Germany Data Center Networking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

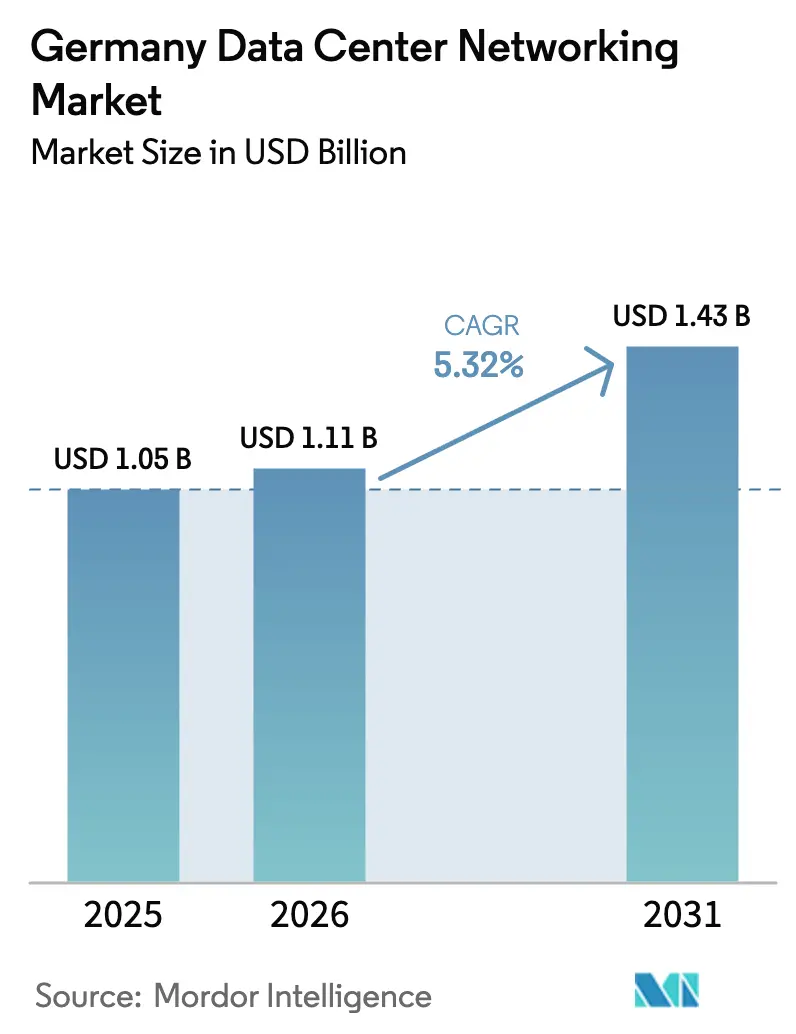

| Base Year Market Size (2025) | USD 1.05 Billion |

| Market Size (2026) | USD 1.11 Billion |

| Market Size (2031) | USD 1.43 Billion |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany Data Center Networking Market Analysis by Mordor Intelligence

Germany data center networking market size in 2026 is estimated at USD 1.11 billion, growing from 2025 value of USD 1.05 billion with 2031 projections showing USD 1.43 billion, growing at 5.32% CAGR over 2026-2031. Hyperscale cloud providers are injecting multibillion-dollar capital into Frankfurt, Berlin, and Munich facilities, accelerating demand for next-generation 400G and 800G switching. Government mandates on fiber roll-out and renewable-energy sourcing tighten compliance deadlines, prompting early equipment refreshes. Rapid AI adoption across automotive, manufacturin,g and research drives a pivot from 25G or 100G architectures toward lossless fabrics that support large-scale GPU clusters. Liquid-cooling requirements, stricter PUE targets, and edge deployments in Industry 4.0 factories together shift spending toward high-efficiency, software-defined networks that can be managed by lean teams.

Key Report Takeaways

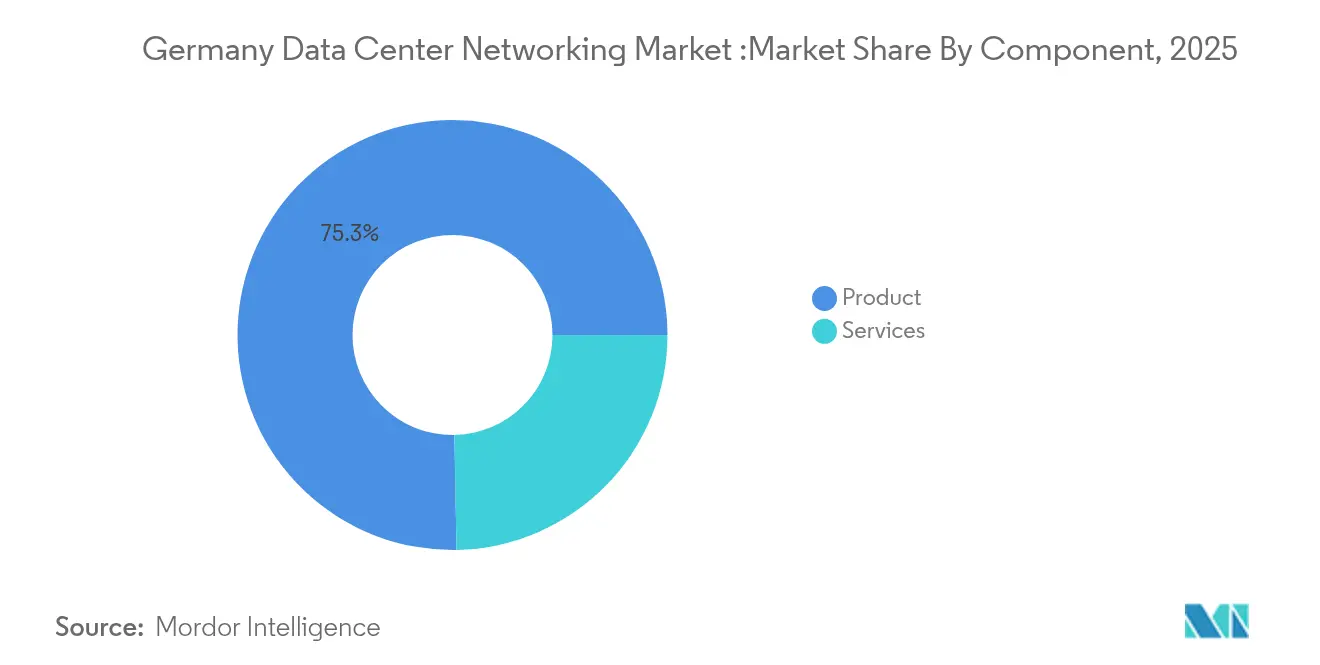

- By component, Products held 75.30% of Germany data center networking market share in 2025; Services post the highest 5.61% CAGR through 2031.

- By end-user, IT and Telecommunications commanded 35.20% share in 2025, while Manufacturing and Industrial is on track for a 6.05% CAGR to 2031.

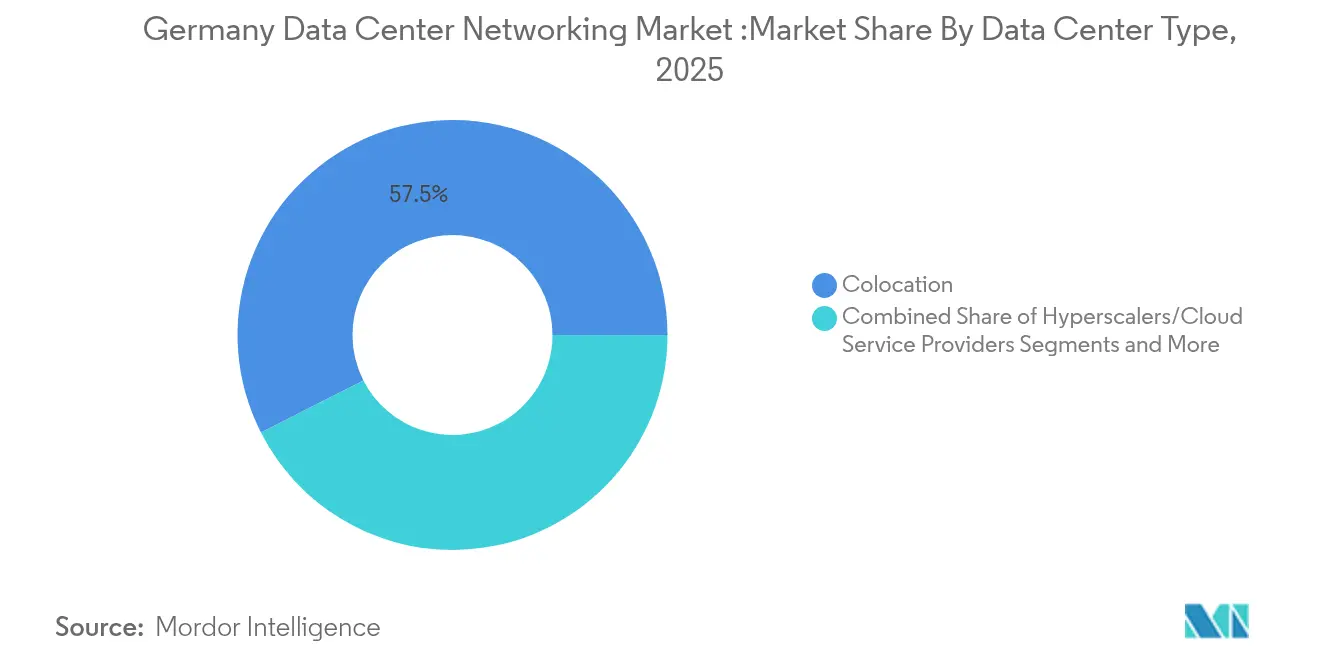

- By data-center type, Colocation led with 57.50% revenue share in 2025; Hyperscalers/Cloud Service Providers expand fastest at 7.68% through 2031.

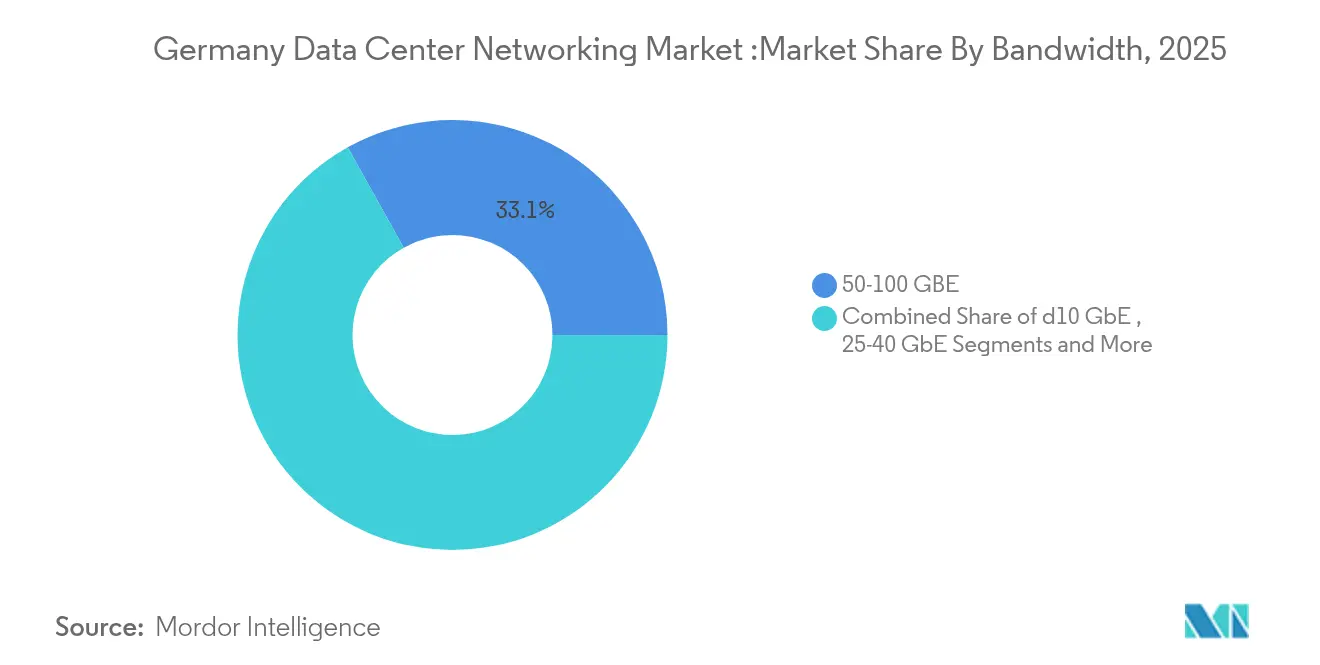

- By bandwidth, the 50–100 GbE segment accounted for 33.10% share of the Germany data center networking market size in 2025, whereas greater than 100 GbE registers a 7.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany holds a defined position within a broader international distribution. The data center networking market share data by Mordor Intelligence maps that allocation across all contributing countries and regions, globally.

Germany Data Center Networking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of hyperscale cloud and colocation footprints | +1.2% | Frankfurt, Berlin, Munich metro areas | Medium term (2-4 years) |

| Government Gigabit Strategy accelerating fiber amd 5G rollout | +0.8% | National, with priority in rural regions | Long term (≥ 4 years) |

| Surging AI/ML traffic driving 400G/800G switch refresh | +1.5% | Frankfurt data center corridor, major cities | Short term (≤ 2 years) |

| Rising edge-data-center deployments for IoT/low latency | +0.7% | Industrial regions, automotive clusters | Medium term (2-4 years) |

| Mandatory waste-heat-reuse rules boosting liquid-cooled gear | +0.4% | National, concentrated in urban areas | Long term (≥ 4 years) |

| EU sovereign-AI grants funding InfiniBand clusters | +0.6% | Research centers, major universities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of hyperscale cloud and colocation footprints

Hyperscalers are reshaping procurement cycles by specifying 800G-ready fabrics and InfiniBand clusters for AI training. AWS alone committed USD 9.44 billion to its Frankfurt region, pushing switch vendors to deliver high-density, liquid-cooling-compatible platforms. Colocation operators such as Digital Realty respond with AI-focused halls, drawing enterprise tenants that then require premium interconnects capable of multi-tenant segmentation. [1]Digitalrealty ,"Digital Realty Expands Frankfurt Footprint with AI-Optimized, Sustainable Data Center,"digitalrealty.com These parallel investments compress equipment lifecycles to under four years and create multiplier effects in secondary metros.

Government Gigabit Strategy accelerating fiber and 5G rollout

Berlin’s Gigabit Strategy funds EUR 17 billion (USD 19.93 billion) for nationwide fiber and 5G, obliging data-center owners to adopt higher-capacity interconnects that sustain rural back-haul traffic.[2]Federal Ministry of Transport, "Gigabit funding 2.0, "bmv.deGrants stipulate adherence to BSI C5 security rules, steering demand toward vendors with European manufacturing lines. Fiber densification also enables distributed edge nodes that rely on software-defined overlays to link new regional facilities with Frankfurt’s internet exchanges.

Surging AI/ML traffic driving 400G/800G switch refresh

Deutsche Telekom’s planned industrial AI cloud with 10,000 GPUs exemplifies the throughput jump that legacy 100G leaf-spine designs cannot support. [3]Deutsche Telekom AG. " AI Turbo for Gigafactories: Telekom announces European Industrial AI Infrastructure with NVIDIA." telekom.com Automotive OEMs integrating real-time vision analytics insist on lossless fabrics with RDMA, driving adoption of InfiniBand and Spectrum-X Ethernet solutions. Research clusters such as the Blue Lion supercomputer propel early trials of 800G optics, anchoring Germany data center networking market demand at the high-bandwidth end.

Rising edge-data-center deployments for IoT/low latency

Industry 4.0 roll-outs in Baden-Württemberg and the Ruhr require ruggedized switches that tolerate factory temperatures yet provide enterprise-grade telemetry. Private 5G licences issued to automotive groups combine OT and IT traffic, increasing reliance on SDN controllers that map deterministic paths. Edge nodes also host CDN caches, steering traffic away from Frankfurt backbones and reshaping traffic engineering policies across national routes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-grid constraints and high electricity costs in FLAP-D | -0.9% | Frankfurt, major metropolitan areas | Short term (≤ 2 years) |

| Shortage of certified network-automation engineers | -0.6% | National, acute in tech hubs | Medium term (2-4 years) |

| Data-sovereignty (BSI C5) limits foreign white-box adoption | -0.3% | National, critical infrastructure sectors | Long term (≥ 4 years) |

| Optical-fiber raw-material shortages delaying builds | -0.4% | National, supply chain dependent | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Energy-grid constraints and high electricity costs in FLAP-D

Frankfurt’s power caps force operators to distribute AI loads across multiple smaller halls, inflating port counts and cabling runs. The Energy Efficiency Act sets a PUE ceiling of 1.3 by 2030, pushing buyers toward higher-price, low-watt ASICs and liquid-cooled optics that lengthen ROI horizons. Renewable-power sourcing adds spatial constraints because solar or wind adjuncts consume land that could host additional racks.

Shortage of certified network-automation engineers

SDN and AI fabrics demand skills in RoCE, Ansible and P4-programmable pipelines that remain scarce. Hyperscale salary premiums drain talent from regional colocation and enterprise facilities, prolonging deployment timelines. SMEs increasingly outsource to managed-service specialists, raising operating expenditure and tempering adoption speed for advanced telemetry features.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Products anchor investment while Services accelerate

Products held 75.30% of Germany data center networking market share in 2025 of Germany data center networking market size. Switch refresh programs shift toward 400G and 800G platforms, and optical interconnect uptake scales with liquid-cooling aisle designs. SDN controller licenses rise as operators centralize management for metro-edge fabrics. Services are forecast to expand at a 5.61% CAGR, adding recurring revenue streams tied to AI-cluster optimisation and IPv6 migration. Managed Network Services absorb the skills gap, while integration specialists link private-5G cells to core data-center fabrics. Training programs see uptake as enterprises re-tool teams for GPU-centric traffic patterns. This mix elevates service spend from 2025 onward, yet hardware outlays remain dominant through 2030 in the Germany data center networking market.

By End-User: Manufacturing’s fast climb challenges IT incumbency

IT and Telecommunications continued to command 35.20% of Germany data center networking market share in 2025, anchored by carriers upgrading core routers for 5G and cloud providers scaling AI regions. DORA compliance bolsters switch-level segmentation and telemetry in financial data centers.Manufacturing and Industrial is projected to register 6.05% CAGR, outpacing all peers. Private 5G at facilities like Tesla’s Gigafactory creates micro-data-centers adjacent to production lines, each demanding low-latency fabrics. Factories integrate OT sensor grids with IT analytics, necessitating deterministic traffic engineering and redundant edge aggregation layers that lift spending per square meter.

By Data-Center Type: Hyperscalers narrow the gap with colocation

Colocation retained 57.50% share of Germany data center networking market size in 2025,. Tenants span fintech, government and media workloads that mandate sovereign hosting. Operators invest in spine-leaf topologies and SDN overlays to guarantee tenant isolation. Hyperscalers plot an 7.68% CAGR to 2031. Multi-billion-euro campuses specify custom ASICs, leafless fabrics and integrated liquid cooling. Their procurement volumes reshape supplier roadmaps and introduce open compute specifications, influencing wider market standards across the Germany data center networking market.

By Bandwidth: High-speed tiers gain momentum

The 50-100 GbE category accounted for 33.10% revenue in 2025 but faces gradual decline as AI workloads proliferate. Enterprises cling to 100 GbE for virtualisation clusters yet schedule upgrades before 2028 to meet hybrid-cloud latency objectives.Ports above 100 GbE post a 7.05% CAGR. Early 400G deployments in research supercomputers validate scalability, and 800G pilots begin within automotive AI labs. Optics vendors accelerate qualification cycles, pushing coherent-optical roadmaps that support inter-campus dark-fiber links across the Germany data center networking market.

Geography Analysis

Frankfurt anchors traffic flows, hosting DE-CIX peaks of 25 Tbps that necessitate continual spine uplifts and resilient routing. Hyperscalers’ region-build outs cluster at this nexus, driving multi-year purchase agreements for high-density switches and modular optics. Grid capacity limits and rising power tariffs encourage satellite deployments in Rhine-Main towns, yet connectivity gravity keeps Frankfurt dominant.Berlin forms the political and emerging tech twin-hub. Government cloud workloads and sovereign-AI projects foster demand for certified European equipment, steering procurement toward vendors with local assembly lines. Edge nodes sprout around Brandenburg’s automotive plants, each linking back to Berlin data-centers through dark-fiber rings that support real-time analytics.Munich benefits from aerospace and research institutions. The Blue Lion supercomputer anchors a regional 800G testbed, shaping early procurement of next-generation fabric ASICs. Bavaria’s renewable mix attracts sustainability-minded operators, though distance to Frankfurt’s exchange points raises dependence on coherent-optical gear.

Mordor Intelligence delivers a comprehensive view of the data center networking market across all major regions such as Europe, Asia, and Africa, alongside country-level analysis for Netherlands, Poland, China, South Africa, Nigeria, and Israel, each offering a view of the local market realities.

Competitive Landscape

Market structure is moderately concentrated. Cisco leverages a broad enterprise base yet faces rising share loss to Arista in AI-centric engagements. Arista’s Cluster Load Balancing and 800G roadmaps position it to capture hyperscale refreshes. NVIDIA extends vertical integration through Mellanox silicon and Spectrum-X, embedding itself in GPU cluster designs.

Vendor strategies hinge on alliances. Cisco’s silicon integration partnership with NVIDIA aligns Ethernet and InfiniBand under unified management stacks. HPE’s planned acquisition of Juniper seeks to combine compute and networking portfolios, targeting edge-to-cloud consistency demanded by German manufacturers. European regulations around supply-chain provenance give ADVA Optical and Nokia an edge in critical-infrastructure bids.

Germany Data Center Networking Industry Leaders

-

Cisco Systems Inc.

-

Juniper Networks Inc.

-

VMware Inc.

-

Huawei Technologies Co. Ltd.

-

Extreme Networks Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Deutsche Telekom and NVIDIA to build an industrial AI cloud with 10,000 GPUs, operational 2026.

- June 2025: Cisco launched C9000 Smart Switch family featuring AI-native telemetry and quantum-ready security.

- May 2025: HPE added CX 10040 distributed-services switches integrating AMD Pensando DPUs.

- March 2025: Arista released EOS Smart AI Suite and CloudVision Universal Network Observability.

Germany Data Center Networking Market Report Scope

Data center networking refers to the set of technologies, protocols, and hardware used to connect physical and network-based devices and manage the network infrastructure, storage, and processing of application and data. Data center networking is very critical for 100% uptime of data centers. In the current web-connected world, business workloads are executed on single computers, hence leading to the need for data center networking. Networks provide servers, clients, applications, and middleware with a standard plan to stage the execution of workloads and also to manage access to the data produced.

The Germany data center networking market is segmented by component (by product [ethernet switches, router, storage area network (SAN), application delivery controller (ADC), other networking equipment], by services [installation & integration, training & consulting, support & maintenance]), by end-user (IT & telecommunication, BFSI, government, media & entertainment, other end-users). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Products | Ethernet Switches |

| Routers | |

| Storage Area Network (SAN) | |

| Application Delivery Controllers (ADC) | |

| Network Security Appliances | |

| Software-Defined Networking (SDN) Controllers | |

| Optical Interconnects | |

| Services | Installation and Integration |

| Training and Consulting | |

| Support and Maintenance | |

| Managed Network Services |

| IT and Telecommunications |

| Banking, Financial Services and Insurance (BFSI) |

| Government and Defense |

| Media and Entertainment |

| Healthcare and Life Sciences |

| Manufacturing and Industrial |

| Other End-Users |

| Colocation |

| Hyperscalers/Cloud Service Providers |

| Edge/Micro Data Centers |

| Less than 10 GbE |

| 25-40 GbE |

| 50-100 GbE |

| Greater Than 100 GbE |

| By Component | Products | Ethernet Switches |

| Routers | ||

| Storage Area Network (SAN) | ||

| Application Delivery Controllers (ADC) | ||

| Network Security Appliances | ||

| Software-Defined Networking (SDN) Controllers | ||

| Optical Interconnects | ||

| Services | Installation and Integration | |

| Training and Consulting | ||

| Support and Maintenance | ||

| Managed Network Services | ||

| By End-User | IT and Telecommunications | |

| Banking, Financial Services and Insurance (BFSI) | ||

| Government and Defense | ||

| Media and Entertainment | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial | ||

| Other End-Users | ||

| By Data-Center Type | Colocation | |

| Hyperscalers/Cloud Service Providers | ||

| Edge/Micro Data Centers | ||

| By Bandwidth | Less than 10 GbE | |

| 25-40 GbE | ||

| 50-100 GbE | ||

| Greater Than 100 GbE | ||

Key Questions Answered in the Report

What is the size of the Germany data center networking market in 2026?

The market stands at USD 1.11 billion in 2026.

What compound annual growth rate (CAGR) is forecast for the market through 2031?

A 5.32% CAGR is projected between 2026 and 2031.

Which bandwidth segment is expanding the fastest?

Ports above 100 GbE, driven by 400G and 800G adoption, are growing at a 7.05% CAGR.

Why are hyperscale providers channeling large investments into Frankfurt?

Frankfurt hosts DE-CIX’s 25 Tbps traffic peak and offers dense fiber interconnects, making it ideal for AI-ready, high-bandwidth cloud regions.

Page last updated on: