Automotive Fuel Injection Pump Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 10.39 Billion |

| Market Size (2030) | USD 9.48 Billion |

| Growth Rate (2025 - 2030) | -1.82% CAGR |

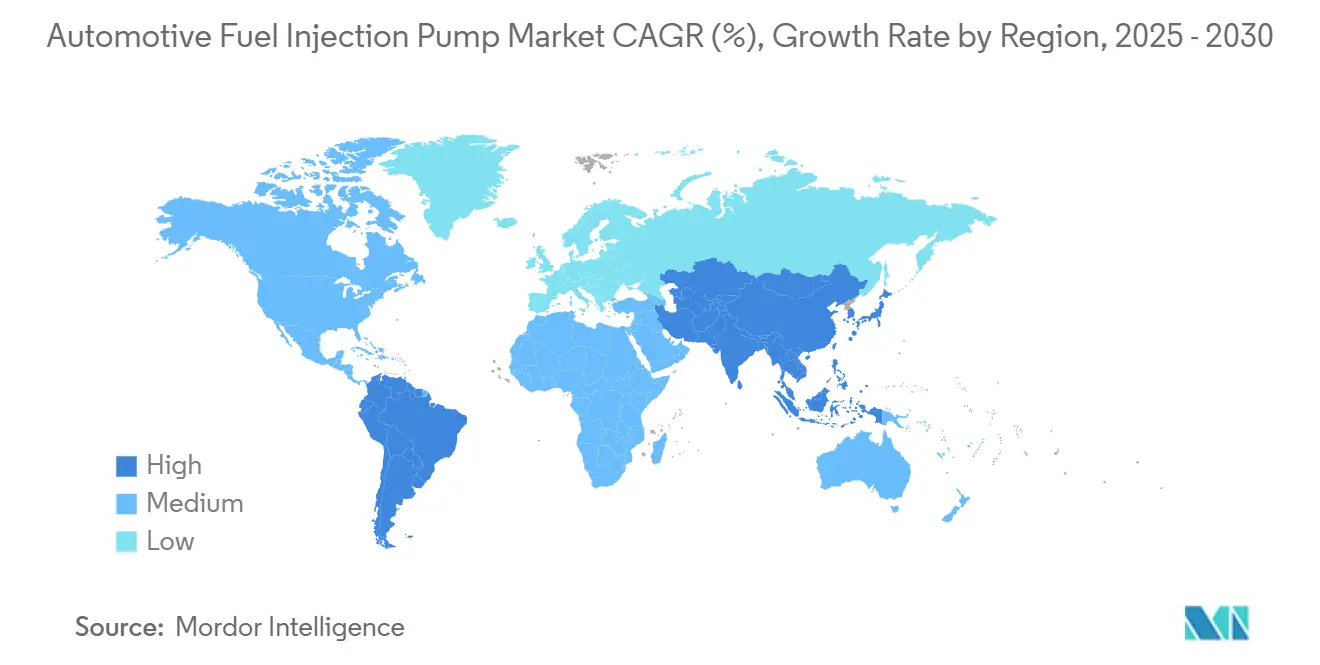

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

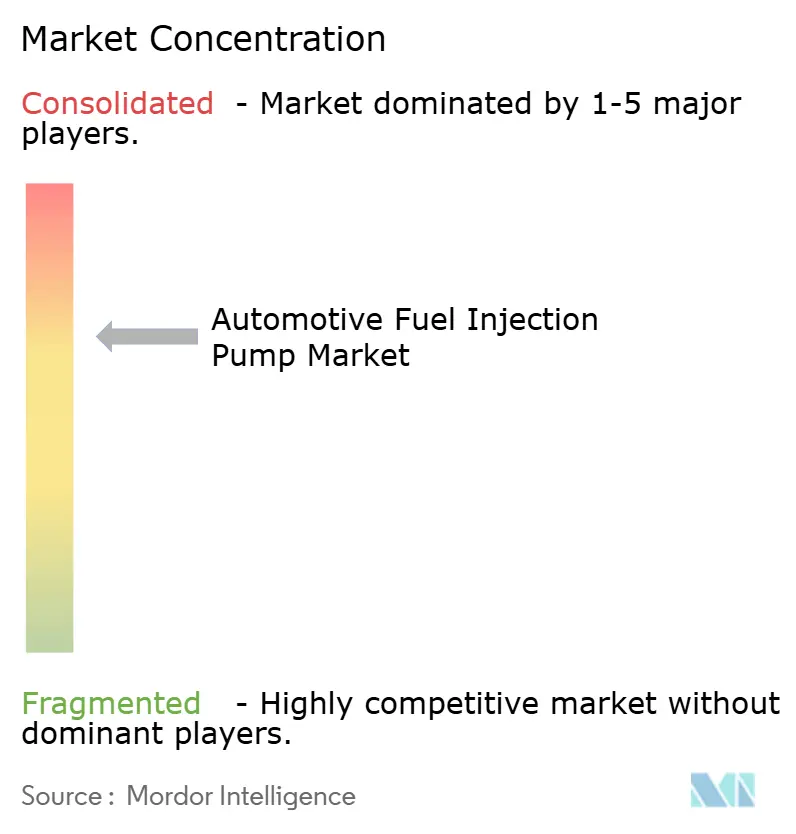

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Fuel Injection Pump Market Analysis by Mordor Intelligence

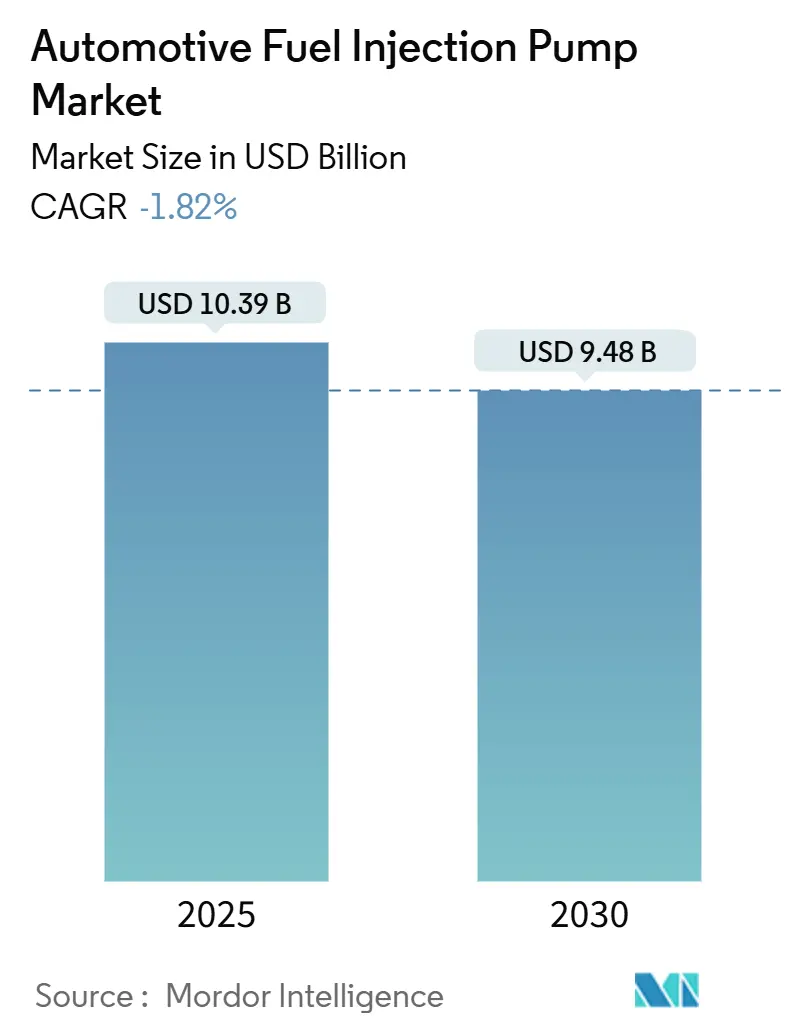

The automotive fuel injection pump market size sits at USD 10.39 billion in 2025 and is forecast to contract to USD 9.48 billion by 2030, translating into a –1.82% CAGR over the period. A deepening shift toward battery-electric vehicles is the primary drag, yet regional manufacturing momentum, stricter emission standards, and alternative-fuel innovation continue to generate pockets of opportunity. Common rail technology remains the dominant architecture because it supports Euro 7-level injection pressures, while gasoline direct injection (GDI) uptake, hybrid powertrains, and hydrogen-ready designs all help slow the retreat. Competition revolves around fuel-agnostic platforms that let OEMs reuse core engine blocks and swap pump modules as fuel choices evolve. Suppliers who can meet 2,500 bar pressure targets, handle biodiesel, HVO, and e-fuels, and still offer attractive cost curves are best placed to defend revenue as the transition unfolds.

Key Report Takeaways

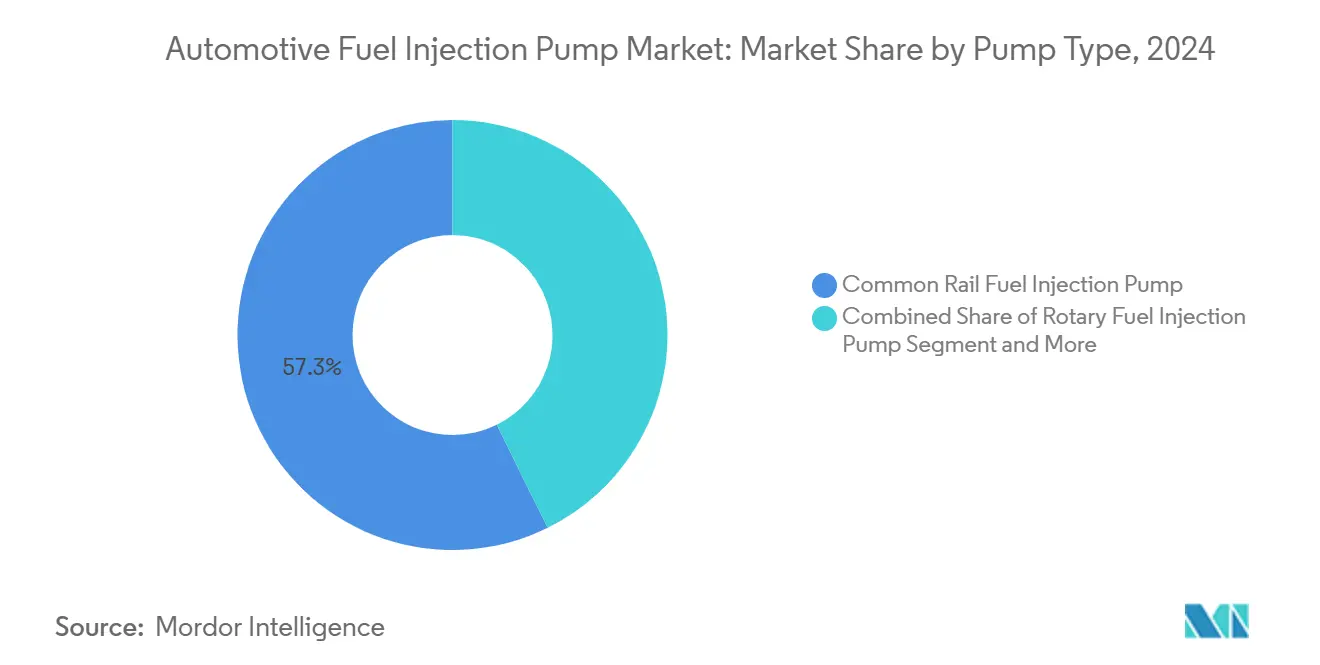

- By pump type, common rail units led with 57.33% of the automotive fuel injection pump market share in 2024, and are advancing at a 0.78% CAGR through 2030

- By pressure type, high-pressure systems accounted for 66.11% of the automotive fuel injection pump market share in 2024 and are advancing at a 0.96% CAGR through 2030.

- By application, direct injection systems captured 71.33% of the automotive fuel injection pump market share in 2024 and posted the fastest 1.15% CAGR to 2030.

- By fuel type, diesel retained a 56.13% of the automotive fuel injection pump market share in 2024, while gasoline exhibited the quickest 0.88% CAGR through 2030.

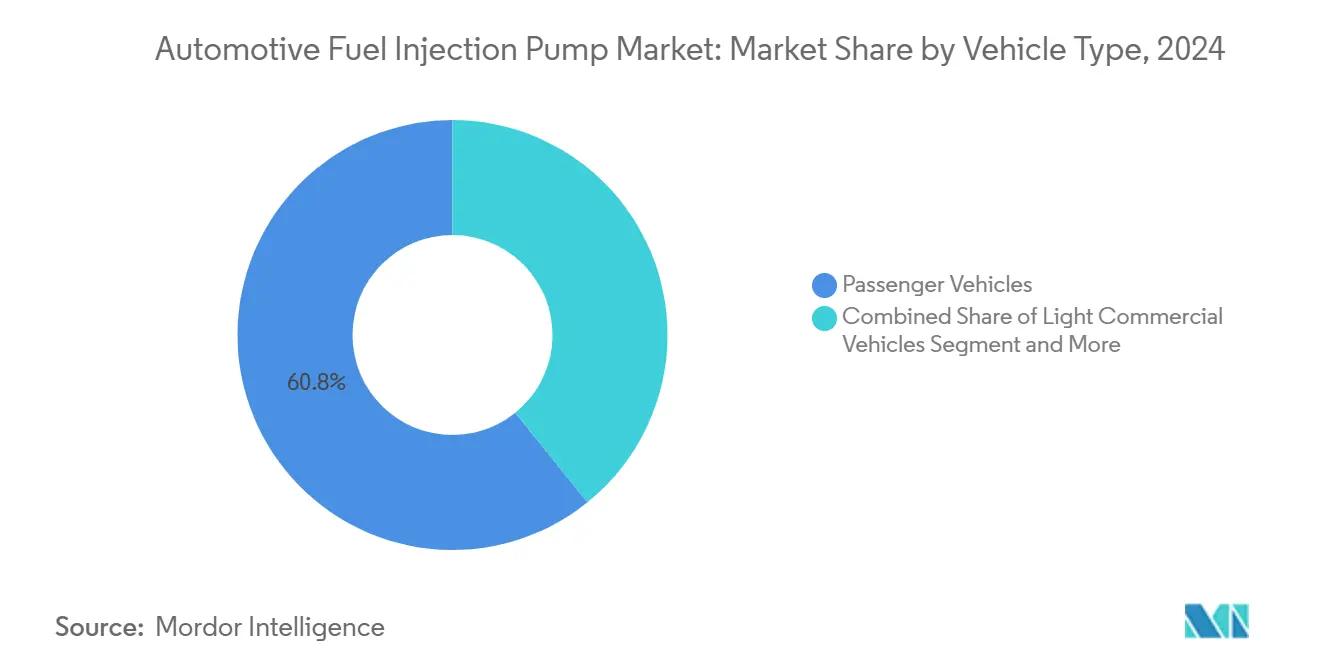

- By vehicle type, passenger cars held 60.84% of the automotive fuel injection pump market share in 2024, and are projected to expand at a 0.52% CAGR through 2030.

- By distribution channel, OEMs dominated with 73.15% of the automotive fuel injection pump market share in 2024; however, the aftermarket is the only segment expanding, recording a 0.54% CAGR to 2030.

- By geography, Asia-Pacific held a 46.25% of the automotive fuel injection pump market share in 2024 and will continue with the fastest growth of 1.44% by 2030.

Market Trends and Insights

Drivers Impact Analysis of Automotive Fuel Injection Pump Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Global Emission Regulations | +0.8% | EU, North America, Asia-Pacific | Medium term (2-4 years) |

| Rising GDI Passenger-Car Production | +0.6% | Asia-Pacific | Short term (≤ 2 years) |

| Demand for Downsized Turbo Engines | +0.5% | Europe, North America, Asia-Pacific | Short term (≤ 2 years) |

| Hybrid-Vehicle Electrified Pumps Demand | +0.4% | Global | Medium term (2-4 years) |

| Hydrogen-Ready High-Pressure Pump R&D | +0.3% | Europe, Asia-Pacific | Long term (≥ 4 years) |

| AI-Enabled Fleet Predictive Maintenance | +0.2% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Global Emission Regulations

Euro 7 caps NOx at 60 mg/km for gasoline and diesel engines and doubles durability to 200,000 km, forcing OEMs to adopt pumps capable of 2,500 bar injection pressures. Continental’s direct-drive piezo injectors remove hydraulic lag and support up to seven injections per combustion cycle, bolstering efficiency under the new rules[1]“Piezo Injector Technology,” Continental AG, continental.com. Heavy-duty applications face onboard monitoring mandates integrating pump control with after-treatment diagnostics, pushing suppliers toward complete system expertise. Because the standard is fuel-neutral, the automotive fuel injection pump market is relevant even as electrification rises. The regulation also creates a standard global template, allowing platforms designed for Europe to scale into other emission-tightening regions.

Rising GDI Passenger-Car Production in Asia

China produced 31.28 million vehicles in 2024, of which roughly 18.4 million still had internal combustion capability. GDI adoption across Asian nameplates leverages local cost advantages in precision machining and electronics. DENSO’s HP5 dual-cylinder pumps with pre-stroke valves exemplify technology pushed from Japan into wider regional supply chains. The ecosystem is robust enough to deliver fourth-generation pumps at scale, keeping Asia-Pacific the largest and fastest-growing territory despite global contraction. Production clustering also shortens lead times, insulating regional OEMs from supply-chain shocks felt elsewhere.

Demand for Downsized Turbo-Turbo Engines

OEMs use twin-scroll and electrically actuated turbochargers to raise power density in smaller displacement blocks, necessitating precise fuel metering to avoid knock and particulate spikes [2]“Turbocharger Contract Extensions,” BorgWarner, borgwarner.com. Electrically actuated wastegates, for instance, demand millisecond-level fuel flow response that only advanced common rail pumps provide. Variable cam timing marries with turbo boost, further tightening injector-pump synchronization. Carter’s high-pressure GDI pumps already support Ford EcoBoost and GM EcoTec arrays that capitalize on this synergy. The downsizing trend shields the automotive fuel injection pump market from a steeper volume drop by adding complexity-based value even as total ICE units taper.

Hybrid-Vehicle Electrified Pumps Demand

Forty-eight-volt mild hybrids employ electrically driven coolant and fuel pumps that reduce parasitic losses while expanding the controllable operating envelope. Cummins’ HELM architecture showcases how a common engine block can simply switch from diesel to natural gas or hydrogen by replacing the above-head gasket fuel-injection hardware [3]“HELM Fuel-Agnostic Platform,” Cummins Inc., cummins.com. Because hybrids still rely on combustion for part-load operation, premium high-pressure pumps remain indispensable. Vitesco’s systems analysis points to deeper pump-thermal module integration, offering additional revenue layers for suppliers. The value-add offsets shrinking pure ICE volumes and keeps pump ASPs elevated.

Restraints Impact Analysis of Automotive Fuel Injection Pump Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating EV Penetration | –2.8% | Europe, China, Global | Short term (≤ 2 years) |

| High Cost And Complexity Of HP Pumps | –0.6% | Global | Medium term (2-4 years) |

| Precision Component Supply-Chain Risks | –0.4% | Global | Short term (≤ 2 years) |

| Shortage Of Skilled Pump Technicians | –0.3% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating EV Penetration

China built 12.9 million new-energy vehicles in 2024, evidencing a 35.5% annual rise that cannibalizes ICE demand. The rapid shift diverts OEM R&D funding to batteries and inverters, leaving fewer new combustion programs to amortize pump development costs. Vitesco identifies axial-flux motors and integrated X-in-1 e-drives as mainstream within five years, accelerating the pivot. While heavy-duty sectors lag, the sheer scale of passenger-car electrification imposes the steepest demand erosion on the automotive fuel injection pump market.

High Cost and Complexity of HP Pumps

Fourth-generation common-rail systems run at 250 MPa and include embedded logic, driving unit prices up while making field repairs nearly impossible; failed modules must be replaced outright. Continental builds piezo stacks under clean-room conditions, stacking over 300 ceramic plates that demand tight dielectric tolerances. Liebherr’s LP11.6 diesel pump offers 15,000-hour life but requires precision-ground eccentric rollers and oil-lubricated housings, straining capital budgets for smaller OEMs. As volumes fall, economies of scale shrink and the cost per unit rises, depressing margins across the chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Automotive Fuel Injection Pump Market Segment Analysis

By Pump Type:

Common Rail Dominance Drives Technology EvolutionCommon rail units held 57.33% of the automotive fuel injection pump market share in 2024 and are expected to post a modest 0.78% CAGR through 2030. Their ability to deliver fuel at variable pressures up to 2,500 bar underpins Euro 7 compliance, keeping them entrenched in passenger cars and heavy-duty trucks. DENSO’s HP5 series, featuring dual-cylinder designs and pre-stroke valves, shows how suppliers refine pressure stability while reducing parasitic losses. Bosch counters with its CPN6 and CP9 families serving heavy engines, while CP4 variants cover light commercial needs.

Rotary pumps still appeal in off-highway and marine engines where electronic complexity is a liability. Liebherr’s oil-lubricated eccentric roller concept extends service life and allows reversible rotation, making it popular in genset applications. In-cylinder configurations aid small motorcycle and compact engine packaging, whereas outside-cylinder units simplify maintenance in big-bore platforms. Fuel-agnostic architectures, like Cummins’ HELM, gain favor by permitting diesel, LNG, or hydrogen swapping with minimal hardware changes. This flexibility injects resilience into the automotive fuel injection pump market, even as absolute volumes erode.

By Pressure Type:

High-Pressure Systems Enable Emissions ComplianceHigh-pressure assemblies owned 66.11% of the automotive fuel injection pump market size in 2024 and should grow 0.96% annually to 2030. Continental’s direct-drive piezo injectors, benchmarked to 2,500 bar, illustrate why OEMs favor high-pressure circuits for precise spray atomization. Woodward’s dual-fuel injectors extend the concept to ammonia and methanol up to 700 bar, supporting maritime and large stationary engines.

Low-pressure pumps persist in older architectures and cost-sensitive regions. Yet even there, Euro-equivalent rules nudge pressures upward, gradually cannibalizing the low-pressure share. Cummins redesigned its X15 pump with opposing pistons to mitigate camshaft wear, underscoring ongoing innovation in the high-pressure realm. Suppliers pairing metal-matrix composites, DLC coatings, and tight clearances can charge premium pricing, which results in revenue loss from unit decline.

By Application:

Direct Injection Systems Lead Efficiency GainsDirect injection captured 71.33% of the automotive fuel injection pump market size in 2024 and logs the highest 1.15% CAGR to 2030. Carter supplies high-pressure GDI pumps for Ford EcoBoost and GM EcoTec lines, highlighting broad OEM endorsement. Transonic Combustion’s super-critical injection pursues spark-less ignition to drive even leaner burn profiles.

Multi-point fuel injection lingers in emerging markets where cost trumps efficiency gains. Even so, DENSO’s i-ART injectors insert electronic brains into each valve body, achieving per-cylinder corrections that shrink emission variability. Hybrid drivetrains also favor direct injection because rapid heat release aids engine-off restart smoothness, reinforcing segment leadership through the transition.

By Fuel Type:

Gasoline Growth Offsets Diesel DeclineDiesel will still command 56.13% of the automotive fuel injection pump market in 2024, but gasoline will enjoy a quicker 0.88% CAGR as European diesel backlash and tighter particulate caps bite. Fischer-Tropsch and HVO blends reach near-parity energy density, encouraging fleets to remix without hardware overhaul. Cummins' HELM allows the same block to pivot between diesel and natural gas or hydrogen, depending on injector and pump swap-outs.

Alternative fuels, though small, rise fastest. Woodward's 250-bar hydrogen rail and Bosch's lube-free injector prototype target this niche. Pumps must now handle alcohol corrosion, biodiesel viscosity, and hydrogen embrittlement, pressuring suppliers to broaden metallurgy and seal offerings. Those capabilities insulate revenue as diesel volume shrinks.

By Vehicle Type:

Passenger Vehicles Drive Volume Despite ElectrificationPassenger vehicles retained 60.84% of the automotive fuel injection pump market share in 2024 and will grow with a 0.52% CAGR, buoyed by hybrids in Europe and emerging-market ICE sales. BorgWarner secured turbocharger contracts for midsize and large SUVs into 2028, implying continuing pump pull-through. Light commercial vans benefit from last-mile e-commerce growth yet still favor diesel for payload range, extending pump life.

Medium and heavy trucks lean on Cummins’ X15 HELM, capable of B20 biodiesel or 100% renewable diesel without power loss. Off-highway equipment, from tractors to excavators, remains strongly diesel-centric, offering a decades-long aftermarket tail. Thus, pump suppliers preserve meaningful scale across diversified vehicle classes despite EV acceleration.

By Distribution Channel:

Aftermarket Resilience Supports Service DemandOEM installations delivered 73.15% of the automotive fuel injection pump market share in 2024, but the aftermarket is the sole segment growing at a 0.54% CAGR. Continental added 700 high-pressure fuel pump part numbers in 2024-2025, raising average vehicle coverage by 50%. Independent diesel shops note marine injector cleaning takes twice the parts and 50% more labor versus on-highway units, lifting ticket value.

The complexity of fourth-gen common rail means many units are now “replace-only,” funneling profits to OE-authorized dealers. DPF cleaning bundles and pump service raise customer spending while ensuring emissions compliance. As electrified fleets age, specialized hybrid pump modules will add another aftermarket layer, sustaining parts demand beyond initial ICE decline.

Geography Analysis

APAC Automotive Fuel Injection Pump Market

Asia-Pacific held 46.25% of the automotive fuel injection pump market share in 2024 and posted the sole positive 1.44% CAGR through 2030. China’s 18.4 million ICE-capable vehicles signal a large installed base needing pumps despite rising EV sales. Japanese suppliers such as DENSO and Hitachi Astemo export fourth-generation pumps regionally, while India’s component roadmap targets USD 100 billion exports by 2030, securing future scale.

North America Automotive Fuel Injection Pump Market

North America shows flat volumes yet steady value as pickups, SUVs, and heavy trucks maintain combustion relevance. Cummins builds X15 HELM engines in New York and is trialing variable-speed natural-gas variants with Liberty Energy for fracking fleets. Regulatory proposals remain technology-neutral, leaving room for low-carbon fuels that still need high-pressure pumps.

Europe Automotive Fuel Injection Pump Market

Europe faces the steepest volume drop but leads in technical sophistication. Continental’s Limbach-Oberfrohna site surpassed 40 million piezo injectors by 2024, showing depth in ultra-high-precision manufacturing. Euro 7’s July 2025 start keeps pump R&D active, and the region champions HVO, e-diesel, and hydrogen ICE pilots that sustain niche demand. Liebherr’s Deggendorf plant sends common-rail pumps worldwide for large engines, converting European know-how into export revenue.

Competitive Landscape

The automotive fuel injection pump market remains top-heavy: Bosch, DENSO, and Continental capture a significant share, while Cummins, Delphi-Phinia, and BorgWarner round out the leading cohort. Bosch spans passenger to heavy applications with CP and HDP families and is betting on hydrogen injectors to anchor its post-diesel roadmap. DENSO’s i-ART embedded intelligence gives it a data-rich moat and supports self-tuning combustion, appealing to fleet uptime goals.

Niche specialists flourish in alternative fuels. Woodward’s dual-fuel maritime injectors and Hoerbiger’s hydrogen systems aim at hard-to-electrify sectors. Lumax Auto’s 2024 acquisition of Greenfuel Energy Solutions signals new entrants hedging bets on CNG and hydrogen delivery modules.

Continental’s aftermarket push diversifies revenue as OE volumes slip, while BorgWarner’s turbo-pump integration locks in future combustion programs. The prevailing strategy is to straddle legacy ICE profits and emergent fuel niches without overcommitting to any single pathway.

Automotive Fuel Injection Pump Industry Leaders

Robert Bosch GmbH

Denso Corporation

Continental AG

BorgWarner Inc. (Phinia Inc.)

Hitachi Astemo Ltd.

- *Disclaimer: Major Players sorted in no particular order

Automotive Fuel Injection Pump Market Companies Covered in this Report

- Robert Bosch GmbH

- Denso Corporation

- Continental AG

- Hitachi Astemo Ltd.

- Aisin Corporation

- Stanadyne LLC

- Cummins Inc.

- Woodward Inc.

- Weifu Group

- BorgWarner Inc. (Phinia Inc.)

- Magna International Inc.

- Mikuni Corporation

- SHW AG

- Marelli Holdings

Recent Industry Developments in Automotive Fuel Injection Pump Market

- January 2025: The U.S. National Highway Traffic Safety Administration reported that Ford recalled over 295,000 Super Duty F-Series trucks due to biodiesel deposits on high-pressure fuel-pump rollers that could cause pump failure.

- January 2024: Standard Motor Products expanded its gasoline fuel-injection program to more than 2,100 SKUs, adding high-pressure pumps, modules, and ancillary components for full repair solutions.

Global Automotive Fuel Injection Pump Market Report Scope

Segmentation Overview

| Common Rail Fuel Injection Pump |

| Rotary Fuel Injection Pump |

| In-Cylinder Pump |

| Outside-Cylinder Pump |

| Low Pressure |

| High Pressure |

| Direct Injection System |

| Multi-Point Fuel Injection System |

| Gasoline |

| Diesel |

| Alternative Fuels |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Pump Type | Common Rail Fuel Injection Pump | |

| Rotary Fuel Injection Pump | ||

| In-Cylinder Pump | ||

| Outside-Cylinder Pump | ||

| By Pressure Type | Low Pressure | |

| High Pressure | ||

| By Application | Direct Injection System | |

| Multi-Point Fuel Injection System | ||

| By Fuel Type | Gasoline | |

| Diesel | ||

| Alternative Fuels | ||

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What CAGR is forecast for automotive fuel injection pumps between 2025 and 2030?

The market is projected to contract at -1.82% CAGR, dropping from USD 10.39 billion in 2025 to USD 9.48 billion by 2030.

Which pump type holds the largest share today?

Common rail pumps command 57.33% of global demand, thanks to precision metering and emissions compliance advantages.

Why is Asia-Pacific still growing while the global market shrinks?

China’s large ICE and hybrid production base, coupled with cost-efficient regional supply chains, drives a 1.44% CAGR even as other regions plateau.

How will Euro 7 affect fuel injection technology?

Euro 7 requires up to 2,500 bar rail pressure and more injection events per cycle, accelerating adoption of piezo injectors and high-pressure pumps.

Page last updated on: