Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.22 Billion |

| Market Size (2031) | USD 3.92 Billion |

| Growth Rate (2026 - 2031) | 3.99% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

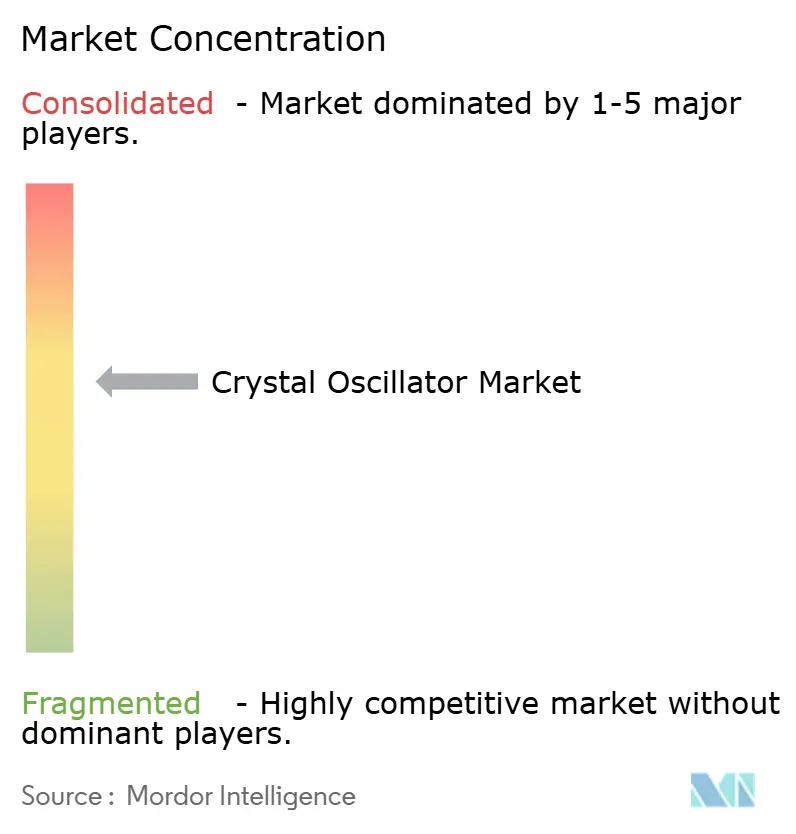

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Crystal Oscillator Market Analysis by Mordor Intelligence

The crystal oscillator market size in 2026 is estimated at USD 3.22 billion, growing from 2025 value of USD 3.10 billion with 2031 projections showing USD 3.92 billion, growing at 3.99% CAGR over 2026-2031. The technology’s entrenched role in 5G base stations, automotive radar, and precision industrial networks sustains demand even as component lifecycles shorten. Adoption accelerates wherever timing precision mitigates interference or data-integrity risks, such as 5G Time Division Duplex cells and GHz-level radar arrays. Migrations away from bulky rubidium standards toward compact Oven-Controlled Crystal Oscillators (OCXOs) in Low Earth Orbit satellites broaden the addressable base. Power-efficient designs for wearable and IoT nodes are expanding the reach of the crystal oscillator market into energy-harvesting environments where every microampere matters. Meanwhile, supply-chain fragility around synthetic quartz and tightening RoHS compliance remain persistent headwinds.

Key Report Takeaways

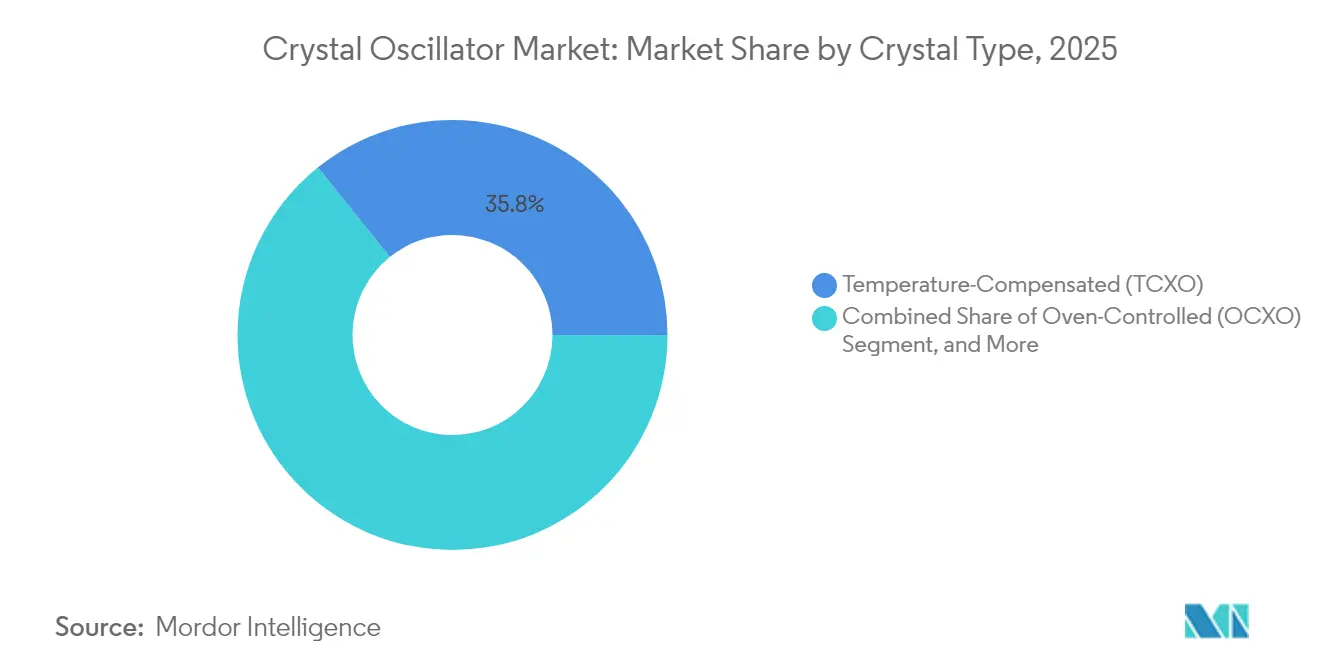

- By crystal type, Temperature-Compensated Crystal Oscillators led with 35.78% of the crystal oscillator market share in 2025, while OCXOs post the fastest 4.18% CAGR through 2031.

- By mounting scheme, surface-mount packages captured 68.05% of the crystal oscillator market in 2025; through-hole units cater to niche aerospace and industrial uses.

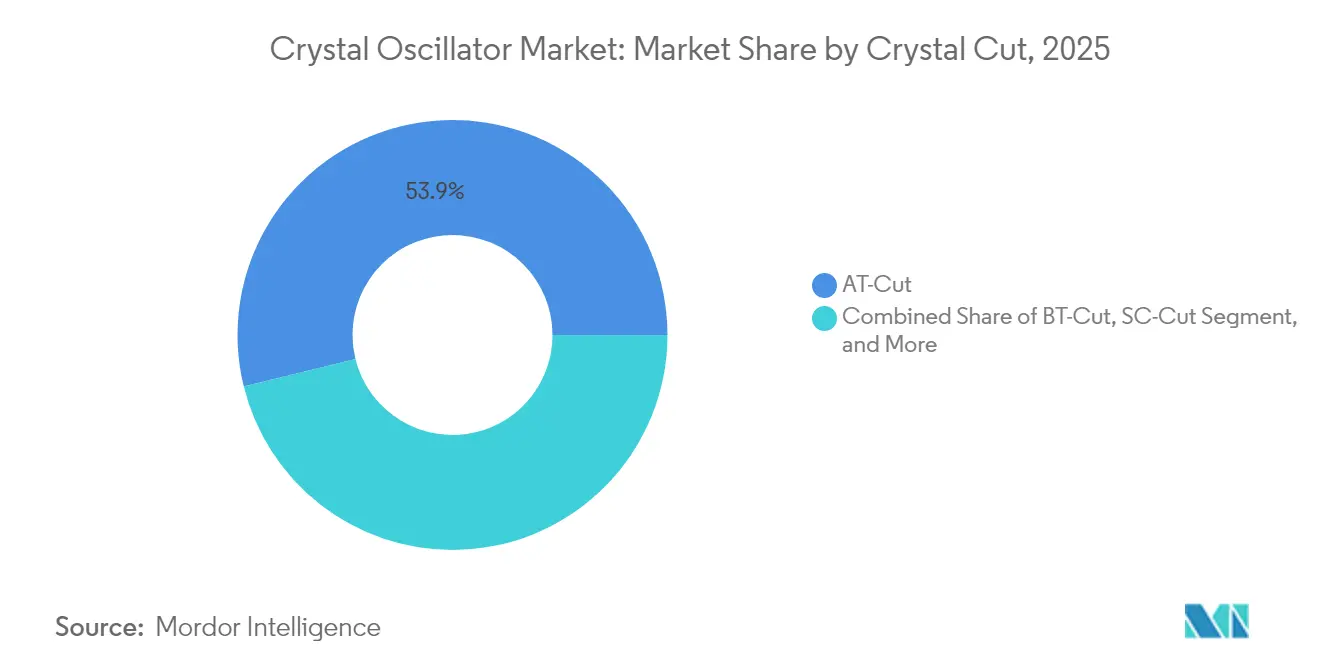

- By crystal cut, AT-Cut devices held 53.85% share of the crystal oscillator market in 2025; SC-Cut demand is rising in mission-critical holdover clocks.

- By end-user industry, telecommunications dominated revenue at 27.12% in 2025, whereas automotive timing solutions expand at a 5.01% CAGR to 2031.

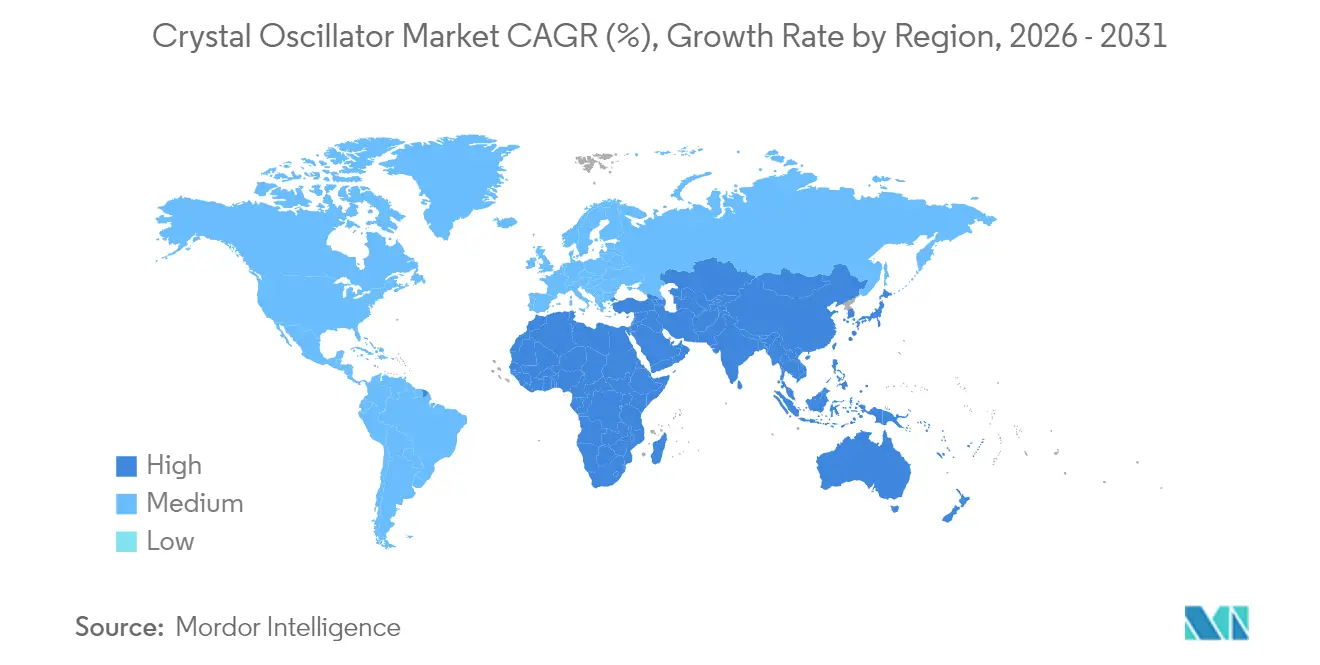

- By geography, Asia Pacific commanded 47.15% of 2025 revenue, while the Middle East and Africa crystal oscillator market size posts a 5.49% CAGR on semiconductor-hub investments.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Crystal Oscillator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in 5G RRH and Small-Cell Deployments Requiring Ultra-Stable TCXOs | +0.80% | Global, led by APAC & North America | Medium term (2-4 years) |

| Automotive Radar and ADAS Uptake Driving GHz-Level OCXO Demand | +0.60% | North America, Europe, APAC | Medium term (2-4 years) |

| Migration from Rubidium to High-Stability OCXOs in LEO Satellites | +0.40% | North America & Europe space programs | Long term (≥ 4 years) |

| Rapid Proliferation of Wearable/IoT Nodes Mandating Miniature SPXOs & MEMS-XO Hybrids | +0.50% | Global, APAC manufacturing | Short term (≤ 2 years) |

| Factory-Floor Digitalisation Elevating VCXO Use in TSN | +0.30% | Europe, North America, APAC | Medium term (2-4 years) |

| Military Shift to Software-Defined Radios Boosting SC-Cut OCXO Procurement | +0.20% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in 5G RRH and Small-Cell Deployments Requiring Ultra-Stable TCXOs

5G networks demand frequency and phase alignment within 1.5 µs to prevent uplink–downlink interference. Remote Radio Heads now embed ±50 ppb TCXOs and rely on Precision Time Protocol holdover when GNSS is spoofed, elevating timing from a cost line item to a quality-of-service safeguard. [1]Jim Olsen, “The Critical Role of Timing in 5G Networks,” MW RF, mwrf.com Network operators specify SC-cut crystal units from Epson that survive thermal shock, while small-cell vendors integrate board-level OCXO backups for indoor sites where GNSS is unavailable.

Automotive Radar and ADAS Uptake Driving GHz-Level OCXO Demand

The shift to 77–79 GHz radar enables centimeter-scale resolution but necessitates OCXOs with sub-100 fs jitter to avoid ghost targets. Vehicles hosting eight or more radar modules depend on coherent timing to fuse sensor data for Level-3 autonomy. Skyworks’ Si5332 clock generator delivers ISO26262 compliance and phased-array synchronization to meet this requirement. Entry barriers rise because devices must pass AEC-Q200 and function from -40 °C to 125 °C, limiting competition to firms with deep automotive pedigrees.

Migration from Rubidium to High-Stability OCXOs in Space-Constrained LEO Satellites

Mega-constellations prioritize SWaP, pushing operators to replace rubidium clocks with OCXOs such as Bliley’s Iris unit, which withstands 38 krad radiation while holding ±50 ppb over temperature in a 1-inch package. European Space Agency qualification lists now feature multiple quartz devices, validating performance once exclusive to atomic standards. OCXO makers refine SC-cut geometries and adaptive temperature-compensation codes to narrow the gap with rubidium for phase-link stability.

Rapid Proliferation of Wearable/IoT Nodes Mandating Miniature SPXOs and MEMS-XO Hybrids

Sub-10 µA system budgets in asset trackers and health bands force designers to adopt 1.2 mm² MEMS-quartz hybrids that boot in 3 ms and sustain ±3 ppm across -40 °C to 85 °C. [2]SiTime Press Team, “SiTime Continues to Advance Precision Timing with an Integrated Clock Chip for AI Datacenters,” SiTime, sitime.com Energy-harvesting sensor boards connect piezoelectric harvesters directly to timing rails, so any excess current draw truncates node life. Vibration immunity also improves, letting smartwatches endure 800 g shocks without frequency jumps.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| MEMS Clock-Generator ASP Erosion Cannibalising Low-End Quartz XOs | -0.70% | Global, APAC fabs | Short term (≤ 2 years) |

| Supply-Chain Fragility of Synthetic Quartz Wafers | -0.50% | Global, Japan-centric | Medium term (2-4 years) |

| High-Temperature Drift Limiting XO Adoption in SiC Powertrains | -0.20% | Automotive regions | Long term (≥ 4 years) |

| Stringent EU RoHS Lead-Free Solder Windows Raising Requalification Cost | -0.30% | Europe, spillover global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

MEMS Clock-Generator ASP Erosion Cannibalising Low-End Quartz XOs

SiTime’s Clock-SoC integrates PLLs, resonators, and spread-spectrum functions, shrinking board area by 50% and letting OEMs drop multiple SPXOs. Although quartz still delivers 0.18 ps jitter at half the current of MEMS, the flexible frequency menu and reduced SKU count entice cost-sensitive buyers. Average selling prices on commodity SPXOs face down-pressure as MEMS volume grows, prompting quartz suppliers to double down on premium OCXO and automotive lines.

Supply-Chain Fragility of Synthetic Quartz Wafers

Nearly all hydrothermal quartz ingots come from a handful of Japanese autoclave farms. When Hurricane Helene cut high-purity quartz shipments from Spruce Pine, the semiconductor ecosystem flashed warning lights because suitable alternatives require 12-month growth cycles. Switzerland-based QuartzCom added in-region capacity, yet geopolitical shocks or earthquakes could still squeeze oscillator lead times from eight to 20 weeks. Buyers now dual-source wafers and hold two quarters of safety stock, elevating working-capital costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Crystal Type: OCXO Growth Outpaces TCXO Dominance

The TCXO category held a 35.78% slice of the crystal oscillator market in 2025, supported by telecom equipment that values ±100 ppb stability within tight budgets. Continuous miniaturization now reaches 2.0 × 1.6 mm packages without sacrificing ±1 ppm performance. However, the OCXO subsegment leads growth at 4.18% CAGR to 2031, fueled by LEO satellites and 5G edge servers demanding sub-ppm holdover. These trends position OCXOs to capture a larger share of the crystal oscillator market size for precision infrastructure spending.

OCXOs leverage double-oven designs, composite crystal cuts, and digital temperature compensation to slash warm-up power by 56% in Epson’s OG7050CAN series. Simple Packaged Crystal Oscillators keep cost-driven consumer goods ticking, while VCXOs gain in Time-Sensitive Networking gateways that must retune frequency on demand. MEMS-based XOs command design wins where footprint trumps phase noise, despite higher BOM cost. FCXOs and SAW devices remain niche, serving test equipment and mm-wave links.

By Mounting Scheme: Surface-Mount Dominance Reflects Miniaturization Trends

Surface-mount packages owned 68.05% revenue in 2025 and expand alongside smartphone and IoT board densities. Automated placement trims assembly minutes and frees designers to stack components on both PCB sides, reinforcing the crystal oscillator market’s shift toward chip-level integration. The through-hole share persists only where vibration or thermal gradients threaten solder-joint integrity, such as rail-signaling modules or launch-vehicle avionics.

Legacy defense and space programs specify through-hole cans for field repairs and hermeticity. Rakon’s space-qualified HC45 package offers 10-year aging below ±0.1 ppm, meeting QML-V screening levels. Meanwhile, surface-mount roadmap devices test 1,000-cycle-per-hour reflow profiles to endure consumer production lines. The dichotomy ensures both schemes stay relevant, although volume tilts further toward pick-and-place friendly outlines across the wider crystal oscillator market.

By Crystal Cut: AT-Cut Leadership Faces SC-Cut Innovation

AT-Cut blanks generated 53.85% of 2025 sales given their forgiving slope across –40 °C to 85 °C, low motional resistance, and mature tooling. Manufacturers lock in yields above 92%, holding cost advantages as cloud-service operators require millions of timing nodes yearly. The segment anchors mainstream packets, routers, and smart meters that underpin recurring demand in the crystal oscillator market.

SC-Cut units now populate 10 ppb OCXOs for military radios and satellite payloads, trading higher unit cost for twice the thermal-shock immunity. BT-Cut and IT-Cut slices service mm-wave synthesizers above 50 MHz but stay niche. Epson’s redesigned SC-Cut resonators show aging drift of 0.05 ppm / year, aligning with rubidium holdover specs while keeping start-up within 2 W. Continuous R&D thus shifts premium value toward next-generation cuts that unlock new timing performance tiers.

By End-User Industry: Automotive Acceleration Challenges Telecom Leadership

Telecommunications captured 27.12% of 2025 revenue on the back of base-station densification and optical-transport upgrades demanding femtosecond-grade jitter. Carrier-class sync cards deploy redundant OCXOs for GNSS-denied holdover, cementing telecom’s baseline pull on the crystal oscillator market. Yet automotive clocks record the briskest 5.01% CAGR to 2031 as radar, LiDAR, and battery-management networks multiply oscillator sockets per vehicle.

Automakers adopt AEC-Q200 tested XOs rated for 125 °C and permanent 40 g vibration; Siward’s differential oscillator achieves 60 fs rms jitter to satisfy PCIe Gen4 ECU data pipes. Industrial automation rides Industry 4.0 conversions, using VCXOs in TSN bridges so robotic arms sync within microseconds. Aerospace and defense absorb high-margin hermetic OCXOs that survive launch shock, while medical devices push for nanowatt standby levels in implantables. Collectively, these cross-industry pulls sustain a balanced demand spectrum for the larger crystal oscillator market size across 2026-2031.

Geography Analysis

Asia Pacific held 47.15% of crystal oscillator market revenue in 2025, anchored by Japan’s synthetic quartz autoclaves and China’s PCB assembly scale. Japanese volumes dipped on weak Chinese handset output, with parts shipments down 25% year-on-year in 2024, yet regional capacity remained unrivaled for 8-inch wafer slicing. China’s push for indigenous 5G radios still drives bulk SPXO purchases, cushioning producers against handset softness. South Korea and Taiwan specialize in midstream wafer processing, enabling regional closed-loop supply that lowers logistics cost per oscillator.

North America commands premium share in MEMS-based and military-grade OCXOs. SiTime’s Silicon Valley fabless model co-opts TSMC MEMS lines, while Microchip’s New Hampshire crystal plant supports Vectron-labelled aerospace cans. Defense budgets and datacenter upgrades prioritize performance over price, thus supporting higher average selling prices within the regional crystal oscillator market.

Europe concentrates on supply-chain hedge strategies. QuartzCom’s Swiss wafers and Germany’s R&D clusters mitigate Japan concentration risk. EU RoHS deadlines accelerate lead-free requalifications, creating services revenue for local test houses. Middle East and Africa advance fastest at 5.49% CAGR, spearheaded by Saudi Arabia’s USD 266 million semiconductor hub forming 50 design houses by 2030. Smart-city rollouts in Riyadh and Dubai further expand regional demand for precise timing in IoT gateways and 5G small cells, broadening the crystal oscillator market footprint. South America remains modest, driven mainly by carrier upgrades in Brazil and Colombia, but logistic distances and limited upstream supply temper growth.

Regulatory Landscape

Crystal oscillators and related frequency-control devices are primarily shaped by electronics environmental compliance and component quality standards. In Europe, RoHS 3 (Directive 2015/863/EU) drives ongoing lead-free and restricted-substance compliance workflows, while REACH (Regulation 1907/2006/EU) increases chemical disclosure obligations for materials used in packages, adhesives, and processing chemicals. These requirements affect qualification cycles and documentation for global shipments of TCXO, OCXO, VCXO, and SPXO devices.

On the standardization side, IEC 60679-1:2017 provides a generic framework for piezoelectric, dielectric, and electrostatic oscillators, supporting quality assessment practices across multi-region supply chains. Trade policy and export controls also influence cross-border movement of frequency-control components, including restrictions affecting shipments to sanctioned jurisdictions (for example, Russia, Belarus, and Iran) under EU and allied regimes. In the United States, a January 2026 Federal Register action outlined a two-phase approach to semiconductor imports, including a 25% ad valorem tariff on a narrow category of semiconductors tied to AI and technology policy. That development increased the need for active tariff classification management for components moving under mounted piezoelectric crystal classifications, commonly grouped under HS 8541.60.00.

Value Chain Analysis

The crystal oscillator value chain starts with quartz inputs and crystal growth, then progresses through wafer slicing and blank processing, resonator fabrication, oscillator IC and analog front-end integration, and ends with packaging and test, including temperature characterization, aging, and screening for higher-reliability applications. Vertical integration is a key differentiator among leading suppliers such as Seiko Epson and Daishinku Corp. (KDS), which operate internal quartz growth capabilities and can manage blank availability, yields, and delivery schedules more tightly than firms that rely on third-party quartz procurement.

Midstream and downstream steps remain sensitive to material purity, process control, and qualification timelines, so logistics and supply continuity are strategic. Upstream concentration risk has been reinforced by disruptions to high-purity quartz supply from Spruce Pine, North Carolina, after Hurricane Helene in October 2024, which strengthened the rationale for dual-sourcing, higher safety stock, and longer buffer inventories for blanks and critical packages. On the commercial flow, standard surface-mount oscillator SKUs typically move through distribution with shorter lead times, while customized stability, low-jitter differential outputs, or higher-reliability screening often extend lead times, supporting preferred-supplier positioning, consignment stocking, and vendor-managed inventory programs with telecom, automotive, and data center OEMs.

Competitive Landscape

Top Companies in Crystal Oscillator Market

The market remains moderately fragmented. Seiko Epson, Kyocera, and NDK defend share through vertical integration that begins with proprietary seed-crystal growth and ends with packaged oscillators ready for robotics deployment. Combined, the top five brands control roughly 55-60% of global shipments, enough to command scale yet leave room for challengers. They lock in telecom OEMs via multiyear dual-sourcing contracts that guarantee sub-ppm aging and consignment stock.

Disruptors leverage MEMS. SiTime’s Chorus family integrates resonator and driver on silicon, delivering 10× phase-noise advantage in AI servers that heat to 105 °C rack inlet. The device occupies half the footprint of a dual-output SPXO, letting hyperscale builders cut PCB layers. Traditional crystal firms answer with micro-oven architectures and mixed-signal ASICs to reclaim performance crowns.

M&A remains active. Microchip’s earlier Vectron acquisition and potential future moves by Kyocera into European MEMS houses illustrate consolidation as firms chase adjacent know-how. Intellectual-property portfolios around SC-Cut simulation, oven-control algorithms, and radiation-shield layouts form the new battleground. Environmental mandates create differentiation as leaders roll out halogen-free epoxies and 100% renewable-powered fabs, appealing to ESG-minded OEMs and adding a soft moat around premium oscillator lines.

Crystal Oscillator Industry Leaders

Seiko Epson Corporation

Kyocera Corporation

Nihon Dempa Kogyo (NDK) Co. Ltd

Daishinku Corp.

TXC Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

AI servers, optical interconnects, and heterogeneous compute platforms are creating a whitespace for ultra-low-jitter differential crystal oscillators and higher-performance timing devices that can handle elevated board temperatures. Kyocera started mass production of its X Series differential clock crystal oscillators in January 2026, citing 30 fs-class phase jitter and aligning this move with tighter synchronization needs and higher-speed links in data center architectures. This pull also supports adjacent opportunities for high-frequency SPXOs and compact, higher-temperature TCXOs used to meet synchronization and holdover requirements in 5G radio and edge compute hardware.

Supply resilience and regional diversification are also shaping opportunity areas as buyers respond to upstream concentration in high-purity quartz and synthetic quartz capacity. The October 2024 Hurricane Helene disruption around Spruce Pine reinforced the business case for multi-region sourcing, inventory buffering, and closer supplier integration for critical blanks and packaging materials. At the same time, product roadmaps that reduce power and volume while preserving stability are expanding design-in options for edge infrastructure and space-constrained platforms, supporting demand for compact OCXO architectures and higher-stability quartz solutions as rubidium clocks are being constrained by SWaP trade-offs.

Recent Industry Developments

- June 2026: Seiko Epson introduced the OG7050CAN low-power OCXO, positioned for AI and edge infrastructure and described as 56% lower power and 85% smaller by cubic volume than earlier models. The update targets timing nodes where thermal density and power budgets constrain holdover and jitter performance, supporting continued OCXO penetration beyond traditional telecom sync cards.

- February 2026: Nihon Dempa Kogyo (NDK) announced sample availability for a 625 MHz differential crystal oscillator aimed at next-generation optical transceivers used in AI data centers. Bringing higher-frequency differential oscillators into the sampling pipeline supports migration to 800G and 1.6T-class links where phase noise and jitter directly affect signal integrity.

- October 2024: Hurricane Helene disrupted operations around Spruce Pine, North Carolina, a critical source of high-purity quartz used across semiconductor and frequency-control supply chains. The event highlighted upstream fragility for quartz-dependent components and reinforced procurement shifts toward dual-sourcing, increased safety stock, and tighter supplier qualification planning.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers packaged crystal oscillator devices that use a quartz element to generate a stable timing signal for electronic systems across major end uses worldwide.

Scope exclusions: We exclude pure MEMS oscillators without a quartz element and clock-generator ICs that do not contain a crystal resonator.

Segmentation Overview

- By Crystal Type

- Temperature-Compensated (TCXO)

- Oven-Controlled (OCXO)

- Voltage-Controlled (VCXO)

- Simple Packaged (SPXO)

- Frequency-Controlled (FCXO)

- MEMS-Based Crystal Oscillators

- Other Crystal Types

- By Mounting Scheme

- Surface-Mount

- Thru-Hole

- By Crystal Cut

- AT-Cut

- BT-Cut

- SC-Cut

- Others (IT-CUT, FC-Cut)

- By End-user Industry

- Consumer Electronics

- Telecom and Networking

- Automotive

- Aerospace and Defense

- Industrial Automation

- Medical and Healthcare

- Research and Measurement

- Other Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Nordics

- Rest of Europe

- South America

- Brazil

- Rest of South America

- Asia-Pacific

- China

- Japan

- India

- South-East Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Gulf Cooperation Council Countries

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research helped us build the base structure of the model and set realistic boundaries for what is being counted. We referenced public sources such as ITU connectivity indicators, World Semiconductor Trade Statistics trends, UN Comtrade trade codes for electronic components, and standards and guidance from IEC that clarify how frequency control parts are described and tested.

To ground demand signals, we also reviewed releases from telecom and spectrum regulators, and automotive safety and electronics publications from agencies like NHTSA. Patent databases were used to understand frequency control and timing design approaches that show up in qualification-heavy categories. Company filings, investor presentations, and reputable press were used to read shipment momentum and any pricing commentary for timing components. For cross-checking financial direction and deal signals, we used paid subscriptions for company financials and news, plus patent analytics, and then kept assumptions aligned to what could be explained from public materials. The sources listed here are illustrative and not exhaustive, and many additional references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were used to confirm what desk research cannot show cleanly, such as typical design-in cycles, how ASPs move by package grade, and how much demand comes from communications, automotive electronics, and industrial uses. We spoke with a mix of component suppliers, channel-side participants, and product engineers and sourcing managers, and coverage was balanced across major regions so regional production footprints and end-demand patterns could be checked before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 14% | APAC: 41% |

| Mid tier: 51% | Functional/Unit leaders: 35% | EMEA: 32% |

| Smaller Players: 14% | Managers: 51% | Americas: 27% |

Market-Sizing & Forecasting

Sizing started with a top-down rebuild of the demand pool, using electronics output trends and trade flows for related component categories to estimate how many oscillator units are likely consumed across regions and end uses. We then corroborated totals using selective bottom-up checks, such as sampled ASP-by-grade times estimated volumes, plus channel checks that show how pricing changes with supply tightness and qualification requirements.

A few inputs were treated as main market fingerprints, because they shift demand and value in a visible way. These included smartphone and connected device shipments, automotive electronics content growth (including ADAS-related timing needs), 5G radio and network build activity, industrial automation and IoT node growth, and the mix shift toward higher stability parts like temperature-compensated and oven-controlled devices in select applications. For forecasting, we used scenario analysis supported by expert views on electronics cycles and mix shifts, and then applied conservative assumptions where evidence was mixed. When bottom-up checks were thin for niche packages or specialty uses, the gaps were handled through proxy ratios and then re-tested with interview feedback until the totals remained consistent.

Data Validation & Update Cycle

Outputs were tested through multiple checks so that one single assumption did not drive the result. We compared the implied market value against independent signals such as electronics production direction, import and export movements, and the expected pricing ladder across common oscillator grades, then reviewed and corrected outliers before sign-off.

A second analyst review was carried out to re-check key formulas, conversion logic, and year-over-year movements. If a variable moved outside a reasonable band, we performed targeted re-contact. Reports are refreshed annually, and interim updates are made when material events occur that can shift supply or demand. Before delivery, a fresh review pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Global Crystal Oscillator Market Market Size Versus Other Published Estimates

Published market values for crystal oscillators can look far apart because each publisher draws the boundary differently and also applies its own price and mix assumptions. The gaps usually come from what is counted as an oscillator, which year is treated as the anchor, and how demand signals are validated across communications, automotive, and industrial uses.

Shipment-linked checks such as electronics output direction, trade-flow movements for component categories, and cross-verified ASP ladders by oscillator grade are the evidence that keeps Mordor Intelligence aligned to a quartz-based oscillator-only scope, instead of blending in adjacent clock and timing IC categories that inflate totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.22 B (2026) | |

| Industry Publisher A | USD 2.83 B (2024) | Uses a different anchor year and a longer-range forecast window, and the scope write-up is broader, which can shift what gets counted as oscillator revenue and how pricing is carried forward. |

| Research Portal B | USD 6.12 B (2024) | The number appears to reflect a wider timing-components pool, where adjacent devices and modules can be combined under a single label, and this can raise the total beyond quartz oscillator-only counting. |

Taken together, the spread mainly reflects scope edges and year anchors more than a true disagreement on demand direction. By tying value to observable demand signals and keeping inclusion rules clear, the resulting market size stays traceable to repeatable checks that can be revisited as the market shifts.

Key Questions Answered in the Report

What is the current crystal oscillator market size?

The crystal oscillator market size stands at USD 3.22 billion in 2026 and is projected to reach USD 3.92 billion by 2031 at a 3.99% CAGR.

Which crystal type leads revenue today?

Temperature-Compensated Crystal Oscillators hold 35.78% of 2025 sales, reflecting wide telecom deployment.

Why are OCXOs gaining share despite higher cost?

OCXOs provide sub-ppm holdover stability that small satellites, 5G edge servers, and GHz automotive radar demand, supporting a 4.18% CAGR through 2031.

Which region grows fastest?

The Middle East and Africa crystal oscillator market posts a 5.49% CAGR thanks to Saudi Arabia’s semiconductor-hub investments and smart-city rollouts.

How are MEMS oscillators affecting quartz demand?

MEMS clock generators integrate multiple functions, eroding ASPs in low-end quartz segments; however, quartz retains power and jitter advantages in mission-critical designs.

What are the main supply-chain risks?

Synthetic quartz production remains concentrated in Japan, so natural disasters or geopolitical events there could extend oscillator lead times from eight to 20 weeks.

Page last updated on: