France Electronics Manufacturing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

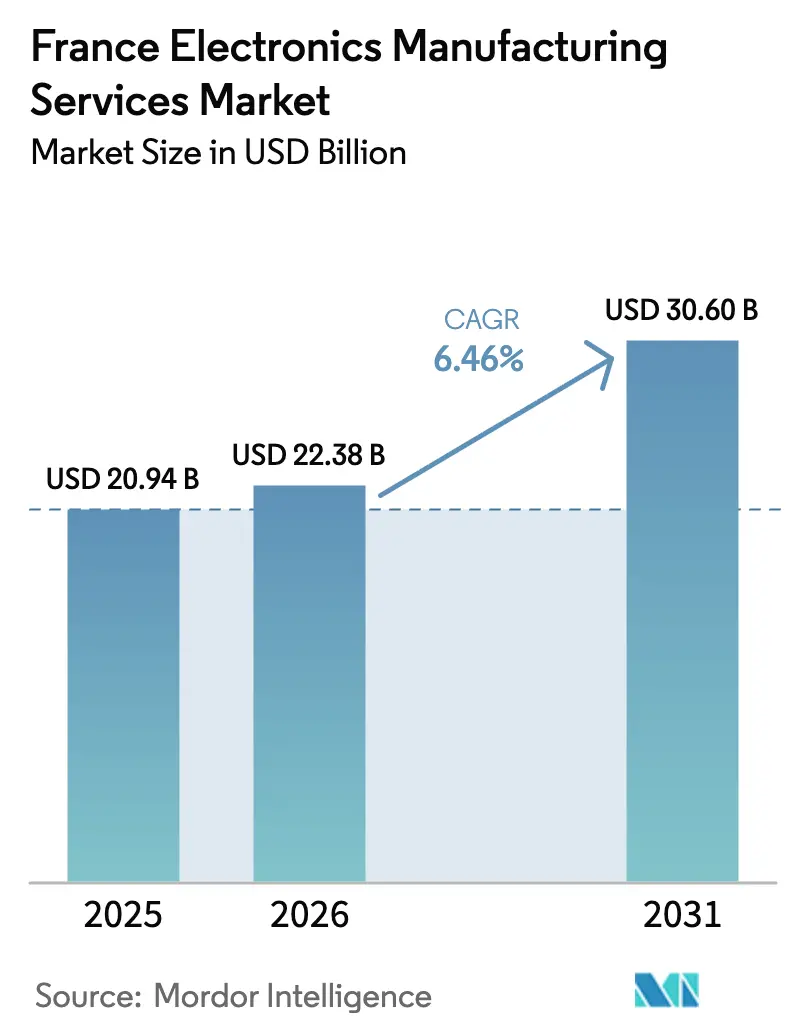

| Base Year Market Size (2025) | USD 20.94 Billion |

| Market Size (2026) | USD 22.38 Billion |

| Market Size (2031) | USD 30.60 Billion |

| Growth Rate (2026 - 2031) | 6.46% CAGR |

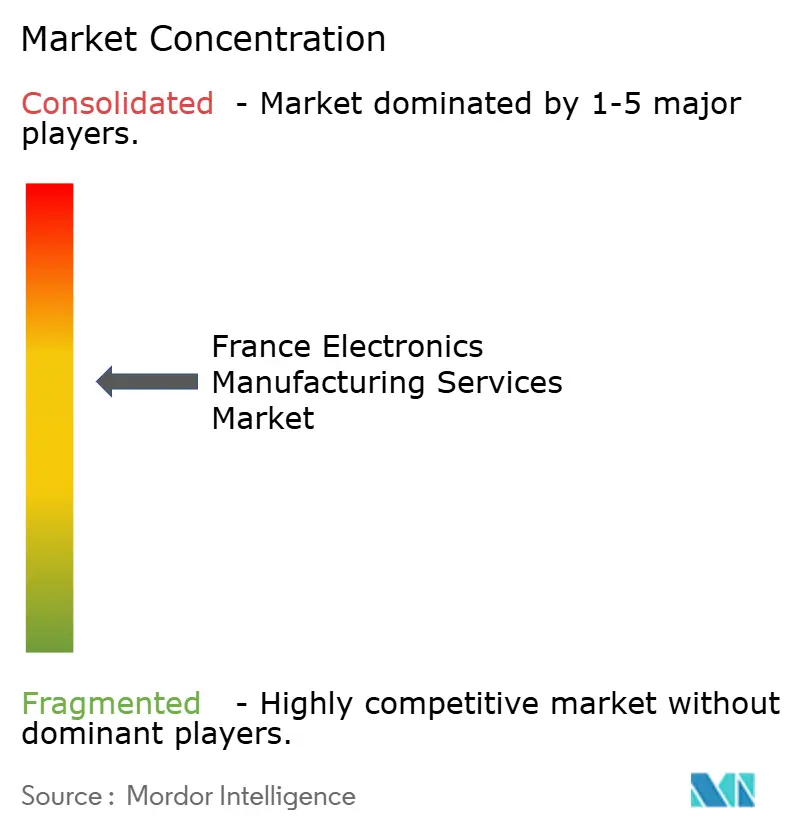

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Electronics Manufacturing Services Market Analysis by Mordor Intelligence

The France Electronics Manufacturing Services Market size was valued at USD 20.94 billion in 2025 and is estimated to grow from USD 22.38 billion in 2026 to reach USD 30.60 billion by 2031, at a CAGR of 6.46% during the forecast period (2026-2031).

Robust public incentives, a shift toward asset-light production models among domestic original equipment manufacturers, and the rise of high-mix low-volume projects are propelling revenue growth. At the same time, upstream semiconductor investments in Crolles and Grenoble are anchoring a local supply chain that shortens lead times and supports advanced packaging needs. Competitive dynamics are moderating cost pressure as French providers accelerate automation and emphasize quick-turn, automotive-grade quality. Finally, labor and energy costs continue to temper margin expansion, making operational efficiency a primary focus for market participants.

Key Report Takeaways

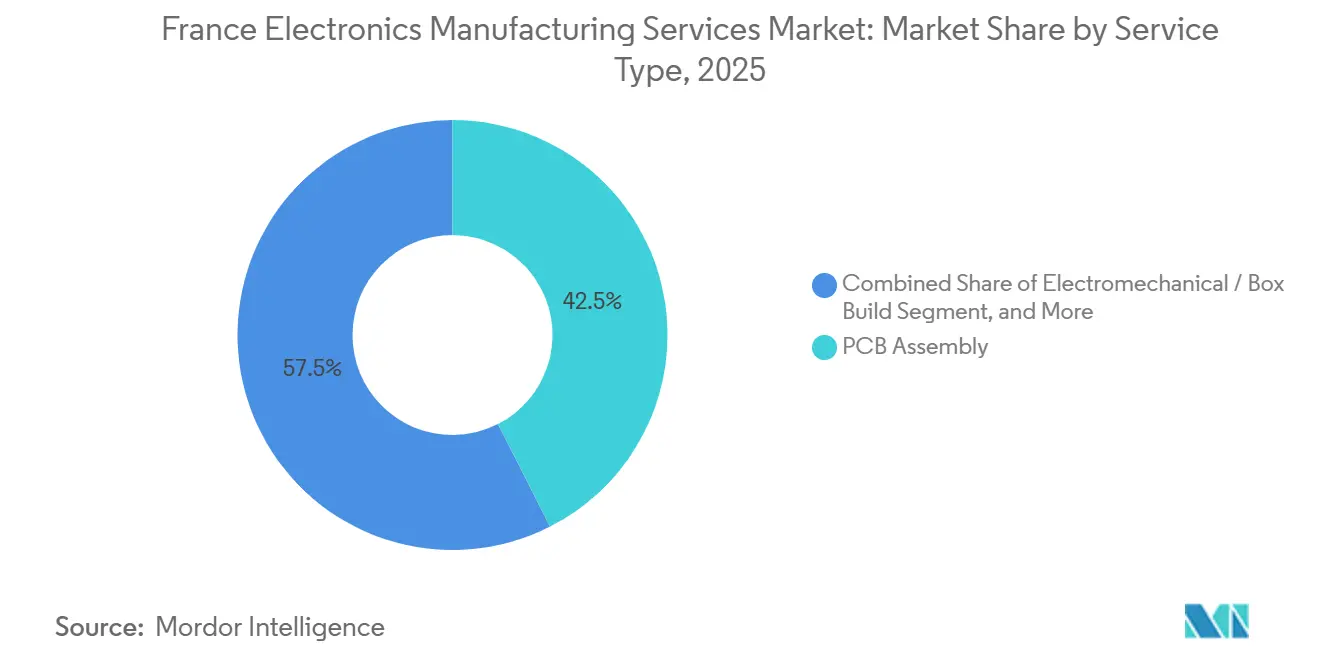

- By service type, Electronic Manufacturing Services commanded 42.50% France electronics manufacturing services market share in 2025, while Engineering Services are set to expand at a 6.80% CAGR through 2031.

- By business model, the Contract Manufacturing segment held 61.90% of the France electronics manufacturing services market size in 2025, yet Hybrid and Turnkey models are forecast to grow at a 4.50% CAGR.

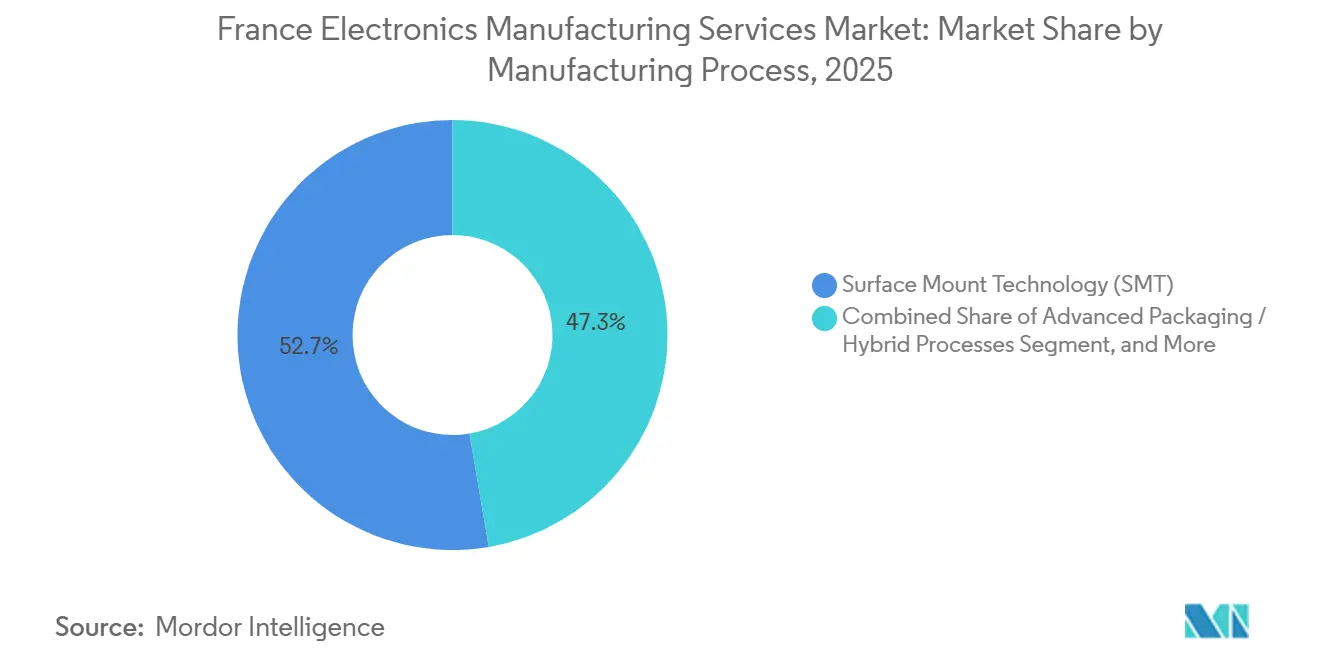

- By manufacturing process, Surface-Mount Technology accounted for 52.70% of value in 2025, whereas Advanced Packaging and Hybrid Processes are projected to advance at a 5.10% CAGR.

- By end-user, Industrial applications controlled 38.60% of 2025 revenue, but Automotive is the fastest-growing segment at a 5.80% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Projections can easily extend beyond country and regional trends as they are defined by movement across the full international system. Mordor Intelligence's worldwide electronics manufacturing services market outlook captures this forward trajectory.

France Electronics Manufacturing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Incentives for On-Shore Electronics Production under France 2030 Plan | +1.8% | National, concentrated in Île-de-France, Auvergne-Rhône-Alpes, Nouvelle-Aquitaine | Medium term (2-4 years) |

| Growing Outsourcing Trend Among French OEMs | +1.2% | National, strongest in Grand Est and Hauts-de-France | Short term (≤ 2 years) |

| Increasing Demand for High-Mix Low-Volume Production in Automotive and Industrial Sectors | +1.0% | National, with spillover to Germany and Spain | Medium term (2-4 years) |

| Rapid Expansion of IoT and Edge AI Devices Requiring Localised Assembly | +0.9% | National, early adoption in smart building and automation | Long term (≥ 4 years) |

| Surge in Niche Medical Device Start-Ups Leveraging Regional EMS Hubs | +0.5% | Occitanie and Nouvelle-Aquitaine | Long term (≥ 4 years) |

| Rise of Semiconductor Substrate Fab Expansions in Crolles | +0.6% | Auvergne-Rhône-Alpes, nationwide effects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Incentives for On-Shore Electronics Production

The EUR 5 billion (USD 5.5 billion) electronics allotment within the France 2030 plan co-funds factory automation, workforce training, and R&D partnerships, contingent on seven-year domestic production commitments[1]“France 2030 Industrial Plan,” Gouvernement.fr, gouvernement.fr. Unlike earlier subsidy rounds that focused only on wafer fabrication, the current framework supports printed-circuit assembly, box build, and functional test activities, creating guaranteed demand for compliant EMS firms. Providers must add roughly 1.6 million square feet of clean-room and assembly floor space by 2027, a build-out that secures multi-year contracts with automotive and industrial OEMs and reinforces national supply-chain resilience.

Growing Outsourcing Trend Among French OEMs

European vehicle and machinery builders now outsource 62% of electronics value-add, up from 48% in 2019, as internal equipment depreciates faster than product cycles. French Tier-1 suppliers are divesting non-core assembly lines to fund software and sensing innovations, releasing high-value contracts to EMS partners. The model allows OEMs to shift inventory risk and leverage EMS automation for cost parity with Asian production while still meeting EU quality and sustainability standards.

Increasing Demand for High-Mix Low-Volume Production

Batch sizes have fallen from 10 000 units to near 500 units, spurred by diverse electric-vehicle variants and customized industrial control boards. Flexible pick-and-place lines with sub-60-minute changeovers enable French EMS plants to process more than 200 bill-of-material permutations weekly while maintaining first-pass yields above 98%. Geographic proximity cuts order-to-delivery times to 48 hours and lets OEMs reduce safety stock by 30%, advantages that high-volume offshore contractors cannot match efficiently[2]“European Automotive Supplier Competitiveness Study,” CLEPA, clepa.eu.

Rapid Expansion of IoT and Edge AI Devices

Edge gateways and sensing nodes require miniature, low-power designs assembled under tight electromagnetic-compatibility limits. Partnerships such as the Lyon hardware lab between Altyor and Advantech speed prototype cycles from 18 months to 9 months[3]“Advantech and Altyor Launch IoT Hardware Lab,” Altyor, altyor.com. EU data-sovereignty rules further encourage on-shore assembly, and advanced processes like micro-bump bonding and underfill dispensing are differentiators for French EMS providers that qualify them.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Semiconductor Component Supply and Pricing | -0.8% | National, acute in automotive and industrial segments | Short term (≤ 2 years) |

| Intense Pricing Pressure from Asian Contract Manufacturers | -0.6% | National, severe in consumer electronics and telecom | Short term (≤ 2 years) |

| Chronic Skilled Labour Shortages in Precision Soldering and Test Engineering | -0.4% | Pays de la Loire and Nouvelle-Aquitaine | Medium term (2-4 years) |

| Escalating Energy Costs for Factory Clean-Rooms and Reflow Ovens | -0.3% | National, higher impact on advanced packaging | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Semiconductor Component Supply and Pricing

Lead times for automotive-grade microcontrollers jumped from 12 to 18 weeks by mid-2025, forcing EMS firms to carry 90 days of buffer stock and exposing them to obsolescence risk. Price swings of up to 40% for key power devices compressed gross margins, and although the EU Chips Act introduced a crisis-response mechanism, meaningful local capacity will not come online until late 2026.

Intense Pricing Pressure from Asian Contract Manufacturers

Foxconn, BYD Electronics, and Luxshare operate at global scale and deliver 25–35% lower unit costs on consumer devices. These firms have begun establishing Central-European sites with ISO 13485 and IATF 16949 certifications, encroaching on French niches. Domestic EMS providers counter with proximity, intellectual-property security, and compliance with EU directives, yet price sensitivity in mass-market segments remains a headwind.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Diversifying Beyond PCB Assembly

Engineering Services work is forecast to grow at a 6.80% CAGR, outstripping the broader France electronics manufacturing services market. The service integrates printed boards with enclosures, cabling, and thermal interfaces, aligning with automotive electrification that triples control-unit counts per vehicle. Electronic Manufacturing Services, while still holding 42.50% of 2025 revenue, is maturing as automation raises yields and lowers labor exposure. Engineering, test, and logistics services are expanding because medical and IoT entrants need design-for-manufacturability reviews and just-in-time inventory programs.

Providers offering turnkey warehousing linked to OEM enterprise systems can automatically replenish parts, cutting customer carrying costs by up to 30%. Circular-economy regulations are also opening demand for repair and refurbishment, positioning after-sales services as a steady margin contributor. The evolution broadens the France electronics manufacturing services market size and cushions price pressure on commoditized assembly lines.

By Business Model: Turnkey Gains Traction Among New Entrants

Contract Manufacturing maintained 61.90% share of the France EMS market in 2025, reflecting its importance for automotive and industrial customers that keep design ownership. Hybrid and Turnkey models are climbing at a 4.50% CAGR as startups seek partners to navigate sourcing constraints and regulatory paperwork. LACROIX Electronics grew turnkey revenue from 22% to 31% within a year by taking over procurement during the chip shortage.

Turnkey engagement compresses development timelines by up to 25% but trades off price transparency, prompting many OEMs to establish open-book audits. Original Design Manufacturing remains niche, limited mainly to standardized power supplies and sensors where differentiation is low. Each model enriches the France EMS market by aligning cost, risk, and speed preferences across diverse customer profiles.

By Manufacturing Process: Advanced Packaging Meets Miniaturization

Surface-Mount Technology dominated with 52.70% share, yet advanced packaging and hybrid flows are moving ahead at a 5.10% CAGR as wearable and edge-AI products shrink form factors. STMicroelectronics and GlobalFoundries are scaling a EUR 7.5 billion (USD 8.25 billion) fully-depleted silicon-on-insulator fab in Crolles, catalyzing local demand for die attach and wafer-level fan-out services. French EMS firms near the cluster can now offer one-stop post-fab processing, trimming logistics time and enhancing yield.

Through-hole technology still serves aerospace and nuclear projects where long life and field repair trump size constraints. Hybrid lines that merge automated placement with manual insertion allow compliance with both modern density needs and legacy reliability targets. This versatility shields the France EMS market from overreliance on any single process technology.

By End-User: Automotive Leads Growth Curve

Industrial equipment generated 38.60% of 2025 revenue, but automotive is accelerating the fastest at 5.80% CAGR. Battery-electric vehicles require roughly 75 electronic control units versus 25 in combustion models, lifting board counts and test hours. French automakers and Tier-1 suppliers localize production to meet zero-defect targets and reduce geopolitical risk.

Communication equipment and mobile devices lag due to price wars and deferred 5G spending, segments where Asian producers dominate. Medical electronics, fueled by ISO 13485-certified regional hubs, offers a steady pipeline of low-volume, high-margin assemblies that further diversifies the France EMS market.

Geography Analysis

Île-de-France hosts corporate headquarters and prototype labs yet faces real-estate and labor constraints that push volume work to regions with lower costs. Auvergne-Rhône-Alpes benefits from the Crolles semiconductor cluster and collaboration with CEA-Leti, creating a tight ecosystem for advanced packaging. Grand Est and Hauts-de-France support just-in-time deliveries to cross-border automotive supply chains, leveraging proximity to German OEMs.

Nouvelle-Aquitaine fosters a growing medical-device corridor around Biarritz and Bordeaux, where ISO 13485-qualified EMS firms partner with implantable-sensor start-ups. Pays de la Loire experiences skilled labor shortages, raising hourly technician wages above EUR 25 and eroding competitiveness.

Occitanie, centered on Toulouse, is emerging as a secondary aerospace electronics hub tied to Airbus programs. Planned capacity additions under France 2030 will likely favor regions with available industrial land and vocational training pipelines, rebalancing the France electronics manufacturing services market across the country.

The electronics manufacturing services market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Europe, Asia, and North America. This is complemented by country-specific insights for United Kingdom, Germany, India, United States, Thailand, and Singapore, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The top five providers control roughly 35–40% of national revenue, placing the France electronics manufacturing services market in a moderately concentrated band. Cofidur’s purchase of SEICO added three plants and 400 staff, signaling a push for scale to win component allocations during supply crunches. éolane has deployed machine-vision inspection and cobots, cutting labor per assembly by 18% and boosting yields.

Global Tier-1 players such as Jabil and Flex maintain satellite French sites mainly for engineering services, while Nordic firms like Kitron link French capacity into pan-European production networks.

Automation, vertical integration, and digital twins are the main strategic levers. Providers able to integrate design, procurement, and after-sales support under one roof are securing long-term contracts especially in the automotive and edge-AI spaces. Increasingly, competitive differentiation centers on speed, regulatory compliance, and the ability to absorb supply-chain shocks rather than on pure labor arbitrage.

France Electronics Manufacturing Services Industry Leaders

Asteelflash Group

LACROIX Electronics

ALL CIRCUITS SAS

éolane Group

Cofidur EMS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: STMicroelectronics reached first-silicon at its Crolles 300-mm fab, targeting 18 nm automotive microcontrollers, with volume output slated for H2 2026.

- November 2025: Jabil reported 22% year-over-year growth in European automotive electronics and plans an additional 150 000 sq ft of clean-room space in Central Europe by mid-2026.

- September 2025: Flex partnered with a French Tier-1 supplier to co-develop modular 800-V traction-inverter platforms, with pilot runs scheduled for Q1 2026.

- July 2025: The French government signed the Strategic Electronics Contract, releasing EUR 5 billion in co-financing and targeting a 90% capacity boost by 2027.

France Electronics Manufacturing Services Market Report Scope

The France Electronics Manufacturing Services Market Report is Segmented by Service Type (Engineering Services, and More), Business Model (Contract Manufacturing (CM), Original Design Manufacturing (ODM), and More), Manufacturing Process (Surface Mount Technology (SMT), Through-Hole Technology (THT), and More), End-User (Industrial, Automotive, Communication, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | |

| Prototyping | |

| Other Electronic Manufacturing Services | |

| Engineering Services | |

| Test and Development Implementation | |

| Logistics Services | |

| Other EMS Type |

| Contract Manufacturing (CM) |

| Original Design Manufacturing (ODM) |

| Hybrid / Turnkey / Other Business Models |

| Surface Mount Technology (SMT) |

| Through-Hole Technology (THT) |

| Advanced Packaging / Hybrid Processes |

| Mobile Devices (Smartphones and Tablets) |

| Consumer Electronics |

| Computer (PCs/Desktop/Laptops) |

| Industrial |

| Automotive |

| Communication |

| Lighting |

| Medical |

| Other End-users |

| By Services Type | Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | ||

| Prototyping | ||

| Other Electronic Manufacturing Services | ||

| Engineering Services | ||

| Test and Development Implementation | ||

| Logistics Services | ||

| Other EMS Type | ||

| By Business Model | Contract Manufacturing (CM) | |

| Original Design Manufacturing (ODM) | ||

| Hybrid / Turnkey / Other Business Models | ||

| By Manufacturing Process | Surface Mount Technology (SMT) | |

| Through-Hole Technology (THT) | ||

| Advanced Packaging / Hybrid Processes | ||

| By End-user | Mobile Devices (Smartphones and Tablets) | |

| Consumer Electronics | ||

| Computer (PCs/Desktop/Laptops) | ||

| Industrial | ||

| Automotive | ||

| Communication | ||

| Lighting | ||

| Medical | ||

| Other End-users |

Key Questions Answered in the Report

How large is the France electronics manufacturing services market in 2026?

The market is valued at USD 22.38 billion in 2026 and is projected to reach USD 30.60 billion by 2031.

Why are turnkey models gaining popularity?

Turnkey contracts shift sourcing risk to EMS partners and can shorten product development cycles by up to 25%.

Which end-user segment drives future growth?

Automotive electronics leads with a 5.80% CAGR because electric vehicles require three times more control units than combustion models.

What regional factors influence capacity expansion?

Auvergne-Rhône-Alpes benefits from semiconductor investments, while Pays de la Loire faces skilled labor shortages that inflate costs.

Page last updated on: