Europe Electronic Manufacturing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

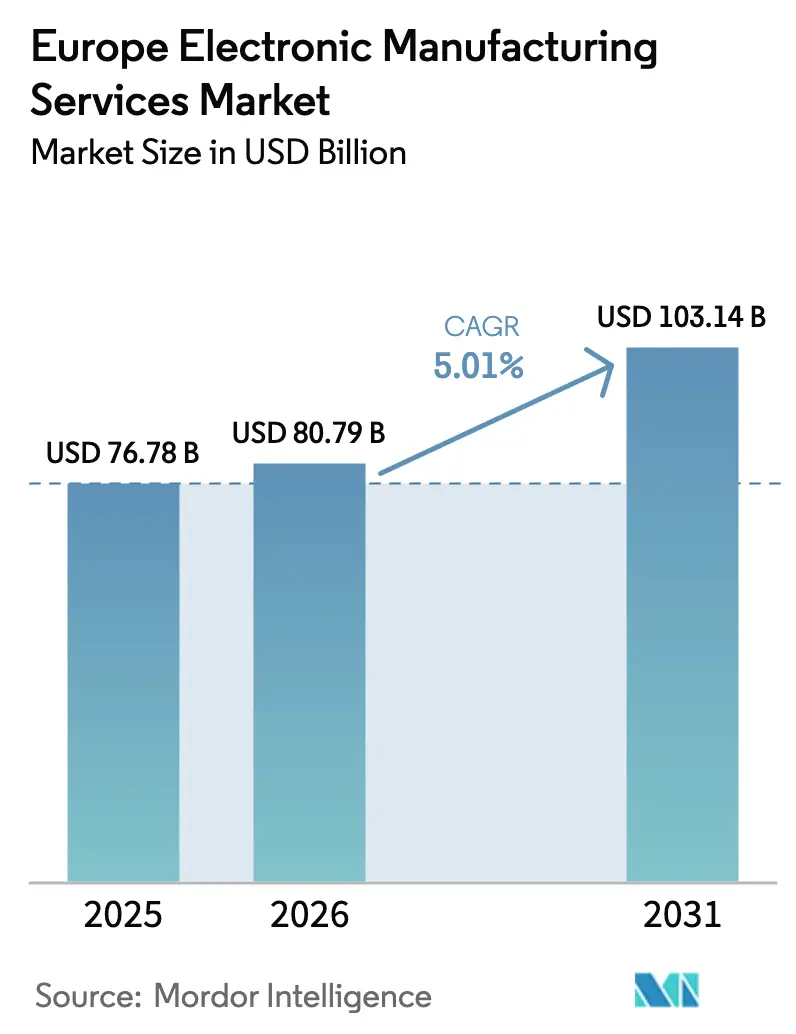

| Base Year Market Size (2025) | USD 76.78 Billion |

| Market Size (2026) | USD 80.79 Billion |

| Market Size (2031) | USD 103.14 Billion |

| Growth Rate (2026 - 2031) | 5.01% CAGR |

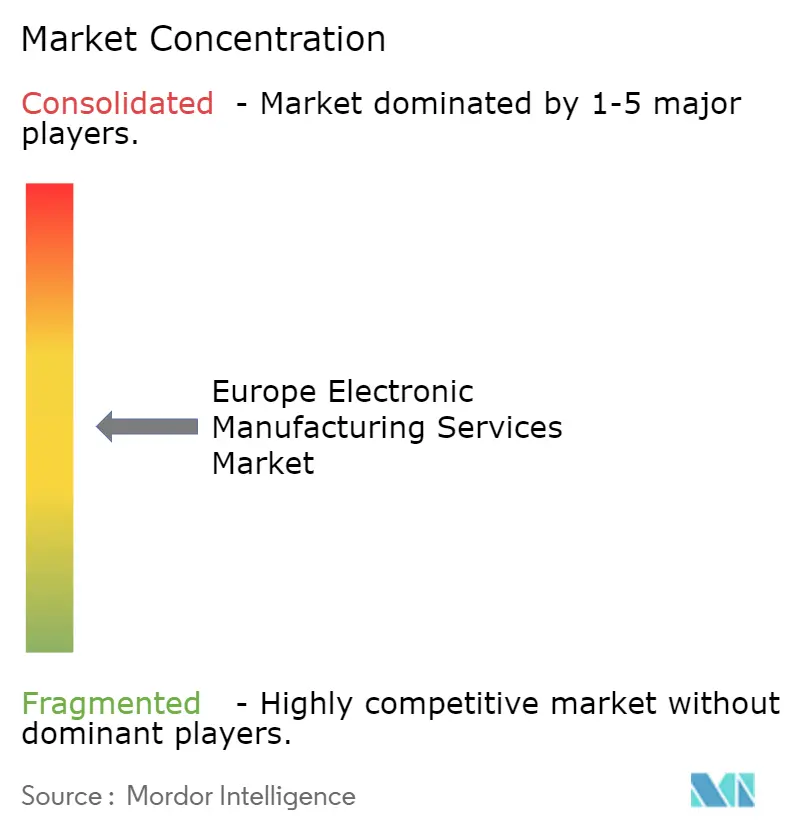

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Electronic Manufacturing Services Market Analysis by Mordor Intelligence

The Europe electronic manufacturing services market size is projected to be USD 76.78 billion in 2025, USD 80.79 billion in 2026, and reach USD 103.14 billion by 2031, growing at a CAGR of 5.01% from 2026 to 2031. The momentum of the Europe electronics manufacturing services market stems from legislation that prioritizes supply-chain transparency, mounting demand for local capacity in automotive, industrial, and medical verticals, and the ongoing relocation of high-mix, low-volume programs from Asia to compliant European plants. Contract manufacturers that can prove ISO 14001 alignment and Corporate Sustainability Reporting Directive readiness are securing multi-year frameworks, while providers lacking carbon-accounting systems are losing bids to rivals offering traceable, low-emission assembly. Near-shoring also shortens prototype cycles from eight to three weeks, an advantage that offsets labor premiums through faster design iterations and lower freight expense. Automation, collaborative robotics, and AI-driven optical inspection continue to trim direct labor content, narrowing the cost delta with Asia to roughly 20% for complex assemblies, down from 40% five years earlier.

Key Report Takeaways

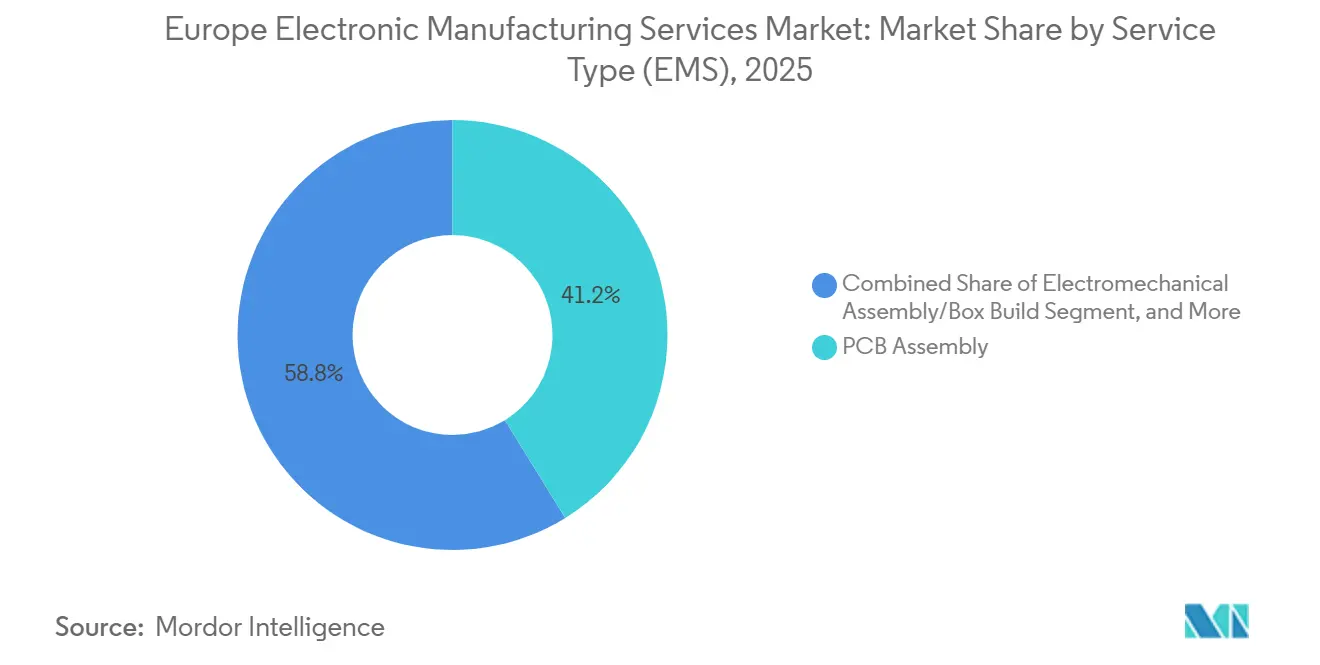

- By service type, PCB assembly accounted for 41.22% of the Europe electronic manufacturing services market size in 2025, while electromechanical box build is set to grow the fastest CAGR at 6.11% to 2031.

- By business model, contract manufacturing dominated with 63.71% of Europe EMS market revenue share in 2025; hybrid and turnkey models will register the highest CAGR at 5.67% through the forecast horizon.

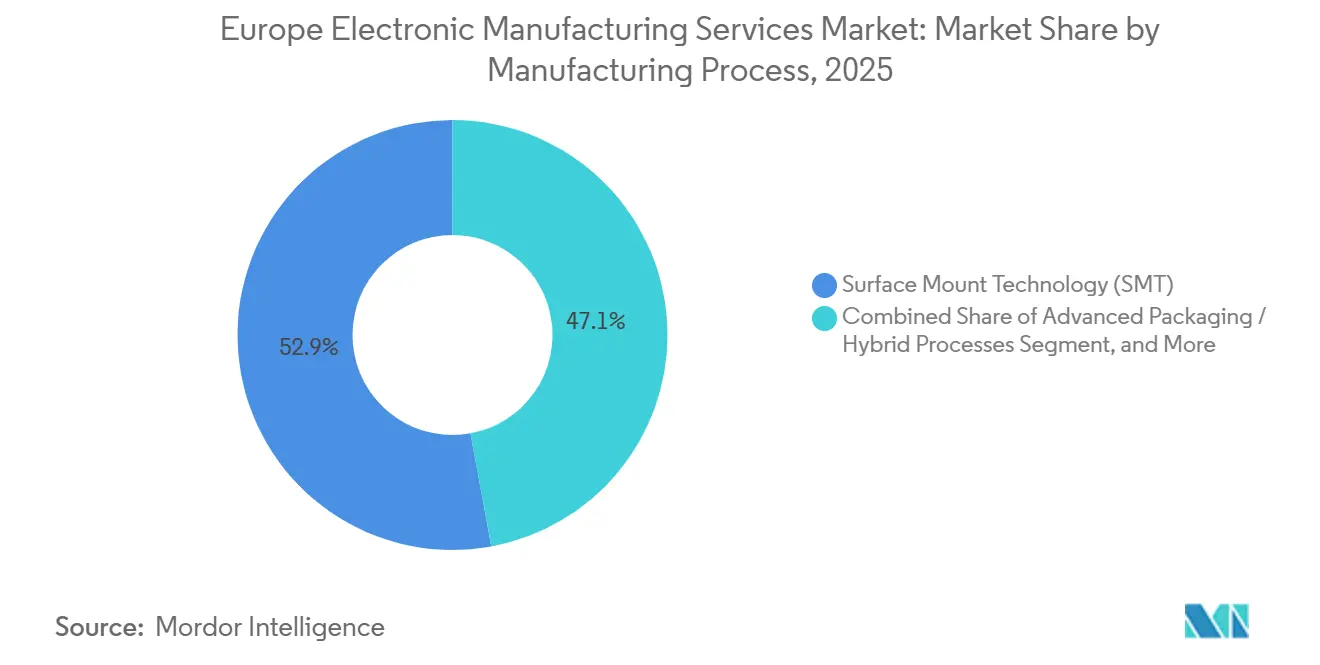

- By manufacturing process, surface-mount technology led with 52.89% of 2025 revenue, yet advanced packaging and hybrid processes are forecast to rise at a 5.71% CAGR through 2031.

- By end-user, industrial electronics held 37.83% of the Europe electronics manufacturing services (EMS) market share in 2025, whereas automotive applications are projected to expand at a 6.89% CAGR through 2031.

- By geography, Germany retained 31.24% of 2025 revenue of Europe EMS market, and the United Kingdom is poised for the quickest expansion at a 5.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide industry scale is not derived from any single region but from the combination of national and regional inputs. The electronics manufacturing services market size of Mordor Intelligence integrates these into one global valuation.

Europe Electronic Manufacturing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising outsourcing of electronics production by European OEMs | +1.2% | Germany, France, Italy, spillover to Poland and Czech Republic | Medium term (2-4 years) |

| Surge in automotive electronics demand (EVs, ADAS) | +1.5% | Germany, United Kingdom, Sweden, expanding to Hungary and Slovakia | Long term (≥ 4 years) |

| Growth of high-mix, low-volume industrial and medical devices | +0.8% | Germany, Switzerland, Netherlands, Nordic countries | Medium term (2-4 years) |

| EU Battery-Booster incentives for local BMS and power electronics | +0.7% | Germany, France, Poland, with pilot projects in Spain and Portugal | Short term (≤ 2 years) |

| Near-shoring triggered by supply-chain security legislation | +1.0% | Pan-European, strongest in Germany, France, Benelux | Short term (≤ 2 years) |

| CSRD-driven demand for low-carbon EMS facilities | +0.5% | Germany, Netherlands, Nordic countries, expanding to Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Outsourcing of Electronics Production by European OEMs

OEMs are channeling capital away from in-house lines toward software and electrification, pushing complex board population and box build into the hands of contract partners that already meet ISO 13485 and IPC standards. Siemens’ 2025 divestiture of its Amberg PCB operation and Bosch’s deeper collaboration with Zollner typify the transition, allowing manufacturers to release cash tied up in surface-mount lines and reflow ovens.[1]Siemens AG, “Annual Report 2025,” siemens.com Outsourcing penetration in Europe climbed to 38% in 2025 yet still trails Asia, implying runway for the Europe electronics manufacturing services market to convert additional captive plants. Providers able to co-locate engineering with manufacturing speed revisions from prototype to pilot in under a week, a cycle that captive plants rarely match. The trend is most pronounced in medical and industrial programs, where compliance and revision-control overhead favor specialist EMS partners.

Surge in Automotive Electronics Demand

Each battery electric vehicle embeds three to five times more PCB area than its combustion predecessor, and Europe’s legal green-light for Level-3 autonomous functions is adding lidar, radar, and high-compute domain controllers.[2]European Automobile Manufacturers’ Association, “Electric Vehicle Production Statistics,” acea.auto Volkswagen PowerCo’s BMS co-development with Kontron and widespread adoption of 48-volt architectures increase silicon-carbide and gallium-nitride module demand. EMS sites that master flip-chip and wire-bond assembly under automotive-grade thermal cycling secure higher-margin content and long contracts. As Tier-1 suppliers push software-defined vehicles, they rely on EMS partners to iterate hardware every 18 months. This momentum positions automotive as the fastest advancing slice of the Europe electronic manufacturing services market through 2031.

Near-Shoring Triggered by Supply-Chain Security Legislation

The EU Supply Chain Due Diligence Directive imposes legal exposure on companies that cannot verify labor and environmental compliance across tier-2 suppliers.[3]European Commission, “Corporate Sustainability Reporting Directive, EU Supply Chain Due Diligence Directive,” eur-lex.europa.eu Flex’s EUR 120 million (USD 135.6 million) Althofen expansion illustrates how risk-adjusted total cost now favors continental manufacturing for regulated products. Poland, Czech Republic, and Hungary continue luring overflow programs with 9% to 15% corporate tax rates, slashing prototype lead times by up to 60% and trimming freight carbon footprints. While high-volume consumer devices remain Asia-bound, European EMS facilities now capture automotive radar modules, industrial IoT gateways, and class-II medical electronics where proximity outvalues labor savings. Accelerated feedback loops between OEM R&D and shop floor reduce iteration cycles, improving working capital efficiency for both parties.

CSRD-Driven Demand for Low-Carbon EMS Facilities

Scope 3 disclosure rules coming into force in 2026 compel OEMs to trace carbon intensity throughout their supply chains, elevating low-emission assembly lines to a procurement criterion. Scanfil’s rooftop-solar and heat-recovery retrofit cut grid draw by 35%, allowing it to guarantee sub-50 kilograms of CO₂ per finished unit, a threshold many Asian factories cannot document. Contracts now stipulate renewable energy usage and digital-twin traceability, essentially tying revenue to emissions profiles. Buyers also view electricity price volatility as a risk, favoring EMS partners that hedge with on-site generation. Consequently, sustainability credentials are shaping competitive dynamics inside the Europe electronics manufacturing services market as strongly as cost and lead-time metrics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher European labor and energy costs vs. Asia | -0.9% | Germany, France, Benelux, Nordic countries | Long term (≥ 4 years) |

| Ongoing component shortages and inventory risk | -0.6% | Pan-European, acute in automotive and industrial segments | Short term (≤ 2 years) |

| Skilled-labor gap in advanced SMT and automation | -0.5% | Germany, United Kingdom, France, expanding to Eastern Europe | Medium term (2-4 years) |

| Fragmented EU compliance burden for smaller EMS firms | -0.3% | Smaller firms in Southern and Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher European Labor and Energy Costs vs. Asia

Fully loaded German labor averages EUR 35 per hour (USD 39.6) against EUR 4 in Vietnam (USD 4.5), a gulf only partly bridged by robotics.[4]International Energy Agency, “European Electricity Prices and Industrial Competitiveness,” iea.org Industrial power in Germany cost EUR 0.18 per kWh (USD 0.20) during 2025, more than double Chinese rates, eroding margins on wave solder and selective-solder lines. Although automation trimmed direct labor minutes by 25%, amortization of robotics and inspection cameras keeps overhead high. Products that mandate European proximity, such as BMS modules subject to the Battery Regulation, survive the premium, but price-sensitive consumer gear does not. The imbalance caps the upper range of the Europe electronics manufacturing services market CAGR until energy-price convergence or more aggressive automation emerges.

Skilled-Labor Gap in Advanced SMT and Automation

Germany recorded 60,000 unfilled electronics-technician posts in 2025, leaving pick-and-place lines idle despite backlogs.[5]German Federal Statistical Office, “Electronics Technician Employment Statistics,” destatis.de Programming 01005-size components on 40,000 CPH machines demands two years of experience, yet vocational enrollment keeps sliding as graduates favor software. Initiatives like Zollner’s augmented-reality training compressed certification to 16 months, but the scale of the shortage still constrains capacity expansion. Eastern European hubs face similar headwinds as unemployment hits multi-decade lows, forcing companies to recruit across borders and absorb language-integration costs. Persistent gaps in optical inspection and failure analysis prolong debug cycles, stretching lead times and tempering the ability of the Europe electronic manufacturing services market to absorb repatriated programs at the desired pace.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type (EMS): Box Build Expands as OEMs Exit Final Assembly

Europe electronic manufacturing services market size for PCB assembly commanded 41.22% of revenue in 2025, yet electromechanical box build is posting a 6.11% CAGR through 2031 as OEMs outsource enclosure integration, cable harnessing, and functional test benches. The migration frees OEM cash otherwise tied up in clean rooms and climate-controlled chambers, simultaneously reducing headcount dedicated to compliance audits. EMS providers capture additional margin by bundling firmware flashing and in-circuit verification, locking clients into multi-year agreements with penalty clauses for schedule slippage.

Industrial and medical programs fuel the surge because product lifecycles run a decade or more, and engineering change notifications often cascade deep into assembly. Box-build plants located near design centers in Germany and Switzerland complete engineering feedback loops in days, diminishing the impact of labor premiums by avoiding air freight on reworked sub-assemblies. The Europe electronic manufacturing services market gains further momentum as providers embed supply-chain orchestration software that pulls real-time component availability into scheduling, allowing split-lot kitting and concurrent engineering on low-volume runs. In turn, ODM-style engineering services grow alongside, enabling EMS firms to tweak board layouts for manufacturability without incurring redesign cycles that jeopardize regulatory approvals.

By Business Model: Hybrid and Turnkey Structures Shift Inventory Risk

Contract manufacturing held a 63.71% share of the Europe electronic manufacturing services market in 2025, reflecting entrenched consignment models where OEMs own parts and EMS firms charge labor fees. However, hybrid and turnkey contracts, projected at a 5.67% CAGR, are resetting liability frameworks by making EMS vendors responsible for component sourcing, obsolescence, and traceability. Smaller OEMs embrace the model because it taps the bulk-buying leverage of distributors like Arrow and Avnet, thereby insulating them from allocation shortages that defined 2024-2025.

Turnkey deals also empower EMS houses to swap pin-compatible alternates instantly, bypassing OEM engineering change orders and preventing production stops. Providers with deep balance sheets underwrite six months of safety stock, a strategy out of reach for niche players. Consequently, scale advantages accumulate, prompting consolidation as evidenced by Kontron’s integration of KATEK that merged design, procurement, and assembly inside a single ERP backbone. The Europe EMS market therefore witnesses a progressive concentration among operators capable of absorbing inventory carrying costs while maintaining just-in-time delivery metrics for critical medical and automotive projects.

By Manufacturing Process: Advanced Packaging Captures High-Value Modules

Surface-mount technology generated 52.89% of the Europe electronic manufacturing services market size in 2025 thanks to pervasive application across automotive, industrial, and consumer boards. Yet advanced packaging and hybrid processes are gaining a 5.71% CAGR, catalyzed by 77-gigahertz radar modules, implantable medical sensors, and gallium-nitride power stages that demand flip-chip, fan-out, and embedded-die capabilities. Investment barriers reach EUR 40 million (USD 45.2 million) for a class 10,000 clean room and thermocompression bonders, narrowing participation to a handful of Tier-1 EMS groups.

Mixed-technology boards complicate processing because through-hole components such as relays coexist with micro-BGAs, forcing wave-solder profiles to harmonize with reflow temperatures. That complexity elevates the value proposition of advanced-packaging lines able to consolidate die and passives into single modules, cutting board real estate by up to 30%. As Europe’s automotive OEMs push toward domain controller centralization, the Europe EMS market increasingly rewards suppliers that master heterogenous integration under AEC-Q100 stress parameters.

By End-User: Automotive Electrification Drives Fastest Growth

Automotive electronics are projected to rise at a 6.89% CAGR, the highest within the Europe electronic manufacturing services market, as battery packs, onboard chargers, and zonal controllers inflate per-vehicle electronic content. Industrial automation still represented 37.83% of 2025 revenue by virtue of Europe’s advanced factory-equipment base, and it remains resilient due to high-mix requirements that fit continental cost structures. Medical devices follow closely, undergirded by ISO 13485 compliance needs and proximity-driven field-failure analysis that Asian subcontractors cannot match without prohibitive logistics.

Conversely, communication infrastructure dipped in 2025 as telcos paused 5G densification, while consumer devices constitute less than 8% of regional EMS revenue because scale economies favor Asia. Lighting and computer segments exhibit replacement demand rather than breakout growth, but incremental smart-lighting controllers and ruggedized industrial PCs continue to contribute stable volumes. Across all verticals, the Europe electronics manufacturing services market benefits from OEM focus on core intellectual property, leaving material procurement, certification, and yield management to specialized partners.

Geography Analysis

Germany accounted for 31.24% of the Europe electronic manufacturing services market size in 2025, anchored by a vast automotive supply chain and Mittelstand EMS specialists situated in Bavaria and Baden-Württemberg. The Bavarian state’s EUR 2 billion (USD 2.26 billion) semiconductor-subsidy fund further cements a local cluster where fabs and assembly plants co-innovate on power-electronics modules for electric vehicles. Despite formidable labor and energy costs, Germany sustains high-value prototypes and advanced packaging, while volume runs of stable SKUs increasingly migrate to satellites in Hungary and Czech Republic that share quality systems and enterprise-wide MES dashboards.

The United Kingdom is forecast as the fastest-growing sub-region at a 5.62% CAGR, supplied by post-Brexit incentive packages that cover up to 30% of capital outlay for semiconductor packaging lines in Scotland and Wales. Accession to Horizon Europe restored collaborative R&D grants, prompting university-EMS consortia to pursue gallium-nitride device research, a move expected to seed future box-build contracts. Nissan’s Sunderland gigafactory and Jaguar Land Rover’s battery partnerships amplify local demand for battery-management boards, effectively pulling niche EMS capacity into the country.

Rest of Europe, which combines Poland, Czech Republic, Hungary, and the Nordics, collectively captures roughly 37% of the Europe electronics manufacturing services market. Poland’s Special Economic Zones levy a 9% corporate tax versus Germany’s 30%, enabling plants to absorb overflow demand without ballooning cost-of-sales for OEMs chasing mid-volume runs. Nordic countries lead on renewable-energy sourcing, giving their EMS firms a sustainability edge that resonates with CSRD-driven procurement checklists. Altogether, geographic diversification supports risk mitigation, currency hedging, and labor arbitrage, strengthening the overall resilience of European value chains.

Mordor Intelligence tracks the electronics manufacturing services market across other major regions such as Asia and North America, with additional country-level coverage spanning United Kingdom, Germany, France, Thailand, Singapore, South Korea, and Japan, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

The top five players, Foxconn, Flex, Jabil, Zollner, and GPV, held around 28% combined share in 2025 of Europe EMS market, indicating moderate concentration. Global Tier-1 competitors fund EUR 20 million (USD 22.6 million) to EUR 50 million (USD 56.5 million) automation rollouts, integrating machine-learning algorithms that adjust reflow profiles in real time to maintain first-pass yields above 99%. Regional champions like Scanfil and LACROIX differentiate through sustainability metrics, clinching multi-year automotive and medical contracts that explicitly reference low-carbon manufacturing thresholds rather than pure cost.

Eastern European disruptors such as BMK Group and Videoton pair EU compliance with labor rates 50% below Germany, enabling them to win volume contracts formerly booked in Shenzhen. Technology capabilities now operate as a market divider: providers with embedded design services and advanced packaging capture automotive radar modules, while conventional SMT houses gravitate toward industrial controllers and power supplies. Strategic vertical integration, exemplified by Kontron’s acquisition of KATEK, packages hardware, software, and cloud connectivity under one roof, reducing OEM vendor count and expediting time-to-market.

Standardization participation also plays a role; NOTE and Neways serve on IPC-A-610 revision committees, shaping criteria that later influence sourcing specifications. AI-driven optical inspection, collaborative robots, and digital twins represent the next battleground, as early adopters achieve labor compression and predictive maintenance that lifts gross margins three points above laggards. Over the forecast period, the Europe electronics manufacturing services market is expected to see further consolidation as capital intensity rises in tandem with regulatory demands.

Europe Electronic Manufacturing Services Industry Leaders

Flex Ltd.

Foxconn Technology Group

Jabil Inc.

Zollner Elektronik AG

Scanfil Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Flex announced a EUR 120 million (USD 135.6 million) expansion of its Althofen, Austria site to add 15,000 square meters of floor space and automotive advanced-packaging capacity.

- December 2025: Kontron completed integration of KATEK’s embedded division, realizing EUR 35 million (USD 39.6 million) in synergies via unified ERP and procurement platforms.

- November 2025: Scanfil signed a 5-year, EUR 180 million (USD 203.4 million) contract with a German Tier-1 to build BMS modules, including a dedicated clean room targeting ISO 26262 certification.

- October 2025: Jabil opened a 12,000 square-meter prototyping center in Kwidzyn, Poland, offering 48-hour PCB assembly for industrial and medical clients.

Europe Electronic Manufacturing Services Market Report Scope

The Europe Electronic Manufacturing Services Market Report is Segmented by Service Type (Electronic Manufacturing Services, Engineering Services, Test and Development Implementation Services, Logistics Services, and Other Service Types), Business Model (Contract Manufacturing (CM), Original Design Manufacturing (ODM), and Hybrid / Turnkey / Other Business Models), Manufacturing Process (Surface Mount Technology (SMT), Through-Hole Technology (THT), and Advanced Packaging / Hybrid Processes), End-user (Mobile Devices (Smartphones and Tablets), Consumer Electronics, Computer (PCs/Desktop/Laptops), Industrial, Automotive, Communication, Lighting, Medical, and Other End-users), and Geography (Germany, United Kingdom, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | |

| Prototyping | |

| Other Electronic Manufacturing Services | |

| Engineering Services | |

| Test and Development Implementation Services | |

| Logistics Services | |

| Other Service Types |

| Contract Manufacturing (CM) |

| Original Design Manufacturing (ODM) |

| Hybrid / Turnkey / Other Business Models |

| Surface Mount Technology (SMT) |

| Through-Hole Technology (THT) |

| Advanced Packaging / Hybrid Processes |

| Mobile Devices (Smartphones and Tablets) |

| Consumer Electronics |

| Computer (PCs/Desktop/Laptops) |

| Industrial |

| Automotive |

| Communication |

| Lighting |

| Medical |

| Other End-users |

| Europe | Germany |

| United Kingdom | |

| Rest of Europe |

| By Service Type | Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | ||

| Prototyping | ||

| Other Electronic Manufacturing Services | ||

| Engineering Services | ||

| Test and Development Implementation Services | ||

| Logistics Services | ||

| Other Service Types | ||

| By Business Model | Contract Manufacturing (CM) | |

| Original Design Manufacturing (ODM) | ||

| Hybrid / Turnkey / Other Business Models | ||

| By Manufacturing Process | Surface Mount Technology (SMT) | |

| Through-Hole Technology (THT) | ||

| Advanced Packaging / Hybrid Processes | ||

| By End-user | Mobile Devices (Smartphones and Tablets) | |

| Consumer Electronics | ||

| Computer (PCs/Desktop/Laptops) | ||

| Industrial | ||

| Automotive | ||

| Communication | ||

| Lighting | ||

| Medical | ||

| Other End-users | ||

| By Geography | Europe | Germany |

| United Kingdom | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How big is the Europe electronics manufacturing services market in 2026?

It stood at USD 80.79 billion in 2026 and is expected to hit USD 103.14 billion by 2031.

Which end-user segment grows fastest in European EMS?

Automotive programs, fueled by electrification and ADAS adoption, are projected to rise at a 6.89% CAGR through 2031.

Why are OEMs favoring turnkey contracts with EMS providers?

Turnkey deals transfer inventory risk and leverage EMS bulk-buying power, ensuring component availability during shortages and shortening lead times.

What impact does the CSRD have on EMS sourcing decisions?

Scope 3 reporting rules push OEMs toward EMS plants with documented low-carbon footprints and renewable energy sourcing.

Which geography leads the market, and which grows fastest?

Germany retains the largest share at 31.24%, while the United Kingdom is set for the quickest growth at 5.62% CAGR.

How concentrated is the competitive landscape?

The top five players command roughly 28% of revenue, reflecting moderate concentration and leaving room for regional specialists.

Page last updated on: