North America Electronics Manufacturing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

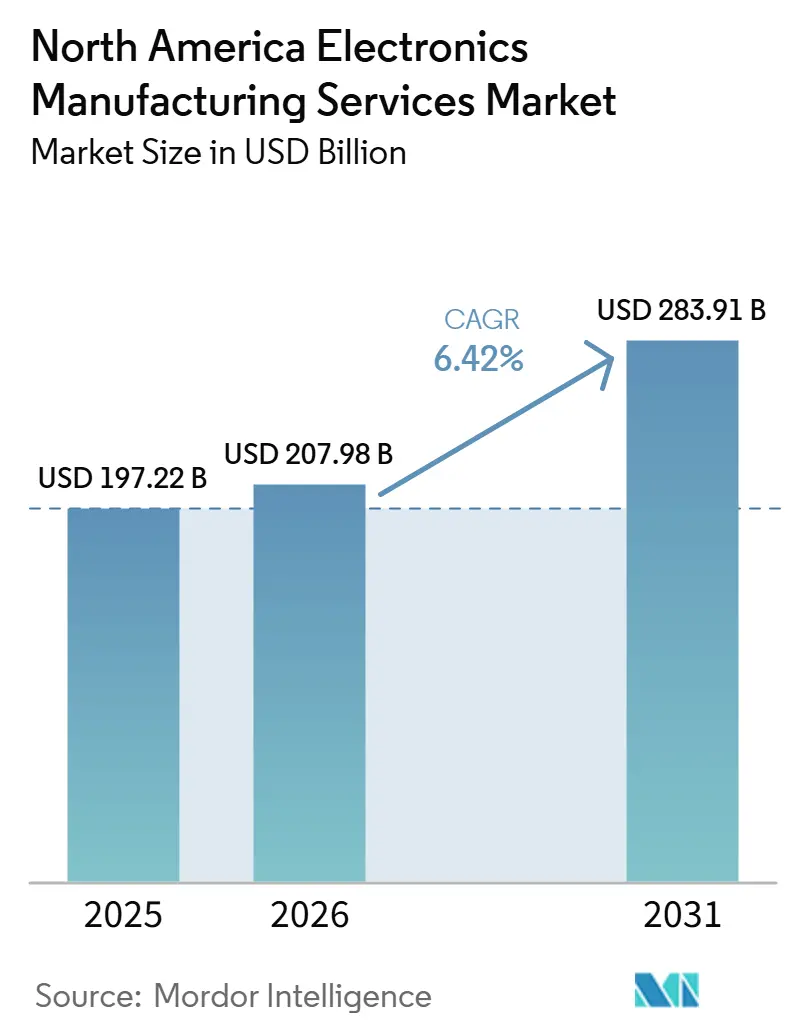

| Base Year Market Size (2025) | USD 197.22 Billion |

| Market Size (2026) | USD 207.98 Billion |

| Market Size (2031) | USD 283.91 Billion |

| Growth Rate (2026 - 2031) | 6.42% CAGR |

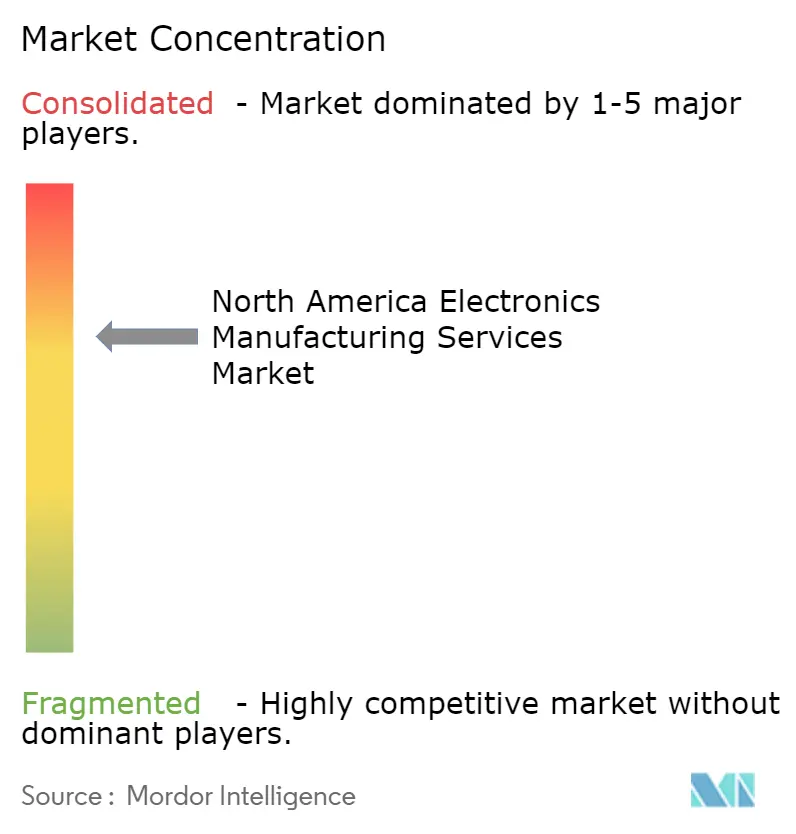

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Electronics Manufacturing Services Market Analysis by Mordor Intelligence

North America electronics manufacturing services market size was valued at USD 197.22 billion in 2025 and is estimated to grow from USD 207.98 billion in 2026 to reach USD 283.91 billion by 2031, at a CAGR of 6.42% during the forecast period (2026-2031). The North America electronics manufacturing services market size expands as public incentives, automotive electrification, and defense-grade compliance converge to redistribute assembly capacity from Asia to the United States, Canada, and Mexico. Federal subsidies under the CHIPS and Science Act deliver large capital infusions to fabrication plants, but the downstream shortage of printed-circuit-board and box-build lines remains the critical bottleneck that contract manufacturers now race to close. Automotive original equipment manufacturers (OEMs) are accelerating local sourcing because electric-vehicle battery-management systems and advanced driver-assistance modules require quick-turn prototypes that offshore megasites cannot supply within an eight-week design window. Medical-device makers, facing the 2026 U.S. Food and Drug Administration Quality Management System Regulation, are consolidating work with ISO 13485-certified partners to compress new-product-introduction (NPI) cycles, while hyperscale cloud providers are anchoring new facilities for artificial-intelligence (AI) server box builds near semiconductor back-end operations. Competitive pressure intensifies as Asian giants such as Foxconn and Pegatron establish North American lines, squeezing margins for long-time regional specialists even as total addressable revenue climbs.

Key Report Takeaways

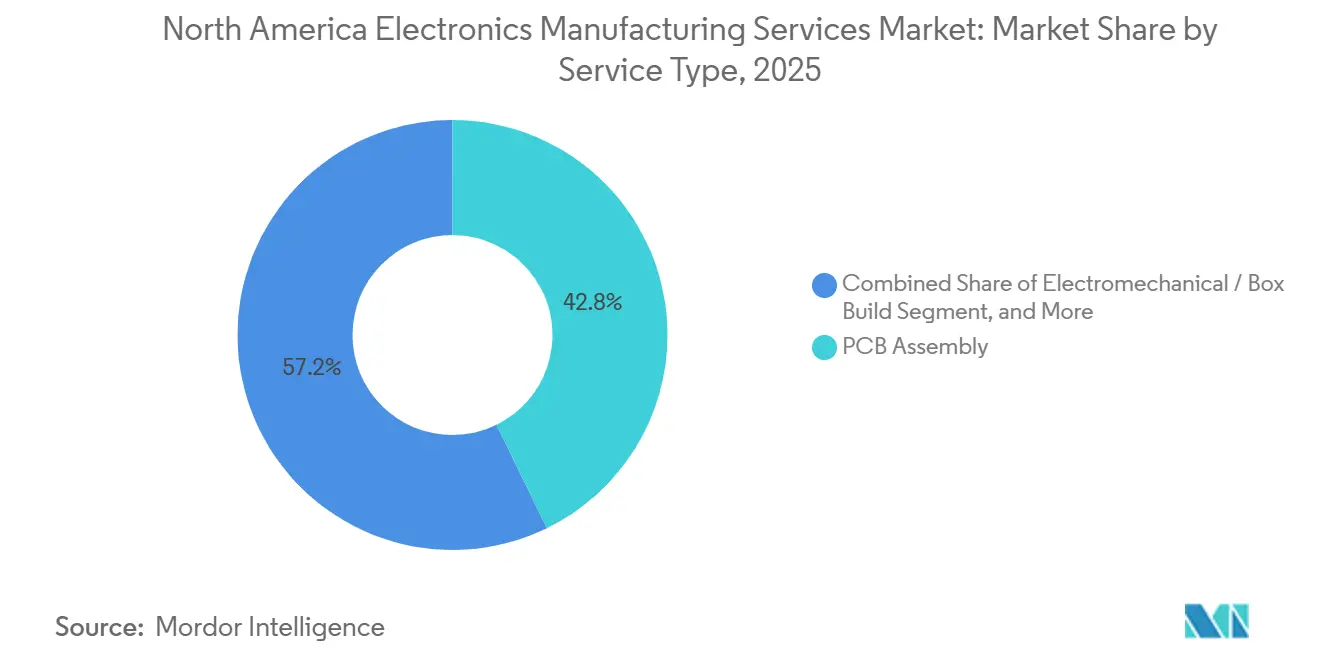

- By service type, printed-circuit-board assembly led with 42.76% of the North America electronics manufacturing services market share in 2025, while electromechanical assembly and box build are expanding at a 6.72% CAGR through 2031.

- By business model, contract manufacturing dominated with a 64.58% of the North America electronics manufacturing services market share in 2025, but hybrid and turnkey arrangements are forecast to rise at a 6.81% CAGR to 2031.

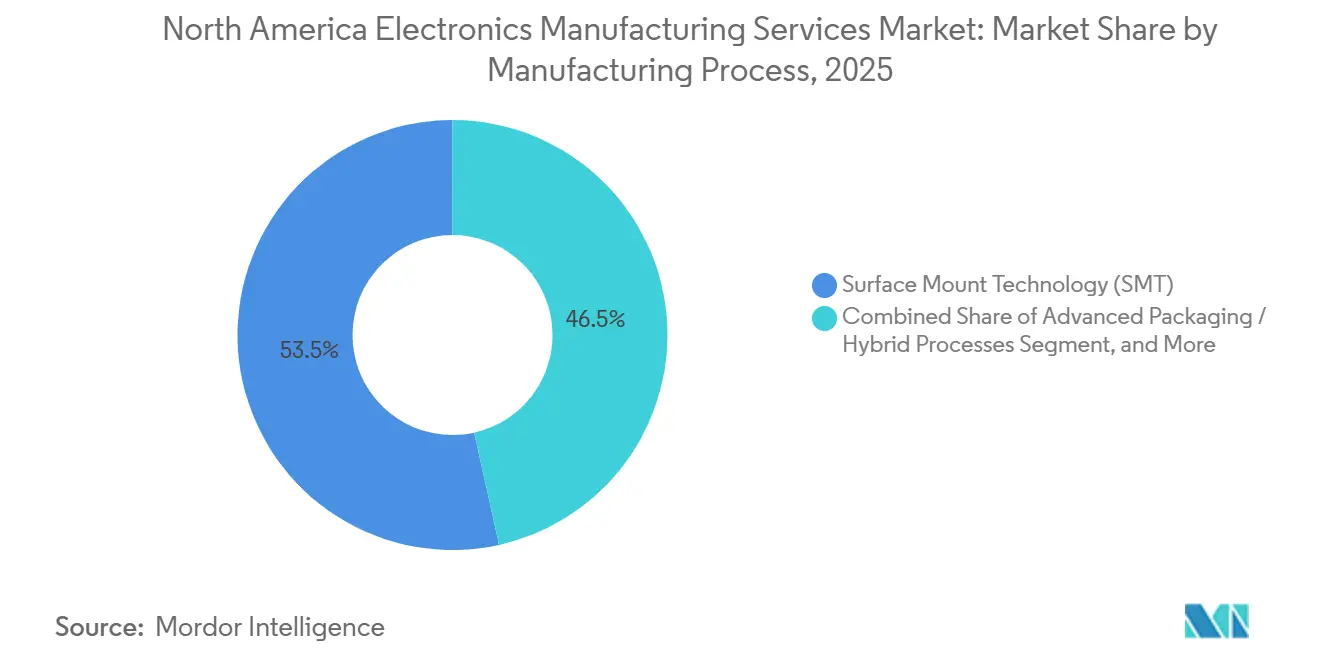

- By manufacturing process, surface-mount technology accounted for 53.47% of the North America electronics manufacturing services market share in 2025, and advanced packaging and hybrid processes are poised to grow at a 6.97% CAGR.

- By end-user, industrial electronics held the largest slice at 38.93% of the North America electronics manufacturing services market share in 2025, whereas automotive electronics is projected to expand at a 7.54% CAGR to 2031.

- By geography, the United States captured 86.71% of regional revenue in 2025, and is set to post the quickest growth at a 7.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Companies active in North america frequently operate across several geographies, linking regional presence to global strategy. Mordor Intelligence captures the entire market landscape of the global electronics manufacturing services industry and how these positions are distributed.

North America Electronics Manufacturing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust Reshoring Incentives from the CHIPS and Science Act | +1.4% | United States, with spillover to Canada and Mexico for assembly and test | Medium term (2-4 years) |

| Accelerating Demand for Automotive Electronics in EV and ADAS Platforms | +1.5% | United States and Mexico automotive corridors, Ontario Canada | Long term (≥4 years) |

| Growing Need for Rapid NPI Turn-Around in Regulated Medical Devices | +0.9% | United States FDA-regulated facilities, select Health Canada sites | Medium term (2-4 years) |

| Expansion of AI-Server and High-Speed Computing Hardware Production | +1.2% | United States hyperscale datacenter hubs (Virginia, Oregon, Texas) | Short term (≤2 years) |

| Defense Mandatory ITAR Compliance Driving On-Shore Box-Build Contracts | +0.7% | United States defense industrial base, limited Canada participation | Long term (≥4 years) |

| Low-Earth-Orbit Satellite Constellation Builds Requiring Quick-Turn PCB Assembly | +0.6% | United States (Florida, California launch corridors), limited Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Robust Reshoring Incentives from the CHIPS and Science Act

Awards totaling USD 36.4 billion across 40 fabrication and packaging projects by late 2025 ignited a downstream wave of electronics assembly investments.[1]CHIPS for America, “CHIPS for America Announces Over $36 Billion in Preliminary Awards,” chips.gov Contract manufacturers colocate new surface-mount lines near fabs to offer OEMs integrated wafer-to-board supply chains that shorten lead times and mitigate logistics risk. Jabil’s USD 500 million North Carolina project, announced in mid-2025, typifies the strategy of aligning box-build capacity with advanced packaging nodes to capture AI and high-performance computing demand. Reshoring Initiative data showing 287,299 U.S. manufacturing jobs announced in 2023 place electrical equipment and electronics at the top of the repatriation list. Tax credits under Section 48D further improve project economics, driving a sustained capex cycle through 2028 even if end-market demand temporarily softens. Policy-driven capacity additions are therefore expected to keep the North America electronics manufacturing services market on an above-trend growth trajectory.

Accelerating Demand for Automotive Electronics in EV and ADAS Platforms

Electric-vehicle powertrains use three to five times more circuit-board real estate than internal-combustion equivalents, while ADAS sensor-fusion modules require quick-turn iterations at small and mid volumes that Asian sites struggle to support cost-effectively.[2]Hyundai Motor Group, “Electrification Strategy and ADAS Platform Development,” hyundaimotorgroup.com Foxconn’s June 2025 EV.OS platform illustrates that even top Asian electronics manufacturing service providers now need North American hubs for co-development with local OEMs. U.S. National Highway Traffic Safety Administration proposals mandating automatic emergency braking on all new light vehicles by model year 2029 will embed radar and vision hardware into mass-market cars, boosting demand for printed circuit boards across Mexico and the U.S. automotive belts. Strategic collaborations such as DENSO and ROHM’s silicon-carbide inverter program intensify design complexity, making proximity to chip suppliers and prototyping labs a competitive necessity. These factors underpin the 7.54% CAGR outlook for automotive electronics revenue through 2031.

Growing Need for Rapid NPI Turn-Around in Regulated Medical Devices

The February 2026 FDA Quality Management System Regulation aligns 21 CFR Part 820 with ISO 13485:2016, raising documentation and validation requirements for medical-device OEMs.[3]U.S. Food and Drug Administration, “Quality Management System Regulation Final Rule,” fda.gov To compress NPI cycles and comply with new audit rules, OEMs increasingly select contract manufacturers that are already ISO 13485-certified and capable of managing design-history files. Facility announcements in 2025, including Jabil’s USD 70 million Mississippi plant and Kimball Electronics’ 308,000-square-foot Indianapolis site, show how suppliers build smaller, regulator-friendly lines that speed market entry. A surge of mid-tier firms, NIKOMED USA, Ezurio, CAIRE, and others, secured certification during 2024-2025, broadening the qualified supply base. Because 510(k) submissions require proof of stable manufacturing before clearance, OEMs cannot defer process validation, reinforcing demand for turnkey electronics manufacturing services partners within the region.

Expansion of AI-Server and High-Speed Computing Hardware Production

Hyperscale operators ordered around 1.5 million AI accelerator servers in 2025, each integrating 8-16 high-bandwidth-memory modules and liquid-cooling manifolds beyond the scope of legacy rack lines. AMD’s MI325X accelerator, shipping in Q4 2025, increases on-module power draw to 750 watts, creating new thermal and signal-integrity challenges that require collaborative design between OEMs and contract manufacturers. Oak Ridge National Laboratory demonstrated that liquid cooling cuts datacenter energy use by up to 40%, spurring commercial adoption and new hardware SKUs. Cerebras’ wafer-scale systems require custom enclosures that can only be built in clean-room-equipped North American facilities under tight non-disclosure agreements. Jabil’s acquisitions of Mikros Technologies and Hanley Energy Group reinforce the importance of thermal and power-delivery expertise in capturing this short-cycle, high-margin workload. Consequently, AI-server assembly emerges as a major incremental revenue pool from 2026-2027.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled Labor Shortages Across Tier-2/3 EMS Providers | -1.1% | United States rural manufacturing clusters, select Canada sites | Medium term (2-4 years) |

| Margin Pressure from Asian High-Volume Contract Manufacturers | -0.9% | North America-wide, most acute in consumer electronics and mobile devices | Long term (≥4 years) |

| Accelerating PFAS and RoHS Regulatory Compliance Costs | -0.6% | United States EPA jurisdictions, California Proposition 65 zones | Short term (≤2 years) |

| Wave of Baby-Boomer Engineering Retirements Eroding Institutional Know-How | -0.7% | United States and Canada legacy electronics manufacturing services sites | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Skilled Labor Shortages Across Tier-2/3 EMS Providers

The average U.S. manufacturing worker's age reached 56.5 years in 2025, and retirements outpace incoming talent, making soldering, inspection, and process-engineering roles scarce. Tier-1 firms run their own IPC certification academies, but smaller shops in rural clusters cannot match wage offers from automotive assembly plants. Community-college apprenticeship programs launched in North Carolina, Texas, and Arizona graduate fewer than 500 students per state each year, which is inadequate for the 40 CHIPS Act projects scheduled through 2028. Consequently, new capacity ramps more slowly than capital budgets anticipate, reducing effective supply in the North America EMS market and tempering growth despite healthy demand.

Margin Pressure from Asian High-Volume Contract Manufacturers

Foxconn, Pegatron, Compal, Quanta, and Wistron generated more than USD 200 billion in fiscal 2024 revenue, leverage economies of scale, and now replicate core lines inside the region. Their entry drives OEMs to dual-source strategies that pit incumbents against new Asian-backed plants, forcing price concessions and eroding gross margins. Lincoln International’s EMS Stock Index fell 11.5% in Q1 2025 before recovering as investors balanced competition against policy tailwinds. Benchmark Electronics, Sanmina, and Kimball Electronics each reported sub-5% operating margins in 2024-2025, evidencing the squeeze. The effect is most visible in consumer electronics, but Asian firms are rapidly earning ISO 13485 and IATF 16949 certifications, extending pricing pressure into the medical and automotive verticals as well.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Box Build Captures Complex Integration Demand

Electromechanical assembly and box build generated the fastest revenue growth, rising at a 6.72% CAGR, driven by defense primes and medical-device OEMs outsourcing final integration to save engineering bandwidth. The segment now captures growing portions of the North America EMS market as OEMs delegate full system-level testing, regulatory documentation, and thermal-solution co-design to trusted partners. Printed-circuit-board assembly still accounted for 42.76% of the 2025 value but shows maturity, with demand shifting from commodity placement to high-reliability Class 3 builds. Engineering services focused on design-for-manufacturability, failure-mode-and-effects analysis, and obsolescence monitoring deepen supplier embeddedness and raise switching costs. Prototyping and test implementation businesses flourish as mixed-signal content in industrial IoT and low-earth-orbit (LEO) satellite hardware multiplies the need for automated-test-equipment programming. Jabil’s Hanley Energy acquisition illustrates how logistics and power-delivery know-how now differentiate leading providers. Surface-mount lines remain ubiquitous; nonetheless, system-integration shops offering conformal coating, potting, and environmental stress screening capture premium pricing in aerospace and defense, pulling further profit toward box-build specialists.

Demand inflection in AI servers heightens the importance of enclosure, cold-plate, and cable-assembly expertise, further lifting box-build wallet share. Tier-2 players such as Plexus, which won the Evolv Technology contract in November 2025, underscore that quick-turn system integration creates opportunity outside megacaps. Over 2026-2031, the North America EMS market size for box-build work is forecast to approach USD 40 billion, roughly one-quarter of the regional value, as turnkey bookings displace purely board-level awards.

By Business Model: Hybrid Turnkey Gains as OEMs Seek Single-Source Accountability

Contract manufacturing maintained a 64.58% share in 2025, reflecting deep legacy agreements in industrial automation, telecom, and automotive electronics. Yet hybrid and turnkey models post a 6.81% CAGR because OEMs want single-invoice accountability for materials procurement, design verification, and compliance paperwork. In AI-server assembly, hyperscalers specify performance envelopes and delegate sourcing risk for high-bandwidth memory and substrates to their electronics manufacturing services partner, paying a 5-8% premium to reduce allocation surprises. Hybrid agreements also dominate new medical-device NPIs, where OEMs co-own tooling but the contractor manages FDA audits. Original design manufacturing remains a niche for North America electronics manufacturing services participants, concentrated in consumer peripherals and carrier-branded IoT nodes, yet cloud appliance vendors increasingly adopt design assistance to minimize reliance on in-house hardware teams.

Jabil’s North Carolina AI campus typifies the hybrid model: customers retain firmware, while Jabil co-invests in automation and owns test fixtures, delivering speed advantages that consignment shops cannot match. Kimball Electronics discloses over 30% revenue concentration across its top three auto clients, signaling that traditional contract manufacturing carries customer-dependency risk. As OEMs prioritize supply resilience over marginal cost, turnkey agreements penetrate deeper into automotive and defense, reshaping revenue mix through 2031.

By Manufacturing Process: Advanced Packaging Rises With AI Accelerator Complexity

Surface-mount technology (SMT) held a 53.47% share in 2025 after decades of capital investment, yet growth has tracked below the market average because advanced packages absorb incremental spend. The North America EMS market size tied to 2.5D interposers, fan-out wafer-level, and chiplet assembly will climb at a 6.97% CAGR through 2031 as AI and high-bandwidth-memory designs exceed SMT thermal and signal limits. Through-hole remains vital in rugged power supplies and military connectors, but loses share as press-fit and SMT variants improve vibration resistance. IPC Class 3 criteria are migrating toward consumer AI devices, boosting inspection intensity and favoring suppliers with automated optical and X-ray inspection lines. Jabil leverages Mikros Technologies’ micro-machined cold plates to address hot-spot densities above 150 W/cm², demonstrating that thermal IP and advanced packaging skills are increasingly intertwined.

Celestica recorded 17% year-over-year growth in datacenter revenue in Q3 2024 after adopting chiplet-ready substrates for graphics-processing-unit modules, illustrating an early-mover advantage. Automotive radar modules adopt antenna-in-package designs to shrink form factors while improving electromagnetic performance, shifting value from board-level to package-level assembly. Therefore, while SMT remains ubiquitous, the highest-profit pools are moving toward advanced packaging, where technical barriers safeguard margins against high-volume Asian entrants.

By End-User: Automotive Electrification Drives Fastest Segment Growth

Industrial electronics led with 38.93% of 2025 revenue, spread across factory automation, building systems, test equipment, and energy controls, where long product life cycles promote domestic production. Automotive electronics, however, records the strongest CAGR at 7.54% as electric-vehicle platforms and ADAS regulatory mandates multiply board content. A single battery-electric powertrain requires complex inverter, charger, and battery-management assemblies, each of which demands IPC Class 3 build quality and traceability. Communication infrastructure remains steady as 5G and edge gateways roll out, but OEMs are consolidating suppliers to those with global footprints, limiting small-shop participation. Medical devices yield superior margins, often above 12% gross, thanks to FDA and Health Canada audits that deter new entrants. Consumer electronics remains price-led; Asian mega-sites preserve dominance, but quick-turn prototypes still flow to local partners when product roadmaps compress.

Defense, aerospace, and LEO satellite ventures maintain captive demand under International Traffic in Arms Regulations constraints. SpaceX’s Starlink roadmap to 42,000 satellites supports recurring four-week PCB assembly runs across U.S. and Mexican sites. Over the forecast window, the automotive industry’s incremental USD 8-billion opportunity underpins above-market growth, ensuring the North America electronics manufacturing services market continues to diversify away from consumer handsets toward mission-critical hardware.

Geography Analysis

The United States accounted for 86.71% of regional electronics manufacturing services revenue in 2025, and is set to post the quickest growth at a 7.61% CAGR through 2031. The market is driven by clusters in Texas, California, Arizona, and North Carolina that host Tier-1 providers, semiconductor fabs, and defense primes. CHIPS Act funds concentrate wafer-fab and advanced packaging builds in Arizona, Ohio, and New York, but assembly capacity still lags, sustaining tight regional utilization. Defense and aerospace contracts, governed by ITAR and Buy America clauses, further anchor production, as OEMs cannot offload sensitive programs offshore. As a result, the North America electronics manufacturing services market enjoys a structural revenue floor even during semiconductor downturns.

Canada contributes a smaller base in the North America EMS market. The driver is niche specialization in aerospace avionics around Montreal and Toronto, and in regulated medical electronics near Ottawa, where OEMs value proximity to engineering hubs and regulatory agencies. Jabil’s August 2025 Ottawa expansion and Celestica’s longstanding aerospace programs validate the growth path. ISO 13485 adoption rates outpace U.S. averages, positioning Canada to capture spillover NPIs when U.S. Tier-1 lines are saturated.

Mexico benefits from USMCA rules of origin and logged USD 36.1 billion of foreign direct investment in 2023, much of it aimed at automotive harness and sensor-module lines in Guadalajara and Tijuana. Labor arbitrage remains attractive, yet OEMs increasingly locate higher-value radar, lidar, and camera builds here to balance cost with logistics. Electronics employment exceeded 700,000 workers by 2024, and the government promotes technical training pipelines to support the assembly of complex modules. While U.S. command of high-reliability defense and medical work caps Mexico’s upside, the country will still outpace SMT global averages as nearshoring accelerates.

Cross-border supply chains are tightening as semiconductor fabs in Arizona feed advanced-package substrates to Jalisco board plants, which then ship subassemblies to final system integrators in Texas. The arrangement keeps the North America electronics manufacturing services market costs competitive with Asia while meeting security requirements. However, rail and port congestion along the U.S.–Mexico border occasionally disrupts flow, highlighting infrastructure gaps that regional planners must fix to sustain the forecast trajectory.

The electronics manufacturing services market is assessed by Mordor Intelligence through a multi-layered geographic lens, covering other regions such as Europe and Asia, along with detailed country-level analysis for United States, Thailand, Singapore, United Kingdom, South Korea, Japan, and Germany.

Competitive Landscape

The North America electronics manufacturing services market shows moderate concentration: Jabil, Flex, Celestica, and Sanmina held an estimated 35-40% combined share in 2025, with the rest fragmented among Tier-2 specialists and captive operations. Asian heavyweights Foxconn, Pegatron, Compal, Quanta, and Wistron are building U.S. and Mexican facilities to serve hyperscale cloud providers and automotive OEMs, subject to ITAR and Buy America constraints, injecting fresh capacity and intensifying price competition. Strategy divides into scale players pursuing vertical integration and niche providers defending regulated verticals where FDA, IATF 16949, or ITAR certifications create barriers. Jabil’s acquisitions of Mikros Technologies and Hanley Energy Group exemplify the vertical-integration path, pairing thermal and power IP with assembly to win AI server contracts.

Plexus and Benchmark focus on medical and defense, leveraging ISO 13485 and AS9100 certifications to sustain double-digit margins even as consumer demand softens. Foxconn’s EV.OS platform threatens to commoditize automotive hardware by standardizing interfaces and shifting value to software, potentially eroding box-build pricing power if widely adopted. Technology adoption accelerates across the field: machine-vision-driven inline inspection, selective soldering, and AI-based process control cut defect escape rates to below 10 ppm in Class 3 builds, becoming table stakes by 2028. Players unable to fund automation upgrades risk margin erosion and client attrition. Capital-market sentiment turned positive when Lincoln International’s EMS index rebounded 20.7% in Q3 2025, reflecting investor belief that reshoring volume outweighs near-term labor and compliance costs.

Risk factors include component-allocation volatility in high-bandwidth memory, PFAS phase-out compliance expenses, and the aging skilled-labor pool. Nonetheless, white-space opportunities persist in advanced packaging, liquid-cooling assemblies, and quick-turn LEO satellite prototypes. Firms mastering these niches are poised to carve sustainable profit streams even as headline margins compress elsewhere.

North America Electronics Manufacturing Services Industry Leaders

Jabil Inc.

Flex Ltd.

Celestica Inc.

Sanmina Corporation

Plexus Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Oak Ridge National Laboratory completed a coolant-distribution-unit retrofit across its Frontier supercomputer, demonstrating 35% energy savings and opening service contracts for regional electronics manufacturing services providers.

- November 2025: Jabil acquired Hanley Energy Group, enhancing power-distribution and energy-storage solutions for AI datacenter and electric-vehicle charging customers.

- November 2025: Kimball Electronics opened a 308,000-square-foot Indianapolis medical-device plant, consolidating Tampa operations to gain scale in sterilization validation and traceability systems.

- November 2025: Plexus won Evolv Technology’s contract to co-develop AI-enabled security-screening hardware, leveraging rapid prototype and design-for-manufacturability expertise.

North America Electronics Manufacturing Services Market Report Scope

The North America Electronics Manufacturing Services Market Report is Segmented by Service Type (Electronics Manufacturing Services, Engineering Services, Test and Development Implementation Services, Logistics Services, Other Service Types), Business Model (Contract Manufacturing (CM), Original Design Manufacturing (ODM), Hybrid / Turnkey / Other Business Models), Manufacturing Process (Surface Mount Technology (SMT), Through-Hole Technology (THT), Advanced Packaging / Hybrid Processes), End-user (Mobile Devices, Consumer Electronics, Computer, Industrial, Automotive, Communication, Lighting, Medical, Other End-users), and Geography (North America). The Market Forecasts are Provided in Terms of Value (USD).

| Electronics Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | |

| Prototyping | |

| Other Electronics Manufacturing Services | |

| Engineering Services | |

| Test and Development Implementation Services | |

| Logistics Services | |

| Other Service Types |

| Contract Manufacturing (CM) |

| Original Design Manufacturing (ODM) |

| Hybrid / Turnkey / Other Business Models |

| Surface Mount Technology (SMT) |

| Through-Hole Technology (THT) |

| Advanced Packaging / Hybrid Processes |

| Mobile Devices (Smartphones and Tablets) |

| Consumer Electronics |

| Computer (PCs/Desktop/Laptops) |

| Industrial |

| Automotive |

| Communication |

| Lighting |

| Medical |

| Other End-users |

| North America | United States |

| Canada | |

| Mexico |

| By Service Type | Electronics Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | ||

| Prototyping | ||

| Other Electronics Manufacturing Services | ||

| Engineering Services | ||

| Test and Development Implementation Services | ||

| Logistics Services | ||

| Other Service Types | ||

| By Business Model | Contract Manufacturing (CM) | |

| Original Design Manufacturing (ODM) | ||

| Hybrid / Turnkey / Other Business Models | ||

| By Manufacturing Process | Surface Mount Technology (SMT) | |

| Through-Hole Technology (THT) | ||

| Advanced Packaging / Hybrid Processes | ||

| By End-user | Mobile Devices (Smartphones and Tablets) | |

| Consumer Electronics | ||

| Computer (PCs/Desktop/Laptops) | ||

| Industrial | ||

| Automotive | ||

| Communication | ||

| Lighting | ||

| Medical | ||

| Other End-users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

How large is the North America electronics manufacturing services market in 2026?

It generated USD 207.98 billion in 2026 and is forecast to reach USD 283.91 billion by 2031.

Which service type is growing fastest in regional electronics manufacturing?

Electromechanical assembly and box build is projected to expand at a 6.72% CAGR on demand for integrated system builds.

Why are automotive OEMs reshoring electronics assembly?

Electric-vehicle platforms and ADAS mandates raise board content and require quick-turn prototypes that local facilities deliver faster than offshore megasites.

What regulatory shift affects medical-device manufacturing timelines?

The February 2026 FDA Quality Management System Regulation harmonizes 21 CFR Part 820 with ISO 13485:2016, compelling OEMs to partner with certified contract manufacturers.

How does the CHIPS and Science Act influence regional capacity?

It allocates USD 36.4 billion to fabs and packaging plants, creating downstream demand for board-level and box-build lines that contract manufacturers now add across North America.

Which manufacturing process offers the highest margin upside?

Advanced packaging and hybrid processes, including 2.5D interposers and fan-out wafer-level techniques, carry higher margins due to technical complexity and capital intensity.

Page last updated on: