United States Frequency Control And Timing Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

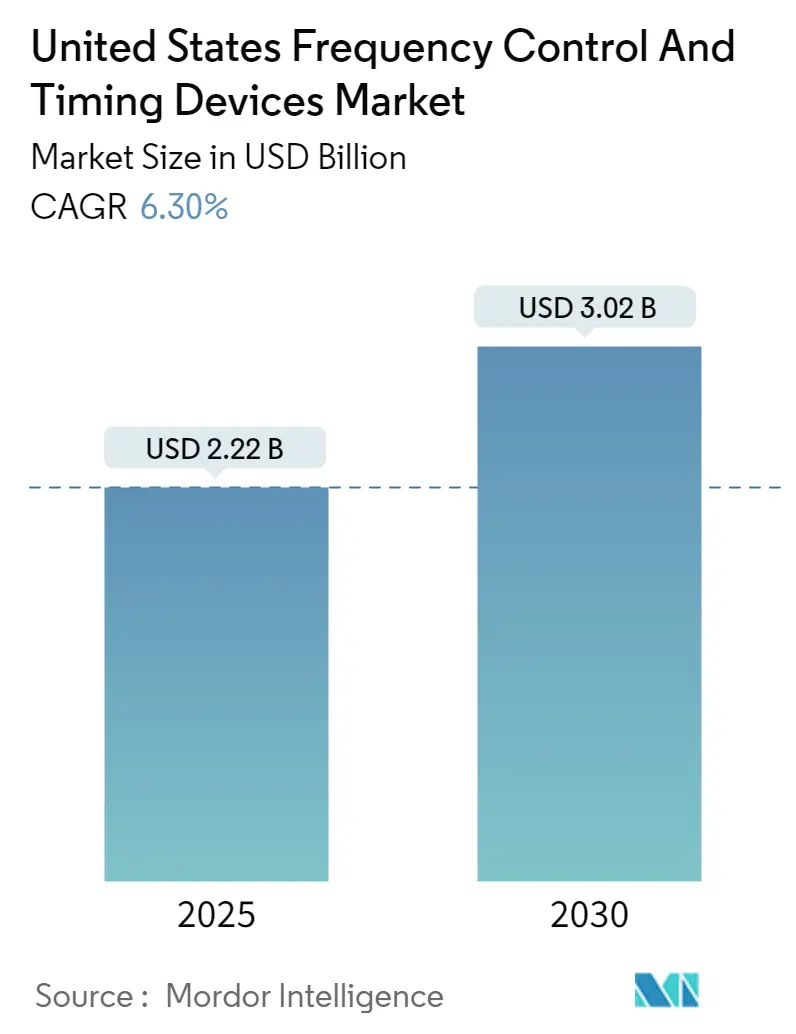

| Market Size (2025) | USD 2.22 Billion |

| Market Size (2030) | USD 3.02 Billion |

| Growth Rate (2025 - 2030) | 6.30% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Frequency Control And Timing Devices Market Analysis by Mordor Intelligence

The United States Frequency Control And Timing Devices Market size is estimated at USD 2.22 billion in 2025, and is expected to reach USD 3.02 billion by 2030, at a CAGR of 6.3% during the forecast period (2025-2030).

The digital transformation landscape in the United States continues to evolve rapidly, with frequency control and timing devices playing an increasingly critical role in modern electronics. According to DataReportal's early 2024 findings, the United States boasts 331.1 million internet users with a remarkable 97.1% penetration rate, while mobile connections have reached 396.0 million, representing 116.2% of the total population. This digital infrastructure expansion has created unprecedented demands for precise timing solutions and synchronization devices across various electronic systems, from consumer devices to industrial applications. The integration of artificial intelligence features in devices has become a key focus for chip manufacturers, who are actively developing new capabilities to drive upgrades across various platforms, including PCs and smartphones.

The data center landscape is experiencing significant expansion, reflecting the growing demand for robust timing solutions in cloud computing and data storage applications. As of March 2024, Cloudscene reported 5,381 data centers operating across the United States, the highest count globally. This expansion is evidenced by major investments from industry leaders, with Google announcing an additional USD 2.3 billion investment in its Ohio data centers in June 2023, while Meta initiated an USD 800 million data center campus project in Jeffersonville, Indiana. These developments underscore the critical importance of precise frequency control in maintaining data center operations and ensuring seamless communication between facilities.

The gaming and entertainment sector has emerged as a significant driver for timing device applications, with the 2023 Essential Facts report revealing that 65% of Americans, approximately 212.6 million people, engage in video gaming weekly. This high level of engagement has spurred innovations in timing technologies to support enhanced gaming experiences and virtual reality applications. Industry leaders are particularly focused on augmented reality and virtual reality headsets as key growth drivers, with companies like Meta Platforms and Xreal showcasing diverse extended reality devices at CES 2024.

The consumer technology sector continues to demonstrate robust growth potential, with the Consumer Technology Association (CTA) projecting retail sales to reach USD 512 billion in 2024, marking a 2.8% increase from the previous year. This growth is particularly significant in the context of timing devices, as modern consumer electronics increasingly require precise frequency reference for optimal performance. In April 2024, SiTime unveiled the innovative Chorus clock-system-on-a-chip, specifically designed for AI data centers, demonstrating the industry's response to evolving technological demands. This development represents a significant advancement in electronic timing systems, offering ten times better performance in half the size of traditional quartz-based devices, while addressing the growing needs of AI infrastructure and high-performance computing applications.

United states contributes to a system defined not by any single country or region but by the interaction of many. The global frequency control and timing devices market data by Mordor Intelligence represents that combined structure.

United States Frequency Control And Timing Devices Market Trends and Insights

Growing Adoption of 5G Augmenting the Demand for Frequency Control and Timing Devices

The rapid expansion of 5G infrastructure across the United States is creating unprecedented demand for frequency control and timing devices, which are crucial for maintaining network synchronization and reliability. The technology's projected penetration rate of 95% by 2030 underscores the massive scale of infrastructure development required, necessitating precise timing solutions across the network. This expansion is supported by significant government initiatives, such as the Public Wireless Supply Chain Innovation Fund's USD 1.5 billion investment announced in April 2023, focusing on fostering open and interoperable networks. The National Science Foundation's allocation of USD 25 million in September 2023 for the NSF Convergence Accelerator Track G further demonstrates the commitment to advancing 5G infrastructure and operations.

The economic impact of 5G deployment spans multiple sectors, driving demand for timing devices across various applications. By 2025, 5G is projected to contribute significantly to different industries, with communications leading at USD 251 billion, followed by business and professional services at USD 187 billion, and manufacturing at USD 159 billion. The healthcare sector is also expected to benefit substantially, with a projected contribution of USD 120 billion. This widespread adoption is facilitated by carriers offering various 5G smartphone models at different price points, often with promotional bundles, making the technology more accessible to consumers. The extensive 5G coverage across North America ensures high service availability, further driving the need for precise frequency control and timing devices in network infrastructure.

Rising Demand for Advanced Automotive Applications

The automotive industry's transformation through electrification and autonomous driving capabilities is creating substantial demand for frequency control and timing devices. Electric vehicle adoption has shown remarkable growth, with new registrations reaching 1.4 million in 2023, marking a 40% increase from the previous year. This surge in EV adoption is driving the need for sophisticated timing solutions in various applications, from power management systems to charging infrastructure. The industry's focus on reducing battery costs, improving charging infrastructure, and extending driving range requires increasingly precise timing and synchronization components, making frequency control devices essential for optimal performance.

The advancement in autonomous driving technologies and safety systems is further accelerating the demand for precise timing solutions. The National Highway Traffic Safety Administration's recent mandate requiring Automatic Emergency Braking (AEB) on all new vehicles under 10,000 lbs by 2029 exemplifies the growing emphasis on safety technologies that rely on precise timing. This regulation, expected to save up to 400 lives annually and prevent thousands of injuries, necessitates sophisticated timing devices for proper system function. Modern vehicles increasingly incorporate advanced features like collision-avoidance systems, automatic parking, and lane-change sensors, all requiring precise synchronization and timing control. These systems, combined with the broader trend toward autonomous driving capabilities, are creating sustained demand for high-performance frequency control and timing devices in the automotive sector. Additionally, the integration of frequency synthesizer technology is becoming crucial for ensuring the precision required in these advanced systems.

Segment Analysis: By Type

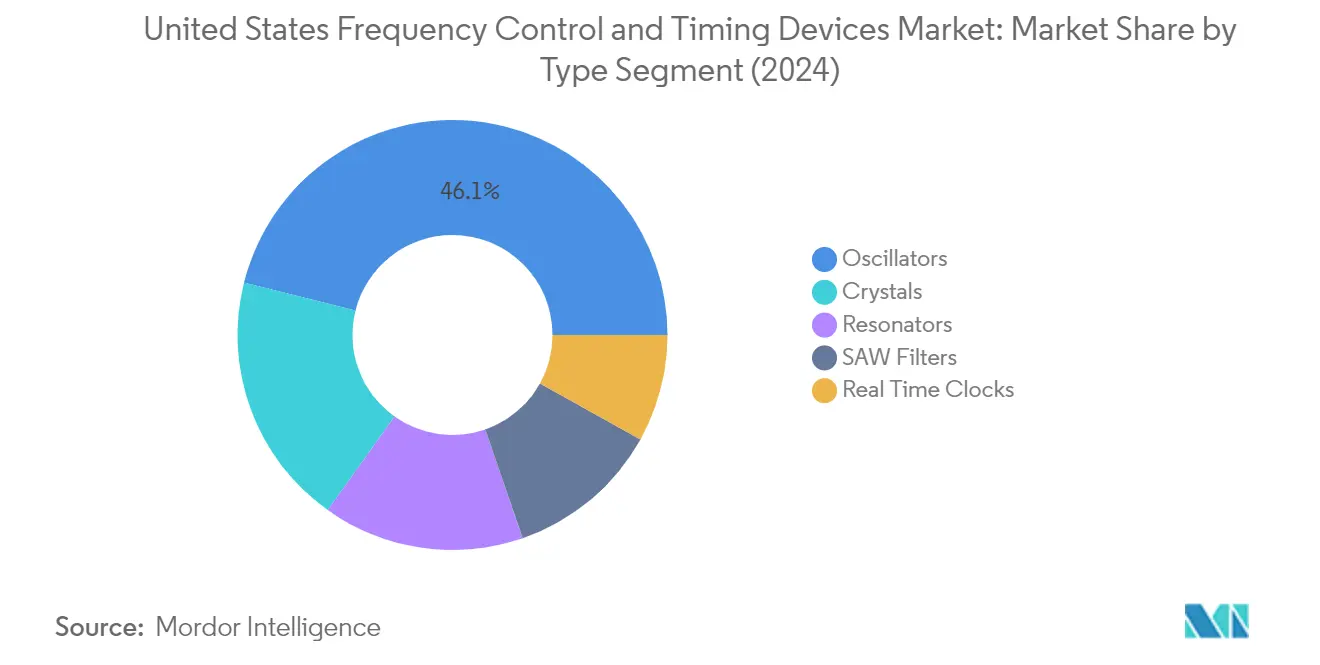

Oscillators Segment in United States Frequency Control and Timing Devices Market

The oscillators segment dominates the United States frequency control and timing devices market, commanding approximately 46% market share in 2024. This segment's prominence is primarily driven by the thriving demand from the consumer electronics industry and the growing deployment of oscillator components in 5G networks for their precise and stable frequency generation. The segment's growth is further bolstered by its crucial role in digitization efforts across various industries. Within the oscillator category, temperature-compensated crystal oscillators (TCXOs) have emerged as particularly significant components, maintaining high precision in electronic devices. The market has witnessed a rising demand for compact and low-power TCXOs with improved frequency stability, reflecting the broader trend of electronics miniaturization. This segment is expected to maintain its market leadership through 2029, growing at approximately 7% annually, driven by continuous technological advancements and increasing applications in emerging technologies.

Remaining Segments in United States Frequency Control and Timing Devices Market by Type

The market's remaining segments include crystals, resonators, SAW filters, and real-time clocks, each serving distinct roles in the frequency control ecosystem. Crystals, being fundamental piezoelectric devices, provide highly precise frequency outputs and are extensively used in various electronic applications. Resonators offer a balance between frequency precision and mechanical strain resistance, making them particularly valuable in industrial applications. SAW filters play a crucial role in signal processing and frequency selection, especially in wireless communication devices and mobile applications. Real-time clocks serve as essential components in devices requiring accurate timekeeping and calendar functionalities, particularly in IoT devices and embedded systems. These segments collectively contribute to the market's diversity and cater to specific requirements across different industries and applications.

Segment Analysis: By End User Industry

Consumer Electronics Segment in US Frequency Control and Timing Devices Market

The consumer electronics segment dominates the US frequency control and timing devices market, holding approximately 28% market share in 2024. This significant market position is driven by the increasing complexity and technological integration in modern consumer devices. The segment's growth is particularly fueled by the surge in 5G smartphone adoption, with carriers offering various 5G smartphone models across different price points. The Consumer Technology Association projects a 2.8% increase in US retail sales of consumer tech, reaching USD 512 billion in 2024, indicating strong market fundamentals. The integration of artificial intelligence features is expected to drive upgrades across various devices, including PCs and smartphones, while augmented reality and virtual reality headsets are emerging as significant growth drivers in the market.

Automotive Segment in US Frequency Control and Timing Devices Market

The automotive segment is projected to witness the highest growth rate of approximately 8% during the forecast period 2024-2029. This robust growth is primarily driven by the increasing adoption of electric vehicles and the integration of advanced driver-assistance systems (ADAS). The National Highway Traffic Safety Administration's mandate for Automatic Emergency Braking (AEB) on all new vehicles by 2029 is expected to significantly boost the demand for frequency control and timing devices. The surge in smarter, connected vehicles, coupled with the rising adoption of electric cars, is fueling demand for advanced precision oscillators, which are crucial for precise timing in automotive electronics, from power management and driver assistance systems to entertainment features.

Remaining Segments in End User Industry

The other significant segments in the market include communications/server/data storage, computer & peripherals, industrial, defense and aerospace, and IoT applications. The communications segment is particularly vital due to the ongoing 5G network expansion and increasing data center investments. The industrial segment is driven by Industry 4.0 initiatives and smart manufacturing adoption. The defense and aerospace sector's demand is fueled by satellite communications and advanced defense systems, while the IoT segment is growing due to increasing smart device adoption and connected technologies. The computer & peripherals segment continues to be significant due to the rising demand for high-performance computing solutions and gaming devices.

Competitive Landscape

Top Companies in United States Frequency Control and Timing Devices Market

The market features established players like Murata Manufacturing, Kyocera Corporation, Rakon Limited, Microchip Technology, TXC Corporation, Seiko Epson, Daishinku Corporation, Nihon Dempa Kogyo, SiTime Corporation, and Texas Instruments, among others. These companies are heavily investing in research and development to advance their timing device technology capabilities, particularly focusing on miniaturization and enhanced precision for 5G, automotive, and IoT applications. The industry is witnessing a strong trend toward developing products with improved phase noise performance, lower power consumption, and higher frequency stability. Companies are increasingly adopting vertical integration strategies to maintain better control over their supply chains and manufacturing processes. Strategic partnerships and collaborations, especially in emerging technologies like AI and cloud computing, have become crucial for maintaining a competitive advantage. Market leaders are also expanding their production capabilities and distribution networks while simultaneously focusing on developing environmentally sustainable products to meet growing customer demands.

Market Dominated by Global Technology Conglomerates

The competitive landscape is characterized by the strong presence of large multinational corporations with diverse product portfolios, alongside specialized frequency control device manufacturers. These companies typically maintain significant manufacturing facilities across multiple regions, with many establishing strong footholds in the United States to serve the growing demand from sectors like telecommunications, automotive, and industrial automation. The market structure shows a moderate level of consolidation, with top players holding substantial market share through their established brand reputation and technological capabilities. Recent years have witnessed increased merger and acquisition activities, particularly focused on acquiring specialized technology firms to enhance product offerings and expand market reach.

The industry demonstrates a clear trend toward strategic consolidation, with larger players acquiring smaller, specialized manufacturers to strengthen their technological capabilities and market position. Companies are increasingly focusing on building comprehensive product portfolios that can serve multiple end-user segments, from consumer electronics to aerospace and defense. The competitive dynamics are further shaped by the presence of both traditional crystal manufacturers and newer entrants specializing in MEMS-based solutions, creating a diverse competitive environment that drives innovation and market development. Market participants are actively pursuing vertical integration strategies to ensure better control over critical components and reduce dependency on external suppliers.

Innovation and Adaptability Drive Market Success

Success in this market increasingly depends on companies' ability to develop innovative timing solutions that address the evolving needs of key end-user industries, particularly in emerging applications like 5G infrastructure, autonomous vehicles, and IoT devices. Market incumbents are strengthening their positions through continuous investment in research and development, focusing on developing products with enhanced performance characteristics and reliability. Companies are also expanding their presence in high-growth application segments while maintaining strong relationships with key customers in traditional markets. The ability to provide customized solutions, maintain competitive pricing, and ensure reliable supply chains has become crucial for maintaining market share.

For new entrants and smaller players, success largely depends on their ability to identify and serve niche market segments with specialized products or innovative technologies. Companies must navigate challenges such as high development costs, stringent quality requirements, and the need for extensive technical expertise. The market shows relatively low substitution risk due to the critical nature of electronic timing systems in electronic systems, but companies must still contend with pricing pressures and the need to continuously improve product performance. Regulatory compliance, particularly in sectors like automotive and aerospace, continues to play a crucial role in shaping competitive strategies, with successful companies maintaining robust quality management systems and necessary certifications.

United States Frequency Control And Timing Devices Industry Leaders

Murata Manufacturing Co. Ltd

Kyocera Corporation

Rakon Limited

Microchip Technology Inc.

TXC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024 - TXC Corporation has introduced its latest innovation in precision timing technology, the Xterniti Platform. This cutting-edge advancement is designed with meticulous engineering to meet the growing demands of telecommunications networks, ensuring unparalleled reliability and performance, especially in extending holdover capabilities. At the heart of the Xterniti Platform lies the proprietary Extended Holdover OCXO technology, setting new standards for uninterrupted precision timing.

- January 2024 - Seiko Epson Corporation created a new differential output type called Wide Amplitude LVDS (WA-LVDS) for crystal oscillators. WA-LVDS allows for the flexible selection of the appropriate output amplitude for the LSI. The company plans to release crystal oscillators featuring WA-LVDS by fiscal year 2025.

United States Frequency Control And Timing Devices Market Report Scope

The market is defined by the revenue accrued through the sale of various types of frequency control and timing devices, such as crystals, oscillators, resonators, saw filters, and real-time clocks, in the United States.

The United States frequency control and timing devices market is segmented by type (crystals, oscillators (temperature compensated crystal oscillator (TCXO), voltage-controlled crystal oscillator (VCXO), oven-controlled crystal oscillator (OCXO), MEMS oscillator, other types of oscillators), resonators, saw filters, real-time clocks), end-user industry (automotive, computer & peripherals, communications/server/data storage, consumer electronics, industrial, defense and aerospace, IoT, and other end-user industries). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Crystals | |

| Oscillator | Temperature Compensated Crystal Oscillator (TCXO) |

| Voltage-controlled Crystal Oscillator (VCXO) | |

| Oven-controlled Crystal Oscillator (OCXO) | |

| MEMS Oscillator | |

| Other Types of Oscillators | |

| Resonators | |

| Saw Filters | |

| Real Time Clocks |

| Automotive |

| Computer and Peripherals |

| Communications/Server/Data Storage |

| Consumer Electronics |

| Industrial |

| Defense and Aerospace |

| IoT (Wearables, Fitness Tracker, Smart Home Devices, Smart Cities, Smart Lighting System, and Others) |

| Other End-user Industries (Healthcare, Oil and Gas, Agriculture, Retail, Test and Measurement, and Others) |

| By Type | Crystals | |

| Oscillator | Temperature Compensated Crystal Oscillator (TCXO) | |

| Voltage-controlled Crystal Oscillator (VCXO) | ||

| Oven-controlled Crystal Oscillator (OCXO) | ||

| MEMS Oscillator | ||

| Other Types of Oscillators | ||

| Resonators | ||

| Saw Filters | ||

| Real Time Clocks | ||

| By End-user Industry | Automotive | |

| Computer and Peripherals | ||

| Communications/Server/Data Storage | ||

| Consumer Electronics | ||

| Industrial | ||

| Defense and Aerospace | ||

| IoT (Wearables, Fitness Tracker, Smart Home Devices, Smart Cities, Smart Lighting System, and Others) | ||

| Other End-user Industries (Healthcare, Oil and Gas, Agriculture, Retail, Test and Measurement, and Others) | ||

Key Questions Answered in the Report

How big is the United States Frequency Control And Timing Devices Market?

The United States Frequency Control And Timing Devices Market size is expected to reach USD 2.22 billion in 2025 and grow at a CAGR of 6.30% to reach USD 3.02 billion by 2030.

What is the current United States Frequency Control And Timing Devices Market size?

In 2025, the United States Frequency Control And Timing Devices Market size is expected to reach USD 2.22 billion.

Who are the key players in United States Frequency Control And Timing Devices Market?

Murata Manufacturing Co. Ltd, Kyocera Corporation, Rakon Limited, Microchip Technology Inc. and TXC Corporation are the major companies operating in the United States Frequency Control And Timing Devices Market.

What years does this United States Frequency Control And Timing Devices Market cover, and what was the market size in 2024?

In 2024, the United States Frequency Control And Timing Devices Market size was estimated at USD 2.08 billion. The report covers the United States Frequency Control And Timing Devices Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the United States Frequency Control And Timing Devices Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: