Frankfurt Data Center Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

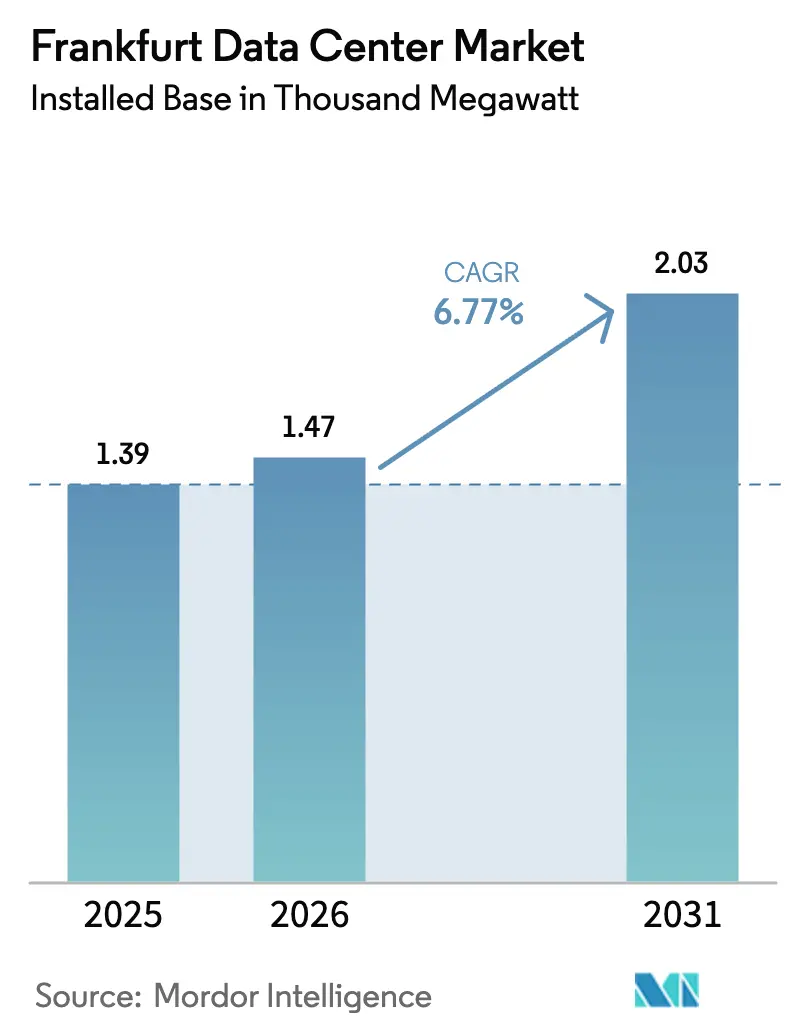

| Base Year Market Size (2025) | 1.39 Thousand megawatt |

| Market Volume (2026) | 1.47 Thousand megawatt |

| Market Volume (2031) | 2.03 Thousand megawatt |

| Growth Rate (2026 - 2031) | 6.77% CAGR |

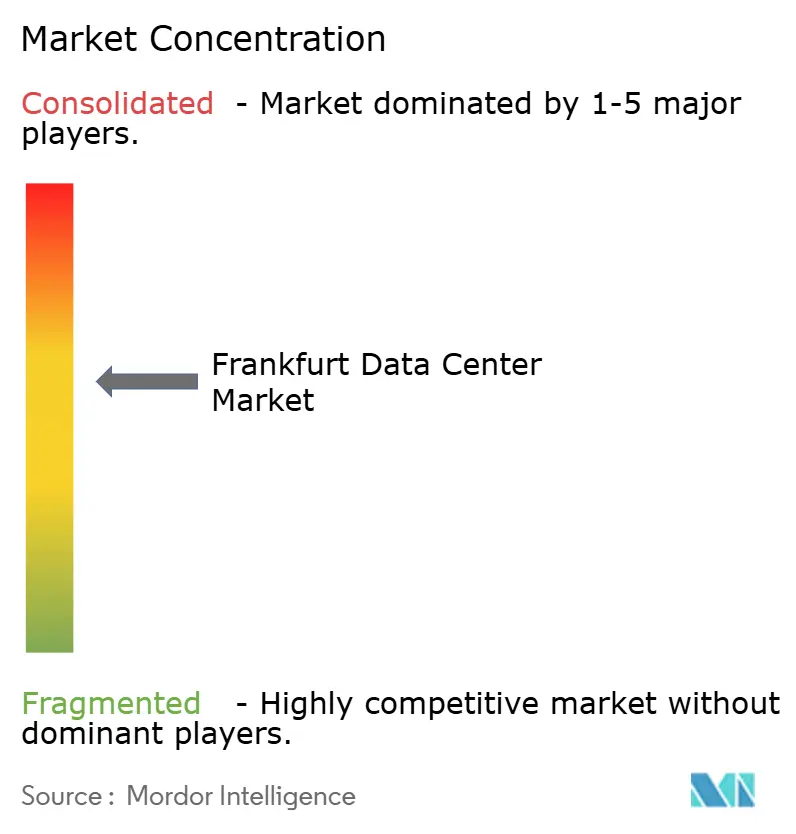

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Frankfurt Data Center Market Analysis by Mordor Intelligence

The Frankfurt Data Center Market size in terms of installed base is projected to expand from 1.39 thousand megawatt in 2025 and 1.47 thousand megawatt in 2026 to 2.03 thousand megawatt by 2031, registering a CAGR of 6.77% between 2026 to 2031. Capital continues to pour into Germany’s digital capital as hyperscalers accelerate sovereign-cloud builds, yet grid queues of three to five years push new capacity into adjacent towns, lifting land values and nudging operators toward behind-the-meter generation. Colocation providers that secured power reservations before 2024 now command premium prices, while newcomers shoulder 15-25% higher upfront costs for liquid-cooling retrofits. Demand for 150-240 kW racks tied to AI inference drives early adoption of direct-to-chip cooling, and regulatory pressure to reuse waste heat converts thermal output into a secondary revenue stream. Competitive intensity rises as Data4, CyrusOne, Vantage, and STACK Infrastructure collectively announce 663 MW of greenfield builds, compressing wholesale rates in outer-ring sub-markets.

Key Report Takeaways

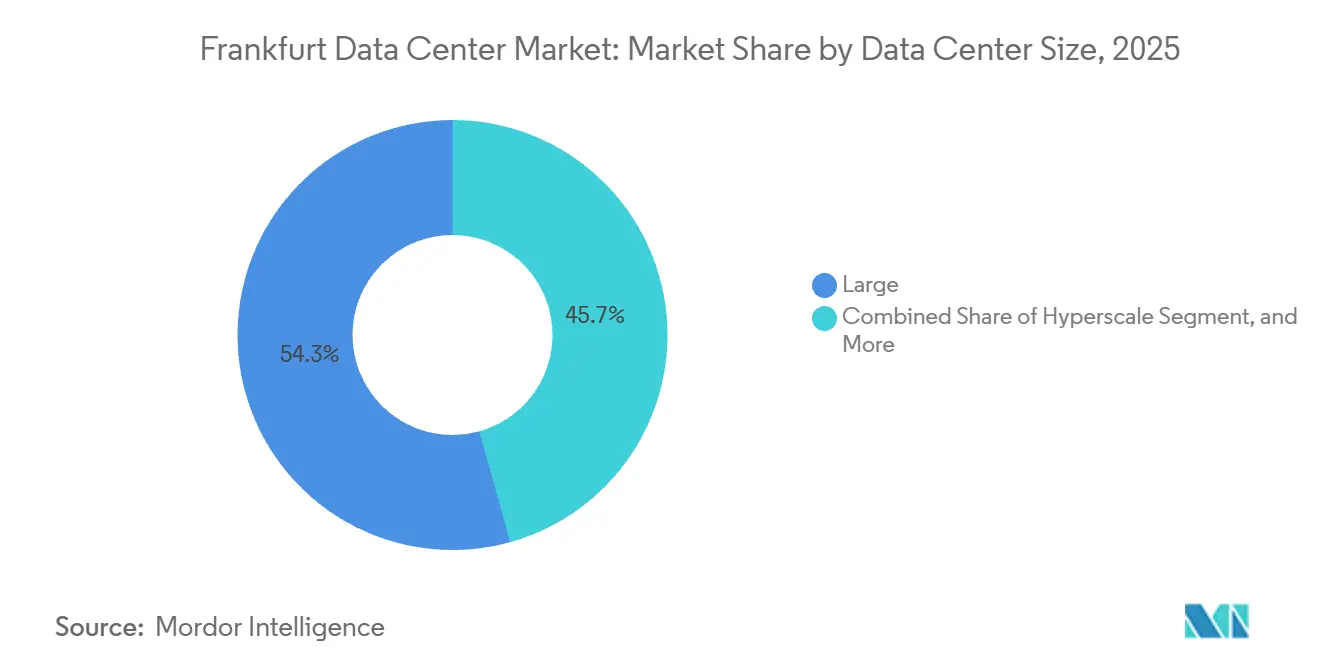

- By data center size, large facilities held 54.32% of 2025 installed capacity, while hyperscale campuses are projected to expand at a 7.41% CAGR through 2031.

- By tier, tier 3 captured 64.86% of 2025 deployments, whereas tier 4 builds are set to grow at 7.24% as financial institutions migrate to higher-resilience halls.

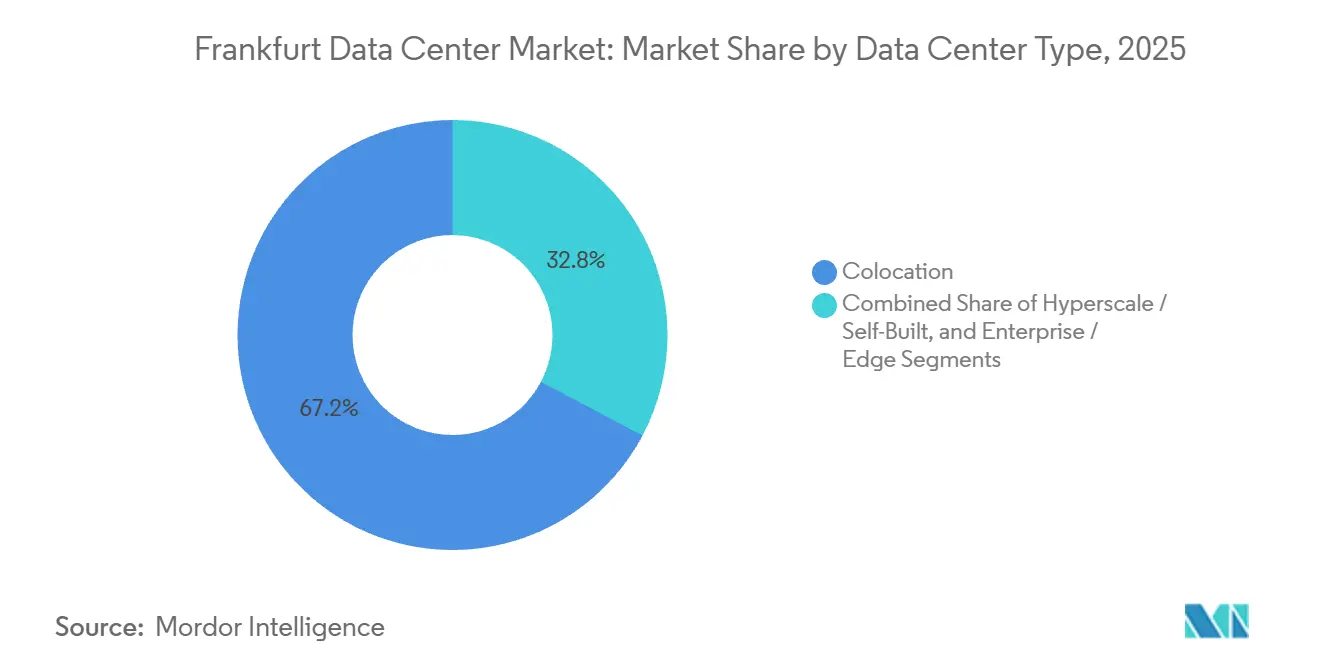

- By data center type, colocation represented 67.25% of 2025 installed capacity, yet hyperscale and self-build capacity will expand at 7.62% annually as major cloud providers internalize operations.

- By end user, IT and ITES accounted for 27.86% of 2025 installed capacity, but BFSI workloads will accelerate by 8.59% due to real-time payment mandates.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Frankfurt Data Center Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale Cloud Expansion by US Tech Majors | +1.8% | Frankfurt metro, spill-over to Hanau, Dietzenbach, Offenbach | Medium term (2-4 years) |

| AI Clusters Driving High-Density Liquid-Cooling Demand | +1.5% | Global, concentrated in Frankfurt core and Hanau edge zones | Short term (≤ 2 years) |

| Sovereign-AI Initiatives of German Federal Agencies | +1.2% | National, with early deployments in Frankfurt, Berlin, Munich | Long term (≥ 4 years) |

| Strategic FLAPD Network-Latency Advantage | +0.9% | Frankfurt metro, competitive with Amsterdam, Paris, London, Dublin | Medium term (2-4 years) |

| New Submarine Cable Landings Boost Bandwidth | +0.6% | Frankfurt metro, extending to Prague, Vienna corridors | Long term (≥ 4 years) |

| Grid-Decarbonisation Commitments Lure Green Tenants | +0.5% | Frankfurt metro, Hesse state, broader Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hyperscale Cloud Expansion By US Tech Majors

Amazon Web Services earmarked EUR 8.8 billion for capacity adds through 2026, Google pledged EUR 5.5 billion between 2026 and 2029, and Microsoft is expanding Azure regions, all targeting purpose-built campuses that support 150 kW-plus racks and liquid cooling. The shift pulls development toward Hanau and Dietzenbach, locations offering faster power approvals and room for 100-MW blocks. Established colocation operators respond by acquiring peripheral land or accepting margin compression as tenants migrate. CyrusOne’s tie-up with E.ON delivers 61 MW of on-site generation, signalling that utility partnerships become a prerequisite for projects over 50 MW.[1]CyrusOne Press Team, “CyrusOne and E.ON Announce Strategic Partnership to Overcome Data Center Grid Capacity Constraints,” CyrusOne, cyrusone.comOverall, hyperscale spending lifts construction pipelines but also intensifies the battle for scarce power allocations.

AI Clusters Driving High-Density Liquid-Cooling Demand

Rack densities in the latest Frankfurt builds now range from 132 kW to 240 kW, quadruple the 30-40 kW standard that was prevalent only three years ago. Digital Realty’s FRA18 debuted in March 2025 with direct-to-chip cooling, supporting NVIDIA H100 clusters at 150 kW per rack without throttling. Hyperscalers pay a 20-30% capex premium, while mid-market enterprises stick with traditional air-cooled floors. Liquid cooling simultaneously unlocks 50-60 °C waste heat suitable for district heating, helping operators meet Germany’s Energy Efficiency Act, which requires heat reuse above 30% for new halls. Early movers monetize both AI demand and thermal by-products, whereas laggards face stranded assets when tenants chase denser footprints.

Sovereign-AI Initiatives of German Federal Agencies

DataHub Europe and allied projects mandate that sensitive models and datasets stay on German soil, reserving 10-15% of Frankfurt’s addressable load for providers with German operational control. Procurement cycles shorten to three to four months under framework agreements, rewarding operators already vetted for security. Data4’s Hanau campus offers air-gapped zones and on-premises key management to meet federal standards.[2]Data4 Group, “Data4 Lays the Foundations on Its First Mega Campus in Germany,” Data4, data4group.comOnce a ministry lands a workload, migration costs lock demand for five-seven years, providing durable revenue. Providers lacking sovereign credentials risk exclusion from a high-margin, low-churn segment projected at EUR 400-600 million annually by 2029.

Strategic FLAPD Network-Latency Advantage

Frankfurt anchors the FLAPD cluster and hosts DE-CIX, which introduced 800G optics in November 2025 and an AI-IX service two months earlier.[3]DE-CIX Media, “DE-CIX Launches AI-IX,” DE-CIX, de-cix.netRound-trip latency under two milliseconds remains critical for algorithmic trading between Xetra and London’s LSE. As hyperscalers expand into outer-ring towns, the city’s interconnection density helps maintain premium retail pricing for latency-sensitive workloads. Operators bundling direct cross-connects to DE-CIX and sub-one-millisecond paths to cloud on-ramps capture BFSI demand that values speed over cost.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-Connection Moratorium and Power-Availability Limits | -1.4% | Frankfurt core, moderate impact in Hanau, Dietzenbach, Offenbach | Short term (≤ 2 years) |

| Rising Electricity Costs from EU Carbon Pricing | -0.9% | Frankfurt metro, broader Germany and EU | Medium term (2-4 years) |

| Community Opposition over Water-Consumption Spikes | -0.5% | Hanau, Griesheim, Dietzenbach municipalities | Medium term (2-4 years) |

| Specialised-Talent Shortage in Frankfurt DC Operations | -0.4% | Frankfurt metro, broader Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid-Connection Moratorium and Power-Availability Limits

Mainova and Amprion extended lead times for new power links to as long as five years, forcing newcomers to seek brownfield sites or finance behind-the-meter generation. CyrusOne’s FRA7 illustrates the workaround, with 61 MW of on-site gas generators that raise capex but shave up to 2 years off delivery. Scarcity inflates land within 500 m of substations by 40-60%, spawning a land-banking strategy for investors awaiting Amprion’s EUR 1.2 billion transmission upgrade due in 2029. Operators without power reservations face high entry barriers, pushing the market toward consolidation.

Rising Electricity Costs from EU Carbon Pricing

EU ETS allowances averaged EUR 85 per tonne CO₂ in 2025 and are forecast to top EUR 100 by 2028, adding roughly 18% to gas-peaker backup costs. Deutsche Telekom covered 50% of its data-center load with renewable PPAs by end-2025, locking in rates 15-20% below spot. Google’s 24/7 carbon-free arrangement with Engie and Ørsted lifts its German portfolio to 85% carbon-free energy in 2026. Operators without multi-country scale struggle to sign sub-50 MW PPAs, leaving them exposed to rising carbon pass-throughs and squeezing already tight wholesale margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Size: Hyperscale Campuses Capture AI Workload Surge

Hyperscale campuses delivered the fastest trajectory, rising from a modest base toward a projected 7.41% CAGR through 2031, underpinned by cloud providers internalizing 150-240 kW racks. Large sites accounted for 54.32% of installed load in 2025, yet their share erodes as AWS, Google, and Microsoft favor 100-MW blocks outside the grid-constrained core. Medium facilities anchor enterprise cages within five milliseconds of DE-CIX, supporting stable but slower 5.8% growth. Small edge nodes tied to 5G standalone networks maintain relevance in telecom deployments across 12 German metros. The Frankfurt data center market for hyperscale campuses is on track to outpace all other segments, while large halls remain the bulk of near-term revenue.

Hyperscale operators spread cooling and fiber backhaul across mega-campuses, cutting per-kW capex by up to 35% compared with modular builds. Compliance with Germany’s Energy Efficiency Act raises capital intensity but creates a moat for well-financed projects such as NTT’s 482 MW Nierstein campus, slated for commissioning in 2029. Hyperscale-ready white space in Hanau and Dietzenbach underpins a bifurcated Frankfurt data center market where latency-sensitive loads stay downtown and large AI workloads flock outward.

By Tier Type: Tier 4 Builds Accelerate Under Financial-Sector Mandates

Tier 3 halls commanded 64.86% of 2025 capacity, but Tier 4 rooms accelerate at 7.24% CAGR after BaFin’s January 2026 resilience update that obliges systemically important banks to migrate core stacks into 2N+1 redundant environments. The Frankfurt data center market share of Tier 4 facilities inches up each year as Commerzbank and Deutsche Bank move their payment rails and trading engines to higher-redundancy zones. Operators such as Equinix and Digital Realty leverage multi-tenant footprints to amortize the 35-45% capex premium required for Tier 4 builds.

CyrusOne’s FRA7 targets a PUE below 1.3 while reusing up to 40 MW of heat for the Westside district network, marrying Tier 4 uptime to BREEAM “Very Good” certification. Operators unable to retrofit older Tier 2 halls face occupancy declines as tenants recontract to compliant sites, reinforcing a consolidation trend in the Frankfurt data center market.

By Data Center Type: Colocation Dominance Erodes as Hyperscalers Internalize

Colocation captured 67.25% of installed load in 2025, yet hyperscale self-builds will post 7.62% CAGR, the quickest among all facility types. Retail colocation maintains pricing of EUR 180-220 per kW by bundling meet-me-room access to DE-CIX, which is critical for BFSI and manufacturing workloads. Wholesale colocation anchors cost-sensitive enterprise tenants at EUR 120-150 per kW, expanding at a mid-6% pace. The Frankfurt data center market for self-built hyperscale capacity is projected to surpass wholesale revenue by 2031 as pre-leasing absorbs remaining inventory.

Digital Realty’s hybrid FRA18 template reserves one-fifth of space for retail cages within an otherwise hyperscale-oriented hall, hedging against demand swings. Vacancy across the Frankfurt data center market fell to 4.8% by mid-2025, tightening to a forecast 3.4% in 2026, suggesting higher price elasticity for operators with ready-to-fit halls.

By End User: BFSI Leads Growth on Real-Time Payment Mandates

BFSI workloads are set to climb at an 8.59% CAGR through 2031 as EU instant payment rules cap transaction windows at 10 seconds, forcing banks to locate compute within 2-millisecond round-trips to Xetra. IT and ITES remain the largest slice, accounting for 27.86% of installed load and expanding at the market’s average pace. E-commerce, manufacturing, and government clusters deliver steady mid-6% gains, while media and telecom edge nodes fragment workloads across multiple metros. Tier 4 space within ten kilometers of downtown Frankfurt wins the lion’s share of BFSI expansion, underscoring the value of low latency.

Commerzbank and Lufthansa’s 2025 migration to Google’s Hanau site illustrates the swivel toward resilient, sovereign facilities that meet both BaFin and CSRD benchmarks. This momentum bolsters the Frankfurt data center market share of Tier 4 halls, even as outer-ring hyperscale builds capture less latency-sensitive AI training clusters.

Geography Analysis

Frankfurt commands roughly 60% of Germany’s upcoming power capacity and hosted between 831 MW and 1,020 MW of live IT load in mid-2025. DE-CIX handled 79 exabytes of traffic in 2025, a 16% lift that underscores the city’s interconnection gravity. Yet protracted power queues reroute expansion to Hanau, Dietzenbach, and Nierstein, which collectively logged 742 MW of announced builds. Core sites preserve premium retail colocation prices, whereas outer-ring halls trade performance for faster grid access and cheaper land.

Secondary German hubs, chiefly Berlin and Munich, house 80-120 MW apiece, but their smaller internet exchanges limit appeal for ultra-low-latency applications. Hesse’s tax incentives for sub-1.2 PUE builds drew Colt DCS’s 63 MW Frankfurt 4 and 5 projects, reinforcing regional clustering. Frankfurt’s eastern vantage offers under-10 millisecond paths to Prague and Vienna, drawing Central European cloud tenants seeking EU residency without western rates.

Network upgrades bolster the hub-and-spoke pattern. Eurofiber’s Frankfurt-Vienna route and GlobalNet’s DWDM rings trimmed latency, enabling banks to comply with DORA’s geographic dispersion mandates. While grid scarcity pushes capacity outward, interconnection density assures Frankfurt’s status as the focal point of the German and Central European digital economy.

Competitive Landscape

The market is moderately concentrated, with players such as NTT Global Data Centers, Digital Realty, Equinix, and others. Wholesale prices in Griesheim, Offenbach, and Hanau slid 8-12% as new capacity hit the market. Incumbents differentiate on cooling maturity, renewable PPAs, and DE-CIX cross-connect density rather than raw scale.

Digital Realty introduced 150 kW liquid-cooled racks at FRA18, while CyrusOne’s E.ON alliance eliminates grid dependency for FRA7. Municipal utilities such as Mainova leverage substation access to bundle power and colocation, undercutting private peers on electricity by up to 15%. Antin bought NorthC’s 140 MW platform in December 2025; STACK acquired Wortmann's assets; and Iron Mountain picked up three EWE halls, signaling that private equity views regulatory complexity as an entry hurdle favoring larger portfolios.

Certification and sustainability emerge as table stakes. Germany’s 2024 Energy Efficiency Act enforces PUE below 1.2 and 30% heat reuse on new halls, nudging smaller operators toward sale or shutdown. The Frankfurt data center market thus inches toward an oligopoly where capital depth, energy partnerships, and sovereign-cloud credentials dictate share gains.

Frankfurt Data Center Industry Leaders

Digital Realty Trust Inc.

Equinix Inc.

NTT Global Data Centers

CyrusOne Inc.

Vantage Data Centers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: DE-CIX reported global exchange traffic hit 79 exabytes in 2025, a 16% rise, reinforcing Frankfurt’s interconnection magnet.

- December 2025: Antin Infrastructure Partners agreed to acquire NorthC Datacenters, adding 140 MW of secured capacity in German metros.

- December 2025: NTT Global Data Centers secured approval for a 482 MW Nierstein campus, with operations slated for 2029.

- November 2025: DE-CIX Frankfurt activated the world’s first 800 G IX port using Nokia 800 G ZR+ optics.

Frankfurt Data Center Market Report Scope

The data center market encompasses the infrastructure, services, and technologies that support the storage, management, and processing of data. This market includes various data center sizes, tier classifications, types, end-user industries, and hotspots, reflecting the diverse needs of businesses and organizations operating in them.

The Frankfurt Data Center Market Report is Segmented by Data Center Size (Small, Medium, Large, and Hyperscale), Tier Type (Tier 1 and 2, Tier 3, and Tier 4), Data Center Type (Hyperscale/Self-Built, Enterprise/Edge, and Colocation), and End User (BFSI, IT and ITES, E-Commerce, Government, Manufacturing, Media and Entertainment, Telecom, and Other End Users). The Market Forecasts are Provided in Terms of IT Load Capacity (Megawatt).

| Small |

| Medium |

| Large |

| Hyperscale |

| Tier 1 and 2 |

| Tier 3 |

| Tier 4 |

| Hyperscale / Self-Built | ||

| Enterprise / Edge | ||

| Colocation | Non-Utilized | |

| Utilized | Retail Colocation | |

| Wholesale Colocation | ||

| BFSI |

| IT and ITES |

| E-Commerce |

| Government |

| Manufacturing |

| Media and Entertainment |

| Telecom |

| Other End Users |

| By Data Center Size | Small | ||

| Medium | |||

| Large | |||

| Hyperscale | |||

| By Tier Type | Tier 1 and 2 | ||

| Tier 3 | |||

| Tier 4 | |||

| By Data Center Type | Hyperscale / Self-Built | ||

| Enterprise / Edge | |||

| Colocation | Non-Utilized | ||

| Utilized | Retail Colocation | ||

| Wholesale Colocation | |||

| By End User | BFSI | ||

| IT and ITES | |||

| E-Commerce | |||

| Government | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Telecom | |||

| Other End Users | |||

Key Questions Answered in the Report

How fast is the Frankfurt data center market expected to grow?

Capacity is projected to rise from 1.47 thousand MW in 2026 to 2.03 thousand MW by 2031 at a 6.77% CAGR.

Which customer segment shows the strongest demand momentum?

BFSI workloads expand at 8.59% per year as instant payment regulations drive ultra-low-latency requirements.

Why are hyperscalers building outside Frankfurt’s city limits?

Three-to-five-year grid queues in the core push hyperscalers to Hanau, Dietzenbach, and Nierstein where power can be secured sooner and land is cheaper.

What cooling technology is gaining traction in new Frankfurt halls?

Direct-to-chip liquid cooling enabling 150-240 kW racks is standard in 2025-2026 openings, supporting AI inference clusters.

How do German regulations influence future builds?

The 2024 Energy Efficiency Act demands PUE below 1.2 and at least 30% waste-heat reuse, increasing capex but creating a barrier to entry for smaller operators.

Which operators currently dominate capacity?

NTT Global Data Centers, Digital Realty, and Equinix together control roughly 45% of installed load, though new entrants are rapidly adding supply.

Page last updated on: