India Electronics Manufacturing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

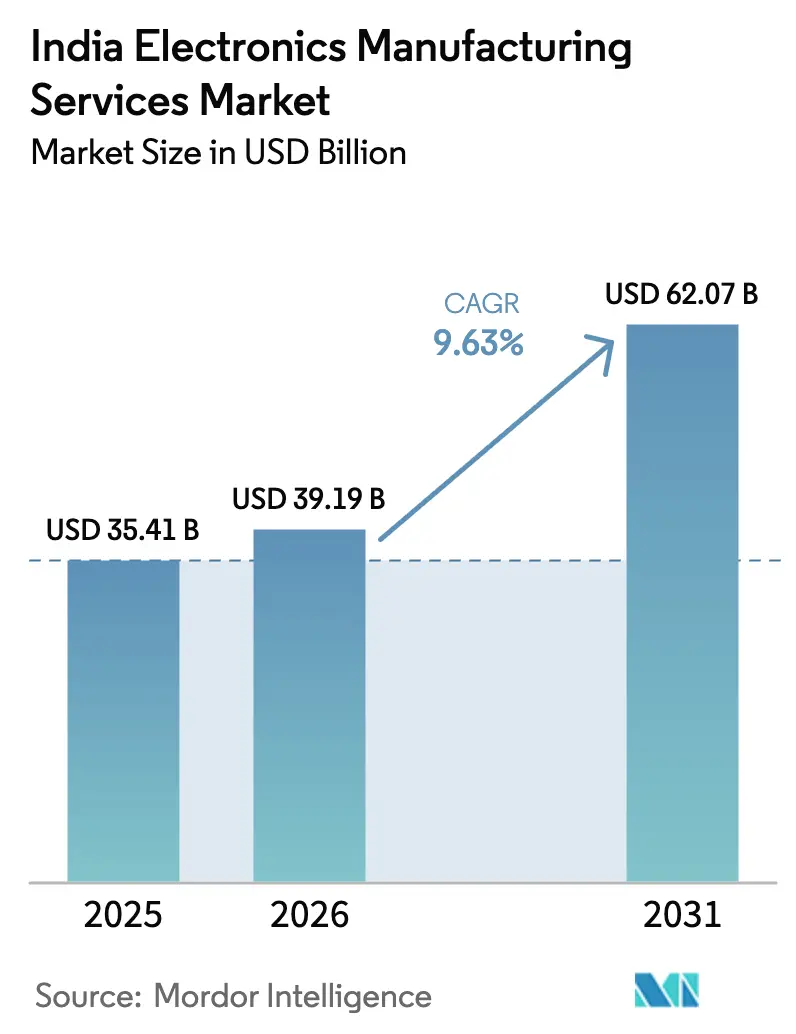

| Base Year Market Size (2025) | USD 35.41 Billion |

| Market Size (2026) | USD 39.19 Billion |

| Market Size (2031) | USD 62.07 Billion |

| Growth Rate (2026 - 2031) | 9.63% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Electronics Manufacturing Services Market Analysis by Mordor Intelligence

The India electronics manufacturing services market size was valued at USD 35.41 billion in 2025 and expected to grow from USD 39.19 billion in 2026 to reach USD 62.07 billion by 2031, at a CAGR of 9.63% during the forecast period (2026-2031). This momentum reflects global supply-chain rebalancing that is shifting assembly and test work from coastal China toward India, where Production Linked Incentive (PLI) 2.0 subsidies and targeted component schemes are shrinking the country’s import bill for printed circuit boards (PCBs), camera modules, and passive components. Tight integration between state-level incentives and greenfield investments from Foxconn, Tata Electronics, and Dixon Technologies has established Tamil Nadu, Karnataka, and Uttar Pradesh as key clusters, while emerging corridors in Andhra Pradesh and Madhya Pradesh are picking up capacity for multilayer boards and copper-clad laminates. Rapid design-win cycles in smartphones, EV battery-management systems, and 5G infrastructure are encouraging original equipment manufacturers (OEMs) to move beyond build-to-print orders toward turnkey engagements that bundle firmware integration, regulatory testing, and after-sales logistics. At the same time, margin pressure persists as Chinese rivals use idle capacity to underbid on export tenders, compressing Indian EMS gross margins by 150–200 basis points since 2024.

Key Report Takeaways

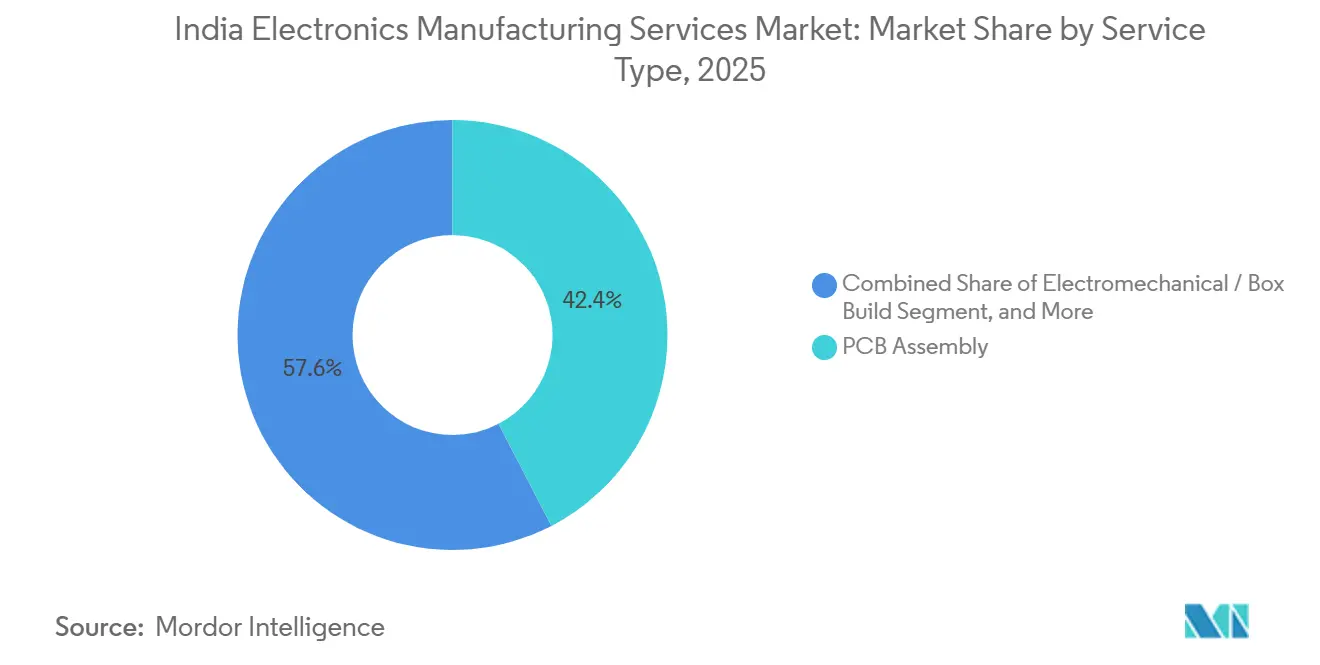

- By service type, PCB assembly led with 42.39% of India electronics manufacturing services market share in 2025, while box-build and electromechanical assembly is advancing at a 10.61% CAGR through 2031.

- By business model, contract manufacturing accounted for 61.73% of the India electronics manufacturing services market in 2025, whereas hybrid and turnkey models are growing at a 10.22% CAGR through 2031.

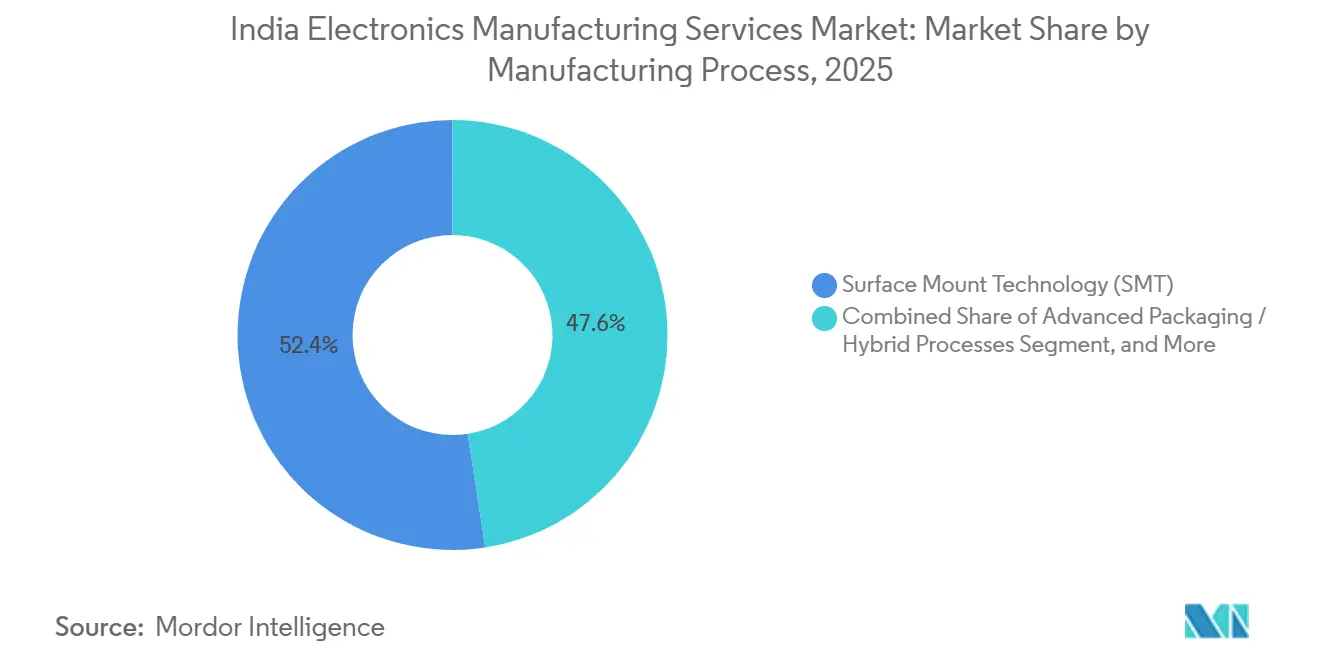

- By manufacturing process, surface-mount technology accounted for 52.44% of the India electronics manufacturing services market in 2025; advanced packaging and hybrid processes are forecast to expand at a 10.28% CAGR through 2031.

- By end-user, consumer electronics held 38.79% of the India EMS market in 2025, while the automotive segment is projected to post the fastest 11.46% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Proportional positioning is established by comparing country level and regional contributions against the global total, including that of India. The electronics manufacturing services market share in our global report expresses these relative weights.

India Electronics Manufacturing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Incentives Under PLI 2.0 and Component Schemes | +2.8% | National, with concentration in Tamil Nadu, Andhra Pradesh, Karnataka, Gujarat | Medium term (2-4 years) |

| China-Plus-One Outsourcing Shift to India | +2.1% | Global, with primary impact in North India (Uttar Pradesh, Haryana) and South India (Tamil Nadu, Karnataka) | Short term (≤ 2 years) |

| Vertical Integration Into Component Manufacturing Boosting Value-Add | +1.6% | National, early gains in Tamil Nadu, Andhra Pradesh, Madhya Pradesh | Long term (≥ 4 years) |

| Rising Domestic Demand for Smart Devices and EV Electronics | +1.4% | National, urban clusters and Tier-2 cities | Medium term (2-4 years) |

| Expansion of Export-Oriented Production-Linked Incentives | +1.0% | National, export hubs in Tamil Nadu, Karnataka, Uttar Pradesh | Medium term (2-4 years) |

| Adoption of Industry 4.0 Automation in Indian Factories | +0.7% | National, led by large-scale facilities in Tamil Nadu, Karnataka, Haryana | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Incentives Under PLI 2.0 And Component Schemes

The Ministry of Electronics and Information Technology cleared seven projects worth INR 5,532 crore (USD 660 million) in October 2025, marking India’s first domestic production of copper-clad laminates and polypropylene film for capacitors.[1]Press Information Bureau, “Second tranche of 17 approvals under ECMS announced,” pib.gov.in Differentiated incentives that blend turnover-linked payouts, capex subsidies, and employment targets are nudging investors toward labor-intensive assembly without sacrificing high-value multilayer and HDI PCB capability. A second tranche of 17 projects sanctioned in November 2025 lifted approved outlays to INR 12,704 crore (USD 1.5 billion) and underscored official intent to double local value addition to 40% by the decade’s end. While the pipeline of 249 applications signals robust confidence, the lag between approval and capacity ramp could lead to localized oversupply, compressing margins by 2028 if export absorption falters.

China-Plus-One Outsourcing Shift To India

Apple’s iPhone exports from India crossed INR 1 lakh crore (USD 12 billion) in 2024, a 40% jump driven by expansions at Foxconn and Tata Electronics in Tamil Nadu.[2]Zee Business Desk, “iPhone exports from India jump 40% in 2024,” zeebiz.com The relocation is selective: older iPhone models are moving to India, while Pro variants remain in Zhengzhou to leverage established supplier ecosystems. Domestic conglomerates are matching the pace. Tata announced plans for nine new plants and USD 18 billion in investments in electronics and semiconductors, banking on geopolitical tailwinds that keep India’s cost-plus premium intact. Chinese EMS leaders, such as Luxshare, are meanwhile exploring minority joint ventures to gain access to PLI, illustrating a pragmatic mix of competition and collaboration.

Vertical Integration Into Component Manufacturing

Domestic value addition hovered at 20-25% in 2024, but multilayer PCB and laminate projects from Syrma SGS, Ascent Circuits, and SRF are set to lift the metric toward 40% once new lines reach steady state.[3]The Hindu Staff, “Syrma SGS to set up India’s largest PCB plant,” thehindu.com Syrma’s INR 1,595 crore (USD 191 million) plant and Ascent’s INR 1,100 crore (USD 131 million) facility will together add roughly 2 million m² of annual multilayer capacity, equal to one-fifth of 2024-25 domestic demand. Upstream moves into copper-clad laminates demand chemistry expertise and multi-year payback horizons, yet offer strategic insulation against supply shocks similar to the 2017-18 MLCC crunch.

Rising Domestic Demand For Smart Devices And EV Electronics

Electronics output surged from INR 1.90 lakh crore (USD 22.7 billion) in fiscal 2015 to INR 9.52 lakh crore (USD 114 billion) in fiscal 2024, supported by a 20% export CAGR. EV penetration in two-wheelers hit 5-6% in 2024, and each vehicle consumes up to 15,000 multilayer ceramic capacitors, five to ten times as many as an internal-combustion equivalent, multiplying PCB and passive component demand. While smartphone replacement cycles have lengthened, OEMs now emphasize design-for-manufacturability and cost-down engineering, giving EMS partners that provide early-stage design input an edge in capturing refreshed model pipelines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dependence on Imported Semiconductors and Components | -1.2% | National, with acute impact on high-end electronics and automotive segments | Medium term (2-4 years) |

| Skill Shortages in High-Precision Electronics Assembly | -0.9% | National, particularly in Tier-2 cities and emerging clusters | Short term (≤ 2 years) |

| Policy Uncertainty Post-PLI Phase-Out | -0.6% | National | Medium term (2-4 years) |

| Intensifying Price Competition Driving Margin Compression | -0.5% | National, with spillover to export markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Dependence On Imported Semiconductors And Components

India still imports 88% of its PCB demand and more than 90% of multilayer ceramic capacitors, resistors, and inductors, exposing EMS firms to tariff swings and geopolitical shocks. The October 2025 PLI tranche will meet only one-fifth of domestic PCB needs by 2027-28, leaving the bulk of sourcing tied to China, Taiwan, and South Korea. Anti-dumping duties on imported bare boards raised EMS input costs before local plants became operational, illustrating the trade-off between infant-industry protection and export competitiveness.

Skill Shortages In High-Precision Electronics Assembly

Syrma SGS is flying technicians to South Korea and China for four-week training stints to master multilayer lamination and automated optical inspection, underscoring the domestic talent gap in HDI and automotive-grade assembly. Attrition runs 25-30% a year as experienced engineers command wage premiums, while Centers of Excellence lag industry requirements by up to 18 months due to equipment procurement cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Box-Build Gains As OEMs Demand Turnkey Delivery

PCB assembly accounted for 42.39% of 2025 revenue, anchored by high-volume smartphone boards assembled at sub-three-minute takt times. Electromechanical and box-build services are logging a 10.61% CAGR, powered by automotive customers outsourcing complete battery-management systems and infotainment modules. The India EMS market size tied to box-build lines is projected to rise steadily as OEMs seek single-invoice solutions that cover plastics, metal enclosures, and firmware flashing.

The shift draws capital into mechanical integration and end-of-line testing. Zetwerk’s INR 500–800 crore expansion blends PCB lines with enclosure stamping and heat-sink machining, illustrating the convergence of electronics and precision metal parts. Mid-tier EMS firms that add rapid-turn prototyping, with three-day cycle times versus the usual two weeks, are capturing early design wins that lock in downstream production volumes.

By Business Model: Hybrid And Turnkey Contracts Capture Design-Led Programs

Build-to-print contract manufacturing still accounted for 61.73% of revenue in 2025, yet hybrid and turnkey models are expanding at 10.22% a year as brand owners outsource schematic capture, component selection, and regulatory testing. India's electronics manufacturing services market share aligned with hybrid engagements is widening because OEMs want flexible boundaries, allowing them to phase in or out elements of the value chain without renegotiating contracts.

Tata Electronics’ 60% purchase of Pegatron India gives the conglomerate a vertically integrated platform spanning iPhone assembly, PCB fabrication, and upcoming 28-nanometer wafer output in Gujarat. Mid-tier competitors are responding by hiring design engineers and building reliability labs, but the upfront cost of acquiring firmware talent and specialized test gear erodes asset turns for 12–18 months, stretching balance sheets.

By Manufacturing Process: Advanced Packaging Rises With SiP Modules

Surface-mount technology (SMT) retained 52.44% revenue in 2025, driven by smartphones and PCs that pack more than 1,000 placements per board. Advanced packaging and hybrid processes are on a 10.28% CAGR path as system-in-package (SiP) modules integrate RF, memory, and logic in compact footprints for 5G radios and edge-AI accelerators. The India EMS market for advanced packaging is poised to accelerate once AT and S India, and Micropack bring 16-layer HDI lines online in 2028.

Yield remains a significant hurdle for Indian HDI boards, as their first-pass rates lag those of Taiwanese counterparts by 10–15 percentage points. This performance gap has driven high-mix manufacturers to invest more in advanced technologies, such as automated X-ray inspection systems and boundary-scan testers, to enhance production efficiency and quality. Although capital subsidies under the component scheme provide some financial support to manufacturers, they come with a critical limitation. Firms are required to finalize and lock in their equipment models at the application stage itself, which significantly restricts their flexibility to make mid-cycle upgrades or adopt newer technologies as they become available.

By End-User: Automotive Electronics Outpaces All Other Verticals

Consumer electronics still dominated demand at 38.79% in 2025, driven by smartphone assembly for Apple, Samsung, and Xiaomi. Yet automotive electronics is projected to post an 11.46% CAGR through 2031, the fastest among all verticals, as EV traction inverters, battery-management boards, and ADAS controllers localize. The India EMS market size tied to automotive contracts will therefore rise disproportionally to its current share.

OEM localization mandates and state EV subsidies require AEC-Q-qualified PCBs and high-voltage film capacitors, which only a handful of domestic plants can supply. Syrma’s acquisition of Elcome Integrated Systems to gain defense-grade and maritime electronics capabilities shows EMS players hedging against cyclicality by diversifying into adjacent regulated segments. Medical-device assembly, though small, offers premium margins because ISO 13485 traceability requirements deter low-cost entrants.

Geography Analysis

Tamil Nadu anchors nearly one-third of national EMS output, buoyed by Foxconn’s iPhone campus in Sriperumbudur, Tata Electronics’ Pegatron acquisition, and Zetwerk’s new 15-acre SMT cluster in Pannur. Robust port access and a mature component distributor base enable door-to-dock times under 48 hours for ASEAN shipments, a key differentiator for export-oriented factories. Karnataka follows, fueled by the Bengaluru design ecosystem and state commitments worth INR 1,750 crore for PCB projects announced at Bengaluru Tech Summit 2025.

Uttar Pradesh and Haryana together captured sizeable smartphone assembly contracts under the original PLI scheme, leveraging proximity to the National Capital Region for skilled labor and air-cargo connectivity. However, land-acquisition bottlenecks around Noida have slowed new capacity, pushing some investors toward neighboring Madhya Pradesh, where greenfield parcels cost up to 25% less. Andhra Pradesh is emerging as India’s multilayer PCB hub after Syrma SGS and AT and S India broke ground in Naidupeta and SriCity respectively, lured by 50% capital subsidies and a deepwater port at Krishnapatnam.

Second-tier corridors in Goa, Jammu and Kashmir, and Assam illustrate the government’s geographic diversification strategy. The Electronics Manufacturing Cluster in Jagiroad, Assam, tied to Tata Semiconductor’s planned assembly-and-test unit, offers the Northeast its first foothold in advanced packaging. While early movers gain higher subsidies, they also incur higher logistics costs, as containerized freight from Guwahati to Mumbai can take 9 days, compared with 3 days from Chennai. Over the forecast horizon, regional competition for skilled technicians will intensify, pressuring wage structures even in historically low-cost interiors.

Mordor Intelligence examines the electronics manufacturing services market across diverse other regional markets as well, including Europe, Asia, and North America, while also offering granular country-level perspectives for Singapore, South Korea, Germany, United States, United Kingdom, and Japan and more.

Competitive Landscape

The top five players, Dixon Technologies, Foxconn Hon Hai India, Tata Electronics, Bharat FIH, and Flex India, collectively accounted for 45–50% of revenue in 2025, leaving ample room for mid-tier specialists such as Kaynes Technology, Syrma SGS, and Avalon Technologies to thrive in niches. Tata Electronics’ 60% stake in Pegatron India vaulted the group to 44% of India’s iPhone assembly value, narrowing Foxconn’s lead and signaling a willingness to absorb working-capital swings to win flagship contracts.

Strategic moves gravitate toward upstream integration: Kaynes Circuits committed INR 3,280 crore to multilayer PCBs and copper-clad laminates, while Flex India partnered with AT and S to qualify 16-layer boards for European automotive customers. Geographic diversification is another lever; Avalon’s new plant in Jammu taps lower land costs and 30-year tax holidays, offsetting longer lead times to west-coast ports.

Technology adoption differentiates leaders. Foxconn deploys real-time statistical process control and predictive-maintenance algorithms that cut SMT downtime by 12%, whereas many domestic peers still rely on batch-level functional testing. Shared infrastructure initiatives, such as the Pillaipakkam Electronics Manufacturing Cluster, aim to democratize access to environmental chambers and EMC labs, reducing capex hurdles for firms with revenue below USD 200 million.

Looking ahead, advanced packaging, automotive power electronics, and medical-device subassemblies represent high-margin frontiers with significant growth potential. However, barriers to entry include multi-year qualification cycles, which can delay market penetration, and the stringent requirement for ISO 13485 or AEC-Q credentials, which are critical for ensuring compliance and quality standards in these industries. Despite these challenges, early movers who successfully navigate these hurdles could command double-digit EBITDA margins, offering a substantial advantage compared to the mid-single-digit returns typically observed in the consumer electronics market.

India Electronics Manufacturing Services Industry Leaders

Dixon Technologies (India) Limited

Tata Electronics Private Limited

DBG Technology India Private Limited

Flextronics Technologies (India) Private Limited

Jabil Circuit India Private Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Syrma SGS commenced construction of a multilayer PCB plant in Naidupeta, Andhra Pradesh, budgeting INR 700 crore and targeting 2.1 million m² of annual capacity upon full ramp.

- November 2025: The Ministry of Electronics and Information Technology approved 17 projects worth INR 7,172 crore under the Electronics Components Manufacturing Scheme, including India’s first optical-transceiver lines by Jabil Circuit India and Zetchem Supply Chain Services.

- November 2025: Karnataka secured INR 1,750 crore of fresh PCB investment at Bengaluru Tech Summit, highlighted by Wipro Electronics’ upcoming Doddaballapura plant.

- November 2025: Syrma SGS announced a separate INR 1,595 crore multilayer PCB facility near Naidupeta, projected to create 2,170 skilled jobs.

India Electronics Manufacturing Services Market Report Scope

The India Electronics Manufacturing Services Market Report is Segmented by Service Type (Electronic Manufacturing Services, Engineering Services, Test and Development Implementation Services, Logistics Services, Other Service Types), Business Model (Contract Manufacturing (CM), Original Design Manufacturing (ODM), Hybrid / Turnkey / Other Business Models), Manufacturing Process (Surface Mount Technology (SMT), Through-Hole Technology (THT), Advanced Packaging / Hybrid Processes), End-user (Mobile Devices, Consumer Electronics, Computer, Industrial, Automotive, Communication, Lighting, Medical, Other End-users). The Market Forecasts are Provided in Terms of Value (USD).

| Electronics Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | |

| Prototyping | |

| Other Electronics Manufacturing Services | |

| Engineering Services | |

| Test and Development Implementation Services | |

| Logistics Services | |

| Other Service Types |

| Contract Manufacturing (CM) |

| Original Design Manufacturing (ODM) |

| Hybrid / Turnkey / Other Business Models |

| Surface Mount Technology (SMT) |

| Through-Hole Technology (THT) |

| Advanced Packaging / Hybrid Processes |

| Mobile Devices (Smartphones and Tablets) |

| Consumer Electronics |

| Computer (PCs/Desktop/Laptops) |

| Industrial |

| Automotive |

| Communication |

| Lighting |

| Medical |

| Other End-users |

| By Service Type | Electronics Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | ||

| Prototyping | ||

| Other Electronics Manufacturing Services | ||

| Engineering Services | ||

| Test and Development Implementation Services | ||

| Logistics Services | ||

| Other Service Types | ||

| By Business Model | Contract Manufacturing (CM) | |

| Original Design Manufacturing (ODM) | ||

| Hybrid / Turnkey / Other Business Models | ||

| By Manufacturing Process | Surface Mount Technology (SMT) | |

| Through-Hole Technology (THT) | ||

| Advanced Packaging / Hybrid Processes | ||

| By End-user | Mobile Devices (Smartphones and Tablets) | |

| Consumer Electronics | ||

| Computer (PCs/Desktop/Laptops) | ||

| Industrial | ||

| Automotive | ||

| Communication | ||

| Lighting | ||

| Medical | ||

| Other End-users |

Key Questions Answered in the Report

What is the current value of the India electronics manufacturing services market?

The market stood at USD 39.19 billion in 2026 and is projected to reach USD 62.07 billion by 2031.

Which service type is expanding fastest in India electronics manufacturing?

Electromechanical and box-build assembly is growing at a 10.61% CAGR through 2031, reflecting OEM demand for turnkey delivery.

How will automotive electronics influence demand?

Automotive contracts are forecast to grow at an 11.46% CAGR as EV traction inverters and battery-management boards localize, outpacing all other verticals.

What role do government incentives play in sector growth?

PLI 2.0 and the Electronics Components Manufacturing Scheme together contribute an estimated 2.8 percentage-point uplift to market CAGR by subsidizing capex and output.

Which regions are emerging as new EMS hubs?

Beyond Tamil Nadu and Karnataka, Andhra Pradesh, Madhya Pradesh and Assam are securing greenfield PCB, laminate and advanced-packaging investments through generous subsidies.

How concentrated is competition among leading EMS providers?

The top five firms hold roughly half the revenue, indicating moderate concentration where scale advantages coexist with opportunities for mid-tier specialists.

Page last updated on: