Photoinitiator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

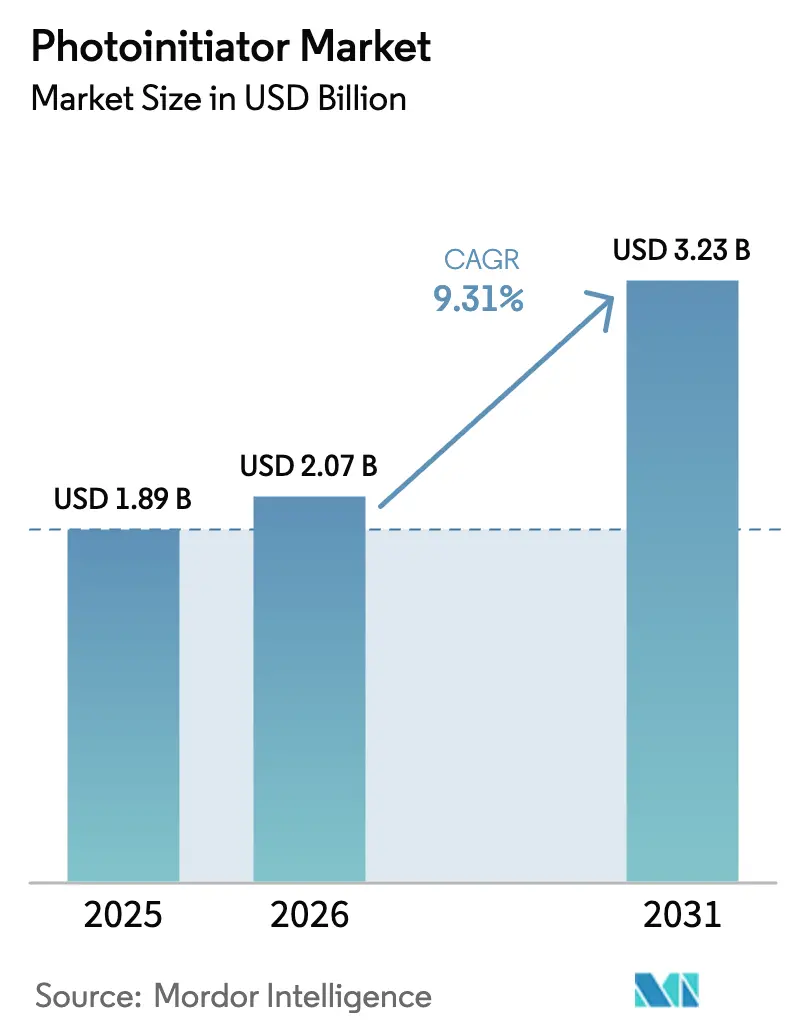

| Market Size (2026) | USD 2.07 Billion |

| Market Size (2031) | USD 3.23 Billion |

| Growth Rate (2026 - 2031) | 9.31% CAGR |

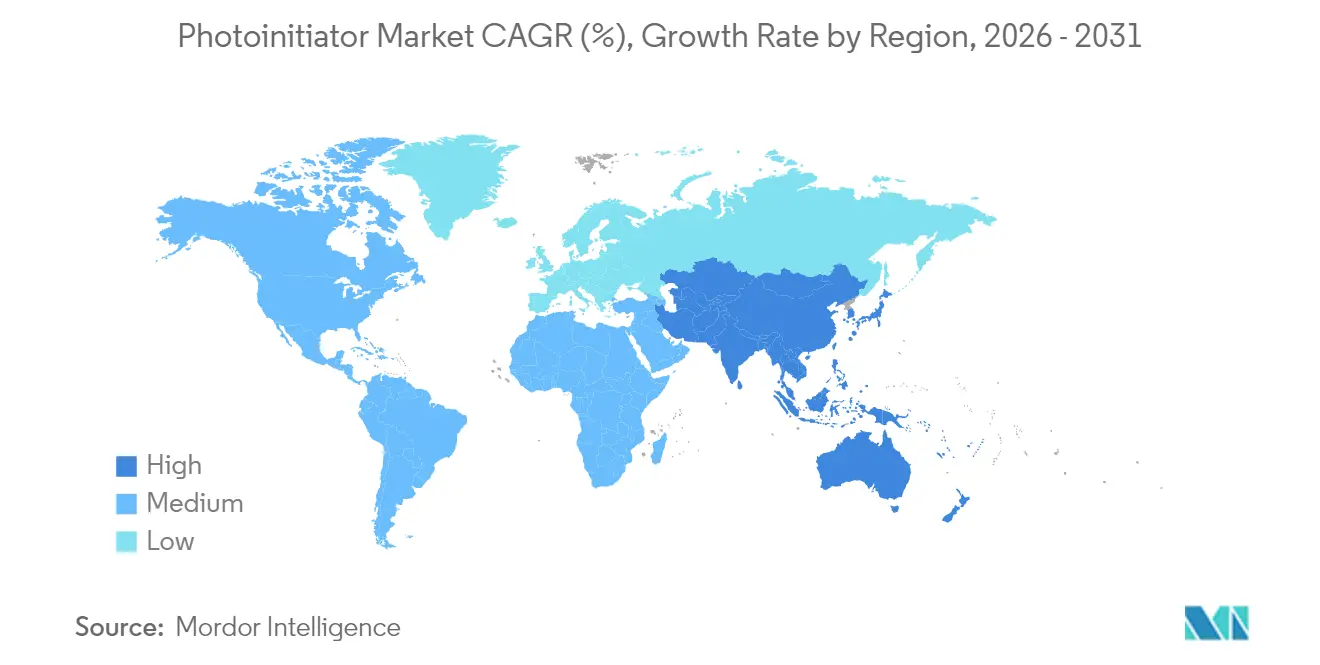

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Photoinitiator Market Analysis by Mordor Intelligence

Photoinitiator market size in 2026 is estimated at USD 2.07 billion, growing from 2025 value of USD 1.89 billion with 2031 projections showing USD 3.23 billion, growing at 9.31% CAGR over 2026-2031. LED-centric curing processes are replacing broad-spectrum mercury lamps, so formulators are redesigning photoinitiator packages to absorb efficiently at 365 nm-405 nm wavelengths. Demand is also expanding as UV curing migrates from coatings and printing into electronics assembly, 3D printing, and biomedical devices. Manufacturers that master LED compatibility, low migration, and regulatory compliance now differentiate themselves, while raw-material volatility for acylphosphine oxides adds cost pressure. Asia Pacific remains the manufacturing nerve center, keeping the photoinitiator market tightly linked to regional electronics and packaging supply chains.

Key Report Takeaways

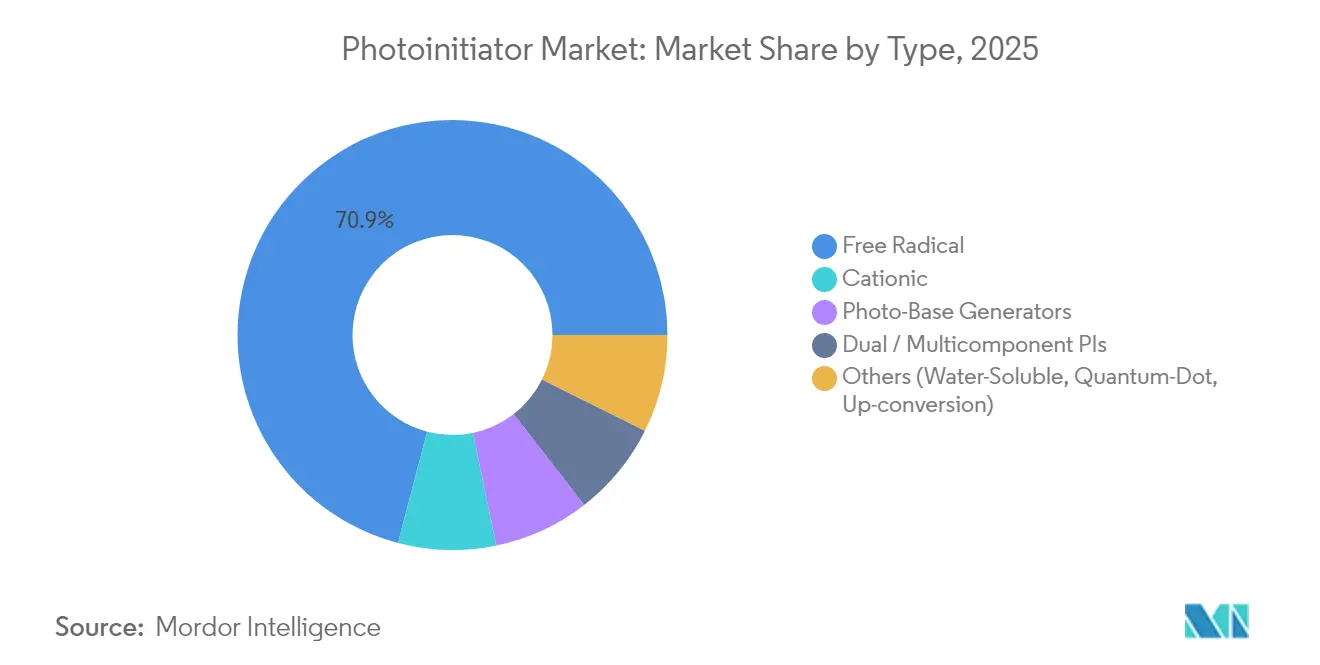

- By type, free-radical photoinitiators held 70.92% of photoinitiator market share in 2025, and the segment is tracking a 10.12% CAGR through 2031.

- By light source, UV mercury lamps accounted for 54.60% of the photoinitiator market size in 2025, but UV-LED systems post the fastest growth at a 9.98% CAGR.

- By application, coatings delivered 43.78% revenue share in 2025, while 3D printing and additive manufacturing is projected to expand at a 10.05% CAGR.

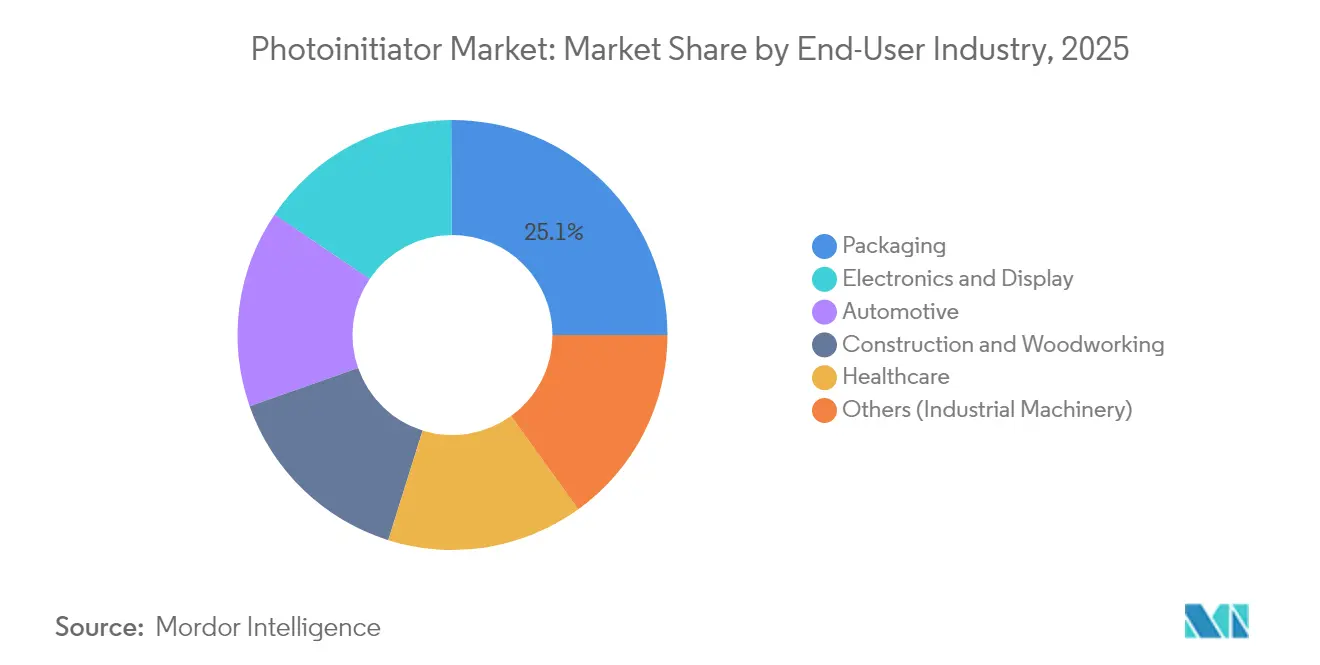

- By end-user industry, packaging captured 25.10% of the photoinitiator market size in 2025, whereas electronics and display applications lead in growth at 10.74% CAGR.

- By geography, Asia Pacific commanded 39.55% of the photoinitiator market share in 2025 and is set to climb at an 11.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Photoinitiator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand from UV-LED printing & packaging | +2.8% | Global, with concentration in Asia Pacific and Europe | Medium term (2-4 years) |

| Expansion of 3D-printing photopolymers | +2.1% | North America & Europe, expanding to Asia Pacific | Long term (≥ 4 years) |

| Growth of dental & biomedical light-curing applications | +1.6% | Global, with premium segments in developed markets | Medium term (2-4 years) |

| Regulatory push for VOC-free industrial coatings | +1.4% | North America & EU, with spillover to Asia Pacific | Short term (≤ 2 years) |

| In-line UV curing in high-speed electronics assembly | +1.2% | Asia Pacific core, with expansion to Mexico and Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand from UV-LED Printing & Packaging

UV-LED units deliver narrow-band light at 365-405 nm with higher photon density, so packaging converters must switch to initiators such as bis(2,4,6-trimethylbenzoyl)-phenylphosphine oxide (BAPO) that show strong absorption in that window and photobleach rapidly for deep cures. Food-contact compliance intensifies the need for low-migration grades, and the regulatory direction in the United States and European Union continues to tighten VOC limits, accelerating the LED shift[1]Environmental Protection Agency, “National Volatile Organic Compound Emission Standards for Aerosol Coatings,” epa.gov. Suppliers investing early in LED-ready chemistries gain favored status in pressroom retrofits across label and flexible-packaging lines.

Expansion of 3D-Printing Photopolymers

Digital light processing (DLP) and stereolithography (SLA) printers now move into manufacturing volumes, demanding initiators that perform in pigmented, high-viscosity, or ceramic-filled resins without sacrificing dimensional fidelity. Water-soluble charge-transfer packages enable cell-friendly hydrogel builds, while low-loading (0.1-0.5 wt%) BAPO formulations deliver stronger mechanical properties and faster layer times than legacy camphorquinone systems.

Growth of Dental & Biomedical Light-Curing Applications

Dental composites are trending away from yellow-tint camphorquinone toward acylphosphine oxides such as TPO and BAPO that cure under 405 nm LEDs and keep shades neutral. Yet cytotoxicity screening shows notable variance: BAPO rates highest in cellular stress, whereas MBF and TPOL record safer profiles, pushing formulators to balance cure kinetics and biocompatibility. Germanium-based initiators offer lower toxicity and red-shifted absorption but remain costly and niche.

Regulatory Push for VOC-Free Industrial Coatings

North American and European standards for architectural and maintenance coatings now cap VOCs so tightly that 100% solids UV systems have become the rule for metal and plastic components. BAPO-driven polyurethane acrylates meet corrosion and scratch thresholds without solvents, while thiol-ene-based waterborne UV coatings achieve full cure in sunlight with just 3 wt% initiator loading. Upconversion nanoparticle-assisted systems also open near-infrared curing for sections thicker than 2.5 cm.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Toxicity concerns on benzophenone & TPO derivatives | -1.8% | Global, with stricter enforcement in North America & EU | Short term (≤ 2 years) |

| Rising raw-material prices for acylphosphine oxides | -1.2% | Global, with particular impact on cost-sensitive Asian markets | Medium term (2-4 years) |

| Supply bottlenecks for specialty photoinitiator precursors | -0.8% | Global, with concentration risk in specialized chemical suppliers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Toxicity Concerns on Benzophenone & TPO Derivatives

Health Canada has listed benzophenone as toxic under Schedule 1, citing potential kidney and liver impacts, and regulators weigh similar moves on TPO derivatives, spurring converters to phase down suspect grades[2]Government of Canada, “Risk Management Scope for Benzophenone,” canada.ca. To stay ahead, formulators explore benzoxazin-2-one scaffolds that keep quantum yields high while avoiding classification triggers.

Rising Raw-Material Prices for Acylphosphine Oxides

A narrow global producer base for organophosphorus intermediates means outages or freight spikes flow straight into BAPO or TPO-L pricing. Trade actions on epoxy system inputs during 2024 added further volatility, so resin blenders began trialing liquid BAPO variants that ease handling and dosing but still command premiums.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Free-Radical Dominance Drives Innovation

Free-radical initiators generated 70.92% of the photoinitiator market in 2025 and are projected to grow at 10.12% CAGR to 2031. Their compatibility with acrylate and methacrylate systems underpins coatings, inks, and 3D-printing resins across every region. Cationic initiators retain niches in electronics encapsulation and fiber-optic coatings that require low shrinkage, while emerging photo-base generators crack oxygen inhibition issues in high-flex applications.

Structure-guided design now yields acyldiphenylphosphine oxide (ADPO) variants that absorb strongly at 395 nm but release lower yellowing by-products than legacy BAPO grades. Two-component systems pairing iodonium salts with meta-terphenyl photosensitizers further expand visible-light possibilities. As a result, the photoinitiator market size for free-radical grades could surpass USD 2.24 billion by 2031 if adoption stays on its present curve.

By Light-Source Compatibility: LED Transition Accelerates

Although mercury lamps still occupy 54.60% of installed curing lines, LED modules now anchor new investments and will post a 9.98% CAGR. Their cool operation, instant on-off cycling, and lower energy draw resonate with converters under carbon-reduction mandates. The shift forces formulators to tailor absorption peaks: coumarin-iodonium hybrids respond at 365 nm, carbazolyl α-diketones perform under 405 nm-460 nm, and upconversion strategies unlock 780 nm-wavelength curing.

Within five years, the photoinitiator market size linked to LED platforms is expected to overtake mercury lamp demand, even though legacy lines will run until bulbs sunset. Suppliers balancing dual-platform portfolios will buffer revenue volatility during this crossover.

By Application: Coatings Leadership Faces 3D-Printing Disruption

Coatings represented 43.78% of the photoinitiator market in 2025 and remain the cash generation backbone. Automotive clearcoats, metal cans, and wood flooring all exploit UV curing for throughput, durability, and VOC compliance. Metal substrates especially benefit as 100% acrylate films achieve full hardness in seconds and provide superior chip resistance.

However, 3D printing posts the highest momentum at a 10.05% CAGR. The photoinitiator market share for additive processes may still be single digits, yet production-scale SLA and DLP lines demand initiators capable of curing pigmented or ceramic-filled slurries without warpage. Safranin-triggered three-component packages deliver high resolution and low shrinkage, positioning them for aerospace and dental molds.

By End-User Industry: Electronics Growth Outpaces Packaging Base

Packaging held 25.10% of the photoinitiator market in 2025 thanks to labels, folding cartons, and flexible films that rely on rapid-cure inks. But electronics and displays will outstrip all other sectors at an 10.74% CAGR. Semiconductor fabs specify ultra-pure initiators with controlled ionic content to protect wafer yields, and display makers need formulations that avoid migration under high brightness operation.

Medical devices and dental products occupy a premium niche demanding ISO 10993 compliance and blue-light cures to minimize thermal load on tissues. Automotive growth stems from UV-bonded glass, battery potting, and scratch-resistant interiors, extending photoinitiator penetration beyond exterior clearcoats.

Geography Analysis

Asia Pacific controlled 39.55% of the photoinitiator market in 2025 and should post 11.02% CAGR until 2031. China anchors PCB and display production, Japan refines high-purity grades for photoresist makers, and South Korea drives demand from advanced memory and OLED lines. The photoinitiator market size in Asia could exceed USD 1.28 billion by 2031 as regional converters invest in LED retrofits to curb energy usage.

North America focuses on high-value, regulated niches - aerospace composites, healthcare disposables, and specialty graphics - where performance counts more than cost. BASF’s shift toward bio-based ethyl acrylate underpins a broader trend to embed renewable monomers in UV systems, and the United States Food and Drug Administration’s migration limits guide photoinitiator selection.

Europe prioritizes REACH compliance and circular-economy goals. Automakers headquartered in Germany and France adopt UV coatings to shorten bake cycles and lower CO₂ footprints. Legislators’ scrutiny of benzophenone, TPO, and potential endocrine disruptors keeps European formulators on a fast track to safer scaffolds. Consequently, the region invests heavily in quantum-dot and bio-based photoinitiator R&D.

Competitive Landscape

The photoinitiator market remains moderately concentrated. BASF, Arkema, and IGM Resins hold solid portfolios spanning free-radical, cationic, and specialty LED grades. Arkema’s EUR 45 million acquisition of Lambson in 2019 strengthened its composite and 3D-printing line-card. BASF leverages upstream monomer integration to cushion raw-material spikes, while IGM Resins differentiates through regional production and custom blends.

Asian suppliers such as Changzhou Tronly and Tianjin Jiuri compete fiercely on commodity free-radical initiators, benefiting converters sensitive to cost. Specialty entrants target migration-safe or water-dispersible chemistries; Everlight Chemical’s 2023 launch of a water-compatible initiator illustrates this niche strategy. Intellectual-property filings in acylgermane and carbide-based initiators indicate a pipeline of visible-light solutions poised to challenge incumbents.

Photoinitiator Industry Leaders

Arkema

IGM Resins

Tianjin Jiuri New Materials Co. Ltd

BASF

ADEKA Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2023: Due to continued significant increases in costs, IGM Resins announced a price increase on its Omnirad, Esacure, and Omnipol photoinitiator portfolio. Global geopolitical events have caused sustained pressure and have increased the costs to unprecedented levels.

- January 2023: Everlight Chemical introduced a water-based photoinitiator that disperses rapidly in aqueous coatings, cutting UV energy demand and shortening exposure times.

Global Photoinitiator Market Report Scope

A photoinitiator is a molecule that creates reactive species when exposed to radiation. Synthetic photoinitiators are critical components in photopolymers. Some small molecules in the atmosphere can also act as photoinitiators by decomposing to give free radicals. The photoinitiator market is segmented by type, application, and geography. By type, the market is segmented into free radical and cationic. By application, the market is segmented into adhesives, ink, coating, and other applications. The report covers the market size and forecast for the photoinitiator agent market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done based on value (USD million).

| Free Radical |

| Cationic |

| Photo-Base Generators |

| Dual / Multicomponent PIs |

| Others (Water-Soluble, Quantum-Dot, Up-conversion) |

| UV Mercury Lamps |

| UV-LED (UVA) |

| Visible-LED / Blue Light |

| Near-Infrared (Up-conversion Assisted) |

| Adhesives and Sealants |

| Printing Inks |

| Coatings |

| 3D Printing / Additive Manufacturing |

| Others |

| Packaging |

| Automotive |

| Construction and Woodworking |

| Healthcare |

| Electronics and Display |

| Others (Industrial Machinery) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Free Radical | |

| Cationic | ||

| Photo-Base Generators | ||

| Dual / Multicomponent PIs | ||

| Others (Water-Soluble, Quantum-Dot, Up-conversion) | ||

| By Light-Source Compatibility | UV Mercury Lamps | |

| UV-LED (UVA) | ||

| Visible-LED / Blue Light | ||

| Near-Infrared (Up-conversion Assisted) | ||

| By Application | Adhesives and Sealants | |

| Printing Inks | ||

| Coatings | ||

| 3D Printing / Additive Manufacturing | ||

| Others | ||

| By End-User Industry | Packaging | |

| Automotive | ||

| Construction and Woodworking | ||

| Healthcare | ||

| Electronics and Display | ||

| Others (Industrial Machinery) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the Asia Pacific photoinitiator market be by 2031?

Asia Pacific is projected to surpass USD 1.28 billion by 2031, reflecting its 11.02% CAGR and manufacturing concentration.

What is driving the rapid growth of the photoinitiator market?

The transition to energy-efficient LED curing, expanding 3D-printing applications, and stringent VOC regulations collectively propel demand across coatings, packaging, and electronics.

Why are LED-compatible photoinitiators important?

LED lamps emit narrow-band light, so initiators must absorb intensely at 365 nm-405 nm to ensure fast, full cures while meeting energy-saving goals.

What regulatory issues affect photoinitiator selection?

Restrictions on benzophenone and VOC emissions push formulators toward low-migration, non-toxic, and solvent-free UV-curable systems.

Page last updated on: