Injector Nozzle Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

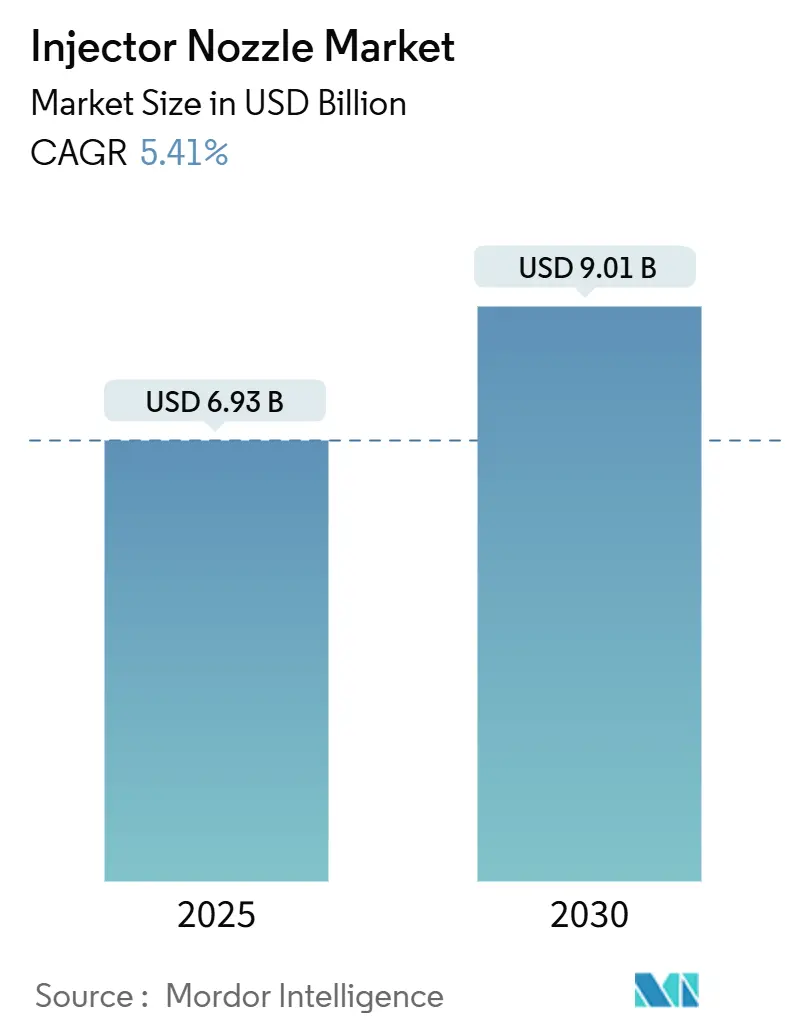

| Market Size (2025) | USD 6.93 Billion |

| Market Size (2030) | USD 9.01 Billion |

| Growth Rate (2025 - 2030) | 5.41% CAGR |

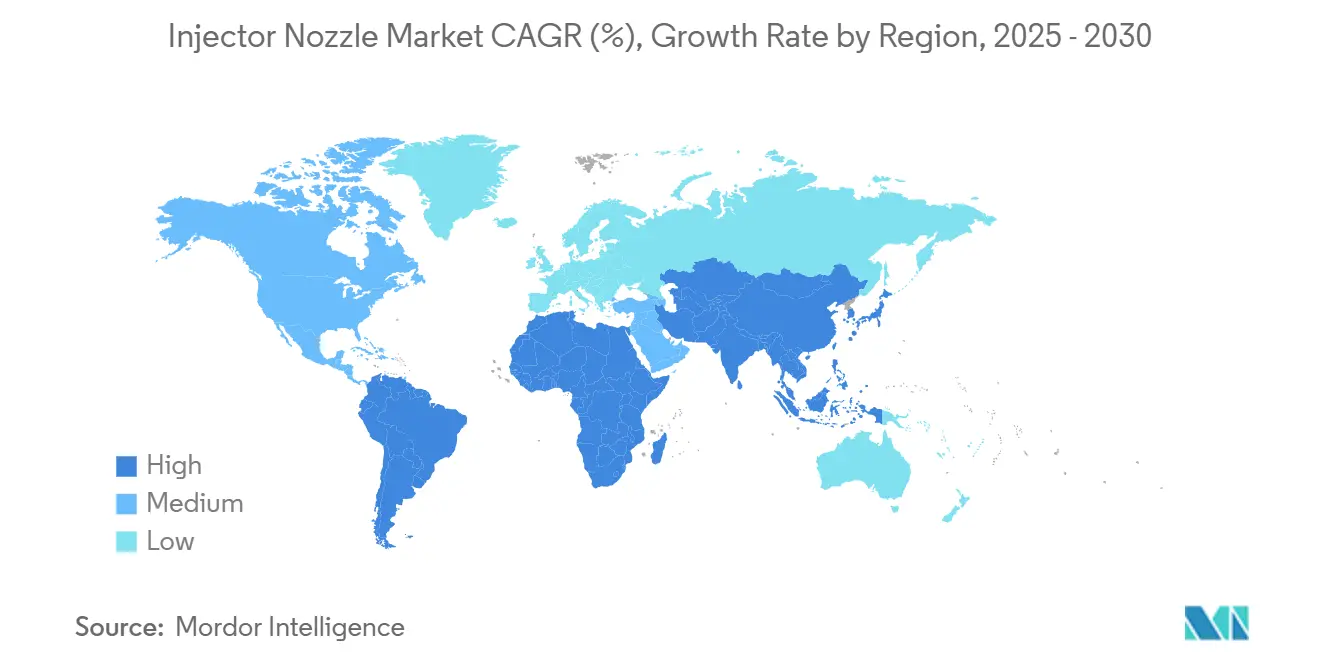

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Injector Nozzle Market Analysis by Mordor Intelligence

The injector nozzle market size is valued at USD 6.93 billion in 2025 and is forecast to reach USD 9.01 billion by 2030, expanding at a 5.41% CAGR over 2025-2030. Robust ICE demand in commercial vehicles, mounting emission standards, and the rise of hydrogen dual-fuel engines underpin this growth trajectory. Tighter tail-pipe regulations in Europe and China have shifted OEM focus to high-pressure gasoline direct-injection (GDI) platforms that require precision-machined multi-hole nozzles. Software-defined injectors with over-the-air calibration are gaining traction, turning the component into a connected subsystem. Meanwhile, electrification headwinds limit volumes in small urban vehicles, yet heavy-duty fleets continue to favor advanced diesel and emerging hydrogen solutions, cushioning overall demand.

Key Report Takeaways

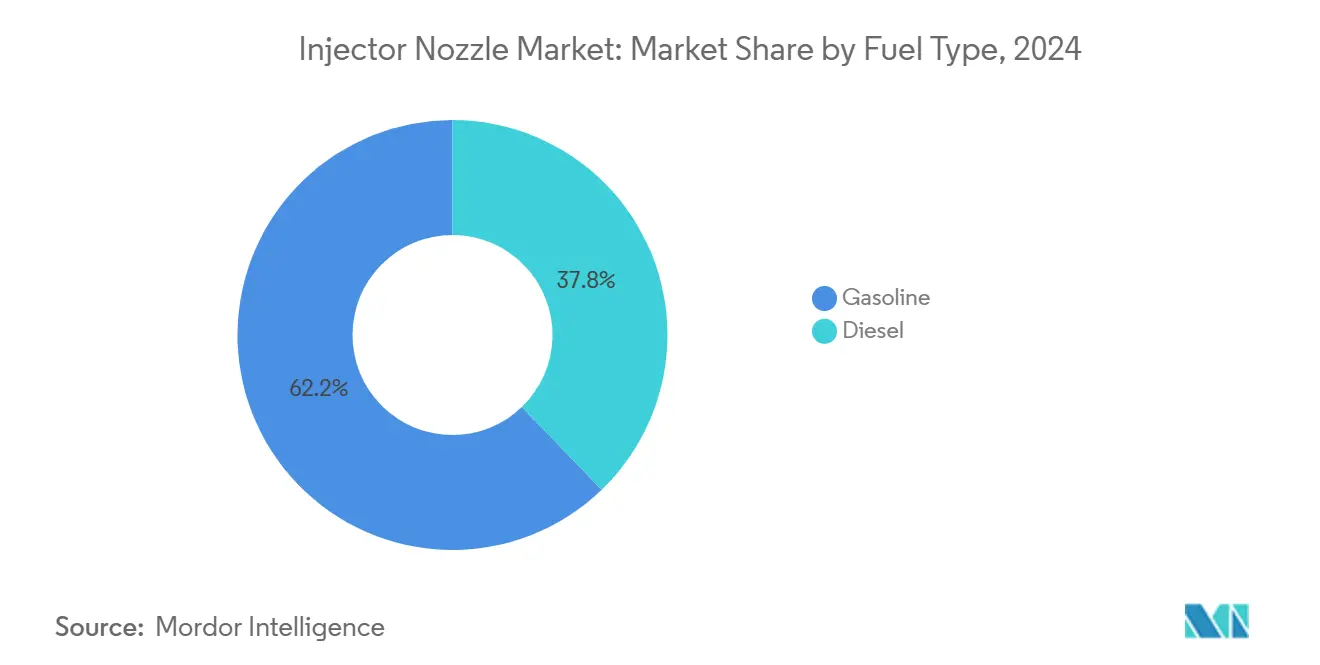

- By fuel type, gasoline led with 62.19% of the injector nozzle market share in 2024; diesel is projected to post the fastest 5.93% CAGR to 2030.

- By vehicle type, passenger cars accounted for a 71.87% share of the injector nozzle market size in 2024, and light commercial vehicles are advancing at a 6.84% CAGR through 2030.

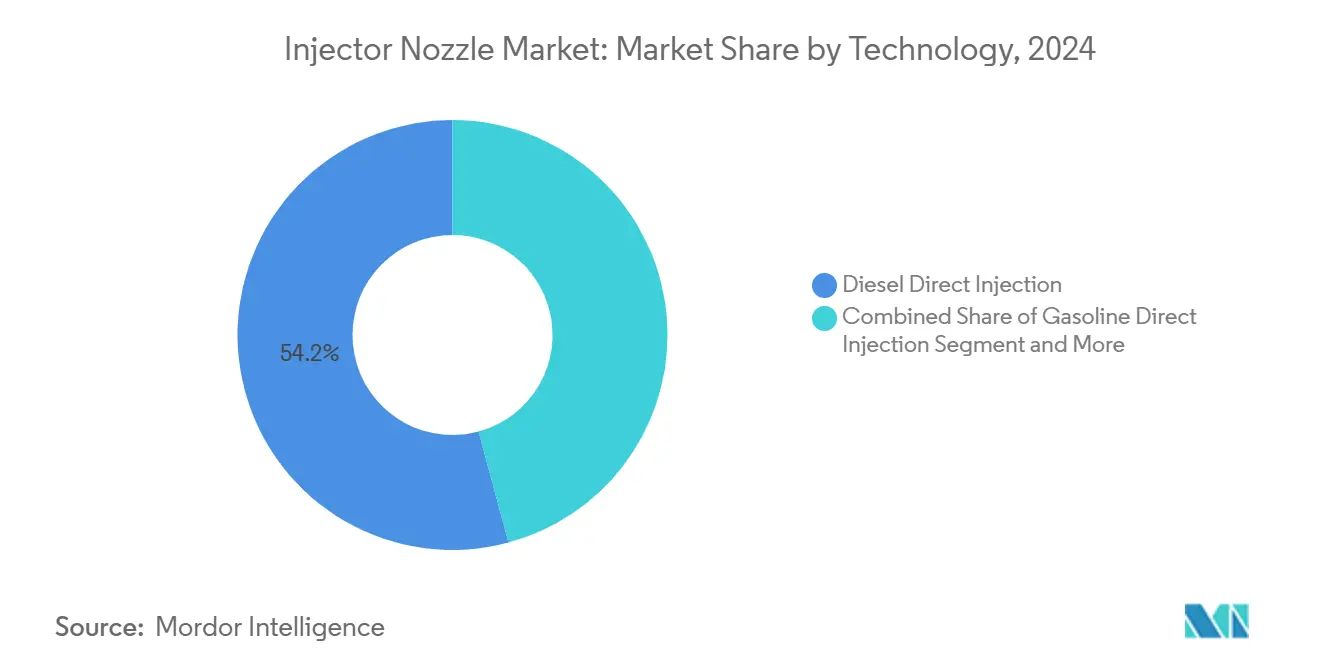

- By technology, diesel direct injection captured 54.16% share of the injector nozzle market size in 2024, while gasoline direct injection records the highest 7.27% CAGR to 2030.

- By nozzle type, multi-hole designs held 46.12% share of the injector nozzle market size in 2024 and are growing at a 6.37% CAGR through 2030.

- By geography, Asia-Pacific led with 48.23% of the injector nozzle market share in 2024; South America is projected to post the fastest 7.46% CAGR to 2030.

Global Injector Nozzle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Tail-Pipe and Evaporative Emission Norms | +1.8% | EU, China | Short Term (≤ 2 Years) |

| Rapid OEM Shift to Gasoline Direct-Injection Platforms | +1.5% | Asia-Pacific, Europe | Medium Term (2-4 Years) |

| Downsized Turbo Engines Demanding High-Pressure Multi-Hole Nozzles | +1.2% | Europe, North America | Medium Term (2-4 Years) |

| OEM Software-Defined Injector Pilots Enabling OTA Flow Tuning | +0.8% | North America, EU | Long Term (≥ 4 Years) |

| Surge in Hydrogen Dual-Fuel Retrofits for Heavy Trucks | +0.7% | Europe, China, North America | Medium Term (2-4 Years) |

| 3D-Printed Metallic Nozzles Reducing Prototype Lead-Time 60% | +0.6% | Global R&D Hubs | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Stringent Tail-Pipe and Evaporative Emission Norms

Euro 7 regulations introduce particle number limits of PN10 (particles >10 nanometers) that demand injection systems capable of achieving near-perfect fuel atomization to minimize particulate formation during combustion[1]"Commission proposes new Euro 7 standards to reduce pollutant emissions from vehicles and improve air quality," European Commission, europa.eu.. This regulatory shift forces OEMs beyond traditional PN23 compliance toward ultra-fine particle control, creating demand for multi-hole nozzles with optimized spray patterns and injection pressures exceeding 350 bar. China's implementation of China VI-B standards with extended warranty periods transfers emission compliance risk to tier-1 suppliers, compelling injection system manufacturers to invest in more robust designs and quality assurance processes. The regulatory cascade effect extends to emerging markets where Euro 4 and Euro 5 adoption accelerates, expanding the addressable market for precision injection technologies previously reserved for premium applications.

Rapid OEM Shift to Gasoline Direct-Injection Platforms

Toyota's expansion of its 2.0-liter Dynamic Force turbocharged engine family and Hyundai's Smartstream 1.0-liter turbo GDi deployment across compact vehicle platforms demonstrate how major OEMs prioritize direct injection for fuel economy gains. Volkswagen Group's EA888 Evo 5 engine achieves 500-bar injection pressure, representing a 67% increase from previous generations, while Mercedes-Benz integrates piezoelectric injectors across its M254 engine lineup to enable precise multi-injection strategies. This technological arms race creates differentiated demand for high-pressure fuel rails, precision-machined nozzle tips, and advanced control electronics that can manage injection timing within microsecond tolerances. The shift particularly benefits suppliers capable of integrating sensor technologies directly into injector bodies, enabling real-time feedback for adaptive injection strategies.

Downsized Turbo Engines Demanding High-Pressure Multi-Hole Nozzles

Engine downsizing strategies that maintain power output while improving fuel economy create extreme operating conditions requiring injection systems to deliver precise fuel metering under varying boost pressures and combustion chamber temperatures. Multi-hole nozzle designs with 6-8 holes optimize fuel distribution across downsized combustion chambers, while spray-guided injection strategies minimize wall wetting that causes particulate emissions. Advanced manufacturing techniques enable hole diameters below 150 micrometers with precise flow matching between holes, critical for maintaining combustion stability across the engine's expanded operating envelope. The trend toward 48-volt mild hybrid systems compounds complexity by requiring injection systems that can rapidly adapt to engine start-stop cycles and regenerative braking events.

Surge in Hydrogen Dual-Fuel Retrofits for Heavy-Duty Trucks

Bosch's hydrogen engine program targets a USD 1 billion market opportunity by 2030[2]"Bosch is banking on innovations, partnerships, and acquisitions – cost reduction remains in focus," Bosch, bosch-presse.de., with production orders from major truck OEMs across Europe, China, and North America for both port and direct hydrogen injection variants. Cummins' 15-liter X15H hydrogen engine and Volvo's collaboration with Westport Fuel Systems demonstrate how established powertrain manufacturers adapt existing injection expertise to hydrogen applications. Hydrogen injection systems require specialized materials and sealing technologies to handle hydrogen's unique properties, including its tendency to cause hydrogen embrittlement in conventional steel components. The retrofit market particularly benefits suppliers who can adapt existing diesel injection infrastructure for hydrogen compatibility, reducing capital requirements for fleet operators transitioning to carbon-neutral fuels.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Battery-EV Penetration in City-Bus and Entry Segments | -1.4% | Europe, China | Short Term (≤ 2 Years) |

| High Tooling Cost for Piezo and Ultra-High-Pressure Systems | -1.2% | Global | Medium Term (2-4 Years) |

| Tightening EU Particle-Number Rules Forcing Costly After-Treatments | -0.9% | Europe | Medium Term (2-4 Years) |

| China VI-B Warranty-Period Extension Shifting Risk to Suppliers | -0.8% | China | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Accelerating Battery-EV Penetration in City-Bus and Entry Car Segments

China's new energy vehicle penetration reached 55.1% of domestic passenger car sales in August 2025, with pure electric vehicles comprising the majority of this transition[3]"China’s automotive price war rages on despite regulatory crackdown," Nikkei Asia, kr-asia.com.. Urban bus electrification programs in major European cities eliminate thousands of diesel injection systems annually, while entry-level EV models like BYD's sub-USD 15,000 offerings directly compete with traditional ICE vehicles that would otherwise require fuel injection systems. The restraint particularly impacts suppliers focused on high-volume, cost-sensitive applications where electric powertrains achieve price parity with conventional engines. However, the transition creates opportunities in hybrid applications where injection systems must integrate with electric drive systems, demanding new control strategies and component specifications.

High Tooling Cost for Piezo and Ultra-High-Pressure Systems

Piezoelectric injector manufacturing requires specialized ceramic processing equipment and precision assembly capabilities that can exceed USD 50 million for complete production lines, creating barriers for smaller suppliers and limiting market participation to established tier-1 companies. Ultra-high-pressure fuel system development demands extensive testing infrastructure to validate component durability under pressures approaching 500 bar, while regulatory compliance testing for new injection technologies can extend development timelines by 18-24 months. These capital intensity requirements favor consolidation among injection system suppliers while potentially limiting innovation from smaller, specialized manufacturers who lack the resources for comprehensive tooling investments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Diesel Growth Outpaces Gasoline Despite Smaller Base

Diesel injection systems command 37.81% market share in 2024 but demonstrate superior growth momentum at 5.93% CAGR through 2030, outpacing gasoline's 5.41% expansion despite gasoline's dominant 62.19% market position. This counterintuitive dynamic reflects diesel's resilience in commercial vehicle applications where electrification faces range and payload constraints, particularly in long-haul trucking and construction equipment segments. Heavy-duty applications increasingly adopt common rail systems operating at pressures exceeding 2,500 bar, requiring precision-engineered nozzles capable of multiple injection events per combustion cycle.

Gasoline injection systems benefit from widespread GDI adoption across passenger car platforms, but face headwinds from accelerating EV penetration in urban mobility segments. The gasoline segment's evolution toward piezoelectric actuation and software-defined injection strategies creates value migration toward higher-specification components, partially offsetting volume declines in entry-level applications. Emerging alternative fuel compatibility, including synthetic e-fuels and hydrogen blends, positions both diesel and gasoline injection systems for extended relevance in carbon-neutral fuel applications.

By Vehicle Type: Commercial Segments Drive Growth Despite Passenger Car Dominance

Passenger Cars commanded 71.87% market share in 2024, while Light Commercial Vehicles emerged as the fastest-growing segment at 6.84% CAGR through 2030, significantly exceeding Passenger Cars' growth rate. This divergence reflects commercial vehicle operators' slower EV adoption due to total cost of ownership considerations, creating sustained demand for advanced injection systems in delivery, service, and utility applications. Medium and heavy commercial vehicles maintain steady demand for high-pressure diesel injection systems. At the same time, buses and coaches benefit from hydrogen dual-fuel retrofit programs that extend ICE powertrains' operational life.

The passenger car segment's large market share masks significant internal shifts toward hybrid powertrains that require injection systems capable of seamless integration with electric drive components. Advanced driver assistance systems and connected vehicle architectures drive demand for injection systems with embedded sensors and communication capabilities, transforming traditional mechanical components into integrated vehicle subsystems. Commercial vehicle applications particularly value injection system durability and serviceability, creating differentiated requirements for components designed for million-mile service intervals and harsh operating environments.

By Technology: GDI Acceleration Challenges Diesel Direct Injection Leadership

Diesel Direct Injection currently holds a 54.16% market share, while Gasoline Direct Injection technology accelerates at a 7.27% CAGR through 2030, positioning it to challenge diesel's dominance by the end of the forecast period. This technology transition reflects OEM strategies to maximize fuel economy from downsized engines while meeting increasingly stringent emission standards through precise fuel metering and combustion control. Advanced GDI systems incorporate spray-guided injection strategies and multi-hole nozzles operating at pressures approaching 500 bar, rivaling diesel system specifications.

Gasoline port fuel injection maintains relevance in cost-sensitive applications and hybrid powertrains where simplicity and reliability outweigh peak efficiency considerations. The technology's maturity enables manufacturers to achieve extremely competitive pricing while meeting basic emission requirements in markets where Euro 6 compliance suffices. Diesel direct injection systems evolve toward even higher pressures and more sophisticated injection strategies, including ducted fuel injection concepts that optimize fuel-air mixing in advanced combustion modes designed for carbon-neutral fuel compatibility.

By Nozzle Type: Multi-Hole Dominance Reflects Performance Demands

Multi-hole nozzles capture 46.12% market share in 2024 while maintaining the segment's highest growth rate at 6.37% CAGR, reflecting their superior fuel atomization capabilities essential for meeting Euro 7 particle number regulations. These designs typically incorporate 6-8 precisely machined holes with diameters below 150 micrometers, enabling spray patterns optimized for specific combustion chamber geometries and injection strategies. Advanced manufacturing techniques, including laser drilling and electrical discharge machining, achieve hole-to-hole flow variation below 2%, critical for maintaining combustion stability across all operating conditions.

Pintle nozzles retain significance in applications requiring variable spray patterns and robust operation in contaminated fuel environments, particularly in off-highway and marine applications where fuel quality varies significantly. Single-hole designs serve specialized applications including pilot injection strategies and alternative fuel compatibility testing, while pintaux configurations offer compromise solutions for applications requiring both performance and cost optimization. The nozzle type evolution toward additive manufacturing enables rapid prototyping and customization for specific engine applications, reducing development timelines by up to 60% compared to conventional machining processes.

Geography Analysis

Asia-Pacific accounted for 48.23% of global revenue in 2024. China’s August 2025 light-vehicle sales hit 2.54 million units, reflecting 16.5% year-on-year growth even as NEV mix surpassed 55%. India’s move to Bharat Stage VI norms and ethanol-blend mandates drives fresh demand for robust gasoline injectors. Japan and South Korea anchor high-precision manufacturing of piezo nozzles and supply significant export volumes across regions.

South America is the fastest-growing territory at a 7.46% CAGR. Brazilian flex-fuel programs require injectors tolerant of variable ethanol ratios, while Argentine pickup production supports high-pressure diesel component demand.

Europe and North America present contrasting pictures: stricter Euro 7 and EPA proposals push technology innovation—500-bar GDI and NOx-reducing diesel concepts—yet aggressive electrification targets curtail long-term volume. The Middle East and Africa leverage infrastructure investments for commercial truck demand, though currency volatility adds supplier risk. Overall, regional dynamics underscore the injector nozzle industry’s pivot from pure volume to value-rich, regulation-driven niches.

Competitive Landscape

Global supply is moderately concentrated. Bosch, Denso, and Continental shipped nearly half of the 2024 injector nozzles and are racing to commercialize hydrogen-ready systems. Bosch targets USD 5 billion in hydrogen revenue by 2030 and has secured five heavy-truck engine programs across three continents. Continental widened its aftermarket catalog in 2025, betting on sustained ICE servicing needs as global fleets age.

Denso’s semiconductor alliance with ROHM integrates power electronics into injector control modules, reducing latency and improving spray precision. Emerging competitors use additive manufacturing to target low-volume, high-customization niches such as motorsports and off-highway. The competitive battleground is shifting from mechanical excellence alone to full-system integration, blending hardware, embedded software, and cloud analytics.

OEMs increasingly award long-term module contracts that bundle injectors, pumps, rails, and control logic. Suppliers capable of life-cycle services—spanning calibration, real-time diagnostics, and over-the-air updates—achieve stickier revenue streams and higher margins. Market entrants lacking large-scale 500-bar validation assets face high barriers, tilting opportunities toward collaborative innovation or niche specialization.

Injector Nozzle Industry Leaders

-

Robert Bosch GmbH

-

Denso Corporation

-

Continental AG

-

Delphi Technologies (Phinia)

-

Magneti Marelli S.p.A

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Continental launched a major aftermarket product range expansion, including high-pressure fuel pumps as a first-time aftermarket introduction, expanding engine management offerings with approximately 700 new part numbers to increase coverage by 50% on average. The initiative leverages Continental's 20+ years of experience and 200+ million sensors/control units supplied to capture growing aftermarket demand for precision injection components.

- January 2024: Bosch announced hydrogen internal combustion engine development for heavy-duty trucking at CES 2024, featuring both port and direct injection variants expected to launch later in 2024. Company positioned dual approach continuing electrification while developing hydrogen technologies across production, supply infrastructure, and components.

Global Injector Nozzle Market Report Scope

| Diesel |

| Gasoline |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Buses and Coaches |

| Gasoline Port Fuel Injection |

| Gasoline Direct Injection |

| Diesel Direct Injection |

| Pintle |

| Multi-hole |

| Pintaux |

| Single-hole |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Fuel Type | Diesel | |

| Gasoline | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| Buses and Coaches | ||

| By Technology | Gasoline Port Fuel Injection | |

| Gasoline Direct Injection | ||

| Diesel Direct Injection | ||

| By Nozzle Type | Pintle | |

| Multi-hole | ||

| Pintaux | ||

| Single-hole | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the injector nozzle market?

The injector nozzle market size stands at USD 6.93 billion in 2025.

How fast is the injector nozzle market expected to grow?

It is projected to expand at a 5.41% CAGR between 2025 and 2030.

Which fuel type shows the strongest growth potential?

Diesel injector systems will post the fastest 5.93% CAGR due to heavy-duty and hydrogen dual-fuel demand.

Why are multi-hole injector nozzles gaining popularity?

Multi-hole designs achieve superior atomization needed for Euro 7 PN10 limits and command the highest 6.37% CAGR.

Which region leads global demand for injector nozzles?

Asia-Pacific remained the largest market with 48.23% share in 2024, driven by China and India.

How is hydrogen influencing injector nozzle development?

Tier-1 suppliers are launching hydrogen-compatible nozzles for heavy-duty trucks, opening a new multi-billion-dollar revenue stream by 2030.

Page last updated on: