United States Defense Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

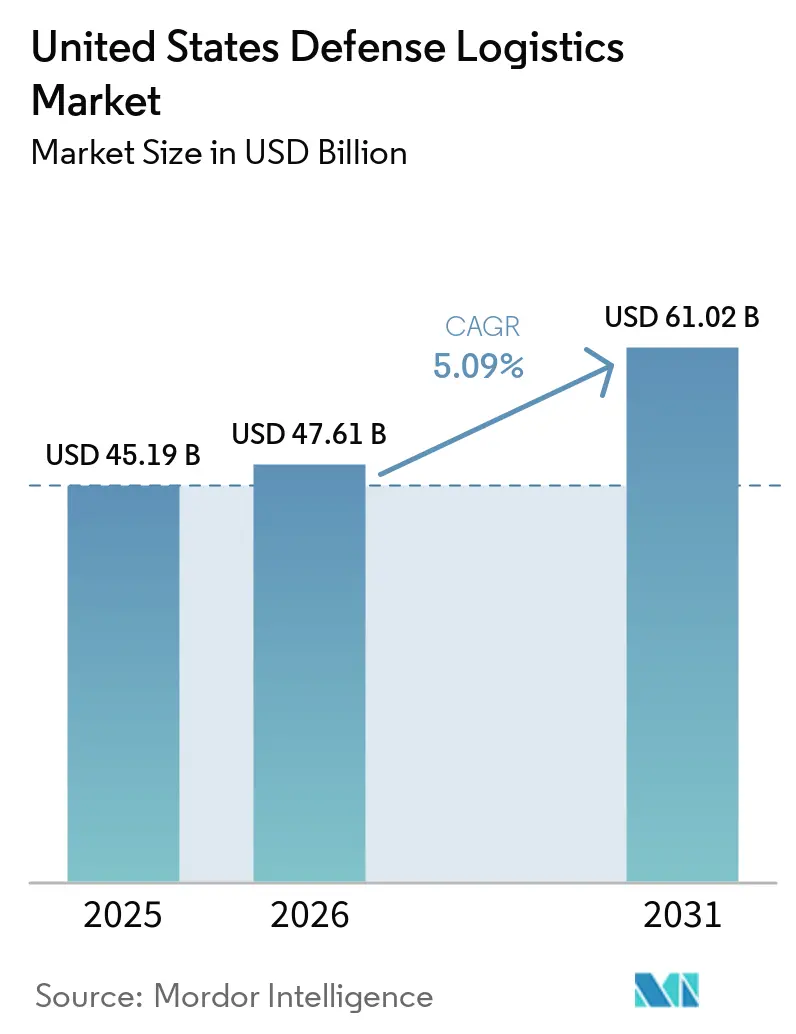

| Base Year Market Size (2025) | USD 45.19 Billion |

| Market Size (2026) | USD 47.61 Billion |

| Market Size (2031) | USD 61.02 Billion |

| Growth Rate (2026 - 2031) | 5.09% CAGR |

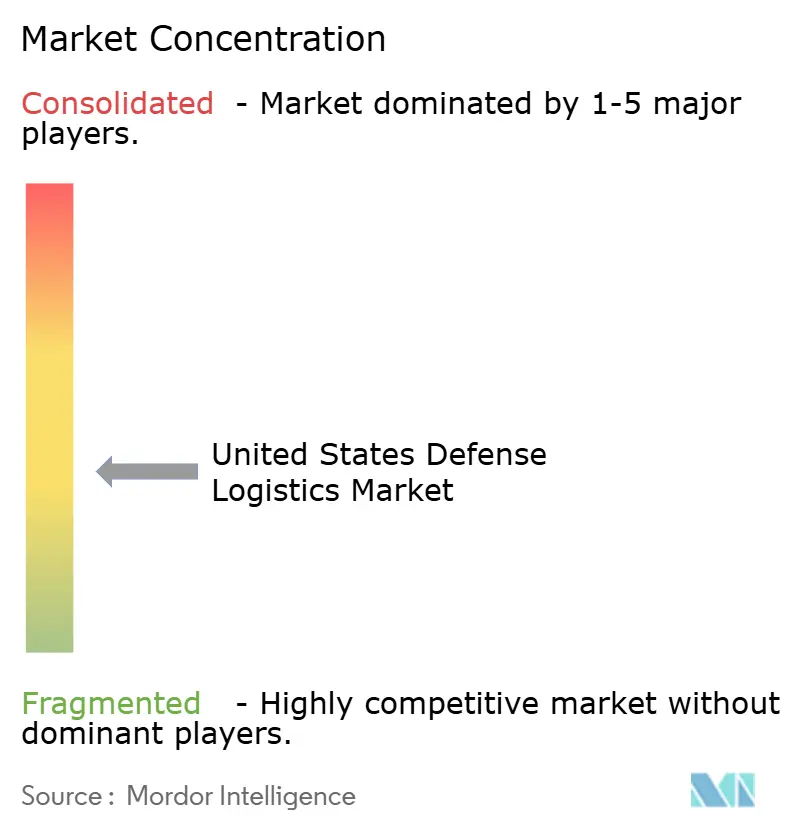

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Defense Logistics Market Analysis by Mordor Intelligence

The United States defense logistics market size was valued at USD 45.19 billion in 2025 and is estimated to grow from USD 47.61 billion in 2026 to reach USD 61.02 billion by 2031, at a CAGR of 5.09% during the forecast period 2026 to 2031.

The United States defense logistics market is expanding because the Department of Defense entered 2026 with a materially higher procurement pipeline, stronger munitions replenishment needs, and continued shipbuilding and missile spending that have kept transportation, warehousing, and sustainment demand elevated for multiple years. The United States defense logistics market also benefits from sustained operating requirements across the Indo-Pacific and Central Command theaters, since longer distances and distributed deployments require larger stock positioning, more frequent movement, and heavier coordination between depots and forward locations. The Defense Logistics Agency’s warehouse modernization program and the broader push toward predictive logistics are raising the technology content in service contracts, supporting higher-value work for firms that can integrate systems, data, and physical distribution workflows.

Key Report Takeaways

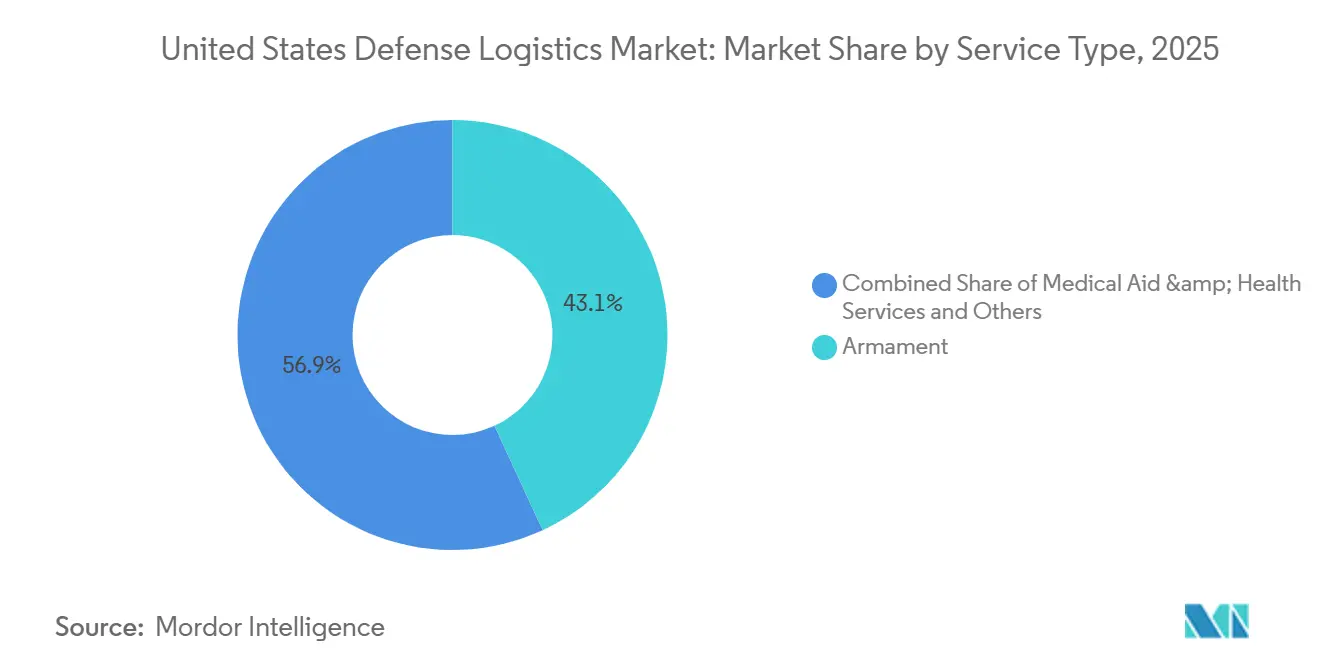

- By service type, armament accounted for 43.11% of the United States defense logistics market size in 2025, while medical aid and health services are forecast to expand at a 7.93% CAGR through 2031.

- By logistics function, transportation accounted for 64.73% of the United States defense logistics market share in 2025, while value-added services are projected to grow at a 7.10% CAGR through 2031.

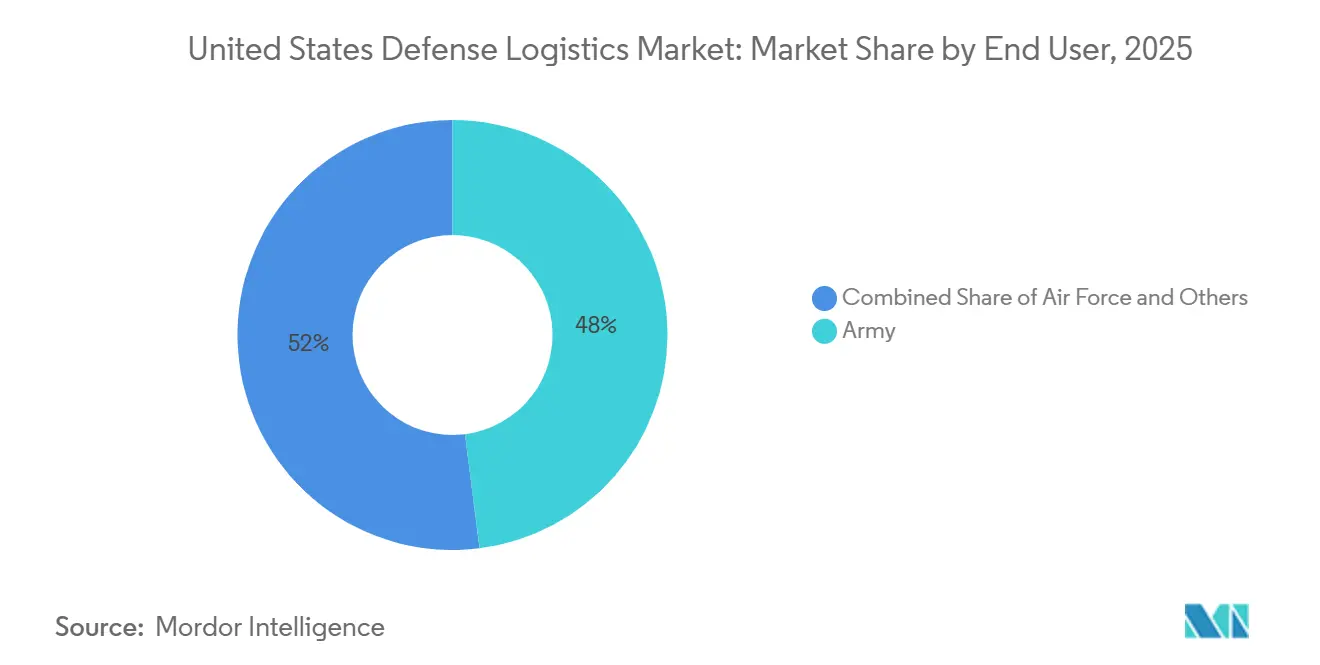

- By end user, the army accounted for 47.95% of revenue in 2025, while the air force is expected to record the highest CAGR of 8.23% through 2031.

- By region, the southeast represented 29.6% of revenue in 2025, while the Southwest is forecast to grow at a 6.47% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Defense Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising DoD Procurement for Sustainment and Modernization | +1.5% | National, concentrated at CONUS depots in the Southeast and Southwest | Short term (≤ 2 years) |

| Indo-Pacific Pivot Boosting Pre-Positioned Stocks | +1.2% | Asia-Pacific core, with procurement pull-through to CONUS | Medium term (2-4 years) |

| Digital Transformation and AI-Enabled Predictive Logistics | +0.8% | Global, with early gains at CONUS distribution centers and Transcom operating areas | Medium term (2-4 years) |

| DLA WMS Roll-Out Unlocking Outsourced 3PL Demand | +0.5% | National, concentrated at DLA Distribution hubs in the Southeast and Midwest. | Short term (≤ 2 years) |

| Net-Zero Mandates Spurring Electric and Autonomous Base Fleets | +0.4% | National, with early adoption at Air Force and Navy installations | Medium term (2-4 years) |

| Warstopper and Industrial-Base Funds for Niche Suppliers | +0.3% | National, targeting specialty munitions and component manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising DoD Procurement for Sustainment and Modernization

The Pentagon’s FY2026 procurement budget stands near USD 205 billion, up from the FY2025 enacted procurement of USD 174 billion, and that increase directly expands the logistics workload associated with receiving, storing, transporting, and maintaining new equipment and spare parts. Reconciliation spending also includes a USD 25 billion munitions envelope, which supports armament handling, depot throughput, and secure transportation across the United States defense logistics market. The demand is not limited to the initial procurement year, because logistics costs continue throughout the life of each platform, thereby extending contract visibility for firms with established sustainment capacity. Reverse logistics also remains important because the Defense Logistics Agency processed property originally valued at USD 232 billion in FY2025 and reutilized 2.4 million items valued at USD 2 billion, demonstrating that disposal, recovery, redistribution, and reuse continue to generate workload beyond forward delivery[1]Defense Logistics Agency, “DLA FY 2024 History,” Defense Logistics Agency, dla.mil. As the 2026 budget is executed and follow-on plans are shaped, contractors with proven depot support, hazardous material handling, and inventory management records are positioned to capture recurring work across the United States defense logistics market. This maintains revenue durability even as acquisition cycles eventually moderate.

Indo-Pacific Pivot Boosting Pre-Positioned Stocks

The strongest structural shift in the United States defense logistics market remains the Indo-Pacific posture, where theater scale, distributed islands, and long sea and air routes require more inventory nodes and more resilient sustainment planning. The Marine Corps also established a new prepositioning program at Subic Bay. They evaluated additional sites in Palau and Australia, while the Navy pursued a large, climate-controlled storage facility in the Philippines under a 10-year lease. Joint exercises also validated forward arming and refueling concepts near the first island chain, indicating rising demand for fuel handling, ammunition staging, and rapid resupply services in austere settings. Japan’s 2026 Indo-Pacific deployment schedule adds another layer of multinational sustainment coordination, and that supports more contracting activity for transportation, warehousing, and forward support across the United States defense logistics market. The result is a wider logistics footprint that depends less on single hubs and more on flexible commercial and military distribution links.

Digital Transformation and AI-Enabled Predictive Logistics

Digital transformation is becoming a material growth lever for the United States defense logistics market because service buyers now want visibility, forecasting, and decision support embedded directly inside sustainment programs. United States Transportation Command said in April 2026 that AI-enabled visualization and smart systems are being used to manage multi-theater logistics, improve situational awareness, and support faster resupply decisions under active operational conditions. The Army’s PORTAL program reinforced that shift in March 2026, when Gallatin AI and Rune Technologies received awards for edge-first logistics software that can forecast demand for fuel, munitions, and parts without relying on central servers[2]Rune Technologies, “U.S. Army Awards Rune Technologies USD 2M for Predictive Logistics Platform,” Rune Technologies, runetech.co . The Defense Innovation Unit also moved sustainment planning further toward predictive models in 2025, supporting a broader shift from reactive distribution to earlier intervention and better allocation of constrained assets. As logistics decision support is treated more like an operational capability, the technology value within each contract increases, expanding the addressable scope for software-enabled providers in the United States defense logistics market. This trend also rewards firms that can combine cybersecurity, integration, and physical distribution rather than offering only one part of the service chain.

DLA WMS Roll-Out Unlocking Outsourced 3PL Demand

The Defense Logistics Agency’s warehouse modernization program is creating practical demand for system integration, migration support, and commercial warehousing capability inside the United States defense logistics market. By the end of FY2024, the enterprise-wide SAP Warehouse Management System had reached 22 of 34 DLA distribution centers, and the program then moved through major implementations at high-volume locations, including Susquehanna and overseas distribution points. The new platform replaces legacy tools with a more auditable and connected environment that aligns more closely with commercial operating practices. That change matters because smoother interoperability lowers a long-standing barrier to outsourcing routine kitting, cross-docking, labeling, and inventory execution work to third-party providers. It also raises the value of firms that can connect warehouse automation, enterprise software, and daily operating procedures in a single delivery model. The modernization path, therefore, expands the service mix inside the United States defense logistics market, even when the physical square footage of warehouse networks changes only gradually.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vendor Base Contraction and Supply-Chain Fragility | -1.0% | National, most acute in Tier-2 and Tier-3 specialty manufacturing in the Midwest and Southeast | Long term (≥ 4 years) |

| Federal Budget Uncertainty and Continuing Resolutions Delaying Contract Awards | -0.8% | National, concentrated on CONUS-based primes and subcontractors | Short term (≤ 2 years) |

| PFAS Remediation Inflating Infrastructure Costs | -0.4% | National, with the highest impact at Air Force and Army installations in the Southwest and Southeast | Long term (≥ 4 years) |

| Zero-Trust Cyber Compliance Slowing System Roll-Outs | -0.3% | National, with global implications for coalition-facing logistics IT systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Vendor Base Contraction and Supply-Chain Fragility

Supplier fragility remains a restraint on the United States defense logistics market because logistics performance depends on stable access to components, specialized materials, and qualified maintenance inputs. Naval Postgraduate School research in 2026 found that more than 84% of prime contractors lacked visibility beyond Tier-1 suppliers, which means disruptions in castings, energetics, bearings, and similar inputs can surface late and delay program execution. Certification and cyber compliance costs add more pressure on smaller firms that were already operating with limited capital and narrow labor pools. Business Executives for National Security also warned in 2025 that a large wave of small-business ownership transitions is approaching, increasing the risk of exits or consolidation among specialized suppliers that are difficult to replace. In practical terms, a thinner supplier base can slow replenishment cycles, reduce pricing flexibility, and increase the need for working capital buffers across the United States defense logistics market. That is especially relevant in ammunition, aviation parts, and other categories where alternate sourcing is limited.

Federal Budget Uncertainty/CRs Delaying Contract Awards

Budget uncertainty continues to weigh on the United States defense logistics market because continuing resolutions delay new starts and reduce planning clarity for both prime contractors and their supplier networks. Congressional Research Service reporting on FY2025 appropriations shows that defense funding moved through short-term continuing resolutions before a full-year outcome was reached. That pattern has become common enough to shape operating behavior across the procurement chain. When those stopgap periods extend, task orders move later, bridge contracts last longer, and depot-level inventory planning becomes less efficient. Contractors are then left carrying labor, transportation, and fuel cost increases against older pricing assumptions, which limits margin quality even when headline demand is still intact. The FY2026 structure added another layer of uncertainty because suppliers had to assess which spending items were part of the base budget and which depended on the timing of reconciliations. That timing mismatch can delay hiring, investment, and supplier commitments at the very moment the United States defense logistics market is being asked to absorb a larger operational load.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Armament Logistics Anchored by Drawdown-Driven Replenishment

Armament held 43.11% of the United States defense logistics market size in 2025, making it the largest service type. Its leading position reflects ongoing munitions drawdowns, replenishment demand, and a 2026 funding environment that continues to prioritize procurement and supply-chain support for weapons inventories. The operating pattern is broader than a short procurement wave because live theater support and war reserve rebuilding occur in parallel, creating sustained throughput at depots and distribution sites. Contractors with hazardous-material transport qualifications, secure storage capacity, and certified handling processes remain well-positioned under this demand structure. The scale and sensitivity of munitions movement also limit the number of providers that can compete across the full workflow, which supports repeat business for established performers.

Medical aid and health services are the fastest-growing service type. They are projected to expand at a 7.93% CAGR through 2031, supported by evolving casualty care requirements and heightened evacuation readiness in dispersed theaters. That keeps medical supply positioning, cold-chain support, and field response logistics relevant to future contracting scopes. Military troop movement, firefighting protection, and other services add a stable base of recurring activity, and together they keep the United States defense logistics industry tied not only to combat resupply but also to installation continuity, readiness support, and contingency planning.

By Logistics Function: Transportation Dominates but Value-Added Services Accelerate

Transportation accounted for 64.73% of the United States defense logistics market share in 2025, confirming that movement remains the central function within the United States defense logistics market. The share is supported by the need to connect CONUS depots, industrial sites, ports, air bases, and forward operating locations through road, air, and sea networks. Organic military lift remains important, but commercial carriers continue to play a material role in non-tactical distribution and in surge support where flexibility matters. This structural need is unlikely to change because a geographically dispersed force requires frequent inter-depot movement, last-mile delivery, and time-sensitive replenishment. As Indo-Pacific pre-positioning expands, the transportation function should remain the largest part of the cost base over the forecast period.

Value-added services are the fastest-growing logistics function, and the United States defense logistics market size for value-added services is projected to expand at a 7.10% CAGR between 2026 and 2031. Labeling, kitting, supply-chain consulting, data migration, and process redesign are becoming more relevant as the DLA warehouse modernization program changes how public and private systems connect. Warehousing and distribution sit between the two ends of the function mix, benefiting from network modernization while also facing pressure to automate routine activity. The Army’s PORTAL work suggests that some planning and forecasting tasks may gradually become more standardized, potentially shifting future value toward providers that combine physical execution with software integration rather than offering stand-alone consulting. That keeps the United States defense logistics industry focused on hybrid service models where transport, visibility, and digital workflow support are sold together.

By End User: Air Force Outpaces Army and Navy on Growth Trajectory

The Army held 47.95% of the United States defense logistics market share in 2025, making it the largest end-user. That position reflects the scale of Army sustainment needs across training bases, overseas garrisons, ammunition sites, pre-positioned stock locations, and deployed formations. Army demand is broad rather than narrow, spanning ground systems, fuel, engineering stores, medical support, and recurring transport across a wide site network. It also remains the service most directly tied to the redistribution of pre-positioned stocks and the movement of land-based equipment across multiple theaters. This gives the Army a large and persistent pull on depot, warehousing, and transportation contracts.

The Air Force is the fastest-growing end user and is forecast to grow at a 8.23% CAGR through 2031, supported by base-fleet electrification activity, transport aircraft sustainment awards, and the continued expansion of digital logistics support tools. Northrop Grumman’s overseas contractor logistics support for Air Force platforms in South Korea, Japan, and Italy also shows that Air Force demand is increasingly tied to distributed support requirements rather than solely to domestic base operations. The others category, which includes the Space Force and special operations elements, should also grow steadily because those missions rely on secure sustainment and dispersed operational support. As a result, the United States defense logistics market is becoming more balanced across end users, even though the Army remains the largest buyer today.

Geography Analysis

The Southeast accounted for 29.6% of the United States defense logistics market share in 2025, giving it the largest regional share. That lead comes from the dense concentration of military installations, depot maintenance capacity, and contractor logistics hubs across states, including Virginia, Georgia, North Carolina, and Florida. The DLA warehouse management system go-live at Warner Robins in February 2026 shows that the region remains central to distribution modernization and physical sustainment execution[3]Defense Logistics Agency, “Warehouse Management System Implemented at DLA Distribution Warner Robins,” DLA News, dla.mil. The Southeast also faces meaningful environmental compliance pressure because PFAS cleanup requirements continue to influence infrastructure planning and capital allocation at legacy military sites.

The Southwest is forecast to record the fastest regional growth, with the United States defense logistics market size for the Southwest advancing at a 6.47% CAGR from 2026 to 2031. Growth there is supported by Army aviation activity, ordnance handling, special operations logistics, and a broad installation footprint that keeps transport and sustainment demand active. The region also carries a larger compliance burden at selected bases, which can increase facility reconfiguration work even when operating budgets are tight. The Midwest remains more stable than fast-growing, but it stays important because it houses ammunition plants and a meaningful share of sub-tier industrial suppliers. That makes the Midwest a region to watch for consolidation, supplier exit, and capacity risk as smaller firms absorb higher cyber and certification costs.

The Northeast continues to benefit from naval infrastructure, high-volume distribution activity, and the Washington-area contractor ecosystem. The DLA’s largest SAP WMS deployment at Defense Distribution Susquehanna reinforces the Northeast’s role as a critical node for eastern CONUS flows and inventory visibility improvements. The West is most closely tied to Pacific operations because California, Washington, and Hawaii support trans-Pacific movement, planning, and forward theater linkage. Hawaii remains central because USINDOPACOM planning is coordinated there, even as more operational stocks move westward toward partner sites in the Philippines, Australia, Japan, and other forward locations. California also adds a stricter compliance environment for facility operators, which can make leased operating models more attractive than fully owned infrastructure in some parts of the United States defense logistics market.

Competitive Landscape

The United States defense logistics market remains moderately fragmented, with the top 5 participants accounting for only around 45% of revenue, leaving a large secondary field of mid-market providers and commercial logistics companies competing for transportation, base support, warehousing, and integration work. Large defense primes still hold an advantage in long-cycle contractor logistics support because they can pair platform expertise with recurring maintenance, software, and training services. Lockheed Martin’s April 2026 C-130J MATS IV award, with a ceiling of up to USD 1.9 billion, is a clear example of how a prime can extend platform-related sustainment revenue across multiple services for a decade[4]Lockheed Martin, “Pentagon Awards Lockheed Martin Up to USD 1.9 Billion to Continue C-130J Maintenance and Aircrew Training System Program,” Lockheed Martin News, lockheedmartin.com. Northrop Grumman’s Air Force logistics support modification, which lifted cumulative contract value to USD 596 million through April 2027, shows a similar pattern in overseas support. These contracts are hard to displace because they combine maintenance, training, parts support, and digital tools into a single performance structure.

Mid-market contractors remain competitive because they can scale quickly in base operations and expeditionary support without needing control over original platforms. KBR’s LOGCAP V task order modifications in May 2026 and its AFCAP V task orders in Southwest Asia show that life-support and theater support contracts still offer meaningful room for growth outside the prime. Commercial specialists such as FedEx Government Services, J.B. Hunt, and Schneider National are also finding space in non-tactical distribution as public warehousing systems become more compatible with commercial practices. The DLA warehouse modernization path supports that opening because better interoperability lowers switching barriers and makes outsourced execution easier to manage. At the same time, digital reporting and systems integration are becoming more important differentiators in recompete decisions.

A second competitive shift is the rising role of cyber-enabled logistics infrastructure. Corsha’s April 2026 sole-source IDIQ with the Defense Logistics Agency shows that machine-identity security and Zero Trust connectivity are now being applied directly to fuel systems, advanced manufacturing controls, and building management assets inside logistics operations. Providers that can integrate operational technology security with daily logistics execution should have a durable advantage as compliance demands tighten. Another open area is contested-environment predictive logistics, where early Army awards suggest there is still room for capable firms to move from prototype work into larger-scale production support. The supplier stabilization gap also creates room for acquisition and consolidation strategies among firms that can finance certification and operational upgrades for smaller niche providers. That combination of fragmented share, recurring sustainment demand, and rising digital complexity should keep the United States defense logistics market competitive through 2031.

United States Defense Logistics Industry Leaders

Lockheed Martin

Northrop Grumman

RTX Corporation (Raytheon business units)

General Dynamics

Boeing Defense, Space & Security

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: KBR received two firm-fixed-price task orders under AFCAP V for transient aircraft services across Southwest Asia and dining facility services at Al Dhafra Air Base, UAE, with a combined ceiling exceeding USD 41 million.

- April 2026: The Pentagon awarded Lockheed Martin a 10-year, sole-source IDIQ contract worth up to USD 1.9 billion for the C-130J Maintenance and Aircrew Training System (MATS) IV program, expanding coverage to the U.S. Navy Reserve and U.S. Coast Guard and cementing Lockheed's multi-service sustainment mandate for the C-130J fleet.

- April 2026: The United States Air Force awarded Northrop Grumman a USD 207.9 million contract modification for overseas contractor logistics support at bases in South Korea, Japan, and Italy, bringing the cumulative contract value to USD 596 million through April 2027.

- April 2026: The Defense Logistics Agency awarded Corsha a USD 50 million sole-source IDIQ to deliver identity-driven zero-trust connectivity across DLA's mission-critical operational technology, including fuel distribution, advanced manufacturing, and building management systems. The award is the first of its kind to apply machine-identity cybersecurity directly to core logistics infrastructure at scale.

United States Defense Logistics Market Report Scope

| Armament |

| Military Troops Movement Support |

| Technical Support & Maintenance |

| Medical Aid & Health Services |

| Fire-fighting Protection |

| Other Services |

| Transportation | Road |

| Air | |

| Sea and Inland Waterways | |

| Rail | |

| Warehousing & Distribution | |

| Value-added Services (Labelling, Kitting, Consulting) |

| Army |

| Navy |

| Air Force |

| Others |

| Northeast |

| Southeast |

| Midwest |

| Southwest |

| West |

| By Service Type | Armament | |

| Military Troops Movement Support | ||

| Technical Support & Maintenance | ||

| Medical Aid & Health Services | ||

| Fire-fighting Protection | ||

| Other Services | ||

| By Logistics Function | Transportation | Road |

| Air | ||

| Sea and Inland Waterways | ||

| Rail | ||

| Warehousing & Distribution | ||

| Value-added Services (Labelling, Kitting, Consulting) | ||

| By End User | Army | |

| Navy | ||

| Air Force | ||

| Others | ||

| By Region | Northeast | |

| Southeast | ||

| Midwest | ||

| Southwest | ||

| West | ||

Key Questions Answered in the Report

What is the 2026 value of the United States defense logistics market?

The United States defense logistics market is valued at USD 47.61 billion in 2026.

Which service type leads defense logistics spending in the United States?

Armament is the largest service type, holding 43.11% of revenue in 2025, supported by munitions replenishment and stockpile rebuilding.

Which logistics function is growing the fastest through 2031?

Value-added services are the fastest-growing logistics function with a 7.10% CAGR, driven by warehouse system upgrades, integration work, and outsourced process support.

Which military branch is expanding logistics demand the fastest?

The Air Force is the fastest-growing end user, with an 8.23% CAGR through 2031, supported by airlift sustainment, electrification, and digital logistics programs.

Which United States region has the largest defense logistics footprint?

The Southeast led with 29.6% of revenue in 2025 due to its dense cluster of depots, military installations, and contractor support hubs.

What is the main long-term factor shaping future defense logistics demand?

The Indo-Pacific posture is the main long-term driver because distributed operations across long distances require larger pre-positioned stocks, more transport capacity, and stronger forward sustainment networks.

Page last updated on: