Germany Data Center Rack Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

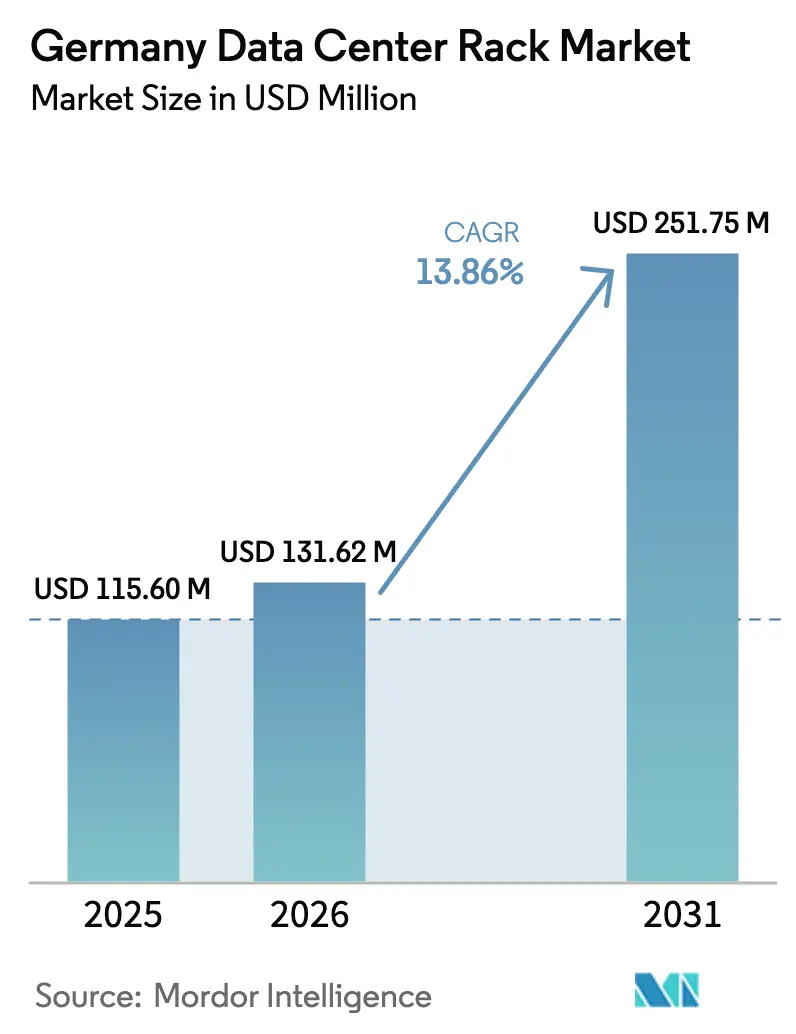

| Base Year Market Size (2025) | USD 115.6 Million |

| Market Size (2026) | USD 131.62 Million |

| Market Size (2031) | USD 251.75 Million |

| Growth Rate (2026 - 2031) | 13.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Data Center Rack Market Analysis by Mordor Intelligence

Germany data center rack market size in 2026 is estimated at USD 131.62 million, growing from 2025 value of USD 115.6 million with 2031 projections showing USD 251.75 million, growing at 13.86% CAGR over 2026-2031. Sustained capital expenditure by hyperscale cloud operators in Frankfurt, the national roll-out of 5G edge nodes by telecom firms, and the federal GAIA-X data-sovereignty agenda underpin this vigorous trajectory. Liquid-cooling-ready cabinets are moving from proof of concept to mainstream as artificial intelligence (AI) servers double average rack power densities, while the Energy Efficiency Act (EnEfG) steers buyers toward integrated cooling and monitoring solutions that can help future sites reach a 1.2 PUE target. Cabinet-type enclosures hold a structural advantage because German insurers, financial regulators, and GDPR auditors all demand high levels of physical security, driving continuous refresh cycles. Finally, brownfield conversions of idle industrial buildings into micro facilities are spreading demand toward secondary locations and opening fresh revenue streams for German rack suppliers that can offer modular, pre-certified solutions.

Key Report Takeaways

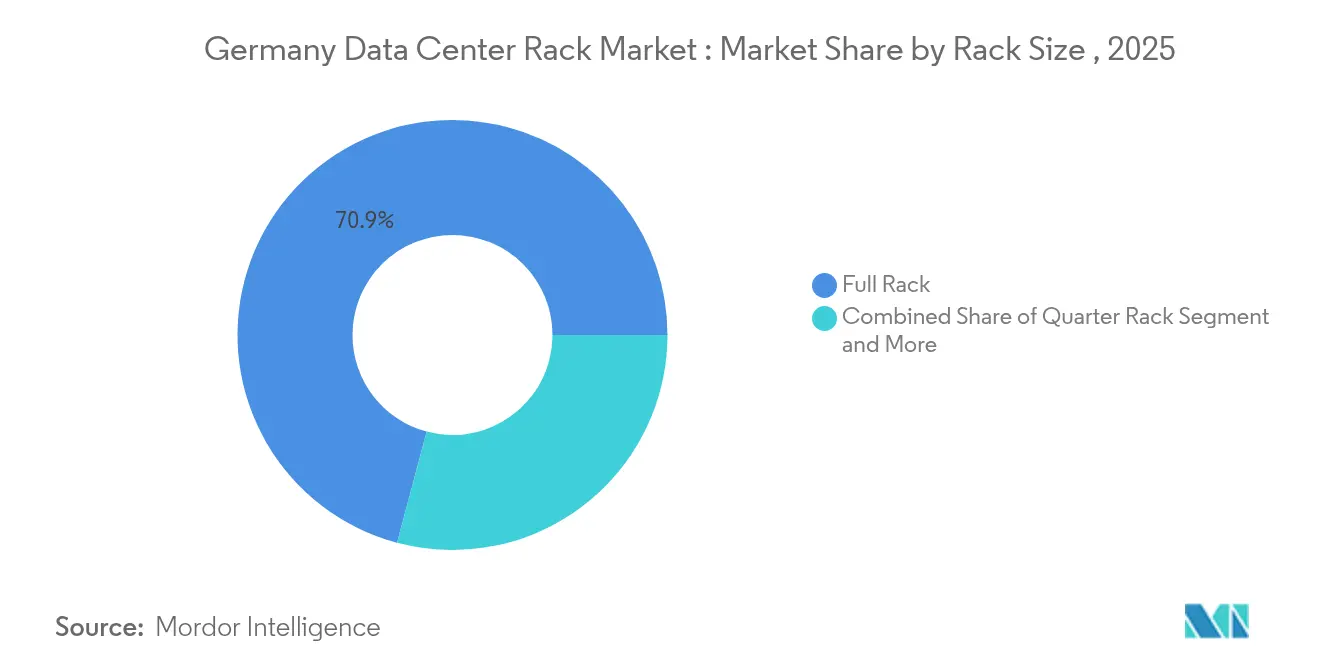

- By rack size: Full racks led with 70.85% of Germany data center rack market share in 2025, while the same category expands at 15.91% CAGR through 2031.

- By rack height: 42U racks held 55.12% share of the Germany data center rack market size in 2025; 48U racks post the fastest 17.08% CAGR to 2031.

- By rack type: Cabinet (closed) solutions captured 74.68% revenue share in 2025 and progress at 15.64% CAGR through 2031.

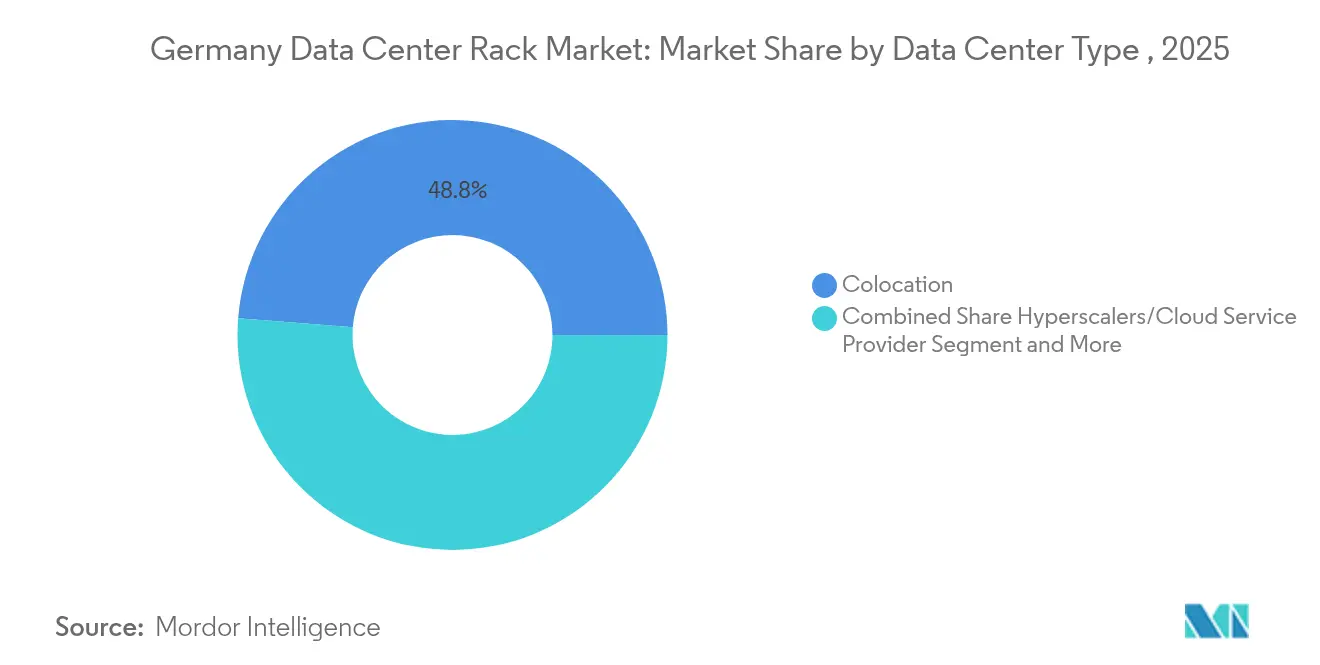

- By data center type: Colocation facilities represented 48.75% of the Germany data center rack market size in 2025, whereas hyperscale and cloud sites record the highest 18.12% CAGR to 2031.

- By material: Steel frames retained 81.47% share in 2025; aluminum racks advance at 16.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Projections can easily extend beyond country and regional trends as they are defined by movement across the full international system. Mordor Intelligence's worldwide data center rack market outlook captures this forward trajectory.

Germany Data Center Rack Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging hyperscale cloud investments in Frankfurt region | +3.2% | Frankfurt metropolitan area, spillover to Rhine-Main | Medium term (2-4 years) |

| Rapid growth in edge computing deployments by telecom operators | +2.8% | National, early gains in Berlin, Munich, Hamburg | Short term (≤2 years) |

| Government support for digitalization (GAIA-X initiative) | +2.1% | National, concentrated in major urban centers | Long term (≥4 years) |

| Adoption of high-density servers and liquid cooling drives rack refresh cycles | +3.5% | Frankfurt, Berlin, secondary markets | Medium term (2-4 years) |

| Demand for seismic-rated racks to meet German insurance standards | +1.2% | National, industrial zones | Long term (≥4 years) |

| Retrofit of brownfield industrial sites into micro data centers | +1.0% | Regional, former industrial areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Hyperscale Cloud Investments in Frankfurt Region

Frankfurt’s role as Europe’s main interconnection hub fuels an aggressive build-out that commits more than EUR24 billion in capacity between 2024 and 2029. [1]German Datacenter Association, “Market Study 2024,” germandatacenterassociation.orgMicrosoft has pledged EUR3.2 billion and Amazon Web Services EUR16.6 billion to enlarge regional footprints, pulling the Germany data center rack market toward taller 48U cabinets that can host AI GPU sleds. Digital Realty’s FRA18 site, installed inside a listed building, shows how land scarcity pushes innovative layouts that still require full-depth, liquid-ready racks datacenterknowledge.com. Seismic-rated frames also see greater adoption because German insurers link lower premiums to robust cabinet construction. Overall, hyperscale capex concentrates demand, shortens replacement cycles, and locks in volume contracts that favor suppliers with local assembly plants and fast lead times.

Rapid Growth in Edge Computing Deployments by Telecom Operators

Telecom carriers introduce distributed mini-hubs to support 5G network slicing and low-latency industrial IoT, which broadens the geographic spread of the Germany data center rack market. Deutsche Telekom’s involvement in the EU-funded AI Gigafactory positions dozens of micro installations across manufacturing corridors, creating steady orders for quarter- and half-racks that can be installed by a two-person crew. Cisco’s reference design for telco edge nodes calls for unified, remotely managed, standards-based cabinets that simplify unmanned site operations. Edge nodes stimulate incremental demand because every 5G region needs its own micro-facility, yet operators insist on TÜV-certified frames that meet German safety codes, allowing local vendors such as Rittal to capitalize on proximity and fast service response.

Government Support for Digitalization (GAIA-X Initiative)

GAIA-X strengthens the national requirement for sovereign data processing and accelerates workload migration from non-European clouds to domestic infrastructure. More than 300 stakeholder firms, among them Deutsche Telekom, shape a reference architecture that standardizes compliance, security, and interoperability. Because GAIA-X prescribes where data can reside, customers prefer in-country, colocation suites and request racks with built-in access logs and environmental sensors that satisfy GDPR audits. The policy outlook ensures consistent demand for compliant cabinets and gives German manufacturers an edge over offshore rivals that lack local certification credentials.

Adoption of High-Density Servers and Liquid Cooling Drives Rack Refresh Cycles

AI training clusters now exceed 30 kW per rack in Frankfurt’s latest halls, double the 2017 average, forcing a transition toward rear-door heat exchangers, direct-to-chip cold plates, and immersion options. Rittal’s 400 kW prototype, unveiled at the 2024 OCP Global Summit, demonstrates how the supply chain redesigns frameworks to host manifolds, pumps, and quick-disconnect fittings. Liquid-ready products command premium prices yet also shorten deployment because the cooling lines arrive pre-integrated. Operators appreciate the operational resilience and the ability to comply with the EnEfG 1.2 PUE mandate from July 2026, thereby ensuring a sustained refresh opportunity for the Germany data center rack market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating land and power costs in major colo clusters | -2.8% | Frankfurt, Berlin | Short term (≤2 years) |

| Data security breaches and compliance cost escalation | -1.5% | National, financial hubs | Medium term (2-4 years) |

| Lengthy permitting under Federal Immission Control Act | -2.1% | National, urban areas | Medium term (2-4 years) |

| Shortage of TÜV-certified installers for advanced containment | -1.3% | National, secondary markets | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Lengthy Permitting Under Federal Immission Control Act

Projects that install more than 2 MW of diesel backup must obtain a Federal Immission Control Act license, lengthening timelines by 12-18 months because of public consultations and environmental reviews. Each new requirement—waste-heat capture plans, energy-management audits, biodiversity reports—adds engineering scope, which then delays the rack procurement stage. International entrants without established local partners struggle to navigate separate city and state approval layers, occasionally abandoning purchase intentions or shifting capacity to the Netherlands. For the Germany data center rack market, the biggest impact is a stop-start order pattern that complicates factory planning and inventory management for domestic suppliers.

Escalating Land and Power Costs in Major Colo Clusters

Construction prices averaged USD9.1 million per megawatt in Frankfurt during 2024, up 6.5% year-on-year, eroding headroom for equipment budgets and slowing purchase orders for new cabinets.

[2]Savills, “Frankfurt Data Center Construction Cost Tracker 2024,” savills.de Grid bottlenecks mean certain projects wait up to two years for transformer slots, pushing operators to enter capacity-swap deals and secondary locations. Rising electricity tariffs, along with the 100% renewable energy requirement by 2027, oblige operators to co-invest in solar and battery assets, leaving fewer funds for discretionary rack upgrades. Smaller colocation firms that compete on price have postponed non-critical refresh programs, translating into a near-term drag on Germany data center rack market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rack Size: Full Racks Dominate Enterprise Deployments

Full racks held 70.85% of Germany data center rack market share in 2025, progressing at a 15.91% CAGR through 2031 as hyperscale halls standardize on 42U and taller footprints for GPU clusters. This dominance reflects economies of scale, uniform cable management layouts, and easier hot-aisle containment integration. Quarter racks and half racks serve niche edge locations or retrofitted office basements where depth or ceiling limits prevail, but their combined revenue remains below one-third of the Germany data center rack market size. The preference for full racks also aligns with the EnEfG waste-heat clause, because contiguous rows improve airflow modeling and enable rear-door exchanger retrofits that capture thermal output for district heating loops. As more AI inference nodes migrate to factories and logistics warehouses, compact variants will grow, yet standardized full racks should retain the top position given hyperscalers’ sizeable forward purchase contracts.

German engineering groups have responded by developing prefabricated modules where full racks leave the factory pre-wired, reducing site work from weeks to days. Siemens and Cadolto promote an ISO-container design that includes twelve 42U enclosures, in-line cooling, and a dedicated battery pod, lowering total installed cost for multiregional edge fleets. Local fabricators also secure a logistics edge; proximity to Frankfurt permits next-day delivery of spare parts, which remains a critical factor for colocation tenants bound by stringent service-level agreements. As Germany data center rack market demand broadens to secondary cities, flexible service coverage and rapid replacement options will strengthen full-rack adoption further.

By Rack Height: 48U Configurations Lead Innovation

42U frameworks, the global benchmark, retained 55.12% share of the Germany data center rack market size in 2025. Operators nonetheless upgrade to taller 48U units to squeeze additional servers into unchanged footprints, achieving up to 14% space savings on a per-rack basis. This trend produces the segment’s highest 17.08% CAGR through 2031. Taller layouts offer the headroom to mount liquid distribution manifolds above the server area, which keeps servicing clear of live power rails. They also allow operators to install two cable trays—one for fiber, one for power—improving fault isolation.

A smaller yet visible share of buyers select 45U or 52U custom heights for research labs and automotive test cells that host experimental compute clusters. Rittal’s 400 kW specimen, effectively a custom 52U chassis with reinforced uprights, demonstrates how design boundaries are being pushed to accommodate AI accelerators that draw more than 130 kW per cabinet. Ceiling clearance in urban Frankfurt remains the practical governor; most new builds retain a 3.6 m raised-floor height, which imposes a physical cap on rack height. Consequently, the Germany data center rack market will continue to record a migration from 42U toward 48U without fully displacing the legacy form factor.

By Rack Type: Cabinet Solutions Ensure Security Compliance

Cabinet enclosures secured 74.68% share in 2025 and keep a 15.64% CAGR outlook, driven by data-sovereignty guidelines, insurer requirements, and the practical need to segregate colocation tenants. Cabinet models arrive with lockable front and rear doors, adjustable side panels, and integrated access logs that interface with building management systems, all of which streamline ISO27001 audits. Open-frame racks cater mainly to hyperscale interiors where each hall is already a restricted zone, but their open sides complicate hot-aisle containment retrofits, delaying the move to liquid cooling.

Wall-mount and micro variants serve small telecom huts and campus facilities where floor space is scarce. German operators value TÜV certification, so suppliers must provide documentation on load ratings, corrosion resistance, and seismic scores. Cabinet solutions therefore remain the default across financial services, public sector hosting, and cloud regions that require per-tenant security fencing. As liquid cooling adoption accelerates, cabinet doors with 70% perforation or rear-door heat exchangers will reinforce the cabinet model’s continued primacy within the Germany data center rack market.

By Data Center Type: Hyperscalers Drive Infrastructure Transformation

Colocation providers accounted for 48.75% of the Germany data center rack market share in 2025 as landlords spread fixed infrastructure costs over multiple tenants. Nevertheless, hyperscale and cloud sites post the highest 18.12% CAGR because AI investments require enormous power densities that in-house data centers cannot accommodate. Cloud builders negotiate multi-year volume agreements that bundle racks, power rails, and hot-aisle containment into a single invoice, therefore exerting price pressure yet offering predictable revenue flow to suppliers.

Enterprises are right-sizing on-premise footprints and moving non-core loads to hosted clouds, which releases capital but also shifts procurement timing. Edge deployments rise within manufacturing and automotive verticals where latency targets fall below 10 milliseconds. Every automated factory or smart logistics hub thus orders between two and eight cabinets, providing a different sales rhythm—small batches on fast turnaround. Overall, the Germany data center rack market size tilts toward hyperscale buyers, yet growth potential remains diversified across the deployment continuum.

By Material: Steel Dominance Faces Aluminum Challenge

Steel frames captured 81.47% of revenue in 2025 because they offer robust load capacity, vibration resistance, and cost advantages. The Germany data center rack market gradually adopts aluminum at a 16.98% CAGR through 2031 as operators factor weight restrictions in multi-storey halls and seismic requirements mandated by insurers. Aluminum dissipates heat faster than steel, making it a suitable pick for liquid-cooling backbones, and it eases manual handling during on-site assembly. Vendors combat steel’s weight disadvantage by offering pre-galvanized sheets with thinner gauges while retaining the 1 500 kg load rating typical for Frankfurt hyperscale rooms.

Composite and hybrid alloys remain niche and often appear in research institutes or military sites that demand electromagnetic shielding. Certification efforts add cost, thereby limiting broader uptake. The EnEfG waste-heat rule, however, introduces higher permissible operating temperatures, so materials that maintain structural integrity at 45 °C will gain relevance. Local firms already integrate recycled aluminum in new models, aligning with European Union circular-economy targets and adding an eco-label that resonates with sustainability-driven colocation tenants.

Geography Analysis

Germany hosts 522 operational data centers, making it the second-largest global market behind the United States and the largest national network in Europe. Frankfurt leads with 745 MW of live IT capacity and the DE-CIX internet exchange, concentrating more than one-third of the Germany data center rack market size within a 25 km radius. Land scarcity and grid congestion, however, are redirecting expansion to adjacent Rhine-Main towns, which draw incremental rack demand as hyperscalers adopt a campus model that spans ten or more buildings.

Berlin has transitioned from an emerging node into a strong alternate hub. Google and NTT each secured multi-hectare parcels, and new halls will support over 200 MW of additional load by 2030 cushmanwakefield.com. The capital’s lower land values and access to renewable power attract AI and high-performance computing tenants who prefer the region’s technology talent pool. Munich follows with fresh activity, including Portus and PGIM Real Estate projects that anchor 5.5 MW and 30 MVA phases respectively, broadening the Germany data center rack market toward southern Bavaria. Consistent with EnEfG policy, Munich utilities promote waste-heat capture, spurring rack redesigns that integrate rear-door exchangers compatible with district heating circuits.

Secondary cities such as Hamburg, Düsseldorf, and Stuttgart escalate appeal because local governments offer streamlined permits and renewable energy credits. Edge deployments further diffused demand to industrial towns where automotive factories and chemical plants require sub-10 ms latency links to cloud workloads. Brownfield conversions of disused steel mills and paper plants in the Ruhr Valley demonstrate that rack suppliers able to furnish modular, corrosion-resistant enclosures can secure high-margin projects. Consequently, while Frankfurt remains the focal point, a distributed build-out narrative now shapes the geography of the Germany data center rack market and reinforces the need for a national service footprint.

The data center rack market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Europe, Africa, and Middle East. This is complemented by country-specific insights for Russia, Spain, Nigeria, Saudi Arabia, Thailand, and South Korea, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The Germany data center rack market displays moderate concentration. Rittal, Schneider Electric, and Eaton combine strong domestic production with global service networks, while Vertiv uses its thermal management leadership to cross-sell integrated racks plus rear-door coolers. Local champions differentiate through compliance documentation, TÜV stamps, and proximity, which cut delivery lead times to less than one week for standard SKUs. Global entrants, including Legrand and Huawei Digital Power, seek footholds through partnerships with German engineering, procurement, and construction contractors who can navigate municipal zoning and federal emission laws.

Technological differentiation tilts toward platform bundles. Schneider Electric’s EcoStruxure IT Gateway update in 2025 added multivendor device mapping, meeting a market request for unified monitoring across mixed asset fleets. Siemens advanced a turnkey concept with Cadolto and Legrand that pairs prefabricated rooms with factory-installed 42U racks, thus trimming on-site fit-out by 40% and responding to tight edge deployment schedules. Northern Data Group signals a new buyer persona: AI-focused infrastructure operators that demand 48U liquid-ready frames, high copper weight load ratings, and extensive sensor arrays for machine-learning power optimization.

Mergers and long-term supply agreements intensify competition. Rittal signed a five-year framework with two hyperscale landlords that locks a baseline of 100 000 cabinets across European sites. Vertiv countered by aligning with a German colocation provider to integrate its CoolLoop rear-door heat exchangers as a standard option. New entrants chase sustainability differentiation by marketing aluminum frames with a 70% recycled content claim, targeting customers that disclose cradle-to-grave carbon assessments to investors. The evolving competitive chessboard thus combines engineering capability, regulatory fluency, and green credentials as the key winning vectors in the Germany data center rack market.

Germany Data Center Rack Industry Leaders

Eaton Corporation

Rittal GMBH & Co.KG

Schneider Electric SE

Vertiv Holdings Co

nVent Electric plc (incl. Schroff)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Siemens, Cadolto, and Legrand unveiled a modular edge data center with AI-ready compute zones and flexible finance packages at Data Center World Frankfurt

- May 2025: SAP, Deutsche Telekom, Ionos, and Schwarz formed a strategic alliance to explore an AI data center project within Germany

- May 2025: Deutsche Telekom joined a consortium vying for part of the EU’s EUR20 billion AI Gigafactory budget

- April 2025: Digital Realty opened FRA18 inside a historically preserved building, extending capacity within the Frankfurt city limits

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Germany data center rack market as all newly manufactured 19-inch or 23-inch open-frame and enclosed cabinets installed inside colocation, cloud, enterprise, and edge facilities across Germany, together with the associated power distribution rails and blanking panels that ship with the frame. According to Mordor Intelligence analysts, replacement, leased, or refurbished racks, standalone in-row cooling doors, and aftermarket monitoring kits are outside the scope.

Scope Exclusion: Pre-owned or retrofitted cabinets and any third-party integration fees are not counted.

Segmentation Overview

- By Rack Size

- Quarter Rack

- Half Rack

- Full Rack

- By Rack Height

- 42U

- 45U

- 48U

- Other Heights (52U and Custom)

- By Rack Type

- Cabinet (Closed) Racks

- Open-Frame Racks

- Wall-Mount Racks

- By Data Center Type

- Colocation Facilities

- Hyperscale and Cloud Service Provider DCs

- Enterprise and Edge

- By Material

- Steel

- Aluminum

- Other Alloys and Composites

Detailed Research Methodology and Data Validation

Primary Research

Mordor's team interviewed German facility managers, colocation procurement heads in Frankfurt and Berlin, and local integrators that install racks alongside busways. Follow-up calls with thermal consulting engineers and energy auditors validated average rack densities, pricing shifts, and adoption rates of 48U formats, filling gaps discovered in desk work and anchoring sensitive assumptions.

Desk Research

Desk research began with regulatory and statistical material such as the Federal Network Agency's Energy Efficiency Act guidelines, the Federal Statistical Office's machinery production index, and customs records for HS-code 84733020 that track rack and cabinet imports. Industry intelligence from Bitkom, the German Data Center Association, and EN50600 certification databases helped size installed capacity and upcoming projects.

To calibrate value, we reviewed vendor 10-K filings, selected press releases on hyperscale campus build-outs, and leveraged D&B Hoovers plus Dow Jones Factiva for revenue splits of key rack suppliers. Additional cross-checks came from EU-27 steel price indices (rack BOM cost proxy) and patent families in Questel that flag emerging liquid-ready enclosures. The desk sources cited above are illustrative; many others informed data validation, clarification, and context building.

Market-Sizing & Forecasting

Market value is first estimated top-down by reconstructing the national rack demand pool from annual data center floor area additions, average racks per MW, and prevailing ASPs, which are then validated by selective bottom-up supplier revenue roll-ups and channel checks. Key variables like new data center construction permits, rack power density trends, GAIA-X compliant build share, German steel price index, and 5G edge node counts drive the model. A multivariate regression on these inputs forecasts 2026-2030 demand, while scenario analysis adjusts for policy-driven PUE caps. Sampled ASP times volume data help close residual gaps where supplier disclosures are partial.

Data Validation & Update Cycle

Before release, analysts reconcile model outputs with import data, vendor shipment tallies, and energy consumption benchmarks; anomalies trigger re-checks. A peer review and senior sign-off complete the cycle. Reports refresh annually, with interim updates if material events such as a large hyperscale land acquisition shift the base.

Why Mordor's Germany Data Center Rack Baseline Earns Trust

Published estimates diverge because firms choose disparate rack definitions, bundle services differently, or refresh on uneven cadences. By aligning scope strictly to new physical frames and validating each driver with German-specific evidence, Mordor delivers a baseline clients can audit with limited effort.

Key Gap Drivers include: some publishers roll installation and managed service revenue into rack value, others pool Germany within wider DACH figures, and a few extrapolate from global averages without checking local PUE-driven height migration.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 115.6 M (2025) | Mordor Intelligence | - |

| USD 1.86 B (2024) | Global Consultancy A | Bundles installation and services; counts refurbished racks; includes adjacent DACH demand |

| USD 221.1 M (2023) | Industry Journal B | Uses older ASPs; applies European average rack per MW ratio rather than German density |

These comparisons show that Mordor's disciplined scope, Germany-specific variables, and yearly refresh cadence provide the most balanced and reproducible starting point for strategic decisions.

Key Questions Answered in the Report

What is the current size of the Germany data center rack market?

The market generated USD 131.62 million in 2026 and is forecast to reach USD 251.75 million by 2031.

Which rack type leads in Germany

Cabinet (closed) racks command 74.68% revenue share, driven by GDPR security and cooling efficiency requirements.

Why are 48U racks gaining popularity?

48U frames allow operators to host more servers in the same footprint and provide space for liquid-cooling manifolds, supporting a 17.08% CAGR through 2031.

How do energy regulations influence rack design?

The Energy Efficiency Act mandates a 1.2 PUE for new sites from July 2026, prompting buyers to adopt racks with integrated cooling and monitoring.

Page last updated on: