Singapore Electronics Manufacturing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

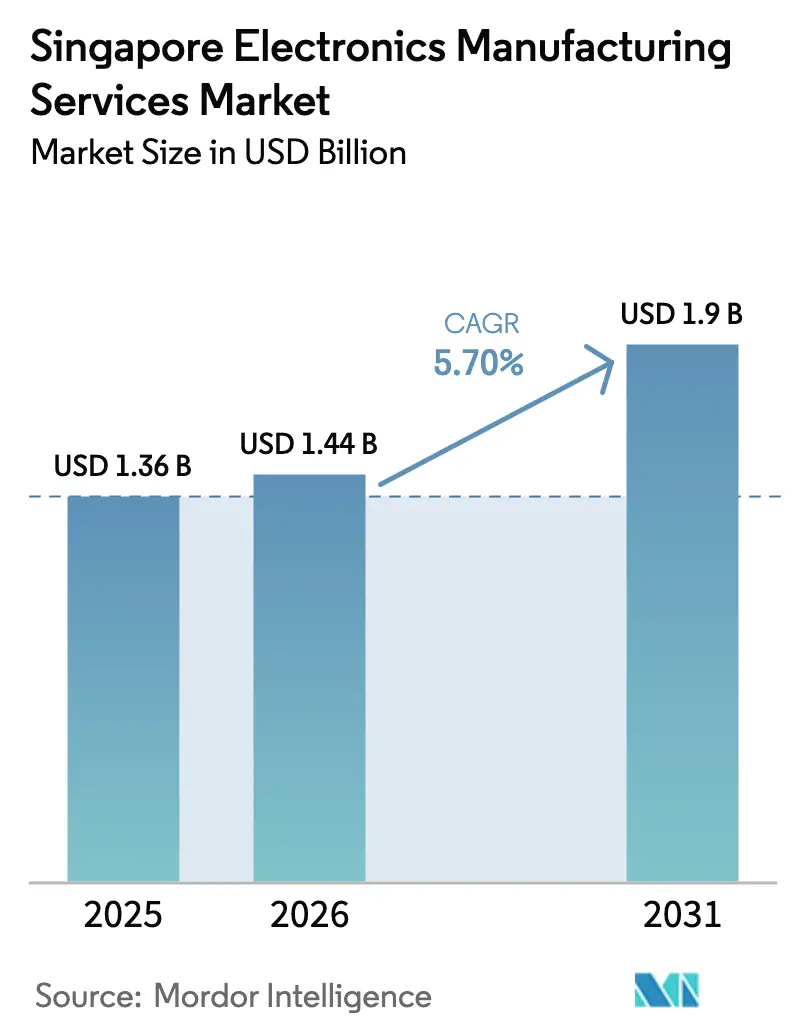

| Base Year Market Size (2025) | USD 1.36 Billion |

| Market Size (2026) | USD 1.44 Billion |

| Market Size (2031) | USD 1.9 Billion |

| Growth Rate (2026 - 2031) | 5.70% CAGR |

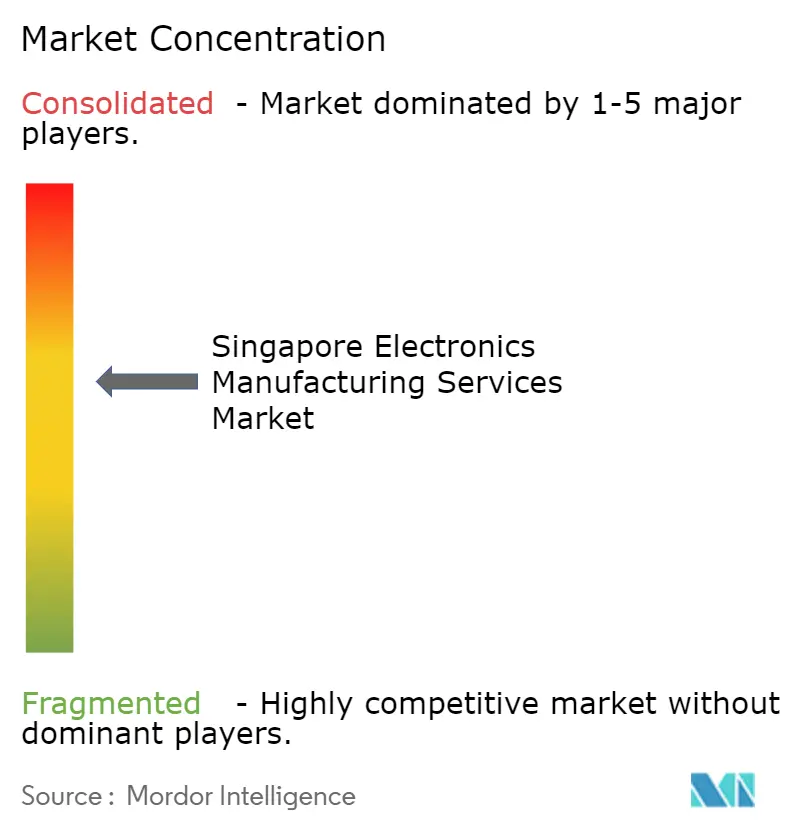

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Electronics Manufacturing Services Market Analysis by Mordor Intelligence

The Singapore Electronics Manufacturing Services Market is expected to grow from USD 1.36 billion in 2025 to USD 1.44 billion in 2026 and is forecasted to reach USD 1.9 billion by 2031 at 5.70% CAGR over 2026-2031. Precision-engineered, high-mix low-volume programs for aerospace, medical devices and automotive power electronics are replacing commoditized handset assembly, allowing providers to capture higher margins and shorten lead times. Micron’s USD 7 billion high-bandwidth memory plant and Silicon Box’s USD 2 billion chiplet-integration facility, both commissioned in 2024, confirm Singapore’s pivot toward advanced packaging and heterogeneous integration. At the same time, 40% of domestic factories had adopted digital-twin simulation by 2025 under the Smart Industry Readiness Index, lifting yields and lowering rework. Wage differentials with Vietnam have pushed local firms to automate inspection, while low-Earth-orbit satellite programs and electric-vehicle power modules are opening premium export niches.

Key Report Takeaways

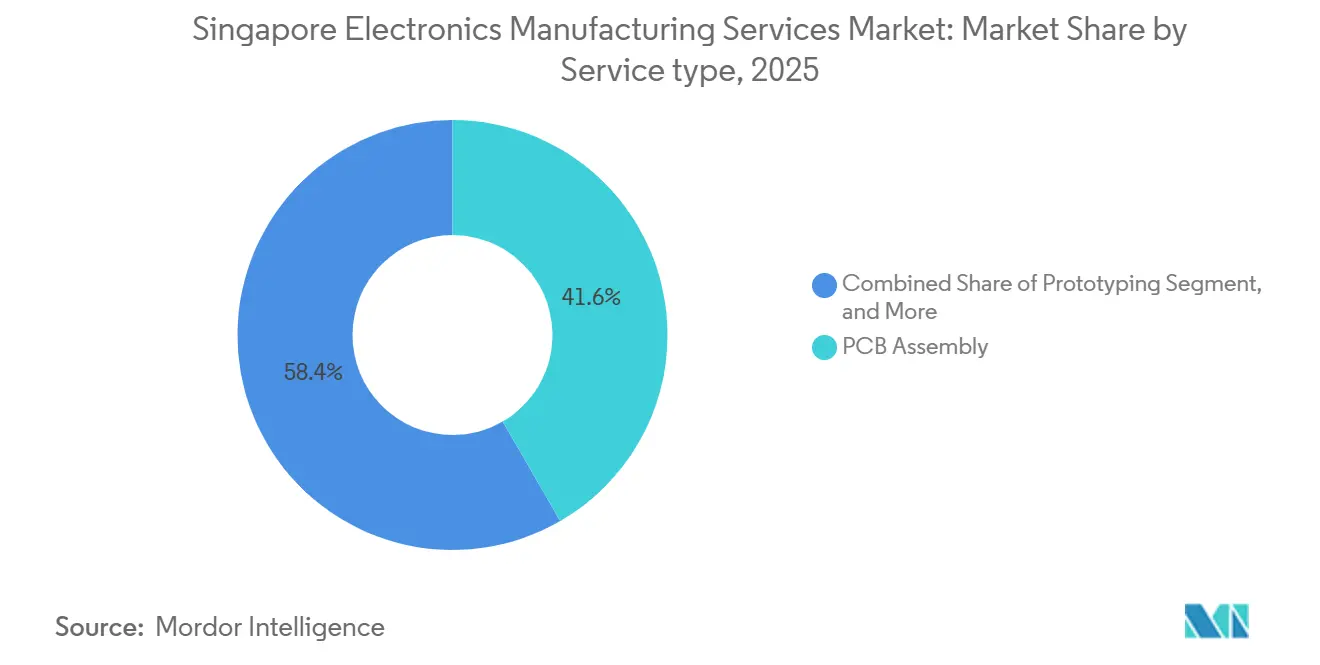

- By service type, PCB assembly led with 41.64% of Singapore electronics manufacturing services market share in 2025; electromechanical assembly and box-build services are expected to expand at a 5.82% CAGR through 2031.

- By business model, contract manufacturing accounted for 62.74% of revenue in 2025, whereas hybrid and turnkey models are projected to grow at a 6.03% CAGR during 2026-2031.

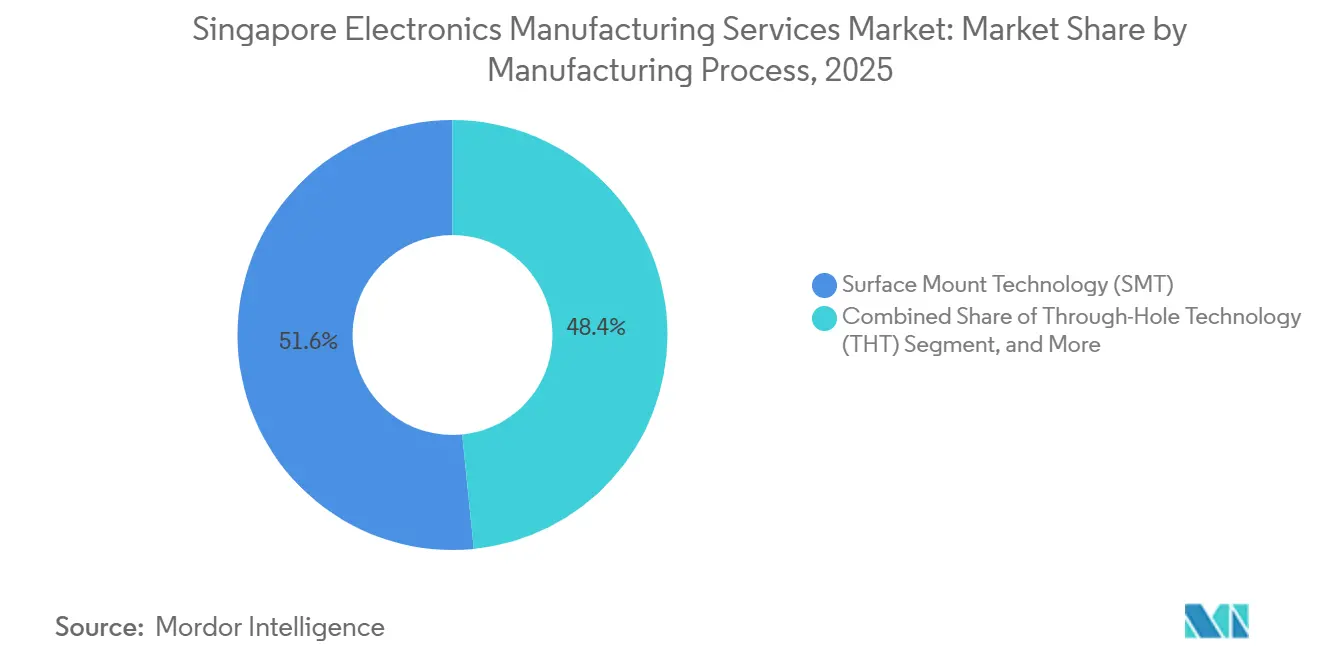

- By manufacturing process, surface-mount technology generated 51.57% of sales in 2025; advanced packaging and hybrid processes are forecast to rise at a 6.43% CAGR to 2031.

- By end-user, consumer electronics held 33.71% share in 2025, while automotive electronics is poised to register a 6.95% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Future direction is shaped by developments occurring across multiple countries and regions, with Singapore contributing to the overall trajectory. The outlook on worldwide electronics manufacturing services market reflects how these are expected to evolve collectively.

Singapore Electronics Manufacturing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for High-Mix Low-Volume Production from Consumer Electronics | +1.2% | Singapore, with spillover to Malaysia and Thailand precision clusters | Medium term (2-4 years) |

| Expansion of Semiconductor Supply Chain Incentives | +1.5% | Singapore national, anchored by Woodlands and Tampines industrial zones | Long term (≥ 4 years) |

| Rising Adoption of Industry 4.0 Smart Factories | +0.9% | Singapore national, early gains in Jurong and Tuas manufacturing hubs | Medium term (2-4 years) |

| Increasing Outsourcing Trend to Reduce Time-to-Market | +1.0% | Global, with APAC core benefiting Singapore and Taiwan | Short term (≤ 2 years) |

| Surge in LEO Satellite Electronics Assembly Contracts | +0.7% | Global, with Singapore capturing high-reliability segment | Long term (≥ 4 years) |

| Government Sustainable Manufacturing Grants | +0.4% | Singapore national, administered via EDB and Enterprise Singapore | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Semiconductor Supply-Chain Incentives

Micron’s USD 7 billion high-bandwidth memory complex and Silicon Box’s USD 2 billion chiplet plant, both initiated in 2024, anchor a USD 15 billion project pipeline and push yield rates above 95%, outstripping emerging ASEAN fabs. Budget 2025 earmarked SGD 500 million (USD 370 million) for an extreme-ultraviolet research center, while tax deductions covering 250% of automation spend further sweeten capital economics.[1]Ministry of Trade and Industry Singapore, “Budget 2025 Semiconductor Research Facility Allocation,” mti.gov.sg These policies secure equipment that would otherwise be restricted by export controls, positioning the city-state as a safe harbor for advanced packaging. Co-funded R&D with A*STAR subsidizes up to 70% of joint projects, accelerating technology transfer into pilot lines. As a result, Singapore attracts heterogeneous-integration programs that rivals cannot yet industrialize at scale.

Growing Demand for High-Mix Low-Volume Production

Batch sizes of 50–5,000 units and life cycles of 18–36 months dominate aerospace avionics, medical implantables and industrial sensors, which represented roughly 35% of EMS revenue in 2025, up from 28% in 2020. Venture Corporation disclosed that life-sciences and industrial accounts delivered 42% of Q3 2024 sales, evidencing migration away from consumer devices.[2]Venture Corporation Limited, “Third-Quarter 2024 Financial Results,” venture.com.sg Lead times for functional prototypes have compressed from four weeks in 2020 to 10 days in 2025 as additive manufacturing and digital twins mature. Health Sciences Authority pre-qualification for ISO 13485 sites shortens market authorization for medical start-ups, giving local assemblers a regulatory edge. Collectively, these factors shift competitive emphasis from unit cost to reliability, traceability and rapid design-for-manufacturability iteration.

Increasing Outsourcing Trend to Reduce Time-to-Market

Continental cut concept-to-production cycles for 800-V inverters from 12–18 months in Germany to six months in Singapore by leveraging local EMS partners for rapid prototyping. Jabil reported that 60% of its 2024 Singapore revenue came from engineering services and new-product introduction, underscoring client appetite for process-development support. Dual-sourcing imperatives arising from export-control risks motivate European and North American brands to place sensitive sub-assemblies in IP-secure jurisdictions, and Singapore ranks second globally in intellectual property protection. Rigid-flex PCBs and conformal coating for 5G radios, now standard among local assemblers, further reduce validation cycles. These gains translate into accelerated revenue capture for customers and premium gross margins for providers.

Rising Adoption of Industry 4.0 Smart Factories

By 2025, 40% of electronics plants reached Level 3 readiness on the Smart Industry Readiness Index, doubling the 2021 share. Flex’s Kallang site deployed autonomous mobile robots in 2024, trimming work-in-process inventory by 30% and redeploying technicians to failure analysis. A*STAR’s Model Factory showed that simulating reflow profiles via digital twins can cut solder defects by 18% and energy use by 12%, results now replicated by 15 EMS companies. Mandatory IEC 62443 segmentation for operational technology networks has spurred investment in zero-trust architectures to shield export-controlled designs. Together, these initiatives lower operating costs, boost uptime, and cement Singapore’s reputation for high-reliability production.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Skilled Electronics Assembly Technicians | -0.8% | Singapore national, acute in Jurong and Woodlands industrial estates | Short term (≤ 2 years) |

| Volatile Semiconductor Component Supply and Pricing | -1.0% | Global, with Singapore exposed via memory and logic chip imports | Short term (≤ 2 years) |

| Rising Energy Tariffs Under Carbon Tax Expansion | -0.5% | Singapore national, concentrated in energy-intensive SMT lines | Medium term (2-4 years) |

| Competition from Emerging Vietnamese EMS Clusters | -0.6% | Regional ASEAN, with Vietnam targeting mid-tier consumer electronics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Semiconductor Component Supply and Pricing

DRAM spot prices jumped 88% year-on-year in Q3 2024, while NAND prices climbed 30%, forcing EMS firms to hold 90-120 days of safety stock, up from the historical 30-45 days. Lead times for power-management ICs stretched past 52 weeks, and Flex stated that component inflation drove 40% of its FY2025 Q2 gross-margin compression. Smaller Singapore providers lack the purchasing leverage to secure allocation during shortages, heightening write-down risk when orders normalize. Geopolitical tensions around Taiwan, which supplies 60% of global logic chips, could disrupt shipments within 48 hours, amplifying exposure. Although larger players have broadened sourcing to Japan and South Korea, procurement volatility remains a structural headwind until new capacity comes online.

Shortage of Skilled Electronics Assembly Technicians

IPC-certified vacancies hit 12% in 2025 as the median age of production technicians reached 48 years, and younger workers gravitated toward software roles. Wage inflation of 4-5% per annum since 2022 has compressed margins for mid-tier EMS firms without extensive automation. AEM Holdings indicated that labor costs rose 6.8% year-on-year in Q3 2024 despite static headcount, driven by overtime and retention bonuses. Government retraining grants cover up to 90% of course fees, but annual polytechnic graduations in precision engineering (1,200 in 2024) fall short of industry demand for 2,000 new hires. In the near term, talent scarcity limits capacity expansion and elongates new-product introduction ramps, tempering the sector’s growth trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Box-Build Gains as Customers Seek Turnkey Solutions

Lectromechanical assembly and box-build activities expanded at a 5.82% CAGR through 2031, surpassing the broader Singapore electronics manufacturing services market. PCB assembly still accounted for 41.64% of 2025 revenue, yet its share of the Singapore electronics manufacturing services market eroded as high-volume handset programs migrated to lower-cost ASEAN sites. Turnkey contracts bundle enclosure design, cable harnessing, and final systems test, giving original equipment manufacturers a single accountable partner and compressing time-to-market by up to eight weeks. Venture Corporation disclosed that turnkey programs accounted for 38% of Q3 2024 sales, up 9 percentage points from 2022, validating the pivot toward full-system outsourcing.

Engineering services and test-and-development implementation earned gross margins of 22%, almost triple standard surface-mount assembly, because clients value design-for-manufacturability, accelerated life testing and regulatory pre-qualification.[3]Jabil Inc., “Fiscal Year 2024 Annual Report,” jabil.com Additive manufacturing trimmed prototype lead times from four weeks in 2020 to 10 days in 2025, enabling rapid iteration before tooling is set. Logistics services, though smaller, are now bundled with assembly so customers can hold vendor-managed inventory near Singapore’s free-trade port. Reverse-logistics and refurbishment work streams are also scaling as European circular-economy mandates require take-back programs, a niche that favors providers with ISO 14001 certification.

By Business Model: Hybrid Approaches Capture Design-to-Manufacturing Value

Contract manufacturing retained 62.74% of Singapore's electronics manufacturing services market share in 2025, reflecting the long-standing preference to outsource labor-intensive scale-up while safeguarding intellectual property. Hybrid and turnkey models, however, are projected to grow at 6.03% CAGR, driven by start-ups and mid-tier firms that lack in-house design bandwidth and want access to the EMS provider’s component library and supplier network. Flex’s USD 1.8 billion acquisition of Anord Mardix in 2024 illustrates the appeal: the deal layered power-distribution design atop cabinet integration, allowing Flex to quote hyperscale data-center projects end-to-end.

Original design manufacturing remains a modest slice of the Singapore electronics manufacturing services market, yet it is gaining ground in industrial gateways and medical diagnostics, where regulatory barriers deter new entrants. Sanmina reported that 28% of 2024 contract wins bundled engineering services, up from 18% in 2021, confirming the monetization potential of design support. Gross-margin spreads reinforce the trend: hybrid deals earn 15-20% versus 8-12% for pure build-to-print. Certification loads also tilt the field in favor of ISO 13485 and IATF 16949, reducing client audit burdens and encouraging customers to migrate from traditional contract manufacturing toward a more integrated partnership.

By Manufacturing Process: Advanced Packaging Captures AI-Chip Demand

Surface-mount technology accounted for 51.57% of 2025 process revenue, driven by decades of placement-speed gains and defect rates below 10 ppm for 0201 passives. Yet advanced packaging and hybrid flows will grow 6.43% CAGR as AI accelerators and high-performance computing modules require chiplet integration, through-silicon vias and micro-bump pitches under 40 µm. Micron’s high-bandwidth-memory complex, operational since 2024, stacks 12 dielectric layers to achieve 1 TB/s bandwidth, a capability that wire-bonding cannot match. Silicon Box’s chiplet line likewise targets heterogeneous 2.5D packages, posting yield rates above 95% compared with sub-90% in newer ASEAN fabs.

Through-hole technology persists in power electronics and aerospace due to its mechanical robustness and high current capacity, though its share is forecast to shrink at a −1.2% CAGR as press-fit connectors proliferate. Hybrid lines that combine SMT, through-hole, and advanced packaging now run at 85% utilization on automotive inverter programs, according to Benchmark Electronics’ Q3 2024 call. In-line X-ray and laser-height metrology safeguard reliability when three distinct solder processes share one substrate. As more programs embrace chiplet architectures, capital expenditures will favor thermocompression bonders and laser-assisted die placers over conventional reflow ovens

By End-User: Automotive Electronics Leads Growth Amid Electrification

Consumer electronics still supplied 33.71% of 2025 turnover, but its growth has plateaued as smartphones and wearables migrate to Vietnam and India where labor costs run 60-70% lower. Automotive electronics is set to expand at 6.95% CAGR, the fastest among end-users, propelled by battery-management systems and silicon-carbide power modules for electric vehicles. Continental’s Singapore R&D hub prototypes 800-V inverters and leverages local ISO 26262 talent for functional-safety validation, shortening homologation by six months.

Industrial automation and robotics benefit from ASEAN’s manufacturing upshift and accounted for a rising share of the Singapore electronics manufacturing services market size in 2025. Communication infrastructure-5G base stations, optical modules, and network switches-leverages Singapore’s radio-frequency and photonics testing expertise, with Fabrinet deriving 68% of Q1 FY2025 revenue from optical products. Medical devices, though lower in volume, command premium pricing because the Health Sciences Authority pre-qualifies ISO 13485 sites, halving approval timelines relative to neighboring countries. Aerospace and defense work, underpinned by AS9100 and export-control compliance, yields margins exceeding 20%, reinforcing the city-state’s pivot to high-reliability niches.

Geography Analysis

Singapore anchors a tightly integrated ASEAN supply chain, acting as the high-value node for precision assembly, advanced packaging, and new-product introduction, while Malaysia, Thailand, and Vietnam handle volume manufacturing. The city-state captured 20% of global semiconductor back-end services in 2025, supported by Micron, GlobalFoundries and outsourced test specialists such as UTAC. Budget 2025 allocated SGD 500 million (USD 370 million) for an extreme-ultraviolet research hub, locking in technology parity with Taiwan and South Korea. Cross-border corridors deepen regional efficiency: ASE’s 2024 pact with Malaysia’s Kulim Hi-Tech Park splits wafer probing and final packaging to balance labor costs and capital intensity.

Competitive pressure arises from Vietnam, whose electronics exports hit USD 150 billion in 2024, driven by Samsung and Foxconn capacity additions. Vietnamese monthly wages of USD 300–400 undercut Singapore’s SGD 2,500-3,500, pushing Singapore facilities to automate optical inspection and conformal-coat lines. Even so, Vietnam’s eight-hour-per-month power outages and port delays of up to seven days constrain time-critical and Class-3 workmanship programs, which remain in Singapore. Thailand’s Eastern Economic Corridor attracted USD 12 billion of electronics FDI in 2024, especially for automotive electronics and battery packs, adding another midsized rival.

Regulatory differentials help Singapore retain premium work. ISO 13485 pre-qualification by the Health Sciences Authority cuts device-approval lead times from 18 to nine months, a decisive factor for venture-funded med-tech firms. The intellectual-property office’s 12-month expedited patent review, versus 24-36 months in neighboring states, encourages co-location of R&D and pilot lines. Carbon-tax escalation from SGD 25 per tonne-CO₂e in 2024 to SGD 50-80 by 2030 has inflated energy-intensive SMT operating expenses by 15-20%, yet also positions compliant plants for EU carbon-border adjustments. For customers that must document Scope 3 emissions, Singapore offers a verified pathway that lower-cost hubs cannot yet provide.

Analysis of the electronics manufacturing services market by Mordor Intelligence spans multiple other regional evaluations across Europe, Asia, and North America, supported by country-level insights for Japan, Malaysia, United Kingdom, United States, Germany, and France, wherein local market conditions keep varying from one country to another.

Competitive Landscape

The top five suppliers- Flex, Jabil, Sanmina, Venture Corporation and Celestica- controlled a considerable share of 2025 revenue, indicating a moderately concentrated Singapore electronics manufacturing services market. Flex exploits global scale while tailoring Singapore operations to high-reliability niches such as healthcare and aerospace, and its 2024 Anord Mardix deal added data-center power-distribution design, shifting bids from pure assembly to turnkey infrastructure. Jabil emphasizes engineering services; 60% of 2024 Singapore revenue came from new-product introduction, reflecting client demand for process-development expertise over labor-arbitrage savings.

Mid-tier specialists capture margin through domain depth. Venture Corporation derived 42% of Q3 2024 sales from life-sciences and industrial clients, reinforcing its pivot away from commoditized consumer devices. AEM Holdings and UMS Holdings disrupt incumbents in semiconductor test handlers and precision machining by offering application-specific intellectual property and rapid engineering turnaround. Technology adoption is a key differentiator: Flex’s autonomous mobile robot deployment trimmed work-in-process inventory by 30% in 2024, and 15 EMS companies have replicated A*STAR’s digital-twin reflow simulation with an average 18% defect reduction.

White-space opportunities span three verticals. First, low-Earth-orbit satellites: SpaceX’s 6,000-unit Starlink constellation fuels demand for space-grade phased-array antennas and power-distribution units, programs that few ASEAN plants are qualified to build. Second, electric-vehicle power electronics: Continental’s Singapore lab prototypes silicon-carbide modules that must meet ISO 26262, and regional electrification targets promise volume upside. Third, advanced packaging for AI accelerators: Micron and Silicon Box run sub-40 µm micro-bump lines, a capability fewer than 10 global sites possess, giving Singapore early-mover leverage in heterogenous integration.

Singapore Electronics Manufacturing Services Industry Leaders

Venture Corporation Limited

Flex Ltd.

Jabil Circuit Singapore Pte Ltd

Sanmina-SCI Systems Singapore Pte Ltd.

Beyonics Pte Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Jabil Circuit Singapore finished a SGD 120 million (USD 89 million) expansion of its automotive-electronics campus, adding 40,000 ft² of space for electric-vehicle battery-management systems and 800-V inverters.

- December 2025: Celestica secured a multi-year, USD 250 million contract to build optical transceivers and silicon-photonics modules for a leading hyperscale cloud provider. The deal covers design-for-manufacturability services and supply-chain management for 800 GbE and 1.6 TbE components, with output ramping at the firm’s Singapore facility through 2027.

- November 2025: Venture Corporation agreed to buy a European medical-device contract manufacturer for SGD 180 million (USD 133 million), boosting its ISO 13485-certified capacity by 60% and adding European Union Medical Device Regulation expertise.

- October 2025: AEM Holdings won a SGD 200 million (USD 148 million) follow-on order for semiconductor test handlers from multiple AI-chip makers.

- September 2025: Sanmina opened a 50,000-ft² advanced-packaging plant in Singapore focused on system-in-package modules for 5G infrastructure and automotive radar.

Singapore Electronics Manufacturing Services Market Report Scope

The Singapore Electronics Manufacturing Services Market Report is Segmented by Service Type (Electronic Manufacturing Services including PCB Assembly, Electromechanical Assembly/Box Build, Prototyping, and Other EMS; Engineering Services; Test and Development Implementation; Logistics Services; Other EMS Types), Business Model (Contract Manufacturing, Original Design Manufacturing, Hybrid/Turnkey/Other), Manufacturing Process (Surface Mount Technology, Through-Hole Technology, Advanced Packaging/Hybrid Processes), End-User (Mobile Devices, Consumer Electronics, Computer, Industrial, Automotive, Communication, Lighting, Medical, Other End-users), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | |

| Prototyping | |

| Other Electronic Manufacturing Services | |

| Engineering Services | |

| Test and Development Implementation | |

| Logistics Services | |

| Other Service Types |

| Contract Manufacturing (CM) |

| Original Design Manufacturing (ODM) |

| Hybrid / Turnkey / Other Business Models |

| Surface Mount Technology (SMT) |

| Through-Hole Technology (THT) |

| Advanced Packaging / Hybrid Processes |

| Mobile Devices (Smartphones and Tablets) |

| Consumer Electronics |

| Computer (PCs / Desktops / Laptops) |

| Industrial |

| Automotive |

| Communication |

| Lighting |

| Medical |

| Other End-Users |

| By Service Type | Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | ||

| Prototyping | ||

| Other Electronic Manufacturing Services | ||

| Engineering Services | ||

| Test and Development Implementation | ||

| Logistics Services | ||

| Other Service Types | ||

| By Business Model | Contract Manufacturing (CM) | |

| Original Design Manufacturing (ODM) | ||

| Hybrid / Turnkey / Other Business Models | ||

| By Manufacturing Process | Surface Mount Technology (SMT) | |

| Through-Hole Technology (THT) | ||

| Advanced Packaging / Hybrid Processes | ||

| By End-User | Mobile Devices (Smartphones and Tablets) | |

| Consumer Electronics | ||

| Computer (PCs / Desktops / Laptops) | ||

| Industrial | ||

| Automotive | ||

| Communication | ||

| Lighting | ||

| Medical | ||

| Other End-Users |

Key Questions Answered in the Report

What is the current value of Singapore’s electronics manufacturing services market?

The market was valued at USD 1.44 billion in 2026 and is projected to reach USD 1.9 billion by 2031.

Which service type is growing fastest?

Electromechanical assembly and box-build services are forecast to expand at a 5.82% CAGR between 2026 and 2031.

Why are hybrid and turnkey business models gaining traction?

They offer design-for-manufacturability expertise and single-vendor accountability, generating gross margins of 15–20% versus 8–12% for pure contract manufacturing.

How is Singapore positioned in advanced semiconductor packaging?

Facilities from Micron and Silicon Box provide sub-40 µm micro-bump capability, giving Singapore a first-mover edge in chiplet and high-bandwidth-memory integration.

What is the main growth driver on the demand side?

Automotive electronics, especially electric-vehicle battery-management and power-module assemblies, is projected to grow at a 6.95% CAGR through 2031.

Page last updated on: