FRP Grating Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 547.78 Million |

| Market Size (2031) | USD 703.13 Million |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

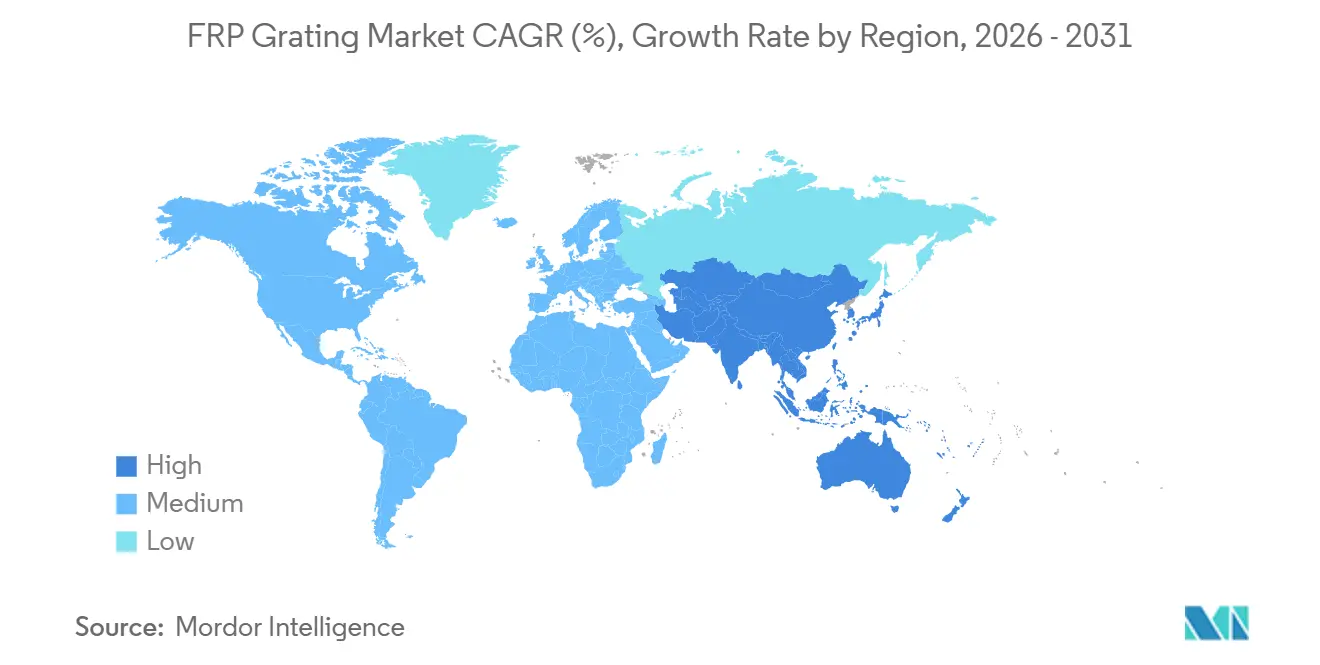

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

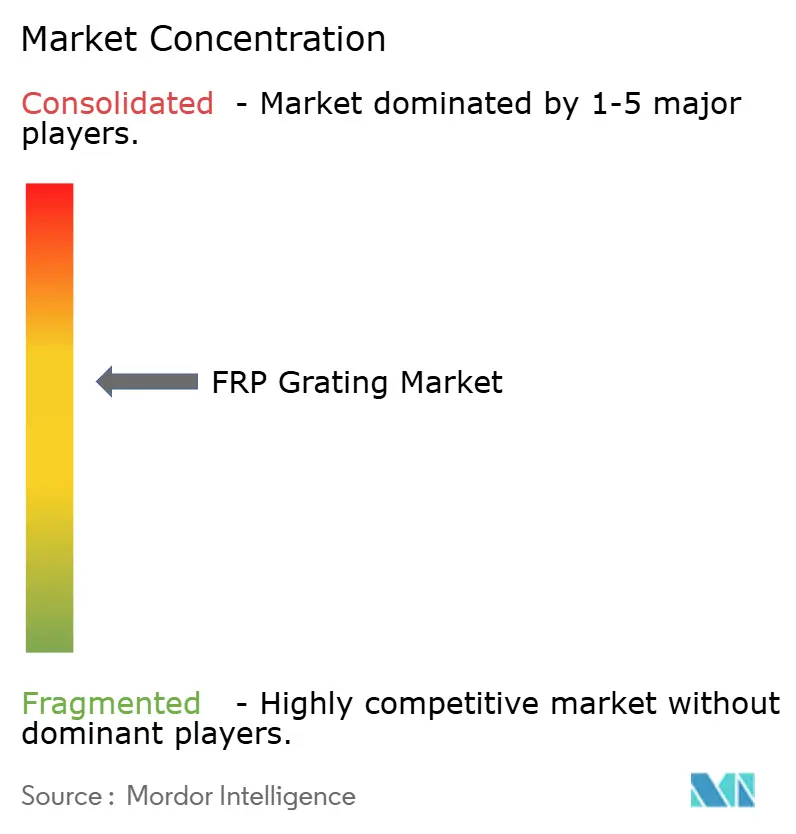

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

FRP Grating Market Analysis by Mordor Intelligence

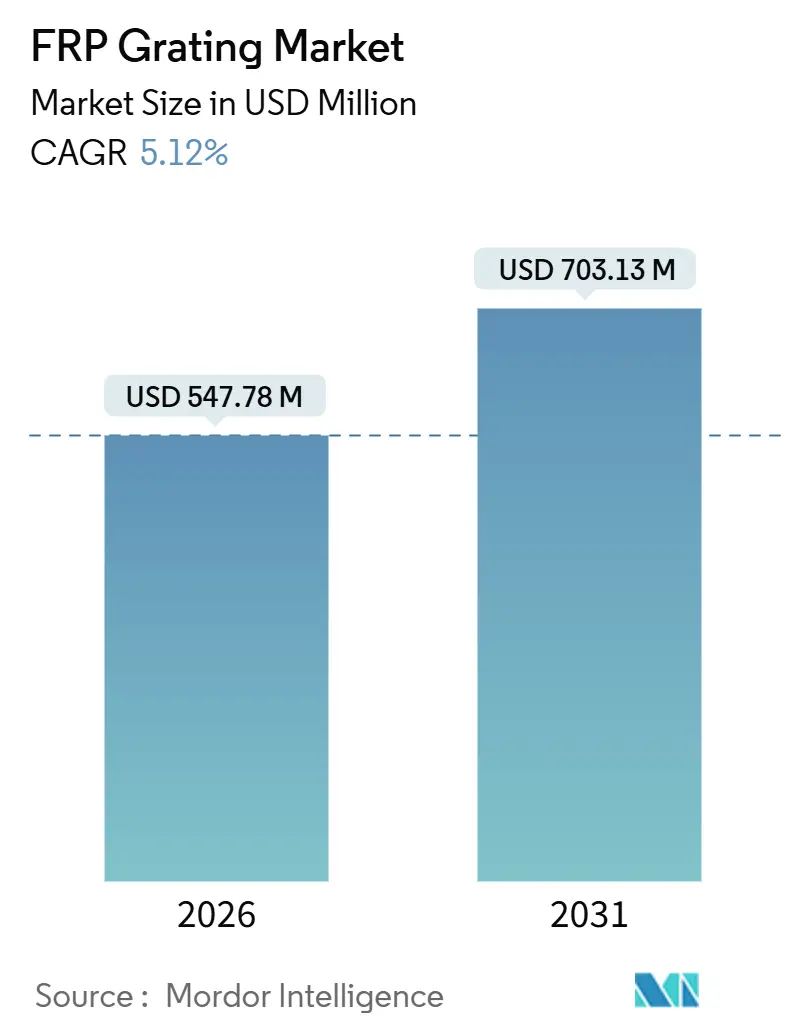

The FRP Grating Market size is estimated at USD 547.78 million in 2026, and is expected to reach USD 703.13 million by 2031, at a CAGR of 5.12% during the forecast period (2026-2031). The acceleration is underpinned by regulatory pressure to replace corrosion-prone mild steel, simultaneous capacity additions in wastewater treatment, and mounting demand from offshore renewable energy installations. Weight savings, slip resistance, and low maintenance costs continue to differentiate composites, encouraging asset owners in chemicals, water treatment, and energy to standardize specifications on molded or pultruded panels. Volatile styrene costs and tightening environmental rules surrounding styrene emissions are pushing fabricators toward bio-attributed formulations, while glass-fiber oversupply in China is easing reinforcement costs. Competitive dynamics remain moderate because the top five suppliers hold less than half of global revenue, allowing regional specialists to address emerging niches such as antimicrobial coatings and fire-rated phenolic products.

Key Report Takeaways

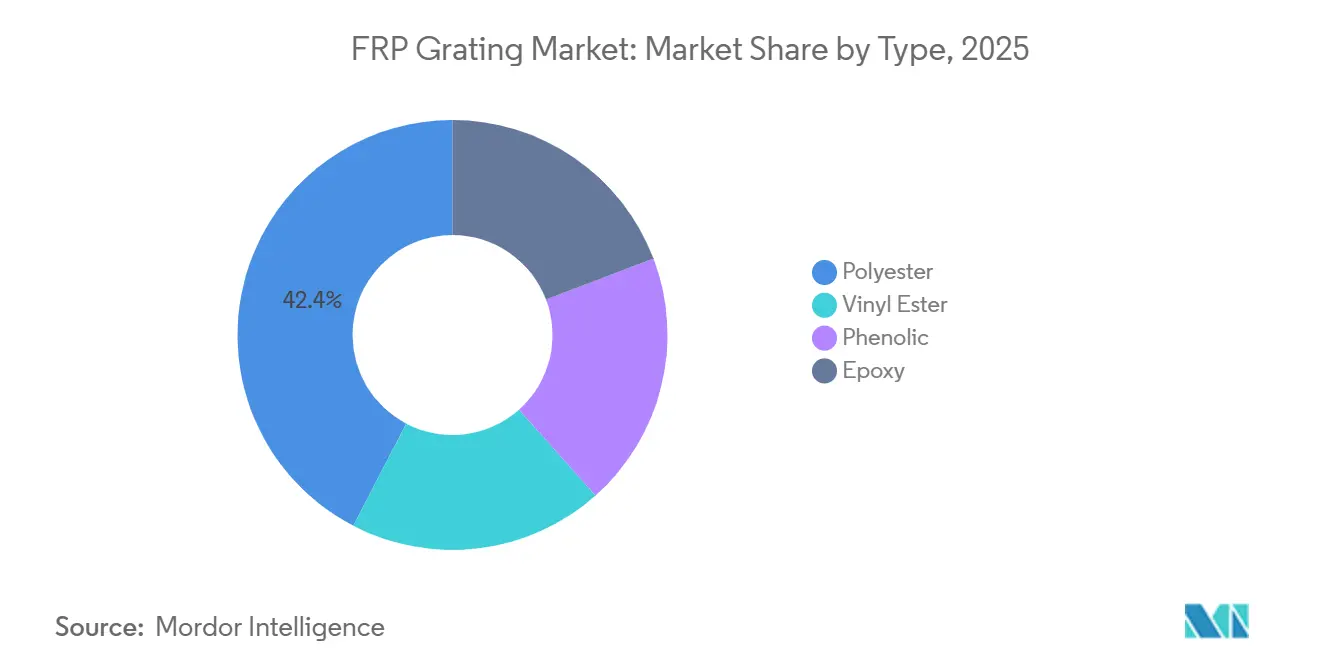

- By resin type, polyester captured 42.36% revenue in 2025, while vinyl ester is advancing at a 6.24% CAGR through 2031.

- By manufacturing process, molded products led with 58.47% volume in 2025; pultruded panels are the fastest-growing at 6.18% through 2031.

- By application, walkways accounted for 34.28% of 2025 revenue; floor systems are progressing at a 6.31% CAGR to 2031.

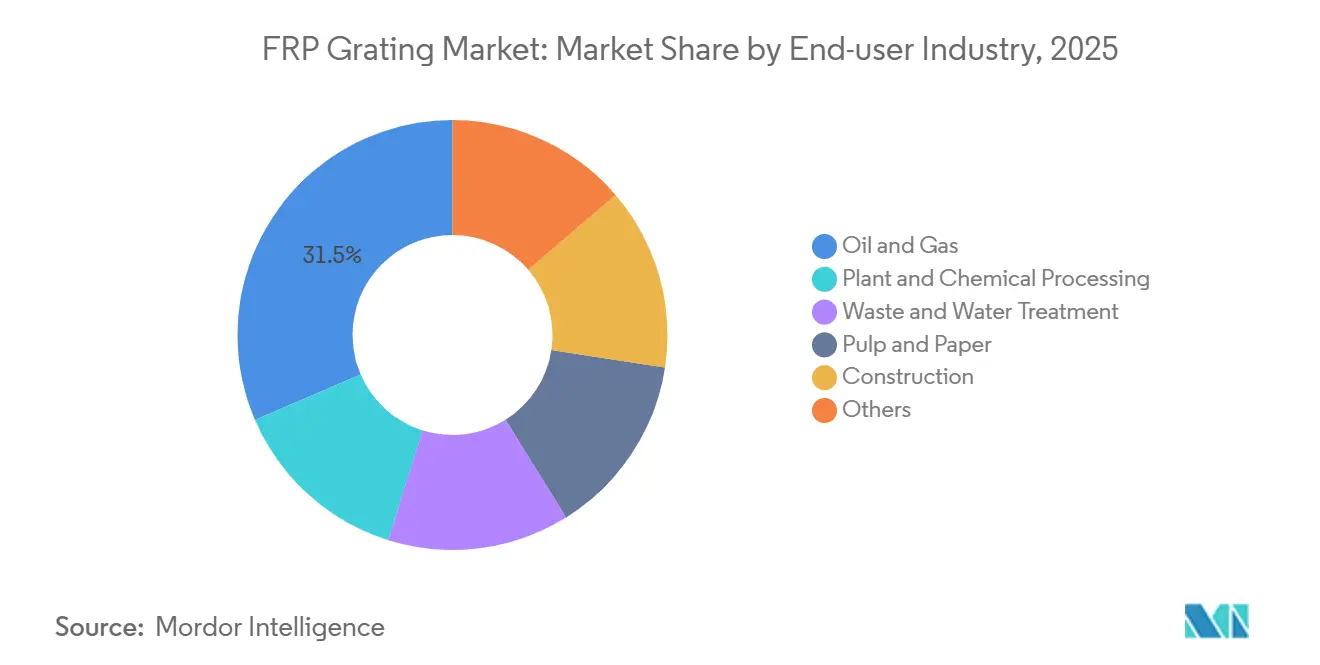

- By end-user, oil and gas held 31.46% demand in 2025, whereas wastewater treatment is expanding at 6.27% CAGR through 2031.

- By region, Asia-Pacific represented 47.38% 2025 revenue, registering a projected 5.94% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global FRP Grating Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift from steel to corrosion-resistant FRP gratings | +1.2% | Global, with highest adoption in Asia-Pacific chemical hubs and Middle East offshore platforms | Medium term (2-4 years) |

| Rising CAPEX in wastewater treatment facilities | +0.9% | North America and Asia-Pacific, particularly US EPA-funded projects and India's Jal Jeevan Mission zones | Long term (≥ 4 years) |

| Expansion of offshore wind and floating solar platforms | +0.8% | Europe (North Sea), Asia-Pacific (Taiwan Strait, South China Sea), and US East Coast | Medium term (2-4 years) |

| Stricter worker-safety and anti-slip regulations | +0.7% | Global, with enforcement intensity highest in North America (OSHA) and EU (ISO 14122 compliance) | Short term (≤ 2 years) |

| Adoption of smart-sensor embedded FRP walkways | +0.4% | Pilot deployments in North America and Europe; scalability contingent on IoT infrastructure maturity | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift from Steel to Corrosion-Resistant FRP Gratings

Lifecycle studies demonstrate that composites outperform mild steel in corrosive environments, despite a 30-50% upfront premium. Shell’s Mars Platform retrofit in 2024 recorded a 60% fall in maintenance downtime and saved USD 1.2 million in coating labor across fifteen years[1]Shell, “Mars Platform Composites Retrofit Case Study,” shell.com. Publication of ISO 24681:2023 unified marine-grade design criteria, allowing offshore wind developers to quote identical load, fire, and UV benchmarks. China’s 2024 Industrial Structure Adjustment Catalogue further incentivizes large-scale alkali-free glass-fiber production, ensuring consistent fiber quality.

Rising CAPEX in Wastewater Treatment Facilities

Hydrogen sulfide environments degrade galvanized steel within five to seven years, whereas molded FRP panels resist corrosion and satisfy OSHA 1910.22 slip rules without coatings[2]Occupational Safety and Health Administration, “Walking-Working Surfaces Final Rule,” osha.gov. India’s USD 12 billion Jal Jeevan Mission program specifies molded gratings for clarifier walkways to meet tight construction windows.

Expansion of Offshore Wind and Floating Solar Platforms

Dogger Bank Wind Farm uses phenolic gratings that meet IMO SOLAS fire standards while reducing topside weight by 40%. Taiwan’s 5.6 gigawatt offshore pipeline favors UV-stabilized pultruded panels to tolerate typhoon winds. Southeast Asian floating solar pilot projects, such as Singapore’s Tengeh Reservoir array, revealed early UV embrittlement, triggering resin suppliers to blend hindered amine stabilizers.

Stricter Worker-Safety and Anti-Slip Regulations

OSHA’s 2024 guidance on walking-working surfaces now audits static coefficent of friction, leading U.S. refineries to phase out coated steel in favor of FRP concave meniscus surfaces. EU ISO 14122 directives likewise disallow uncoated mild steel in corrosive process zones, accelerating substitution in Germany’s Rhine-Ruhr complexes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost versus mild-steel grating | -0.6% | Price-sensitive markets in South America, Middle East, and Africa; less impact in North America and Europe where lifecycle costing prevails | Short term (≤ 2 years) |

| UV-induced resin degradation in high-insolation zones | -0.4% | Equatorial regions (Southeast Asia, Middle East, East Africa) and high-altitude installations (Andean mining, Tibetan infrastructure) | Medium term (2-4 years) |

| Volatile styrene and glass-fiber prices | -0.5% | Global, with acute impact on smaller fabricators lacking hedging capacity; China's glass fiber overcapacity partially offsets fiber price risk | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Versus Mild-Steel Grating

FRP gratings command a 30-50% price premium over galvanized steel equivalents, creating a procurement barrier in capital-constrained projects despite superior lifecycle economics. Budget-driven municipal wastewater projects in Brazil and Argentina often default to steel due to upfront cost constraints, even though FRP's 25-30 year service life versus steel's 10-15 year repaint-and-replace cycle would yield lower total cost of ownership. KPS Capital Partners’ 2024–25 acquisitions of INEOS and Crane Composites aim to scale resin volumes that could trim fabricator costs by up to 12% by 2028.

UV-Induced Resin Degradation

Polyester and vinyl ester resins exhibit surface chalking and micro-cracking after 5-7 years of continuous exposure to solar radiation exceeding 1,000 watts per square meter, a threshold routinely exceeded in Middle Eastern desalination plants and Southeast Asian petrochemical facilities. At the same time, UV-stabilized formulations incorporating hindered amine light stabilizers and titanium dioxide pigments extend service life to 15-20 years. Field failures in Saudi Arabia's Ras Tanura refinery, where unstabilized polyester gratings delaminated after 4 years, have prompted asset owners to mandate vinyl ester or phenolic resins with proven UV resistance, effectively segmenting the market between cost-driven buyers accepting shorter service life and quality-focused operators willing to pay for longevity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Vinyl Ester Gains on Polyester’s Installed Base

Polyester retained a 42.36% 2025 FRP grating market share, reflecting a vast legacy in municipal walkways. Vinyl ester’s 6.24% CAGR signals momentum in acid and solvent rich zones. Phenolic panels satisfy IMO SOLAS and ASTM E84 Class A requirements but command 50-70% higher prices. Epoxy remains confined to cleanrooms needing electrostatic discharge performance. Resin suppliers are introducing bio-attributed vinyl ester formulations to cut carbon intensity, pointing to wider acceptance as corporate sustainability targets tighten.

Vinyl ester uptake will accelerate because offshore and chemical buyers already budget for premium materials. Polyester will persist where cost drives decisions, while phenolic will capture fire-critical niches. Epoxy’s limited load capacity restricts growth, though conductive additives inside vinyl ester threaten to cannibalize epoxy in electronics flooring.

By Manufacturing Process: Molded Dominates, Pultruded Gains in Heavy-Duty

Molded panels commanded 58.47% of 2025 volume, pultrusion dies, and bi-directional load distribution that suits platforms and trench covers subjected to multi-axis stresses. Pultruded panels, although capital intensive, are registering 6.18% CAGR by delivering higher tensile strength for truck loading bays and heavy-duty offshore walkways.

Molded products give bi-directional load paths that resist crack propagation, while pultruded variants yield tight tolerances ideal for modular retrofits. North American and European producers emphasize pultrusion to offset labor costs via automation, whereas Asian manufacturers exploit labor advantages in hand-layup molded production.

By Application: Floor Systems Outpace Walkways in Retrofit Demand

Walkways represented 34.28% of 2025 application revenue, reflecting their ubiquity in chemical plants, wastewater facilities, and offshore platforms where elevated access routes connect process equipment. Floor systems, however, are expanding at 6.31% CAGR through 2031, driven by modular retrofit projects in aging industrial facilities that prioritize rapid installation and minimal production downtime. Stair treads and platforms, though smaller segments, benefit from OSHA 1910.24 enforcement of fixed industrial stair requirements, which mandate slip-resistant surfaces and defined load ratings that FRP products meet without secondary coatings.

Walkways remain the largest segment due to their role in connecting dispersed equipment, yet growth is moderating as new plant construction slows in mature markets. Stair treads are benefiting from ASTM E303 slip-resistance testing protocols that disqualify steel grating with worn coatings, creating a replacement cycle every 8-10 years in high-traffic zones. Platforms face competition from modular aluminum systems in light-duty applications, though FRP retains dominance where chemical exposure or electrical insulation is required.

By End-User Industry: Waste Treatment Overtakes Oil and Gas Growth

Oil and gas end-users contributed 31.46% of 2025 demand, reflecting FRP's entrenched position on offshore platforms, refineries, and petrochemical complexes where saltwater exposure and hydrocarbon vapors accelerate steel corrosion. Waste and water treatment, however, is the fastest-growing vertical at 6.27% CAGR through 2031, propelled by municipal infrastructure mandates and industrial pretreatment facility expansions. Plant and chemical processing remains a steady demand source, with vinyl ester gratings specified for reactor mezzanines and scrubber towers where acids and caustics attack conventional materials. Pulp and paper mills and construction scaffolding represent incremental niches likely to expand as lifecycle cost accounting becomes mainstream.

The waste and water treatment surge reflects a confluence of regulatory drivers and infrastructure aging. The United States Environmental Protection Agency's 2024 guidance on nutrient removal upgrades is forcing municipalities to retrofit secondary clarifiers and membrane bioreactors, creating demand for corrosion-resistant gratings in high-humidity zones where steel fails within 5-7 years.

Geography Analysis

Asia-Pacific held 47.38% of 2025 revenue and is set for 5.94% CAGR through 2031. Chinese policy encourages premium glass-fiber output, ensuring feedstock quality. India’s Jal Jeevan Mission injects USD 12 billion into sewage projects, establishing steady molded grating demand. ASEAN chemical hubs in Malaysia and Indonesia turn to vinyl ester panels for corrosion control. Japan sustains stable purchases for coastal civil structures that require seismic and corrosion resilience.

In North America, the US EPA’s USD 515.4 billion water program will drive the largest slice of regional spending, complemented by East Coast offshore wind farm construction. Canada’s oil sands operations specify pultruded panels for extreme temperature swings, and Mexican near-shoring is spurring molded panel demand in new automotive parks.

In Europe, Dogger Bank Wind Farm demonstrates FRP advantages in offshore substations. Germany’s Rhine-Ruhr legislative environment is replacing steel walkways with vinyl ester to meet ISO 14122 mandates. Spain and Greece invest in desalination plants that adopt UV-stabilized polyester, though field feedback has already prompted resin reformulations.

In South America and the Middle East-Africa price sensitivity limits penetration, yet Brazil’s pre-salt platforms and Saudi petrochemical complexes buy higher-grade vinyl ester and phenolic panels for corrosion and fire safety.

Regulatory Landscape

FRP grating specifications are increasingly grounded in formal safety and marine-performance standards. In the United States, OSHA 29 CFR 1910 walking-working surface requirements for firm, stable, slip-resistant surfaces and fall protection continue to drive replacement of coated steel in industrial platforms and walkways, aligning with asset-owner specifications that reference measurable slip performance.

For marine and offshore use, ISO 24681:2023 provides unified technical requirements and test methods for FRP gratings on ships and offshore platforms, including durability and fire-related criteria. ASTM F3059-24 also standardizes performance requirements for FRP gratings used in marine construction and shipbuilding. On trade and chemicals-compliance, the European Commission imposed definitive anti-dumping duties in April 2026 on certain continuous filament glass fibre products from Bahrain, Egypt, and Thailand under Regulation (EU) 2026/831, which affects EU import economics for glass-fiber-based inputs used across FRP grating supply chains. Separately, Regulation (EU) 2023/2055 introduces an instruction and labeling-related compliance milestone from 17 October 2026 for products containing specified synthetic polymer microparticles, pushing suppliers to update documentation and professional-user guidance where applicable.

Value Chain Analysis

The FRP grating value chain starts with upstream feedstocks, primarily glass fiber reinforcement and thermoset resins (unsaturated polyester, vinyl ester, epoxy, and phenolic systems), along with curing agents, fillers (such as aluminum hydroxide or calcium carbonate), pigments, and performance additives (UV stabilizers and flame-retardant packages). Volatility in styrene-linked resin inputs and regionally uneven glass fiber economics influence conversion costs, while end-use specifications in offshore, chemical processing, and wastewater applications shape formulation choices, including higher-performance vinyl ester and phenolic systems where corrosion or fire performance is critical.

Midstream manufacturing is dominated by molded and pultruded processes. Molded grating supports bidirectional load distribution and customization for platforms and walkways, while pultrusion provides tighter tolerances, consistent profiles, and higher tensile performance for heavy-duty panels. Industry-standard design and acceptance practices are supported by the ANSI-approved reaffirmation of the ANSI/ACMA/FGMC-Grating Manual-2017 (R2025) and by marine-focused standards such as ASTM F3059-24 and ISO 24681:2023, which shape qualification testing and documentation. Downstream, producers typically combine fabrication services (cut-to-size, fastening systems, and installation support) with distribution networks serving municipal water and wastewater projects, chemical plants, and offshore operators, where procurement increasingly weighs lifecycle cost, safety compliance, and documentation readiness.

Competitive Landscape

The FRP Grating market is moderately concentrated. Upstream integration is accelerating, exemplified by KPS Capital Partners’ EUR 1.7 billion acquisition of INEOS Composites and USD 227 million purchase of Crane Composites in late 2024. Hill & Smith’s June 2025 purchase of United Fiberglass illustrates geographic consolidation to secure municipal waste-water projects. Regional competitors exploit proximity and faster turnaround, notably ACEON and Webforge in ASEAN. Technology gaps persist because smaller firms lack automated pultrusion lines, hindering consistency.

FRP Grating Industry Leaders

Bedford Reinforced Plastics

STRONGWELL CORPORATION

Fibergrate Composite Structures, Inc.

Gebrüder MEISER GmbH

Techno-Composites Domine GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Wastewater and water treatment remains a practical whitespace for molded FRP grating, especially where hydrogen sulfide exposure and humidity shorten the service life of galvanized steel, and procurement increasingly ties selection to safety and corrosion-resistance specifications. Evidence of active replacement work includes Seapeak Composite delivering 175 tons of corrosion-resistant molded FRP grating in May 2026 for a full replacement of steel grating at a large wastewater treatment plant, indicating project-level conversion rather than incremental trials.

Offshore and industrial platforms also offer an expansion lane where standardized marine requirements reduce adoption friction and shift purchasing toward qualified, documented products. ISO 24681:2023 and ASTM F3059-24 create clearer pass-fail frameworks for shipbuilding and offshore applications, supporting wider bid alignment across developers and yards. In parallel, suppliers are adjusting formulations and surface systems for extreme UV and heat exposure, highlighted by technical upgrades cited in May 2026 aimed at higher-temperature and anti-aging performance for Middle East environments. R&D activity around self-sensing composites, such as embedding fiber Bragg grating sensors for structural health monitoring reported in 2026 academic research, points to premium, maintenance-oriented product positioning for access systems where downtime and inspection costs are material.

Recent Industry Developments

- June 2026: Bedford Reinforced Plastics completed full-scale testing of a 100-foot by 10-foot FRP truss bridge designed for H-5 emergency vehicle loads in partnership with West Virginia University. The testing reinforces performance validation for FRP structures used in access and industrial infrastructure, supporting broader specification acceptance where higher load ratings and documented verification are required.

- October 2025: Fibergrate Composite Structures Inc. acquired ThruBeam Structural Science Composites Ltd., a specialist in composite manhole and trench covers. The acquisition expands Fibergrate's access-solutions portfolio adjacent to grating-heavy municipal and industrial projects, enabling more bundled offerings around covers, platforms, and walkway systems.

- January 2024: Fibergrate Composite Structures Inc. partnered with Microban International to launch FRP products with integrated antimicrobial technology. The collaboration targets hygiene-sensitive end uses and facilities where biofilm control and easier cleaning are part of procurement criteria, adding a differentiated surface-performance feature to standard corrosion and slip-resistance value propositions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the FRP grating market covers the sales value of fiberglass reinforced plastic grating used as load bearing and anti-slip surfaces in industrial and commercial settings, including walkway, platform, and flooring related uses, across major regions.

Scope exclusions: We exclude traditional metal grating, handrails and ladders sold as standalone items, and installation services that are not bundled with grating supply.

Segmentation Overview

- By Type

- Polyester

- Vinyl Ester

- Phenolic

- Epoxy

- By Manufacturing Process

- Pultruded

- Molded

- By Application

- Stair Treads

- Walkways

- Platforms

- Floor Systems

- By End-User Industry

- Oil and Gas

- Plant and Chemical Processing

- Waste and Water Treatment

- Pulp and Paper

- Construction

- Others

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started by mapping where FRP grating is usually consumed and what triggers replacement or new demand. We referenced public sources such as US Census construction spending releases, USGS materials statistics, OSHA and other safety guidance documents, and wastewater infrastructure publications from agencies such as the US EPA. For cross-country direction checks, we also used sources such as UN Comtrade for trade flows and World Bank macro indicators to align demand with industrial activity.

Alongside these, we reviewed company filings, annual reports, investor presentations, product catalogs, and credible press coverage to understand pricing language, mix changes, and capacity additions. In a few cases, paid subscriptions for company financials and intelligence, news and financials, and patent databases were used to fill gaps around ownership structures and technology claims. This list is not exhaustive, and additional public sources were also used to collect, validate, and clarify data points for the FRP grating scope.

Primary Interviews and Surveys

Primary work focused on confirming real buying patterns for FRP grating across process industries and construction, and then testing assumptions on pricing, replacement cycles, and specification preferences. We spoke with a balanced mix of manufacturers, distributors, fabricators, and end users across APAC, EMEA, and the Americas, which helped close gaps that desk sources cannot explain well (for example, resin choice shifts between polyester, vinyl ester, and phenolic under corrosion or fire performance needs).

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 14% | APAC: 39% |

| Mid tier: 47% | Functional/Unit leaders: 35% | EMEA: 35% |

| Smaller Players: 14% | Managers: 51% | Americas: 26% |

Market-Sizing & Forecasting

Sizing was built using top-down and bottom-up logic. Industrial activity and infrastructure spending were used first to reconstruct the demand pool, then application-level penetration assumptions were applied for where FRP grating is selected over metal options. After the demand pool was formed, it was translated into value using typical installed grating volumes by application (walkways, platforms, stair treads, and floor systems), then checked against resin and process mixes that influence realized pricing.

To keep the model tied to reality, we corroborated totals using selective bottom-up approximations, including supplier revenue splits, sampled price ranges by resin type, and distributor channel checks in key countries. Key inputs used in the model included end user capex cycles in oil and gas and chemical processing, wastewater treatment expansion and retrofit activity, construction project momentum in coastal and industrial zones, resin price direction and availability, and observed shifts between molded and pultruded grating based on load rating needs. Where bottom-up data was missing for smaller markets, gaps were handled through ratio-based extrapolation from similar industrial profiles, and then corrected after expert feedback.

Forecasting relied mainly on scenario analysis, since FRP grating demand depends on lumpy projects and replacement decisions rather than a linear progression. The scenarios were anchored on expert views of industrial maintenance spend, corrosion-related replacement timing, and adoption pace in water and wastewater facilities, and then converted into yearly growth paths with conservative, base, and faster-adoption cases.

Data Validation & Update Cycle

Validation was done through repeated triangulation between model outputs, independent demand signals, and what primary respondents described as typical order patterns. When outliers appeared, such as a sudden spike in implied pricing or an unusual regional mix shift, the assumptions were rechecked, and the relevant interviews were revisited to confirm whether a real market event was present.

Before sign-off, the dataset and calculations go through multiple analyst reviews so arithmetic, unit conversions, and scope boundaries remain consistent across regions and applications. Reports are refreshed annually, with interim updates triggered by material events such as major plant shutdowns, sharp resin price swings, or meaningful infrastructure spending changes. Right before delivery, an analyst completes a final update pass so clients receive the latest view that matches the current market context.

Mordor Intelligence's Frp Grating Market Size Compared With Other Published Estimates

Published market sizes for FRP grating can vary a lot, even when they look like they are talking about the same product. In practice, the biggest reasons are differences in what is counted as grating revenue, how pricing is treated across resin types, and which end uses are included in the demand pool.

By tracking application-level volumes and refreshing resin and process mix assumptions each cycle, Mordor Intelligence keeps the estimate tied to where FRP grating is actually specified (such as platforms, walkways, and stair treads) instead of pulling in adjacent FRP panels or broader composite structures. The spread also comes from how firms handle inflation and currency timing, and whether they use project-driven demand signals (water and wastewater upgrades, industrial maintenance cycles) or rely more on broad composites growth rates.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 547.78 M (2026) | |

| Industry Publisher A | USD 1.17 B (2024) | Uses an earlier base year and appears to include a wider scope that can bundle broader FRP structural products beyond grating, which increases the value pool compared with a grating-only boundary. |

| Research House B | USD 1.12 B (2024) | Applies a faster growth trajectory and a broad application set that likely counts more construction and general composites demand, with limited visibility on how resin mix and molded versus pultruded pricing are normalized. |

The table mainly shows that scope and base year choices drive most of the gap, not just different math. When the model is anchored to clear application demand, realistic mix-led pricing, and repeatable checks, the result is easier to reconcile with what buyers and suppliers see in the market year to year.

Key Questions Answered in the Report

How large is the FRP grating market in 2026 and how fast is it growing?

The FRP grating market size reached USD 547.78 million in 2026 and is growing at a 5.12% CAGR toward 2031.

Which region leads global demand for FRP panels?

Asia-Pacific accounts for 47.38% of 2025 revenue and maintains the fastest 5.94% CAGR through 2031.

Which resin type is advancing most rapidly?

Vinyl ester gratings post a 6.24% CAGR as chemical and offshore users pay premiums for greater corrosion resistance.

What end-user sector shows the highest growth?

Waste and water treatment purchases are rising at 6.27% CAGR due to large municipal infrastructure programs.

How concentrated is supplier competition?

The top five vendors control roughly 43% of revenue, reflecting a moderately concentrated landscape that leaves room for regional specialists.

Page last updated on: