Thailand Electronics Manufacturing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

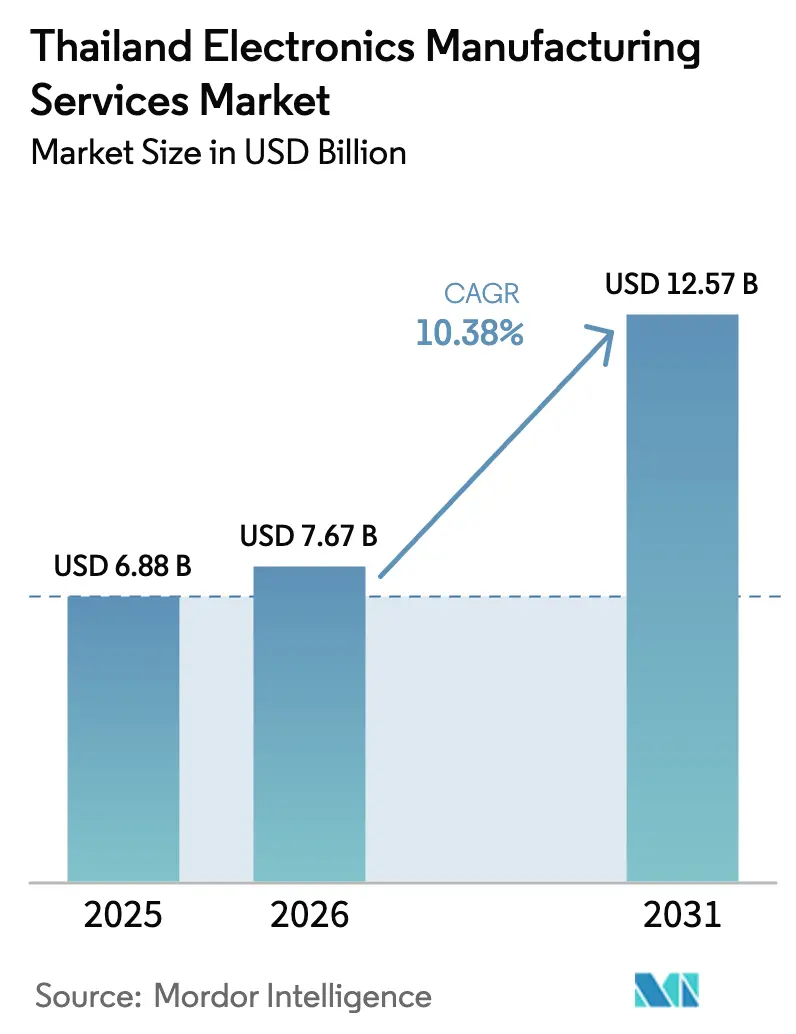

| Base Year Market Size (2025) | USD 6.88 Billion |

| Market Size (2026) | USD 7.67 Billion |

| Market Size (2031) | USD 12.57 Billion |

| Growth Rate (2026 - 2031) | 10.38% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Electronics Manufacturing Services Market Analysis by Mordor Intelligence

Thailand Electronics Manufacturing Services Market size in 2026 is estimated at USD 7.67 billion, growing from 2025 value of USD 6.88 billion with projections showing USD 12.57 billion, growing at 10.38% CAGR over 2026-2031. Accelerated investment in electric-vehicle electronics, 5G module assembly, and medical devices is steering the Thailand electronics manufacturing services market toward higher-margin activities. Continuous inflows of foreign and domestic capital, preferential tax holidays, and proximity to established automotive and medical supply chains sustain momentum despite regional labor and energy-cost pressures. Intensifying relocation of orders from mainland China, coupled with tight global component supply, is prompting customers to favor providers that combine sophisticated process capabilities with agile sourcing. Competition remains fragmented but technologically uneven, allowing firms with advanced packaging, system-in-package, and co-packaged optics expertise to secure long-term programs.

Key Report Takeaways

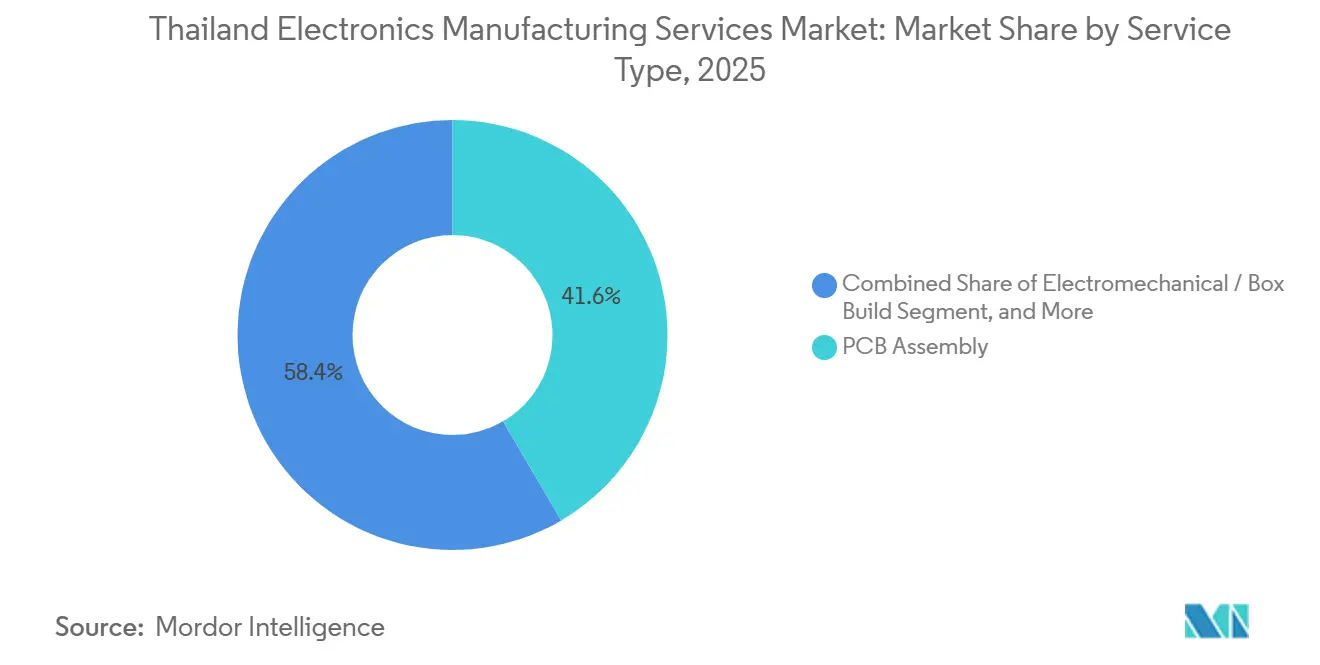

- By service type, printed circuit board assembly led with 41.57% of the Thailand electronics manufacturing services market share in 2025; electromechanical and box-build services are forecast to expand at an 11.41% CAGR to 2031.

- By business model, contract manufacturing accounted for 63.48% of the Thailand electronics manufacturing services market size in 2025, while hybrid and turnkey structures are advancing at a 10.93% CAGR through 2031.

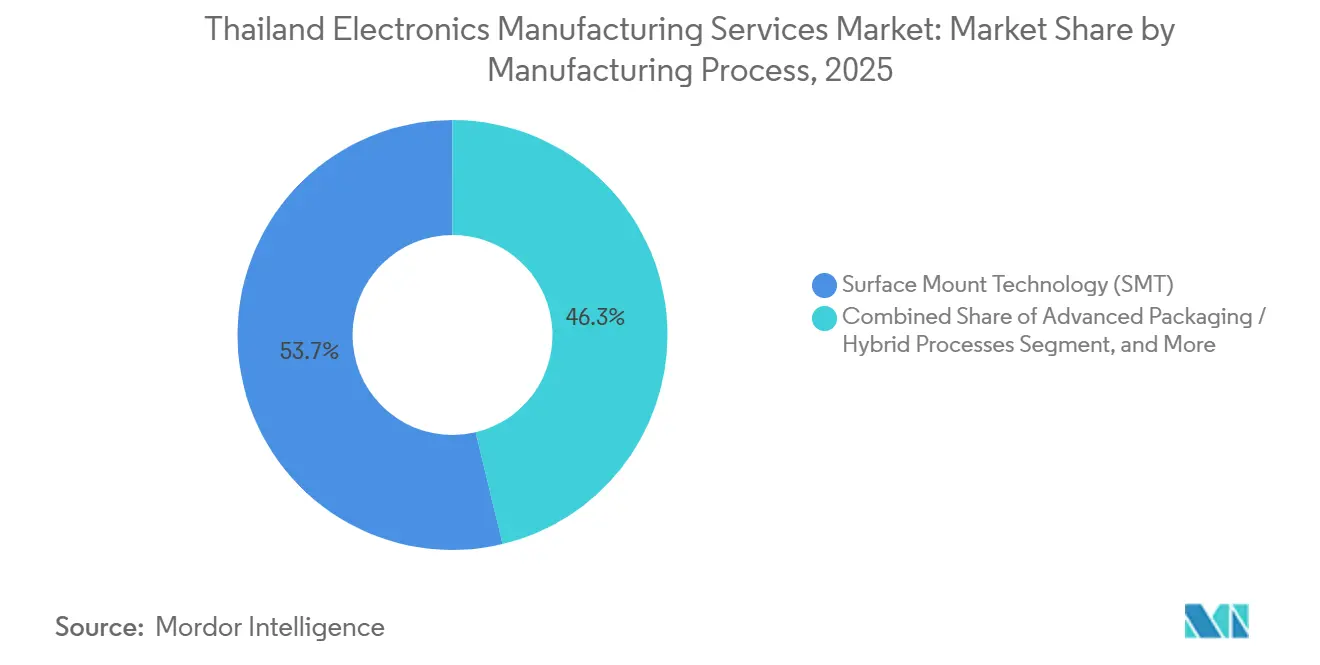

- By manufacturing process, surface-mount technology commanded 53.73% of the Thailand electronics manufacturing services market in 2025, and advanced packaging is set to grow at an 11.07% CAGR through 2031.

- By end-user, consumer electronics held a 36.89% share in 2025, and automotive applications are poised to register a 12.17% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Competitive positioning in Thailand includes both locally based firms and those operating across multiple regions. The market landscape in the global electronics manufacturing services industry research shows how these players are arranged internationally.

Thailand Electronics Manufacturing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth of Thailand's Electric Vehicle Supply Chain | +1.8% | National, concentrated in Eastern Economic Corridor | Medium term (2-4 years) |

| Government Incentives for High-Value-Added Manufacturing | +1.5% | National, with spillover to ASEAN supply chains | Short term (≤ 2 years) |

| Relocation of Chinese OEM Orders Post Trade Tensions | +1.3% | Global, benefiting Thailand and Vietnam | Short term (≤ 2 years) |

| Rising Demand for Advanced Packaging in 5G Modules | +1.2% | Global, with Thailand serving Asia-Pacific and North America | Medium term (2-4 years) |

| Expansion of Medical Electronics Exports from Thailand | +0.9% | Global, targeting North America, EU, and Japan | Long term (≥ 4 years) |

| Increasing Local Content Requirements in Automotive Electronics | +0.8% | National, with regulatory influence from Thai Customs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth of Thailand’s Electric Vehicle Supply Chain

Battery-management systems, traction inverters, and on-board chargers now anchor high-value program awards in the Thailand electronics manufacturing services market. BYD began series production at its Rayong plant in July 2024, with an annual goal of 150,000 vehicles, creating pull-through demand for locally sourced printed circuit assemblies and power modules. A joint venture between Foxconn Technology Group and PTT targets modular EV platforms and power electronics, underpinned by an initial THB 10.5 billion investment that will enter pilot production in 2026.[1]PTT Public Company, “Foxconn-PTT Joint Venture Announcement,” ptt.co.th Board of Investment policy EV 3.5 obliges automakers claiming tax incentives to assemble battery packs domestically from 2026, locking in demand for Thai automotive-grade electronics. Local providers consequently upgrade to IATF 16949 and AEC-Q100 standards to secure qualification slots. These combined forces raise content value per vehicle and keep production in Thailand rather than in China or South Korea.

Government Incentives for High-Value-Added Manufacturing

Expanded A1+ and A1 tiers grant eight-year corporate-income-tax holidays, duty-free machinery imports, and 50% electricity-tariff rebates, directly lowering the cost base of new advanced-electronics projects.[2]Board of Investment Thailand, “A1+ Incentive Schedule,” boi.go.th The FastPass scheme accelerates approvals for projects exceeding THB 1 billion within 30 days; sixteen electronics expansions cleared the gate by December 2025, signaling policy traction. Joint ventures with at least 30% Thai ownership receive an additional 2 years of tax exemption, a lure for silicon-carbide and gallium-nitride initiatives. These inducements offset Thailand’s wage premium relative to Vietnam and Indonesia, enabling firms to invest in fine-pitch surface-mount technology, flip-chip bonding, and system-in-package lines. The predictable incentive framework reassures global tier-1 OEMs that long-term total cost of ownership is competitive.

Relocation of Chinese OEM Orders Post Trade Tensions

United States tariffs of 25-100% on Chinese electronics accelerated order transfers during 2024-2025, prompting OEMs to reroute final assembly to the Thailand electronics manufacturing services market. Thailand’s free trade agreements with Japan, Australia, and the European Union allow duty-free entry for many finished goods.[3]Thai Customs Department, “Free Trade Agreement Tariff Handbook,” customs.go.th Chinese board makers such as Compeq commenced production at new Thai plants valued at over THB 10 billion, moving from groundbreaking to volume output within 18 months. Appliance brands, including Haier approved mid-double-digit-billion-baht investments explicitly to neutralize tariff exposure. The influx diversifies Thailand’s customer base and broadens service volumes beyond legacy consumer devices into white goods, industrial controls, and smart appliances.

Rising Demand for Advanced Packaging in 5G Modules

Miniaturized 5G radios require fan-out wafer-level packages and embedded passives, stimulating a shift from traditional surface-mount toward hybrid semiconductor-board processes. Infineon’s backend plant in Samut Prakan, operational in 2026, will conduct wafer bumping, plasma cleaning, and over-mold for automotive microcontrollers and 5G power discretes. Hana Microelectronics partnered with PTT Digital Solutions to build a silicon carbide wafer line valued at THB 11.5 billion, with first wafers scheduled for 2027. Fabrinet is scaling co-packaged optics for 800-Gbps and 1.6-Tbps transceivers, merging photonics dies with ASICs on common substrates. These investments raise capital intensity while unlocking higher margins, positioning Thailand as a regional hub for heterogeneous integration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled Labor Shortages in Precision Electronics Assembly | -0.7% | National, acute in Eastern Economic Corridor | Short term (≤ 2 years) |

| Volatility in Semiconductor Component Supply | -0.5% | Global, affecting automotive and industrial segments | Medium term (2-4 years) |

| Rising Electricity Costs Impacting Factory Margins | -0.4% | National, with regional variation by utility provider | Short term (≤ 2 years) |

| Competition from Lower-Cost Neighboring Countries | -0.6% | ASEAN, primarily Vietnam and Indonesia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled Labor Shortages in Precision Electronics Assembly

The National Economic and Social Development Council estimated a gap of 400,000 electronics and automotive workers in 2024, with a median employee age of 40 years. Graduating cohorts of 180,000 technicians annually fall short of replacement needs, while the minimum wage rose to THB 400 per day in 2025, tightening labor cost structures. Providers respond by accelerating factory automation: collaborative robots now populate insertion, optical inspection, and packaging cells, reducing direct headcount but increasing capital budgets. Government re-skilling programs target 50,000 workers over three years, but tangible benefits will materialize after 2027. In the interim, underutilized capacity and overtime premiums threaten margins, especially for labor-intensive consumer device lines.

Volatility in Semiconductor Component Supply

Lead times for automotive-grade microcontrollers and power-management ICs remain extended at 16-52 weeks, forcing Thai contract manufacturers to hold above-normal inventory buffers. Mature 40-nm and 65-nm process capacity lags demand despite foundry expansions at 5 nm and below. Thailand electronics manufacturing services market participants are responding with consignment agreements whereby customers own long-lead components, reducing working-capital drag. Some firms now co-locate with distributor hubs inside industrial estates to shorten replenishment cycles. While partial mitigation is feasible, unpredictable allocation shifts continue to disrupt schedule adherence, especially in high-mix industrial and medical programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: PCB Assembly Remains Core While Box-Build Gains Momentum

Printed circuit board assembly accounted for 41.57% of the Thailand EMS market share in 2025, spanning smartphones, factory automation, and networking gear. Electromechanical and box-build work is forecast to expand at a 11.41% CAGR through 2031, elevating its share of Thailand's electronics manufacturing services market as customers request fully tested enclosures rather than bare boards. Jabil and Inno have already broken ground on a 15,000-square-meter enclosure plant to integrate sheet-metal, thermal interface, and final test lines. Rapid-prototype labs operated by Team Precision compress design validation cycles from two weeks to one, reducing time-to-market for industrial sensor makers.

Box-build adoption rides on automotive battery packs, home energy storage, and smart-appliance modules that integrate mechanical, thermal, and electronic components. Providers invest in automated torque tools, conformal-coating booths, and environmental stress chambers to satisfy reliability targets. Engineering service attachment rates climb as design-for-manufacturability, vibration analysis, and regulatory certification are migrated to contract partners. Logistics services, from global component brokerage to direct-to-store delivery, are bundled into master service agreements, deepening supplier lock-in and anchoring long-term revenue streams for the Thailand EMS market.

By Business Model: Contract Manufacturing Dominates While Hybrid Engagements Accelerate

Contract manufacturing accounted for 63.48% of revenue in 2025, confirming OEMs' preference for outsourcing capital-intensive assembly while retaining product IP. Hybrid and turnkey partnerships are projected to grow at 10.93% through 2031, as automotive and medical customers demand co-development, supply-chain orchestration, and after-sales logistics under a single umbrella. SVI Public Company exemplifies the model, running synchronized factories in Thailand, the United States, and China to offer regional build-to-order with centralized design control.

Original-design manufacturing remains narrow, concentrated in smart lighting and consumer peripherals, where reference designs can be licensed with minimal liability exposure. Hybrid arrangements gain favor when rapid regulatory or trade changes require flexible sourcing footprints. Joint ventures like the Hana-PTT silicon-carbide line share process risk and capital burden, aligning interests across value-chain nodes. As a result, inventory financing, demand-forecast collaboration, and digital twin simulations become routine features of high-value contracts in the Thailand EMS market.

By Manufacturing Process: Surface-Mount Leads, Advanced Packaging Rises

Surface-mount technology retained 53.73% revenue share in 2025, underpinning the bulk of consumer and industrial assembly. Advanced packaging and hybrid processes are on track to grow at a 11.07% CAGR through 2031, driven by demand for radar modules, 5G RF front-ends, and edge-AI wearables. Infineon’s Samut Prakan plant showcases wafer bumping, die attach, and over-mold in a single cleanroom, shortening supply chains that previously stretched to Malaysia. Board of Investment incentives specifically reward sub-0.4-mm pitch placement and system-in-package lines with longer tax holidays, tilting new capital toward high-density processes.

Through-hole assembly persists in rugged industrial controls and power conversion but continues to cede ground as OEMs redesign boards for reflow compatibility. Providers now blend laser-drilled microvias, embedded passives, and copper coin inserts to manage thermal loads in automotive power electronics. Co-packaged optics transceivers assembled by Fabrinet illustrate the convergence of semiconductor backend and board assembly, a trend that elevates technical barriers and reinforces Thailand’s competitive edge in complex builds.

By End-User: Consumer Electronics Largest, Automotive Fastest Growing

Consumer electronics accounted for 36.89% of demand in 2025, including smartphones, tablets, wearables, and smart appliances. Automotive electronics are forecast to post a 12.17% CAGR through 2031, fueled by electric-vehicle content growth and local-content mandates. Industrial automation remains a steady contributor as factories digitize operations, leveraging Thailand’s machinery clusters for co-located mechanical and electronic sub-assembly.

Communication infrastructure, especially 5G base stations and optical transport, commands premium gross margins owing to tight performance tolerances. Medical electronics benefit from dense ISO 13485 certification and near-shore supply to Japanese OEMs, while lighting transitions to smart LED drivers elevate embedded wireless content. Government policy targeting 30% domestic innovation in medical devices by 2027 creates upside for design services. Collectively, these shifts diversify revenue sources and cushion cyclicality in the Thailand EMS market.

Geography Analysis

The Eastern Economic Corridor accounts for over 70% of Thailand's electronics manufacturing services market because it is home to industrial estates, deep-sea ports, and related logistics hubs. Chonburi, Rayong, and Samut Prakan host multi-building campuses for global providers such as Jabil, Flex, and Sanmina. New advanced-packaging facilities by Infineon and Compeq add critical mass to Samut Prakan, deepening semiconductor backend capabilities. Border provinces like Sa Kaeo attract feeder plants that perform metal stamping and injection molding within one trucking day of assembly sites, reinforcing localized supply.

Northern Thailand, primarily Lamphun and Chiang Mai, specializes in optoelectronics and high-reliability modules. Hana Microelectronics and Stars Microelectronics deploy class-100 cleanrooms for image-sensor and medical-device assembly, leveraging the region’s university engineering talent and lower labor competition relative to Bangkok. Logistics connectivity relies on air freight from Chiang Mai International Airport, which is upgrading cargo capacity to 200,000 tons a year by 2027, ensuring time-critical shipments reach Japan and the United States quickly.

Western and southern regions account for a modest share, focusing on niche industrial and lighting applications. Proximity to Malaysia encourages cross-border supply of passive components and wire harnesses. Government efforts to expand the Southern Economic Corridor could unlock new coastal sites with access to Andaman Sea shipping lanes, but infrastructure build-out remains in early stages. Overall, the geographic dispersion balances risk and provides customers with options to split production across floodplains and seismic zones, enhancing resilience in the Thailand electronics manufacturing services market.

Mordor Intelligence tracks the electronics manufacturing services market across other major regions such as Europe, Asia, and North America, with additional country-level coverage spanning South Korea, Japan, France, United States, United Kingdom, and Germany, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

Competition is moderate with clear technology tiers. Global heavyweights Jabil, Flex, Celestica, and Sanmina leverage scale purchasing and global manufacturing-execution systems, attracting automotive and industrial accounts that value multi-site redundancy. Thai-listed firms Hana Microelectronics, SVI Public Company, and Cal-Comp Electronics win programs requiring small-lot flexibility, fast prototyping, and engineering collaboration. Fabrinet dominates high-speed optical transceivers, generating more than USD 2.5 billion in fiscal-2024 revenue from Thai plants alone.

Strategic moves center on vertical integration and geographic diversification. Hana and PTT are co-investing in silicon-carbide wafer fabrication, targeting wide-bandgap devices for EV inverters and 5G base stations. SVI opened plants in Texas and Suzhou to complement Thai capacity and mitigate single-country risk. Delta Electronics is expanding into power module packaging, aiming to capture the rising demand for DC-fast-charging converters. Automation equipment vendors Yamaha Robotics and Juki embed collaborative robots within customer lines, reducing labor intensity by up to 20% per unit shipped. The Board of Investment FastPass program shortens approval cycles for expansions above THB 1 billion, indirectly favoring incumbents with strong balance sheets and compliance histories.

White-space segments include medical device sub-assemblies and ruggedized industrial modules for oil and gas. Regulatory and environmental qualification hurdles deter smaller entrants, enabling specialists to earn double-digit operating margins. Providers that combine ISO 13485, traceability software, and extended-temperature test chambers command price premiums. As automation spreads, the gap between technology leaders and laggards is widening, setting the stage for consolidation waves in the Thailand electronics manufacturing services market.

Thailand Electronics Manufacturing Services Industry Leaders

Cal-Comp Electronics (Thailand) Public Company Limited

Hana Microelectronics Public Company Limited

SVI Public Company Limited

Stars Microelectronics (Thailand) Public Company Limited

Delta Electronics (Thailand) Public Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Infineon commenced construction of an automotive microcontroller and power-discrete backend facility in Samut Prakan, with start-up slated for early 2026.

- December 2025: The Board of Investment cleared 16 electronics projects under FastPass, unlocking over THB 20 billion in new capital commitments.

- December 2025: Identiv completed the shift of RFID-transponder production to its Bangkok plant, boosting annual capacity by 30 million units.

- November 2025: Jabil and Inno broke ground on a 15,000-square-meter battery-energy storage enclosure facility in Rayong, targeting volume output in Q1 2027.

Thailand Electronics Manufacturing Services Market Report Scope

The Thailand Electronics Manufacturing Services Market Report is Segmented by Service Type (Electronic Manufacturing Services, Engineering Services, Test and Development Implementation Services, Logistics Services, Other Service Types), Business Model (Contract Manufacturing (CM), Original Design Manufacturing (ODM), Hybrid / Turnkey / Other Business Models), Manufacturing Process (Surface Mount Technology (SMT), Through-Hole Technology (THT), Advanced Packaging / Hybrid Processes), End-user (Mobile Devices, Consumer Electronics, Computer, Industrial, Automotive, Communication, Lighting, Medical, Other End-users). The Market Forecasts are Provided in Terms of Value (USD).

| Electronics Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | |

| Prototyping | |

| Other Electronics Manufacturing Services | |

| Engineering Services | |

| Test and Development Implementation Services | |

| Logistics Services | |

| Other Service Types |

| Contract Manufacturing (CM) |

| Original Design Manufacturing (ODM) |

| Hybrid / Turnkey / Other Business Models |

| Surface Mount Technology (SMT) |

| Through-Hole Technology (THT) |

| Advanced Packaging / Hybrid Processes |

| Mobile Devices (Smartphones and Tablets) |

| Consumer Electronics |

| Computer (PCs/Desktop/Laptops) |

| Industrial |

| Automotive |

| Communication |

| Lighting |

| Medical |

| Other End-users |

| By Service Type | Electronics Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | ||

| Prototyping | ||

| Other Electronics Manufacturing Services | ||

| Engineering Services | ||

| Test and Development Implementation Services | ||

| Logistics Services | ||

| Other Service Types | ||

| By Business Model | Contract Manufacturing (CM) | |

| Original Design Manufacturing (ODM) | ||

| Hybrid / Turnkey / Other Business Models | ||

| By Manufacturing Process | Surface Mount Technology (SMT) | |

| Through-Hole Technology (THT) | ||

| Advanced Packaging / Hybrid Processes | ||

| By End-user | Mobile Devices (Smartphones and Tablets) | |

| Consumer Electronics | ||

| Computer (PCs/Desktop/Laptops) | ||

| Industrial | ||

| Automotive | ||

| Communication | ||

| Lighting | ||

| Medical | ||

| Other End-users |

Key Questions Answered in the Report

What is the projected value of the Thailand electronics manufacturing services market in 2031?

The market is forecast to reach USD 12.57 billion by 2031, reflecting a 10.38% CAGR.

Which segment will grow fastest within Thai EMS over the next five years?

Automotive electronics is expected to post a 12.17% CAGR through 2031, outpacing all other end-user segments.

How significant is advanced packaging in Thailand’s EMS landscape?

Advanced packaging and hybrid processes are set to expand at 11.07% annually, driven by 5G modules and automotive radar assemblies.

What government incentives support high-value electronics projects?

A1+ and A1 tiers provide eight-year tax holidays, duty-free machinery imports, and discounted electricity, while the FastPass scheme speeds project approvals.

Why are OEMs relocating orders from China to Thailand?

U.S. tariff exposure and Thailand’s extensive free-trade agreements motivate shippers to shift high-mix, high-value assembly to Thai plants.

Page last updated on: