Automotive Fuel Tank Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 17.43 Billion |

| Market Size (2031) | USD 21.32 Billion |

| Growth Rate (2026 - 2031) | 4.11% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Fuel Tank Market Analysis by Mordor Intelligence

The automotive fuel tank market size is valued at USD 17.43 billion in 2026 and is projected to reach USD 21.32 billion by 2031, growing at a 4.11% CAGR from 2026 to 2031. The steady output of internal-combustion and hybrid vehicles in the Asia-Pacific, South America, and the Middle East continues to anchor global demand, even as battery-electric penetration rises in China and Europe. Tier-1 suppliers are transitioning from steel to multi-layer HDPE systems and investing in composite Type IV cylinders for hydrogen trucks, striking a balance between regulatory pressure and material innovation. Tightening Euro 7 and LEV III evaporative-emission limits add USD 15-25 per unit but unlock compliance credits worth multiples of that cost, spurring rapid adoption of barrier-layer technologies. At the same time, raw material volatility has compressed margins, prompting suppliers to shift toward low-cost molding hubs and vertical integration.

Key Report Takeaways

- By capacity, the 45 to 70 liter segment commanded a 44.72% share of the automotive fuel tank market in 2025; tanks exceeding 70 liters are projected to rise at an 11.68% CAGR through 2031.

- By material type, plastic tanks led with 43.15% share of the automotive fuel tank market size in 2025; composite cylinders are forecast to expand at a 10.67% CAGR to 2031.

- By vehicle type, passenger cars held a 68.47% share of the automotive fuel tank market size in 2025, while medium- and heavy-commercial vehicles are expected to advance at a 12.63% CAGR through 2031.

- By fuel type, gasoline systems accounted for 67.69% of the automotive fuel tank market share in 2025; however, hydrogen tanks are projected to grow at a 16.42% CAGR through 2031.

- By geography, the Asia-Pacific region captured 53.88% of the automotive fuel tank market share in 2025. In contrast, the Middle East and Africa region is set to record the fastest growth, with a 10.47% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Fuel Tank Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweight Plastic Tanks For CO₂ Compliance | +1.2% | Global, with EU and North America leading adoption | Medium term (2-4 years) |

| ICE and Hybrid Production Recovery | +0.8% | Asia-Pacific core, spill-over to North America and Europe | Short term (≤ 2 years) |

| Stricter Euro 7 Regulations | +0.7% | North America and EU, with regulatory spillover to emerging markets | Long term (≥ 4 years) |

| Flex-fuel Roll-Outs | +0.5% | North America, Brazil, with selective adoption in Asia-Pacific | Medium term (2-4 years) |

| High-Pressure Composite tanks for Fuel-Cell Trucks | +0.6% | EU and North America, early adoption in Japan and South Korea | Long term (≥ 4 years) |

| Off-Road and Defense Demand | +0.4% | Global, with concentrated demand in North America and Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lightweight Plastic Tanks Drive CO₂ Compliance

OEMs are transitioning from steel to multi-layer HDPE tanks, which weigh 30-40% less, resulting in a 3-5 kg reduction per passenger car and a 1% improvement in combined-cycle efficiency. Co-extruded EVOH barriers are now integrated directly into HDPE substrates, cutting cycle time by 12-15% and becoming a baseline requirement in Europe and North America. Fleet-wide CO₂ penalties reached EUR 95 per gram per kilometer in 2025, making barrier-equipped tanks a cost-effective compliance lever. Suppliers lacking in-house barrier capability are increasingly being excluded from OEM sourcing panels, underscoring the strategic need to co-locate extrusion lines near final assembly plants. This driver supports sustained demand in the automotive fuel tank market across regulated regions.

ICE and Hybrid Production Recovery Fuels Demand

Global ICE and hybrid production rebounded in 2025, stabilizing near pre-2020 levels despite gains in BEVs. Hybrid vehicles dominate markets with sparse charging infrastructure, notably Southeast Asia and Latin America, sustaining demand for 35-50 liter barrier tanks. Suppliers with Asia-Pacific manufacturing hubs benefit from this diversified volume, whereas those in Western Europe face sharper declines. The resiliency of hybrid output underpins medium-term growth for the automotive fuel tank market.

Euro 7 Regulations Tighten Evaporative Standards

Euro 7 standards[1]"Fact sheet #6 – Euro 7: Realistic or unrealistic timings?" ACEA, acea.auto. , effective September 2027, cut permissible evaporative emissions to 0.05 g per test, a 60% tightening from Euro 6d, while U.S. LEV III[2]"86.1813-17 Evaporative and refueling emission standards," Code of Federal Regulations, ecfr.gov rules impose comparable 0.05 g/day DBL limits for 2027-2032. These ceilings effectively render single-layer HDPE tanks obsolete. Tier-1 suppliers must front-load capital to validate multi-layer solutions by 2026, adding 25-30% content value per unit. Regulatory asymmetry allows emerging-market suppliers to defer investment. Still, global OEM platforms require universal compliance, prompting multinational suppliers to accelerate the deployment of barrier technology and preserve their share in the automotive fuel tank market.

Flex-Fuel Infrastructure Drives Barrier-Tank Adoption

Brazil’s E27 mandate and India’s nationwide E20 program expose conventional HDPE tanks to ethanol-induced swelling of 8-12%, raising vapor escape by up to 300% over a decade. Multi-layer HDPE with EVOH liners maintains permeation rates below 2% of those of single-layer materials, ensuring long-term compliance. The United States' approval of year-round E15 sales in 2024 is expected to expand the retrofit pool by an estimated 12 million vehicles through 2030. Aftermarket suppliers capture 40-50% price premiums on barrier replacements, adding a lucrative revenue stream to the automotive fuel tank market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Electrification | -1.8% | Global, with accelerated impact in EU, China, and California | Long term (≥ 4 years) |

| Raw Material Cost Volatility | -0.6% | Global, with particular impact on cost-sensitive emerging markets | Short term (≤ 2 years) |

| BEV Platforms Eroding OEM CAPEX | -0.5% | Global, with concentrated impact in premium vehicle segments | Long term (≥ 4 years) |

| Fire-Safety Concerns With High-Ethanol Blends | -0.4% | North America and Brazil, with selective impact in E85 adoption markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Electrification Erodes Traditional Fuel Tank Demand

During the period from January to November 2024, global EV sales amounted to 18.5 million units[3]Suki, "Global EV Sales Hit 18.5M Jan-Nov, China’s Share at 62.7%," ChinaEVHome, chinaevhome.com , reflecting a 21% growth compared to the corresponding period in the previous year. China’s BEV share in 2025 will initially squeeze the high-margin sedan and city-car segments, leaving suppliers reliant on lower-margin commercial and off-road demand. Accelerating zero-emission mandates threatens a direct volume drain in the automotive fuel tank market, obliging tier-1s to diversify into battery-thermal or hydrogen-storage systems.

Raw Material Cost Volatility Pressures Margins

HDPE resin traded between USD 950 and USD 1,150 per ton during 2024-2025, while aluminum sheet premiums rose 18% early in 2025 before easing. Fixed-price OEM contracts require suppliers to absorb these swings, resulting in a 150-200 basis point reduction in gross margins. Smaller tier-2 firms lacking hedge strategies face acquisition or exit, accelerating consolidation within the automotive fuel tank market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Capacity: Commercial Fleets Drive Oversized Demand

Medium-capacity 45 to 70-liter tanks account for 44.72% of the automotive fuel tank market share in 2025, serving global sedans and crossovers. Growth is slowing as hybrids adopt downsized units to make room for battery packs, yet the segment remains the backbone of the automotive fuel tank market. The demand for vehicles with a displacement below 45 liters is shrinking in China and Western Europe, where BEVs are dominating the micro-car segment.

The above-70-liter category is expanding at an 11.68% CAGR through 2031, fueled by pickup trucks, full-size SUVs, and long-haul commercial vehicles in North America and the Gulf states, while holding a 20-25% share of the automotive fuel tank market size. Tanks in Ford F-Series or Toyota Land Cruiser models range from 90 to 136 liters, supporting extended range expectations. Auxiliary metal tanks for off-road and defense add niche volume at 30-40% price premiums. Regional fuel-price disparities continue to favor smaller capacities in Europe and Japan, thereby sustaining parallel tooling requirements for suppliers.

By Material Type: Composites Gain Strategic Momentum

Plastic tanks captured 43.15% of the automotive fuel tank market share in 2025, split between cost-efficient single-layer HDPE for unregulated markets and multi-layer barrier variants for Euro 7 and LEV III regions. Composite Type IV cylinders for hydrogen and CNG, although niche, are climbing at a 10.67% CAGR and underpin premium growth for the automotive fuel tank market share in commercial trucks. Aluminum maintains a 15-20% foothold in luxury cars and light vans due to its crash-energy benefits, but this share erodes as OEMs pursue mass reduction. Steel continues its retreat to a single-digit share due to corrosion and weight penalties.

Ongoing infrastructure build-out added 150 European hydrogen stations in 2025, enabling cross-border corridors and reinforcing composite demand. Suppliers are developing thermoplastic liners that could halve cure times and lower cost by up to 30%, setting the stage for deeper penetration in the automotive fuel tank industry.

By Vehicle Type: Commercial Platforms Accelerate Share Shift

Passenger cars contributed 68.47% of the automotive fuel tank market share in 2025, but face headwinds from the adoption of urban BEVs. Medium and Heavy Commercial Vehicles are projected to grow at a 12.63% CAGR through 2031, driven by global freight growth of 2.5-3% annually and persistent range anxiety in battery-powered vans. Commercial-vehicle tanks earn 2-3 times the per-unit revenue of passenger-car systems, buffering suppliers against volume erosion elsewhere.

Light commercial vans prolong diesel tank demand because total-cost-of-ownership gaps with BEV equivalents remain 30-40% on routes above 150 km. Buses transition to CNG and hydrogen in city duty cycles but continue to use diesel for intercity routes, ensuring diversified revenue streams for the automotive fuel tank market industry through 2031.

By Fuel Type: Hydrogen Unlocks Next-Wave Growth

Gasoline systems held a 67.69% share of the automotive fuel tank market in 2025; however, hydrogen tanks are projected to rise at a 16.42% CAGR through 2031, driven by the deployment of Daimler GenH2 and Hyundai XCIENT trucks. Diesel content is declining as Euro 7 and China VI raise after-treatment costs, steering OEMs toward gasoline-hybrid or BEV alternatives for light vehicles. Flex-fuel tanks in Brazil, India, and the United States gain incremental volume from E20 to E85 blends, while CNG and LPG maintain a stable share within taxis and municipal fleets.

Hydrogen’s edge is compelling for heavy-duty applications—two 300-liter Type IV tanks store 80 kg of hydrogen and preserve payload, whereas a comparable BEV loses 4-5 tons to batteries. This operational advantage positions hydrogen as the fastest-growing slice of the automotive fuel tank market.

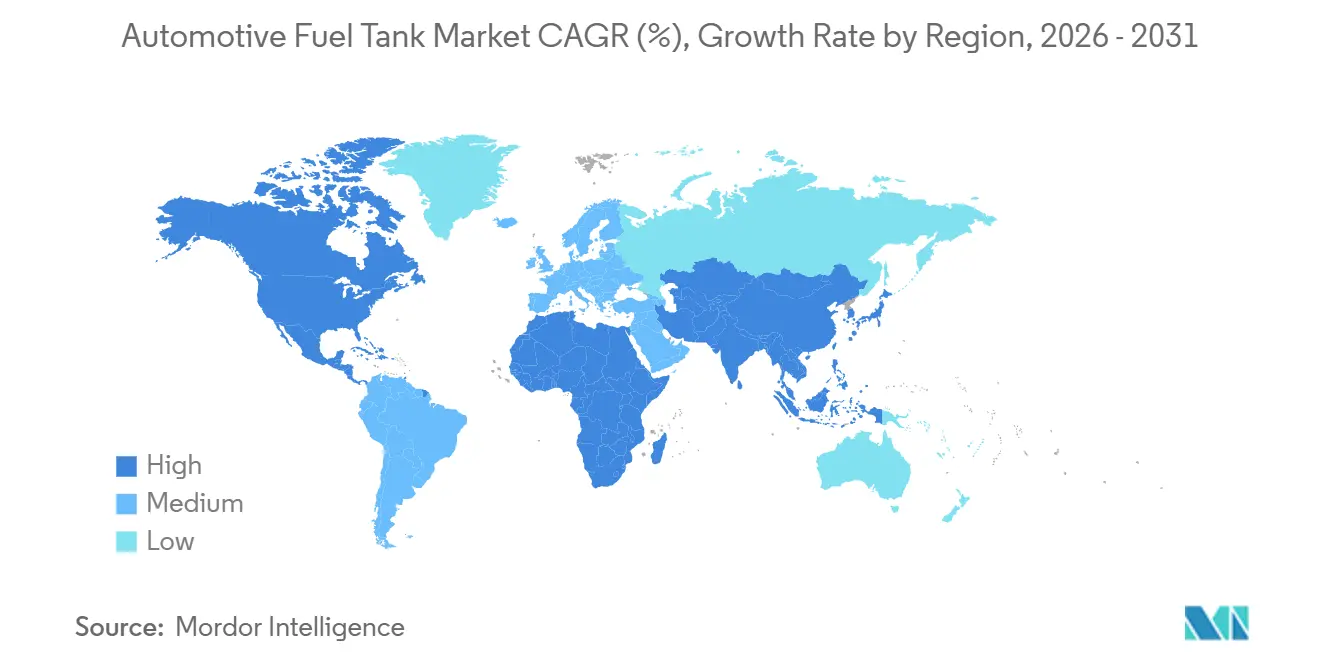

Geography Analysis

Asia-Pacific commanded 53.88% of the automotive fuel tank market share in 2025. China's E10 mandate, although partial, presents a retrofit opportunity worth nearly USD 2 billion. In Japan, a consistent demand for 40-55 liter tanks is upheld by the country's hybrid mix. Meanwhile, South Korea is on track to boost its Type IV exports to 50,000 units annually by 2026. Southeast Asia experiences a surge in demand, with motorcycle and three-wheeler tank sales, thereby bolstering the automotive fuel tank market.

The Middle East and Africa are the fastest-growing regions, with a 10.47% CAGR through 2031. Saudi Arabia aims to reach a vehicle production capacity of 300,000 by 2030, as outlined in Vision 2030, and Egypt is expanding its assembly capabilities for exports to the North African region. The UAE’s plan to establish 10 hydrogen stations by 2027 creates an early market for composite tanks. South Africa’s Euro 6d export requirements are driving the adoption of plastic barriers, while nascent plants in Kenya and Nigeria are localizing plastic tanks, thereby trimming logistics costs.

North America and Europe combined accounted for a significant share of the revenue in 2025. Europe is bifurcated: Western markets see fuel tank demand decline by 8-10% annually as the BEV share accelerates, whereas Central and Eastern European plants sustain ICE output for export.

Competitive Landscape

The automotive fuel tank market demonstrates moderate concentration. Key players leverage their global presence, in-house design capabilities, and long-standing relationships with OEMs to dominate volume programs. In 2024, TI Fluid Systems secured EUR 2.1 billion in electrification-related orders, while continuing to optimize cash flow from conventional tanks to support its expansion in thermal management. Magna integrates steel, plastic, and battery-enclosure technologies, aligning with OEM platform convergence that incorporates ICE, hybrid, and BEV variants.

Second-tier players, including Kautex, are advancing sustainability initiatives such as Green+, which incorporates recycled resins to maintain their position in Europe’s eco-label procurement market. Motherson Group has expanded its scale through the acquisition of Yachiyo Industry Co., enhancing its supply capabilities to Honda across Asia and North America. Specialist firms like Quantum Fuel Systems are focusing on ultra-high-pressure hydrogen cylinders, capturing opportunities in truck and railroad pilot projects. Although cost inflation and declining ICE volumes are driving consolidation, high technical barriers and regional homologation requirements prevent the market from transitioning into a complete oligopoly, maintaining competitive dynamics within the automotive fuel tank market.

Disruptors such as Hexagon Composites and Worthington Industries are leveraging their expertise in CNG to secure hydrogen contracts. Hexagon’s ISO 11439-certified cylinders are 30% lighter than aluminum-lined alternatives, offering a 600 km range for Class 8 trucks. Chinese manufacturers, including Cangzhou Mingzhu Plastic, operate at 30-40% lower costs, enabling them to submit competitive bids in price-sensitive markets. As margin pressures increase, consolidation is anticipated, compelling smaller tier-2 suppliers to pursue scale.

Automotive Fuel Tank Industry Leaders

-

TI Fluid Systems plc

-

Magna International Inc.

-

YAPP Automotive Systems Co. Ltd.

-

OPMOBILITY SE

-

Kautex Textron GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Quantum Fuel Systems and OneH2 unveiled 930-bar Type 4 cylinders, each holding 27 kg of hydrogen, eliminating the need for onsite compression.

- January 2025: The NHTSA issued FMVSS 307 and 308, governing the fuel-system integrity of hydrogen vehicles, with compliance effective as of September 2028.

- September 2024: The BMW Group expanded its hydrogen partnership with Toyota, aligning with a broader circular economy roadmap, which is expected to lead to an increase in demand for composite tanks.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the automotive fuel tank market as the value generated from new, factory-installed liquid or gaseous fuel storage systems fitted to passenger cars, light commercial vehicles, medium- and heavy-duty trucks, and buses that still rely on combustible energy. The valuation is expressed in USD at the original-equipment transaction level.

We deliberately exclude retrofit aftermarket replacement tanks and all battery enclosures from this scope.

Segmentation Overview

-

By Capacity

- Less than 45 Liter

- 45 to 70 Liter

- Above 70 Liter

-

By Material Type

- Plastic - single-layer

- Plastic - multi-layer/barrier

- Aluminium

- Steel

-

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Medium and Heavy Commercial Vehicles

- Buses and Coaches

-

By Fuel Type

- Gasoline

- Diesel

- Flex-fuel/Ethanol blends

- Hydrogen

- CNG and LPG

-

By Geography

-

North America

- United States

- Canada

- Rest of North America

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Egypt

- Turkey

- South Africa

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with Tier-1 tank makers, polymer suppliers, vehicle program managers, and regional homologation officials across Asia-Pacific, Europe, North America, and the GCC. These conversations tested secondary findings, refined average selling prices, and gauged adoption intent for composite hydrogen tanks, allowing us to close information gaps.

Desk Research

We began with structured desk work. Open data from OICA, Eurostat customs files, and the U.S. Energy Information Administration mapped vehicle output, cross-border flows, and average tank capacities. Regulations issued by UNECE WP.29 and NHTSA FMVSS 301/304 clarified material and permeation requirements, signaling demand shifts. Investor filings, Questel patent families, and Volza shipment logs revealed supplier footprints, while Dow Jones Factiva tracked capacity additions and recalls. The sources named are illustrative only; our analysts referenced many other records to validate every datapoint.

Market-Sizing & Forecasting

In our model, a top-down construct converts verified 2024 production and trade volumes into a demand pool, which is then matched with class-wise tank capacities and material penetration shares. Targeted bottom-up cross-checks, supplier revenue samples, Marklines program counts, and channel checks help fine-tune totals. Key inputs include vehicle build rates, average tank size per segment, plastic-to-metal substitution ratios, evaporative-emission thresholds, polymer price indices, and regional fuel-mix trends. A multivariate regression links these drivers to forecast 2025-2030 growth; any bottom-up variance beyond three percent is reconciled toward the converging mean.

Data Validation & Update Cycle

Our outputs undergo a two-stage peer review, with anomaly flags raised against OICA statistics and company filings. Divergences above five percent trigger respondent callbacks. Reports refresh every twelve months, with interim updates after material events. A final pre-delivery audit ensures clients receive the latest view.

Why Mordor's Automotive Fuel Tank Baseline Commands Reliability

Published estimates differ because firms choose unique scopes, price ladders, and refresh cadences. Some count only metal tanks, while others add hydrogen cylinders, and currency bases vary, so outputs inevitably diverge.

Key gap drivers include whether aftermarket units are tallied, inclusion of off-highway machinery, and unvalidated ASP assumptions that overlook rapid multilayer-plastic uptake.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 20.15 B | Mordor Intelligence | |

| USD 18.37 B | Regional Consultancy A | Omits composite hydrogen tanks and Asia aftermarket demand |

| USD 33.10 B | Global Consultancy B | Bundles CNG cylinders and retrofit sales, applies upper-quartile ASPs |

| USD 18.51 B | Industry Journal C | Uses 2023 exchange rates and excludes commercial buses |

The comparison shows that our disciplined scope choices, respondent-validated prices, and annual refresh cycle give decision-makers a balanced, transparent baseline that mirrors real production economics and can be readily reproduced by any diligent analyst.

Key Questions Answered in the Report

How large is the automotive fuel tank market in 2026?

The automotive fuel tank market size reached USD 17.43 billion in 2026.

What CAGR is expected for fuel tanks from 2026-2031?

Market value is projected to advance at a 4.11% CAGR through 2031.

Which region leads demand for automotive fuel tanks?

Asia-Pacific generated 53.88% of 2025 revenue due to high ICE and hybrid output.

Which capacity segment is growing fastest?

Tanks above 70 liters are forecast to post an 11.68% CAGR on the back of SUV and truck production.

How quickly are hydrogen tanks expanding?

Hydrogen systems are the fastest-growing fuel-type segment, rising at a 16.42% CAGR through 2031.

Page last updated on: