Germany Data Center Processor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

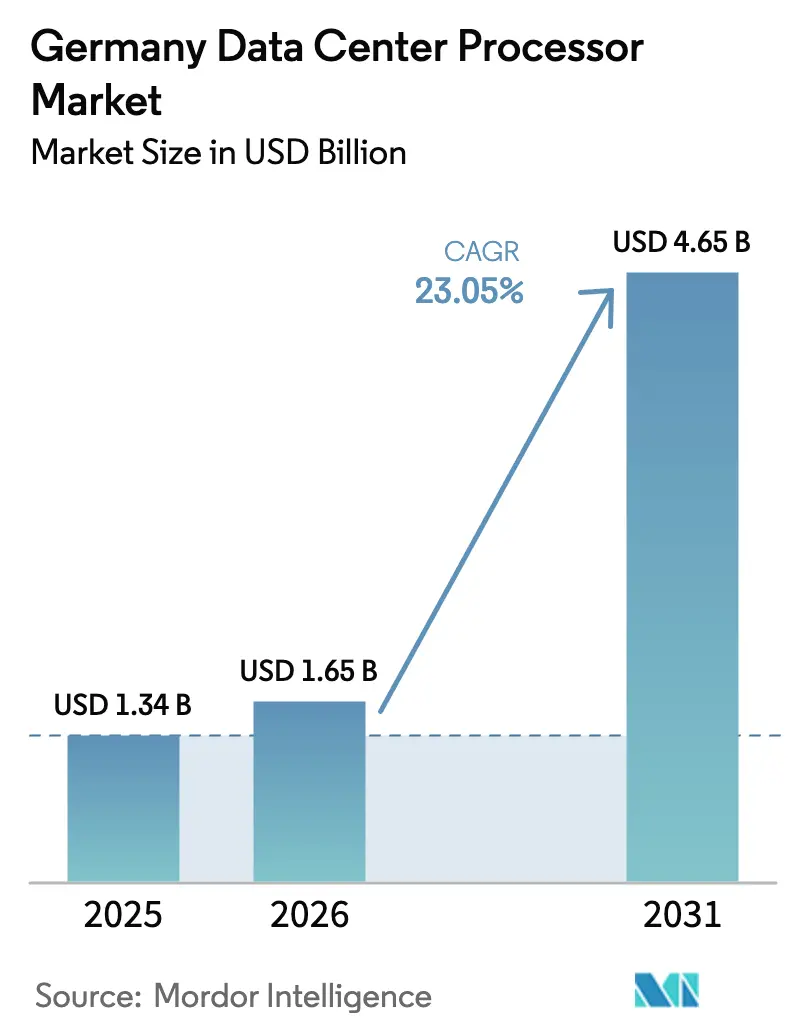

| Base Year Market Size (2025) | USD 1.34 Billion |

| Market Size (2026) | USD 1.65 Billion |

| Market Size (2031) | USD 4.65 Billion |

| Growth Rate (2026 - 2031) | 23.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Data Center Processor Market Analysis by Mordor Intelligence

The Germany data center processors market size is expected to grow from USD 1.34 billion in 2025 to USD 1.65 billion in 2026 and is forecast to reach USD 4.65 billion by 2031 at 23.05% CAGR over 2026-2031. Rapid cloud build-outs, sovereign computing mandates and fast-rising AI workloads in automotive and manufacturing keep demand expanding at a pace unmatched elsewhere in continental Europe. Hyperscale operators view Germany as the gateway to European digital sovereignty, so they deploy heterogeneous CPU-GPU-FPGA nodes that satisfy both GAIA-X and GDPR requirements. Renewable-energy availability keeps facility power usage effectiveness (PUE) low, which supports the rollout of dense racks filled with high-performance processors. At the same time, domestic fabrication projects by Intel and the TSMC-Bosch-Infineon-NXP consortium promise to shorten supply chains and reduce import risks. Electricity-price swings and an engineering talent gap remain near-term constraints, yet mandatory waste-heat reuse rules are spurring innovation in cooling and energy-efficient chip design.

Key Report Takeaways

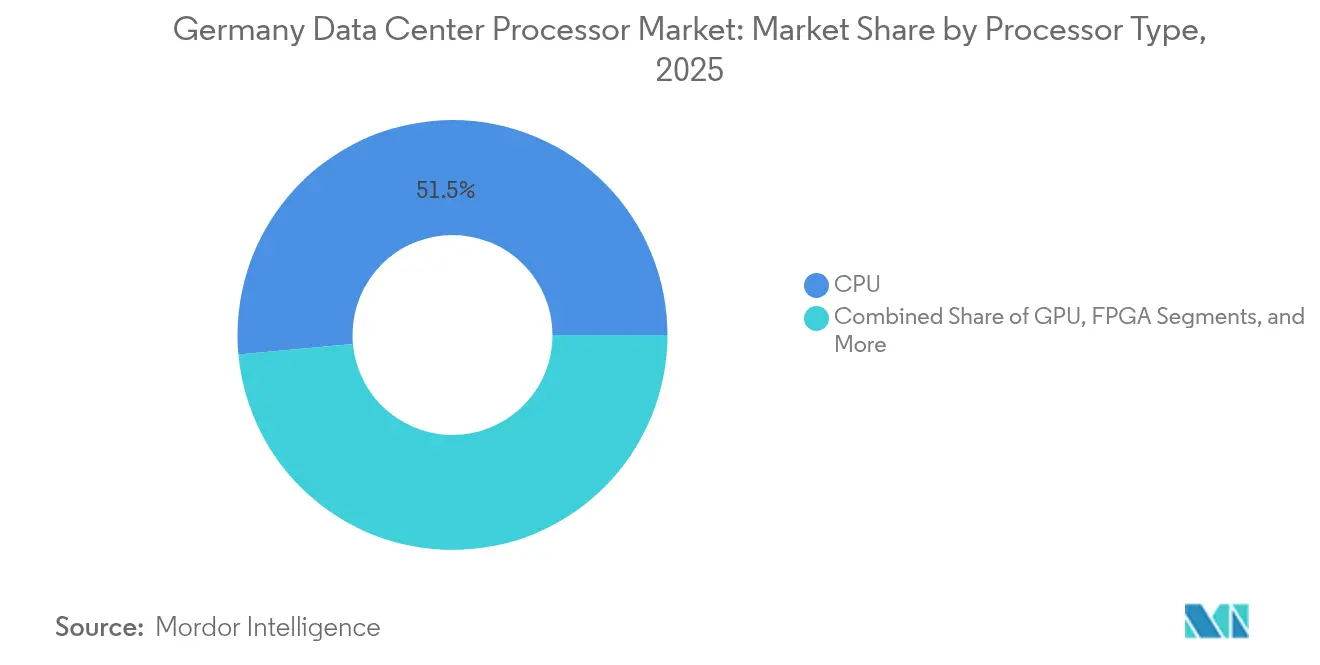

- By processor type, CPUs led with 51.45% of Germany data center processors market share in 2025, while AI Accelerators are expanding at a 25.61% CAGR through 2031.

- By application, AI/ML Training and Inference held 32.60% revenue share in 2025; Advanced Data Analytics is projected to advance at a 24.4% CAGR to 2031.

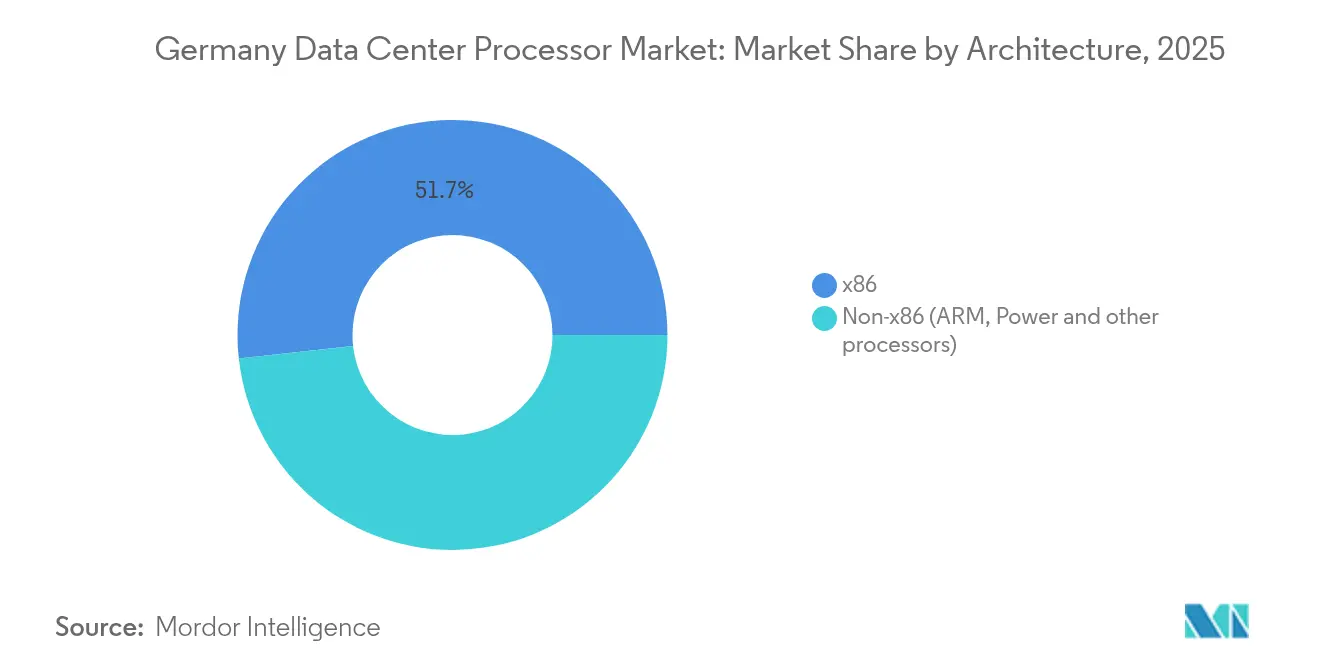

- By architecture, x86 maintained 51.75% share in 2025, whereas non-x86 solutions, helped by ARM-based designs, are growing at a 24.05% CAGR.

- By data center type, Cloud Service Providers accounted for 48.70% of the Germany data center processors market size in 2025 and are expected to post a 26.2% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Figures recorded within Germany feed into a worldwide estimate while studying the global industry. Mordor Intelligence's data center processor market size captures this aggregation.

Germany Data Center Processor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Germany's drive for digital transformation fuels hyperscale build-outs | +3.8% | National, with concentration in Frankfurt/Rhein-Main region | Medium term (2-4 years) |

| Accelerated AI/ML adoption in automotive and Industry 4.0 | +4.2% | National, with emphasis on Bavaria, Baden-Württemberg, North Rhine-Westphalia | Short term (≤ 2 years) |

| EU GDPR-driven data-sovereignty demand for domestic compute | +2.9% | National, with spillover effects to broader EU market | Long term (≥ 4 years) |

| Abundant renewable energy enabling sustainable facilities | +1.7% | National, with advantages in northern regions | Medium term (2-4 years) |

| Emergence of quantum-ready hybrid nodes spurring heterogeneous CPU-GPU-FPGA installs | +2.1% | National, with focus on research centers in Munich, Jülich, Dresden | Long term (≥ 4 years) |

| GAIA-X compliance favoring European-sourced/non-x86 processors | +1.9% | National, with broader European implications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Germany’s Drive for Digital Transformation Fuels Hyperscale Build-Outs

Germany's data center processors market gains strong momentum from the federal AI funding increase and landmark private projects such as Microsoft’s EUR 3.2 billion expansion of local AI infrastructure.[1]Microsoft Corporation, “Microsoft invests €3.2 billion to expand AI infrastructure in Germany”, microsoft.com Large cloud clusters concentrated around Frankfurt achieve rack densities that exceed traditional enterprise norms, leading operators to favor AMD EPYC-based servers that condense three racks of legacy nodes into one. Vantage Data Centers’ EUR 1.4 billion regional investment further confirms Germany’s hyperscale status vantage-dc.com. These facilities demand ever-higher core counts and memory bandwidth, reinforcing the shift toward heterogeneous architectures optimised for AI training. The pull from hyperscale players therefore keeps processor volumes on an upward trajectory even as unit efficiency improves.

Accelerated AI/ML Adoption in Automotive and Industry 4.0

The automotive sector deploys predictive-maintenance and digital-twin models that require constant inferencing across factory sites. BMW’s roll-out prevents hundreds of minutes of downtime annually and underpins steady consumption of AI accelerators.[2] Volkswagen’s Industrial Cloud links 124 plants and 1,500 suppliers, lifting processor demand beyond the design phase into day-to-day analytics. NVIDIA’s 10,000-GPU industrial AI cloud located in Germany underscores the scale of compute now dedicated to manufacturing optimisation nvidia.com.[2]NVIDIA Corporation, “NVIDIA and Deutsche Telekom unveil industrial AI cloud with 10,000 GPUs”, nvidia.com As plant managers adopt edge-AI gateways for real-time quality checks, shipments of specialised processors keep rising faster than those of general-purpose CPUs. Energy-efficient designs also help factories reach sustainability targets, creating an additional purchase criterion.

EU GDPR-Driven Data-Sovereignty Demand for Domestic Compute

Strict data-protection rules lead enterprises to localise sensitive workloads, favouring processors that come with confidential-computing features and European supply chains. The Schwarz Group’s sovereign productivity-suite deal with Google illustrates how hardware choices align with encryption demands and EU-resident data storage. SiPearl’s ARM-based Rhea chip will power the JUPITER exascale supercomputer at Jülich and is optimised for sovereign deployments.[3]SiPearl, “Rhea processor selected for JUPITER exascale supercomputer”, sipearl.com GAIA-X participation by more than 300 organisations reinforces market preference for processors developed or at least fabricated in Europe. As a result, non-x86 options gain credibility in high-performance missions once dominated by US vendors.

Abundant Renewable Energy Enabling Sustainable Facilities

Germany ranks among the top European producers of wind and solar power, allowing large data centers to reach aggressive PUE targets. Google’s local sites already run on renewable electricity, achieving significant waste diversion and enabling higher-density GPU clusters. EcoDataCenter’s partnership with CoreWeave to deploy NVIDIA DGX SuperPods at 1.22 PUE shows how green power supports very high-TDP accelerators. New regulations require 10% heat-reuse by 2026 and 20% by 2028, so operators prefer processors with granular power-management functions that ease integration with liquid-cooling systems. Vendors demonstrating real-world energy savings therefore gain a procurement edge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising electricity costs | -2.4% | National, with particular impact on energy-intensive regions | Short term (≤ 2 years) |

| Global semiconductor supply-chain disruptions | -1.8% | National, with dependencies on Asian manufacturing | Medium term (2-4 years) |

| Mandatory waste-heat reuse limits high-TDP processor design | -1.2% | National, with stricter enforcement in urban areas | Medium term (2-4 years) |

| Talent shortage in advanced chip design inside Germany | -1.6% | National, with concentration in technology clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Electricity Costs

Industrial power prices doubled between 2021 and 2023, prompting some silicon producers to idle capacity. Data-center operators respond by selecting CPUs and GPUs with better performance per watt and by co-locating workloads in wind-rich northern regions. ARM-based chips gain traction because they cut electricity bills without sacrificing throughput. Deployment of very high-TDP GPUs is now concentrated in sites that secure long-term renewable contracts or integrate on-site generation, keeping overall expansion in check until energy prices stabilise.

Talent Shortage in Advanced Chip Design Inside Germany

An estimated 62,000 specialist vacancies across semiconductor disciplines curb the pace at which vendors can localise design for Germany-specific use cases.Large fabs under construction in Magdeburg and Dresden will absorb thousands of engineers, tightening availability for smaller firms. Companies therefore rely more on international partnerships, possibly slowing the customisation of processors for emerging quantum and edge workloads. Government programmes that streamline skilled immigration and boost STEM education may ease the gap after 2027, yet near-term hiring challenges remain a growth limiter.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Processor Type: Specialised Accelerators Outpace Legacy CPUs

CPUs still account for a 51.45% Germany data center processors market share in 2025, anchored by consistent demand for general-purpose compute. Yet AI accelerators expand at 25.61% CAGR because factories, research institutes and cloud providers deploy GPUs and ASICs purpose-built for training and inference. Their proliferation lifts the Germany data center processors market size for accelerator-class devices to new highs, matching the nation’s push into software-defined vehicles and smart-factory operations. Intel’s Xeon 6 E-core variants help hyperscalers compress three racks into one, while AMD’s MI350 accelerators quadruple AI compute, illustrating parallel progress in both camps. FPGAs keep a strategic niche in hybrid quantum nodes where algorithm flexibility matters. Emerging RISC-V boards such as Tenstorrent Blackhole™ add architectural diversity, suggesting that the segment’s growth story will continue beyond 2030.

Continued investment by Deutsche Telekom and Microsoft in AI cloud clusters sustains volume for GPUs, confirming that accelerator demand is not a short-lived spike but a structural pivot. New regulations on waste-heat reuse reinforce interest in accelerators with superior energy efficiency because every watt saved eases compliance. The result is a market where general-purpose CPUs evolve toward power-density optimisation, while specialised chips chase raw AI throughput, together expanding the overall Germany data center processors market.

By Application: Analytics Surges Following Early AI/ML Training Wave

AI/ML Training and Inference lead with 32.60% revenue contribution in 2025 because organisations rushed to build large language models and predictive systems. Now, Advanced Data Analytics overtakes on growth pace at 24.4% CAGR, reflecting a shift toward production deployment where continuous data interrogation drives processor cycles. This phase keeps the Germany data center processors market size tied to persistent rather than batch workloads. Automotive OEMs process telemetry to optimise assembly lines and customer services, so processor utilisation transitions from episodic model training to round-the-clock analytics. High-performance computing for climate models and materials science remains steady, while security workloads rise as GDPR pushes confidential-computing adoption.

Hybrid quantum-classical jobs enter the landscape through installations such as IBM Quantum System One, creating fresh demand for processors that integrate tightly with qubit controllers. Network functions virtualisation also gains share as 5G rollouts require edge-ready chips that handle packet processing. These forces together broaden the user base and secure multi-year processor refresh budgets across verticals.

By Architecture: European ARM Designs Erode x86 Dominance

x86 processors hold 51.75% share yet their weight declines as non-x86 solutions grow 24.05% CAGR. Europe-backed projects like SiPearl’s Rhea pump capital into ARM-based HPC devices, giving the Germany data center processors market a sovereign alternative that satisfies GAIA-X goals. Fujitsu’s forthcoming 2 nm MONAKA chip promises strong performance within tight power envelopes, reinforcing ARM’s rise. Intel and AMD counter with dense-core models and massive L3 caches, keeping x86 relevant for legacy workloads and many enterprise stacks. Meanwhile, RISC-V opens an open-source path that entices research labs seeking maximal customisation and licensing flexibility.

ARM’s strong showing at the edge further accelerates its share gains because power budgets in distributed sites are less forgiving. European fabs coming online after 2027 should boost the regional supply of 3 nm and below non-x86 chips, giving users another reason to widen architectural portfolios. The competition keeps innovation lively and benefits buyers through faster performance gains per watt

By Data Center Type: Cloud Providers Dominate Spend and Growth

Cloud Service Providers control 48.70% of the Germany data center processors market size in 2025 and deliver a 26.2% CAGR to 2031 because hyperscale expansions and sovereign cloud services overlap. Deutsche Telekom’s industrial AI cloud with 10,000 GPUs demonstrates how service providers are the largest single buyers of advanced processors. Enterprise operators continue to refresh fleets but generally pursue hybrid strategies that shift spiky workloads into the cloud. Colocation firms capture new demand from mid-size companies that need proximity to hyperscale regions yet wish to keep certain data on German soil. GAIA-X compliance drives these customers toward facilities that can guarantee data residency, which in turn influences processor purchasing standards around security features.

Edge locations appear as a cross-cutting category because both telcos and industry participants deploy micro-data centers near end points. These distributed nodes need chips optimised for constrained power and sometimes harsh environments. Vendors that blend cloud-grade performance with edge-ready thermals find fertile ground, indicating that all data-center types share in the long-term expansion of the Germany data center processors market.

Geography Analysis

The Frankfurt/Rhein-Main corridor remains the epicentre of German compute with the largest cluster of hyperscale campuses and Europe’s busiest internet exchange. Processor demand there surpasses any other European metro, and capacity is projected to exceed 4,800 MW by 2030, sustaining a wide pipeline for multicore CPUs and AI accelerators. To the south, Bavaria and Baden-Württemberg harness automotive and industrial AI, pushing vendors to position technical support teams near Munich and Stuttgart. Northern states leverage abundant wind output to host energy-intensive GPU farms, providing an economic edge when electricity prices spike elsewhere.

Eastern Germany is fast becoming a fabrication stronghold. Intel’s EUR 30 billion Magdeburg fabs and the European Semiconductor Manufacturing Company in Dresden give the nation scaled domestic supply of advanced nodes intel.com. These plants reduce shipping risks from Asia, shorten lead times and may encourage more local processor design. Dresden already hosts Infineon’s Smart Power Fab, further anchoring the region. Quantum-computing advances cluster around Jülich and Munich, creating demand peaks for specialist chips that integrate with cryogenic control hardware. Grid saturation in Frankfurt forces new builds into secondary cities such as Nauen and Leipzig, spreading processor uptake more evenly across the country.

Renewable-energy mandates differ by locale, so data-center operators in coastal areas tie power purchases to offshore wind, while those inland depend on solar-plus-storage arrangements. Facilities near district-heating networks reuse waste heat to satisfy new regulations, influencing processor cooling choices. The government’s balanced-development plan encourages edge-compute nodes in rural zones, broadening geographic demand. Overall, regional diversity helps stabilise shipment volumes for the Germany data center processors market even when one area faces grid constraints or construction delays.

Mordor Intelligence evaluates the data center processor market across all key regional markets, including Asia, with deeper country-level insights covering Spain, Netherlands, South Korea, Indonesia, India, Chile, Brazil, and Saudi Arabia.

Competitive Landscape

Market concentration stays moderate as global heavyweights meet motivated European entrants. Intel secures the broadest footprint thanks to its mature x86 ecosystem and forthcoming Magdeburg manufacturing, ensuring deep ties with cloud and enterprise buyers intel.com. AMD rides EPYC performance advantages plus MI350 accelerators to win deals with hyperscalers and HPC centres. NVIDIA dominates AI training through its CUDA stack and newly launched industrial cloud in partnership with Deutsche Telekom.

SiPearl leads the sovereignty movement with ARM-based Rhea chips and EUR 90 million Series A funding, gaining preferred status in GAIA-X projects. IQM Quantum Computers opens Germany’s first dedicated quantum data centre, positioning it at the nexus of hybrid workloads. Infineon, Bosch, NXP and TSMC converge in Dresden to fabricate advanced nodes locally, ensuring that at least part of future supply comes from within national borders. Intellectual-property filings cluster around confidential-computing and energy-efficient liquid-cooling integration, signalling where the next competitive breakouts may occur. Overall, buyer power remains high because multiple credible suppliers vie for share, while regulatory emphasis on sovereignty keeps market doors open for regional innovators.

Germany Data Center Processor Industry Leaders

Intel Corporation

Advanced Micro Devices Inc.

Arm Limited

NVIDIA Corporation

Marvell Technology, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: NVIDIA opened the world’s first industrial AI cloud in Germany with 10,000 DGX B200 GPUs to modernise European manufacturing undefined

- Jun 2025: AMD debuted Instinct MI350 accelerators delivering 4x AI compute and announced 5th Gen EPYC processors for rack-scale AI infrastructure

- May 2025: AMD agreed to a USD 10 billion collaboration with HUMAIN to deploy 500 MW of AI compute capacity by 2026

- May 2025: Infineon secured EUR 1 billion government funding toward its EUR 5 billion Smart Power Fab in Dresden set for 2026 production

- March 2025: IQM Quantum Computers inaugurated a quantum data center to accelerate industrial applications

- February 2025: Microsoft committed EUR 3.2 billion to double AI infrastructure and upskill workers in Germany.

Germany Data Center Processor Market Report Scope

- Data centers house and manage critical applications and data, using computing and storage networks for efficient delivery. Processors—GPUs, CPUs, and TPUs—are central to their operation. GPUs handle multitasking, excelling in graphics rendering and AI tasks. CPUs, with multi-core architecture, support parallel processing. TPUs, designed for machine learning, stand out from GPUs, which have transitioned from graphics to AI applications.

- Germany Data Center Processor Market is Segmented by Processor Type (CPU, GPU, FPGA, AI Accelerators), by Application (Advanced Data Analytics, AI/ML Training and Inferences, High Performance Computing, Security and Encryption, Network Functions, and Others), by Architecture (x86 and Non-x86 (ARM, Power and other processors), and by Data Center Type (Enterprise, Colocation and Cloud Service Providers). The Report Offers the Market Size and Forecasts for all the Above Segments in Terms of Value (USD).

| GPU |

| CPU |

| FPGA |

| AI Accelerator |

| Advanced Data Analytics |

| AI/ML Training and Inferences |

| High Performance Computing |

| Security and Encryption |

| Network Functions |

| Others |

| x86 |

| Non-x86 (ARM, Power and other processors) |

| Enterprise |

| Colocation |

| Cloud Service Providers |

| By Processor Type | GPU |

| CPU | |

| FPGA | |

| AI Accelerator | |

| By Application | Advanced Data Analytics |

| AI/ML Training and Inferences | |

| High Performance Computing | |

| Security and Encryption | |

| Network Functions | |

| Others | |

| By Architecture | x86 |

| Non-x86 (ARM, Power and other processors) | |

| By Data Center Type | Enterprise |

| Colocation | |

| Cloud Service Providers |

Key Questions Answered in the Report

What is the value of the Germany data center processors market today and how large will it be by 2031?

The market stands at USD 1.65 billion in 2026 and is forecast to rise to USD 4.65 billion by 2031 on a 23.05% CAGR.

Which processor type shows the fastest growth through 2031?

AI Accelerators lead all categories with a 25.61% CAGR, reflecting soaring demand for training and inference in automotive and manufacturing workloads.

Why do Cloud Service Providers dominate both share and growth?

Hyperscale build-outs and sovereign-cloud offerings put Cloud Service Providers at 48.70% share in 2025 and a 26.2% CAGR, making them the chief buyers of high-performance CPUs, GPUs and FPGAs.

How does Germany’s renewable-energy mix affect processor purchases?

Data-center operators pair low-carbon power with processors that deliver high performance per watt, ensuring compliance with energy-efficiency and waste-heat reuse rules while keeping operating costs in check.

What are the main obstacles to market expansion?

Elevated electricity prices and a shortage of 62,000 semiconductor specialists restrict near-term capacity growth, and strict heat-reuse mandates limit deployment of the highest-TDP chips.

When will major domestic fabs begin supplying advanced nodes?

Intel’s Magdeburg complex and the European Semiconductor Manufacturing Company in Dresden are slated to start production in 2027, giving Germany a local source of leading-edge processors.

Page last updated on: