United States HVAC Equipment And Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

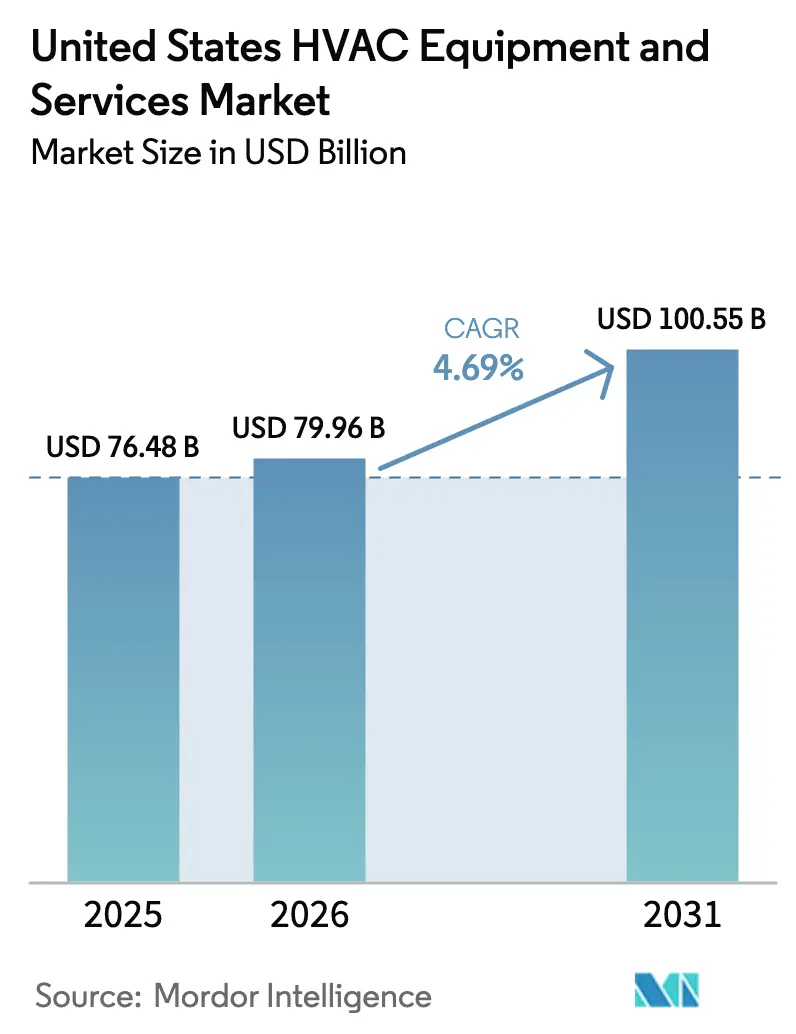

| Base Year Market Size (2025) | USD 76.48 Billion |

| Market Size (2026) | USD 79.96 Billion |

| Market Size (2031) | USD 100.55 Billion |

| Growth Rate (2026 - 2031) | 4.69% CAGR |

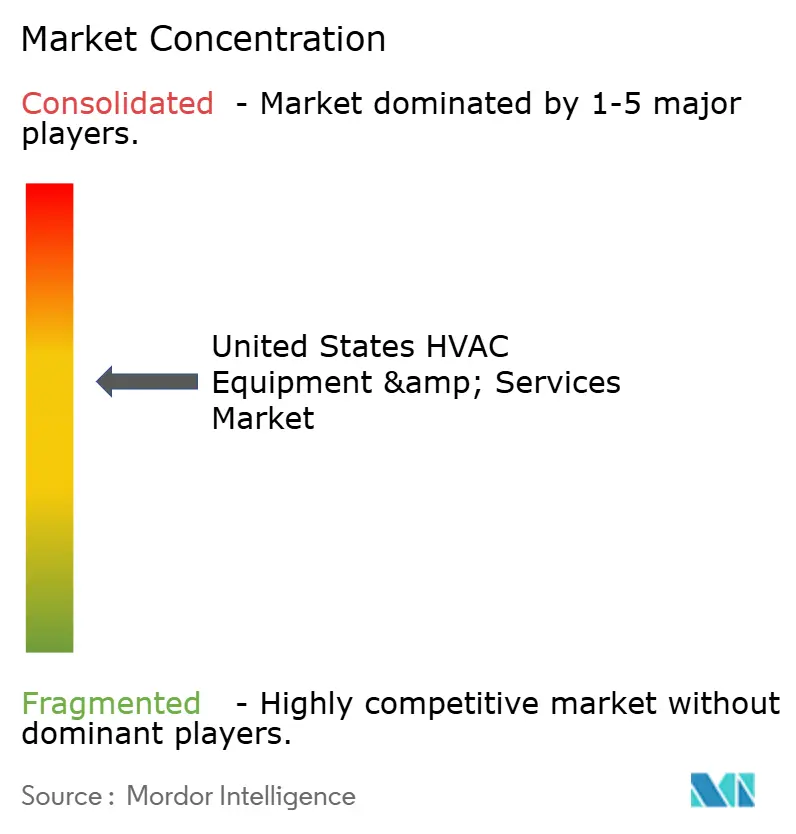

| Market Concentration | Medium |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States HVAC Equipment And Services Market Analysis by Mordor Intelligence

The United States HVAC Equipment and Services Market size is projected to be USD 76.48 billion in 2025, USD 79.96 billion in 2026, and reach USD 100.55 billion by 2031, growing at a CAGR of 4.69% from 2026 to 2031. This growth profile signals a mature industry in which regulatory compliance, federal incentives, and replacement cycles outrank new‐build demand as primary volume drivers. Tax credits of up to USD 2,000 for qualifying heat pumps, combined with sizable state rebate programs, sharply reduce payback periods and tip customer choice toward high-efficiency equipment.[1]Internal Revenue Service, “Air Source Heat Pumps Tax Credit,” energystar.gov Mandatory hydrofluorocarbon phase-downs reshape product roadmaps as manufacturers move to A2L refrigerants and accelerate R-410A system retirements.[2]Environmental Protection Agency, “Phasedown of Hydrofluorocarbons,” federalregister.gov Simultaneously, extreme heat events in southern states lengthen cooling seasons and lift service runtimes, partly offsetting tempered heater turnover in milder regions. Intensifying grid modernization efforts create adjacent opportunities for smart thermostats and connected HVAC platforms that enable demand-response value pools.

Key Report Takeaways

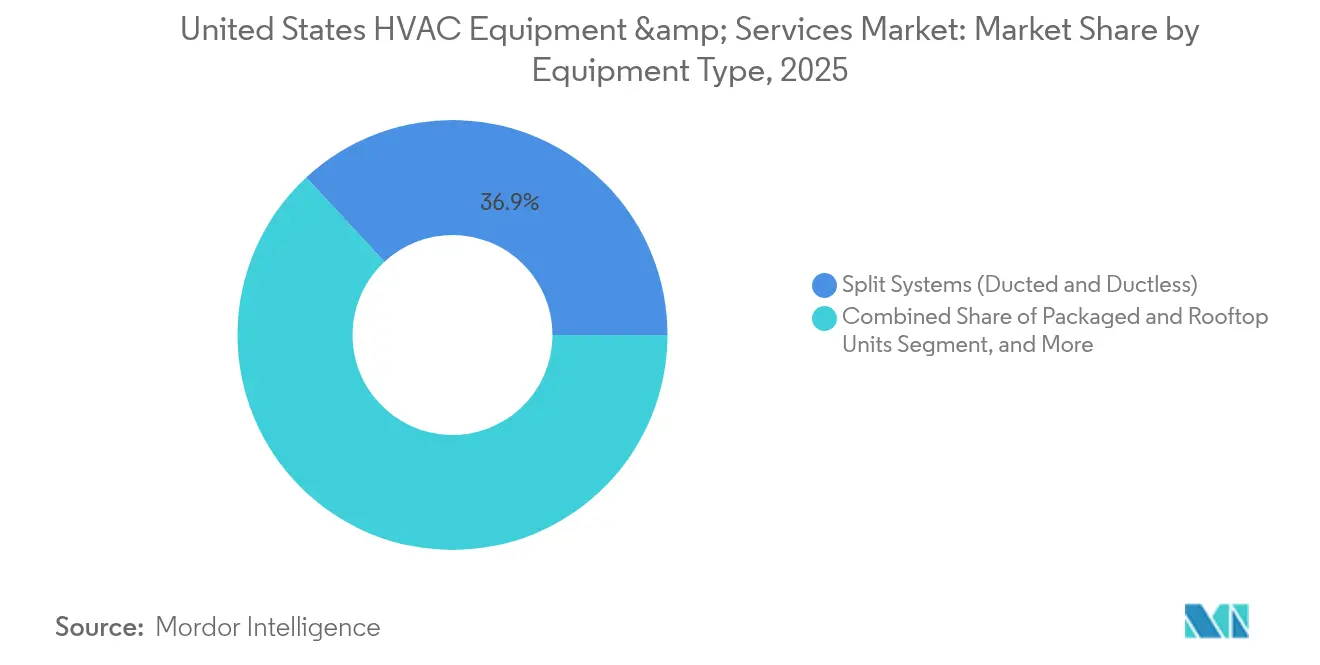

- By equipment type, split systems led with 36.92% revenue share in 2025, while heat pumps recorded the fastest 5.89% CAGR through 2031.

- By service type, new installations contributed 43.62% of revenue in 2025; retrofits and replacements are projected to expand at a 5.74% CAGR to 2031.

- By distribution channel, wholesalers held 49.02% share in 2025, whereas online platforms post the highest 9.08% CAGR over the forecast window.

- By end user, residential customers accounted for 55.21% revenue share in 2025; data centers exhibit the fastest 6.91% CAGR through 2031.

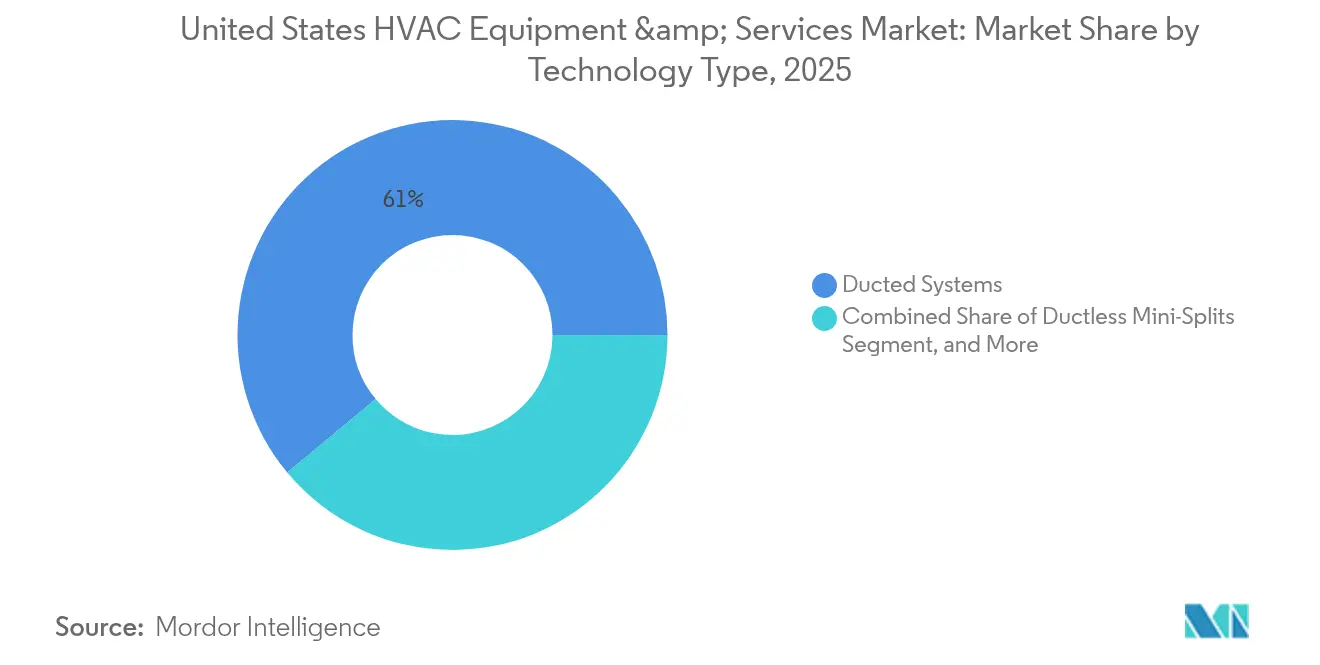

- By technology, ducted systems maintained 61.05% share in 2025; smart and connected HVAC solutions are advancing at an 8.37% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States HVAC Equipment And Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal incentives for high-efficiency HVAC upgrades | +0.8% | National, with higher adoption in California, New York, Washington | Medium term (2-4 years) |

| Mandatory refrigerant phase-downs accelerating equipment replacement | +0.6% | National, with commercial sector leading adoption | Short term (≤ 2 years) |

| Southern heat-wave frequency boosting cooling demand | +0.4% | Southern states, particularly Texas, Florida, Arizona | Long term (≥ 4 years) |

| Building-electrification mandates in key states | +0.3% | California, New York, Washington, Massachusetts | Medium term (2-4 years) |

| IoT-enabled predictive-maintenance cost savings | +0.2% | Commercial and industrial segments nationwide | Medium term (2-4 years) |

| Growth of data-center cooling load | +0.1% | Technology hubs in Virginia, Texas, California, Oregon | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Federal Incentives for High-Efficiency HVAC Upgrades

Federal tax credits covering up to USD 2,000 for qualified heat pump systems, extended through 2032 under the Inflation Reduction Act, are changing total-cost-of-ownership calculations for homeowners and small businesses. The USD 4.5 billion High-Efficiency Electric Home Rebate Program targets low- and moderate-income households, offering rebates up to USD 8,000 and stacking with state programs to offset as much as 70% of installed cost. Nine states have pledged to secure 65% heat-pump penetration by 2030, signaling a coordinated policy push that compresses decision cycles.[3]NESCAUM, “Nine States Pledge Joint Action to Accelerate Transition to Clean Buildings,” nescaum.org California’s TECH Clean California program augments the federal incentives with contractor training and technical assistance, reducing soft costs that often derail projects. Collectively, these measures shorten payback periods to fewer than five years for average households, propelling heat pump adoption in the United States HVAC Equipment and Services market.

Mandatory Refrigerant Phase-Downs Accelerating Equipment Replacement

The American Innovation and Manufacturing Act restricts new HVAC systems to refrigerants under 700 GWP starting January 2025, prompting an abrupt shift away from R-410A. Manufacturers have converted assembly lines to A2L refrigerants such as R-454B and R-32 while deploying technician safety programs to address mild flammability characteristics. Rapid switchover drives a pronounced replacement spike and channels capital toward compliant solutions despite material cost inflation. Early adopters benefit from reduced lifecycle emissions, aiding ESG compliance for corporate buyers. With A2L systems already representing more than 60% of new residential shipments, the United States HVAC Equipment and Services market is realigning its product mix toward low-GWP offerings well ahead of the statutory deadline.

Southern Heat-Wave Frequency Boosting Cooling Demand

Record heat waves drove peak demand surges of 15-20% across southern grids in 2024, and meteorological forecasts indicate above-normal temperatures again in 2025. Extended cooling seasons increase compressor runtimes, hastening system wear and promoting early replacements. Utilities such as TXU Energy are enlarging demand-response programs, paying up to USD 150 for smart thermostat enrollment that curbs peak loads. Elevated runtime hours also improve the value proposition for variable-speed compressors and advanced controls that trim operating costs, stimulating technology-rich retrofits in the United States HVAC Equipment and Services market.

Building-Electrification Mandates in Key States

California’s building codes will require electric heat pumps in all new construction from January 2026, charting deployment of 500,000 units within three years. New York and Washington have adopted parallel measures, and combined policies now affect nearly one quarter of the national population. These mandates create captive demand streams for high-efficiency electric systems, widening the service addressable market for contractors and OEMs. Ancillary rebate programs targeting existing stock further accelerate heat-pump uptake in retrofit applications, lifting the mid-term outlook for the United States HVAC Equipment and Services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging HFC-alternative refrigerant prices | -0.4% | National, with commercial sector most affected | Short term (≤ 2 years) |

| Skilled-labor shortages inflating install costs | -0.3% | National, with rural areas most severely impacted | Medium term (2-4 years) |

| Rising electricity tariffs dampening HVAC run-time | -0.2% | Regional variations, highest impact in California, Northeast | Medium term (2-4 years) |

| Volatility of steel and copper input costs | -0.1% | National, affecting all equipment manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging HFC-Alternative Refrigerant Prices

Prices for R-454B have climbed from USD 17 to USD 60 per pound, adding USD 3,000-5,000 to the cost of large commercial systems and transferring roughly USD 25 billion of incremental expense to end users since 2024. Supply remains heavily dependent on imports from China, exposing the market to geopolitical risks and freight volatility. Limited domestic production capacity constrains availability during the regulatory transition, forcing contractors to pre-purchase inventory and strain working capital. Larger refrigerant charges in chillers and VRF systems intensify the effect on commercial buyers, delaying some projects despite compelling efficiency gains.

Skilled-Labor Shortages Inflating Install Costs

The industry counts more than 110,000 open technician positions, with experienced workers retiring faster than apprentices complete multi-year training pipelines. Labor scarcity elevates installation lead times and wage pressures, raising project costs and occasionally missing utility incentive deadlines. Rural areas feel the impact most severely, where technician travel adds expenses and weakens service coverage. The shortage also dampens the pace of heat-pump rollouts because installers need new certifications to handle flammable A2L refrigerants safely. Companies offering in-house training gain competitive leverage but cannot fully close the skills gap before the mid-term horizon.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment: Heat Pumps Propel Electrification Momentum

Heat pumps represent the fastest-expanding equipment class at a 5.89% CAGR through 2031 as incentives and decarbonization policies redirect budgets toward electric heating solutions. Split systems retain dominance with 36.92% revenue share in 2025 due to entrenched dealer familiarity and broad SKU variety. However, their growth moderates as households and light commercial sites migrate to dual-function heat pumps. Packaged and rooftop units remain staples for quick-turn commercial retrofits, particularly in retail strip centers and low-rise offices that value plug-and-play replacement. Chillers continue to anchor large central plants in hospitals, universities, and manufacturing sites that demand tight temperature controls. VRF solutions gain traction in medium-size offices and hospitality because zone-level modulation slashes part-load energy use. Air-handling units, fan coils, and coils support these core systems, with demand linked to the trajectory of ducted versus ductless architectures.

Heat-pump technological diversity from ducted split to ductless mini-split, hybrid, and geothermal configurations broadens addressable climates. Advancements in variable-speed inverters allow cold-climate models to deliver 100% heating capacity at 5 °F, expanding relevance across the northern tier. Furnaces still dominate in the coldest rural markets but face a measured share decline as homeowner economics improve for dual-fuel or all-electric packages. Window and through-the-wall units serve legacy multifamily buildings and temporary structures, yet their share erodes as compact mini-splits provide superior seasonal efficiency. Boilers continue to underpin hydronic heating in institutions and older high-rise assets where radiant distribution exists. Ancillary air-quality equipment such as humidifiers and dehumidifiers grew steadily after pandemic-era awareness, though they remain supplementary revenue streams rather than volume drivers. The resulting portfolio mix underscores a gradual but clear pivot toward electric, variable-speed heat-pump platforms within the United States HVAC Equipment and Services market.

By Service Type: Retrofit Activity Outpaces New Construction

New installations commanded 43.62% of 2025 revenue, fueled by ongoing commercial fit-outs and residential new-builds. Yet retrofit and replacement workstreams are set to grow more quickly, expanding at a 5.74% CAGR as regulatory and efficiency triggers pull forward system changeouts. Ageing HVAC fleets average 15-20 years in service, and new refrigerant rules now make many R-410A units technically obsolete once major repairs arise. End users are increasingly attracted to turnkey upgrade packages that combine equipment changeouts with utility rebates, financing, and predictive-maintenance subscriptions.

Maintenance contracts remain stable anchor revenue, but digital tools are reshaping execution practices. Cloud-based diagnostics detect anomalies early, allowing service providers to shift from reactive dispatches to scheduled interventions that minimize downtime. Performance-based service agreements, in which contractors share verified energy savings, are gaining traction in municipalities and school districts. Utility demand-response programs augment profitability by creating revenue for capacity curtailment events. These models position service firms as long-term energy partners rather than one-off installers inside the United States HVAC Equipment and Services market.

By Distribution Channel: Digital Platforms Disrupt Price Transparency

Traditional wholesalers controlled 49.02% of shipments in 2025, leveraging credit terms, local inventory, and technical assistance that contractors value. However, online HVAC marketplaces post a 9.08% CAGR as price transparency and rapid shipping appeal to cost-sensitive installers. COVID-19 catalyzed digital adoption; many contractors now source commodity components online and reserve complex system purchases for dedicated reps. OEM direct-sales teams penetrate large commercial and mission-critical segments, bundling advisory engineering and factory commissioning to secure specification loyalty. Retail and DIY outlets target filter replacements, thermostat upgrades, and small ductless kits that homeowners install with minimal professional help.

Hybrid models blend e-commerce convenience with last-mile expertise. Distributors have launched online portals that marry real-time stock data with curbside pickup, minimizing downtime for field crews. Some national wholesalers employ algorithmic pricing that matches internet offers to retain share. As contractors consolidate through private equity rollups, their procurement sophistication rises, further increasing the bargaining power of digital channels within the United States HVAC Equipment and Services market.

By Technology: Connectivity Redefines System Value

Ducted architectures held 61.05% share in 2025 owing to legacy prevalence and familiarity among installers. Ductless mini-splits flourish in retrofit scenarios where duct fabrication is disruptive or cost prohibitive. Hybrid and geothermal heat-pump variants serve premium efficiency niches, attractive to institutional buyers chasing zero-carbon goals. Smart and connected HVAC solutions, advancing at an 8.37% CAGR, embed Wi-Fi thermostats, IoT sensors, and AI algorithms that synchronize operation with occupancy and weather forecasts. Utilities leverage these connected endpoints for virtual power plant (VPP) programs, rewarding building owners for real-time flexibility.

Predictive-maintenance platforms digest vibration, temperature, and current data to diagnose mechanical fatigue up to 90 days in advance, cutting emergency calls by 75%. Machine learning further optimizes setpoints, delivering 20-40% runtime energy savings. As connected device penetration rises, cybersecurity has become a board-level topic, prompting OEMs to certify products under UL-2900. Software subscription models unlock recurring revenue, allowing manufacturers to monetize installed bases beyond initial hardware margin in the United States HVAC Equipment and Services market.

By End User: Data Centers Set the Pace

Residential properties generated 55.21% of 2025 demand, reflecting ongoing replacement cycles and robust single-family construction in southern growth corridors. Commercial buildings trail closely, upgrading outdated HVAC assets to meet tighter codes and tenant sustainability goals. Industrial users deploy specialized chillers and process coolers to safeguard production quality, while institutional clients emphasize air quality alongside cost efficiency to comply with healthcare and educational standards. Data centers, expanding at a 6.91% CAGR, represent the fastest-moving segment as hyperscalers and colocation providers race to satisfy cloud and AI workloads.

Higher rack densities drive liquid and immersion cooling pilots that reduce airflow requirements and free capacity in existing white space. Edge facilities proliferate near population clusters, demanding compact, modular cooling units that installers can set and commission quickly. Data-center operators adopt redundant heat-pump chillers that shift seasonal energy loads between heating and cooling functions. This specialized growth amplifies opportunities for integrators versed in environmentals and controls, strengthening sector diversification in the United States HVAC Equipment and Services market.

Geography Analysis

Regional climate patterns, policy frameworks, and economic conditions create distinct demand clusters within the United States HVAC Equipment and Services market. Southern states, led by Texas and Florida, confront prolonged cooling seasons and frequent heat waves that propel high-efficiency air-conditioning and dual-fuel heat-pump sales. Utility rebates for connected thermostats accelerate smart equipment uptake, and peak-pricing tariffs encourage variable-speed compressors that optimize part-load performance. Rapid population inflows to metropolitan areas such as Austin and Orlando further sustain residential replacement volume.

California wields outsized influence through building-electrification mandates and incentive layering that target 6 million additional heat pumps by 2030. The state already captures 24.12% of national revenue, with early adoption of A2L refrigerants and advanced controls positioning it as a technology bellwether. Pacific Gas and Electric’s VPP initiative aggregates residential HVAC assets into grid-responsive fleets, spotlighting the monetization potential of distributed flexibility.

In the Northeast and Midwest, cold-climate heat-pump prototypes tested under the DOE challenge now sustain full heating capacity at –13 °F, opening electrification pathways where gas furnaces historically dominated. Nine northeastern states pursue a coordinated 65% market penetration goal by 2030, backed by utility rebates that mitigate higher upfront costs. Rural counties face pronounced technician shortages, extending project timelines and occasionally curtailing rebate eligibility windows.

The Pacific Northwest and Rocky Mountain regions show rising VRF adoption for mixed-use complexes where temperate climates favor heat-recovery advantages. Meanwhile, the Southeast commands the nation’s fastest data-center construction pace, with Virginia’s “Data Center Alley” driving demand for precision liquid cooling systems. Across all regions, policy momentum and climate extremes argue for continued investment in efficient, low-GWP, and connected HVAC systems, sustaining steady growth for the United States HVAC Equipment and Services market.

Competitive Landscape

The market exhibits moderate concentration, with the top five manufacturers controlling an estimated 62% of aggregate revenue through diverse portfolios and nationwide dealer networks. Carrier, Trane Technologies, Lennox, and Johnson Controls leverage scale economies to negotiate favorable component pricing and keep channel partners well stocked. Competitive intensity has shifted toward solution ecosystems that bind hardware with software and services. Carrier’s alliance with Google Cloud integrates HVAC, battery storage, and AI guidance into home energy management platforms, broadening Carrier’s value proposition beyond compressors and coils.

Strategic consolidation continues. Samsung and Lennox formed a joint venture to accelerate VRF penetration, combining Samsung inverter expertise with Lennox’s distribution reach. Daikin partnered with Copeland to introduce advanced inverter swing rotary compressors, lifting energy efficiency and positioning for tightened 2025 SEER2 benchmarks. Trane Technologies’ planned purchase of BrainBox AI enhances Trane’s autonomous optimization capabilities, supporting service contracts that guarantee savings.

Innovation pipelines emphasize refrigerant transition and electrification. Mitsubishi Electric Trane’s new R-454B product line shows 78% lower GWP than legacy R-410A while sustaining performance across load points. Daikin Applied’s Trailblazer HP chiller introduces air-sourced heat-pump capability for commercial retrofits, achieving up to 300% heating efficiency and positioning the unit for electrified boiler replacement. Intellectual-property races intensify, illustrated by the Hong Kong University of Science and Technology’s elastic-alloy magnetocaloric breakthroughs promising an order-of-magnitude leap in temperature-change efficiency. Vendors able to translate such lab advances into commercial products could reset industry cost curves.

Utility programs and federal incentives magnify the role of after-sales services, making training and field support differentiators amid a labor crunch. OEMs with accredited technician academies position themselves to capture retrofit waves tied to refrigerant rules, solidifying channel loyalty within the United States HVAC Equipment and Services market.

United States HVAC Equipment And Services Industry Leaders

Daikin Industries Ltd.

Lennox International Inc.

Emerson Electric Company

EMCOR Group

Johnson Controls International plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Daikin Applied unveiled the Trailblazer HP air-cooled scroll chiller with integrated heat-pump functionality, allowing commercial buildings to replace fossil-fuel boilers while achieving up to 300% heating efficiency. The launch aligns with Daikin’s strategy to own electrified heating niches ahead of boiler bans.

- May 2025: Trane Technologies completed the DOE Cold Climate Heat Pump Challenge, validating performance specifications that unlock northern markets and reinforcing the firm’s leadership in high-efficiency innovation.

- May 2025: RectorSeal acquired Aspen Manufacturing to broaden its coil and air-handler catalog, supporting cross-selling within residential retrofits where space constraints dictate custom components.

- March 2025: Carrier Global and Google Cloud announced a strategic partnership to deliver AI-driven home energy management systems that merge HVAC, batteries, and solar analytics, diversifying Carrier’s revenue mix into recurring software.

United States HVAC Equipment And Services Market Report Scope

HVAC equipment is an indoor and vehicular environment comfort technology that provides thermal comfort and acceptable indoor air quality. It is an important part of residential structures, such as single-family homes, apartment buildings, hotels, and senior living facilities, as well as medium-to-large industrial and office buildings, such as hospitals, where safe and healthy building conditions are regulated, with respect to temperature and humidity, using fresh air from outdoors. The report offers a comprehensive analysis of the market segmented by type of HVAC equipment, services, and end-users.

| Split Systems (Ducted and Ductless) |

| Packaged and Rooftop Units |

| Chillers |

| Air-Handling Units |

| Furnaces |

| Fan Coils |

| Window / Through-the-Wall / PTAC |

| Boilers |

| Heat Pumps |

| Humidifiers and Dehumidifiers |

| Variable Refrigerant Flow (VRF) Systems |

| Other Equipment Types |

| New Installations |

| Retrofits / Replacements |

| Maintenance and Repair |

| Demand-Response and Performance Contracting |

| Direct Sales (OEM to End-User) |

| HVAC Distributors / Wholesalers |

| Retail / DIY Stores |

| Online E-commerce Platforms |

| Residential |

| Commercial |

| Industrial |

| Institutional (Healthcare, Education) |

| Other End-users |

| Ducted Systems |

| Ductless Mini-Splits |

| Hybrid / Geothermal Heat-Pump Systems |

| Smart and Connected HVAC |

| By Equipment | Split Systems (Ducted and Ductless) |

| Packaged and Rooftop Units | |

| Chillers | |

| Air-Handling Units | |

| Furnaces | |

| Fan Coils | |

| Window / Through-the-Wall / PTAC | |

| Boilers | |

| Heat Pumps | |

| Humidifiers and Dehumidifiers | |

| Variable Refrigerant Flow (VRF) Systems | |

| Other Equipment Types | |

| By Service Type | New Installations |

| Retrofits / Replacements | |

| Maintenance and Repair | |

| Demand-Response and Performance Contracting | |

| By Distribution Channel | Direct Sales (OEM to End-User) |

| HVAC Distributors / Wholesalers | |

| Retail / DIY Stores | |

| Online E-commerce Platforms | |

| By End User | Residential |

| Commercial | |

| Industrial | |

| Institutional (Healthcare, Education) | |

| Other End-users | |

| By Technology | Ducted Systems |

| Ductless Mini-Splits | |

| Hybrid / Geothermal Heat-Pump Systems | |

| Smart and Connected HVAC |

Key Questions Answered in the Report

What is the current value of the United States HVAC Equipment and Services market?

The market stands at USD 79.96 billion in 2026 and is projected to reach USD 100.55 billion by 2031.

Which equipment segment is growing the fastest?

Heat pumps lead growth with a 5.89% CAGR, buoyed by federal incentives and state electrification mandates.

How will refrigerant regulations affect HVAC investments?

The 2025 A2L requirement compels early replacement of R-410A systems, prompting near-term capex spikes and shifting product demand toward low-GWP solutions.

Why are smart HVAC systems gaining traction?

Connected controls enable utility demand-response participation and predictive maintenance, delivering 20-40% energy savings and reducing downtime.

Where is the strongest regional demand?

Southern states show the highest cooling-driven volumes, while California tops policy-driven electrification spending and the Northeast accelerates cold-climate heat-pump adoption.

What strategic moves define current competition?

Partnerships integrating AI, joint ventures on VRF and compressor technologies, and acquisitions that enhance software capabilities signal a pivot from hardware to solutions-based differentiation.

Page last updated on: