Market Overview

| Study Period | 2020 - 2031 |

|---|---|

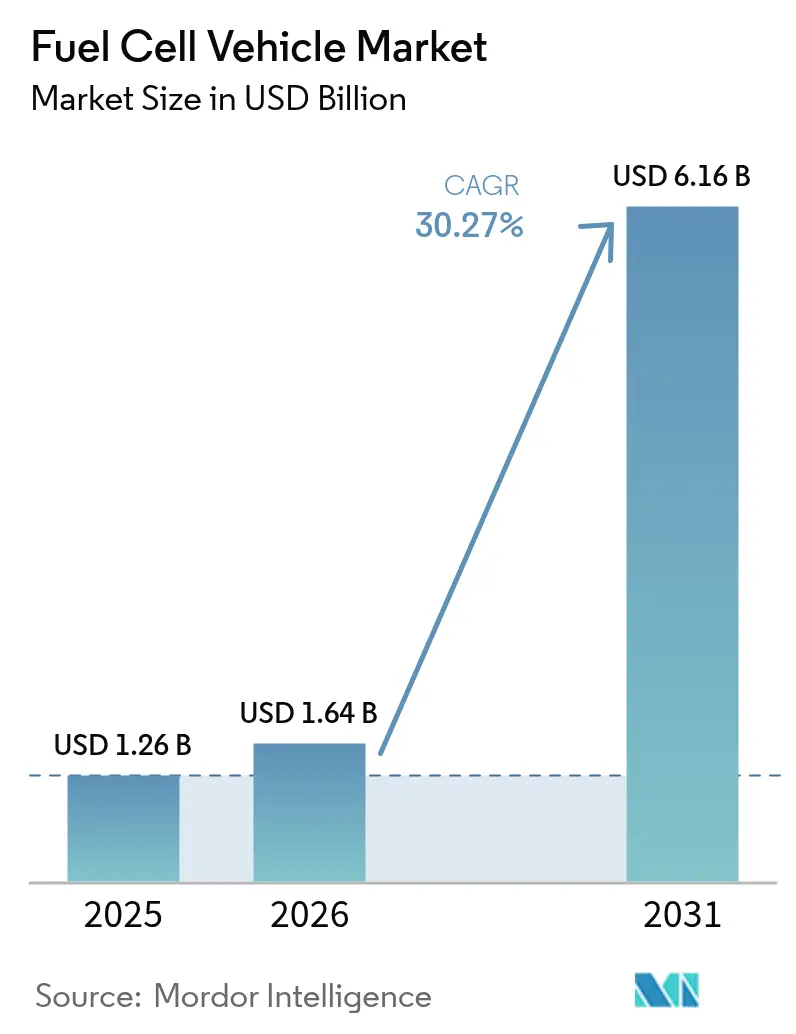

| Market Size (2026) | USD 1.64 Billion |

| Market Size (2031) | USD 6.16 Billion |

| Growth Rate (2026 - 2031) | 30.27% CAGR |

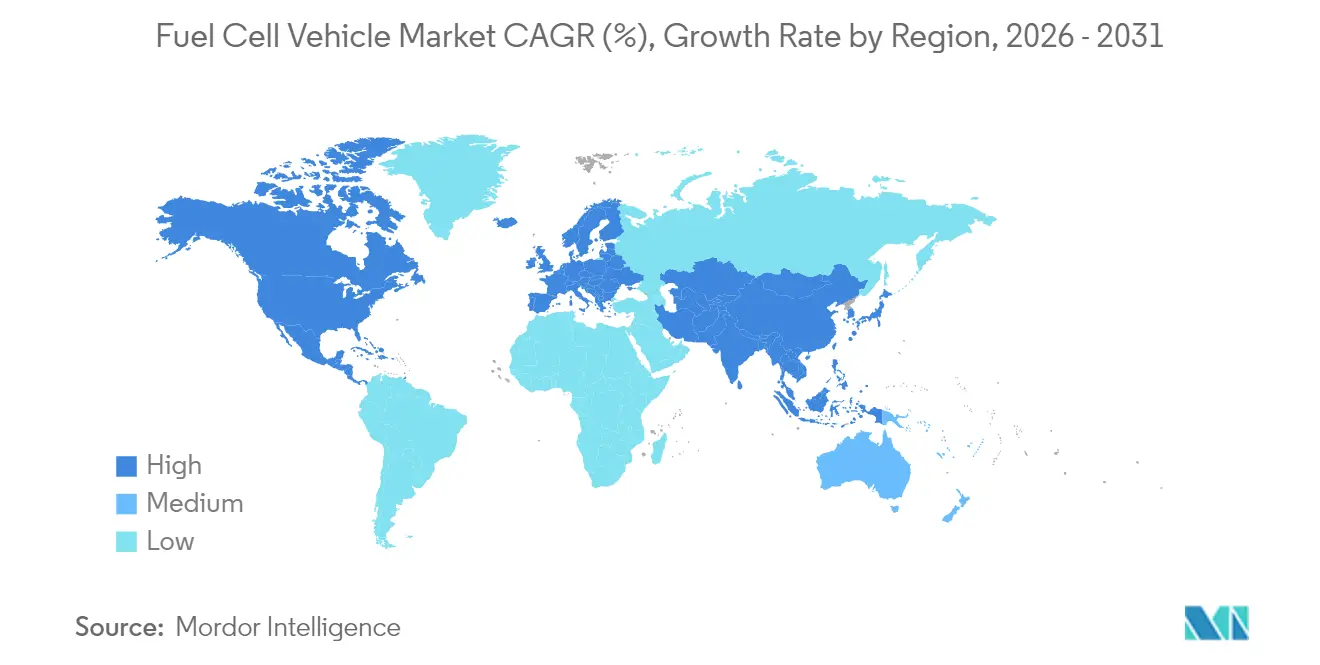

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

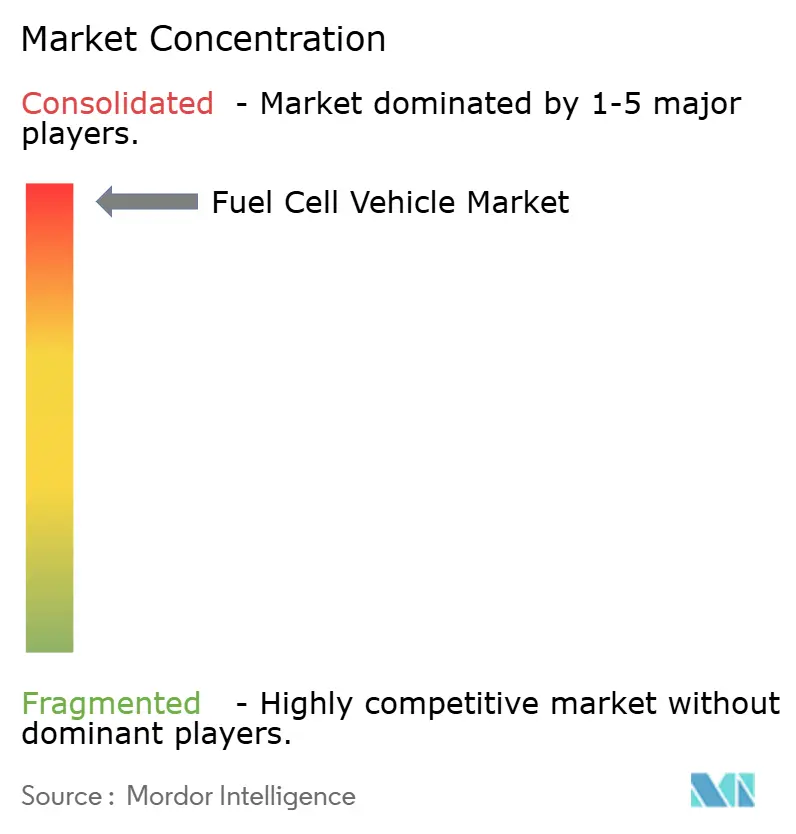

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fuel Cell Vehicle Market Analysis by Mordor Intelligence

The fuel cell vehicle market size in 2026 is estimated at USD 1.64 billion, growing from 2025 value of USD 1.26 billion with 2031 projections showing USD 6.16 billion, growing at 30.27% CAGR over 2026-2031. This acceleration reflects a fundamental shift from experimental deployments to commercial viability, driven by heavy-duty applications where hydrogen's energy density advantages over battery-electric alternatives become economically compelling. The market's momentum stems from converging policy frameworks, particularly the US Inflation Reduction Act's USD 3 billion in hydrogen production tax credits and the EU's Net-Zero Industry Act targeting 10 million tonnes of renewable hydrogen by 2030.[1]“Hydrogen Shot and Regional Clean Hydrogen Hubs,” US Department of Energy, energy.gov .

Key Report Takeaways

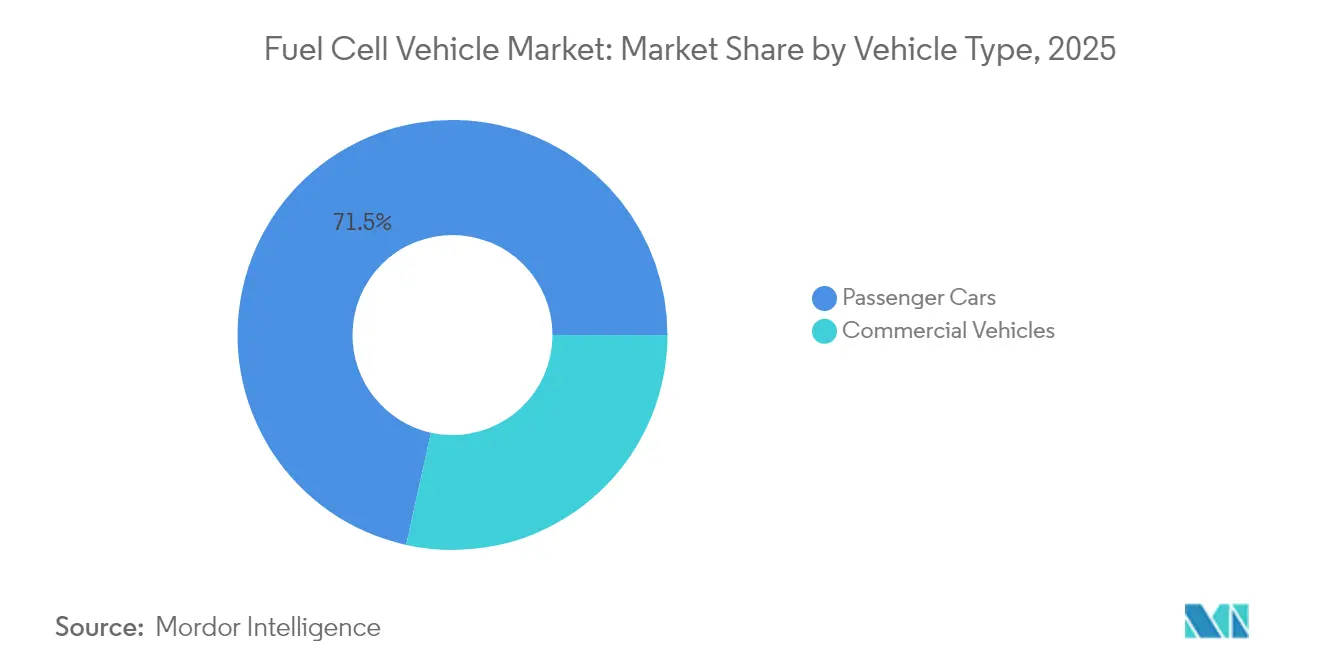

- By vehicle type, passenger cars held 71.54% of the fuel cell vehicle market share in 2025, while commercial vehicles recording the highest 47.10% CAGR through 2031.

- By fuel-cell type, PEM dominated with 90.85% 2025 revenue share; SOFC range-extenders are set to grow at 42.10% CAGR to 2031.

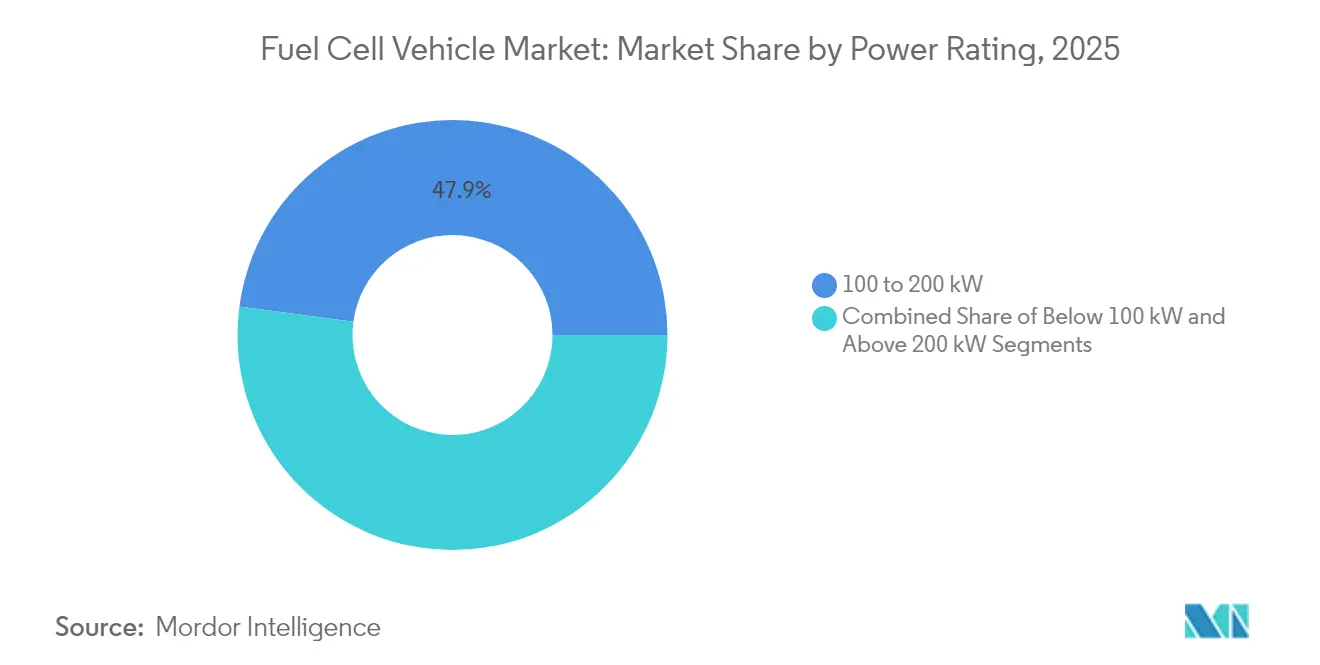

- By power rating, the More than 200 kW segment captured 49.40% CAGR leadership, whereas the 100 to 200 kW segment retained the largest 47.88% 2025 share.

- By component, Stack modules held the largest 43.70%, hydrogen storage systems is growing at 41.95% CAGR to 2031.

- By geography, Asia-Pacific accounted for 52.60% of the 2025 fuel cell vehicle market share; North America is forecast to post a 46.85% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fuel Cell Vehicle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| National ZEV and Hydrogen Road-Maps | +8.5% | Global, with strongest impact in US, EU, China, South Korea | Medium term (2-4 years) |

| Rising Heavy-Duty Fuel-Cell Truck | +6.2% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| China's "hydrogen port" Clusters | +4.8% | APAC core, spill-over to MEA ports | Medium term (2-4 years) |

| IRA & EU Net-Zero Industry Tax Credits | +7.1% | North America & EU | Short term (≤ 2 years) |

| Ammonia-to-Hydrogen Advances | +3.4% | Global, early adoption in maritime corridors | Long term (≥ 4 years) |

| OEM Shift to Methanol | +2.8% | EU & North America, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

National Zero-Emission-Vehicle and Hydrogen Road-maps Drive Market Transformation

Government mandates are reshaping fuel cell vehicle adoption through coordinated policy frameworks that simultaneously address supply and demand constraints. South Korea leads with 14,500 fuel cell electric vehicles, representing 33% of global deployment, supported by incentives reducing vehicle costs by approximately 50% and targets for 6.2 million hydrogen vehicles by 2040. The US Department of Energy's hydrogen strategy allocates USD 9.5 billion through the Bipartisan Infrastructure Law, targeting 10 million metric tons of annual production by 2030, while projecting 10-15% of trucks will utilize fuel cells by 2050. Japan's Hydrogen Society Promotion Act establishes 15-year price support programs and production hub development, aiming for a 12-million-ton hydrogen supply by 2040. These coordinated approaches create self-reinforcing cycles where infrastructure investment enables vehicle deployment, which justifies expanded refueling networks. China's allocation of USD 321 million for regional hydrogen fuel cell vehicle deployment demonstrates how targeted funding accelerates market formation beyond organic growth patterns.

Heavy-Duty Fuel Cell Truck Pilots Establish Commercial Viability

Freight corridor demonstrations prove fuel cell trucks' operational superiority in specific use cases, creating replicable business models for broader deployment. Nikola leads deployment with 90 trucks shipped in Q3 2024, representing 3,000% year-over-year growth, while establishing hydrogen refueling partnerships across key freight routes. Daimler Truck's liquid hydrogen system achieves a 650-mile range with a 45,000-pound payload, demonstrating a competitive advantage over battery-electric alternatives in long-haul applications where weight and refueling time directly impact profitability. Hyundai's XCIENT trucks logged over 13 million kilometers across 13 countries, providing real-world validation of 180 kW fuel cell systems' durability and 450-mile operational range. The National Renewable Energy Laboratory projects zero-emission trucks achieving total cost of ownership parity with diesel by 2035, with fuel cell vehicles particularly advantaged in applications requiring rapid refueling and high daily utilization. These demonstrations establish proof points fleet operators can reference when justifying capital investments, accelerating adoption beyond early-adopter segments.

China's Hydrogen Port Clusters Create Industrial Ecosystem

China's integration of fuel cell forklifts and yard tractors in port operations demonstrates how concentrated industrial applications can achieve economies of scale while building hydrogen infrastructure for broader vehicle deployment. Port operations provide ideal conditions for fuel cell adoption due to predictable duty cycles, centralized refueling infrastructure, and stringent emission regulations in coastal urban areas. The approach leverages existing industrial hydrogen supply chains while creating anchor demand that justifies infrastructure investments for other vehicle types. China's leadership in fuel cell installations, with 506 MW cumulative capacity primarily for trucks and buses, reflects systematic deployment strategies that prioritize high-utilization applications. This model enables port authorities to meet decarbonization targets while demonstrating fuel cell technology's commercial viability to other industrial operators.

IRA & EU Net-Zero Industry Act Accelerate Manufacturing Scale

Manufacturing incentives are shifting fuel cell production economics by reducing capital costs and enabling domestic supply chain development. The US Inflation Reduction Act provides production tax credits for fuel cell manufacturing alongside hydrogen production incentives, creating integrated value chain support that reduces technology costs. EU investments exceed USD 60 billion for battery and fuel cell manufacturing from 2022-2023, with the Net-Zero Industry Act targeting domestic production capacity to reduce import dependence. These policies address the chicken-and-egg problem where high costs prevent scale, which prevents cost reduction, by providing temporary support during the transition to commercial viability. BMW's partnership with Toyota for 2028 fuel cell vehicle production reflects confidence that manufacturing incentives will enable cost-competitive systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Slow Roll-Out of Public Stations | -5.8% | Global, Most Severe in Emerging Markets | Medium term (2-4 years) |

| Battery-Price Plunge Tilting TCO in Favor of BEVs | -4.2% | Global, Strongest Impact in Light-Duty Segments | Short term (≤ 2 years) |

| Persistent On-Board Hydrogen Tank Delays | -2.1% | EU, with Spillover to Other Regulatory Regions | Short term (≤ 2 years) |

| Nickel-based Catalyst Supply Risk Management | -1.9% | Global, Concentrated in High-Volume Applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Slow Roll-out of Public 700-bar Stations Constrains Market Expansion

Infrastructure deployment lags vehicle availability, creating geographic constraints that limit fuel cell vehicle adoption to specific corridors and metropolitan areas. Global hydrogen refueling stations reached only 1,369 by end-2024, with 79% concentrated in China, South Korea, Japan, France, and Germany, leaving vast regions without access. California's hydrogen network decreased to 62 operational stations in 2024 due to supply and reliability issues, forcing automakers to revise FCEV sales projections to only 20,500 vehicles by 2030.[2] “Hydrogen Station Network Update 2024,” California Air Resources Board, arb.ca.gov. The hydrogen fueling station market requires USD 6.17 billion investment by 2034 to support projected vehicle deployment, yet current funding mechanisms remain insufficient for rapid expansion. Station development timelines average 1.6 years compared to 4.9 years for earlier projects, indicating improving processes, yet the absolute number of new stations remains below requirements for mass market adoption.

Battery-Price Plunge Tilts TCO Toward BEVs in Short-Range Applications

Rapidly declining battery costs are expanding the range of applications where battery-electric vehicles achieve total cost of ownership advantages over fuel cell alternatives. Battery system costs may decrease 64-75% by 2050 while fuel cell costs drop 65-85%, yet battery cost reductions are occurring faster and from a lower baseline. The total cost of ownership analysis shows that battery-electric trucks will become competitive with diesel by 2030 in most applications, while fuel cell trucks will face higher hydrogen costs, currently ranging from USD 30-40 per kilogram. The crossover point where fuel cells maintain an advantage occurs primarily in heavy-duty, long-haul applications requiring rapid refueling and high daily utilization, narrowing the addressable market compared to earlier projections. This dynamic forces fuel cell manufacturers to focus on specific niches rather than broad market adoption, potentially limiting scale economies needed for further cost reduction.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Applications Drive Market Transformation

Passenger Cars had a 71.54% of the 2025 share of the fuel cell vehicle market. Heavy-duty trucks benefit from 650-mile ranges and 10-minute refuels that preserve freight utilization metrics. Transit buses are scaling quickly in China—more than 1,000 units—as municipal authorities integrate hydrogen depots with depot-charging hubs. Delivery vans employing methanol-reforming range-extenders circumvent hydrogen station shortages, advancing zero-emission compliance for urban logistics fleets. The structural tilt toward fleet segments underpins long-term resilience of the fuel cell vehicle market.

Commercial vehicles lead growth with a 47.10% CAGR to 2031. Conversely, passenger cars’ share falls despite unit growth as price-sensitive consumers gravitate to battery EVs for short-distance use cases.

By Fuel-Cell Type: SOFC Range-Extenders Challenge PEM Dominance

PEM units supplied 90.85% of fuel cell stacks in 2025, but SOFC range-extenders are forecast to deliver 42.10% CAGR through 2031, exceeding PEM’s. High-temperature SOFCs operate at 500–700 °C, enabling 60–72% system efficiency and tolerance for methanol or ammonia, which eases fuel logistics in infrastructure-poor regions. BMW’s pilot vans with Ceres Power SOFC modules illustrate automaker interest in a platform that can piggyback existing liquid-fuel supply chains.

SOFC solutions now commanded less than 2.80% of the 2025 fuel cell vehicle market size, yet could capture above 8.60% by 2031 if supply chains scale. PEM is expected to keep the majority share but face progressive erosion as multi-fuel flexibility becomes a competitive differentiator.

By Power Rating: High-Power Systems Enable Heavy-Duty Applications

The 100–200 kW bracket held 47.88% of 2025 revenue, balancing power and cost for regional distribution trucks and premium passenger vehicles. Below 100 kW stacks continue serving forklifts and compact cars, but their share declines as automotive OEMs scale higher-output platforms. Systems rated more than 200 kW booked a 49.40% CAGR, buoyed by Class 8 truck roll-outs that prioritize payload retention and hill-climb performance.

Total revenue for the More than 200 kW class is set to rise from 2025 to 2031, representing second largest share of the projected fuel cell vehicle market size. Hyundai’s 180 kW XCIENT platform and Daimler Truck’s 230 kW GenH2 prototype underscore the industry pivot toward high-power architecture.

By Component: Hydrogen Storage Innovation Drives System Integration

Stack modules held the largest 43.70% share but decelerated as learning curves flattened, hydrogen storage rises fastest at 41.95% CAGR as Type-IV carbon-fiber tanks and cryo-compressed systems enhance volumetric density. Plant support systems—including compressors, humidifiers, and thermal loops—contributed 24%, while e-drive components added 13% to the total bill-of-materials. Daimler Truck’s liquid hydrogen system shows how advanced storage can unlock a 650-mile range without increasing chassis weight, underpinning competitive advantage in the fuel cell vehicle market.

Geography Analysis

Asia-Pacific retained a 52.60% 2025 share because China, Japan, and South Korea built integrated hydrogen ecosystems spanning production, distribution, and vehicle incentives. China installed 506 MW of fuel cell capacity and is targeting 100,000 fuel cell trucks by 2030, leveraging port and steel-plant hydrogen by-products. South Korea’s 14,500 vehicles ride on subsidies that cut sticker prices by 50%, while the national roadmap calls for 6.2 million units by 2040. Japan remains the global leader in stationary deployments, but transportation uptake is accelerating under 15-year price guarantees.

North America leading 46.85% CAGR through 2031 thanks to the Inflation Reduction Act’s hydrogen provisions and California’s zero-emission mandates. The US Department of Energy funds seven regional hydrogen hubs, each required to serve mobility loads, ensuring a pipeline of demand for the fuel cell vehicle market. Hyundai’s USD 21 billion plan for US fuel cell truck production and infrastructure exemplifies foreign OEM confidence in policy stability.

Western and Central Europe is growing, spearheaded by Germany’s 113 public stations and the EU’s 10-million-ton hydrogen target. Daimler Truck secured EUR 226 million to field 100 liquid-hydrogen trucks. At the same time, the Clean Hydrogen Joint Undertaking injects EUR 113.5 million into R&D. BMW’s Toyota alliance signals broader European OEM alignment behind hydrogen as a complement to battery EVs.

Competitive Landscape

Competition is highly concentrated, featuring diversified strategies among legacy OEMs and pure-play fuel cell firms. Toyota leads passenger cars with Mirai sales and is refining a third-generation stack that cuts platinum loading. Hyundai’s ecosystem approach covers trucks, buses, and forklifts delivered under its Hydrogen Vision 2040 roadmap. BMW plans series production in 2028 through its partnership with Toyota, leveraging PEM maturity while co-developing SOFC range-extenders with Ceres Power.

Ballard Power Systems supplied 130 MW to global bus fleets, focusing on module standardization for faster OEM integration. Nikola delivered 90 fuel cell trucks in one quarter, underlining a first-mover push in North America with bundled vehicle-and-fuel contracts. Chinese OEMs SAIC and FAW are scaling stack production to serve domestic mandates, sharpening price competition worldwide.

Strategic patterns emphasize vertical integration and ecosystem development rather than component-level competition, reflecting fuel cell vehicles' dependence on hydrogen infrastructure and supply chains. Technology differentiation centers on power density improvements, fuel flexibility through SOFC systems, and manufacturing cost reduction through automotive-scale production. White-space opportunities emerge in medium-duty delivery vehicles where methanol-reforming fuel cells enable zero-emission operation without hydrogen infrastructure, and in industrial applications like port equipment where centralized refueling justifies infrastructure investments. The US Department of Energy's National Electric Vehicle Infrastructure program standards create opportunities for companies developing integrated charging and hydrogen refueling facilities, while BMW's filing for hydrogen vehicle safety systems demonstrates ongoing patent activity in critical enabling technologies .[3] “FMVSS 307 & 308 Hydrogen Fuel Systems,” Federal Register, federalregister.gov.

Fuel Cell Vehicle Industry Leaders

Volkswagen AG

Mercedes-Benz Group

Honda Motor Company Limited

Hyundai Motor Company

Toyota Motor Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Hyundai Motor and Plus Unveil Concept for Autonomous Hydrogen Freight Ecosystem at ACT Expo 2025.The concept demonstrates a scalable approach to achieving zero-tailpipe emissions in autonomous long-haul freight, supported by hydrogen infrastructure.

- April 2025: China allocated USD 321 million for regional hydrogen fuel cell vehicle deployment, demonstrating continued government commitment to market development through targeted funding.

- September 2024: BMW is planning to launch its first-ever series production fuel cell electric vehicle (FCEV) in 2028, thereby expanding its portfolio with an all-electric powertrain option that produces zero local emissions. The BMW Group and Toyota Motor Corporation are leveraging their combined innovative capabilities and technological expertise to develop and commercialize a new generation of fuel cell powertrain technology.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the fuel cell vehicle (FCV) market as the total factory-built on-road passenger and commercial vehicles whose primary traction power is supplied by a hydrogen fuel-cell stack, with energy converted to electricity and emitting only water vapor and warm air. The figure covers shipments and registered stock converted to current-year revenue using weighted average transaction prices for each vehicle class.

Scope exclusion: Stationary fuel-cell sets, off-road industrial equipment, and aftermarket retrofit kits are not counted.

Segmentation Overview

- By Vehicle Type

- Passenger Cars

- Commercial Vehicles

- By Fuel-cell Type

- Proton-Exchange-Membrane (PEM)

- Solid-Oxide (SOFC) Range-Extenders

- By Power Rating

- Less than 100 kW

- 100 to 200 kW

- More than 200 kW

- By Component

- Fuel-cell Stack

- Balance-of-Plant

- Hydrogen Storage

- Power-Electronics & E-Drive

- Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- Turkey

- Egypt

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured discussions with OEM power-train engineers, stack suppliers, hydrogen station operators, and fleet managers across Asia-Pacific, Europe, and North America. These exchanges clarified true sale prices, warranty terms, and likely production run rates, and helped us vet early adoption projections in regions where public statistics lag.

Desk Research

We drew baseline volumes and pricing from open data sets that track hydrogen mobility, such as the US DOE's AFDC station census, Europe's H2Mobility rollout maps, China MIIT new-energy vehicle production logs, OICA road-vehicle statistics, and annual delivery tallies released by national transport agencies. Policy targets and incentive values were verified through sources such as the IEA Global Hydrogen Review, ACEA automotive position papers, and parliamentary budget acts. Corporate disclosures (10-Ks, annual reports, investor decks) delivered cost curves and model launch calendars, which our analysts accessed through D&B Hoovers and Dow Jones Factiva. The sources noted here are illustrative; many others fed into data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down reconstruction starts with country-level FCV registrations and stock, adjusts for scrappage, then multiplies by segment-specific average selling prices to produce current-year value. Select bottom-up checks, stack shipment roll-ups, sampled dealer transaction data, and channel audits are used to calibrate totals. Key variables fed into the model include 1) annual hydrogen station count, 2) announced FCV model launches, 3) average platinum loading cost per kW, 4) national ZEV purchase incentives, 5) median mileage per FCV class, and 6) regional stack durability benchmarks. A multivariate regression anchored to those six drivers generates the 2026-2030 forecast band, with scenario analysis around policy risk. Data gaps in bottom-up inputs are bridged by applying median regional ASPs to verified unit flows.

Data Validation & Update Cycle

Outputs pass three layers of variance and plausibility checks before sign-off. Senior reviewers compare model signals with independent indicators such as hydrogen sales volumes and OEM order backlogs. The report refreshes every twelve months, and an interim update is triggered when material events, policy shifts, cost breakthroughs, and major plant openings move any key variable.

Why Mordor's Fuel Cell Vehicle Baseline Is Dependable

Published estimates differ. They often stem from contrasting scopes, uneven update rhythms, or bold assumptions around hydrogen roll-out.

Key gap drivers include whether buses and heavy trucks are bundled with passenger cars, the treatment of fleet subsidies in ASP calculations, currency conversion timing, and how quickly stack cost declines are embedded.

Mordor Intelligence reports only vehicles proven to be in commercial sale, applies mid-year exchange rates, and refreshes the model annually, which tempers hype-driven swings.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.26 B (2025) | Mordor Intelligence | - |

| USD 1.92 B (2023) | Global Consultancy A | Includes fuel-cell buses plus planned prototypes and applies forward pricing without discounting to sale year |

| USD 0.20 B (2024) | Trade Journal B | Counts only hydrogen passenger cars, excludes Asia fleet purchases, and uses list prices rather than transaction values |

| USD 1.90 B (2024) | Regional Consultancy C | Projects rapid policy uptake across all regions without adjusting for infrastructure readiness |

In sum, by anchoring values to verified registrations, using tempered cost paths, and revisiting assumptions each year, Mordor Intelligence supplies decision-makers with a balanced, reproducible baseline they can cite with confidence.

Key Questions Answered in the Report

What is the current size of the fuel cell vehicle market and its growth projections?

The fuel cell vehicle market is valued at USD 1.64 billion in 2026 and is projected to reach USD 6.16 billion by 2031, exhibiting a compound annual growth rate of 30.27% during the forecast period 2026-2031.

Which vehicle segment is driving the fastest growth in the fuel cell vehicle market?

Commercial vehicles represent the fastest-growing segment with a 47.10% CAGR through 2031, despite holding only 28.46% of current market share.

Which power rating segment is experiencing the strongest growth?

Power ratings above 200 kW demonstrate the fastest growth at 49.40% CAGR through 2031

Which region leads the fuel cell vehicle market?

Asia-Pacific dominates with 52.60% market share in 2025.

Page last updated on: