France Defense Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

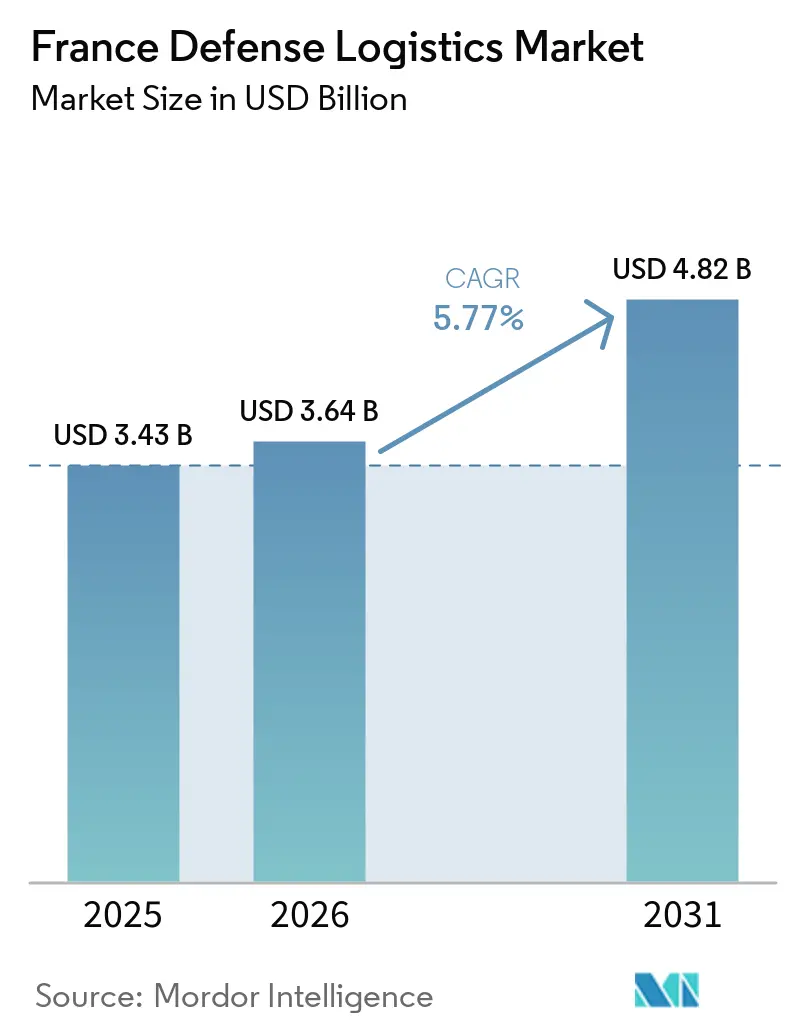

| Base Year Market Size (2025) | USD 3.43 Billion |

| Market Size (2026) | USD 3.64 Billion |

| Market Size (2031) | USD 4.82 Billion |

| Growth Rate (2026 - 2031) | 5.77% CAGR |

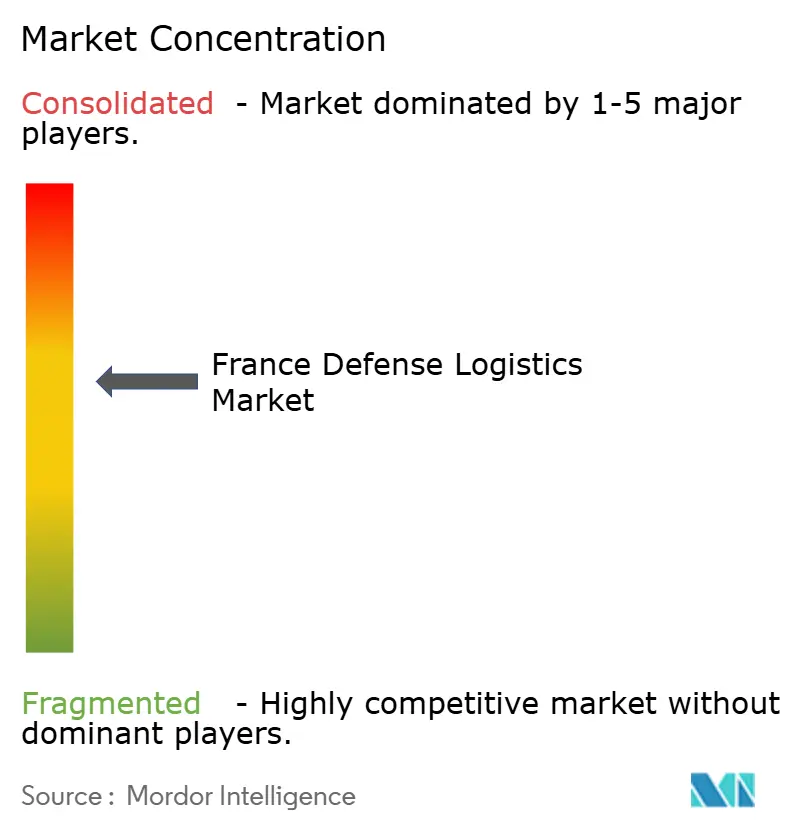

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Defense Logistics Market Analysis by Mordor Intelligence

The France defense logistics market size is expected to grow from USD 3.43 billion in 2025 to USD 3.64 billion in 2026 and is forecast to reach USD 4.82 billion by 2031 at 5.77% CAGR over 2026-2031.

The France defense logistics market is gaining support from the updated Military Programming Law, which sets a defense path of EUR 436 billion (USD 503.6 billion) through 2030, while the 2026 defense budget rises to EUR 57.1 billion (USD 65.9 billion) from EUR 50.4 billion (USD 58.2 billion) in 2025. The near-term spending pattern also favors readiness, as material maintenance credits rise 10% to EUR 6.5 billion (USD 7.5 billion) in 2026, which supports spare parts, maintenance flows, and in-service logistics rather than only new platform deliveries. The France defense logistics market is also being shaped by a shift from steady garrison support to high-intensity warfighting support, as France aligns with higher NATO readiness standards and draws lessons from the speed of replenishment seen in Ukraine. Competition in the France defense logistics market reflects a hybrid model where defense primes, MRO specialists, and civilian logistics groups all play active roles, with GEODIS taking part in ORION 26 and showing that civilian capacity is now tied more closely to military planning. The main limits remain supply dependence, budgetary timing pressures, and labor capacity, as France still depends heavily on Chinese rare-earth inputs for aerospace and defense needs. At the same time, the Ministry of Armed Forces plans to recruit 40,000 in 2026 to ease workforce pressure.

Key Report Takeaways

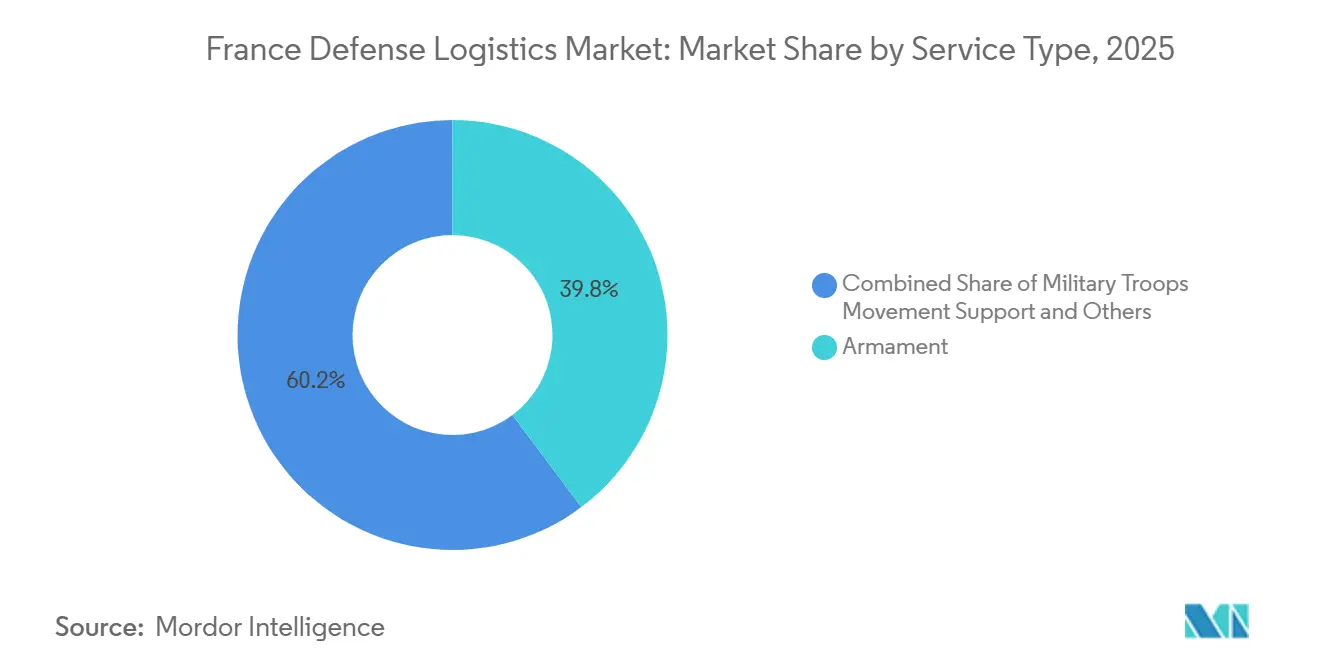

- By service type, armament held 39.77% of the France defense logistics market share in 2025, while medical aid and health services are projected to grow at an 8.61% CAGR through 2031.

- By logistics function, transportation accounted for 60.33% of the France defense logistics market size in 2025, while value-added services are forecast to expand at a 7.78% CAGR through 2031.

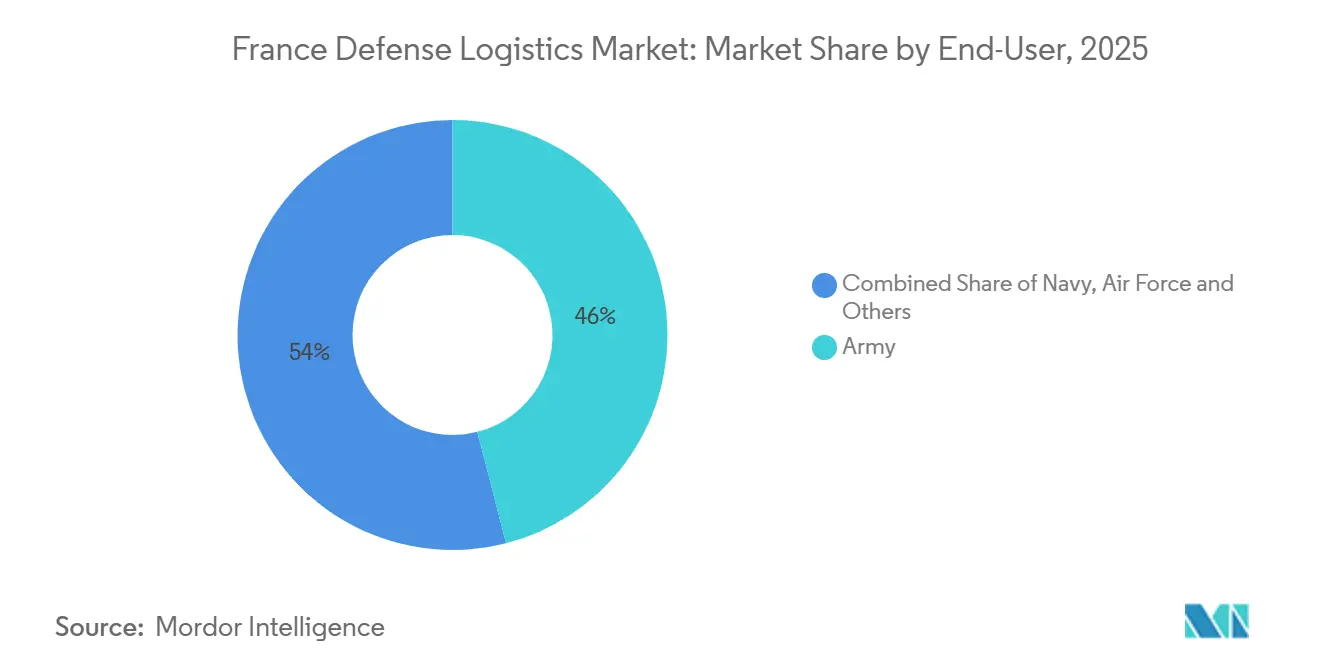

- By end user, the Army led with a 46.00% share in 2025, while the Air Force is projected to record the highest CAGR at 8.91% through 2031.

- By region, Ile-de-France captured 38.50% of the France defense logistics market in 2025, while Occitanie is projected to advance at a 7.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Defense Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Modernization Of Strategic Air- And Sea-Lift Fleets | +1.5% | National, with concentration in Brittany, Provence-Alpes-Cote d'Azur, and Ile-de-France | Medium term (2-4 years) |

| Outsourcing Of SIMMAD And MCO Service Contracts | +1.0% | National, the strongest pull in Nouvelle-Aquitaine and Ile-de-France | Short term (≤ 2 years) |

| NATO Readiness Stockpile Mandates | +0.9% | National, with early concentration in Hauts-de-France and Grand Est border regions | Short term (≤ 2 years) |

| Predictive-Maintenance Rollout | +0.7% | National, SCORPION-connected Army units across Ile-de-France and Center-Val de Loire | Medium term (2-4 years) |

| Climate-Resilient Logistics Infrastructure Upgrades | +0.5% | National, with heightened relevance in coastal Brittany and southern Provence-Alpes-Cote d'Azur | Long term (≥ 4 years) |

| Dual-Use Hubs For Space And Drone Operations Near Toulouse | +0.4% | Occitanie core, spill-over to Nouvelle-Aquitaine | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Modernization of Strategic Air- and Sea-Lift Fleets

The France defense logistics market is seeing larger service volumes as France renews its strategic lift and support fleets. The French Air and Space Force is moving toward 286 Rafale combat aircraft, and Sabena technics secured a 10-year CAROLUS support contract in December 2025 for the Franco-German C-130J and KC-130J fleet[1]Sabena Technics, “Sabena Technics Wins DMAé Contract For Franco-German C-130J Super Hercules Fleet Support,” Journal Aviation, journal-aviation.com. AFI KLM Engineering and Maintenance also signed a 10-year integrated support contract in December 2025 for France's 4 AWACS aircraft. Longer contract terms are pushing suppliers to hold deeper parts inventories and place support teams closer to operations, shifting more value toward domestic logistics specialists. A400M predictive maintenance results have already shown a 9% increase in available flight hours and a 7% decrease in maintenance hours, which support the wider use of data-linked supply chains in the France defense logistics market.

Outsourcing of SIMMAD and MCO Service Contracts

The France defense logistics market is expanding as military aviation support moves further toward outsourced and bundled service models. France's LPM 2024-2030 allocates EUR 49 billion (USD 56.5 billion) to aeronautical MCO, which is 40% above the prior plan, and directs annual payments of EUR 3 billion (USD 3.5 billion) toward spare parts and outsourced services. DMAe has stated that it will move from verticalized contracts to broader global support contracts from 2028, combining supply chain management, continuing airworthiness, and round-the-clock technical support within fewer commercial relationships. That change raises entry barriers for smaller providers, but it also creates larger contract scopes for companies that can manage full logistics performance. The Cour des comptes also pointed to room for competitiveness gains in current contract structures, suggesting tighter benchmarks and greater risk sharing in future awards.

NATO Readiness Stockpile Mandates

The France defense logistics market is benefiting from NATO readiness rules that require deeper and more reliable war-ready stocks. France's revised LPM includes an additional EUR 8.5 billion (USD 9.8 billion) for munitions through 2030, and the France Munitions platform is meant to work as a wholesale buyer that speeds industrial output. This has direct logistics effects because ammunition growth requires secure transport, protected storage, temperature-controlled handling of explosives, and heavier movement into border and staging zones. Hauts-de-France and Grand Est are well-positioned to absorb more of that activity due to their role in France's access to NATO reinforcement routes. KNDS France also signed a multi-year agreement with Les Forges de Tarbes for 60,000 to 150,000 155 mm shell bodies during 2026-2028, which adds more supplier-to-assembler flows inside the France defense logistics market.

Predictive-Maintenance Rollout (Plan SICS-SC2)

The France defense logistics market is also being reshaped by digital maintenance systems tied to the SCORPION program and its SICS backbone. Eviden received a DGA contract in June 2024 for SICS ALAT, with deployment expected in 2026 and 2027, so Army Light Aviation helicopters can connect with the wider Army tactical network[2]Eviden, “SICS ALAT To Be Embedded In The Aircraft Of The French Army Light Aviation By 2026,” Eviden, eviden.com. Real-time equipment data enables spare parts to be moved closer to expected demand, reducing emergency sourcing and altering warehouse planning. It also lowers the information gap that OEM parts suppliers have often held over buyers, which should support lower lifecycle costs even as service demand rises. Thales has reorganized its support capabilities to improve mission readiness for high-intensity Army operations, which shows that digital support intelligence is moving deeper into frontline service structures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budgetary Pressure From Social-Spending Trade-Offs | -0.6% | National, with fiscal constraints most visible in deferred procurement timelines | Short term (≤ 2 years) |

| Global Raw-Material And Component Shortages | -0.5% | National, with upstream pressure on Nouvelle-Aquitaine and Occitanie defense clusters | Medium term (2-4 years) |

| EU Carbon-Emission Caps On Military Transport | -0.3% | National, coastal logistics nodes, and air transport hubs are most affected. | Long term (≥ 4 years) |

| Aging Workforce In Logistics Corps | -0.2% | National, with acute pressure in specialized maintenance and warehousing roles | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Budgetary Pressure from Social-Spending Trade-Offs

The France defense logistics market still faces timing pressure between approved budgets and actual contract flow. Politico reported that France did not sign contracts at the pace implied by its war-economy messaging after the start of the Ukraine war, leaving some DTIB companies waiting after they had already invested to increase output[3]Politico, “France Wanted A War Economy. Here's Why Macron's Big Plan Fizzled,” Politico, politico.eu. For logistics providers, that gap can delay warehouse, transport, and distribution orders even when top-line defense plans look strong. The effect is strongest on medium-sized subcontractors, because they carry working capital pressure more directly than large primes. France's public debt level above 110% of GDP also keeps supplementary defense disbursements politically sensitive, which can delay realized demand into the forecast period.

Global Raw-Material and Component Shortages

The France defense logistics market is also limited by shortages that start upstream in chemicals, components, and rare earth supply. Europe's nitrocellulose production is estimated at 4,500 to 10,000 tons per year, against a combined NATO demand of nearly 20,000 tons, which limits how quickly munitions logistics can scale even when funding is available. France has restarted production at Bergerac through Eurenco, but the ramp-up is still underway. France also sources 90% of its aerospace-defense rare-earth needs from China, leaving logistics planning exposed to geopolitical disruption of critical inputs. These shortages lengthen lead times, increase safety stock levels, and raise the cost of urgent freight, narrowing margins in the France defense logistics market even as revenue grows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Armament Logistics Drives Volume, Healthcare Services Accelerate

Armament services held 39.77% of the France defense logistics market share in 2025, because ammunition handling, storage, transport, and distribution now sit closer to the center of defense readiness planning. France's munitions buildup and the planned France Munitions procurement platform support sustained demand for ordnance logistics through 2031. Military troops movement, support, technical support, and maintenance form the next tier, supported by logistics fleet renewal and broader integrated MCO activity. Fire-fighting protection and other services remain smaller because they are more closely linked to base support and fixed-site requirements than to field-deployment intensity.

Medical aid and health services are projected to grow at 8.61% CAGR from 2026 to 2031, making it the fastest-growing service line in the France defense logistics market. The Service de sante des armees and the General Directorate for Health signed a joint emergency preparedness charter in October 2025, which formalized civil-military coordination for mass-casualty scenarios. ORION 26 tested medical logistics for up to 250 patients per day over 60 days of sustained operations, underscoring the need for cold-chain drugs, pre-positioned surgical kits, and coordinated evacuation. That leaves the France defense logistics industry with a service niche where demand is rising quickly, but specialist capacity still looks limited.

By Logistics Function: Transportation Anchors the Market, Value-Added Services Gain Share

Transportation accounted for 60.33% of the France defense logistics market size in 2025, reflecting the heavy physical movement of troops, munitions, vehicles, and equipment across mainland France and overseas obligations. The January 2026 PL6T contract covers 7,000 military trucks and establishes a long-term delivery and support pipeline that prioritizes transport operations and fleet sustainment. Warehousing and distribution stands as the next layer, supported by higher stockpiles and more forward-positioned inventories near eastern routes. Civilian carrier networks also matter more now, because military exercises and surge plans increasingly rely on national road and multimodal capacity.

Value-added services are projected to grow at 7.78% CAGR through 2031, making it the fastest-moving logistics function in the France defense logistics market. The shift stems from contract complexity, as global support models require consulting, systems integration, and guaranteed-availability services in addition to physical freight and storage. Daher expanded its partnership with Safran in April 2026 by establishing a 3,000 m² MRO and AOG platform at Tremblay-en-France, designed to achieve a maximum emergency response time of 3.5 hours. That pattern favors established aerospace-logistics providers with quality and compliance capability, which strengthens entry barriers across the France defense logistics industry.

By End User: Army Leads Spending, Air Force Commands Fastest Growth

The Army held a 46.00% share in 2025, the largest end-user position in the French defense logistics market, because land-force operations absorb large volumes of vehicles, heavy equipment, troop movements, and ammunition flows. The PL6T truck program remains the clearest sign of Army logistics modernization, with militarization and support activity tied to facilities in Limoges, Garchizy, and Saint-Nazaire. The Navy is also gaining support from shipbuilding and export activity, which broadens sustainment and supplier movements around naval platforms. The others category, including space forces and cyber or special operations, is becoming more relevant as satellite ground support and drone sustainment needs rise.

The Air Force is projected to grow at 8.91% CAGR from 2026 to 2031, the fastest rate among end users in the France defense logistics market. Sabena technics won the 10-year CAROLUS contract for the C-130J and KC-130J fleets, and AFI KLM Engineering and Maintenance received a 10-year integrated AWACS support contract, indicating a clear shift from task-based maintenance to broader lifecycle support. This model increases value per aircraft but also requires deeper contractor investment in inventory, engineering support, and base-level response capability. Companies that can serve both Army volume demand and Air Force performance-based demand are better placed in the France defense logistics market than narrow single-domain providers.

Geography Analysis

Ile-de-France held 38.50% of the market in 2025, the largest regional position in the France defense logistics market, due to its control over procurement and contract management, as well as the concentration of many high-value support functions around the capital. The region benefits from the presence of DGA institutions, large prime contractor sites, and a dense network of Tier-2 service and maintenance suppliers. Daher expanded its aerospace logistics partnership with Safran in April 2026 through a platform at Tremblay-en-France, near Charles de Gaulle Airport, demonstrating how the region is moving toward faster air-linked response standards[4]Daher, “Aerospace Logistics, Daher Expands Its Partnership With Safran,” Daher, daher.com. Hauts-de-France and Grand Est are also gaining ground as secondary hubs because NATO reinforcement logic favors more forward storage of ammunition and heavy-vehicle staging closer to Belgium and Germany.

Occitanie is projected to grow at 7.15% CAGR through 2031, making it the fastest-growing geography in the France defense logistics market. Toulouse's EUR 80 million (USD 92.3 million) Space Command facility opened in November 2025 and now hosts nearly 600 personnel, including the NATO Space Center of Excellence, which gives the region a stronger role in space-related military logistics. The region also reports 25,000 defense jobs, or 15% of the national defense workforce, and its Defense and Future Industry Fund totals EUR 100 million (USD 115 million), with EUR 7 million (USD 8.1 million) dedicated to the drone sector. Local companies are scaling with that backdrop, as Delair's revenue rose from EUR 10 million (USD 11.5 million) in 2023 to EUR 50 million (USD 57.7 million) in 2025. The Francazal dual-use mobility park further strengthens the region by providing a testing ground for drones, autonomous systems, and next-generation supply chain systems.

Nouvelle-Aquitaine remains important in the France defense logistics market because Bordeaux-Merignac hosts DMAe and a dense aeronautical MCO base, which keeps aviation support and spare-parts flows concentrated in the region. Provence-Alpes-Cote d'Azur supports naval logistics around Toulon, while Brittany supports Atlantic naval access and sea-lift activity tied to Brest. Auvergne-Rhone-Alpes benefits from its link to the Franco-German industrial corridor and supports land-systems logistics and manufacturing flows. Normandy, the Center-Val de Loire, and the overseas territories play smaller but specialized roles in air-base support, deterrence infrastructure, and focused logistics capabilities.

Competitive Landscape

The France defense logistics market is moderately concentrated at the top, but it stays fragmented across mid-tier operators and specialist service niches. Large groups such as Airbus Defense and Space, Thales, Safran, Naval Group, KNDS, Daher, and Sabena Technics compete for the highest-value bundled support scopes. In contrast, transport groups and specialist providers address narrower functions across warehousing, distribution, and sustainment. This structure gives large players an advantage in complex contracts, but it still leaves room for many smaller firms in local execution, component support, and specialized maintenance. The France defense logistics market therefore combines concentration in strategic contracts with wide dispersion in day-to-day operational delivery.

Strategic moves in the France defense logistics market show how primes and logistics companies are widening their roles. GEODIS participated in ORION 26, which confirms that civilian third-party logistics capacity is now integrated into defense planning rather than used solely as an emergency overflow. Daher expanded its Safran partnership in April 2026 with a dedicated MRO and AOG logistics platform, which shows how response-time commitments are becoming more central to contract value. Sabena Technics also secured the CAROLUS contract, which combines support infrastructure, supply chain management, and 24/7 technical services around the Franco-German C-130J fleet. Those examples show that contract winners are the firms that can connect physical logistics, maintenance execution, and readiness commitments within one accountable model.

White space in the France defense logistics market remains strongest in predictive sub-tier logistics, medical logistics for sustained high-intensity scenarios, and lower-carbon transport capability. That gap matters because many smaller suppliers still do not operate at scale across the full chain from component flow to operational support. EU transport emissions accounting will also draw more attention to certified, lower-carbon logistics practices over time. Companies that can meet military security needs while also handling traceability, reliability, and environmental compliance should strengthen their position as procurement rules become broader.

France Defense Logistics Industry Leaders

Airbus Defence and Space

Thales Group

Safran

Naval Group

Arquus

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Daher announced 2 new logistics contracts with Safran, including a 3,000 m² MRO and AOG platform at Tremblay-en-France for Safran Electronics and Defense, and a Safran Nacelles warehouse in Hamburg, operations began in April 2026.

- March 2026: At the Brussels European Defense Exhibition, KNDS CBRN inked deals for a new gas mask and the ESSENTIAL DECON decontamination systems. Additionally, the French Army is set to receive 21 L-01 decontamination trucks by 2028.

- January 2026: Arquus (a subsidiary of John Cockerill) and Daimler Truck secured a contract from the French Ministry of Armed Forces for the PL6T logistics carrier program, set to span over a decade. The militarization of Arquus's Zetros will take place in Limoges, Garchizy, and Saint-Nazaire.

- December 2025: At Evreux Air Base 105, DMAe inked a deal with Sabena Technics for the long-term maintenance and operational support of its 10-aircraft Franco-German C-130J/KC-130J fleet. The comprehensive contract encompassed supply chain management, round-the-clock technical assistance, and logistics infrastructure at both Bordeaux and Evreux.

France Defense Logistics Market Report Scope

| Armament |

| Military Troops Movement Support |

| Technical Support & Maintenance |

| Medical Aid & Health Services |

| Fire-fighting Protection |

| Other Services |

| Transportation | Road |

| Air | |

| Sea and Inland Waterways | |

| Rail | |

| Warehousing & Distribution | |

| Value-added Services (Labelling, Kitting, Consulting) |

| Army |

| Navy |

| Air Force |

| Others |

| Ile-de-France |

| Auvergne-Rhone-Alpes |

| Provence-Alpes-Cote d'Azur |

| Hauts-de-France |

| Nouvelle-Aquitaine |

| Occitanie |

| Grand Est |

| Brittany |

| Others |

| By Service Type | Armament | |

| Military Troops Movement Support | ||

| Technical Support & Maintenance | ||

| Medical Aid & Health Services | ||

| Fire-fighting Protection | ||

| Other Services | ||

| By Logistics Function | Transportation | Road |

| Air | ||

| Sea and Inland Waterways | ||

| Rail | ||

| Warehousing & Distribution | ||

| Value-added Services (Labelling, Kitting, Consulting) | ||

| By End User | Army | |

| Navy | ||

| Air Force | ||

| Others | ||

| By Region | Ile-de-France | |

| Auvergne-Rhone-Alpes | ||

| Provence-Alpes-Cote d'Azur | ||

| Hauts-de-France | ||

| Nouvelle-Aquitaine | ||

| Occitanie | ||

| Grand Est | ||

| Brittany | ||

| Others | ||

Key Questions Answered in the Report

What is the 2026 size of France defense logistics?

The France defense logistics market is valued at USD 3.64 billion in 2026.

Which service area leads spending in France?

Armament logistics leads with 39.77% share in 2025 because ammunition handling, secure storage, and transport now carry greater readiness importance.

Which logistics function is growing fastest through 2031?

Value-added services are projected to grow at 7.78% CAGR as contracts increasingly bundle consulting, systems integration, and guaranteed availability support.

Which military branch is expanding logistics demand the fastest?

The Air Force is the fastest-growing end user, with a 8.91% CAGR, driven by long-term integrated support contracts and fleet modernization.

Which French region offers the strongest logistics growth outlook?

Occitanie is the fastest-growing region, with a 7.15% CAGR, supported by Toulouse's space command presence, drone activity, and defense-space infrastructure.

What are the biggest risks to growth through 2031?

The main limits are budgetary timing pressure, shortages of chemicals and rare-earth inputs, and workforce constraints in specialized maintenance and warehousing roles.

Page last updated on: