Frequency Synthesizer Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.98 Billion |

| Market Size (2030) | USD 2.99 Billion |

| Growth Rate (2025 - 2030) | 8.55% CAGR |

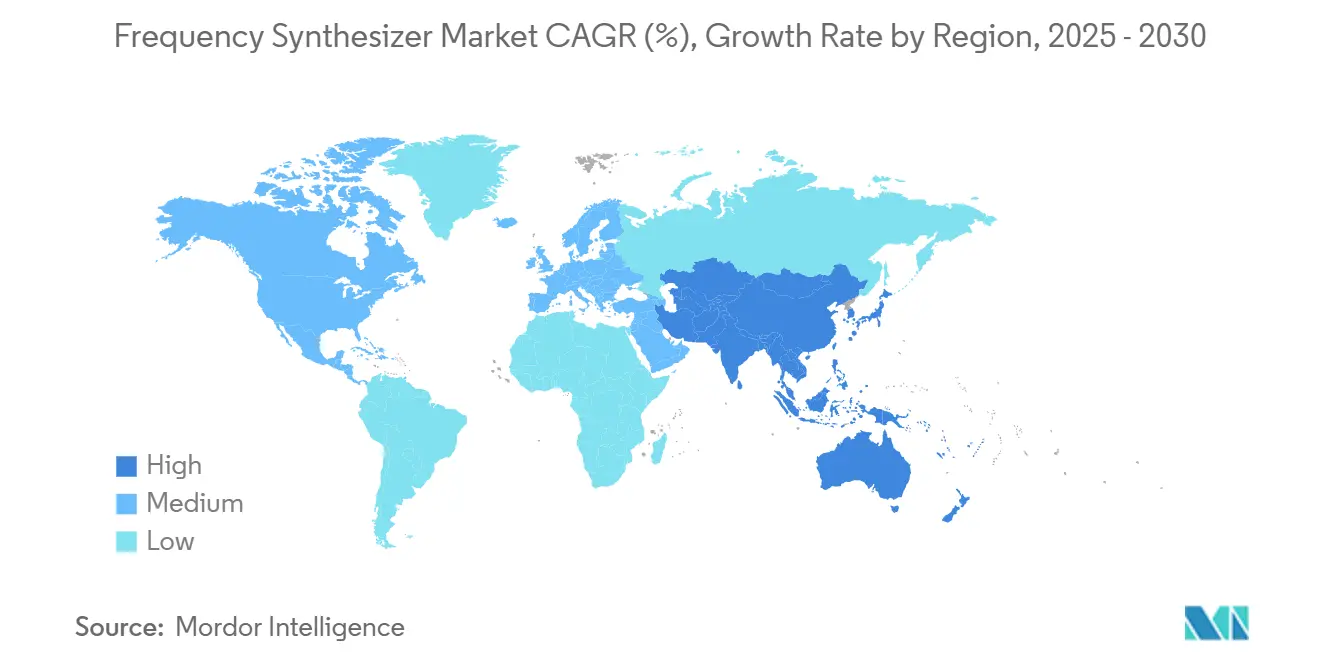

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

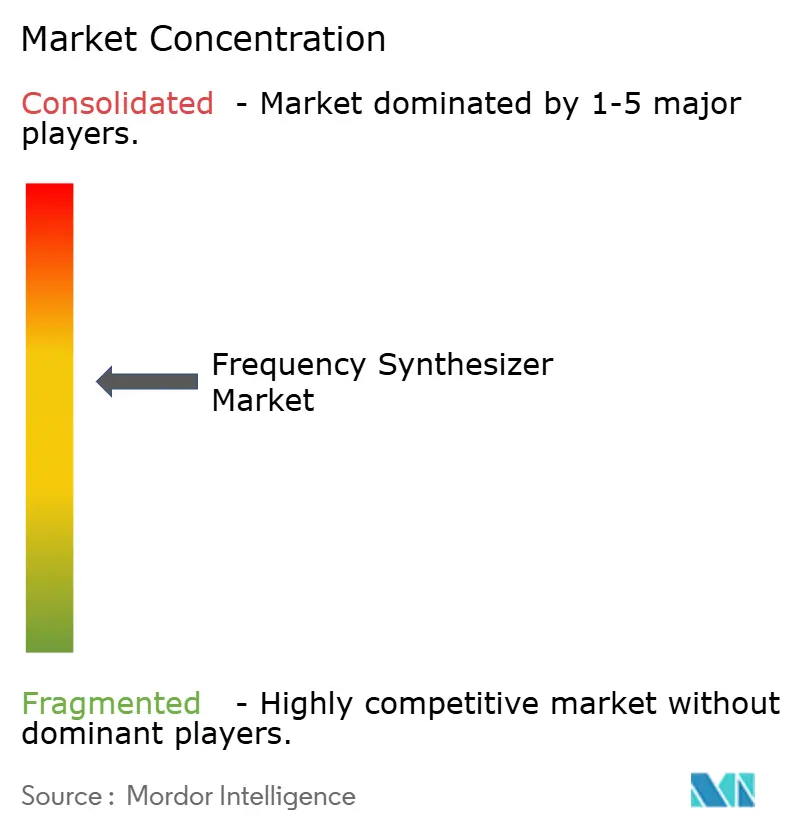

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Frequency Synthesizer Market Analysis by Mordor Intelligence

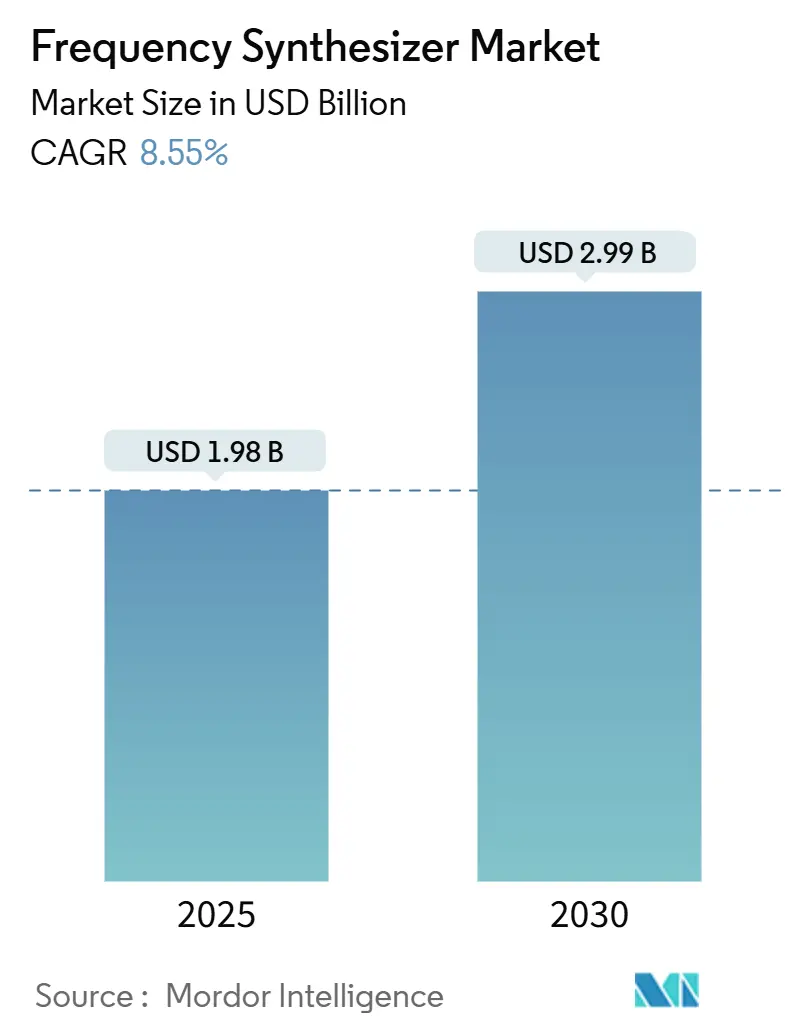

The frequency synthesizer market size stands at USD 1.98 billion in 2025 and is projected to reach USD 2.99 billion by 2030, translating to an 8.55% CAGR over the forecast period. Sustained investment in 5G infrastructure, accelerating launches of low-Earth-orbit (LEO) satellite constellations, and the automotive sector’s rapid shift toward 77–81 GHz radar systems collectively underpin this expansion of the frequency synthesizer market. Quantum-computing control stacks further widen demand for coherent microwave sources, while photonic frequency synthesis moves from lab to pilot lines for bands above 100 GHz. On the supply side, Asia-Pacific’s dense semiconductor ecosystem remains pivotal, yet raw-material bottlenecks in high-purity quartz and compound semiconductors inject risk into near-term output reliability. Competitive intensity is advancing as incumbents embed artificial-intelligence engines into timing cores and extend portfolios into single-chip PLL-VCO combinations that cut board area by 40–50%.

Key Report Takeaways

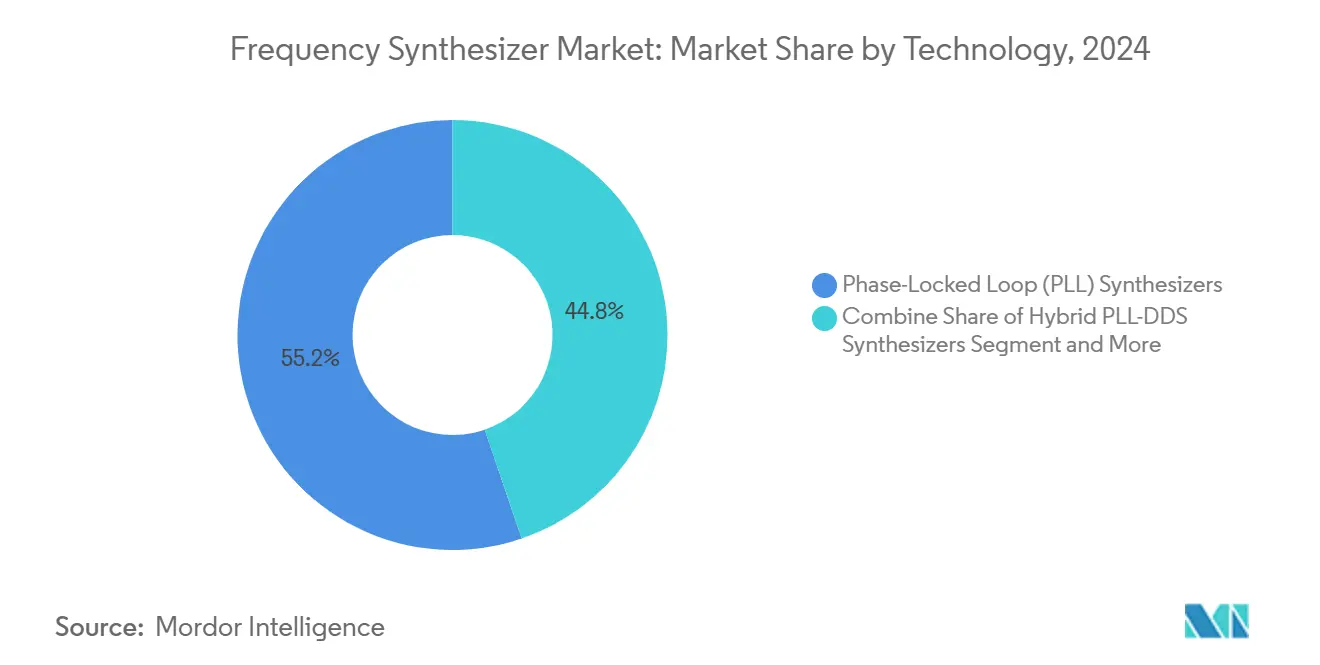

- By technology, phase-locked loop (PLL) synthesizers held 55.21% revenue share in 2024; hybrid PLL-DDS solutions are projected to expand at a 12.34% CAGR through 2030.

- By type, analog frequency synthesizers accounted for 65.32% of the 2024 revenue base; digital architectures are forecast to advance at a 10.26% CAGR to 2030.

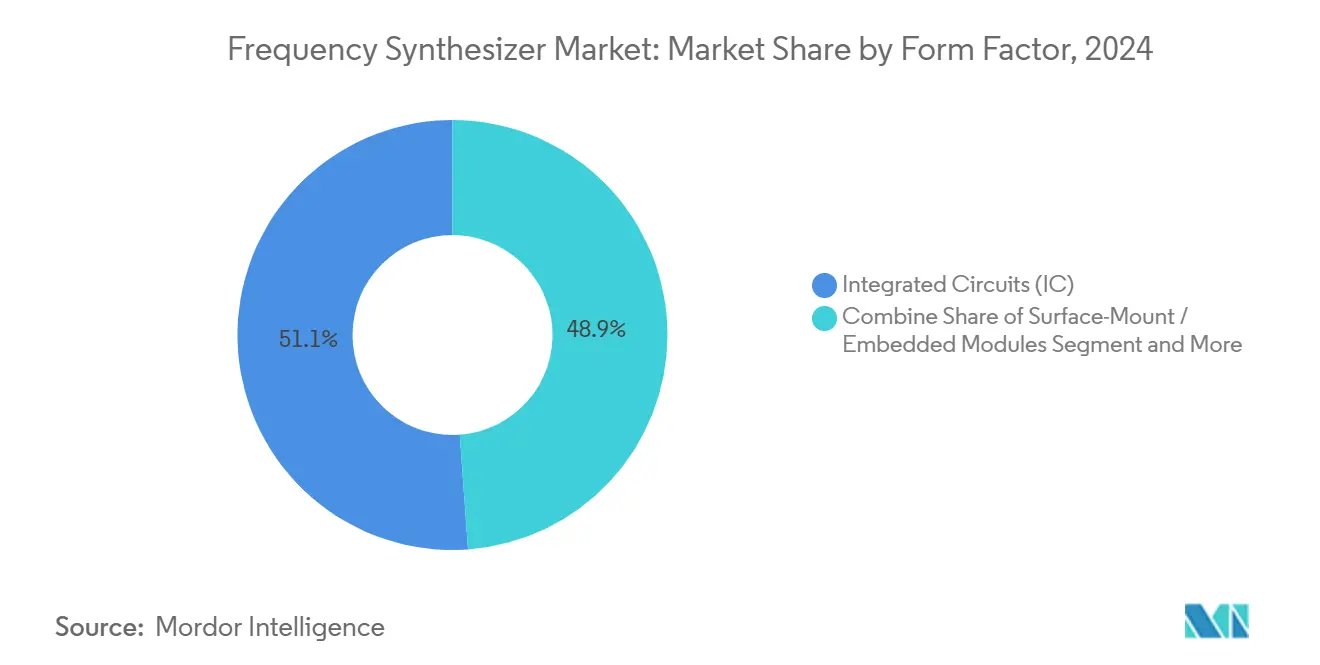

- By form factor, integrated-circuit devices led with 51.14% share in 2024; surface-mount embedded modules are set to grow at an 11.85% CAGR through 2030.

- By application, telecommunications infrastructure captured 38.65% of 2024 revenue; automotive radar is expected to post a 13.25% CAGR between 2025 and 2030.

- By geography, Asia-Pacific commanded 40.21% share in 2024, while the region is on track for a 12.86% CAGR to 2030.

Global Frequency Synthesizer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Widespread 5G deployment requiring agile synthesizers | +1.8% | Global, strongest in Asia-Pacific | Medium term (2-4 years) |

| Rapid expansion of LEO satellite constellations | +2.1% | Global, concentrated in North America and Europe | Long term (≥ 4 years) |

| Integration trend toward single-chip PLL + VCO SoCs | +1.2% | Asia-Pacific manufacturing hubs, global adoption | Short term (≤ 2 years) |

| Automotive 77–81 GHz radar adoption in ADAS | +0.9% | North America, Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Coherent microwave sources for quantum-computing control | +0.7% | North America, Europe, select Asia-Pacific centers | Long term (≥ 4 years) |

| Emergence of photonic frequency synthesis >100 GHz | +0.8% | Advanced research centers globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Widespread 5G Deployment Requiring Agile Synthesizers

Continuous 5G base-station rollouts call for synthesizers that switch channels in under one microsecond while holding phase noise 10–15 dB lower than 4G benchmarks. Massive-MIMO arrays depend on this coherence to support ultra-reliable low-latency links critical for industrial automation and extended-reality services. [1]Anritsu, “6G Technology,” Anritsu.com Vendors such as Renesas deliver 25-femtosecond jitter references, enabling spectrum-sharing schemes that improve throughput by 15–20% in live deployments across China and South Korea. Small-cell densification further amplifies volume demand, as each node integrates two to four independent synthesizers for carrier aggregation. The frequency synthesizer market, therefore, aligns closely with the base-station forecast curve, locking in multiyear visibility for component suppliers. Asia-Pacific operators, benefiting from government-subsidized rollouts, remain the early adopters of sub-7 GHz and millimeter-wave boards embedding monolithic PLL-VCO chips.

Rapid Expansion of LEO Satellite Constellations Demanding Ultra-Low-Jitter Sources

Mega-constellations exceeding 5,000 satellites necessitate synthesizers that maintain parts-per-billion accuracy while withstanding radiation, vibration, and −40 °C to +85 °C swings. [2]Microchip Technology, “Precision Time and Frequency for C5ISR,” Microchip.com Doppler-compensation loops require phase locks across hundreds of inter-satellite links, intensifying design margins for jitter and spurious suppression. Microchip’s space-qualified timing modules illustrate how redundant oven-controlled crystal references pair with radiation-tolerant PLL cores to preserve coherence during eclipses. As operators adopt optical cross-links, photonic synthesis promises improved stability, but cost and size constraints delay mass qualification. North American and European primes, supported by export-credit agencies, drive early procurement, keeping the frequency synthesizer market firmly in their industrial base.

Integration Trend Toward Single-Chip PLL + VCO Solutions in SoCs

Smartphones, IoT gateways, and small-form-factor radios demand footprint cuts without sacrificing spectral purity. Texas Instruments’ LMX2592 family epitomizes this shift, merging wideband PLLs and on-die VCOs to save up to 35 mm² of board area relative to discrete builds. Co-packaged filters and power-management blocks contain spurs, while 3D stacking shortens loop-filter traces for better phase noise. Asia-Pacific foundries benefit as fabless designers tape out at 12 nm CMOS nodes, exploiting lower leakage and tighter process control. In parallel, system-in-package (SiP) variants attach GaAs or GaN power amplifiers atop digital PLLs, offering a turnkey route for private-network gear. This integration wave secures near-term momentum for the frequency synthesizer market as software-defined radio platforms proliferate across verticals.

Automotive 77–81 GHz Radar Adoption in ADAS

Demand for centimeter-level range resolution pushes chirp bandwidths beyond 4 GHz, compelling synthesizers to deliver linear frequency sweeps with minimal phase error. NXP’s RFCMOS radar SoC integrates the synthesizer, transmit chains, and receivers to shrink module size for bumper or windshield mounting. Tier-1 suppliers report double-digit attach-rate growth for 4D imaging radar in premium vehicle trims. Upcoming 140 GHz concepts promise two-millimeter resolution, though they raise fresh thermal and packaging challenges. Europe’s focus on Euro-NCAP safety ratings accelerates OEM adoption timelines, while U.S. regulators move toward mandatory blind-spot detection, cementing radar units as pervasive content. The frequency synthesizer market consequently benefits from consistent volume pull through 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain volatility for RF/PLL ASICs | -0.8% | Global, acute in Asia-Pacific manufacturing corridors | Short term (≤ 2 years) |

| Phase-noise performance ceilings of mainstream CMOS nodes | -0.6% | Global semiconductor hubs | Medium term (2-4 years) |

| Thermal-management limits in wideband > 20 GHz ICs | -0.5% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Export-control hurdles for defense and space-grade synthesizers | -0.4% | North America and allied defense markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Volatility for RF/PLL ASICs

Hurricane Helene’s 2024 disruption to Spruce Pine quartz mines highlighted a single-point failure that feeds 70–90% of global semiconductor-grade quartz, stalling wafer production for weeks and inflating lead times beyond 40 weeks for niche RF ASICs. In 2024 alone, 474,000 electronic components reached end-of-life status, obliging redesign cycles and forcing buffer-stock strategies that inflate working capital for synthesizer vendors. [3]Manufacturing.net, “Semiconductor Trends: Risks, Tech & Global Shifts,” Manufacturing.net Gallium sourcing remains fragile—China controls 98% of global output and has enacted tiered export licenses. These shocks collectively compress gross margins and delay customer qualifications. Diversification into multiple foundry partners and wafer-banking mitigates risk but raises operating costs, trimming near-term growth for the frequency synthesizer market.

Phase-Noise Performance Ceilings of Mainstream CMOS Nodes

At 7-nm and smaller geometries, reduced supply voltages and tighter device spacing elevate flicker-noise injection into VCO cores, capping phase-noise improvements reachable on bulk-CMOS flows. While silicon-on-insulator and SiGe BiCMOS alleviate substrate coupling, wafer costs climb 2–3× over baseline nodes, limiting use to aerospace or instrumentation. Compound-semiconductor alternatives such as GaAs and InP outperform CMOS but face low yield and high per-wafer expense. Circuit-level noise-shaping and digital pre-distortion techniques claw back several dB, yet they consume additional die area and power. Thus, performance ceilings restrain penetration of fully digital architectures, tempering the outlook for high-volume segments within the frequency synthesizer market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: PLL Architectures Dominate Despite Hybrid Innovation

Phase-locked loop devices captured 55.21% of 2024 revenue, illustrating their continued primacy in infrastructure and test systems where stringent phase noise and stability specifications prevail. The frequency synthesizer market size for PLL-based products is poised for steady mid-single-digit growth as 5G densifies and 6G prototype work ramps. Fractional-N and integer-N variants address granularity versus noise trade-offs across base stations, microwave radios, and industrial instrumentation.

Hybrid PLL-DDS devices, however, are projected to grow at a 12.34% CAGR, reflecting combined agility and spectral purity that appeals to quantum-computing control stacks and agile test gear. Vendors tackle hand-off artifacts between DDS and PLL sections through phase continuity algorithms, achieving spur suppression required for coherent qubit gates. As unit costs fall with advanced nodes, hybrid adoption should broaden into LEO payloads and field-programmable radio platforms, gradually raising their share of the frequency synthesizer market.

By Type: Digital Solutions Accelerate Despite Analog Dominance

Analog architectures commanded 65.32% revenue share during 2024, underscoring their entrenched status in aerospace and defense deployments where analog phase-detector topologies deliver best-in-class noise floors. That positions analog products as the baseline of the frequency synthesizer market size, even as their growth moderates.

Digital solutions, limited to 10.26% CAGR ceiling, leverage firmware upgrades that enable frequency hopping, spread-spectrum profiles, and remote diagnostics across software-defined networks. Adoption quickens in private-LTE and open-RAN builds as operators favor cloud-configurable radios. The frequency synthesizer market share for digital implementations is thus expected to widen incrementally, with mixed-signal hybrids bridging legacy and next-gen design approaches.

By Form Factor: Integration Drives Miniaturization Trends

Integrated-circuit variants held 51.14% share in 2024, fueled by volume smartphone, IoT, and small-cell designs that prioritize low cost and tiny footprints. The frequency synthesizer market size within IC form factors benefits from Asia-Pacific’s 300-mm fab dominance that supports sub-14 nm nodes at scale.

Surface-mount embedded modules, expanding at 11.85% CAGR, integrate loop filters, power conditioning, and shielding to simplify procurement for lower-volume industrial or aerospace projects. Qorvo’s multichip modules demonstrate area cuts of 40–50% versus discrete IC-plus-passive builds, capturing design wins in phased-array radar and satcom user terminals. PXI cards and benchtop racks persist in laboratory settings, though their relative slice of the frequency synthesizer market declines as field-programmable platforms gain favor.

By Application: Automotive Radar Emerges as Growth Engine

Telecommunications infrastructure remained the chief revenue contributor at 38.65% in 2024, reflecting continuous macro-cell upgrades and early 6G feasibility studies. The frequency synthesizer market share for telecom is expected to plateau mid-term as initial 5G coverage stabilizes.

Automotive radar leads growth at 13.25% CAGR, fueled by tightening global safety mandates and OEM roadmaps for Level-3 autonomy. The frequency synthesizer market size tied to vehicle radar therefore rises sharply, aided by RFCMOS SoCs that consolidate RF, baseband, and power management on 28-nm nodes. Aerospace, defense, and test-and-measurement maintain high ASPs but moderate unit volumes, while IoT and consumer gadgets drive high-volume low-margin opportunities.

Geography Analysis

Asia-Pacific retained 40.21% of 2024 revenue and is projected to sustain a 12.86% CAGR through 2030, anchored by China’s aggressive 5G rollout, Japan’s satellite-communications investment, and Taiwan’s 66% share of advanced foundry capacity. The frequency synthesizer market size in the region scales with domestic handset and infrastructure supply chains, while export-control frictions motivate localized R&D in defense-oriented timing chips.

North America ranks second, driven by defense-grade demand, quantum-computing test beds, and Tier-1 suppliers such as Analog Devices and Texas Instruments. Government initiatives, including the U.S. SHIP program, channel funds into advanced RF microelectronics, safeguarding domestic strategic reserves and accelerating technology readiness for photonic synthesis.

Europe follows, leveraging Germany’s leadership in ADAS radar and France’s satcom endeavors. Semiconductor-sovereignty initiatives funnel grants toward local fabs, though ramping state-of-the-art capacity requires multi-year horizons. Bilateral export-license processes hamper rapid market entry for U.S. parts, creating white space for European or Asian alternatives. Overall, region-specific regulatory regimes and industrial strategies shape the frequency synthesizer market trajectory through 2030.

Competitive Landscape

The market exhibits moderate concentration: the top five players account for an estimated 48% of global revenue. Analog Devices and Texas Instruments wield cost advantages derived from internal wafer fabs and extensive analog IP libraries. Keysight Technologies and Anritsu dominate the premium test-equipment niche, while Qorvo and Skyworks Solutions capitalize on compound-semiconductor prowess for millimeter-wave modules.

Strategic playbooks include vertical integration, such as Qorvo’s purchase of Anokiwave, melding beam-forming ASICs with synthesizer front ends aimed at 5G base-stations and phased-array radars . AI-assisted calibration engines embedded in newer PLLs enable self-test and in-field phase-noise tuning, differentiating high-performance lines. Vendors also explore photonic frequency-comb architectures for sub-THz test gear, signaling an R&D race that could realign share positions post-2028.

Supply-chain resiliency measures—dual-sourcing wafers, localized packaging, strategic stockpiles—have become competitive imperatives following pandemic-era shortages. Licensing barriers in defense segments mean North American suppliers enjoy protected margins, but European and Asian challengers leverage export-friendly footprints to court global commercial customers. Consequently, the frequency synthesizer market may see further consolidation as firms seek scale to fund next-gen photonic and AI-driven roadmaps.

Frequency Synthesizer Industry Leaders

Analog Devices, Inc.

Texas Instruments Incorporated

Keysight Technologies, Inc.

National Instruments Corporation

Renesas Electronics Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Qorvo announced fiscal 2025 Q4 revenue of USD 869.5 million and highlighted expanding RF content opportunities in synthesizer-rich segments.

- March 2025: Qorvo upgraded its QSPICE simulation suite, adding JFET and MOSFET models that enhance precision in frequency synthesizer circuit design.

- January 2025: Qorvo secured MediaTek’s Wi-Fi 7 FEM supply contract for the Dimensity 9400 platform, with volume shipments kicking off in Q4 2024.

- January 2025: Anritsu extended its MD8430A tester to cover NTN NB-IoT devices for geostationary satellites, addressing growing non-terrestrial demands on phase-coherent synthesizers.

Global Frequency Synthesizer Market Report Scope

| Phase-Locked Loop (PLL) Synthesizers |

| Direct Digital Synthesizers (DDS) |

| Hybrid PLL-DDS Synthesizers |

| Fractional-N Synthesizers |

| Integer-N Synthesizers |

| Analog Frequency Synthesizers |

| Digital Frequency Synthesizers |

| Hybrid Frequency Synthesizers |

| Integrated Circuits (IC) |

| Surface-Mount / Embedded Modules |

| Rack / Benchtop Instruments |

| Open-Architecture PXI / VXI Cards |

| Telecommunications Infrastructure |

| Aerospace and Defense Systems |

| Test and Measurement Equipment |

| Automotive Radar and ADAS |

| Consumer Electronics and IoT |

| Research and Academia |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Technology | Phase-Locked Loop (PLL) Synthesizers | ||

| Direct Digital Synthesizers (DDS) | |||

| Hybrid PLL-DDS Synthesizers | |||

| Fractional-N Synthesizers | |||

| Integer-N Synthesizers | |||

| By Type | Analog Frequency Synthesizers | ||

| Digital Frequency Synthesizers | |||

| Hybrid Frequency Synthesizers | |||

| By Form Factor | Integrated Circuits (IC) | ||

| Surface-Mount / Embedded Modules | |||

| Rack / Benchtop Instruments | |||

| Open-Architecture PXI / VXI Cards | |||

| By Application | Telecommunications Infrastructure | ||

| Aerospace and Defense Systems | |||

| Test and Measurement Equipment | |||

| Automotive Radar and ADAS | |||

| Consumer Electronics and IoT | |||

| Research and Academia | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Netherlands | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the expected revenue of the frequency synthesizer market in 2030?

The frequency synthesizer market is forecast to reach USD 2.99 billion by 2030, representing an 8.55% CAGR from 2025.

Which application will grow fastest through 2030?

Automotive radar systems, particularly 77–81 GHz ADAS units, are projected to grow at a 13.25% CAGR, the highest among all applications.

Why is Asia-Pacific the largest regional buyer?

Asia-Pacific commands 40.21% revenue share because of its dominant semiconductor manufacturing base and aggressive 5G network rollouts in China, South Korea, and Japan.

How will hybrid PLL-DDS technology impact future designs?

Hybrid PLL-DDS synthesizers combine agility and spectral purity, enabling quantum-computing control and agile test equipment, and are set to expand at a 12.34% CAGR.

What supply-chain risks threaten synthesizer production?

Dependence on limited sources of high-purity quartz and gallium can disrupt wafer supply, while component end-of-life cycles force costly redesigns and inventory buffers.

Which companies currently lead the market?

Analog Devices, Texas Instruments, Keysight Technologies, Qorvo, and Skyworks Solutions collectively hold about 48% of global revenue, giving the market a moderate concentration score.

Page last updated on: