Fuel Cell Powertrain Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

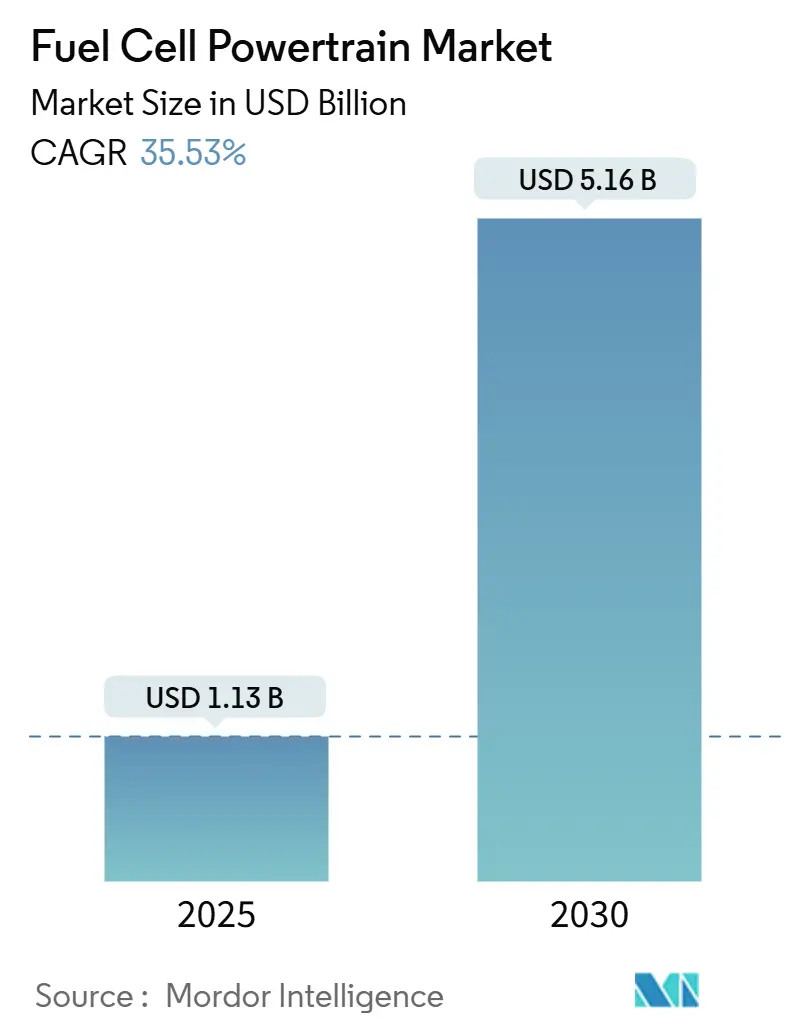

| Market Size (2025) | USD 1.13 Billion |

| Market Size (2030) | USD 5.16 Billion |

| Growth Rate (2025 - 2030) | 35.53% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fuel Cell Powertrain Market Analysis by Mordor Intelligence

The Fuel Cell Powertrain Market size is estimated at USD 1.13 billion in 2025, and is expected to reach USD 5.16 billion by 2030, at a CAGR of 35.53% during the forecast period (2025-2030). Growing regulatory pressure for zero-emission vehicles, rapid cost declines in stack technology, and expanding hydrogen refueling infrastructure propel the fuel cell powertrain market. Government incentives in Asia-Pacific, North America, and Europe have accelerated OEM roll-outs, while breakthrough durability gains extend system lifetimes and compress payback periods. Capital inflows into green-hydrogen projects and strategic alliances between automakers and fuel-cell specialists are lowering technology risk and broadening commercial applications. As cost parity approaches, the fuel cell powertrain market is poised to capture long-haul trucking, heavy-duty fleets, and performance passenger segments that favor quick refueling and high payload capacity.

Key Report Takeaways

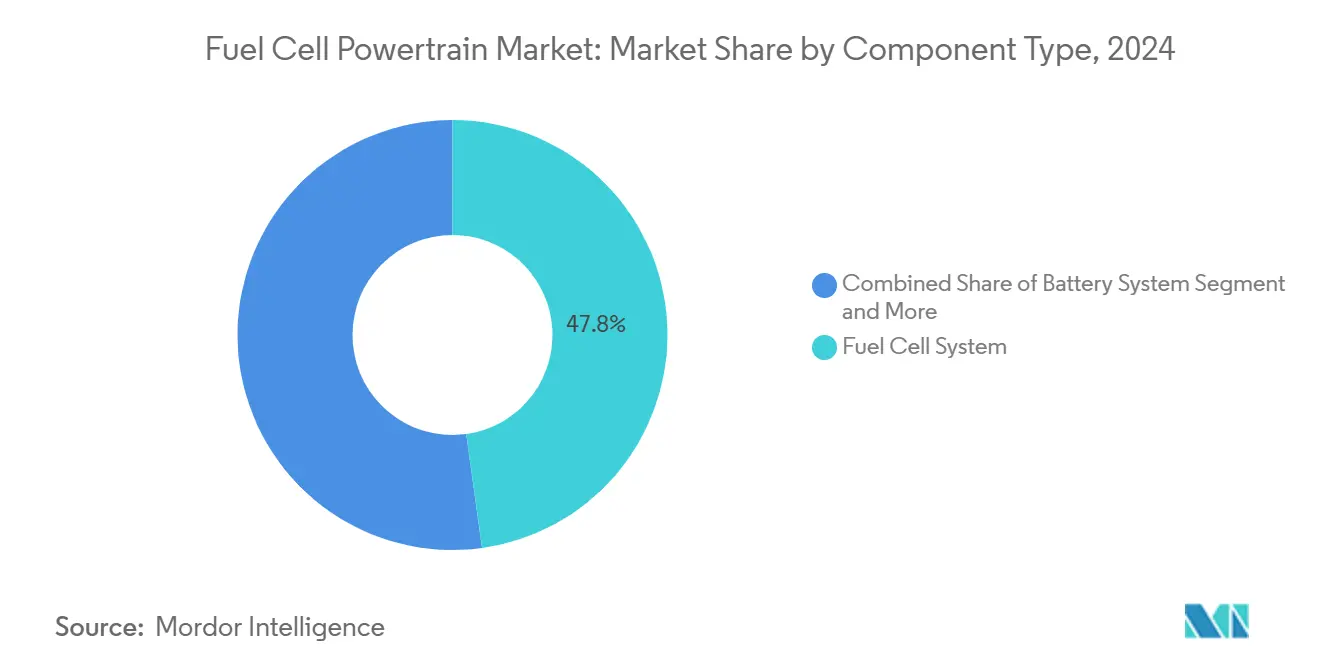

- By component type, fuel cell systems led with a 47.83% fuel cell powertrain market share in 2024, hydrogen storage systems are set to grow at a 35.56% CAGR during the forecast period (2025-2030).

- By drive type, rear-wheel layouts accounted for a 53.41% share of the fuel cell powertrain market in 2024, whereas all-wheel drive is projected to expand at a 35.58% CAGR during the forecast period (2025-2030).

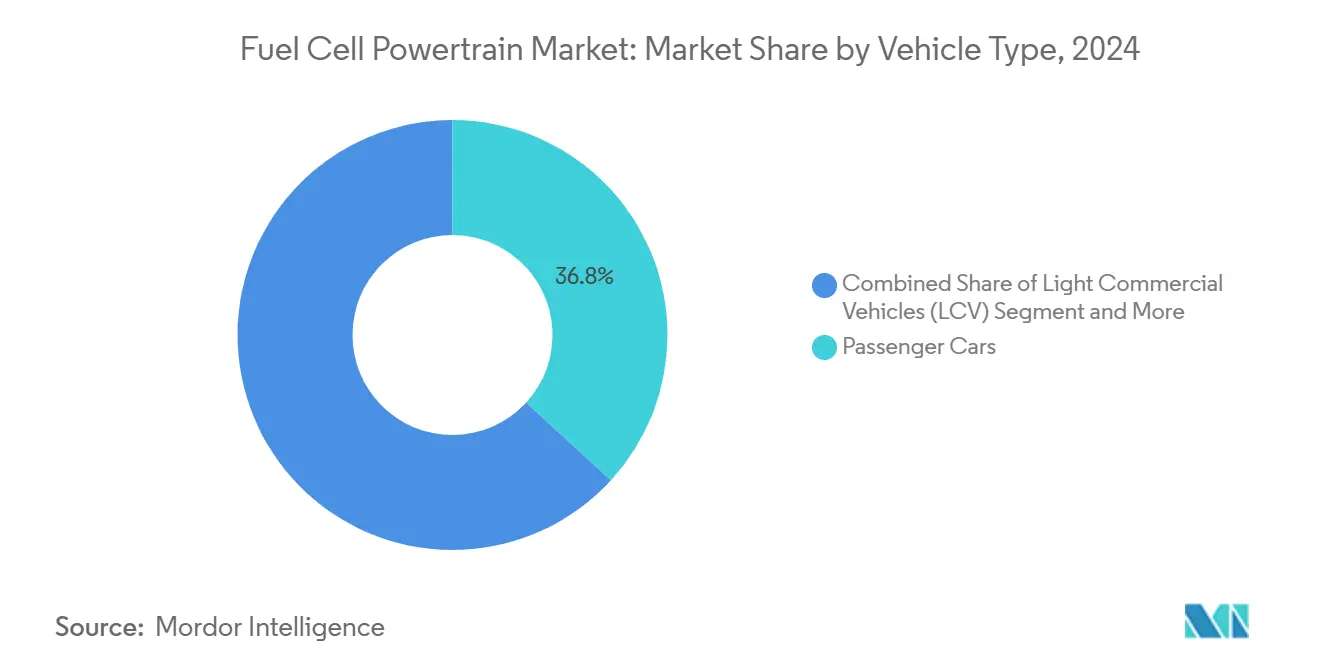

- By vehicle type, passenger cars held a 36.77% share of the fuel cell powertrain market in 2024. Trucks exhibited the highest growth trajectory, at a 35.64% CAGR during the forecast period (2025-2030).

- By power output, 150–250 kW systems controlled a 48.82% share of the fuel cell powertrain market in 2024, while units above 250 kW are rising fastest at a 35.63% CAGR during the forecast period (2025-2030).

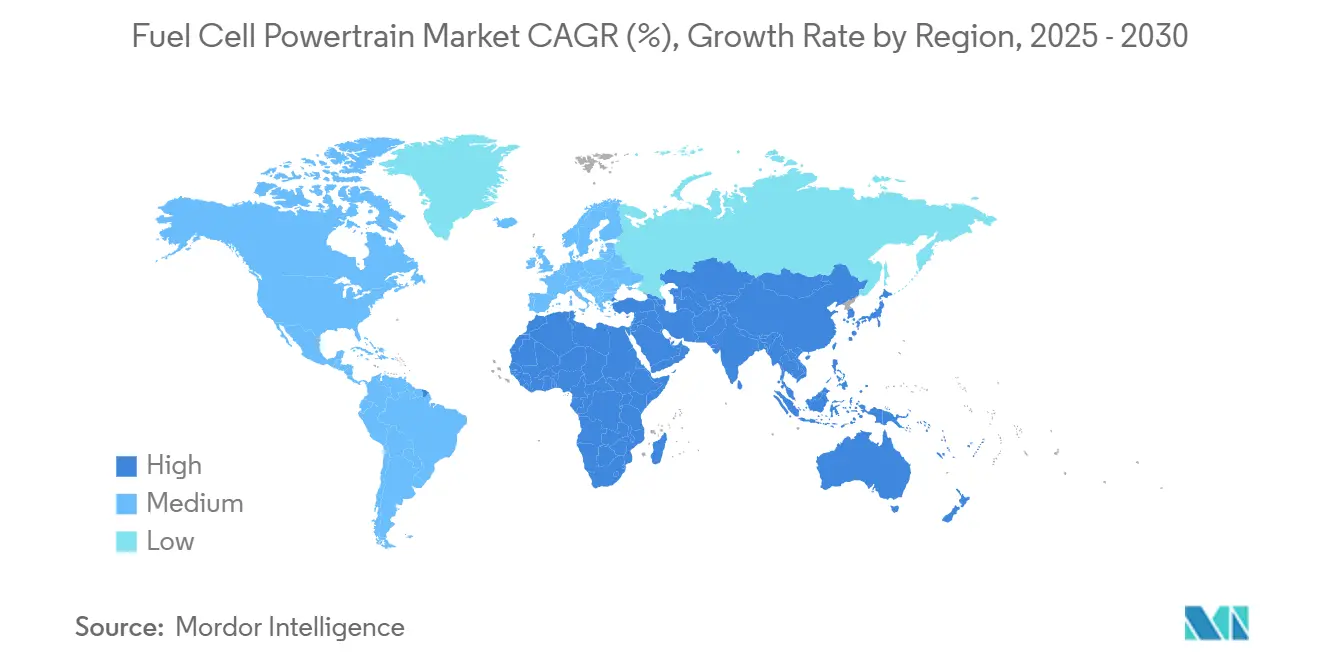

- By region, Asia-Pacific captured 37.84% of the fuel cell powertrain market share in 2024, and the Middle East and Africa segment is accelerating at a 35.61% CAGR during the forecast period (2025-2030).

Global Fuel Cell Powertrain Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Emission Mandates | +8.2% | Global, with early gains in California, EU, China | Medium term (2-4 years) |

| Breakthroughs In Fuel-Cell Stack Durability | +7.8% | Global, spill-over from Japan, Germany to Asia Pacific core | Short term (≤ 2 years) |

| Rapid Build-Out Of Hydrogen Refuelling Corridors | +6.5% | North America and EU, Asia Pacific core | Medium term (2-4 years) |

| OEM Commitments To Fuel-Cell Heavy-Duty Fleets | +5.9% | Global, with early gains in North America, China | Short term (≤ 2 years) |

| Green-Ammonia-To-H₂ Onboard Cracking Synergies | +3.4% | Asia Pacific core, spill-over to MEA | Long term (≥ 4 years) |

| Defence Demand For Silent Powertrains | +2.8% | National, with early gains in US, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Emission Mandates Accelerating Zero-Emission Adoption

California’s Advanced Clean Cars II rule requires complete zero-emission light-duty vehicle sales by 2035, while the European Union mandates more than four-fifths CO₂ reduction for new trucks by 2040[1]“Advanced Clean Cars II,” California Air Resources Board, arb.ca.gov. Similar targets in Japan, South Korea, and China amplify demand signals that favor hydrogen for heavy-duty fleets, where battery weight and charging delays limit practicality. The clarity of these mandates supports OEM investment plans, unlocks supply-chain finance, and drives coordinated infrastructure funding. Fleet operators are responding with long-term procurement contracts that accelerate scale economies. The result is a robust pull effect that anchors the fuel cell powertrain market in commercial trucking corridors.

Breakthroughs in Fuel-Cell Stack Durability & Cost

UCLA scientists reported graphene nanopocket catalysts delivering almost two lakh-hour durability compared with 5,000 hours for legacy platinum stacks[2]“Graphene Nanopocket Catalysts Set Durability Record,” UCLA Newsroom, ucla.edu. Honda’s 2025 fuel-cell module achieves half the cost, doubled life, and triple the volumetric power density over its predecessor. Cellcentric’s NextGen truck stack cuts fuel use by one-fifth and raises power density by three-tenths. These advances align with the U.S. Department of Energy’s USD 60/kW goal, narrowing the total cost-of-ownership gap against diesel. Lower platinum loadings and high-volume bipolar plate production are now feasible, creating a virtuous cycle that accelerates adoption in the fuel cell powertrain market.

Rapid Build-Out of Hydrogen Refueling Corridors

More than a thousand hydrogen stations operate worldwide, and China will target more than a thousand by 2025. Europe’s Hydrogen Backbone envisions dedicated pipelines by 2040. In the United States, a vast investment in federal funding is allocated to freight-corridor hydrogen stations[3]“Hydrogen Infrastructure Funding,” United States Department of Energy, energy.gov. High-flow nozzles exceeding 10 kg/min support heavy-duty trucks, while mobile dispensers bridge network gaps for pilot fleets. Corridor-based deployment maximizes utilization, shortens payback periods, and accelerates demand for the fuel cell powertrain market.

OEM Commitments to Fuel-Cell Heavy-Duty Fleets

Hyundai’s XCIENT trucks have entered fleet service in Switzerland, Germany, and California, supported by an expanding Korean production base. Toyota and Kenworth demonstrated a 450-mile Class 8 tractor in U.S. ports, while Daimler Truck tested liquid-hydrogen GenH2 prototypes on European motorways. Stellantis acquired Symbio to integrate stack kits across its commercial lineup. These commitments de-risk supplier investments and catalyze standardization, positioning the fuel cell powertrain market for commercial scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital Cost Premium Vs. BEVs | -4.2% | Global | Short term (≤ 2 years) |

| Constrained Hydrogen Production | -3.8% | Global, with acute challenges in emerging markets | Medium term (2-4 years) |

| Safety & Regulatory Hurdles | -2.6% | North America and EU, regulatory influence | Medium term (2-4 years) |

| Nickel Price Volatility | -1.9% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Capital Cost Premium vs. BEVs

Fuel-cell systems still carry a hefty price tag compared to battery packs. To make fuel cells competitive in heavy-duty applications, we must see a significant drop in stack costs and hydrogen prices. While passenger cars grapple with higher costs due to the established economies of scale in battery-electric vehicles, fuel-cell powertrains shine for longer routes. In these scenarios, where the weight of batteries can hinder efficiency, fuel cells present a more appealing alternative. Additionally, advancements in hydrogen production technologies and infrastructure development are critical to accelerating the adoption of fuel-cell systems. Governments and private stakeholders are increasingly investing in research and development to address these challenges, aiming to make fuel-cell technology a viable solution across various transportation segments.

Constrained Hydrogen Production & Logistics

Although green hydrogen is gaining momentum, it constitutes a mere sliver of the global supply and is still priced significantly higher than its conventional grey counterpart. China may dominate in production volumes, but distribution remains tethered to select industrial hubs. The global green hydrogen market is witnessing increased investments and policy support, with governments and private players aiming to scale production and reduce costs. Meanwhile, ambitious endeavors like Egypt's expansive capacity plans are stalling, hampered by a nascent pipeline and export infrastructure. As midstream networks await maturation, the fuel cell powertrain sector is left contending with constrained availability and fluctuating prices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component Type: Systems Dominate, Storage Accelerates

Fuel cell systems controlled 47.83% of the fuel cell powertrain market in 2024, reflecting their central role in value creation. High-volume stack lines, integrated balance-of-plant modules, and standardized control software allow OEMs to cut assembly times by three-tenths. The fuel cell powertrain industry increasingly adopts modular cassette designs that permit swapping aging stacks in under an hour, improving uptime for fleet operators.

Hydrogen storage is expected to grow at a 35.56% CAGR during the forecast period (2025-2030). Modern compressed-gas tanks leverage advanced composite materials, shedding weight without compromising high-pressure performance. This innovation bolsters efficiency in hydrogen-powered vehicles. Meanwhile, Daimler Truck's GenH2 prototype showcases liquid hydrogen's promise, potentially revolutionizing driving ranges for long-haul applications and opening doors in the fuel-cell powertrain market. Concurrently, efforts to harmonize ISO and SAE standards are underway, simplifying global certification processes and easing the burden on manufacturers navigating diverse regional landscapes.

By Drive Type: Rear-Wheel Leads, All-Wheel Gains

Rear-wheel drive architectures held 53.41% of the fuel cell powertrain market in 2024 because commercial trucks rely on ladder frames that package tanks and stacks aft the cab. Torsional rigidity and straightforward driveline layouts support high torques for gradeability.

All-wheel drive is expected to grow at a 35.58% CAGR during the forecast period (2025-2030), spurred by passenger SUVs and performance sedans that require traction in variable climates. Dual-motor setups also unlock regenerative braking on both axles, boosting system efficiency by up to one-tenth. BMW intends to pair its third-generation stack with a front-rear e-axle combination for 2028 models, underscoring the technology migration toward the broader fuel cell powertrain market.

By Vehicle Type: Passenger Base, Truck Momentum

Passenger cars like the Toyota Mirai and the Hyundai Nexo represented a 36.77% share of the fuel cell powertrain market in 2024. Sales concentrate in Japan, Korea, and California, where early hydrogen networks exist. However, growth moderates as trucks ascend.

Truck platforms are expected to grow at a 35.64% CAGR during the forecast period (2025-2030), anchored by regulatory targets for long-haul emissions and operational parallels to diesel refueling. Cellcentric’s 350 kW stack delivers 25,000 hours of life, meeting fleet duty cycles of 700,000 km. These capabilities shift investment focus toward trucking, repositioning value pools inside the fuel cell powertrain market.

By Power Output: Mid-Range Core, High-Power Surge

Systems rated 150–250 kW owned 48.82% of the fuel cell powertrain market share in 2024, balancing cost, density, and durability for regional haul trucks and premium sedans. Honda’s 150 kW module exemplifies this sweet spot with 59.8% net efficiency.

Stacks above 250 kW are expected to grow at a 35.63% CAGR during the forecast period (2025-2030), as duty cycles extend. Multi-stack arrays now feed marine propulsion and stationary peaker plants. Advanced cooling plates and silicon-carbide inverters manage elevated current densities, pushing the fuel cell powertrain market frontier toward megawatt-class solutions.

Geography Analysis

Asia-Pacific captured a 37.84% share of the fuel cell powertrain market in 2024, driven by China’s sale of 5,600 hydrogen vehicles and Japan’s steadfast R&D leadership. South Korea’s roadmap envisions multiple FCEVs by 2040, sustaining stack factories for Hyundai and Doosan. Government subsidies covering up to two-fifths of vehicle cost shorten fleet payback windows, anchoring regional demand in the fuel cell powertrain market.

The Middle East & Africa segment is expected to grow at a 35.61% CAGR during the forecast period (2025-2030). Egypt’s 115 GW renewables pipeline and Saudi Arabia’s NEOM project support export-oriented green hydrogen, underpinning future supply security for European buyers. Domestic uptake remains modest due to limited assembly capacity and nascent fueling networks. Yet, the region's strategic geographic position primes it as a key node in global hydrogen trade for the fuel cell powertrain market.

North America and Europe offer mature regulatory ecosystems. California’s zero-emission truck mandate and the European Hydrogen Backbone funnel capital toward public-private station roll-outs. OEM alliances such as Hyundai-Cummins target local content requirements and accelerate homologation. Complex permitting and higher land costs slow station density compared with Asia. However, purchase tax credits and carbon pricing close total cost gaps, sustaining the steady expansion of the fuel cell powertrain market.

Competitive Landscape

The fuel cell powertrain market shows moderate concentration. Toyota leads passenger sales with its Mirai sedan and proprietary solid-polymer stack. Hyundai’s XCIENT dominates heavy-duty deployments, while Ballard supplies PEM modules to bus builders across Europe and North America. Daimler and Volvo’s joint venture, Cellcentric, focuses on high-power systems, aiming for series production in 2027. BMW and Toyota co-develop third-generation stacks for premium SUVs, targeting a two-fifths parts commonality to lower procurement costs.

Chinese manufacturers such as China Commercial rapidly gained a massive global unit share in 2023 through value-priced trucks, leveraging provincial subsidies and vertically integrated supply chains. Honda’s 2025 module reduces production cost by half, opening a licensing pathway for third-party truck builders. Partnerships between fuel-cell firms and Tier-1 suppliers like Bosch and Bosch Rexroth are integrating thermal management and power electronics, strengthening the ecosystem within the fuel cell powertrain market.

Emerging niches include maritime powertrains where Hopium and Orient Express Racing validate 160 kW stacks for 30-meter vessels. Stationary multi-megawatt backup systems attract data-center operators seeking zero-carbon resilience. As applications diversify, intellectual-property differentiation pivots from raw stack performance toward lifecycle cost, manufacturability, and platform adaptability, shaping competitive trajectories in the fuel cell powertrain market.

Fuel Cell Powertrain Industry Leaders

Toyota Motor Corporation

Hyundai Motor Company

Ballard Power Systems Inc.

Daimler Truck AG

Cummins Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Honda announced that its Next Generation Fuel Cell Module will debut in North America at ACT Expo 2025. Compared with current units, it will be 50% cheaper, double the durability, and triple the volumetric power density.

- September 2024: BMW Group and Toyota Motor Corporation expanded their collaboration to develop third-generation hydrogen powertrains, scheduling BMW’s first series-production FCEV for 2028.

- June 2024: Ballard Power Systems and Vertiv partnered to demonstrate 200 kW to multi-megawatt PEM backup power solutions for data centers at Vertiv’s Delaware facility.

Global Fuel Cell Powertrain Market Report Scope

| Fuel Cell System |

| Battery System |

| Drive System |

| Hydrogen Storage System |

| Others |

| Rear Wheel Drive (RWD) |

| Front Wheel Drive (FWD) |

| All-Wheel Drive (AWD) |

| Passenger Cars |

| Light Commercial Vehicles (LCV) |

| Buses |

| Trucks |

| Less than 150 kW |

| 150–250 kW |

| More than 250 kW |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Component Type | Fuel Cell System | |

| Battery System | ||

| Drive System | ||

| Hydrogen Storage System | ||

| Others | ||

| By Drive Type | Rear Wheel Drive (RWD) | |

| Front Wheel Drive (FWD) | ||

| All-Wheel Drive (AWD) | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCV) | ||

| Buses | ||

| Trucks | ||

| By Power Output | Less than 150 kW | |

| 150–250 kW | ||

| More than 250 kW | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the fuel cell powertrain market in 2030?

The market is forecast to reach USD 5.16 billion by 2030.

Which region currently leads global demand?

Asia-Pacific held 37.84% of the global share in 2024.

Which vehicle category is growing fastest?

Trucks are expected to grow at a 35.64% CAGR through 2030.

What power range dominates current commercial applications?

Systems rated 150–250 kW controlled 48.82% of the 2024 market.

Which component segment is expanding the quickest?

Hydrogen storage systems are rising at a 35.56% CAGR.

What policy most strongly drives adoption in the United States?

California’s Advanced Clean Cars II rule mandates 100% zero-emission light-duty sales by 2035.

Page last updated on: