Furnace Filters Market Size and Share

Market Overview

| Study Period | 2023 - 2031 |

|---|---|

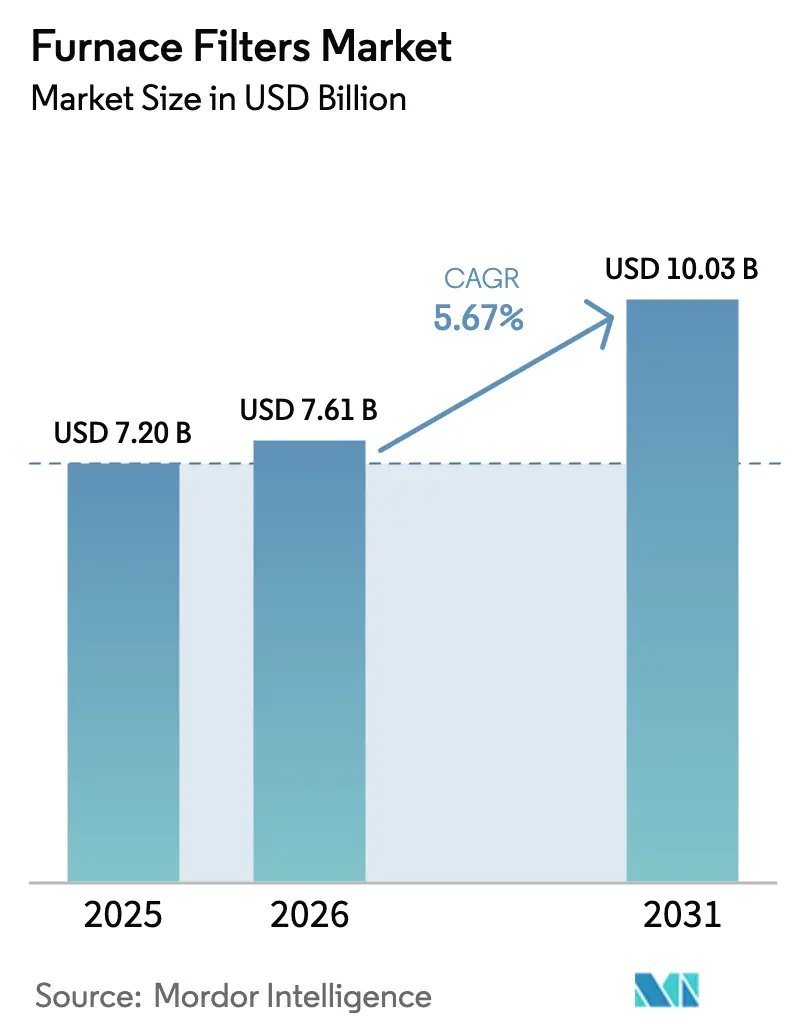

| Market Size (2026) | USD 7.61 Billion |

| Market Size (2031) | USD 10.03 Billion |

| Growth Rate (2026 - 2031) | 5.67% CAGR |

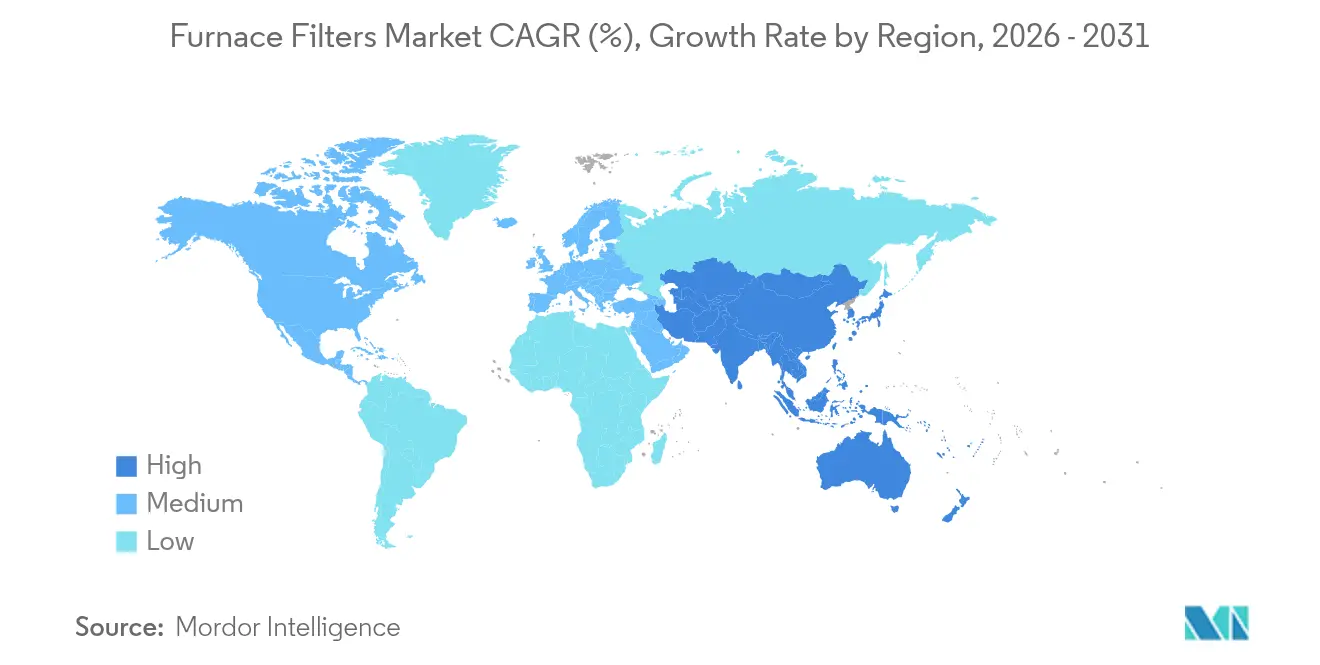

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

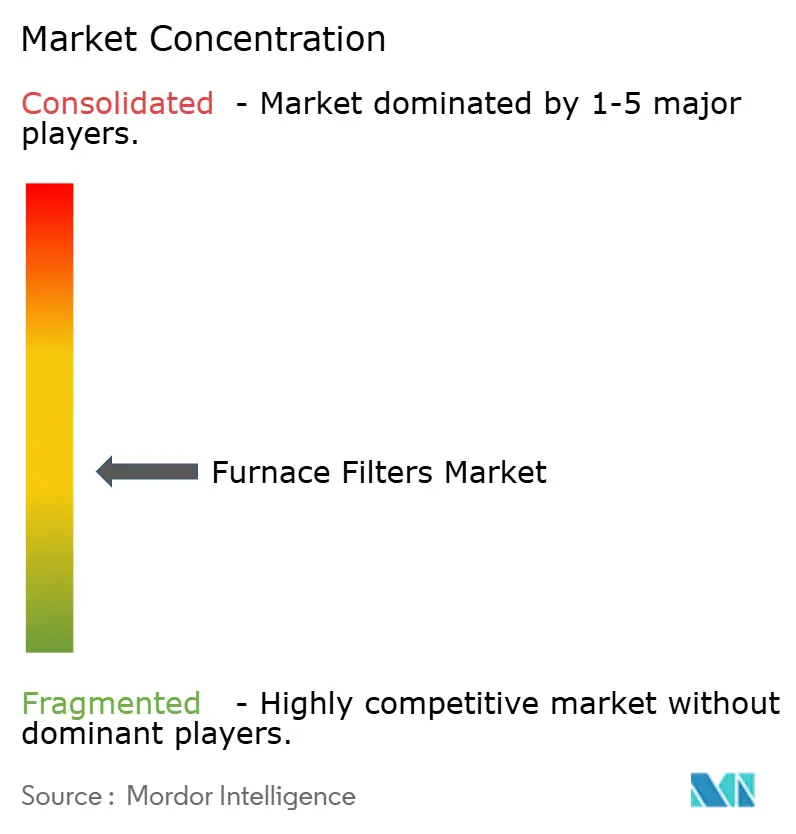

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Furnace Filters Market Analysis by Mordor Intelligence

The furnace filters market size was valued at USD 7.2 billion in 2025 and estimated to grow from USD 7.61 billion in 2026 to reach USD 10.03 billion by 2031, at a CAGR of 5.67% during the forecast period (2026-2031). Heightened indoor-air-quality (IAQ) regulations, the rapid shift to MERV 13-plus standards, and heat-pump electrification programs anchor this expansion. Product demand also rises as wild-fire smoke events shorten replacement cycles, while subscription e-commerce models deepen consumer engagement. On the supply side, synthetic-media innovation supports higher efficiency at lower pressure drop, yet price volatility in petroleum-based inputs strains margins. Meanwhile, consolidation gathers pace as HVAC majors integrate filter specialists to secure technology, distribution, and recurring revenue streams.

Key Report Takeaways

- By furnace type, gas furnaces led with 45.38% of the furnace filters market share in 2025; heat pump/hybrid systems are projected to post the fastest 8.05% CAGR through 2031.

- By MERV rating, MERV 5-8 media captured 37.92% of the furnace filters market size in 2025, while the MERV 13-16 and HEPA tier is forecast to climb at a 9.42% CAGR to 2031.

- By end user, residential applications held 56.65% revenue share in 2025; industrial facilities are expanding at a 7.28% CAGR to 2031.

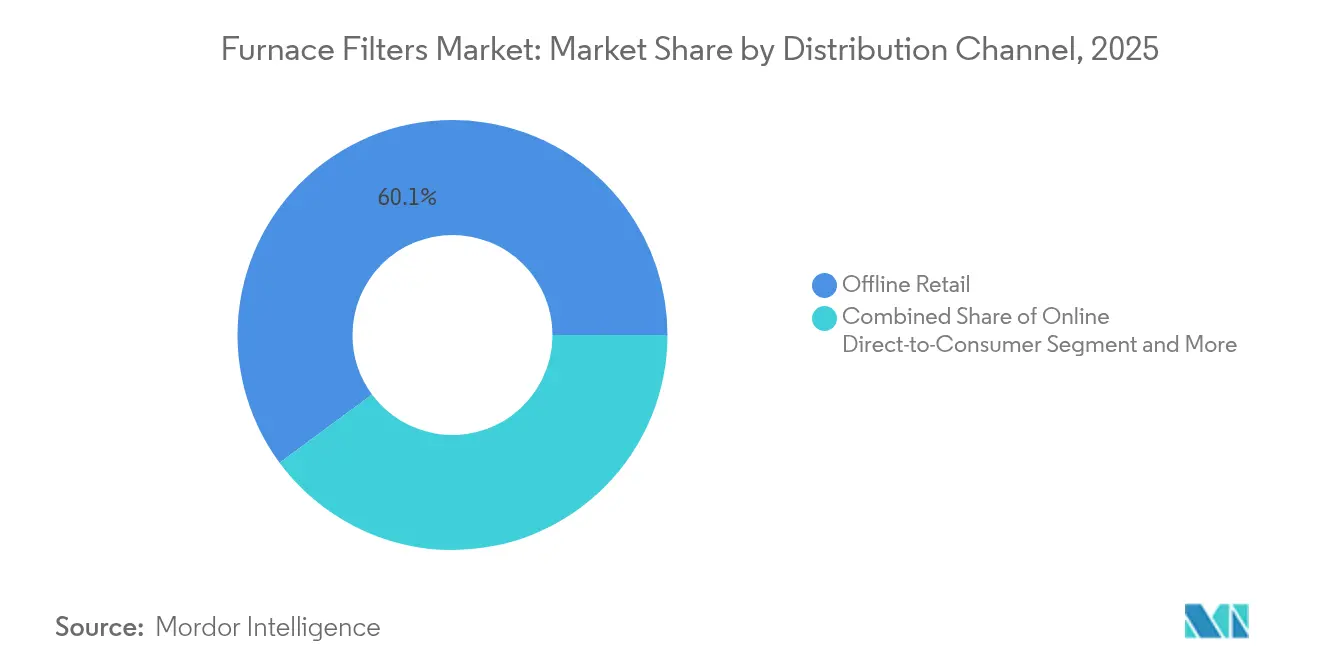

- By distribution channel, offline retail accounted for 60.12% of the furnace filters market size in 2025; subscription services record the highest 9.55% CAGR through 2031.

- By region, North America contributed 36.72% of 2025 revenue; Asia–Pacific is advancing at a 7.74% CAGR through 2031.

- Honeywell, 3M (Filtrete), and Nordic Pure collectively commanded a low-double-digit share of global sales in 2024, underscoring a moderately fragmented competitive field.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Furnace Filters Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing focus on indoor air quality (IAQ) | 1.8% | Global, with concentration in North America and EU | Medium term (2-4 years) |

| Surge in energy-efficient HVAC retrofits | 1.2% | North America and EU core, spill-over to APAC | Medium term (2-4 years) |

| Stricter IAQ and MERV mandates in building codes | 1.5% | North America and EU, emerging in APAC | Long term (≥ 4 years) |

| Heat-pump conversions requiring higher-grade filters | 0.9% | Global, led by North America and China | Long term (≥ 4 years) |

| Wild-fire smoke events boosting replacement frequency | 0.6% | North America West Coast, Australia, Southern Europe | Short term (≤ 2 years) |

| Subscription e-commerce filter services driving volume | 0.4% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Focus on Indoor Air Quality (IAQ)

ASHRAE Standard 241 formalized pathogen-control benchmarks that compel commercial buildings to install MERV 13-plus filters capable of removing nearly 90% of sub-micron particles.[1]David Krause, “ASHRAE Issues Standard 241 for Pathogen Mitigation,” lumalier.com U.S. healthcare facilities already follow OSHA guidance that specifies MERV 13 or higher, a requirement now influencing residential buyers who increasingly link filtration to respiratory health. Wild-fire smoke episodes across the western United States further demonstrate the limitations of legacy MERV 8 products, prompting rapid upgrade cycles.[2]O’Connor Company Technical Note, “MERV 13 vs. MERV 8 Filtration Efficiency,” ocp.com Pharmaceutical production in India and China also fuels demand for high-efficiency media that meet clean-room thresholds. As IAQ awareness rises, building owners view premium filters less as discretionary purchases and more as risk-mitigation tools.

Surge in Energy-Efficient HVAC Retrofits

Federal and state decarbonization incentives encourage property owners to swap dated packaged units for variable-refrigerant-flow and heat-pump systems. These retrofits specify deeper 4-inch media filters that retain MERV 13 performance without excessive pressure drop. Massachusetts regulations now require a 70% enthalpy-recovery ratio in ventilation systems, indirectly lifting demand for low-resistance filters that protect energy gains.[3]Systemair Engineering Bulletin, “Enthalpy Recovery and Filter Selection,” systemair.com As older buildings align with new energy codes, contractors bundle premium filters into rebate-eligible upgrade kits, generating multi-year pull-through revenue for filter suppliers.

Stricter IAQ and MERV Mandates in Building Codes

California’s building code obliges all mechanically ventilated spaces to use a minimum MERV 13 filter and to ensure zero bypass through sealed racks, raising compliance hurdles. Similar directives surface in the European Union where LEED and BREEAM scoring weight filtration performance. Sweden’s shift from plastic to steel frames illustrates regulators’ attention to lifecycle waste, giving established brands with certified products a competitive edge. As multinational firms harmonize global facility standards, higher-efficiency filters become baseline specifications even in jurisdictions without formal mandates.

Heat-Pump Conversions Requiring Higher-Grade Filters

Heat pumps circulate larger air volumes year-round, making them sensitive to airflow restriction. Manufacturers therefore prescribe 4- or 5-inch pleated synthetic filters that hold more dust at MERV 13 efficiency than a thin fiberglass mat. China, which produces one-quarter of global heat pumps, sets filtration requirements that resonate worldwide as export brands standardize on these specifications. Electrification policies in California and the European Union accelerate heat-pump adoption, shortening replacement intervals and lifting consumable sales.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High life-cycle maintenance cost | -0.8% | Global, particularly price-sensitive residential markets | Medium term (2-4 years) |

| Raw-material price volatility (synthetic media) | -0.6% | Global manufacturing, acute in Asia-Pacific | Short term (≤ 2 years) |

| Mini-split adoption (filterless HVAC) | -0.4% | APAC core, expanding to North America and EU | Long term (≥ 4 years) |

| Sustainability push against disposable filters | -0.3% | EU and North America, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Life-Cycle Maintenance Cost

MERV 13 filters cost roughly three to four times more than fiberglass options and load faster, raising annual replacement outlays for households to beyond USD 200. In commercial towers with dozens of air handlers, filter procurement and labor fees reach thousands per year. Elevated energy draw—15-20% higher fan power at comparable airflow—further inflates operating budgets. While subscription platforms smooth monthly payments, total cost often rises versus retail channels, limiting upgrade rates in emerging economies where capital preservation outweighs IAQ priorities.

Raw-Material Price Volatility (Synthetic Media)

Polypropylene and polyester prices swing 30-40% year-on-year as crude-oil benchmarks and freight costs gyrate. The heavy concentration of melt-blown production in China magnifies exposure to regional outages. US tariffs on selected imports compound unpredictability, while steel and aluminum frame costs climb in tandem with global construction demand. Smaller filter makers lacking hedging programs see margin compression when raw-material inflation outpaces price increases, constraining product innovation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Furnace Type: Gas Dominance Faces Heat Pump Challenge

Gas furnaces accounted for 45.38% of the furnace filters market in 2025, underpinned by a vast installed base across North American homes. In contrast, the furnace filters market size linked to heat pump or hybrid systems is projected to grow at an 8.05% CAGR, reflecting electrification incentives that narrow operating-cost gaps. Oil furnaces persist only in geographies lacking pipeline gas, while electric resistance units occupy small niches.

Year-round heat pump operation mandates deeper MERV 13 media to avoid airflow penalties, raising unit revenue per install. Gas models retain standard 1-inch pleated filters, but regulatory convergence will gradually lift their efficiency requirements. As the EPA phases out R-410A, contractors stress system cleanliness, reinforcing demand for premium filters that capture installation debris and safeguard compressors.

By MERV Rating: Regulatory Push Elevates Performance Standards

With a 37.92% share in 2025, MERV 5-8 filters remain common in low-risk residential settings; however, the furnace filters market size for MERV 13-16 and HEPA products is advancing at a 9.42% CAGR through 2031. Smoke events and pandemic-era health messaging make higher ratings the de facto choice for new builds.

Wild-fire prone regions adopt specialty media engineered to maintain efficiency despite extreme particle loading. Healthcare and clean-manufacturing customers set procurement baselines at MERV 13, a threshold now filtering into retail offerings. Mid-range MERV 9-12 options serve cost-conscious users upgrading in steps, though policy tightening could compress this transitional category.

By End User: Industrial Growth Outpaces Residential Demand

Residential buyers represented 56.65% revenue in 2025, but industrial consumption is outpacing at a 7.28% CAGR as pharmaceutical, semiconductor, and food-processing plants tighten contamination controls. The furnace filters market share for institutional and commercial buildings also rises as ASHRAE 241 compliance becomes standard lease language.

Factories deploy differential-pressure sensors to trigger filter changeouts, creating predictable reorder schedules and supporting vendor-managed inventory programs. Residential demand shifts toward subscription deliveries that remind households to replace filters on time, reducing HVAC energy waste and premature fan failures.

By Distribution Channel: Digital Transformation Accelerates

Offline DIY chains and HVAC wholesalers still moved 60.12% of units in 2025, yet e-commerce gains traction through detailed sizing tools and same-day shipping. Subscription portals post a 9.55% CAGR, the highest among channels, as homeowners embrace “set-and-forget” replenishment that arrives before filters clog.

Contractor portals bundle filters with coil cleaners and thermostats at negotiated rates, reinforcing wholesale relevance. Direct-to-consumer brands differentiate through educational content and MERV-rating explainers, nudging buyers toward premium tiers and enlarging average order value.

By Filter Media: Synthetic Innovation Drives Performance

Manufacturers favor pleated synthetic media for its superior dust-holding capacity and bacterial resistance. Fiberglass retains a foothold where price sensitivity eclipses performance, notably in rental units. Electrostatic washable filters appeal to environmentally minded buyers despite higher upfront cost.

Innovations such as 3M’s metal-free frame reduce landfill waste by 3.5 million pounds annually while maintaining rigidity. Nanofiber overlays from MANN+HUMMEL boost capture efficiency at lower pressure drop but remain premium-priced. Biodegradable protein-based media research hints at future disposability breakthroughs that could redefine end-of-life protocols.

Geography Analysis

North America generated 36.72% of global revenue in 2025, buoyed by stringent energy codes that require MERV 13 filters in new construction and major retrofits. Wild-fire smoke across California, Oregon, and British Columbia shortens replacement cycles and lifts unit volumes. The region also leads subscription adoption, as brands like FilterBuy dominate automated delivery programs.

Asia–Pacific is the fastest-growing territory with a 7.74% CAGR through 2031. India’s HVAC market is trending toward USD 30 billion by 2030, creating substantial downstream pull for filter suppliers aligned with the Production Linked Incentive scheme. China’s control of more than one-quarter of global heat-pump sales sets filtration standards that ripple worldwide. Japan and South Korea impose strict IAQ limits in dense urban high-rises, cementing MERV 13-plus adoption.

Europe posts steady gains on the back of Green Deal energy directives and escalating carbon tariffs. Sweden’s steel-frame mandate signals the bloc’s wider push for recyclable materials, while Germany advances subsidy programs for heat-pump retrofits. The Middle East and Africa begin to surface on supplier radars as Saudi Arabia’s Vision 2030 funds large-scale building projects requiring advanced HVAC systems.

Competitive Landscape

The furnace filters market features moderate fragmentation; the top ten suppliers hold well under half of global sales. Strategic acquisitions accelerate as OEMs seek vertical integration: Daikin’s USD 430 million purchase of Flanders Holdings bolstered its industrial-grade portfolio, and Rheem’s move for Fujitsu’s HVAC business extends its installed base. Private-equity interest rises, attracted by the sector’s recurring-replacement model and regulatory tailwinds.

Technology differentiation intensifies around smart filters that alert users to pressure thresholds. 3M’s refillable frame promises a 20-year lifespan, slashing waste and recurring frame cost. Metalmark addresses wild-fire smoke with the first purpose-built MERV 13 filter validated for extreme PM2.5 environments.

Subscription commerce has become a competitive battleground. Nordic Pure leverages direct customer education, while Honeywell experiments with bundled smart thermostats and filter-reorder capabilities. Smaller innovators target heat-pump airflow challenges and biodegradable media niches, compelling incumbents to accelerate R&D and sustainability pledges.

Furnace Filters Industry Leaders

Honeywell

3M Company

MANN+HUMMEL GmbH

Lennox International Inc.

AprilAire LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Thermo Fisher Scientific agreed to acquire Solventum’s Purification & Filtration unit for USD 4.1 billion, expanding its bioprocessing filtration footprint.

- February 2025: Filtration Technology Corporation added 55,000 square feet of capacity, launching the Invicta cartridge line aimed at energy-efficient HVAC projects.

- January 2025: Metalmark introduced the Sierra™ Air Filter, the first MERV 13 filter optimized for wild-fire smoke mitigation.

- January 2025: Rheem’s parent company moved to buy Fujitsu’s HVAC assets for USD 1.6 billion, broadening system specifications that influence filter requirements.

Global Furnace Filters Market Report Scope

Furnace filters filter the air by capturing airborne pollutants, such as allergens, pet dander, dust, smog, and even mold spores. They also protect the blower fan from all the dust the return duct pulls in.

The Furnace Filters Market is segmented by Geography (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa). The market size and forecasts are provided in terms of value (in USD) for all the above segments.

| Gas |

| Oil |

| Electric Resistance |

| Heat-Pump / Hybrid |

| MERV 1-4 |

| MERV 5-8 |

| MERV 9-12 |

| MERV 13-16 and HEPA |

| Residential |

| Commercial |

| Industrial |

| Offline Retail (DIY Stores, HVAC Wholesalers) |

| Online Direct-to-Consumer |

| Subscription Services |

| Fiberglass |

| Pleated Synthetic |

| Electrostatic |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Furnace Type | Gas | ||

| Oil | |||

| Electric Resistance | |||

| Heat-Pump / Hybrid | |||

| By MERV Rating | MERV 1-4 | ||

| MERV 5-8 | |||

| MERV 9-12 | |||

| MERV 13-16 and HEPA | |||

| By End User | Residential | ||

| Commercial | |||

| Industrial | |||

| By Distribution Channel | Offline Retail (DIY Stores, HVAC Wholesalers) | ||

| Online Direct-to-Consumer | |||

| Subscription Services | |||

| By Filter Media | Fiberglass | ||

| Pleated Synthetic | |||

| Electrostatic | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the furnace filters market?

The market is valued at USD 7.61 billion in 2026 and is forecast to reach USD 10.03 billion by 2031.

Which segment is growing fastest within the furnace filters market?

Heat pump/hybrid systems lead growth at an 8.05% CAGR, driven by electrification incentives and building-decarbonization policies.

Which is the fastest growing region in Furnace Filters Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

How do MERV 13 filters differ from MERV 8 products?

MERV 13 filters capture nearly 90% of particles between 0.3 µm and 1 µm, compared with roughly 35% for MERV 8, offering superior IAQ but at higher cost and pressure drop.

Why are subscription services gaining traction?

Automated deliveries ensure on-time replacements, which improve HVAC efficiency and reduce energy bills, supporting the channel’s 9.55% CAGR.

Which region offers the highest growth potential?

Asia–Pacific shows the fastest expansion at a 7.74% CAGR through 2031, led by India’s HVAC build-out and China’s heat-pump leadership.

What impact do raw-material prices have on filter costs?

Volatility in polypropylene, polyester, and metal prices can swing input costs by 30–40%, compressing margins and influencing retail pricing cycles.

Page last updated on: