Germany Data Center Storage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.10 Billion |

| Market Size (2026) | USD 2.17 Billion |

| Market Size (2031) | USD 2.53 Billion |

| Growth Rate (2026 - 2031) | 3.18% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Data Center Storage Market Analysis by Mordor Intelligence

Germany data center storage market size in 2026 is estimated at USD 2.17 billion, growing from 2025 value of USD 2.10 billion with 2031 projections showing USD 2.53 billion, growing at 3.18% CAGR over 2026-2031. This steady trajectory reflects a maturing environment in which infrastructure consolidation, energy-efficient operations and regulated data residency take priority over rapid capacity build-outs. Hybrid cloud strategies that let enterprises stage workloads across on-premises, colocation, and sovereign cloud nodes continue to underpin demand for storage technologies that guarantee low latency, encryption at rest, and transparent audit trails. Edge build-outs tied to Industry 4.0, NVMe acceleration for AI inference and the growing use of liquid cooling are reinforcing interest in modular, software-defined platforms that reduce power draw per terabyte. Meanwhile, electricity-price volatility caused by the Energiewende is prompting operators to favor flash arrays and intelligent tiering engines that can spin down idle capacity and shift I/O when spot prices spike, extending hardware life cycles while curbing operating expenses.

Key Report Takeaways

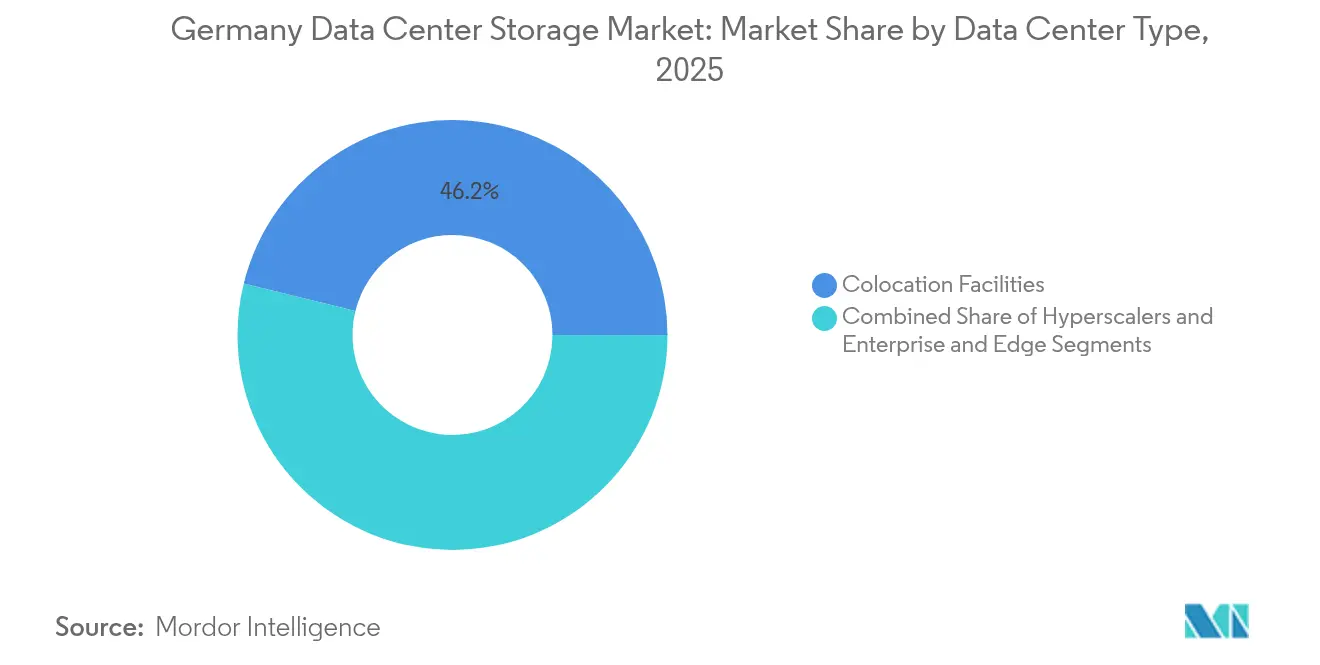

- By data-center type, colocation facilities led with 46.15% of Germany data center storage market share in 2025, whereas hyperscalers are projected to clock the fastest 4.95% CAGR to 2031.

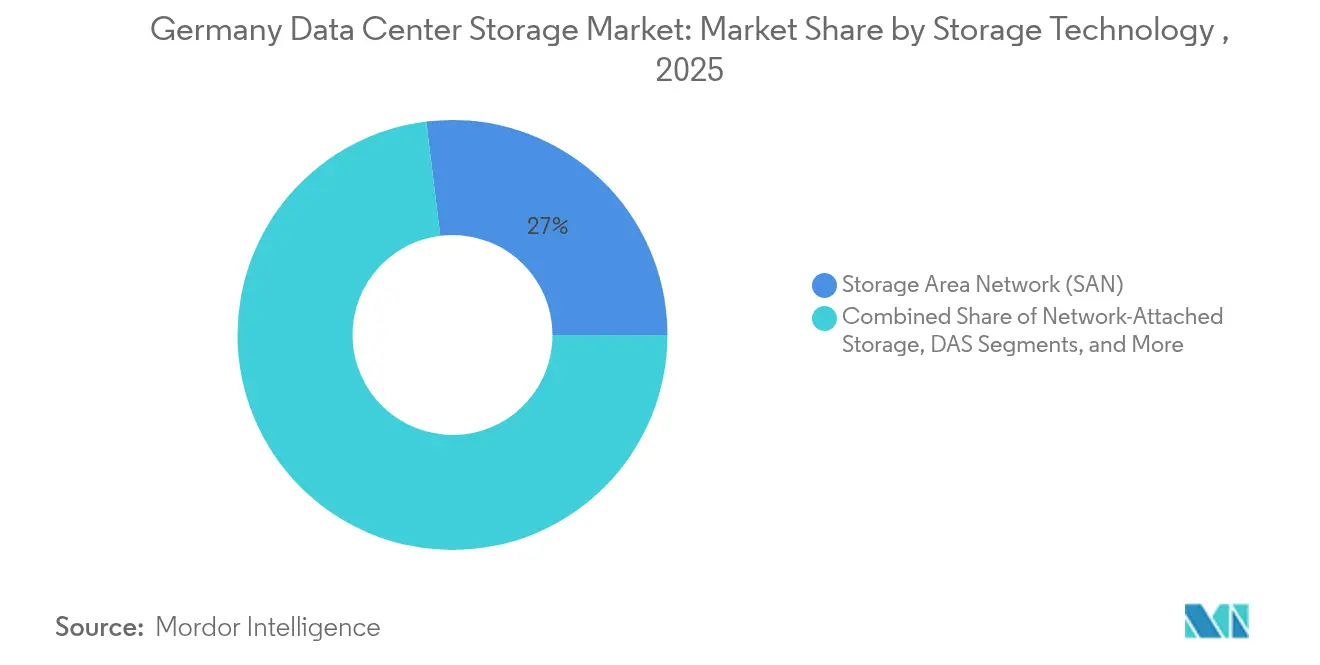

- By storage technology, Storage Area Networks captured 26.95% of revenue in 2025, while Network Attached Storage is advancing at a 3.58% CAGR through 2031.

- By storage type, HDD arrays accounted for 43.05% of the German data center storage market size in 2025; all-flash arrays are set to grow at a 4.12% CAGR during the period.

- By end user, IT & Telecommunications held 27.75% share of the Germany data center storage market size in 2025, but BFSI is expanding at 3.87% CAGR on the back of digitized banking and real-time risk analytics.

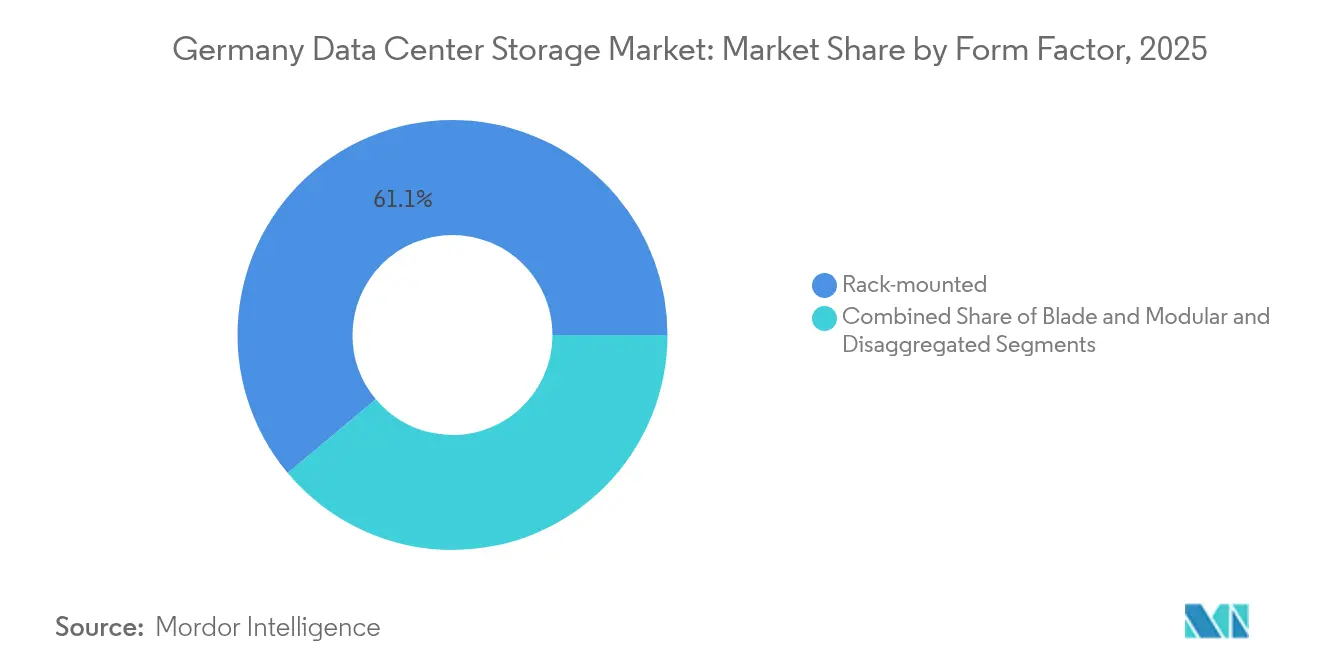

- By Form Factor, Rack-mounted held 61.10% share of the Germany data center storage market size in 2025, but Disaggregated / Composable is expanding at 5.12% CAGR on the back of digitized banking and real-time risk analytics.

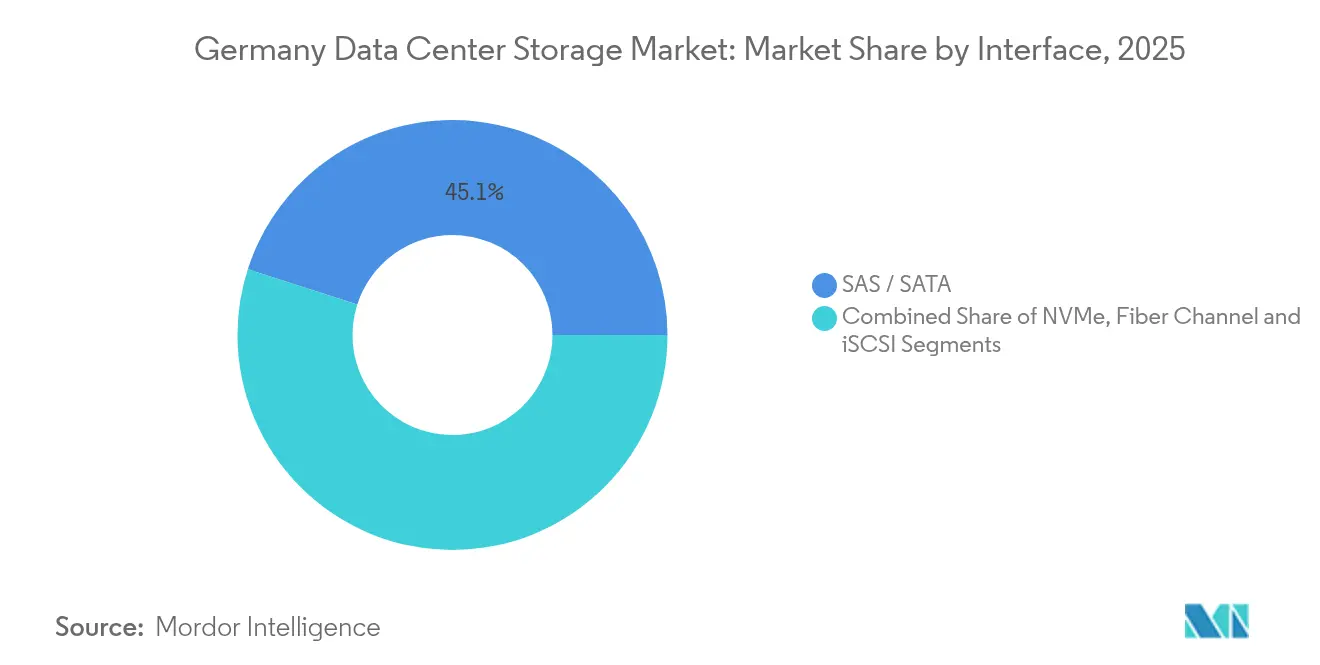

- By Interface, SAS / SATA held 45.05% share of the Germany data center storage market size in 2025, but NVMe is expanding at 5.25% CAGR on the back of digitized banking and real-time risk analytics.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Data Center Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-computing boom among German enterprises | +1.2% | Frankfurt, Munich, Berlin metros | Medium term (2-4 years) |

| Shift to green / energy-efficient data centers | +0.8% | Baden-Württemberg, North Rhine-Westphalia | Long term (≥ 4 years) |

| Accelerated AI and Gen-AI workloads driving flash adoption | +0.6% | Nationwide industrial clusters | Short term (≤ 2 years) |

| Edge-location build-out for Industry 4.0 / 5G | +0.4% | Manufacturing belt | Medium term (2-4 years) |

| Surplus-heat reuse subsidies effective 2025 | +0.3% | Urban district-heating zones | Long term (≥ 4 years) |

| Bundesbank-backed Gaia-X sovereign cloud push | +0.2% | Financial-services nodes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-Computing Boom Among German Enterprises

German firms are migrating workloads to cloud platforms at a controlled pace that preserves on-premises investments while unlocking elastic compute for analytics. A Fraunhofer IESE survey shows systems-engineering complexity scoring 7.6 today and rising to 8.7 within five years, revealing that legacy stacks can no longer cope with real-time integration demands.[1]Fraunhofer IESE, “Systems Engineering Trends 2025–2030,” iese.fraunhofer.de Hybrid storage that bridges data center, colocation and Gaia-X compliant sovereign clouds, therefore finds favor, supporting gradual refactoring without breaching residency rules. Frankfurt, Munich and Berlin remain hubs thanks to latency-sensitive BFSI and SaaS workloads. Federal incentives for digitalization, detailed in the 2024 Haushaltsplan, are further lowering adoption barriers through tax breaks on cloud spending.

Shift to Green / Energy-Efficient Data-Centres

Germany’s carbon-neutrality target for 2045 has moved PUE and recyclability to the top of procurement scorecards. Operators are adopting liquid and immersion cooling to manage thermals in high-density racks where air cooling hits physical limits. AI-driven orchestration platforms, such as Dell Technologies’ Concept Astro, now simulate server and storage loads in a digital twin to modulate fan speeds and CPU states, cutting power draw up to 14% in field tests.[2]C. Jones, “Dell’s Concept Astro Cuts Data-Center Power by 14%,” CIO, cio.com Demand is rising for modular enclosures built from recyclable alloys so components can be swapped without energy-intensive refits.

Accelerated AI / Gen-AI Workloads Driving Flash Adoption

Automotive and manufacturing leaders are embedding vision-based quality control and predictive maintenance algorithms that require millisecond response. Traditional spinning-disk arrays cannot meet those service-level objectives, driving NVMe flash uptake even in capex-constrained environments. Edge micro-data centers in Bavaria and Baden-Württemberg now deploy disaggregated NVMe-over-Fabrics clusters that provide central manageability while hosting inference models locally for privacy compliance. Variable I/O profiles of training versus inference make fine-grained tiering essential to cap energy bills.

Edge-Location Build-Out for Industry 4.0 / 5G

Private 5G networks inside factories are pushing compute and storage closer to robots and machine-vision stations. BSI’s 2025 Open RAN guidelines underscore that local media retention is mandatory when networks degrade, obliging ruggedized NAS or DAS nodes to buffer telemetry until backhaul resumes.[3]Bundesamt für Sicherheit in der Informationstechnik, “Sicherheitsanforderungen 5G Open RAN v2.0,” bsi.bund.deAutomated data-placement tools help cache critical control data at the edge while archiving less-urgent logs in central repositories, balancing cost and resilience.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Up-front capex & stringent data-sovereignty audits | −0.5% | BFSI, public sector | Short term (≤ 2 years) |

| Volatile electricity prices linked to Energiewende | −0.3% | Regions with high renewables | Medium term (2-4 years) |

| Lengthy power-grid connection lead times | −0.4% | Industrial zones | Long term (≥ 4 years) |

| Scarcity of skilled storage engineers (Fachkräftemangel) | −0.2% | Metropolitan clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Up-Front Capex & Stringent Data-Sovereignty Audits

Before procuring new arrays, banks and ministries must complete exhaustive privacy impact assessments that can extend project cycles by six months. The Palantir litigation in Hesse shows how platforms face scrutiny for potential mass-surveillance risk, elevating encryption, key custody and audit log features as must-haves. Custom secure configurations push bill-of-materials costs above standard SKUs, dampening short-term volume.

Volatile Electricity Prices Linked to Energiewende

Wholesale electricity spot rates fluctuated by up to 93 EUR/MWh in 2024, compelling operators to seek arrays that throttle idle power and schedule replication during off-peak windows. HDD-based systems that draw steady wattage regardless of I/O utilization become less attractive than flash that can enter deep sleep states. Procurement teams now model total cost of ownership over 10-year horizons, factoring grid-price hedging and potential carbon taxes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Storage Technology: SAN Leadership Faces NAS Disruption

Storage Area Networks provided the robustness that mission-critical SAP HANA and core-banking workloads demanded, holding 26.95% revenue in 2025. Yet NAS systems, helped by software-defined file services, are projected to record 3.58% CAGR. Adoption is strongest among software-as-a-service vendors that value simplified scale-out and REST-API integration. Direct-attached storage retains a role in line-side robotics cells where deterministic latency trumps shared fabric convenience. Object storage paired with tape remains vital for compliance archives, ensuring immutable copies that satisfy BaFin retention rules.

German operators favor iterative refresh cycles. Fraunhofer IESE notes a sector-wide pivot toward model-driven development that reduces bespoke scripting. Consequently, platform teams gravitate to NAS clusters with familiar NFS and SMB semantics, limiting retraining and freeing scarce storage engineers for optimization work.

By Storage Type: Flash Transition Accelerates Despite HDD Resilience

HDD arrays continued to dominate capacity-oriented tiers, representing 43.05% share in 2025. However, all-flash arrays will expand at 4.12% CAGR as NVMe pricing falls and AI inference gains traction. Hybrid arrays provide a hedge, enabling automatic placement of hot datasets on TLC or QLC NAND and cold files on high-capacity disks, supporting compliance retention yet satisfying performance SLAs. HDD vendors counter with helium-filled 30 TB drives shipping in 2026, delaying full conversion in backup tiers.

By Data Center Type: Colocation Dominance Reflects Sovereignty Priorities

Colocation vendors delivered 46.15% revenue in 2025, supplying sovereign racks and flexible lease tenors. Hyperscalers, after adopting European Processor Initiative chips and opening local regions, will post 4.95% CAGR, driven by analytics sandboxes and disaster-recovery environments. Enterprises keep tier-0 data inside colocation cages to maintain key custody yet burst analytics to the cloud when usage peaks. The Germany data center storage market continues to prize auditability; vendors that expose encryption chipset certificates and support client-supplied HSMs see faster uptake. Edge micro data centers proliferate along autobahn logistics corridors, caching telemetry for last-mile tracking.

By End User: IT Leadership Challenged by BFSI Growth

IT & Telecommunications users maintained 27.75% share in 2025, anchored by SaaS back-ends and streaming platforms. BFSI workloads, spanning real-time risk engines and RegTech analytics, will generate 3.87% CAGR. German banks must store tick-level trade data for ten years, inflating capacity plans. Government digitization, energized by the Onlinezugangsgesetz deadlines, sustains steady demand for compliant systems. Media producers keep editing files on high-throughput NAS, while healthcare accelerates imaging archive migration to hybrid clouds aligned with Gematik guidelines.

By Form Factor: Rack-Mounted Stability Meets Composable Innovation

Rack-mounted enclosures held 61.10% revenue in 2025 due to entrenched data-center designs. Composable infrastructure that pools flash, GPU, and CPU over PCIe-based fabrics is forecast to post a 5.12% CAGR as research labs and semiconductor fabs seek granular scaling. Blade storage sees uptake in space-constrained branch offices. The Germany data center storage industry increasingly values chassis that accept both EDSFF and U.3 flash, future-proofing investments.

By Interface: SAS / SATA Incumbency Faces NVMe Disruption

SAS / SATA remained the default at 45.05% share in 2025. NVMe will attain 5.25% CAGR, driven by microservice architectures that demand sub-100 μs latency. Fibre Channel persists in core banking SANs where dual-path redundancy is entrenched. iSCSI continues to support SMBs transitioning from DAS. NVMe-over-Fabrics pilots in Berlin show 40% CPU utilization drop versus legacy stacks by offloading storage processing.

Geography Analysis

The Frankfurt Rhine-Main cluster dominates capacity demand as Europe’s financial gateway and DE-CIX interconnection hub. Operators there deploy dense all-flash tiers to clear end-of-day settlement batches under BaFin deadlines. Munich’s proximity to automotive OEMs drives edge-ready, low-latency storage to power autonomous-driving simulations. In North Rhine-Westphalia, brownfield steel plants are refitted with Industry 4.0 sensors, spurring rollout of rugged DAS nodes inside milling halls.

Renewables penetration varies: Schleswig-Holstein sources 110% wind power on windy days, letting data-center operators renegotiate green energy PPAs for lower tariffs. Conversely, Bavaria’s grid constraints incentivize on-site solar plus battery storage. Regional regulators interpret GDPR and the new EU Data Act differently; Hesse’s tech-neutral stance benefits multipurpose colocation, whereas Baden-Württemberg imposes stricter audit checkpoints, lengthening go-live lead times. Vendors offering “compliance as code” templates win contracts by speeding state-level certification.

Competitive Landscape

Five global incumbents, Dell Technologies, HPE, NetApp, IBM, and Pure Storage, collectively held major revenue in 2024. They emphasize firmware-upgradable architectures and AI-enabled management rather than disruptive hardware shifts. Dell’s Concept Astro applies reinforcement learning to model thermals and power, cutting array wattage and fan wear. NetApp is integrating BlueXP backup across on-premises and Gaia-X clouds, streamlining compliance evidence packets in audits. HPE’s Alletra platform offers consumption-based pricing that hedges energy-price swings.

Start-ups targeting NVMe disaggregation, such as VAST Data and Fungible, partner with German AI labs seeking exabyte-scale file repositories. Meanwhile, traditional HDD vendors Western Digital and Seagate collaborate with colocation providers to certify helium-filled drives for extended humidity ranges typical in indirect adiabatic cooling halls.

Germany Data Center Storage Industry Leaders

Dell Technologies

Hewlett Packard Enterprise

NetApp

IBM

Huawei Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Dell Technologies introduced Concept Astro, an AI-driven power-optimization suite that melds digital twins with agentic control loops.

- March 2025: The federal government assigned EUR 2.1 billion to digital infrastructure and climate-protection programs in the 2024 budget.

- February 2025: BSI published reinforced 5G Open RAN security guidelines that emphasize certified local storage for edge nodes.

- January 2025: Fraunhofer IESE reported systems-engineering complexity rising from 7.6 to 8.7 by 2030, widening demand for integrable storage.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study counts only revenue generated inside Germany from new, enterprise-class storage subsystems that sit within colocation, hyperscale, enterprise, and edge data centers. Covered technologies span direct-attached, network-attached, object libraries, and SAN arrays; cloud object services are included only when the underlying hardware is physically installed on German soil.

Scope Exclusion: Removable media, battery energy-storage systems, and server boot disks lie outside this scope.

Segmentation Overview

- By Storage Technology

- Network Attached Storage (NAS)

- Storage Area Network (SAN)

- Direct Attached Storage (DAS)

- Object and Tape Storage

- By Storage Type

- Traditional HDD Arrays

- All-Flash Arrays (AFA)

- Hybrid Storage

- By Data Center Type

- Colocation Facilities

- Hyperscalers/Cloud Service Providers

- Enterprise and Edge

- By End User

- IT and Telecommunication

- BFSI

- Government and Public Sector

- Media and Entertainment

- Healthcare and Life Sciences

- Manufacturing

- By Form Factor

- Rack-mounted

- Blade and Modular

- Disaggregated / Composable

- By Interface

- SAS / SATA

- NVMe

- Fibre Channel and iSCSI

Detailed Research Methodology and Data Validation

Primary Research

Analysts speak with procurement heads at colocation firms, cloud architects, OEM channel managers, and IT leads across Bavaria and North-Rhine Westphalia. Their insights on price points, refresh cycles, and NVMe penetration let us reconcile desk findings with market reality.

Desk Research

We compile import codes from the Federal Statistical Office, Bitkom capacity surveys, project filings lodged with BaFin, Eurostat shipment splits, and adoption curves from SNIA. Paid resources such as D&B Hoovers and Dow Jones Factiva help our team trace supplier revenues and construction announcements. The sources named are illustrative; many additional portals and journals feed our library.

Market-Sizing & Forecasting

A top-down build starts with national floor space and rack counts, multiplied by typical terabytes per rack for each facility class. Sampled vendor revenues and channel ASP-unit checks provide bottom-up validation. Core variables include new megawatts commissioned, density progression, flash price curves, replacement intervals, and the share of workloads off-loaded to cloud. Five-year forecasts flow from multivariate regression blended with ARIMA so power-price swings and capex cycles are mirrored. Missing datapoints are imputed from adjacent quarters and re-verified with experts.

Data Validation & Update Cycle

Outputs pass three-stage peer review; anomalies reopen interviews, and models are refreshed annually. Interim updates issue whenever installed capacity deviates by more than five percent.

Why Mordor's Germany Data Center Storage Baseline Earns Trust

Published numbers often diverge because firms bundle wider IT spend, apply varied FX rates, or extrapolate global shares without local build evidence.

Key Gap Drivers: Other publishers fold software fees into hardware totals, assume universal flash adoption, or ignore German customs data that Mordor tracks every quarter.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.10 B (2025) | Mordor Intelligence | - |

| USD 3.20 B (2024) | Regional Consultancy A | Uses supplier revenue, omits end-use adjustment |

| USD 8.10 B (2024) | Trade Journal B | Rolls all data-center hardware, uses static 2023 FX |

Takeaway: By anchoring estimates in verifiable build metrics and cross-checked density assumptions, Mordor Intelligence delivers a balanced, repeatable baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current value of the Germany data center storage market?

The Germany data center storage market size is USD 2.17 billion in 2026

How fast is the market expected to grow?

It is forecast to expand at a 3.18% CAGR, reaching USD 2.53 billion by 2031.

Which data-center type generates the highest storage demand?

Colocation facilities lead with 46.15% of Germany data center storage market share as of 2025 due to data-sovereignty requirements.

Why are all-flash arrays gaining traction?

AI and Gen-AI workloads need sub-millisecond latency, and flash arrays cut power usage compared with HDDs while meeting performance SLAs.

Page last updated on: