Germany Electronics Manufacturing Services Market Size and Share

Market Overview

| Study Period | 2026 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

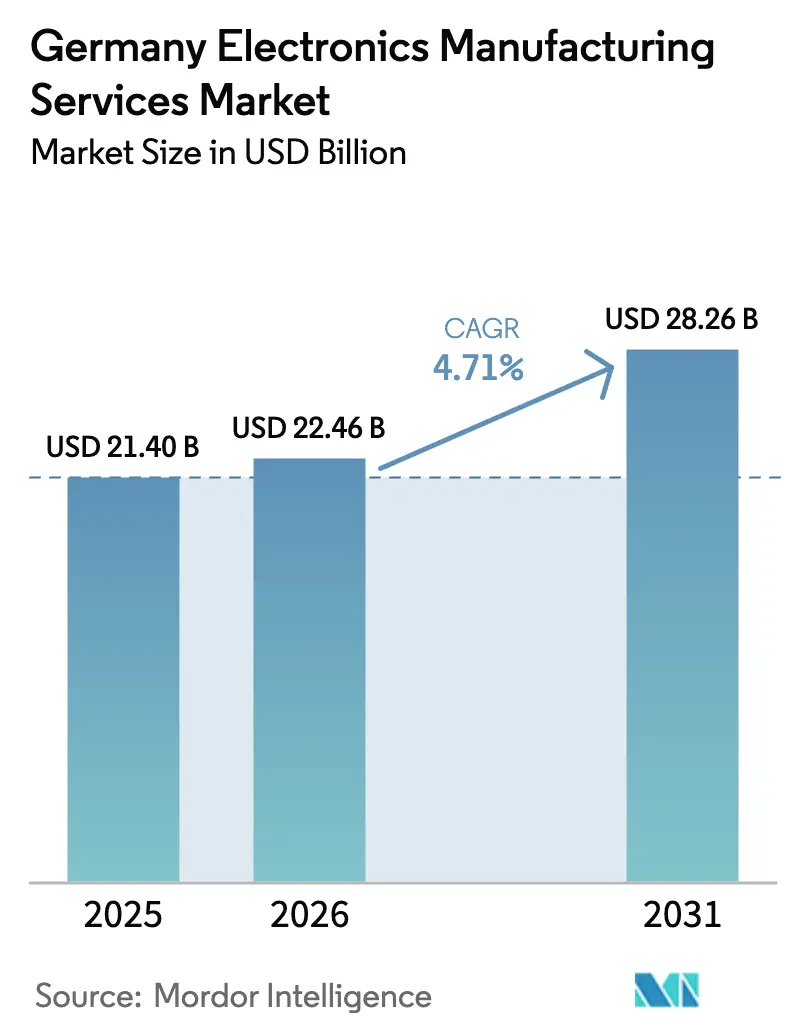

| Base Year Market Size (2025) | USD 21.40 Billion |

| Market Size (2026) | USD 22.46 Billion |

| Market Size (2031) | USD 28.26 Billion |

| Growth Rate (2026 - 2031) | 4.71% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Electronics Manufacturing Services Market Analysis by Mordor Intelligence

The Germany Electronics Manufacturing Services Market is expected to grow from USD 21.40 billion in 2025 to USD 22.46 billion in 2026 and is forecasted to reach USD 28.26 billion by 2031 at 4.71% CAGR over 2026-2031. This Germany EMC market size reflects steady momentum as OEMs shift from legacy automotive and industrial electronics toward compact e-mobility modules and miniaturized medical devices. Demand is reinforced by nearshoring mandates, advanced-packaging subsidies, and the accelerating build-out of semiconductor back-end lines that previously sat in Southeast Asia. Contract manufacturers are leveraging these tailwinds to offset margin pressure coming from Central and Eastern European rivals that concentrate on commodity PCB assembly. Meanwhile, price volatility in copper and rare-earth inputs as well as a widening skilled-labour gap temper overall growth, forcing providers to upgrade automation, hedge material costs, and adopt hybrid business models that transfer more design and inventory risk to the EMS partner. Competitive dynamics remain favourable for regional specialists that can certify to ISO 13485 and IATF 16949, maintain engineering colocation, and deliver rapid design changes for automotive, industrial, and medical customers.

Key Report Takeaways

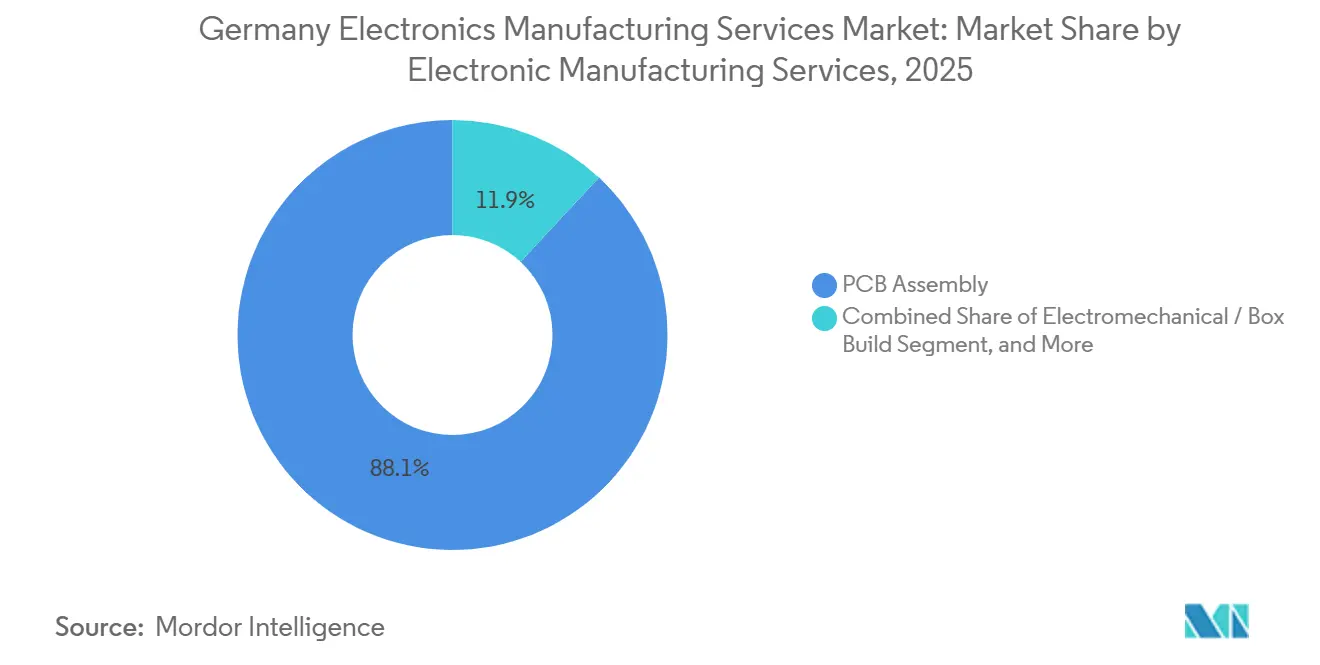

- By services type, PCB assembly led with 42.68% revenue share in 2025 while electromechanical assembly and box build are growing at a 5.78% CAGR through 2031.

- By business model, contract manufacturing held 63.77% of the Germany electronics manufacturing services market share in 2025 and hybrid and turnkey models are advancing at a 5.28% CAGR to 2031.

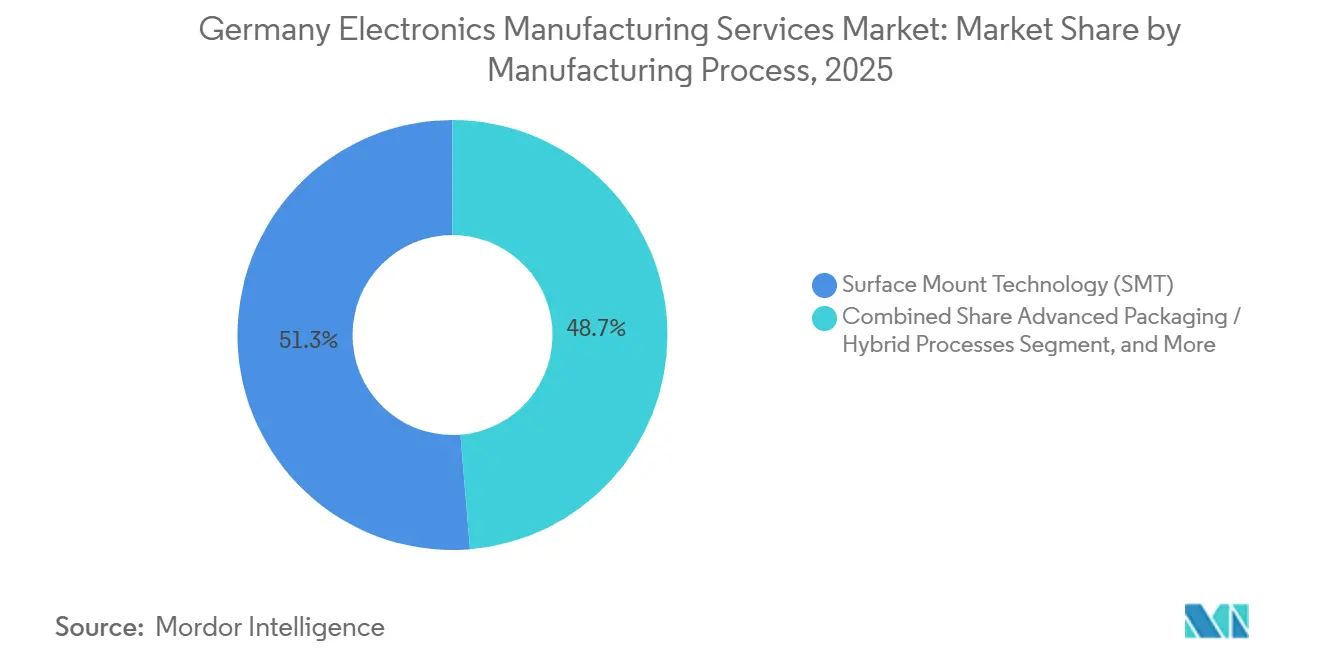

- By manufacturing process, surface-mount technology generated 51.29% revenue in 2025, whereas advanced packaging and hybrid processes are forecast to expand at a 5.55% CAGR through 2031.

- By end user, industrial applications captured 31.44% revenue in 2025, while automotive electronics is projected to climb at a 5.93% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany participates in a competitive field that extends beyond its own borders. The market landscape in the global electronics manufacturing services industry outlined by Mordor Intelligence covers that wider structure.

Germany Electronics Manufacturing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Nearshoring by EU OEMs | +1.20% | Germany and neighboring EU manufacturing hubs | Medium term (2-4 years) |

| Rising Demand for PCB Miniaturisation | +0.90% | Germany and cross-border medical clusters in Netherlands and Austria | Long term (≥ 4 years) |

| Mandatory EU Battery Regulation Compliance | +0.80% | EU wide with concentration in Germany, France, Sweden | Short term (≤ 2 years) |

| Digitisation of Factory-Floor Operations | +0.70% | Germany and wider Northern and Western Europe | Medium term (2-4 years) |

| Government Incentives for Semiconductor Reshoring | +1.00% | Germany, Ireland, France | Long term (≥ 4 years) |

| Surge in E-Mobility Power Electronics | +1.30% | Germany and Central European automotive corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Nearshoring by EU OEMs

European vehicle and industrial brands are moving more electronics assembly back inside the bloc to mitigate supply-chain shocks and to meet tough traceability rules. Volkswagen, BMW, and Stellantis signed USD 4.6 billion of multi-year contracts with German and Czech EMS firms from January 2024 to September 2025, redirecting work from China and Malaysia.[1]Volkswagen AG, “Annual Report 2024,” VOLKSWAGENAG.COM The push focuses on speed and compliance, not labour arbitrage, because German wages are still 40% higher than in Poland. Proximity to design hubs in Bavaria and Baden-Württemberg trims engineering-change lead times by up to 12 weeks while also aligning final products with the EU Battery Regulation that mandates digital product passports from February 2027.[2]European Commission, “EU Battery Regulation (EU) 2023/1542,” EUROPA.EU Nearshoring shields OEMs from tariff risk after the European Commission imposed provisional anti-subsidy duties of up to 38% on Chinese battery-electric vehicles in mid-2024.[3]European Commission, “EU Battery Regulation (EU) 2023/1542,” EUROPA.EU German EMS partners that can provide co-located engineering and zero-defect power modules are therefore in high demand.

Surge in E-Mobility Power Electronics

Battery-electric vehicle output across the EU hit 1.9 million units in 2025, 22% higher than 2024, almost doubling the semiconductor content of each vehicle. Power inverters, on-board chargers, and DC-DC converters require a sintered-silver die attach capable of 175 °C junction temperatures.[4]Infineon Technologies AG, “Power Semiconductor Technology for Electric Vehicles,” INFINEON.COM The International Energy Agency expects Europe to hold 28% of global BEV sales by 2030, translating to an 18% CAGR in power-module assembly. German plants are investing in plasma-cleaning and void-free reflow to achieve sub-3-ppm defect levels for silicon-carbide modules. Commercial vehicle electrification adds another layer of demand as Daimler Truck ordered 15,000 inverter units from domestic EMS partners in 2025.

Government Incentives for Semiconductor Reshoring

The European Chips Act earmarks USD 47 billion to double Europe’s semiconductor share to 20% by 2030, with Germany receiving USD 21.8 billion. A large slice targets advanced packaging lines, a niche where German EMS firms already operate ISO Class 5 cleanrooms. Intel is spending USD 32.7 billion on fabs in Magdeburg and USD 545 million on an advanced-packaging test center in Dresden due by late 2026, creating spill-over demand for wafer-level fan-out and chaplet assembly. The German Ministry of Education and Research’s Microelectronics Germany 2027 program funds up to 40% of capex for EMS plants that install chip-on-wafer-on-substrate tools. Early beneficiaries are already adding gallium-nitride and silicon-carbide lines for power and RF applications.

Digitisation of Factory-Floor Operations

Germany leads Europe in Industry 4.0 adoption, with 68% of EMS sites running integrated MES, ERP, and IoT sensor networks by 2024, versus 41% in Poland. Siemens’s Amberg plant improved overall equipment effectiveness by 12% in two years after deploying AI anomaly detection. The German Engineering Federation calculates that digitized factories cut unplanned downtime by 25% and quality escapes by 18%. Automated traceability also eases ISO 13485 and IATF 16949 audits, slicing 200 hours per certification cycle. These productivity and compliance gains help offset wage inflation and support premium pricing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled Labour Shortage in High-Precision Assembly | -0.60% | Germany with hot spots in Bavaria, Baden-Württemberg, Saxony | Long term (≥ 4 years) |

| Volatility in Copper and Rare-Earth Prices | -0.50% | Global with pronounced effect on German EMS under fixed-price contracts | Short term (≤ 2 years) |

| Intensifying Price Competition from CEE Hubs | -0.40% | Germany vs Poland, Czech Republic, Hungary, Romania | Medium term (2-4 years) |

| Long Qualification Cycles in Medical and Automotive | -0.30% | Germany and other EU certified facilities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled Labour Shortage in High-Precision Assembly

Germany faces 47,000 unfilled electronics-technician and SMT-operator positions as of December 2025, a 23% jump in two years. The shortage is most acute in Bavaria and Baden-Württemberg where automotive and medical clusters overlap, inflating hourly wages by 8.4% in 2024 and another 6.1% in 2025. Apprenticeships and university partnerships exist yet yield technicians only after three to four years, creating a structural deficit that pushes EMS providers toward collaborative robots and automated inspection. Manual intervention remains unavoidable for low-volume, high-mix medical and aerospace jobs, so labour scarcity will persist through the decade.

Volatility in Copper and Rare-Earth Prices

Material inputs make up as much as 18% of EMS cost of goods, and prices swing sharply. Copper averaged USD 9,200 per metric ton in H1 2025, 14% above the 2020-2024 mean. Neodymium oxide fluctuated between USD 68,000 and USD 94,000 per metric ton in 2025 as China adjusted export quotas. Because many German EMS contracts lock pricing a year in advance, sudden commodity spikes compress margins or trigger difficult renegotiations. The International Energy Agency expects rare-earth demand for clean-energy technologies to triple by 2030, implying persistent cost volatility. Providers are therefore adopting dynamic hedging and cost-pass-through clauses in new agreements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Services Type - Turnkey Assembly Accelerates System Integration

The services-type landscape shows that PCB assembly generated 42.68% of 2025 revenue, yet electromechanical assembly and box build are pacing ahead with a 5.78% CAGR that lifts their portion of the Germany EMS market. Box build commands higher margins because it bundles enclosure assembly, cable harnessing, firmware loading, and functional test, tasks that must remain close to engineering teams and that meet sector-specific standards such as IEC 60601 or ISO 26262. This shift became visible when Volkswagen consolidated fourteen Tier-2 suppliers into three full-system integrators for its MEB battery platform, boosting value capture by 40% per unit.

Providers are also scaling engineering services and rapid prototyping, which compress product development by up to ten weeks while de-risking later manufacturing. Logistics services stay largely commoditized, although firms with bonded warehouses defer value-added tax for cross-border customers. Other EMS activities such as repair, refurbishment, and recycling gain traction as the EU Circular Economy Action Plan extends producer responsibility. Overall, deeper vertical integration positions domestic firms to defend pricing power as commodity PCB assembly migrates to lower-cost regions.

By Business Model - Hybrid and Turnkey Capture Design Complexity

Germany EMS Market Contract manufacturing still carries 63.77% of 2025 revenue, yet hybrid and turnkey engagements are growing at 5.28% a year, moving the Germany electronics manufacturing services market toward shared design and sourcing accountability. OEMs with limited electronics expertise lean on EMS partners for early design-for-manufacturability reviews, regulatory paperwork, and component life-cycle management. In turnkey deals, the EMS company procures the full bill of materials and absorbs inventory risk, offsetting that exposure through higher service fees and faster time to market.

Flex disclosed that turnkey contracts made up 58% of its European sales in fiscal 2024, generating gross margins three to five points above legacy build-to-print work. Vertical moves show a similar trend: Katek bought an FPGA design house in March 2025 to integrate firmware development with board fabrication. These steps reflect the complexity of chaplet architectures and system-in-package designs where PCB stack-ups, RF shielding, and thermal paths are co-optimized from day one.

By Manufacturing Process - Advanced Packaging Meets Chiplet Demand

Surface-mount technology provided 51.29% of 2025 process revenue, yet advanced packaging and hybrid flows post the fastest expansion at 5.55% through 2031. The growth links to chiplet architectures that combine multiple dies on a silicon interposer or organic substrate, popularized by Intel’s Foveros and AMD’s 3D V-Cache. German EMS plants are installing ISO Class 5 cleanrooms, five-micron placement tools, and thermal-compression bonders to perform wafer-level fan-out and through-silicon-via assembly. Zollner Elektronik’s new line in Zandt, financed partly by Chips Act subsidies, targets automotive lidar modules integrating MEMS mirrors with ASIC controllers.

Hybrid processes merge SMT, wire bonding, and encapsulation in one workflow, perfect for silicon-carbide power modules on direct-bonded-copper substrates. Equipment orders illustrate the strategic pivot: SEMI recorded a 34% jump in European advanced-packaging tool installations in 2024, the world’s highest regional growth rate. Through-hole technology, in the Germany electronics manufacturing services market, keeps shrinking except for niche industrial and defense programs that require high-current connectors.

By End User - Automotive Electronics Outpaces Industrial Mainstay

Industrial automation, building controls, and renewable-energy inverters delivered 31.44% of 2025 revenue, leveraging Germany’s heritage with Siemens, ABB, and Schneider Electric. Automotive electronics, however, is on track for a 5.93% CAGR that will raise its weight in the Germany EMS market. Each battery-electric vehicle contains roughly USD 1,200 of electronics, triple an internal-combustion car, shifting content toward integrated power modules and domain controllers. Tier-1s rely on EMS partners for zero-defect SiC inverters, radar modules, and battery management systems.

Medical devices remain a high-margin niche because ISO 13485 and EU MDR keep barriers to entry high. Communication infrastructure stays steady on the back of 5G small-cell rollouts, though pricing pressure is intense. Consumer electronics and mobile devices show limited domestic volume since high-volume assembly sits in Asia. Aerospace, defense, and scientific instrumentation offer low-volume, high-mix work where German security clearances and engineering colocation differentiate providers.

Geography Analysis

Germany EMS market remains the anchor of European electronics manufacturing services, thanks to its automotive clusters, engineering universities, and advanced vocational system. Bavaria and Baden-Württemberg together generated roughly 54% of national EMS revenue in 2025, supported by Munich, Stuttgart, and Ingolstadt design hubs. Saxony is the fastest-growing state as Intel and GlobalFoundries expand Dresden’s semiconductor and advanced-packaging ecosystem, creating adjacent EMS demand.

EU policy bolsters this position. Chips Act funding, the Battery Regulation, and circular economy rules all steer contracts toward providers that can guarantee EU origin, traceability, and recycling. Neighbouring Poland, Czech Republic, and Hungary lure high-volume consumer-electronics programs with lower labour costs, yet they lack the ISO 13485 and automotive safety certifications that German plants routinely hold. The Netherlands and Austria service specialized medical clusters, while France and Sweden redirect automotive contracts to Germany for battery-passport compliance.

Competition from Asian giants persists for commodity PCB assembly yet is losing share in high-value segments. Geopolitical uncertainty, tariff threats, and long shipping lead times convince many European OEMs to pay a premium for regional sourcing. With USD 21.8 billion of German Chips Act funds flowing through 2027, advanced-packaging and system integration will concentrate even more in the country, cementing its role as Europe’s high-value EMS hub.

Mordor Intelligence provides coverage of the electronics manufacturing services market across other key regional markets, including Europe, Asia, and North America, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to United Kingdom, France, Vietnam, United States, India, and Thailand incorporating local coverage and market participation, as required.

Competitive Landscape

The market is moderately fragmented. The five largest providers, namely Zollner Elektronik, Katek, BMK Group, TQ-Group, and Jabil, controlled roughly 32% of 2025 revenue, leaving space for midsize specialists. Domestic players leverage proximity, ISO 13485 and IATF 16949 certifications, and cleanroom capacity to defend premium pricing in low-volume, high-mix production. Global giants like Flex, Foxconn, and Sanmina maintain local plants mainly to serve automotive and industrial customers that demand EU-based supply chains.

Strategic moves revolve around three themes. First, technical capability: Zollner added wafer-level fan-out tools, Jabil installed advanced-packaging lines for radar modules, and Katek expanded cleanroom space for medical devices. Second, regulatory compliance: TQ-Group secured ISO 13485, and Sanmina achieved ASIL-D certification for automotive safety. Third, supply-chain resilience: Foxconn announced a USD 164 million investment in Brandenburg to shorten delivery loops for electric-vehicle power electronics.

White-space opportunities include rapid prototyping for quantum-sensor modules, refurbishment programs mandated by the Ecodesign for Sustainable Products Regulation, and aerospace avionics requiring security clearances. Consortia such as Silicon Saxony pool cleanroom assets and share metrology equipment, allowing mid-tier providers to bid on chiplet assembly without incurring full capex. Patent activity underscores the push toward automation, with Lacroix Electronics filing a machine-vision system that trims manual inspection time by 60%.

Germany Electronics Manufacturing Services Industry Leaders

Zollner Elektronik AG

BMK Group GmbH & Co. KG

Katek SE

TQ-Group GmbH

Flex Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Katek SE completed a EUR 35 million (USD 38 million) expansion at its Grassau site, adding 1,200 square meters of ISO Class 7 cleanrooms for implantable cardiac monitors and insulin-pump controllers.

- December 2025: Zollner Elektronik AG won a five-year, EUR 280 million (USD 305 million) contract to assemble battery management systems for a German automotive Tier-1, embedding 12 resident engineers at the customer’s Stuttgart R and D center.

- November 2025: Jabil Inc. invested USD 22 million in advanced packaging tools at its Friedberg facility, achieving ISO 26262 ASIL-D certification for automotive radar modules.

- October 2025: Flex Ltd. formed a joint venture with Siemens AG to blend digital twin software with manufacturing execution, targeting 30% lower downtime and 8% higher first-pass yield across European plants.

Germany Electronics Manufacturing Services Market Report Scope

The Germany Electronics Manufacturing Services Market Report Is Segmented by Services Type (Electronic Manufacturing Services, Engineering Services, Test and Development, Logistics, and Others), Business Model (Contract Manufacturing, Original Design Manufacturing (ODM), Hybrid / Turnkey / Other Business Models), Manufacturing Process (Surface Mount Technology (SMT), Through-Hole Technology (THT), and Advanced Packaging / Hybrid Processes), End User (Mobile Devices (Smartphones and Tablets), Consumer Electronics, Computer (PCs/Desktop/Laptops), Industrial, Automotive, Communication, Lighting, Medical, Others), With All Forecasts Expressed in USD Value.

| Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | |

| Prototyping | |

| Other Electronic Manufacturing Services | |

| Engineering Services | |

| Test and Development Implementation | |

| Logistics Services | |

| Other EMS Type |

| Contract Manufacturing (CM) |

| Original Design Manufacturing (ODM) |

| Hybrid / Turnkey / Other Business Models |

| Surface Mount Technology (SMT) |

| Through-Hole Technology (THT) |

| Advanced Packaging / Hybrid Processes |

| Mobile Devices (Smartphones and Tablets) |

| Consumer Electronics |

| Computer (PCs/Desktop/Laptops) |

| Industrial |

| Automotive |

| Communication |

| Lighting |

| Medical |

| Other End-users |

| By Services Type | Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | ||

| Prototyping | ||

| Other Electronic Manufacturing Services | ||

| Engineering Services | ||

| Test and Development Implementation | ||

| Logistics Services | ||

| Other EMS Type | ||

| By Business Model | Contract Manufacturing (CM) | |

| Original Design Manufacturing (ODM) | ||

| Hybrid / Turnkey / Other Business Models | ||

| By Manufacturing Process | Surface Mount Technology (SMT) | |

| Through-Hole Technology (THT) | ||

| Advanced Packaging / Hybrid Processes | ||

| By End-user | Mobile Devices (Smartphones and Tablets) | |

| Consumer Electronics | ||

| Computer (PCs/Desktop/Laptops) | ||

| Industrial | ||

| Automotive | ||

| Communication | ||

| Lighting | ||

| Medical | ||

| Other End-users |

Key Questions Answered in the Report

What is the current value of the Germany electronics manufacturing services market?

The market stands at USD 22.46 billion in 2026 and is on a 4.71% CAGR trajectory toward USD 28.26 billion by 2031.

Which services type is growing fastest?

Electromechanical assembly and box build are expanding at a 5.78% CAGR, outpacing the overall market due to OEM demand for turnkey system integration.

Why are hybrid and turnkey business models gaining traction?

They shift component sourcing, design validation, and inventory risk to the EMS partner, shortening time to market and supporting higher gross margins.

How is advanced packaging influencing German EMS providers?

Chiplet-based designs require ISO Class 5 cleanrooms and sub-micron placement, prompting significant capex backed by European Chips Act subsidies.

What is the biggest supply-side challenge?

A shortage of skilled SMT operators and precision assemblers, with 47,000 vacancies in late 2025, is forcing automation and wage hikes.

How concentrated is the competitive landscape?

The top five players account for roughly 32% of revenue, indicating moderate concentration with a score of 6 on a 110 scale.

Page last updated on: