24% of the gasoline direct injection market share in 2024, underlining their ubiquity across compact and midsize vehicles worldwide. The gasoline direct injection market size tied to I4 blocks remains resilient because of balanced cost-to-power ratios. Nevertheless, inline-3 engines lead growth with a 7.63% CAGR, as turbocharging and advanced injection strategies unlock 140 hp from sub-1.5 liter displacements, exemplified by Hyundai’s 1.4 T-GDI Kappa engine.

V6 and V8 units persist in performance and luxury niches, exploiting GDI-enabled stratified charge at light loads for efficiency gains while delivering top-end power. Early gasoline compression-ignition prototypes demonstrate brake thermal efficiencies over two-fifths, indicating further headroom for large-bore architectures. The shift toward modular platforms allows OEMs to deploy ordinary injector families from I3 through V8, enhancing scale economies.

By Vehicle Type: SUV Demand Reshapes Calibration Priorities

SUVs & MUVs contributed 38.71% of the gasoline direct injection market share in 2024 and will outpace the gasoline direct injection market at a 7.59% CAGR to 2030. These heavier platforms require torque-rich calibrations that blend larger displacement GDI engines with mild-hybrid assistance. Kia’s new 2.5-liter T-GDI aims to raise power by 12% without compromising fuel economy, catering to midsize SUVs that dominate global showrooms.

Sedans and hatchbacks still benefit the most from downsizing, enabling OEMs to reach fleet CO₂ targets with fewer cylinders. Pickup trucks and vans adopt GDI at a measured pace, constrained by durability expectations and higher upfront costs. Nevertheless, BorgWarner’s renewed turbo contracts for light trucks suggest continued investment in gasoline powertrains for North American utility segments.

By Sales Channel: Service Complexity Fuels Aftermarket Upside

OEM installations comprised 77.63% of the gasoline direct injection market share in 2024, underscoring the necessity of factory-level calibration and validation. The gasoline direct injection market size attributable to OEMs remains sizable, yet the aftermarket shows a 7.65% CAGR as fleets age. High-pressure seals and particulate filters require replacements that independent workshops increasingly offer.

Valvoline’s nationwide GDI carbon-clean program exemplifies aftermarket innovation. For vehicles operating in dusty environments, intervals are recommended as early as 8,000 km. Tooling specialists such as ASNU supply injector-bench rigs capable of 3,000 psi pulsing, broadening service coverage. The shift from remanufactured to new components reflects the micro-level tolerances that preclude traditional rebuild methods.

Geography Analysis

Asia Pacific’s 38.23% of the gasoline direct injection market share in 2024 underscores its dual dominance as the most significant production hub and fastest-growing consumer arena. Even with two-fifths NEV penetration, China’s 31 million-unit output creates an immense installed base that secures volume contracts for regional injector and pump makers. Exports are climbing exponentially, extending Asia Pacific’s supply influence into Latin America and Eastern Europe, anchoring a 7.66% CAGR outlook through 2030.

North America leans on gasoline direct injection market technologies to balance consumer appetite for SUVs and trucks with fuel-economy rules. Tier 3 standards emphasize particulate mass rather than number, shaping calibration strategies around soot mass reduction without adopting particulate filters universally. BorgWarner’s long-term turbocharger extensions validate an enduring combustion-engine roadmap past 2028.

Europe’s leadership in PN10 legislation forces universal gasoline particulate filter adoption, elevating system costs yet positioning regional suppliers at the cutting edge of sensor integration and software diagnostics. Continental’s piezo injector milestone from its German plant demonstrates manufacturing depth that undergirds export competitiveness. Emerging regions in South America, the Middle East, and Africa integrate GDI as global OEMs transplant compliant platforms, with adoption rates linked to fuel quality upgrades and fiscal incentives for lower CO₂ vehicles.

Competitive Landscape

The gasoline direct injection market features a moderately concentrated tier-1 ecosystem. Bosch anchors the field with end-to-end solutions, integrating pumps, rails, injectors, and controllers under a single calibration suite. Continental leverages manufacturing scale, 40 million piezo injectors produced to supply legacy and next-generation direct-drive units that remove hydraulic damping for 90 µs needle responses. DENSO differentiates with i-ART closed-loop injectors that self-adjust every combustion event, enabling tighter emissions conformity without additional ECU cycles[3]“i-ART Fuel Injection System Overview,” DENSO Corporation, denso.com .

Emerging competition centers on advanced sensor modules and over-the-air update architectures. Traditional mechanical firms partner with semiconductor specialists to embed edge AI that forecasts combustion anomalies, reducing warranty risks.

Aftermarket service innovation adds another competitive axis: Valvoline’s national cleaning network and The Aeromotive Group’s acquisition of VaporWorx expand recurring-revenue pools by addressing maintenance pain points inherent to high-pressure fuel systems. Euro 7 anti-tampering clauses elevate software security to tier-1 differentiators, rewarding suppliers with robust cyber-defense frameworks.

Gasoline Direct Injection Industry Leaders

Robert Bosch GmbH

Denso Corporation

Continental AG

Aptiv PLC

Magneti Marelli S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Kia unveiled a 2.5-liter turbocharged T-GDI engine targeting a 5% thermal efficiency gain and 12% power increase. It is slated for hybrids, ICE models, and range-extender generators.

- February 2025: BorgWarner extended wastegate turbocharger contracts with a major North American OEM through 2028, incorporating electrically actuated systems for midsized gasoline engines.

- February 2025: The Aeromotive Group acquired VaporWorx to deepen its aftermarket fuel-delivery portfolio with electronic fuel-control systems, retaining founder Carl Casanova as engineering director.

Global Gasoline Direct Injection Market Report Scope

| Fuel Injectors |

| Engine Control Units (ECUs) |

| Sensors |

| Fuel Pumps |

| Fuel Rails |

| Inline-3 (I3) |

| Inline-4 (I4) |

| V6 |

| V8 |

| Hatchback |

| Sedan |

| SUVs/MUVs |

| Van |

| Pick-up Truck |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Component | Fuel Injectors | |

| Engine Control Units (ECUs) | ||

| Sensors | ||

| Fuel Pumps | ||

| Fuel Rails | ||

| By Engine Type | Inline-3 (I3) | |

| Inline-4 (I4) | ||

| V6 | ||

| V8 | ||

| By Vehicle Type | Hatchback | |

| Sedan | ||

| SUVs/MUVs | ||

| Van | ||

| Pick-up Truck | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the gasoline direct injection market in 2025?

The gasoline direct injection market size is USD 9.46 billion in 2025, projected to reach USD 13.64 billion by 2030.

Which region dominates demand for GDI components?

Asia Pacific leads with 38.23% share in 2024, supported by China’s 31 million-vehicle production and a 7.66% regional CAGR outlook.

What is the fastest-growing engine configuration using GDI?

Inline-3 engines show the highest growth, advancing at a 7.63% CAGR as turbocharging and direct injection enable aggressive downsizing.

Why are sensors the fastest-growing GDI component category?

Sensors post a 7.61% CAGR because Euro 7 and similar rules require precise in-cylinder pressure and rail-pressure monitoring to manage particulate emissions.

How does electrification affect the future of GDI?

Rapid EV adoption trims GDI growth by −1.9 percentage points on the projected CAGR, yet hybrid powertrains still rely on advanced direct-injection engines for efficiency gains.

Page last updated on: