Frequency Control And Timing Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

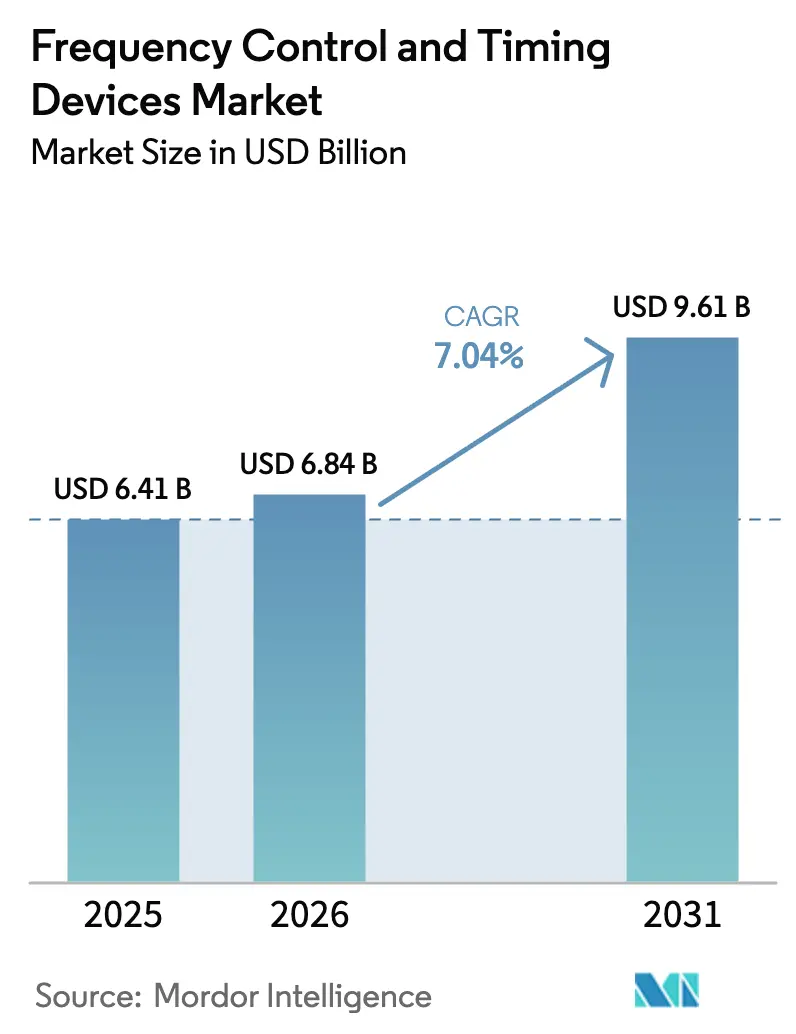

| Market Size (2026) | USD 6.84 Billion |

| Market Size (2031) | USD 9.61 Billion |

| Growth Rate (2026 - 2031) | 7.04% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Frequency Control And Timing Devices Market Analysis by Mordor Intelligence

The frequency control and timing devices market size is projected to be USD 6.41 billion in 2025, USD 6.84 billion in 2026 and reach USD 9.61 billion by 2031, growing at a CAGR of 7.04% from 2026 to 2031. Heightened demand for sub-picosecond jitter sources in 5G small-cell densification, stricter automotive electrification safety mandates and hyperscale data-center AI clusters are widening the addressable base of precision clocks. MEMS oscillators are accumulating design wins in ultra-low-power consumer wearables, while oven-controlled crystal oscillators remain vital to satellite ground stations that require <1 µs holdover during GNSS outages. Programmable timing solutions are also mitigating long quartz-blank lead times, allowing suppliers to spread inventory risk across hundreds of frequencies and voltage options. Export-control scrutiny on strategic timing intellectual property is beginning to split supply chains between Western and Chinese ecosystems, prompting multinationals to dual-source quartz and MEMS devices to hedge regulatory risk.

Key Report Takeaways

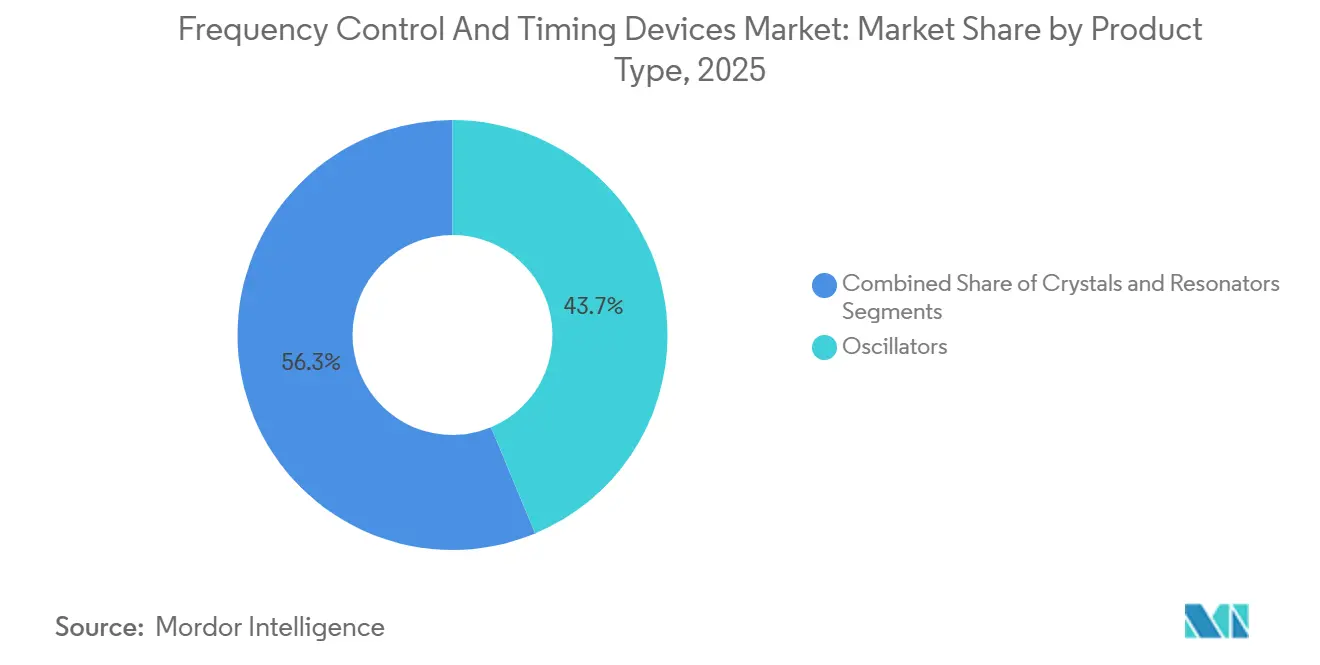

- By product type, crystals led with 43.72% of the frequency control and timing devices market share in 2025, Oscillators are projected to expand at a 7.07% CAGR through 2031.

- By technology, quartz accounted for 71.81% share of the frequency control and timing devices market size in 2025, whereas MEMS is advancing at a 7.11% CAGR over 2026-2031.

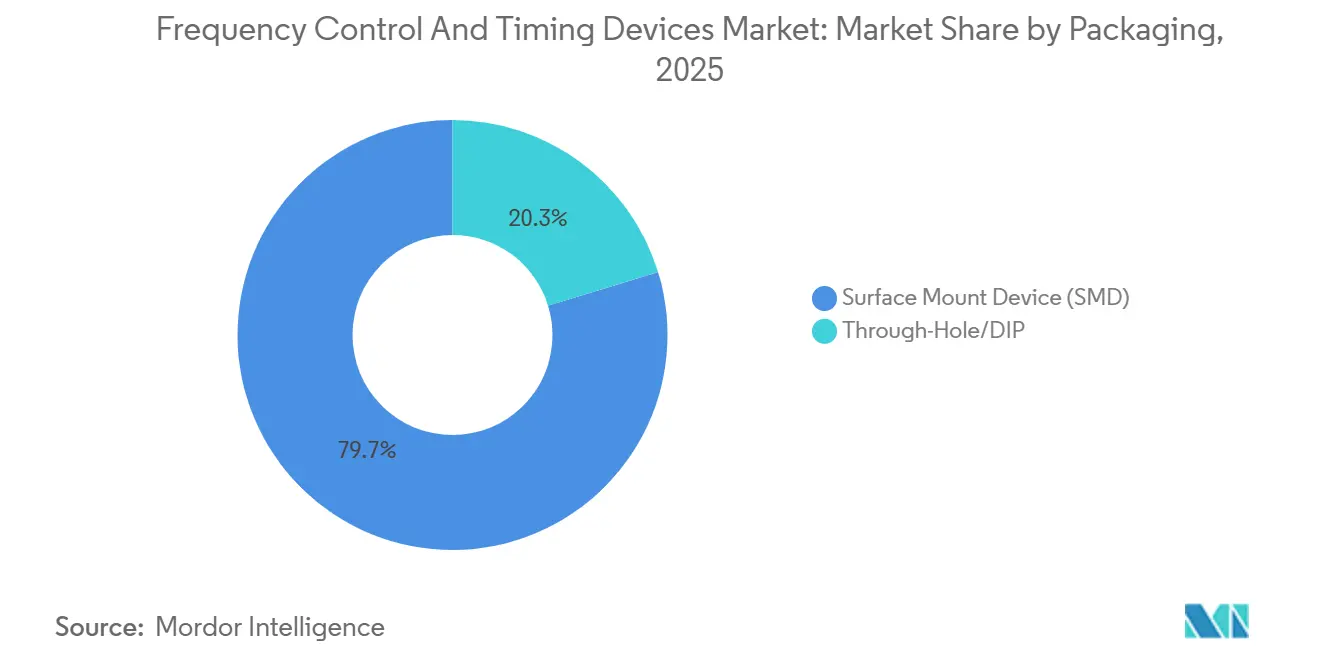

- By packaging, surface-mount devices held 79.74% of the frequency control and timing devices market share in 2025, while through-hole packages are forecast to grow at a 7.16% CAGR.

- By end-user, telecommunications and data centers captured 37.57% share of the frequency control and timing devices market size in 2025, and automotive is the fastest-growing segment at 7.20% CAGR to 2031.

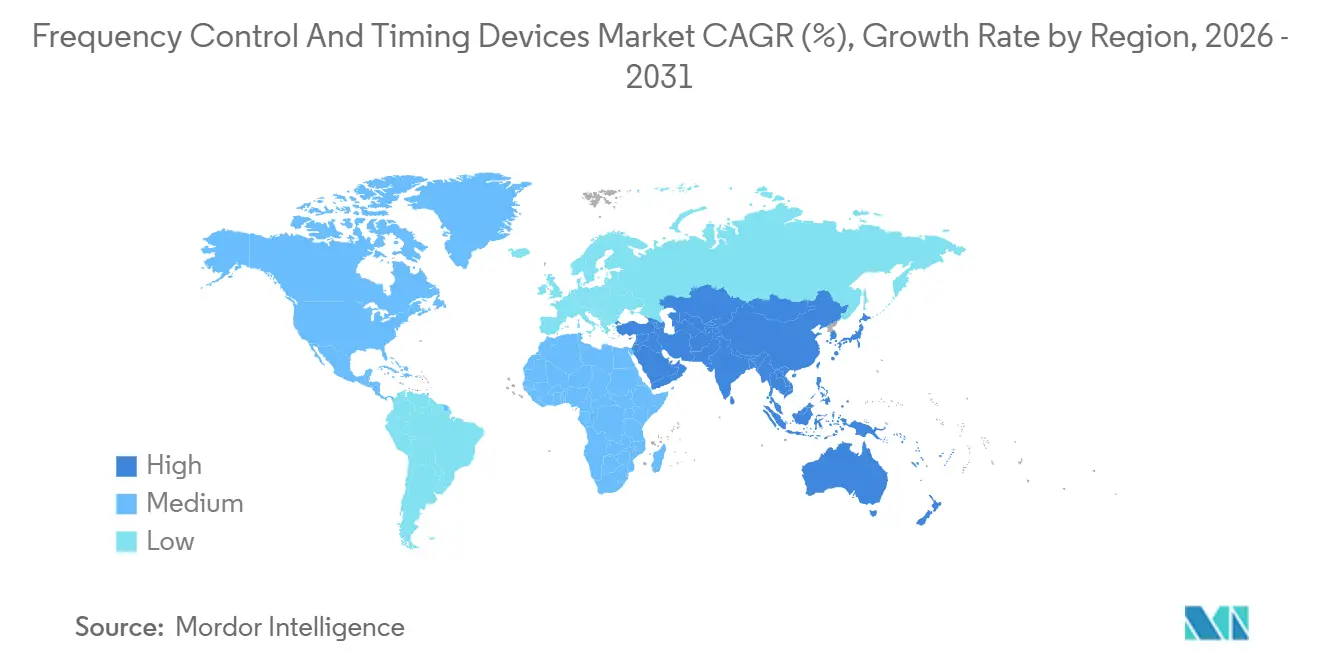

- By geography, Asia Pacific commanded 35.74% revenue share in 2025 and is expected to register the highest regional CAGR at 7.22% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Frequency Control And Timing Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G Infrastructure Build-Out Momentum | +1.2% | Global, APAC and North America lead | Medium term (2-4 years) |

| Electrification and ADAS Penetration | +1.1% | Europe, North America, China | Medium term (2-4 years) |

| Cloud and AI Workloads in Hyperscale Centers | +0.9% | North America and APAC, spill-over to Europe | Short term (≤2 years) |

| Edge-Computing IoT Node Proliferation | +0.7% | Global, smart-city pilots in APAC and Europe | Long term (≥4 years) |

| Satellite Mega-Constellations | +0.6% | North America and Europe launch operators | Long term (≥4 years) |

| Chip-Scale Atomic Clock Breakthroughs | +0.5% | North America and Europe defense and aerospace users | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

5G Infrastructure Build-Out Momentum

Operators deployed 1.8 million 5G base stations during 2025, each needing OCXO or TCXO references that maintain phase noise below -160 dBc/Hz at a 10 kHz offset. Small-cell densification multiplies the count of timing nodes per square kilometer, pushing vendors that provide IEEE 1588v2-certified modules with >1 µs holdover over 24 hours to the front of procurement queues. China Mobile’s plan for another 500,000 5G-Advanced sites by 2027 signals multiyear demand visibility. U.S. carriers following a C-band expansion path recorded a 40% year-on-year jump in stratum-3E oscillator orders in H1 2025.[1]Ericsson, “5G Infrastructure Deployments 2025,” ericsson.com Open RAN disaggregation further raises the clock count because radio units must now self-discipline without relying on centralized GPS alone.

Electrification and ADAS Penetration in the Automotive Industry

Battery electric and plug-in hybrid vehicles reached 18% of global light-duty sales in 2025, each integrating 15-25 oscillators for power-electronics and sensor-fusion modules. ISO 26262 ASIL-D rules cap timing failure rates below 10 FIT, removing consumer-grade crystals from safety-critical designs. Bosch’s adoption of MEMS oscillators in its sixth-generation radar sensors demonstrated 50% power savings versus quartz.[2]Bosch, “Automotive Sensor Technologies,” bosch.com Tesla’s dual-source strategy for its Hardware 4.0 platform underscores the risk-mitigation premium placed on timing supply assurance. Software-defined vehicle roadmaps are also favoring programmable oscillators that can be updated over-the-air instead of requiring board swaps.

Cloud and AI Workloads Fuelling Hyperscale Data Centers

Hyperscalers commissioned 120 GW of capacity in 2025, with AI clusters now requesting synchronization tighter than 100 ns to avoid gradient staleness in distributed GPU training.[3]Uptime Institute, “Data Center Infrastructure Report 2025,” uptimeinstitute.com Microsoft Azure placed IEEE 1588 boundary clocks in every top-of-rack switch during 2025. Amazon Web Services moved further, unveiling a proprietary chip-scale atomic-clock appliance that keeps drift below 70 ns when GNSS is lost, illustrating a willingness to absorb higher component costs for AI latency advantages. These shifts are redirecting OCXO demand into data-center white space once dominated by lower-cost TCXO devices.

Edge-Computing IoT Node Proliferation

Industrial IoT deployments surpassed 14 billion endpoints in 2025, and designers now favor MEMS oscillators that draw <1 µA standby current to maximize battery life. SiTime’s Cascade family delivers ±20 ppm accuracy at 32 kHz while consuming 1.2 µA, extending node battery life to seven years. Horizon Europe earmarked EUR 300 million (USD 318 million) for smart-manufacturing pilots, further accelerating uptake in predictive-maintenance sensor grids. Clock drift directly degrades time-series correlation in these networks, making tightly compensated low-power references a design-critical item.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fab Capacity Constraints for Quartz Blanks | -0.8% | Global, centered on Japanese suppliers | Short term (≤2 years) |

| Price Erosion in Consumer Devices | -0.6% | Global, severe in APAC hubs | Medium term (2-4 years) |

| Export-Control Risks on Timing IP | -0.4% | US-China trade corridor | Medium term (2-4 years) |

| Long Qualification Cycles in Critical Verticals | -0.5% | Global, automotive and aerospace focus | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Fab Capacity Constraints for High-Precision Quartz Blanks

Four Japanese companies supplied most AT-cut quartz blanks above 100 MHz in 2025, operating at 92% utilization with 26-week lead times. Seiko Epson’s JPY 15 billion (USD 107 million) Suwa expansion will add only 15% capacity by late 2027. High capital requirements—USD 80-120 million per cleanroom line—discourage new entrants. This bottleneck has pushed telecom OEMs to mix quartz and MEMS oscillators, trading slightly higher phase noise for reliable delivery.

Price Erosion from Commoditization in Consumer Devices

Average selling prices for 32.768 kHz tuning-fork crystals slid 12% year-on-year in 2025 because of oversupply in China’s Guangdong and Jiangsu provinces. Smartphone application processors that integrate on-chip MEMS resonators, such as Qualcomm’s Snapdragon 8 Gen 4, are shrinking the standalone crystal bill of materials. TXC reported a 9% drop in consumer crystal revenue even as automotive sales rose 18% in its 2025 filings. Margin compression is triggering consolidation among second-tier suppliers and accelerating pivots toward higher-value automotive and industrial niches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Oscillators Accelerate Amid Integration Push

Oscillators added 7.07% CAGR momentum through 2031, outpacing crystals that nonetheless contributed 43.72% of 2025 revenue. The frequency control and timing devices market size attached to temperature-compensated crystal oscillators grew because 5G small-cell radios need ±0.5 ppm stability across a -40 °C to +85 °C envelope. Voltage-controlled crystal oscillators stay critical for RF phase-locked loops that require fine pulling linearity, while oven-controlled variants fetch USD 500-plus for stratum-1 references.

MEMS oscillators gained share by offering digital programmability, slashing SKU counts and trimming board space. SiTime’s Titan platform hit ±0.1 ppm stability at 60% lower power, broadening MEMS acceptance in telecom and automotive applications. Crystals still dominate sub-1 MHz ultra-low-power nodes, sustaining demand for 32.768 kHz watch crystals in IoT and medical implants.

By Technology: MEMS Chips Close Gap on Quartz

Quartz retained 71.81% share in 2025, benefiting from maturity and superior aging. However, MEMS devices are climbing a 7.11% CAGR curve as their monolithic silicon eliminates vibration-induced frequency error that affects quartz in electric powertrains. SAW technology fills a niche in RF filters for 5G carrier aggregation at frequencies where quartz thickness becomes impractical.

Bulk-acoustic and film-bulk-acoustic resonators handle >2 GHz ranges for millimeter-wave radios, an area Texas Instruments entered in 2025. Quartz suppliers are striking back with photolithography-defined electrodes that cut frequency tolerance to ±10 ppm without laser trim, limiting MEMS cost advantage. The frequency control and timing devices market share distribution is therefore bifurcating across precision, power and frequency axes.

By Packaging: Surface-Mount Commands Mass Production, Through-Hole Finds Renewed Use

Surface-mount designs supplied 79.74% of 2025 shipments, reflecting decades of size and assembly automation. Wafer-level chip-scale packages now stand 0.67 mm tall and survive 20,000 g shock, enabling wearables and implants.

Through-hole parts, though a smaller base, are growing at 7.16% CAGR on the back of aerospace and defense retrofit programs. MIL-PRF-55310 still specifies socketed timing sources for field maintainability. Automotive zonal control units facing vibration and thermal cycling also prefer mechanically robust through-hole oscillators when reflow reliability is questioned.

By End-User: Automotive Gains Ground on Telecom

Telecom and data-center operators held 37.57% share in 2025, yet automotive timing demand is rising fastest at 7.20% CAGR. Stricter ASIL-D rules move oscillator sourcing decisions from procurement to system-safety teams, raising unit ASPs. Consumer electronics volume is plateauing because smartphones integrate on-chip oscillators, trimming discrete consumption.

Industrial and IoT verticals are embracing time-sensitive networking under IEEE 802.1AS, and aerospace users continue to specify OCXO and chip-scale atomic clocks for GNSS-denied navigation. Medical implants present an emerging ultralow-power niche where MEMS shock resistance surpasses quartz.

Geography Analysis

Asia Pacific generated 35.74% of 2025 revenue and is forecast to expand at a 7.22% CAGR as China targets 2.3 million 5G sites by 2025 end and Japan deepens its quartz-blank leadership. South Korea’s electronics exports surged 16% on Hyundai’s MEMS-heavy electrification roadmap. India’s production-linked incentive pooled USD 4.2 billion pledges for timing-device assembly plants.

North America ranks second, driven by hyperscalers investing USD 180 billion in new data-center capacity. Precision time appliances are now a competitive weapon for AI latency budgets, spurring OCXO and chip-scale atomic clock procurement. Defense programs seeking radiation-hardened clocks also sustain baseline demand.

Europe’s trajectory hinges on automotive OEM adoption of sub-nanosecond synchronization for connected mobility corridors backed by ETSI mandates. The Middle East faces rising need as Saudi Arabia’s NEOM project designs autonomous transport that hinges on IEEE 1588 grandmaster clocks. Africa and South America are earlier in the curve where 4G densification and industrial automation spark foundational requirements for TCXO and crystals.

Mordor Intelligence provides coverage of the frequency control and timing devices market across other key regional markets, including Europe, Middle East, and Africa, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to United States incorporating local coverage and market participation, as required.

Competitive Landscape

The top five suppliers—Murata, Kyocera, Seiko Epson, SiTime and Microchip—captured about 48% of 2025 sales, giving the frequency control and timing devices market a moderate concentration. Seiko Epson is vertically integrating with a USD 179 million quartz-blank expansion to tame 26-week lead times. MEMS specialists such as SiTime operate fabless, relying on foundry partners and focusing R&D on digital compensation IP.

Patent data from 2025 shows 14 SiTime grants for frequency synthesis and eight Rakon applications on low-phase-noise OCXOs, underlining a pivot toward software-defined compensation. Texas Instruments, NXP and Analog Devices are bundling oscillators in system-on-chip products, internalizing demand and pressuring discrete suppliers.

White-space now exists in AEC-Q100 Grade 0 MEMS oscillators, a spec only six vendors clear today. Smaller firms such as Abracon and IQD court industrial IoT by promising non-standard frequency samples in two weeks, compared with the 12-week norm. IEEE 1588 certification has become a moat, with fewer than 20 oscillator models holding grandmaster-class approval, concentrating telecom wins among early movers.

Frequency Control And Timing Devices Industry Leaders

Murata Manufacturing Co. Ltd

Kyocera Corporation

Rakon Limited

Microchip Technology Inc.

TXC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: SiTime released the Titan Elite MEMS oscillators with ±0.05 ppm stability targeting stratum-1 telecom systems.

- January 2026: Microchip closed its USD 850 million acquisition of Renesas’ timing division to strengthen aerospace and defense OCXO lines.

- December 2025: Kyocera opened a JPY 25 billion (USD 179 million) crystal plant in Kagoshima adding 30% automotive-grade capacity.

- November 2025: Rakon won a NZD 45 million (USD 27 million) OCXO contract for a 120-satellite LEO constellation.

Global Frequency Control And Timing Devices Market Report Scope

Frequency control and timing devices play a crucial role in electronic devices, providing signals that dictate the speed and timing of information transmission. They are instrumental in offering synchronizing signals and ensuring seamless operations in a variety of applications, including Zigbee, Bluetooth, smartphones, automobiles, and medical equipment.

The Frequency Control and Timing Devices Market Report is Segmented by Product Type (Crystals, Oscillators, Resonators), Technology (Quartz, MEMS, SAW, Others), Packaging (SMD, Through-Hole/DIP), End-User (Telecom and Data Centers, Automotive, Consumer Electronics, Industrial and IoT, Aerospace and Defense, Healthcare, Others), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). Market Forecasts are Provided in Terms of Value (USD).

| Crystals | |

| Oscillators | Temperature-Compensated Crystal Oscillator (TCXO) |

| Voltage-Controlled Crystal Oscillator (VCXO) | |

| Oven-Controlled Crystal Oscillator (OCXO) | |

| MEMS Oscillator | |

| Other Oscillators | |

| Resonators |

| Quartz |

| MEMS |

| Surface-Acoustic-Wave (SAW) |

| Others |

| Surface-Mount Device (SMD) |

| Through-Hole / DIP |

| Telecommunications and Data Centers |

| Automotive and Transportation |

| Consumer Electronics |

| Industrial and IoT |

| Aerospace and Defense |

| Healthcare and Medical Devices |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Crystals | |

| Oscillators | Temperature-Compensated Crystal Oscillator (TCXO) | |

| Voltage-Controlled Crystal Oscillator (VCXO) | ||

| Oven-Controlled Crystal Oscillator (OCXO) | ||

| MEMS Oscillator | ||

| Other Oscillators | ||

| Resonators | ||

| By Technology | Quartz | |

| MEMS | ||

| Surface-Acoustic-Wave (SAW) | ||

| Others | ||

| By Packaging | Surface-Mount Device (SMD) | |

| Through-Hole / DIP | ||

| By End-User | Telecommunications and Data Centers | |

| Automotive and Transportation | ||

| Consumer Electronics | ||

| Industrial and IoT | ||

| Aerospace and Defense | ||

| Healthcare and Medical Devices | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What CAGR is forecast for the frequency control and timing devices market from 2026 to 2031?

The market is projected to grow at a 7.04% CAGR during 2026-2031.

Which product segment is expanding fastest through 2031?

Oscillators are the fastest-growing product type, advancing at a 7.07% CAGR through 2031.

Why is MEMS technology gaining share against quartz?

MEMS oscillators offer vibration immunity, digital programmability and lower power, driving a 7.11% CAGR compared with slower quartz growth.

Which region leads revenue and growth?

Asia Pacific leads with 35.74% revenue in 2025 and is forecast to post the highest regional CAGR at 7.22% through 2031.

How are hyperscale data centers influencing oscillator demand?

AI clusters need sub-100 ns synchronization, prompting hyperscalers to specify OCXO and chip-scale atomic clocks for every rack switch.

What is the main supply-chain risk facing quartz suppliers?

Limited high-precision blank capacity in Japan creates 26-week lead times, pushing OEMs to consider MEMS alternatives.

Page last updated on: