United States Electronics Manufacturing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

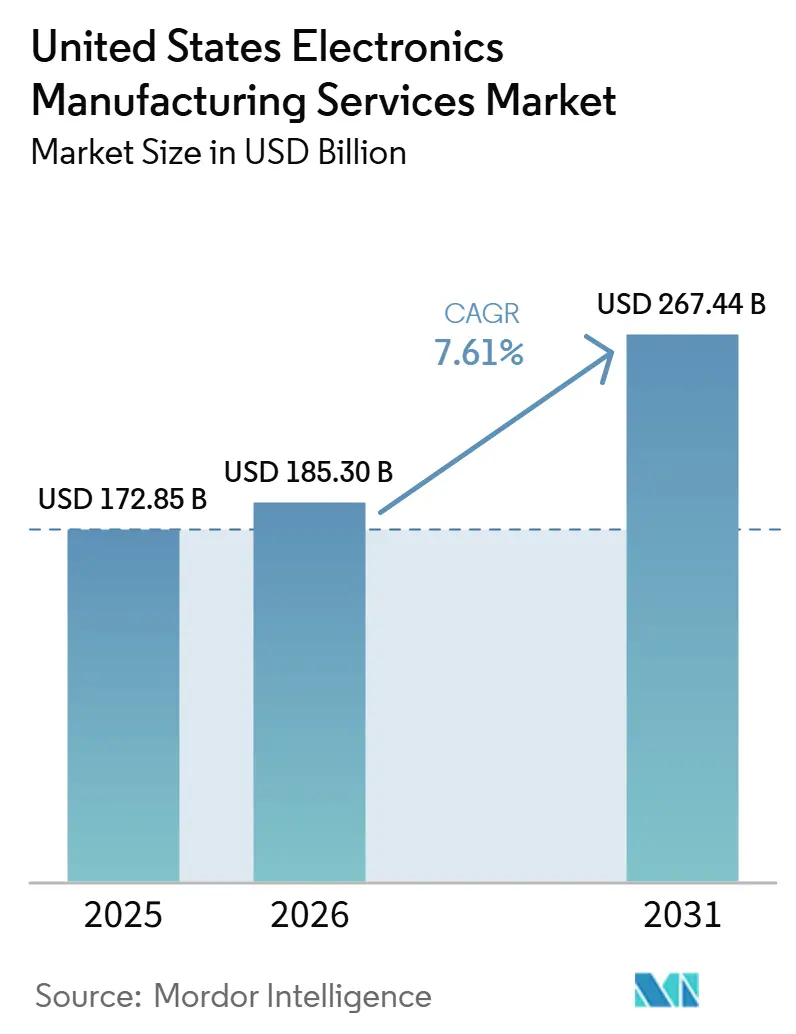

| Base Year Market Size (2025) | USD 172.85 Billion |

| Market Size (2026) | USD 185.30 Billion |

| Market Size (2031) | USD 267.44 Billion |

| Growth Rate (2026 - 2031) | 7.61% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Electronics Manufacturing Services Market Analysis by Mordor Intelligence

The United States Electronics Manufacturing Services Market size in 2026 is projected to expand from USD 172.85 billion in 2025 and USD 185.30 billion in 2026 to USD 267.44 billion by 2031, registering a CAGR of 7.61% between 2026 to 2031. Generative-AI hardware rollouts, electric-vehicle powertrain localization, and federal incentives such as the CHIPS and Science Act together underpin robust demand while simultaneously pushing assembly closer to domestic fabs. Tier-1 contract manufacturers are scaling advanced-packaging lines to capture chiplet integration programs, whereas mid-tier providers are differentiating through turnkey new-product introduction packages that compress prototype cycles. Persistent skilled-labor shortages and volatile passive-component pricing hinder margin expansion, spurring rapid adoption of collaborative robots and predictive-maintenance analytics across SMT lines. Contractual risk-sharing clauses for commodity parts and a pivot toward hybrid business models are emerging as the dominant responses to supply-chain volatility.

Key Report Takeaways

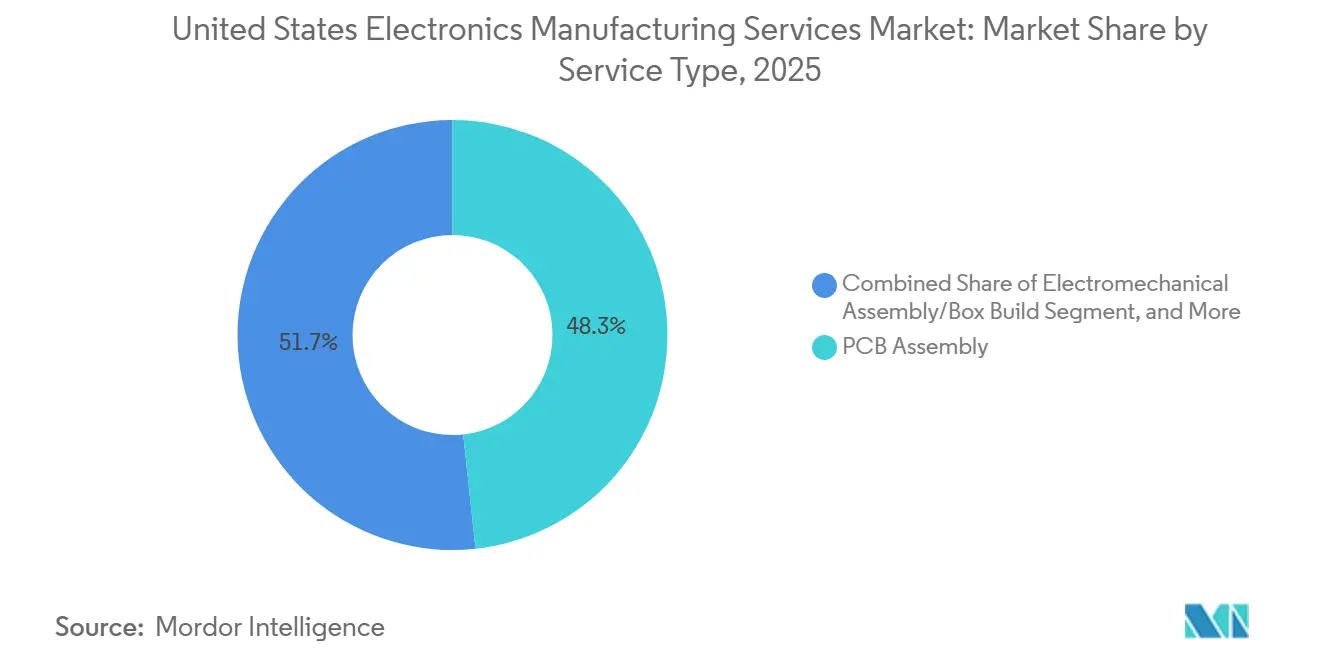

- By service type, PCB assembly sub-segment captured 48.29% of the United States electronics manufacturing services segment market share in 2025, while electromechanical assembly and box build are forecast to grow at a 8.65% CAGR through 2031.

- By business model, contract manufacturing held 71.93% of the US EMS Market revenue in 2025, yet Original Design Manufacturing (ODM) segment is expanding at a 9.97% CAGR to 2031.

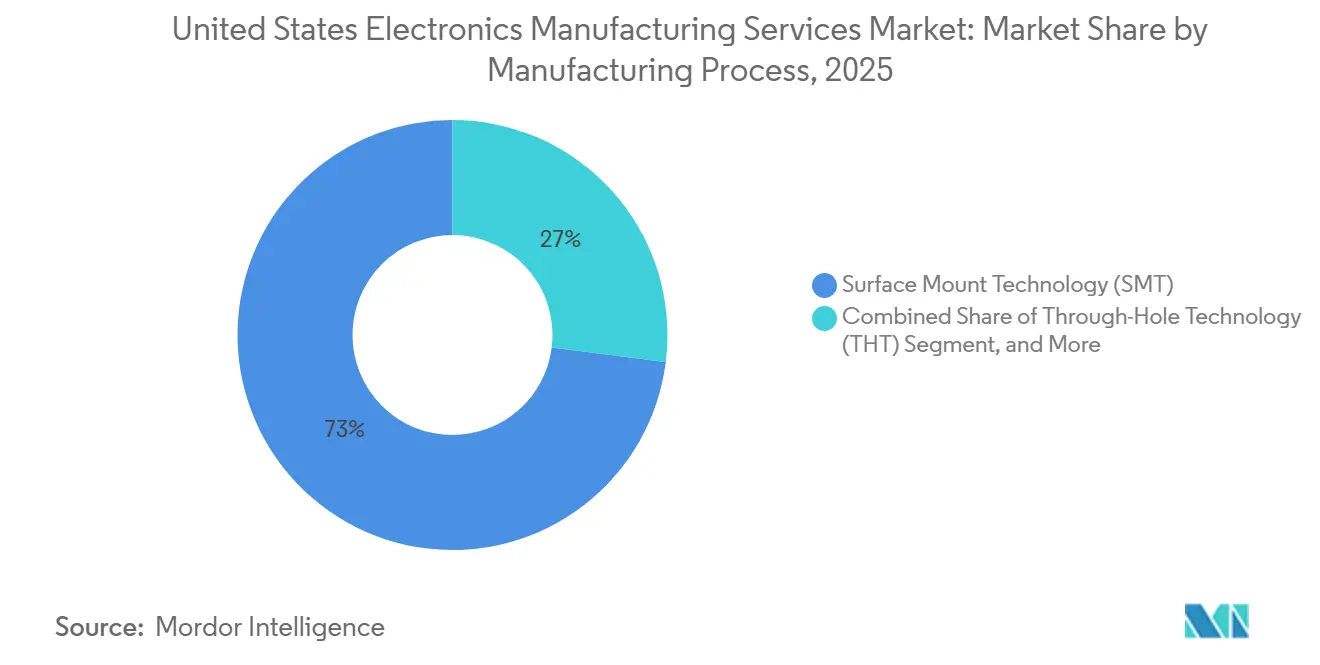

- By manufacturing process, surface-mount technology (SMT) accounted for 72.99% of the United States electronics manufacturing services market size in 2025, and advanced packaging and hybrid processes is advancing at a 9.67% CAGR through 2031.

- By end-user, communications segment led the United States electronics manufacturing services market with 25.17% of the market share in 2025, and is projected to post the fastest 10.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United states holds a defined position within a broader international distribution. The electronics manufacturing services market share data by Mordor Intelligence maps that allocation across all contributing countries and regions, globally.

United States Electronics Manufacturing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Reshoring Incentives and CHIPS Act Subsidies | +2.1% | Arizona, Texas, Ohio, New York | Medium term (2-4 years) |

| Generative-AI Hardware Boom Requiring High-Mix, High-Speed Assembly | +1.5% | California, Washington, Texas | Short term (≤ 2 years) |

| Automotive Electronics Pivot to EV Powertrains and ADAS | +1.3% | Michigan, Tennessee, Georgia, Texas | Medium term (2-4 years) |

| Rising Demand for Secure, ITAR-Compliant Defense Production | +1.1% | California, Virginia, Massachusetts, Arizona | Long term (≥ 4 years) |

| Medical-Device Miniaturization Driving Precision SMT Adoption | +0.9% | Minnesota, California, Massachusetts | Medium term (2-4 years) |

| Tier-2 and Tier-3 OEMs Outsourcing NPI for Time-to-Market Gains | +0.7% | California, Massachusetts, New York, Texas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Reshoring Incentives And CHIPS Act Subsidies

Federal incentives lowered the after-tax cost of new SMT and optical-inspection equipment by 25% under the Advanced Manufacturing Investment Credit, tipping marginal business cases into positive territory. Nearly all of the USD 39 billion CHIPS grant pool was committed by late 2025, including USD 6.6 billion to TSMC, USD 7.86 billion to Intel, and USD 4.74 billion to Samsung, each tied to co-located advanced-packaging capacity that depends on domestic EMS partners reported. Reshoring Initiative data confirm 244,000 U.S. manufacturing jobs announced in 2024, with computer and electronics accounting for 35%, the highest share since tracking began.[1]Reshoring Initiative, “2024 Data Report,” reshortenow.org Together, these levers shorten design-for-manufacturability loops by bringing assembly within a one-day truck haul of wafer output.

Medical-Device Miniaturization Driving Precision SMT Adoption

Implantable cardioverter defibrillators, insulin pumps, and portable ultrasound probes now rely on 01005 passives and µBGAs that demand placement tolerances tighter than 30 µm, prompting EMS providers to upgrade pick-and-place heads and x-ray inspection lines. ISO 13485 audits increasingly require traceability down to individual reel lots, pushing factories to deploy laser marking and automated data-capture systems that feed electronic device history records in real time. Providers with in-house micro-laser welding and conformal-coating booths win more contracts because they can ship fully finished assemblies ready for sterilization, trimming OEM validation cycles by several weeks. The net result is a steady inflow of low-volume, high-margin medical programs that reinforce demand for precision SMT capacity across U.S. campuses.

Tier-2 And Tier-3 OEMs Outsourcing NPI For Time-To-Market Gains

Mid-sized medical-device, industrial-IoT, and networking vendors are handing off new-product introduction to EMS partners so internal teams can focus on software and regulatory filings. Plexus reported double-digit growth in turnkey NPI revenue during fiscal 2025, with average prototype-to-pilot cycles shrinking below 12 weeks for Class II devices. Flex noted that three of its five largest industrial-IoT wins in calendar 2025 were structured as full-turnkey deals covering component sourcing, test-fixture design, and first-article validation. Jabil added that bundling design-for-manufacturability reviews with supply-chain orchestration cut change-order frequency by 30%, freeing engineering bandwidth at smaller OEMs and raising overall demand for domestic NPI slots.

Rising Demand For Secure ITAR-Compliant Defense Production

The Department of Defense’s Trusted Supplier rules bar foreign assembly for many avionics, radar, and communications systems, redirecting more than USD 2 billion in 2024 electronics contracts to domestic EMS plants certified for controlled unclassified information handling.[2]Department of Defense’s Trusted Supplier, " Trusted Supplier Program," defense.gov The eight-hub Microelectronics Commons network funds prototype lots that must remain onshore from wafer singulation through board test, guaranteeing a multiyear backlog for facilities with secure data rooms and Cybersecurity Maturity Model Certification Level 2. Sanmina, Jabil, and Celestica each expanded ITAR-cleared floor space in 2025, citing radar-signal processors and satellite-bus avionics as primary growth drivers.[3]Sanmina Corporation, “Annual Report (Form 10-K) for Fiscal Year 2024,” sanmina.com This captive pipeline insulates providers from consumer-electronics cycles and lifts the long-term growth outlook for secure U.S. electronics manufacturing services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Skilled-Labor Shortage in U.S. Electronics Assembly | -1.0% | Arizona, Texas, Ohio | Short term (≤ 2 years) |

| Margin Compression from Commodity Component Price Swings | -0.8% | National | Short term (≤ 2 years) |

| Fragile PCB Supply Chain for Advanced Substrates | -0.6% | National | Medium term (2-4 years) |

| Cyber-Security and IP Leakage Concerns Limiting Cloud-Based Collaboration | -0.5% | National, defense and medical corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Skilled-Labor Shortage In U.S. Electronics Assembly

In 2025, the Bureau of Labor Statistics highlighted a significant challenge in the electronics assembly sector, reporting a 12% vacancy rate. This shortage extended the median time-to-fill for IPC-A-610 Class 3 roles beyond 90 days.[4]U.S. Bureau of Labor Statistics, “Occupational Employment and Wage Statistics: Electronics Assemblers,” bls.gov As a result of these vacancies, wage premiums surged by 18% year over year. This wage spike had a tangible impact, trimming provider EBIT by approximately 120 basis points. Furthermore, the labor crunch has hastened the adoption of collaborative robots on SMT lines, underscoring the industry's push towards automation. While community-college certificate programs aim to address these shortages, their impact won't be felt until 2027, leading to a projected 0.7% dip in near-term growth.

Margin Compression From Commodity Component Price Swings

In early 2024, prices for multi-layer ceramic capacitors took a significant hit, plummeting by 35%. However, just six months later, these prices recovered by 22%. This volatility in pricing not only affected fixed-fee EMS contracts but also led companies like Sanmina to the negotiating table, pushing for adjustments in their pass-through clauses. Meanwhile, public companies faced challenges as inventory write-downs, primarily due to microcontroller redesigns, shaved off 80 basis points from their operating margins between 2023 and 2025. Consequently, this margin compression led to a 0.5% downward revision in the forecasted CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Box Build Growth Outpaces PCB Assembly

Electromechanical assembly and box build revenue is expected to grow at a 8.65% CAGR to 2031, steadily narrowing the 48.29% 2025 lead held by PCB assembly as the laregets sub-segment of the United States EMS Market. This surge reflects automakers outsourcing battery-management systems and ADAS compute modules to domestic partners that can bundle enclosure fabrication, cable harnesses, and end-of-line functional tests. Tier-1 providers leverage scale purchasing for aluminum housings and high-current busbars, then amortize tooling across multiple vehicle platforms, a dynamic that smaller captive plants cannot replicate.

PCB assembly remains indispensable for smartphones, routers, and industrial controllers, yet its unit volume is flattening as consumer upgrade cycles lengthen. Prototyping orders from AI-hardware startups partially offset this softness, bringing short-run, high-layer-count work into premium-priced Class 3 lines. Engineering services linked to design-for-manufacturability have become table stakes, and providers capable of performing in-circuit test development inside the same campus win a larger share of follow-on production. Logistics services round out turnkey contracts by freeing OEMs from component financing, a decisive edge in capital-constrained medical and industrial niches.

By Business Model: Hybrid And Turnkey Contracts Gain Momentum

Contract manufacturing accounted for 71.93% share of 2025 of the United States EMS Market's revenue, but Original Design Manufacturing (ODM) segment is advancing at a 9.97% CAGR as OEMs seek single-invoice solutions that cover materials, assembly, and regulatory documentation. Under turnkey deals, EMS providers shoulder component-sourcing risk, hold buffer stock, and manage supplier scorecards, features that appeal to medical-device start-ups scrambling to meet FDA submission deadlines. Hybrid contracts carve out firmware and algorithm IP for the customer while delegating PCB layout and test-fixture design to the EMS house, protecting core technology yet expediting builds.

Original design manufacturing remains a niche pathway centered on white-label networking gear and point-of-sale terminals where differentiation is thin. Nonetheless, hybrid models offer a stepping stone for OEMs wary of relinquishing control, and Plexus reported double-digit gains from such engagements in 2025. As supply-chain unpredictability persists, invoice consolidation and faster engineering change-order cycles give the hybrid cohort a durable structural advantage in the United States electronics manufacturing services (EMS) market.

By Manufacturing Process: Advanced Packaging Redefines System Integration

Surface-mount technology (SMT) accounted for 72.99% of process revenue in 2025, yet advanced packaging and hybrid processes are growing at a healthy 9.67% CAGR. Fan-out wafer-level, 2.5D interposer, and through-silicon-via techniques now sit alongside traditional SMT inside the same buildings to shorten yield-learning loops on AI accelerators and SiC power modules. EMS providers with cleanrooms and die-bond capabilities command premium prices, since yield excursions discovered late in the flow can drain project NPV.

Through-hole technology endures in power-conversion modules and avionics, though its share continues to slip as vibration-resistant SMT packages spread into mil-aero catalogs. Intel’s plan to offer Foveros services to external clients underscores the blurring divide between OSAT and EMS lanes, creating a future market where packaged chiplets, system boards, and thermal assemblies leave the floor fully mated and tested. Capital intensity is rising, but so are switching costs for customers once a line is qualified, cementing wallet share for the early adopters.

By End-User: Automotive Electronics Shows Fastest Growth

Communication sector delivered 25.17% of the United States EMS Market 2025 demand, and is projected to post the fastest 10.55% CAGR through 2031. It includes cloud and data center infrastructure, telecommunications infrastructure, enterprise networking, data center networking, satellite communication electronics, and cable and broadband infrastructure equipment. These sub-sectors create distinct manufacturing requirements, making Communication one of the most technically demanding and strategically important verticals for domestic EMS providers.

Medical devices notch steady mid-single-digit growth, thanks to miniaturization of implantables and continuous-monitoring wearables that require ISO 13485 QMS and rigid design-history files. Cloud and data center infrastructure is an important sub-sector within the Communication segment for US EMS providers. Leading hyperscalers, including Amazon Web Services, Microsoft Azure, Google Cloud, Meta, and Oracle, continue to invest heavily in AI infrastructure. Aerospace and defense boards flow almost exclusively through trusted-supply-chain channels, ensuring a baseline workload even when consumer electronics cool.

Geography Analysis

Arizona, Texas, Ohio, and New York captured more than 60% of new semiconductor and advanced-packaging investment from 2022-2025, catalyzing concentric EMS expansions that slash transit time and logistical risk. Each announced fab complex, from TSMC’s USD 65 billion campus to Intel’s USD 100 billion Ohio project, requires a halo of tier-1 and tier-2 EMS partners within a one-hour truck radius to deliver high-value assemblies just in time.

California and Massachusetts keep their advantage in design-centric niches such as implantable medical devices, space avionics, and AI prototype blades, where engineering talent density outweighs higher labor costs. Meanwhile, the Pacific Northwest benefits from hyperscaler AI server rollouts, giving Washington-based EMS plants a steady queue of low-volume, high-mix builds tied to cloud demand spikes.

The Midwest, anchored by Michigan and Tennessee, is pivoting from internal-combustion harnesses to EV power-electronics modules, supported by state incentives that dovetail with IRA credits. Federal procurement rules, such as the Trade Agreements Act, add tailwinds by excluding non-U.S. assemblies for sensitive categories, while forthcoming EPA PFAS restrictions will raise compliance hurdles that may force smaller regional shops to consolidate or exit.

Mordor Intelligence delivers a comprehensive view of the electronics manufacturing services market across all major regions such as Europe, Asia, and North America, alongside country-level analysis for Mexico, Germany, Taiwan, China, Vietnam, and India, each offering a view of the local market realities.

Competitive Landscape

The US EMS market is moderately concentrated, with Jabil, Flex, Sanmina, Celestica, and Plexus among significant players. Scale leaders poured hundreds of millions into collaborative-robot pick-and-place, AI-enabled AOI, and digital-twin line simulations, targeting a 20% reduction in labor hours by 2027. Only a handful of U.S. EMS facilities currently house class 1000 cleanrooms, plasma pretreat, and thermocompression bonders needed for chiplet packaging, setting a high entry bar.

Mid-tier specialists thrive by offering ITAR compliance, ISO 13485 documentation, and rapid NPI slots that larger plants decline due to utilization constraints. Turnkey and hybrid contract uptake compresses quote-to-cash cycles, favoring providers with unified ERP platforms capable of real-time inventory and supplier scoring. White space abounds in secure supply-chain orchestration and in combined advanced packaging and board-level assembly, niches that fewer than 10 domestic firms can service end to end.

Technology roadmaps are diverging, scale incumbents double down on automation and capital-heavy advanced packaging, whereas specialists invest in cross-functional engineering teams to navigate regulatory audits and time-critical engineering change orders. The result is a coexistence model where both extremes grow, yet share battles intensify in the middle tier, lacking either scale or specialization.

United States Electronics Manufacturing Services Industry Leaders

-

Jabil Inc.

-

Flex Ltd.

-

Sanmina Corporation

-

Plexus Corp.

-

Benchmark Electronics Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Flex and Cerebras Systems expanded their partnership to scale U.S.-based manufacturing of wafer-scale AI compute systems, strengthening Flex's position as a key domestic EMS partner for next-generation AI hardware production.

- December 2025: Celestica completed a USD 90 million retrofit of its Richardson, Texas campus, adding a class 1000 cleanroom and thermocompression bonding tools to support chiplet-based AI accelerator modules, with initial customer shipments slated for Q2 2026.

- November 2025: Jabil commissioned a USD 150 million advanced-packaging line at its Chandler, Arizona facility, colocated 12 miles from TSMC’s fab, enabling fan-out wafer-level packaging volumes of up to 20,000 panels per month by mid-2026.

- October 2025: Flex launched a dedicated medical-device NPI center in San Jose, California, featuring ISO 13485 cleanrooms and rapid-prototyping labs designed to cut design-verification cycles by 30% for wearables and minimally invasive surgical tools.

United States Electronics Manufacturing Services Market Report Scope

The United States Electronics Manufacturing Services/US EMS Market Report is Segmented by Service Type (PCB Assembly, Electromechanical Assembly/Box Build, Prototyping, Other EMS, Engineering Services, Test and Development, Logistics, Other Services), Business Model (Contract Manufacturing, ODM, Hybrid/Turnkey), Manufacturing Process (SMT, THT, Advanced Packaging), End-user (Mobile, Consumer, Computer, Industrial, Automotive, Communication, Lighting, Medical, Other). Market Forecasts are Provided in Terms of Value (USD).

| Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | |

| Prototyping | |

| Other Electronic Manufacturing Services | |

| Engineering Services | |

| Test and Development Implementation Services | |

| Logistics Services | |

| Other Service Types |

| Contract Manufacturing (CM) |

| Original Design Manufacturing (ODM) |

| Hybrid / Turnkey / Other Business Models |

| Surface Mount Technology (SMT) |

| Through-Hole Technology (THT) |

| Advanced Packaging / Hybrid Processes |

| Mobile Devices (Smartphones and Tablets) |

| Consumer Electronics |

| Computer (PCs/Desktop/Laptops) |

| Industrial |

| Automotive |

| Communication |

| Lighting |

| Medical |

| Other End-users |

| By Service Type | Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | ||

| Prototyping | ||

| Other Electronic Manufacturing Services | ||

| Engineering Services | ||

| Test and Development Implementation Services | ||

| Logistics Services | ||

| Other Service Types | ||

| By Business Model | Contract Manufacturing (CM) | |

| Original Design Manufacturing (ODM) | ||

| Hybrid / Turnkey / Other Business Models | ||

| By Manufacturing Process | Surface Mount Technology (SMT) | |

| Through-Hole Technology (THT) | ||

| Advanced Packaging / Hybrid Processes | ||

| By End-user | Mobile Devices (Smartphones and Tablets) | |

| Consumer Electronics | ||

| Computer (PCs/Desktop/Laptops) | ||

| Industrial | ||

| Automotive | ||

| Communication | ||

| Lighting | ||

| Medical | ||

| Other End-users |

Key Questions Answered in the Report

How large will United States Electronics Manufacturing Services market spending be by 2031?

The United States electronics manufacturing services market is projected to reach USD 267.44 billion by 2031.

What is the forecast growth rate for the US contract manufacturers?

Overall market revenue is set to rise at a 7.61% CAGR from 2026 to 2031.

Which EMS segment grows fastest through 2031?

Communications sector is expected to expand at a 10.55% CAGR, outpacing all other end-user segments.

Why are turnkey contracts gaining popularity?

Turnkey models transfer component sourcing and inventory risk to the EMS provider, speeding new-product introduction for medical-device and industrial IoT firms.

How is labor scarcity influencing automation?

A 12% vacancy rate for certified assemblers is pushing providers to deploy collaborative robots and predictive maintenance to sustain margins.

What regions attract the most EMS capacity expansion?

Arizona, Texas, Ohio, and New York collectively captured over 60% of announced investments tied to CHIPS Act semiconductor fabs.

Page last updated on: