Fiber-Reinforced Polymer (FRP) Composites Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

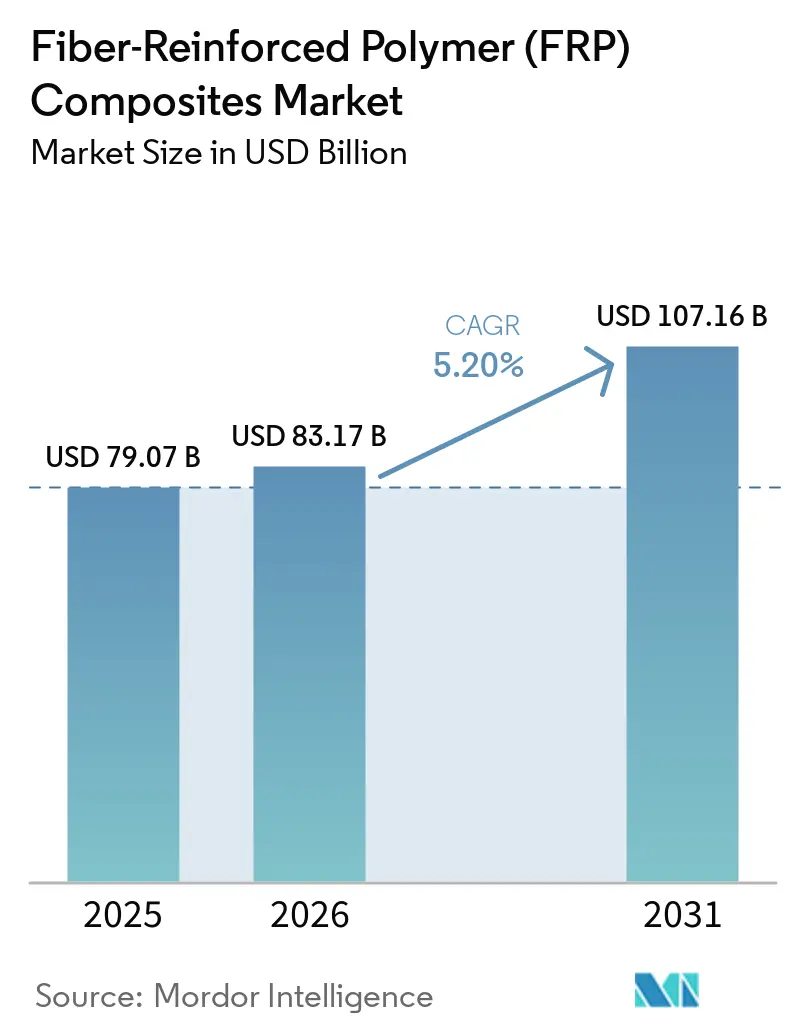

| Market Size (2026) | USD 83.17 Billion |

| Market Size (2031) | USD 107.16 Billion |

| Growth Rate (2026 - 2031) | 5.20% CAGR |

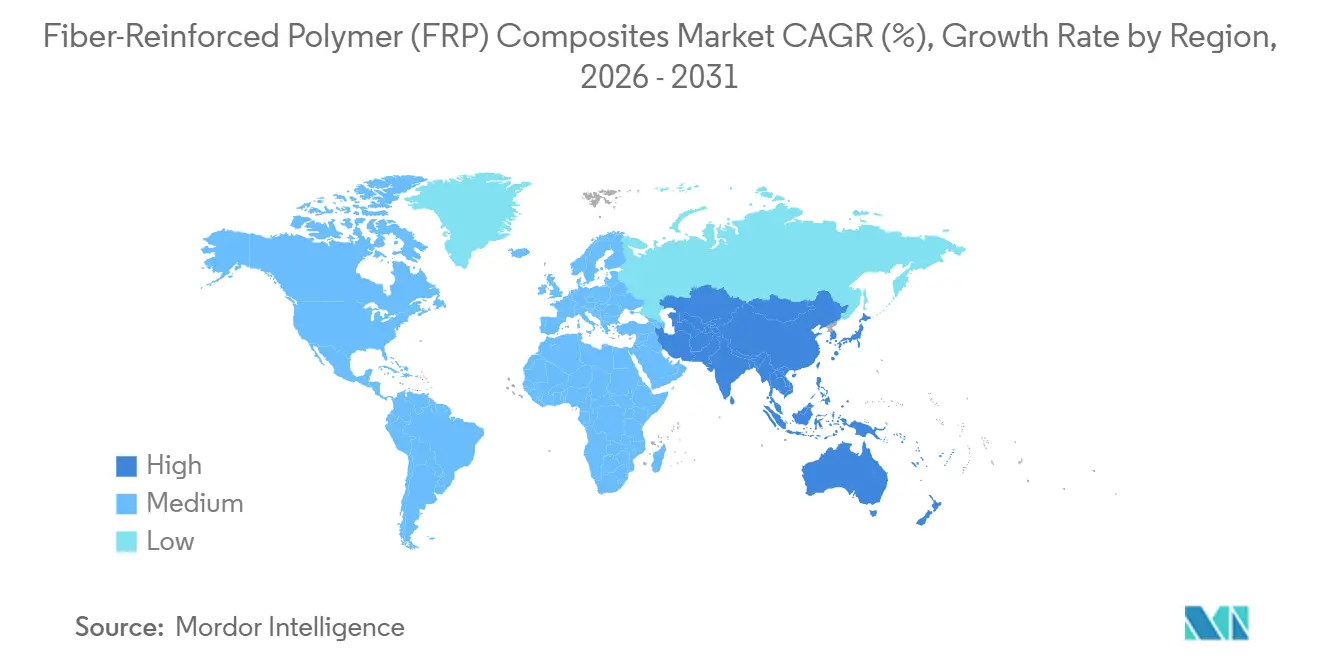

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

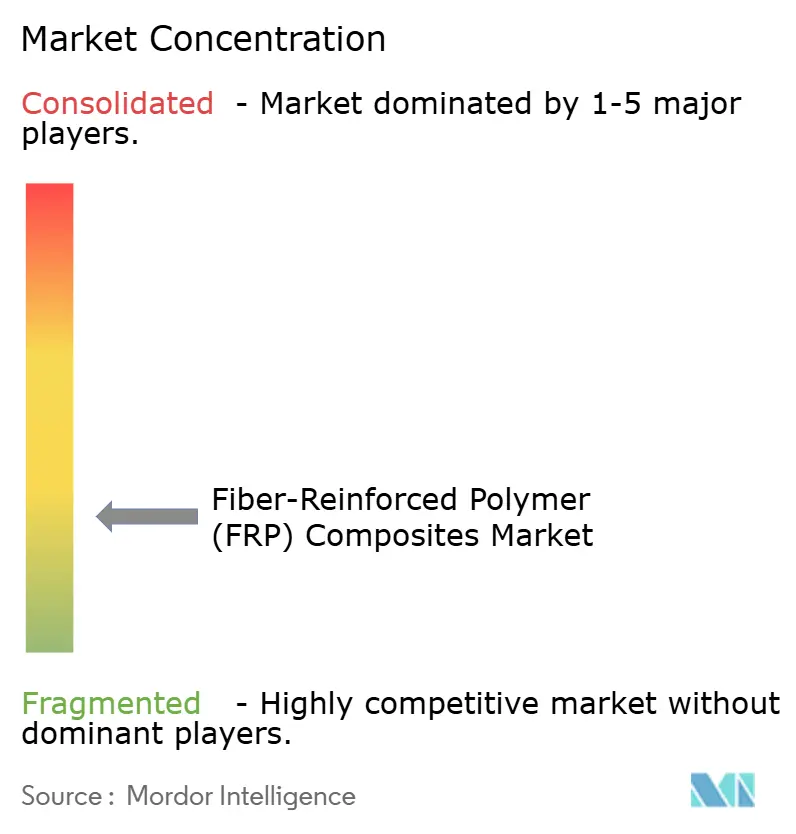

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fiber-Reinforced Polymer (FRP) Composites Market Analysis by Mordor Intelligence

The Fiber-Reinforced Polymer Composites Market size is expected to increase from USD 79.07 billion in 2025 to USD 83.17 billion in 2026 and reach USD 107.16 billion by 2031, growing at a CAGR of 5.20% over 2026-2031. The market is experiencing growth driven by trends such as the increasing adoption of lightweight materials in electric vehicles (EVs), advancements in recyclable thermoplastic matrices, and the rising demand for high-strength materials in aerospace and wind energy applications. Construction spending is shifting toward corrosion-resistant rebar and bridge decks, while the demand for ultra-high-strength GFRP is increasing for wind turbine blades exceeding 120 meters in length. Retrofitting aging infrastructure in regions like the United States, Japan, and the European Union with FRP wraps is also contributing to market growth. The competitive landscape is characterized by innovation in material development and strategic collaborations among key players to address evolving end-user requirements. Opportunities in the market are expanding with the development of advanced FRP materials that offer enhanced performance characteristics, such as improved durability, recyclability, and adaptability to diverse applications. These advancements are opening new avenues in modular construction, 3D-printed structures, and other emerging areas, providing significant potential for market participants to cater to evolving industry demands.

Key Report Takeaways

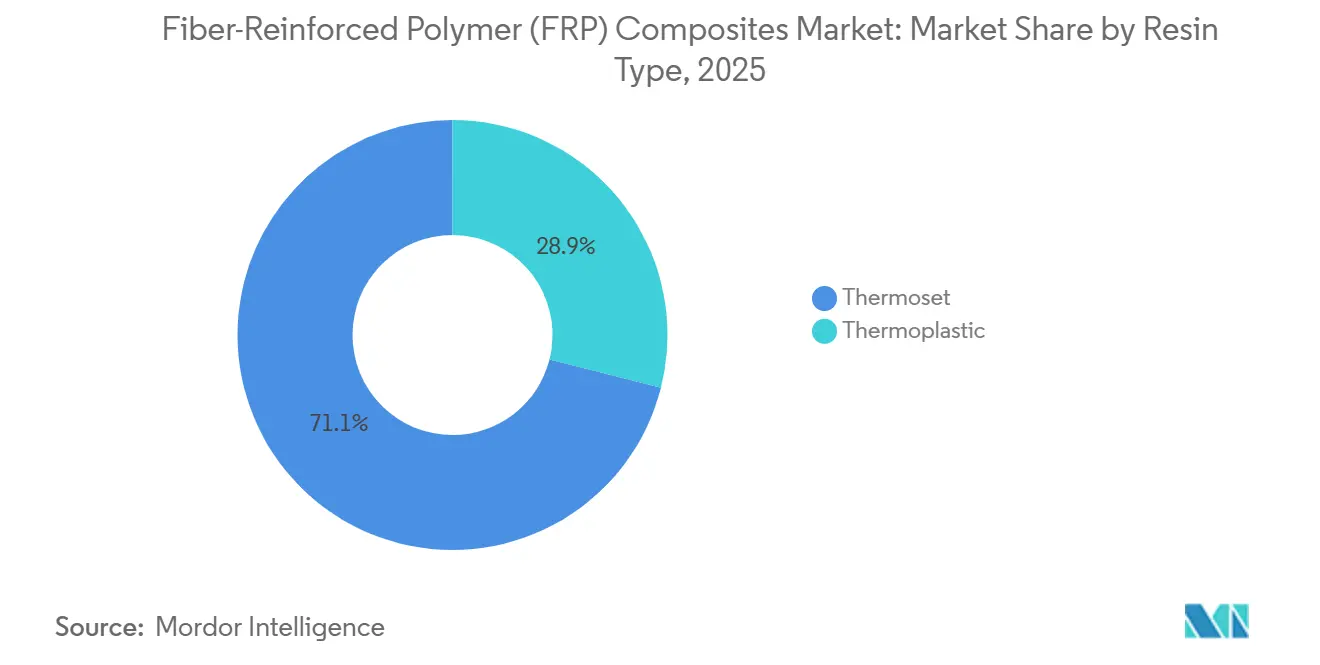

- By resin type, thermoset led with 71.06% of fiber reinforced polymer composites market share in 2025; thermoplastic is forecast to grow at a 6.15% CAGR to 2031.

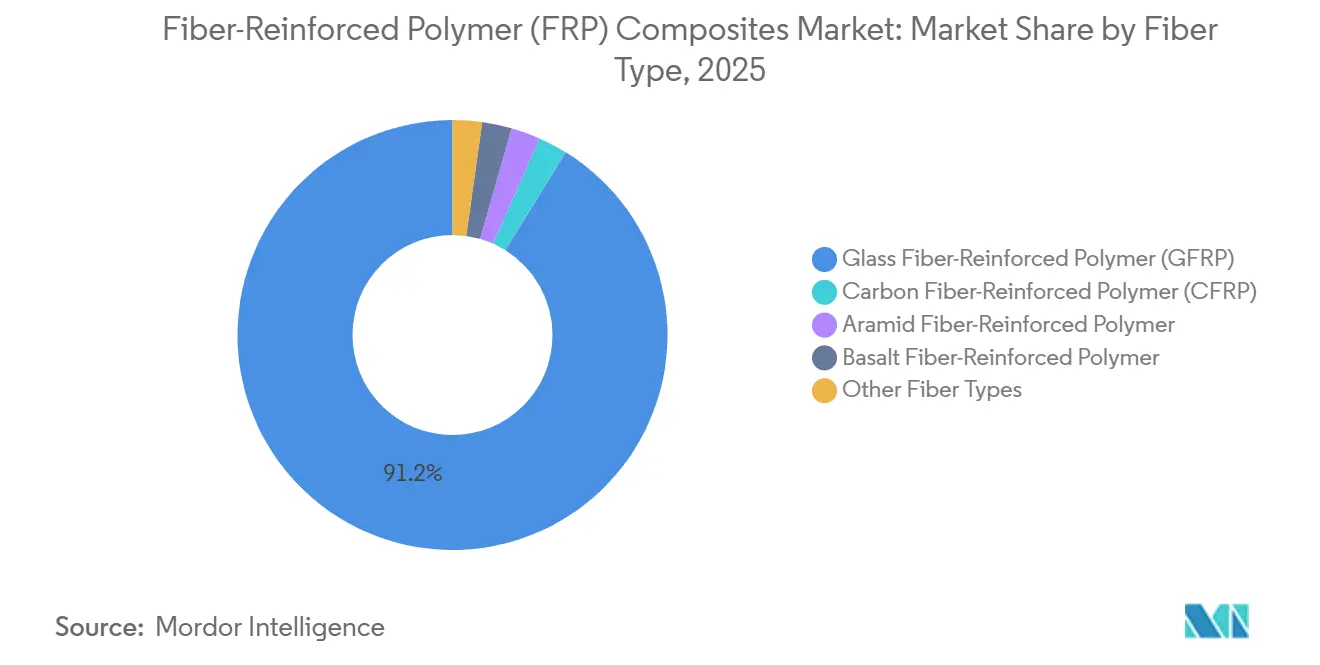

- By fiber type, glass fiber-reinforced polymer (GFRP) captured 91.18% revenue share in 2025, while carbon fiber-reinforced polymer (CFRP) is projected to expand at an 11.14% CAGR through 2031.

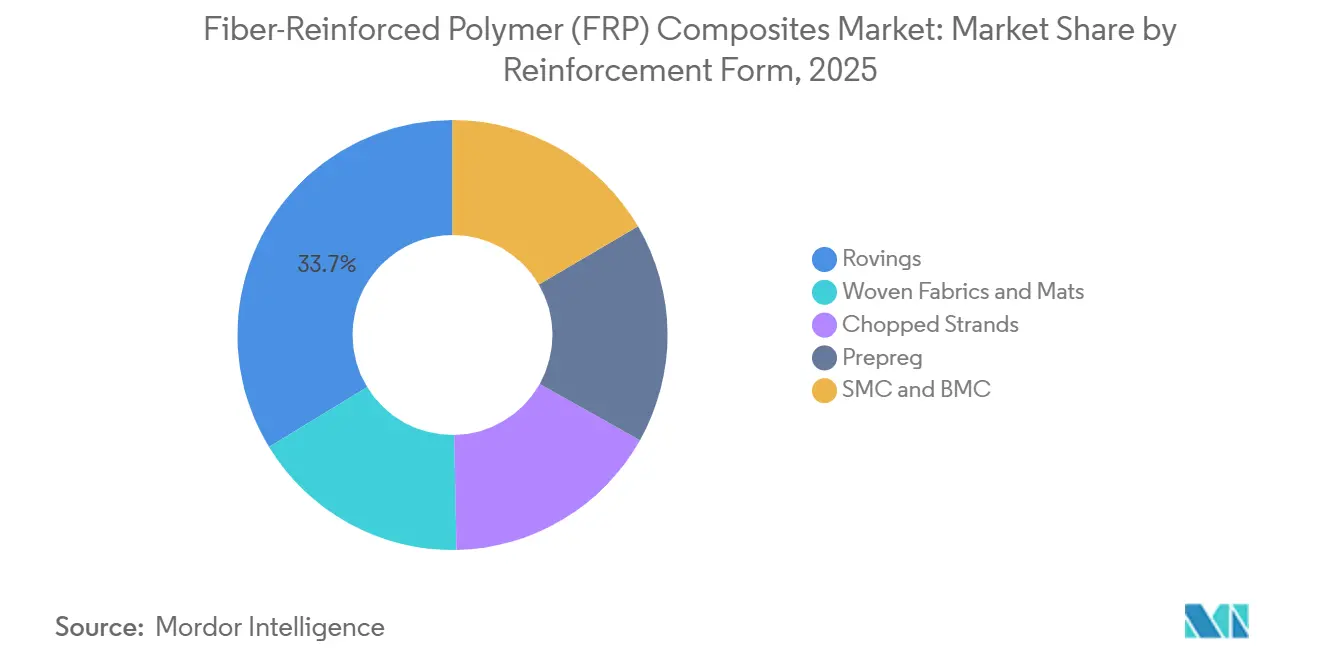

- By reinforcement form, rovings held 33.72% of the fiber reinforced polymer composites market size in 2025 and prepreg is advancing at a 6.26% CAGR to 2031.

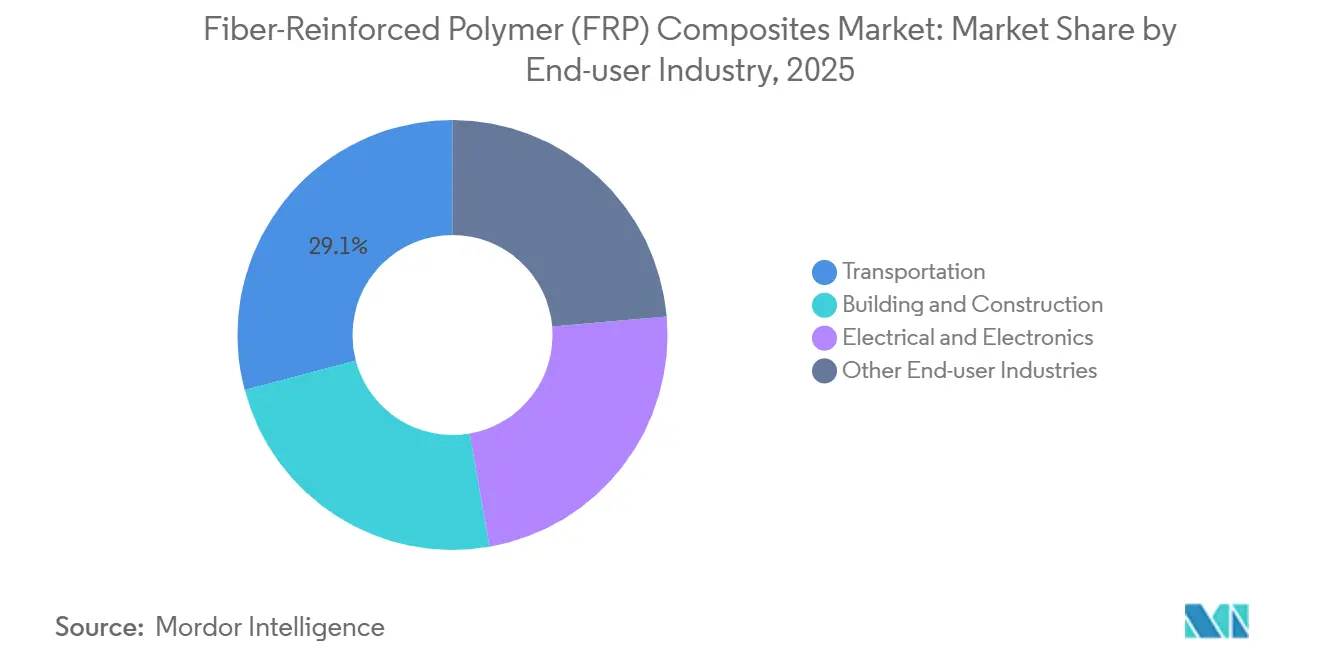

- By end-user industry, transportation accounted for 29.12% share of the fiber reinforced polymer composites market size in 2025 and is progressing at a 5.61% CAGR through 2031.

- By geography, Asia-Pacific held 45.22% revenue share in 2025; the region is forecast to post the highest CAGR at 6.08% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fiber-Reinforced Polymer (FRP) Composites Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction spend shifting to corrosion-free rebar and bridge decks | +0.8% | Global, with concentration in North America, Japan, and Middle East coastal projects | Medium term (2–4 years) |

| Wind-turbine blade length exceeding 120 meters demanding ultra-high-strength GFRP | +1.2% | APAC core (China, India), spill-over to Europe and North America offshore wind | Long term (≥4 years) |

| Lightweighting mandates in EV platforms favoring thermoplastic CFRP | +1.5% | Europe and China, early adoption in North America premium segments | Medium term (2–4 years) |

| Retrofitting of aging bridges in US, Japan, and EU with FRP wraps | +0.6% | North America, Japan, Western Europe | Short term (≤2 years) |

| Modular composite rebar for 3D-printed concrete structures | +0.4% | Middle East, APAC emerging markets, pilot projects in North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Construction Spend Shifting to Corrosion-Free Rebar and Bridge Decks

United States, Japan, and Gulf agencies are increasingly specifying glass- and basalt-fiber rebar to prolong bridge life under chloride attack. In 2025, 42% of the 617,000 U.S. bridges were over 50 years old, and corrosion repairs cost USD 8.3 billion annually, giving GFRP retrofits a 35% life-cycle cost advantage. Japan mandated FRP rebar in coastal highways after 15 years of successful exposure testing along the Tokyo Bay Aqua-Line[1]Ministry of Land, Infrastructure, Transport and Tourism, “Coastal Highway FRP Guidance,” mlit.go.jp . Saudi Arabia’s NEOM project adopted GFRP for 80% of concrete structures to avoid steel oxidation in 45°C ambient conditions. Pultruded bridge decks weigh 75% less than reinforced concrete, reduce foundations by up to 30%, and demonstrated a 40-year design life on West Virginia Route 2 in 2025.

Wind-Turbine Blade Length Exceeding 120 Meters Demanding Ultra-High-Strength GFRP

Turbine makers now deploy rotor diameters above 240 m, which push blade lengths past 120 m and require spar caps with tensile strength over 1,200 MPa. Vestas introduced a 15 MW turbine in 2024 featuring 115.5-m blades incorporating high-modulus glass fiber that cuts blade mass by 8 t per unit. China installed 75 GW of wind capacity in 2025, 60% offshore, and manufacturers shifted to low-void resin-transfer molding to withstand ten-million-cycle fatigue loads. Siemens Gamesa’s thermoplastic RecyclableBlade enables 95% material recovery, aligning with the EU 2028 recycling rule.

Lightweighting Mandates in EV Platforms Favoring Thermoplastic CFRP

European targets of 93.6 g CO₂/km for 2025 vehicles and China’s dual-credit policy motivate OEMs to adopt CFRP battery housings, floor pans, and pillars. BMW’s iX5 Hydrogen uses a PA6-CFRP monocoque saving 150 kg over aluminum while retaining crash integrity. Thermoplastic matrices cut cycle times to under three minutes and allow welding instead of adhesive bonding, reducing assembly labor by 15%. Tesla’s 2025 Cybertruck employs compression-molded CFRP bed liners that trim 22 kg per vehicle. Covestro’s PolyLoop plant recovered 500 t of end-of-life CFRP in 2025 with 90% retained fiber strength, supporting closed-loop car parts.

Retrofitting of Aging Bridges in U.S., Japan, and EU With FRP Wraps

Infrastructure owners wrap deteriorated concrete columns with carbon- or glass-fiber fabrics, restoring capacity for 30–50 years at one-third the replacement cost. The U.S. Bridge Investment Program assigned USD 2.4 billion in 2025, with 18% for FRP wraps on 1,200 West-Coast bridges. Japan’s expressway operator raised shear strength by 60% using Torayca carbon fabric on 340 piers in 2025. Italy applied basalt-fiber wraps on 85 viaduct columns, achieving a cost-effective corrosion barrier. Florida measured zero chloride ingress on wrapped columns of the Seven Mile Bridge over five years.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile carbon-fiber prices hurting automotive cost targets | -0.9% | Global, acute in North America and Europe automotive clusters | Short term (≤2 years) |

| Availability of metal and engineered-wood substitutes | -0.5% | North America and Europe construction, Asia-Pacific infrastructure | Medium term (2–4 years) |

| EU end-of-life recycling gap triggering landfill restrictions | -0.3% | Europe, emerging in California and Japan | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatile Carbon-Fiber Prices Hurting Automotive Cost Targets

Export restrictions on Russian polyacrylonitrile raised precursor prices 18% in 2025, forcing OEMs to absorb USD 4–6 per-kg increases that jeopardize sub-USD 35,000 EV programs. Toyota replaced planned CFRP roof panels on the 2026 Prius with aluminum to protect margins. SGL Carbon and Toray fixed five-year offtake contracts at 12% above 2024 spot prices, transferring volatility upstream. Recycled fiber from ELG retains 90% strength at 40% below virgin cost but suits only non-structural parts. Hexcel shifted 30% of precursor output to a lower-cost U.S. site to blunt European energy spikes.

EU End-of-Life Recycling Gap Triggering Landfill Restrictions

The 2025 EU Waste Framework Directive classifies thermoset scrap as non-recyclable unless processed by certified routes, yet only 12% of 280,000 t composite waste enters approved facilities[2]European Commission, “Waste Framework Directive 2025 Revision,” europa.eu . Wind-blade decommissioning will generate 2.8 million t of scrap by 2035, but pyrolysis plants operate at 15% utilization because sub-USD 80 tipping fees do not cover USD 120 processing costs. Veolia opened a 10,000 t solvolysis plant recovering 98% fiber, although high-temperature processing adds USD 2.50 kg to recycled material costs. California banned composite landfill disposal in 2025, compelling boat builders to stockpile hulls until commercial capacity expands. Japan proposed an extended-producer-responsibility levy of 3% product revenue to fund take-back schemes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Thermoplastics Gain on Recyclability and Speed

Thermoset held 71.06% of 2025 revenue, dominated by epoxy and polyester chemistries specified for corrosion resistance and low-cost open-mold processing. Epoxy captured high thermoset demand because its superior adhesion pairs with carbon fiber in aerospace prepregs. Polyester served in cost-driven marine and tank markets, while vinyl ester filled in highly corrosive chemical plants.

Thermoplastic will grow at 6.15% CAGR through 2031 as carmakers pivot to recyclable matrices. Polypropylene compounds reinforced with 40% glass fiber now form door-module carriers that cut weight 35% and mold in 90 seconds at annual volumes above 500,000 units. Polyamide 6 and 66 secure thermoplastic revenue for under-hood parts operating up to 150 °C. High-performance PEEK, though costly, expanded in aircraft seat structures that demand flame-smoke-toxicity compliance. Covestro’s PolyLoop recovered 500 t of end-of-life PA6-CFRP in 2025 with 90% strength retention, proving a closed-loop route unavailable to thermosets. BMW combines thermoplastic skins with epoxy cores in battery covers for higher impact absorption while retaining stiffness, illustrating hybrid architectures that deepen fiber reinforced polymer composites market adoption.

By Fiber Type: CFRP Surges in Aerospace and Premium EVs

Glass Fiber-Reinforced Polymer (GFRP) accounted for 91.18% of 2025 volume because its USD 2.50/kg cost and 2,400 MPa tensile strength satisfy construction, wind, and marine needs. China Jushi raised capacity to 3.2 million t in 2025, lowering glass fiber prices 8% and squeezing Western suppliers.

Carbon Fiber-Reinforced Polymer (CFRP) will expand at an 11.14% CAGR to 2031 as aerospace OEMs ramp composite airframes and premium EVs adopt structural battery enclosures. Boeing’s 787 and Airbus A350 programs jointly consumed 3,000 t of fiber in 2025. Porsche’s 2024 Taycan roof and bulkhead lowered center-of-gravity 12 mm, validating structural performance premiums. Standard-modulus grades delivered higher CFRP volume, while high-modulus variants served satellites and Formula 1 monocoques requiring more than 200 GPa stiffness-to-weight ratios. Basalt fiber is used for fire-resistant tunnel linings, retaining 85% strength at 600 °C.

By Reinforcement Form: Prepregs Accelerate in Aerospace

Rovings commanded 33.72% of 2025 revenue and remain vital for filament-wound pressure vessels, piping, and bridge decks where continuous orientation yields hoop strength over 1,000 MPa. Spray-up rovings persist in cost-focused marine parts, yet styrene-emission rules spur a gradual shift to closed molds.

Prepreg will grow 6.26% CAGR through 2031 as out-of-autoclave (OOA) aerospace programs scale. Hexcel’s 120 °C-curing OOA system for Boeing 777X wing skins trimmed part cost 35% by eliminating high-pressure autoclaves. Thermoplastic prepregs support three-minute press cycles; Toray’s PPS-based sheet enabled BMW to merge 12 aluminum parts into one compression-molded battery tray. Sheet- and bulk-molding compounds retain relevance for high-volume automotive hoods and seat backs where cycle times under four minutes are mandatory.

By End-user Industry: Transportation Leads on Lightweighting

Transportation controlled 29.12% share in 2025 and is poised for a 5.61% CAGR as regulators tighten emissions and range metrics. General Motors trimmed 48 kg from the 2025 Cadillac Celestiq with CFRP roof and quarter panels, enabling a 520 km range from a 111 kWh battery. Wabash National’s molded-structural-composite trailers weigh 680 kg less than aluminum and recoup the USD 3,200 premium within 18 months via payload gains.

Building and construction is expanding due to corrosion-proof rebar and pultruded profiles. Florida’s Brightline guideways use GFRP to reach 75-year design lives. Electrical and electronics is also growing thanks to epoxy-glass laminates that satisfy UL 94 V-0 and 20 kV/mm dielectric needs across 850 million m² of printed-circuit-board output in 2025. Marine, sports, and consumer goods round out segment demand, leveraging salt-water resistance and lightweight benefits.

Geography Analysis

Asia-Pacific dominated the fiber reinforced polymer composites market with a 45.22% share in 2025 and is projected to grow at 6.08% CAGR. China’s 75 GW wind additions used 18 kg GFRP per kW and spurred 520,000 t of new glass-fiber capacity by regional leaders. India’s USD 1.4 trillion National Infrastructure Pipeline allocates 12% to corrosion-resistant materials, translating to 180,000 t annual GFRP rebar demand by 2028. Japan now mandates FRP rebar in coastal highways after 15-year exposure trials proved zero degradation.

In North America, U.S. Bridge Investment Program earmarked USD 2.4 billion in 2025, with 18% for FRP wraps on 1,200 bridges. Boeing’s South Carolina and Washington plants consumed 1,200 t CFRP for 787 and 777X programs in 2025. Ontario attracted USD 420 million composite capital as GM and Stellantis localized EV underbody parts.

In Europe, Germany installed 8.2 GW of wind capacity in 2025, 55% offshore, demanding blades above 100 m with hybrid carbon-glass spar caps. The EU Waste Framework Directive requires 25% recycled content in composites by 2028, triggering EUR 38 million pyrolysis investments by Owens Corning and Veolia. Airbus increased A350 output to nine per month, adding 1,800 t CFRP demand at Stade and Illescas.

South America captured demand as Brazil’s wind fleet reached 28 GW with 85% located in high-capacity Northeast zones demanding 9,600 t GFRP blades in 2025. Middle East and Africa together held lower share yet promise growth in the near future. Saudi Arabia’s NEOM calls for 140,000 t GFRP rebar through 2030. South Africa added 3.2 GW wind capacity in 2024-2025, with Siemens Gamesa supplying 115-m blades using 16 kg GFRP per kW.

Competitive Landscape

The market is fragmented; the top five suppliers controlled 33% combined revenue in 2025. Owens Corning, Toray Industries, Hexcel Corporation, Teijin, and SGL Carbon pursue vertical integration and specialty-grade innovation to defend margins against cost-focused regional glass-fiber producers. Toray’s chain from PAN precursor to prepreg secures 18% gross margins versus 12% for non-integrated rivals. The 2024 purchase of a 35% stake in Zoltek added 12,000 t low-cost fiber capacity for automotive programs. Owens Corning’s WindStrand HM fiber raises stiffness 20% over E-glass, targeting more than 120 m blades where S-glass is too expensive.

Hexcel’s out-of-autoclave prepreg cures at 120 °C and atmospheric pressure, lowering aerospace part costs 35% and winning 60% of Boeing 777X wing-skin volume in 2024. Patent filings indicate recycled-fiber sizing agents as an emerging arena; SGL Carbon lodged 14 patents in 2024-2025 that restore 95% interfacial shear strength for recycled carbon fiber, lifting structural viability.

Regional challengers undercut pricing: India’s Kemrock raised GFRP rebar output by 18,000 t in 2025 and bid 25% below Western suppliers in Middle East tenders. China’s Weihai Guangwei supplies 40% of domestic wind-blade preforms at 30% less than European peers, pressuring incumbents to accelerate specialty-grade launches. Mitsubishi Chemical’s pilot lignin-epoxy achieved 35% bio-content in auto interior panels without losing flame retardancy, expanding bio-based white space ahead of EU 2028 mandates.

Fiber-Reinforced Polymer (FRP) Composites Industry Leaders

Owens Corning

TORAY INDUSTRIES, INC.

Hexcel Corporation

China Jushi Co., Ltd.

Gurit Services AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: The American Composites Manufacturers Association (ACMA) announced the completion of a new Product Category Rule (PCR) for Fiber Reinforced Polymer (FRP) Composite Products, specifically for Rebar or Dowel Bars. The newly developed PCR allowed FRP rebar manufacturers to create Environmental Product Declarations (EPDs) for their products.

- October 2025: TORAY INDUSTRIES, INC. developed a recycling technology capable of decomposing various carbon fiber reinforced plastics (CFRP) made from thermosetting resins while preserving the strength and surface quality of the fibers. Utilizing this technology, the company produced a nonwoven fabric using recycled carbon fibers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the fiber-reinforced polymer (FRP) composites market as the sale of new, virgin polymer matrices, thermoset or thermoplastic, reinforced with continuous or chopped glass, carbon, aramid, basalt, or natural fibers and supplied in intermediate forms (rovings, fabrics, mats, prepregs, SMC/BMC) or finished molded parts that enter end-use industries such as transportation, building and construction, electrical, and wind energy. According to Mordor Intelligence, revenues are tracked at manufacturers' invoice value and expressed in constant 2025 dollars.

Scope Exclusion: Components made with metal or ceramic matrices, recycled FRP scrap trading, and on-site repair wrap services are outside our numbers.

Segmentation Overview

- By Resin Type

- Thermoset

- Thermoplastic

- By Fiber Type

- Glass Fiber-Reinforced Polymer (GFRP)

- Carbon Fiber-Reinforced Polymer (CFRP)

- Aramid Fiber-Reinforced Polymer

- Basalt Fiber-Reinforced Polymer

- Other Fiber Types

- By Reinforcement Form

- Rovings

- Woven Fabrics and Mats

- Chopped Strands

- Prepreg

- SMC and BMC

- By End-user Industry

- Transportation

- Building and Construction

- Electrical and Electronics

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed resin formulators, pultruders, tier-one auto molders, and wind-blade OEM engineers across Asia-Pacific, Europe, and North America. These calls and short surveys clarified average selling prices, scrap rates, and emerging thermoplastic penetration, letting us tighten every assumption flagged during secondary review.

Desk Research

We began with open datasets from bodies such as the US Geological Survey (glass fiber minerals), the World Wind Energy Association, OICA vehicle production tables, UN Comtrade trade codes for HS-6815/3920, and Eurostat construction output. These volumes and price clues, read alongside association white papers from JEC Group and the American Composites Manufacturers Association, give us baseline demand direction. Our team then mined company 10-Ks, investor decks, and patent counts (Questel) to benchmark capacity additions and resin substitution rates. D&B Hoovers and Dow Jones Factiva provided revenue splits that tie public statistics to supplier balance sheets. This list is illustrative; many other public and paid sources informed the desk phase.

Market-Sizing & Forecasting

We reconstruct apparent consumption through a top-down blend of production and trade data, which is then sense-checked with sampled supplier roll-ups and channel ASP × volume calculations. Key variables in the model include light-vehicle build forecasts, annual installed wind capacity, regional infrastructure capex indices, average glass-fiber price per kilogram, resin-to-fiber mix shifts, and end-use weight-reduction targets. A multivariate regression links these drivers to historical market value. Exponential smoothing carries short-run shocks forward before scenario analysis adjusts for policy or raw-material swings. Bottom-up gaps, for instance, in specialty CFRP niches, are bridged with expert price-volume estimates collected during primary research.

Data Validation & Update Cycle

We run three-layer variance checks, compare outputs with independent indicators (energy blade production, freight car builds), and hold peer reviews before sign-off. Reports refresh yearly, while any material event triggers a mid-cycle revisit so clients receive the freshest view.

Why Mordor's Fiber-Reinforced Polymer Composites Baseline Commands Reliability

Published estimates often diverge because firms pick different inclusion rules, price bases, and refresh schedules.

Key gap drivers are wider scope choices; some studies fold high-performance composites or repair wraps into totals, reliance on single-pass top-down math without supplier cross-checks, aggressive ASP inflation assumptions, and less frequent updates that miss fast moves in Asia-Pacific resin spreads.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 79.06 Bn (2025) | Mordor Intelligence | - |

| USD 104.3 Bn (2024) | Global Consultancy A | Includes high-performance and hybrid composites; limited primary validation |

| USD 98.12 Bn (2024) | Industry Publication B | Uses list prices; annual refresh every two years |

| USD 105.22 Bn (2025) | Trade Journal C | Counts retrofit repair wraps and recycled volumes |

These comparisons show that our disciplined scope selection, live primary touchpoints, and yearly recalibration give decision-makers a balanced baseline they can trace back to clear variables and replicate with confidence.

Key Questions Answered in the Report

What is value of the fiber reinforced polymer composites market?

What is the value of the fiber reinforced polymer composites market?

Which region shows the fastest composite demand growth to 2031?

Asia-Pacific, supported by wind-energy expansion and large infrastructure programs, is expected to grow at a 6.08% CAGR.

Why are thermoplastic composites gaining share in automotive applications?

Thermoplastics offer three-minute cycle times, recyclability, and weldability that cut assembly labor 15%, aligning with EV lightweighting targets.

How much share did glass fiber hold in 2025?

Glass fiber-reinforced polymer commanded 91.18% of global composite volume in 2025.

Page last updated on: