Automotive Electric Fuel Pumps Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 10.61 Billion |

| Market Size (2030) | USD 13.07 Billion |

| Growth Rate (2025 - 2030) | 4.27% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Electric Fuel Pumps Market Analysis by Mordor Intelligence

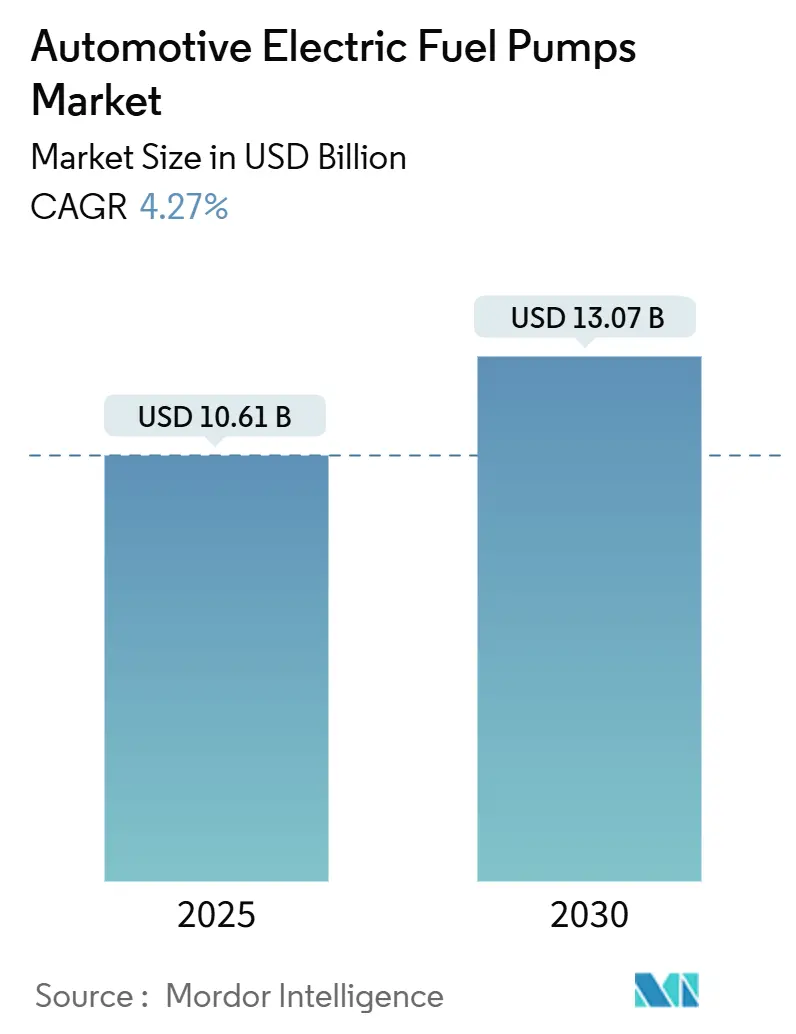

The Automotive Electric Fuel Pumps Market size is estimated at USD 10.61 billion in 2025, and is expected to reach USD 13.07 billion by 2030, at a CAGR of 4.27% during the forecast period (2025-2030). The growth pace reflects a balancing act between shrinking internal-combustion volumes and rising technical complexity per vehicle. Stricter emission rules, wider gasoline direct-injection (GDI) adoption, and OEM migration to brushless DC (BLDC) architectures keep content per unit climbing. Asia Pacific leads demand thanks to China’s large production base and India’s aftermarket expansion, while the Middle East & Africa posts the fastest gains as regional fleets modernize. Suppliers that combine advanced motor control, alternative-fuel compatibility, and predictive maintenance capability outperform rivals that compete only on price.

Key Report Takeaways

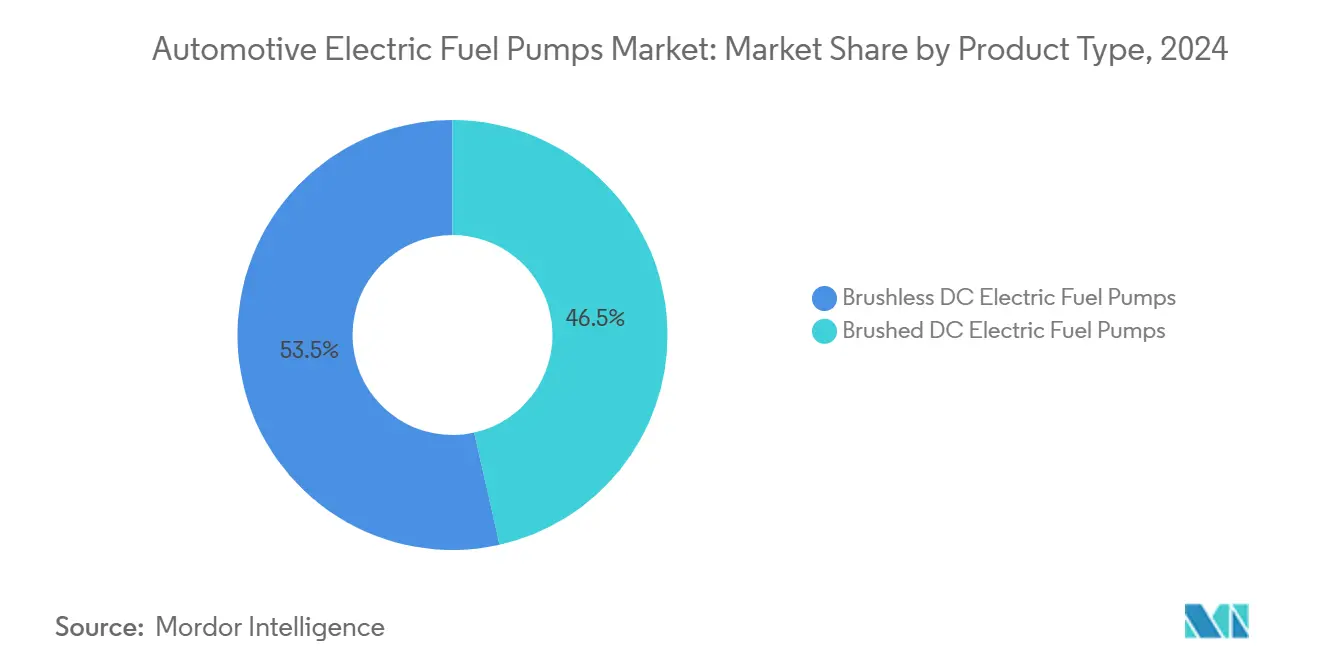

- By product type, brushless DC pumps accounted for 53.47% of the automotive electric fuel pumps market share in 2024, and also grew at a robust CAGR of 4.29% through 2030.

- By technology, turbine designs held 61.21% of the automotive electric fuel pumps market share in 2024 and are expanding at a 4.41% CAGR to 2030.

- By vehicle type, passenger cars controlled 73.46% of the automotive electric fuel pumps market share in 2024, whereas commercial vehicles are advancing at the highest 4.31% CAGR through 2030.

- By fuel type, gasoline retained 58.72% of the automotive electric fuel pumps market share in 2024, while hydrogen compatibility is projected to rise at a 4.35% CAGR by 2030.

- By distribution channel, OEM sales represented 67.73% of the automotive electric fuel pumps market share in 2024, whereas the aftermarket commanded a 4.37% CAGR by 2030.

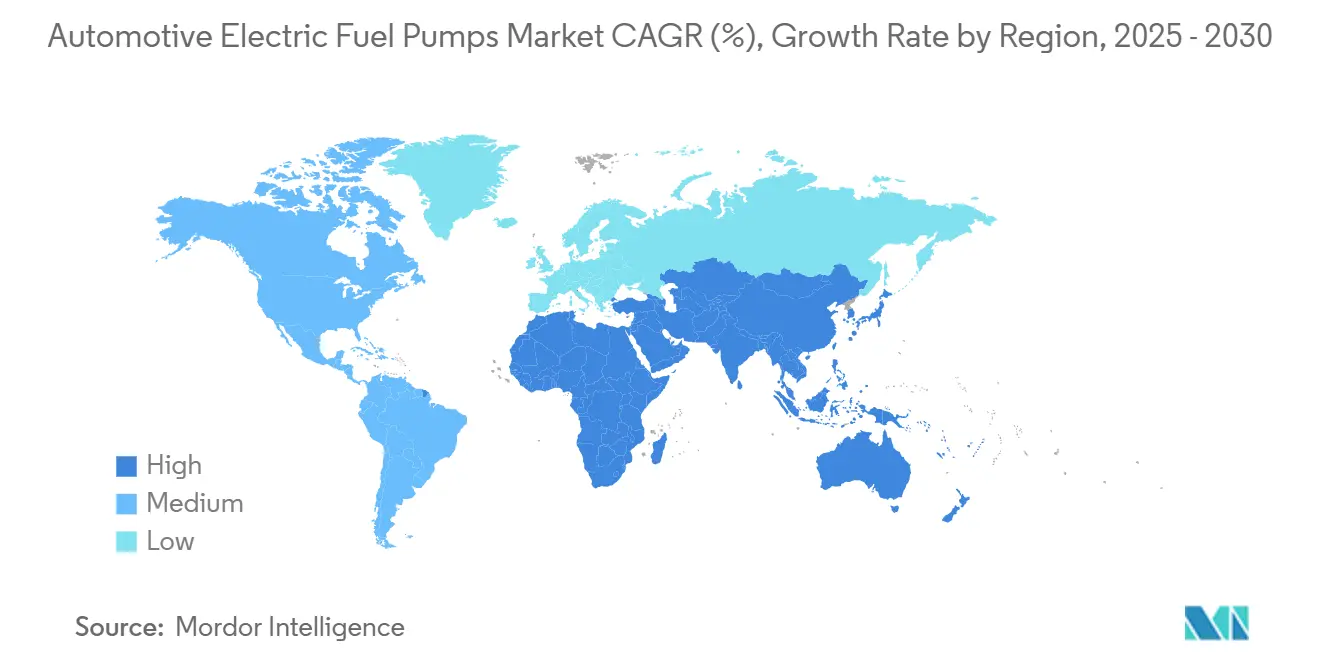

- By geography, Asia Pacific captured 38.26% of the automotive electric fuel pumps market share in 2024; the Middle East & Africa is poised for a 4.34% CAGR through 2030.

Global Automotive Electric Fuel Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Global Emission Regulations | +1.2% | North America and EU, expanding to Asia Pacific | Long term (≥ 4 years) |

| Rapid Growth Of Gasoline Direct-Injection Systems | +0.9% | Global, led by North America and Europe | Medium term (2-4 years) |

| Rising Demand For Fuel-Efficient Passenger Vehicles | +0.8% | Global, with concentration in Asia Pacific and Europe | Medium term (2-4 years) |

| OEM Shift Toward Brushless DC Pumps | +0.7% | Global, with early adoption in premium segments | Short term (≤ 2 years) |

| Integration Of AI-Enabled Predictive Maintenance In Pumps | +0.4% | North America and EU, pilot programs in Asia Pacific | Long term (≥ 4 years) |

| Emerging Low-Carbon E-Fuels | +0.3% | EU and select North American markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Global Emission Regulations For ICE Powertrains

Euro 7 rules, effective November 2026, double durability requirements to 200,000 km, forcing fuel-system parts to meet harsher thermal and contamination cycles[1]“Euro 7 Vehicle Emission Standards,” European Commission, europa.eu. Comparable mandates such as California’s Advanced Clean Cars II apply parallel pressure in North America. Pump makers must guarantee pressure stability from cold start to high-load events while resisting biofuel blends. Longer service life also favors corrosion-resistant housings and ethanol-tolerant elastomers. In-use compliance testing under authentic driving emissions protocols widens the operating envelope, rewarding designs that hold pressure in transient conditions. Suppliers with robust validation facilities and materials science expertise secure more platform awards.

Rapid Growth of Gasoline Direct-Injection Systems

GDI (Gasoline Direct-Injection) penetration exceeded half of the United States light-vehicle fleet in 2024, bringing more than 42 million GDI cars into replacement cycles over five years. Dual-pump architectures pair an in-tank electric pump with an engine-mounted mechanical unit and demand higher flow rates. Electric pumps must feed pressures above 6 bar into mechanical boosters that reach 200 bar. Contamination sensitivity and ethanol blends raise failure risk, lifting aftermarket volume. Component makers design low-pulsation impellers and multilayer filters to maintain clean supply lines. The surge in GDI adoption across mainstream vehicle lines extends growth beyond luxury segments.

Rising Demand For Fuel-Efficient Passenger Vehicles

Fuel economy remains a priority for fleet operators and private buyers amid volatile energy prices. Electric fuel pumps that sustain stable pressure at variable engine loads allow tighter air-fuel ratios, helping turbocharged downsized engines deliver minimal efficiency gains[2]“EcoBoost Technology Overview,” Ford Motor Company, corporate.ford.com. Smaller displacement engines rely on highly responsive fuel delivery to avoid knock and preserve torque. Vehicle makers pair intelligent pump control with engine management to cut parasitic losses, enhancing overall drivetrain optimization. Heightened total cost-of-ownership awareness among commercial buyers reinforces the shift toward components that deliver measurable consumption savings. The trend pushes suppliers to refine motor algorithms and integrate closed-loop control to support lean-burn strategies.

OEM Shift Toward Brushless DC Pumps For Durability & NVH

Brushless DC motors eliminate carbon brush wear and reduce electromagnetic interference that can disrupt modern control networks. BLDC designs offer smoother speed modulation, minimizing cavitation noise and improving passenger comfort. Carter’s latest sensorless BLDC pumps cut component count while elevating startup torque, meeting warranty targets for 10-year life cycles. Toshiba’s control IC series further optimizes efficiency, shrinking thermal footprints and enabling compact modules. As platform electrics migrate to 48 V architectures, BLDC pumps easily adapt, solidifying future relevance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation Of Battery-Electric Vehicles | -1.8% | Global, concentrated in China, EU, and California | Long term (≥ 4 years) |

| Counterfeit Aftermarket Pumps | -0.6% | Global, with highest impact in Asia Pacific and MEA | Medium term (2-4 years) |

| Raw-Material Price Volatility | -0.5% | Global, with acute impact in Asia Pacific manufacturing hubs | Short term (≤ 2 years) |

| High Upfront Cost | -0.4% | North America and EU, expanding to premium Asia Pacific segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation Of Battery-Electric Vehicles Reducing Addressable ICE PARC

Medium and heavy-duty battery electric truck registrations topped in 1H 2024, equal to a minimum of total commercial sales, and China held more than four-fifths of that volume. Every BEV displaces not only initial pump demand but also future aftermarket cycles. Urban distribution fleets are early adopters because duty cycles suit overnight depot charging. Jurisdictions such as California legislate progressive zero-emission quotas culminating in a complete transition by 2045. Suppliers counteract volume loss by diversifying into coolant pumps for thermal management and engineering modules for range-extender hybrids that retain liquid fuel.

Counterfeit Aftermarket Pumps Undermining OEM Volumes

According to industry audits, fake automotive parts generated almost two-tenths in global sales in 2024, and more than four-fifths originated from illicit factories in China. Counterfeit fuel pumps imitate OEM housings yet often use substandard commutators and porous die-castings. Failures lead to stalling and potential fires, eroding consumer confidence in legitimate suppliers. Brand owners deploy QR-code traceability and collaborate with customs agencies, but enforcement gaps persist, particularly in e-commerce channels. Counterfeits depress average selling prices, forcing genuine manufacturers to differentiate through extended warranties and tamper-proof packaging.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Brushless Technology Drives Premium Migration

Brushless DC pumps generated 53.47% of the automotive electric fuel pumps market share in 2024 and are forecast to grow at a 4.29% CAGR through 2030. The automotive electric fuel pumps market size for BLDC designs is projected to grow exponentially by the end of the period, reflecting rapid adoption in new platforms. Superior service life and lower electromagnetic interference make these pumps the preferred choice for emissions-sensitive regions. Suppliers leverage sensorless control chips that simplify wiring and cut bill-of-materials cost.

Brushed pumps remain common in cost-sensitive models and in the replacement channel. The automotive electric fuel pumps market continues to support large installed populations where budget constraints outweigh performance advantages. However, OEM engineering roadmaps indicate a steady phase-out as durability targets tighten. Niche innovations such as magnetic levitation rotors hint at future disruption, though commercial readiness sits beyond the current forecast horizon.

By Technology: Turbine Designs Dominate High-Pressure Applications

Turbine pumps held a 61.21% of the automotive electric fuel pumps market share in 2024, due to consistent flow under high back pressure. This subsegment is expected to expand at a 4.41% CAGR, driven by GDI and turbocharged engines prioritizing pressure stability. The automotive electric fuel pumps market share for turbine architecture is reinforced by ethanol-tolerant impeller resins and compact canister packaging that fits tight under-seat modules.

Sliding-vane pumps serve specialty vehicles that require variable displacement, while roller-cell designs gain traction where space constraints are critical. Suppliers offering modular families that cross over multiple vehicle classes win platform agreements. Enhanced coating technologies reduce wear from particulate contamination, extending warranty coverage to the 200,000 km threshold mandated by upcoming emission standards.

By Vehicle Type: Commercial Segments Drive Future Growth

Commercial vehicles are slated for a 4.31% CAGR to 2030, outpacing the overall automotive electric fuel pumps market despite passenger cars retaining 73.46% market share in 2024. High annual mileage accelerates replacement demand, creating fertile ground for predictive maintenance solutions that minimize downtime. Regulations targeting freight efficiency spur the adoption of advanced fuel-delivery modules that integrate thermal and pressure sensors.

Light commercial vehicles benefit from e-commerce parcel growth, while medium and heavy trucks confront extended emissions durability rules. Fleets value pumps with quick-connect service kits and telematics integration. Conversely, passenger car demand softens in metropolitan areas with high BEV penetration, though emerging markets offset some of the volume decline.

By Fuel Type: Alternative Fuel Compatibility Drives Innovation

Gasoline continued to dominate, with a 58.72% of the automotive electric fuel pumps market share in 2024. However, hydrogen fuel pumps are projected to rise at a 4.35% CAGR as governments promote alternative fuel vehicles. Fuel cell adoption is set to propel the hydrogen vehicle component market into rapid expansion by 2030. Innovations in materials are honing in on graphite bipolar plates, platinum catalysts, and premium stainless steel. These materials resist hydrogen embrittlement and guarantee safe and efficient fuel delivery, even under high pressure. Furthermore, sealing technologies and composite tank advancements are pivotal in adhering to stringent safety and durability benchmarks.

Diesel-oriented pumps face slower growth in passenger cars but remain vital for long-haul trucks. CNG and LPG stay in the niche because infrastructure growth lags. Pilot projects on e-fuel blends drive demand for pumps that tolerate low-lubricity synthetic hydrocarbons. Suppliers that certify parts for multiple fuels capture incremental retrofits.

By Distribution Channel: Aftermarket Growth Signals Replacement Demand

OEM sales commanded a 67.73% of the automotive electric fuel pumps market share in 2024 as factory-fit volumes dominated. The aftermarket is set for a 4.37% CAGR, reflecting aging fleets and complex multi-pump systems that heighten failure incidence. Online platforms improve parts visibility and ease price comparison.

Manufacturers strengthen installer support by supplying video tutorials and live technical chat. E-commerce growth also raises counterfeit exposure, so genuine brands implement holographic seals and blockchain traceability. The automotive electric fuel pumps industry invests in digital engagement to retain customer trust.

Geography Analysis

Asia Pacific held 38.26% of the automotive electric fuel pumps market share in 2024. China’s dense supplier ecosystem reduces component lead times and supports cost leadership, while India’s expanded Bharat Stage-VI fuel standards stimulated OEM demand for durable pumps[3]“China Manufacturing Capacity Statement,” SAIC Motor, saicmotor.com. Local brands source both turbine and sliding-vane designs to satisfy varied platform needs. Aftermarket sales rise as the Indian vehicle parc ages, and warranty expirations push owners to independent garages.

The Middle East and Africa are the fastest-growing territories, with a 4.34% CAGR through 2030. Rising vehicle ownership in Egypt and Nigeria pushes demand for reliable fuel pumps suitable for high-sulfur fuels. Chinese OEMs increased exports to Gulf states by two-fifths in 2024, expanding the installed base and replacement opportunities. Regional governments champion industrial diversification, and new assembly plants in Morocco and South Africa localize sourcing.

North America and Europe remain technologically influential. Euro 7 component durability rules prompt early adoption of BLDC modules with stainless steel internals. Over 42 million GDI cars are due for pump replacements in the United States by 2030, creating a sizable aftermarket. Meanwhile, ZEV mandates trim long-term volume, compelling suppliers to diversify into coolant and hydrogen circulation pumps.

Competitive Landscape

The automotive electric fuel pumps market shows moderate concentration with Bosch, Denso, and Continental leveraging scale and vertically integrated motor-control IP. Mid-tier specialists like Carter Fuel Systems focus on aftermarket agility and ethanol-tolerant variants. Chinese low-cost producers flood price-sensitive regions, elevating competitive tension.

Technology battles now center on sensorless BLDC controls, AI-enabled diagnostics, and corrosion-resistant materials. Bosch invested to scale fuel-cell stack production, demonstrating strategic hedging toward alternative propulsion while preserving ICE revenue. ZF’s stake in CarPay-Diem mobile fueling services illustrates diversification into data-driven ecosystems.

Intellectual property surrounding predictive maintenance algorithms offers sustainable differentiation. Suppliers that embed micro-vibration analysis claim up to one-fifth of warranty cost reduction for OEMs. Consolidation is likely as durability requirements rise and smaller firms struggle with validation costs. Market entrants must offer novel features such as magnetic levitation or integrated pressure sensors to displace incumbents.

Automotive Electric Fuel Pumps Industry Leaders

Robert Bosch GmbH

Denso Corporation

Continental AG

BorgWarner

TI Fluid Systems Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Cummins has unveiled a cutting-edge fuel system for off-highway sectors, including construction and mining. This move signifies a notable leap in the automotive fuel pump arena. The system boasts a common rail design, achieving up to 2200 bar pressures. With serviceable components such as the Low-Pressure Pump and Inlet Metering Valve, it promises heightened durability, improved fuel efficiency, and adherence to emissions standards. These features not only bolster its appeal for widespread industrial use but also contribute to a reduced total cost of ownership.

- April 2025: Delphi, a brand under PHINIA Inc., rolled out 56 new parts, prominently featuring fuel pump module assemblies, targeting the North American aftermarket. These additions aim to address the growing demand for high-quality replacement parts, ensuring reliability and compatibility with a wide range of vehicles.

Global Automotive Electric Fuel Pumps Market Report Scope

| Brushed DC Electric Fuel Pumps |

| Brushless DC Electric Fuel Pumps |

| Turbine Style Pumps |

| Sliding Vane Pumps |

| Roller Cell Pumps |

| Passenger Cars | Hatchback |

| Sedan | |

| Sports Car and Coupe | |

| SUV and Crossover | |

| Commercial Vehicles | Light Commercial Vehicles (LCV) |

| Medium & Heavy Commercial Vehicles (MCV & HCV) |

| Gasoline |

| Diesel |

| CNG & LPG |

| Hydrogen |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Brushed DC Electric Fuel Pumps | |

| Brushless DC Electric Fuel Pumps | ||

| By Technology | Turbine Style Pumps | |

| Sliding Vane Pumps | ||

| Roller Cell Pumps | ||

| By Vehicle Type | Passenger Cars | Hatchback |

| Sedan | ||

| Sports Car and Coupe | ||

| SUV and Crossover | ||

| Commercial Vehicles | Light Commercial Vehicles (LCV) | |

| Medium & Heavy Commercial Vehicles (MCV & HCV) | ||

| By Fuel Type | Gasoline | |

| Diesel | ||

| CNG & LPG | ||

| Hydrogen | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big will the automotive electric fuel pumps market be in 2025?

The market generated USD 10.61 billion in revenue in 2025.

What is the forecast CAGR for automotive electric fuel pumps through 2030?

Revenue is projected to grow at a 4.27% CAGR between 2025 and 2030.

Which product type leads the current demand for electric fuel pumps?

Brushless DC pumps hold the top position with 53.47% revenue share in 2024.

Which region is growing fastest for electric fuel pumps?

The Middle East & Africa posts the highest 4.34% CAGR outlook to 2030.

Why are turbine pumps favored in new vehicle platforms?

Turbine designs maintain stable high-pressure flow, meeting GDI and emissions requirements.

How will battery-electric vehicles influence pump demand?

BEV growth reduces total ICE volumes, but suppliers offset the impact by serving hybrids and developing fuel-cell coolant pumps.

Page last updated on: