United Kingdom Electronics Manufacturing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

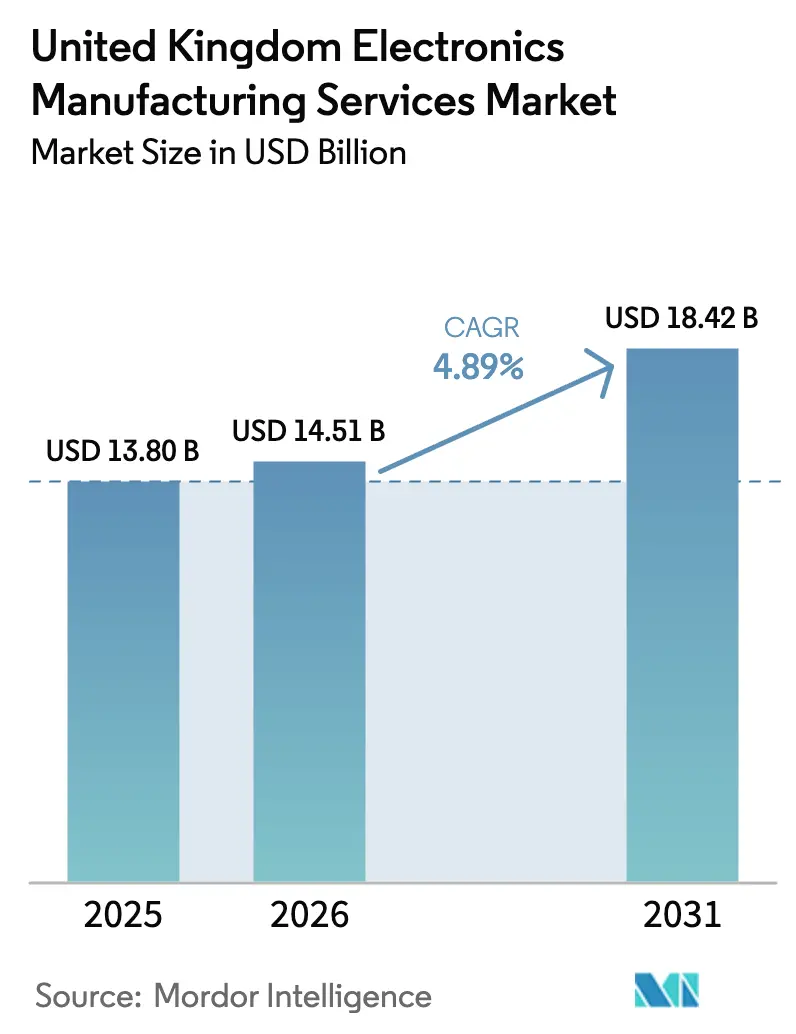

| Base Year Market Size (2025) | USD 13.80 Billion |

| Market Size (2026) | USD 14.51 Billion |

| Market Size (2031) | USD 18.42 Billion |

| Growth Rate (2026 - 2031) | 4.89% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Electronics Manufacturing Services Market Analysis by Mordor Intelligence

The United Kingdom Electronics Manufacturing Services Market size is projected to expand from USD 13.80 billion in 2025 and USD 14.51 billion in 2026 to USD 18.42 billion by 2031, registering a CAGR of 4.89% between 2026 to 2031.

Policy instruments that encourage reshoring, rising defense outlays, and a pivot toward higher-integration offerings are sustaining measured growth despite the nation’s structural cost premium. Demand for sovereign assembly tied to sixth-generation fighter and Type 26 frigate programs shields the sector from pure price competition, while government Made Smarter grants partially offset the 15-20% labour-cost gap versus Eastern Europe. At the same time, digital factory investments, such as AI-driven defect detection, are lifting first-pass yields and freeing capacity for complex, low-to-medium-volume programs. Finally, Extended Producer Responsibility rules are nudging service providers toward circular-economy models that integrate design-for-disassembly and reverse logistics.

Key Report Takeaways

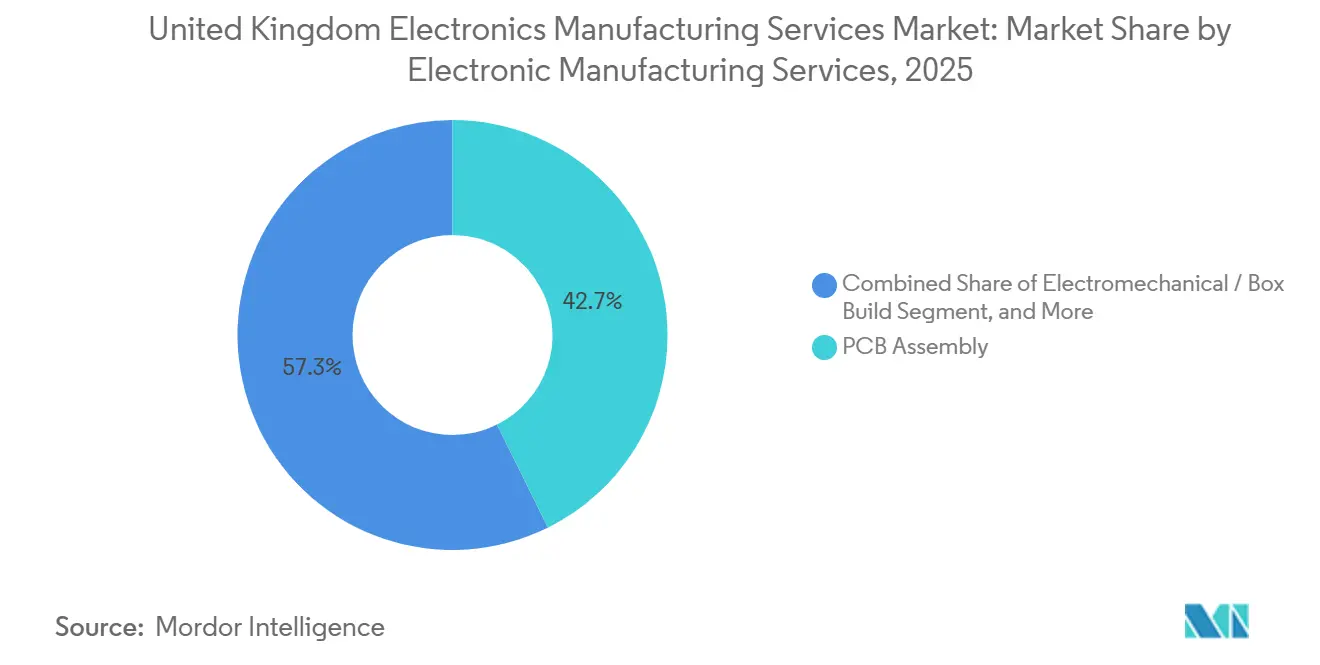

- By services type, PCB Assembly led with 42.68% revenue share in 2025, while Electromechanical Assembly and Box Build are forecast to grow at a 5.78% CAGR through 2031.

- By business model, Contract Manufacturing held 63.77% of the United Kingdom electronics manufacturing services market share in 2025, whereas Hybrid and Turnkey arrangements are advancing at 5.28% CAGR.

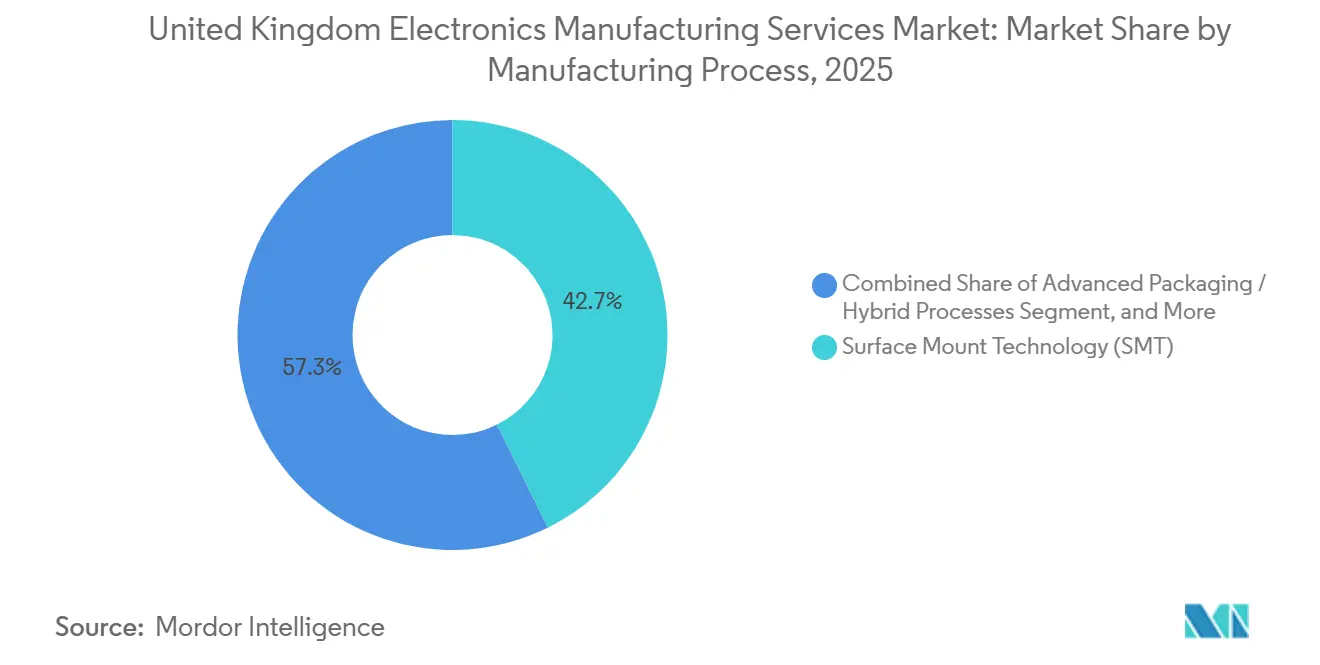

- By manufacturing process, Surface Mount Technology captured 51.29% share in 2025, yet Advanced Packaging and Hybrid Processes are poised to expand at a 5.55% CAGR to 2031.

- By end-user, industrial customers accounted for 31.44% of 2025 revenue, while automotive electronics is the fastest-growing segment at 5.93% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United kingdom operates as part of an interconnected international environment rather than as a self-contained country level unit. The electronics manufacturing services market research by Mordor Intelligence places together all major developments across the globe within that wider frame.

United Kingdom Electronics Manufacturing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Outsourcing Among UK OEMs | +1.20% | National, concentrated in South East England and West Midlands | Medium term (2-4 years) |

| Growth of the UK Aerospace and Defense Electronics Sector | +1.50% | National, with clusters in Lancashire, Hampshire, and Scotland | Long term (≥ 4 years) |

| Increasing Adoption of IoT-Enabled, High-Mix Manufacturing | +0.90% | National, early adopters in automotive and industrial hubs | Medium term (2-4 years) |

| Post-Brexit Reshoring Incentives and Made Smarter Grants | +0.80% | National, with higher uptake in Northern Powerhouse and Midlands Engine regions | Short term (≤ 2 years) |

| Sustainable Electronics and Circular-Economy Capabilities | +0.60% | National, driven by London and South East regulatory enforcement | Long term (≥ 4 years) |

| Demand for Low-Volume, High-Complexity Medical Prototyping | +0.70% | National, concentrated in Cambridge, Oxford, and Greater Manchester life-sciences clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Outsourcing Among UK OEMs

Capital constraints and mounting supply-chain complexity have prompted a clear shift toward external assembly partners. A Make UK survey showed that 68% of manufacturers intended to increase outsourcing within two years, a move most pronounced among mid-size firms that face rising energy and wage bills.[1]Chris White, “Manufacturing Outlook Q4 2024,” Make UK, makeuk.org These customers value flexible capacity and rapid new-product introduction cycles, particularly in industrial automation, where product life cycles now span four to six years. EMS providers that couple SMT flexibility with design-for-manufacturability services are capturing this wave, although aerospace and defense OEMs remain selective, restricting work to List X-approved facilities staffed by security-cleared personnel.

Growth of the UK Aerospace and Defense Electronics Sector

Defense spending is set to climb to 2.5% of GDP by 2030, unlocking an incremental GBP 10-12 billion (USD 13.7–16.4 billion) annually for platforms in which electronics often account for a quarter of total cost. Programs such as Tempest and Type 26 frigates mandate domestic assembly of radar, electronic-warfare, and avionics modules, insulating local providers from offshore competitors and sustaining gross margins near 20%.[2]UK Ministry of Defence, “Strategic Defence Review 2025,” gov.uk NATO surveillance projects and AUKUS commitments further embed British manufacturers in long-duration, security-critical supply chains, ensuring predictable loadings and encouraging investments in Class 3 workmanship capabilities.

Increasing Adoption of IoT-Enabled, High-Mix Manufacturing

High-mix, low-to-medium-volume work now represents roughly two-thirds of UK order books, up sharply from 2020. Made Smarter grants have underwritten IoT-enabled manufacturing execution systems, boosting real-time process visibility and cutting first-pass defects by as much as five percentage points for complex boards. Automotive electrification is a prime beneficiary, as domain-controller proliferation demands multiple firmware variants and tailored test protocols. The capital intensity of these digital upgrades, however, creates a two-tier landscape: larger providers amortize investments across many customers, while smaller shops must secure long-term commitments before taking the plunge.[3]Made Smarter Programme Office, “Technology Adoption Case Studies,” madesmarter.uk

Post-Brexit Reshoring Incentives and Made Smarter Grants

The Advanced Manufacturing Plan earmarked GBP 4.5 billion (USD 6.2 billion) through 2030, with electronics assembly singled out for grant preference. Defense and medical programs have already migrated final build stages back to British soil to meet security and compliance rules. Yet, for cost-sensitive consumer products, the 15-20% labour premium over Poland and Romania still outweighs grant benefits, limiting broad-based reshoring. Absent domestic semiconductor packaging incentives, UK EMS firms continue to import advanced packages from Asia, exposing them to freight delays and currency swings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Labor and Energy Costs Versus Offshore Locations | -1.10% | National, most acute in South East England | Long term (≥ 4 years) |

| Semiconductor Supply Chain Disruptions | -0.80% | National, affecting all segments | Short term (≤ 2 years) |

| Skills Shortage in Advanced Packaging Specialists | -0.60% | National, concentrated in high-tech manufacturing clusters | Medium term (2-4 years) |

| Compliance Costs Under UK Extended Producer Responsibility | -0.40% | National, with higher impact on consumer electronics segment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Labor and Energy Costs Versus Offshore Locations

Production-operator wages averaged GBP 16.50-22.00 (USD 22.6-30.1 per hour) per hour in 2025, a 15-20% premium to Polish rates and roughly double Romanian levels. Electricity bills, though off their 2022 peak, remain twice the 2019 baseline, forcing factories to schedule reflow ovens during off-peak windows. The combined burden trims gross margins by up to three percentage points relative to Eastern Europe, deterring bids for price-sensitive consumer and computing work. Automation can shave up to 18% of direct labour content, yet payback stretches to six years unless multi-year, volume-secured contracts are in place.

Semiconductor Supply Chain Disruptions

Although lead-time spikes subsided after 2022, sporadic shortages persisted through 2024, prompting EMS firms to carry 90-120 days of safety stock double pre-pandemic norms and driving inventory turns down to three or four times per year. The National Semiconductor Strategy focuses on design and compound substrates rather than large-scale fab capacity, leaving mainstream MCU and analog sourcing reliant on imports from Taiwan, South Korea, and the United States. Automotive programs have been hit hardest, with allocation of powertrain microcontrollers delaying vehicle launches and exposing contract manufacturers to liquidated-damages clauses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Services Type: Box-Build Complexity Boosts Margins

Electromechanical Assembly and Box Build in the UK EMS Market are expected to grow at a 5.78% CAGR through 2031, outpacing the broader United Kingdom Electronics Manufacturing Services (EMS) market. OEMs increasingly outsource complete system integration to reduce in-house complexity and accelerate launches. PCB Assembly, while delivering 42.68% of 2025 revenue, has become commoditized, keeping gross margins in the 8-12% band unless providers layer on rapid prototyping or design-for-manufacturability reviews. Prototyping itself, though modest in volume, commands fees 40-60% above production rates and acts as a funnel that locks in downstream orders.

The pivot to integrated builds favours providers with cross-disciplinary teams capable of coordinating enclosures, wire harnesses, firmware flashing, and system-level testing under one roof. Logistics add-ons such as direct-to-customer fulfilment now contribute an extra 3-5% of program value and deepen switching costs. As a result, service providers that market an end-to-end proposition are widening their margin gap over pure board stuffers and gaining share in the UK EMS Market.

By Business Model: Hybrid Engagements Gain Traction

Contract Manufacturing in the UK EMS Market still dominates with 63.77% share in 2025, reflecting its entrenched role in aerospace, defense, and industrial programs were OEMs guard intellectual property. Yet Hybrid and Turnkey frameworks are climbing at 5.28% CAGR as customers seek partners that will procure components, manage compliance, and hold inventory. Automotive Tier-1 suppliers, in particular, want single-point accountability across design and build, pushing EMS firms toward a broader engagement scope.

Turnkey demand rewards scale: providers must finance 60-90 days of inventory and withstand foreign-exchange swings on dollar-denominated components when sterling weakens. Smaller shops unable to accept that balance-sheet strain are retreating into niche verticals where deep engineering know-how offsets their purchasing disadvantage. As Hybrid contracts multiply, design services become a key differentiator, and firms that integrate schematic capture, PCB layout, and DFM reviews are winning a larger slice of the UK EMS Market.

By Manufacturing Process: Advanced Packaging Tackles Miniaturization

Surface Mount Technology accounted for 51.29% of 2025 revenue in the United Kingdom electronics manufacturing services market, yet Advanced Packaging and Hybrid Processes are forecast to register a 5.55% CAGR, reflecting mounting demand for system-in-package and flip-chip solutions. Automotive radar modules operating at 77-81 GHz and medical implantable both require ultra-short interconnects that standard SMT cannot deliver. Only a dozen UK EMS providers currently run the cleanrooms and die-attach gear needed for these builds, creating a margin-protected niche.

Through-Hole Technology usage continues in high-reliability defense and industrial controls, preserving the need for skilled manual soldering despite automation gains elsewhere. Skill shortages in advanced packaging remain acute a restraint noted earlier and are motivating companies to recruit overseas specialists or sponsor multi-year apprenticeships. Providers that successfully integrate substrate design with package assembly are commanding 20-30% price premiums and are reshaping competitive dynamics within the United Kingdom EMS market.

By End-User: Automotive Electrification Drives the Upside

Industrial customers delivered 31.44% of 2025 revenue, benefiting from local robotics and process-control footprints that require short lead times and custom configurations. Automotive electronics, however, is the growth engine, expanding at a 5.93% CAGR through 2031 as OEMs race toward the 2030 petrol and diesel phase-out. Nissan’s GBP 1.12 billion (USD 1.54 billion) Sunderland initiative and Jaguar Land Rover’s electrification roadmap translate into escalating demand for battery-management systems, on-board chargers, and power modules that must meet IATF 16949 standards.

Consumer electronics and mainstream computing segments continue to favour Asian assembly for cost reasons, limiting UK participation to ruggedized or specialized devices. Telecom infrastructure is seeing modest reshoring as operators diversify away from Chinese equipment, opening limited opportunities for local EMS firms. Medical electronics, though lower in volume, offers the highest gross margins often above 20% thanks to ISO 13485 documentation requirements and dual CE/UKCA conformity pathways. Defense electronics, bundled under “other” end-users, remains a stable anchor with multi-year contracts and cost-plus pricing, further underpinning the United Kingdom Electronics Manufacturing Services (EMS) Market.

Geography Analysis

England hosts the bulk of capacity, with clusters in the Southeast, West Midlands, and Northeast supporting automotive, industrial automation, and medical technology firms. The United Kingdom electronics manufacturing services market size derived from these English hubs is projected to expand steadily alongside Nissan’s Sunderland expansion and advanced-packaging investments in Newbury. Scotland specializes in defense and healthcare builds, exemplified by a USD 56.25 million cleanroom expansion in Livingston slated for completion in 2027, reinforcing the region’s high-reliability focus.

Wales contributes niche capability in compound semiconductors and RF assemblies, supplying aerospace radar and 5G infrastructure vendors. Northern Ireland, while smaller, offers cost-competitive labour and proximity to U.S. customers via trans-Atlantic logistics corridors, supporting select medical and industrial contracts. Throughout the home nations, Made Smarter grants and devolved government incentives are steering capital toward digital factory upgrades, ensuring that even smaller locales capture slices of the United Kingdom EMS market.

Cross-border trade dynamics remain critical. While Brexit introduced customs paperwork that adds one to two days to intra-company transfers, well-prepared EMS firms maintain dual warehousing strategies on the Continent to buffer lead-time variability. Sterling volatility influences component-cost budgeting, especially for providers billing customers in pounds but purchasing ICs in U.S. dollars. Successfully navigating these geographic and financial frictions is increasingly a prerequisite for securing long-term, turnkey contracts within the United Kingdom electronics manufacturing services market.

The electronics manufacturing services market is assessed by Mordor Intelligence through a multi-layered geographic lens, covering other regions such as Europe, Asia, and North America, along with detailed country-level analysis for Germany, France, Japan, United States, Mexico, and Malaysia.

Competitive Landscape

Global Tier-1 vendors Jabil, Flex, and Sanmina operate UK sites that focus on aerospace, defense, and healthcare assemblies where accreditation hurdles deter new entrants. Their scale supports AI-enabled inspection, inventory pooling, and currency hedging, allowing them to accept turnkey risk that smaller rivals avoid. Mid-tier specialists such as TT Electronics, Jaltek Systems, SMS Electronics, and Nemco leverage co-location with customer design teams and quick-turn agility, thriving in high-mix niches that reward responsiveness over purchasing clout.

Technology adoption is a key separator. Firms deploying digital twins and predictive analytics report first-pass yield gains of three to five percentage points on complex builds, translating into faster customer ramps and stronger renewal rates. Investments in advanced packaging act as another moat; Celestica’s Newbury facility, for instance, targets automotive radar and medical implantable segments in which only a handful of UK competitors possess equivalent cleanroom infrastructure.

Regulatory compliance shapes competition as well. Extended Producer Responsibility adds roughly 1% to operating costs, a burden easier to absorb for players with larger revenue bases. Meanwhile, skills shortages in die-bonding and RF test spur both wage inflation and poaching, advantages that Tier-1 multinationals counter with global mobility programs. Taken together, these factors produce a moderately fragmented but capability-stratified United Kingdom Electronics Manufacturing Services (EMS) Market.

United Kingdom Electronics Manufacturing Services Industry Leaders

Jabil Inc.

Flex Ltd.

Sanmina Corporation

Celestica Inc.

TT Electronics Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Jabil announced a GBP 45 million expansion of its Livingston, Scotland healthcare facility, adding ISO Class 7 cleanroom space for drug-delivery and diagnostic devices, with completion set for Q3 2027.

- November 2025: Flex secured a multi-year USD 180 million contract to build AI-accelerator server assemblies for a hyperscale cloud provider, splitting production between Hungary and the Czech Republic and influencing UK component sourcing.

- October 2025: TT Electronics acquired a UK power-electronics design consultancy for GBP 12 million to deepen design-for-manufacturability expertise in automotive and industrial programs.

- September 2025: Benchmark Electronics partnered with a UK defense prime to establish a secure manufacturing cell for classified avionics, with first production targeted for Q2 2026.

United Kingdom Electronics Manufacturing Services Market Report Scope

The United Kingdom Electronics Manufacturing Services Market Report is Segmented by Services Type (Electronic Manufacturing Services including PCB Assembly, Electromechanical Assembly/Box Build, Prototyping, and Other EMS; Engineering Services; Test and Development Implementation; Logistics Services; and Other EMS Type), Business Model (Contract Manufacturing, Original Design Manufacturing, and Hybrid/Turnkey/Other Business Models), Manufacturing Process (Surface Mount Technology, Through-Hole Technology, and Advanced Packaging/Hybrid Processes), End-user (Mobile Devices, Consumer Electronics, Computer, Industrial, Automotive, Communication, Lighting, Medical, and Other End-users including Aerospace and Defense), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | |

| Prototyping | |

| Other Services Type | |

| Engineering Services | |

| Test and Development Implementation | |

| Logistics Services | |

| Other Engineering Services |

| Contract Manufacturing (CM) |

| Original Design Manufacturing (ODM) |

| Hybrid / Turnkey / Other Business Models |

| Surface Mount Technology (SMT) |

| Through-Hole Technology (THT) |

| Advanced Packaging / Hybrid Processes |

| Mobile Devices (Smartphones and Tablets) |

| Consumer Electronics |

| Computer (PCs/Desktop/Laptops) |

| Industrial |

| Automotive |

| Communication |

| Lighting |

| Medical |

| Other End-users |

| By Services Type | Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | ||

| Prototyping | ||

| Other Services Type | ||

| Engineering Services | ||

| Test and Development Implementation | ||

| Logistics Services | ||

| Other Engineering Services | ||

| By Business Model | Contract Manufacturing (CM) | |

| Original Design Manufacturing (ODM) | ||

| Hybrid / Turnkey / Other Business Models | ||

| By Manufacturing Process | Surface Mount Technology (SMT) | |

| Through-Hole Technology (THT) | ||

| Advanced Packaging / Hybrid Processes | ||

| By End-user | Mobile Devices (Smartphones and Tablets) | |

| Consumer Electronics | ||

| Computer (PCs/Desktop/Laptops) | ||

| Industrial | ||

| Automotive | ||

| Communication | ||

| Lighting | ||

| Medical | ||

| Other End-users |

Key Questions Answered in the Report

How large is the United Kingdom electronics manufacturing services market today?

The United Kingdom electronics manufacturing services market size is valued at USD 14.51 billion in 2026 and is forecast to reach USD 18.42 billion by 2031.

What is driving growth in UK automotive electronics assembly?

Rapid electrification plans from OEMs such as Nissan and Jaguar Land Rover are lifting demand for battery-management systems, power modules, and domain controllers, pushing automotive segment revenue to a projected 5.93% CAGR.

Which service type is expanding quickest?

Electromechanical Assembly and Box Build are growing fastest at a 5.78% CAGR, as OEMs outsource full system integration to reduce internal complexity.

How are Extended Producer Responsibility rules affecting providers?

Compliance adds roughly 1% to operating costs, favoring EMS firms that offer design-for-disassembly and established take-back partnerships.

What advanced technologies are EMS companies adopting?

Leading firms deploy AI-driven defect detection, IoT-enabled process monitoring, and advanced packaging lines for system-in-package builds, enhancing yields and supporting miniaturization.

How fragmented is the competitive landscape?

The five largest players hold about 45% of revenue, leaving meaningful room for mid-tier specialists and niche advanced-packaging providers.

Page last updated on: