Switzerland Freight And Logistics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

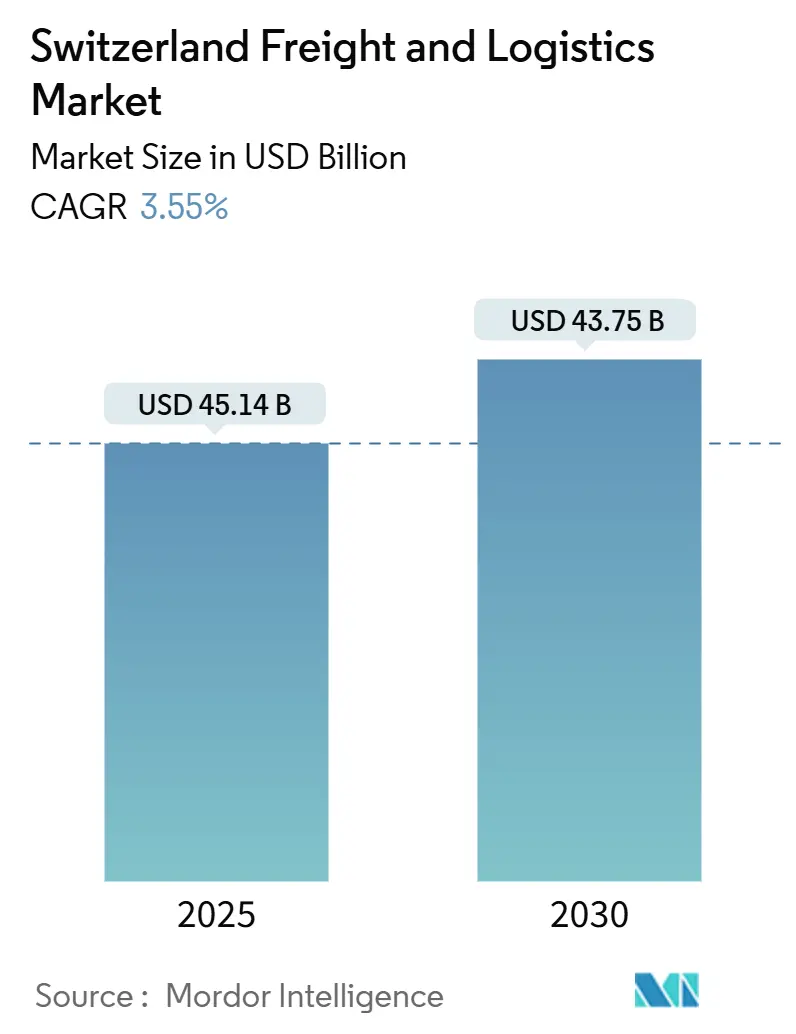

| Market Size (2025) | USD 45.14 Billion |

| Market Size (2030) | USD 43.75 Billion |

| Growth Rate (2025 - 2030) | 3.55% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Switzerland Freight And Logistics Market Analysis by Mordor Intelligence

The Switzerland Freight And Logistics Market size is estimated at USD 45.14 billion in 2025, and is expected to reach USD 43.75 billion by 2030, at a CAGR of 3.55% during the forecast period (2025-2030).

Robust infrastructure investment, an increasingly digital customs regime, and Switzerland’s pivotal transit position at the heart of Europe are the primary tailwinds for steady growth. Road freight continues to anchor day-to-day distribution, yet rail modernization and the emerging Cargo Sous Terrain network are steadily tilting long-haul volumes toward more sustainable modes. Rapid parcel consumption triggered by e-commerce keeps courier, express, and parcel (CEP) flows expanding faster than any other logistics function, while retail trade and temperature-controlled warehousing enlarge the addressable opportunity set for specialized service providers. Competitive intensity is rising as incumbents add automation, alternative-fuel fleets, and customs-integration tools to protect margins under tightening environmental rules.

Key Report Takeaways

- By logistics function, freight transport led with 59.93% of Switzerland freight and logistics market share in 2024, whereas courier, express, and parcel services are projected to post the fastest 4.04% CAGR through 2030.

- By end-user industry, wholesale and retail trade accounted for 35.58% of the Switzerland freight and logistics market size in 2024 and is on track to expand at a 3.78% CAGR to 2030.

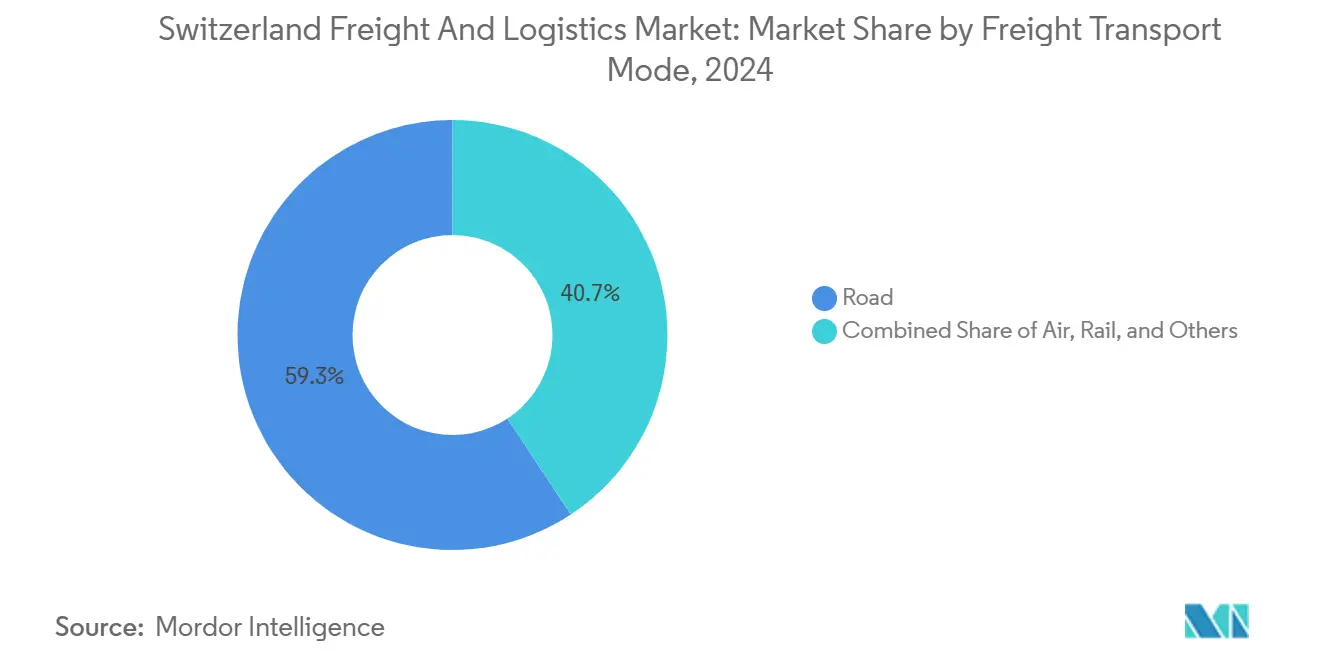

- By freight transport mode, road transport commanded 59.26% share of the Switzerland freight and logistics market size in 2024, while air freight is forecast to grow at a 3.96% CAGR over the same horizon.

- By CEP destination type, domestic services captured 66.52% share in 2024; the international segment is expected to accelerate at a 4.19% CAGR through 2030.

- By freight forwarding mode, sea and inland waterways held 65.86% revenue share in 2024, whereas air forwarding is anticipated to register a 3.75% CAGR to 2030.

- By warehousing temperature control, non-temperature-controlled space represented 91.76% share in 2024, yet temperature-controlled capacity is projected to rise at a 3.42% CAGR over the forecast period.

Switzerland Freight And Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Alpine rail modernization and 4-meter corridor completion | +0.8% | National – Basel–Gotthard–Milan axis | Medium term (2–4 years) |

| E-commerce boom driving CEP volumes | +0.9% | Zurich, Basel, Geneva urban hubs | Short term (≤ 2 years) |

| Strategic central European location fuels transit demand | +0.6% | Nationwide with EU spillovers | Long term (≥ 4 years) |

| Cargo Sous Terrain underground freight network development | +0.4% | Zurich–Basel–St. Gallen triangle | Long term (≥ 4 years) |

| Hydrogen fuel-cell truck adoption accelerates green logistics | +0.3% | Main national corridors | Medium term (2–4 years) |

| Customs digitization (DAIN) enables rapid cross-border clearance | +0.5% | All border crossings | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Alpine Rail Modernization and 4-Meter Corridor Completion

Switzerland is channeling CHF 990 million (USD 1.1 billion) into eliminating height restrictions along strategic Alpine tunnels and bridges so standard 4-meter semi-trailers can cross the Rhine-Alpine axis freely by 2028. Rail freight volumes rose 15% in 2024 after the initial tunnel upgrades came online, and operators expect to capture another 1.2 million t of yearly cargo once the full corridor connects Rotterdam and Genoa. Environmental upside is notable, with potential annual CO₂ savings near 180,000 t as loads migrate away from trucks. The work spans 19 tunnels and 61 bridges, signaling medium-term construction activity that also feeds domestic civil-engineering demand. Rail carriers have accelerated wagon procurement and IT upgrades to prepare for seamless intermodal operations once the route is fully certified. For the Switzerland freight and logistics market, the project underwrites modal diversification and positions rail as a cost-competitive option for north-south flows[1]“Alpine Rail Modernization Program,” Federal Office of Transport, bav.admin.ch.

E-commerce Boom Driving CEP Volumes

Domestic online shopping surged again in 2024, pushing Swiss Post’s parcel throughput to 192 million pieces, 12% higher than the previous year. CEP operators are installing automated sorters and adding electric vans to maintain same-day or narrow time-window delivery pledges embraced by 27% of shoppers. International parcels, often linked to cross-border marketplaces, lean on the DAIN customs engine, which cleared 41 million declarations in 2024. Real-time tracking now reaches 74% consumer adoption, so operators invest heavily in IoT scanners and data analytics to defend service-level guarantees. Municipal congestion rules in Zurich, Basel, and Geneva nudge fleets toward zero-emission formats, further lifting capex requirements. These dynamics collectively reinforce double-digit volume growth, making CEP the most vibrant slice of the Switzerland freight and logistics market during the forecast window[2]“DAIN Digital Customs Platform,” Federal Customs Administration, bazg.admin.ch.

Strategic Central European Location Fuels Transit Demand

Switzerland’s land-locked geography straddles the shortest land bridge between North Sea ports and the Italian seaboard, and that translates into 40.2 million t of cross-border freight in 2024. Germany remained the top trade partner, followed by Italy and France. The Gotthard Base Tunnel operated at 67% capacity, funneling 22.3 million t of rail cargo and underlining its supply-chain criticality. Transit activity injects roughly CHF 2.8 billion (USD 3.1 billion) of value into the economy and supports about 45,000 jobs. Yet reliance on a handful of passes leaves shippers exposed to disruption; every major closure redirects up to 1.5 million t to costlier Austrian or French detours. Still, the country’s neutrality, infrastructure quality, and customs efficiency continue to pull volume toward its corridors, sustaining long-term relevance for the Switzerland freight and logistics market.

Cargo Sous Terrain Underground Freight Network Development

Cargo Sous Terrain (CST) is a CHF 3.6 billion (USD 4 billion) plan to dig 500 km of automated tunnels linking Swiss cities by 2031. Phase one, a 70 km stretch between Zurich, Basel, and St. Gallen, broke ground with backing from major retailers and logistics groups willing to invest CHF 800 million (USD 890 million) in terminals and robotics. Autonomous pods traveling at 30 km/h will move up to 40 million t per year once the grid is mature, eliminating driver constraints and bypassing surface congestion. Continuous 24/7 operations promise tight reliability for food, pharma, and omnichannel retail flows that struggle under current urban land scarcity. Although commercial service is years away, CST’s long-term upside supports Switzerland’s ambition to remain a physics-defying freight laboratory and underpins structural optimism for the Switzerland freight and logistics market.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High operating costs and driver shortage | -0.7% | Nationwide; urban and cross-border routes most affected | Short term (≤ 2 years) |

| Stringent environmental regulations and LSVA toll | -0.4% | Nationwide with heavier impact on small fleets | Medium term (2–4 years) |

| Scarce urban warehouse land availability | -0.3% | Zurich, Basel, Geneva metro zones | Medium term (2–4 years) |

| Trans-Alpine route congestion and disruption risk | -0.2% | Gotthard and Simplon corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Operating Costs and Driver Shortage

The University of St. Gallen projects 80,000 unfilled driver posts by 2032 equal to 35% of required headcount while median monthly pay of CHF 4,700 (USD 5,230) and training bills near CHF 10,000 (USD 11,100) deter new entrants. Multilingual compliance and strict rest-period rules swell labor costs 25–30% on international hauls, pushing smaller carriers into margin stress. Fleet managers resort to premium wage packages and sign-on incentives, but these tactics elevate operating ratios and curb expansion appetites. Automation offers relief longer term, yet near-term tightness subtracts 0.7 percentage points from forecast CAGR for the Switzerland freight and logistics market[3]“Swiss Logistics Labor Market Study 2024,” University of St. Gallen, unisg.ch.

Stringent Environmental Regulations and LSVA Toll

The LSVA heavy-vehicle levy collected CHF 1.6 billion (USD 1.8 billion) in 2024, charging up to CHF 3.50 per ton-kilometer on older engines. Electric or hydrogen rigs can earn partial rebates, but upfront asset prices exceed CHF 150,000 (USD 167,000) for heavy trucks, and associated charging or fueling infrastructure adds roughly CHF 50,000 (USD 55,600) each year. Compliance targets mandate that 30% of urban delivery fleets run on zero-emission powertrains by 2030. Large networks like Swiss Post, already fielding 7,285 electric vehicles, absorb the hit, leaving smaller operators scrambling for capital or ceding share, which tempers growth across the Switzerland freight and logistics market[4]“Industrial Land Report 2024,” Swiss Real Estate Association, swissrealestate.ch.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User Industry: Wholesale and Retail Trade Leads Demand

Wholesale and retail trade delivered 35.58% of the Switzerland freight and logistics market size in 2024 thanks to Switzerland’s consumer-centric economy and its regional distribution role. Retailers exploit dense cross-docking networks to feed store shelves and e-commerce fulfillment nodes within overnight windows.

Retail’s forecast 3.78% CAGR eclipses manufacturing and construction because omnichannel players are opening urban micro-fulfillment hubs and raising small-parcel frequency. Pharmaceutical, engineering, and luxury-goods manufacturers nevertheless keep warehouse demand robust, especially for temperature-controlled or security-enhanced facilities. These balanced flows cushion the Switzerland freight and logistics market against volatility in any one industrial vertical.

By Logistics Function: Freight Transport Dominates Market Share

Freight transport accounted for 59.93% of Switzerland freight and logistics market share in 2024, a level reflecting the country’s role as Europe’s Alpine crossroads. The segment’s scale spans bulk rail consignments, long-haul road trucking, and specialized project cargo that capitalize on Switzerland’s dense highway and tunnel network.

Momentum stays positive as cross-border volumes keep climbing and as shippers upgrade to time-definite contracts. The courier, express, and parcel niche, though smaller, is registering a 4.04% CAGR to 2030, propelled by e-commerce and omnichannel retail strategies that privilege parcel density and rapid delivery. Freight forwarding and value-added services also gain traction as customs compliance evolves under DAIN. Combined, these shifts ensure the Switzerland freight and logistics market remains diversified yet firmly anchored by freight transport revenues.

By CEP Destination Type: Domestic Services Command Market Share

Domestic CEP services captured 66.52% share in 2024, mirroring dense urban populations and consumer preference for rapid home delivery. Swiss Post’s end-to-end network and broad locker footprint shore up market leadership.

International parcels, slated for 4.19% CAGR, benefit from simplified customs via DAIN and expanding EU marketplace linkages. Operators differentiate through late parcel cut-offs, real-time alerts, and premium same-day guarantees in major cities. These trends keep the Switzerland freight and logistics market closely tied to evolving consumer expectations.

By Warehousing Temperature Control: Non-Temperature Controlled Dominates

Conventional storage space formed 91.76% of capacity in 2024, serving consumer goods, industrial parts, and general merchandise. Yet temperature-controlled supply chains, led by biopharma, are advancing at a 3.42% CAGR, catalyzing investment in multi-chamber, GDP-compliant facilities.

Automation specialists like Swisslog report 35–40% throughput gains after deploying robotics in Swiss warehouses. Facility scarcity near Zurich and Basel inflates rents and nudges operators toward subterranean or multi-story designs, reinforcing structural tightness in the Switzerland freight and logistics market.

By Freight Transport Mode: Road Transport Maintains Modal Leadership

Road held 59.26% of Switzerland freight and logistics market share in 2024, supported by a finely meshed motorway grid and the door-to-door flexibility trucks provide. Air freight posted the fastest 3.96% CAGR outlook on continued growth in pharma and high-value micro-electronics.

Rail volumes, up 15% in 2024, will strengthen further once the 4-meter corridor completes, enabling standard trailers to shift from truck to wagon. Inland waterway connections to Rhine ports keep bulk commodities cost-efficient, while pipelines serve discrete energy flows. Mode diversification reduces environmental footprint and supports the Switzerland freight and logistics market’s growth narrative.

By Freight Forwarding Mode: Sea and Inland Waterways Lead Market Share

Sea and inland waterways forwarding represented 65.86% in 2024, anchored by efficient barge and rail transfers at Basel, which link Swiss importers to Rotterdam, Antwerp, and Hamburg. Maritime cost advantages remain decisive for heavy or containerized loads.

Air forwarding, on a 3.75% CAGR path, meets high-value speed requirements and gains from Zurich Airport’s 450,000 t cargo throughput in 2024. Digital booking portals, emissions-tracking dashboards, and multimodal bundling sharpen competitiveness and sustain growth for the Switzerland freight and logistics market.

Geography Analysis

Switzerland’s domestic corridors aggregate the highest share of shipment value, underpinned by a multimodal lattice that blankets Zurich, Basel, Bern, and Geneva. Cross-border volumes reached 40.2 million t in 2024, with Germany contributing 32%, Italy 18%, and France 15%. Within the north-south spine, the Gotthard Base Tunnel is pivotal, channeling 22.3 million t rail cargo at 67% utilization, a figure set to climb once the 4-meter upgrades conclude.

Infrastructure spending shifts east-west flows as well. The CHF 400 million (USD 445 million) DAIN digital customs rollout shaved clearance to under 10 minutes, anchoring Swiss gateways in global just-in-time networks. At the same time, warehouse land scarcity in urban cores forces operators outwards, lengthening final-mile runs yet encouraging adoption of micro-hubs and CST’s planned underground routes.

Regional hubs in St. Gallen, Schaffhausen, and the Ticino border zone complement main corridors by processing specialized clearances or hosting overflow transload yards. The LSVA toll regime influences routing choices, nudging Euro VI fleets toward high-efficiency corridors and pushing older engines onto peripheral roads. Seasonal congestion on Alpine passes remains a soft spot; each closure propels detour costs and jeopardizes schedule integrity, underscoring the need for modal flexibility and redundancy across the Switzerland freight and logistics market.

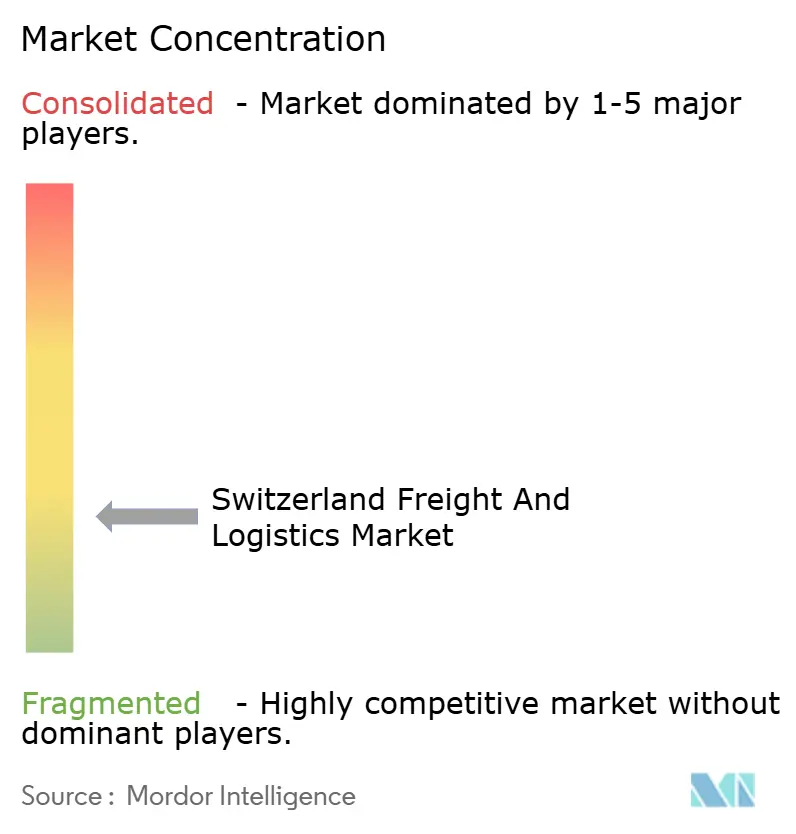

Competitive Landscape

The market is moderately fragmented yet increasingly technology-centric. Swiss Post’s March 2025 rebrand to Swiss Post Cargo pooled freight, warehousing, and distribution into a CHF 2.5 billion (USD 2.96 billion) revenue target by 2027, signalling aggressive vertical integration. Kuehne + Nagel leverages scale to pioneer sustainable aviation fuel deals with 14 airlines, aiming for 20% Scope 3 emissions cuts by 2030. DHL Group allocated CHF 200 million (USD 237.59 million) to automated sorters that lift processing capacity 40% across Zurich, Basel, and Geneva.

Local champions such as Galliker Transport AG pursue M&A, exemplified by the Camion acquisition adding 12 sites and 150 vehicles to its network. Digital natives partner with blockchain and IoT suppliers for end-to-end visibility, a capability fast becoming table stakes. Early movers in hydrogen trucking and CST tunnel slots could secure cost and sustainability edges. Still, high capex and regulatory complexity act as entry barriers, tilting advantage toward well-capitalized incumbents and shaping a competitive topology where the top five operators control an estimated 55–60% of revenue.

Switzerland Freight And Logistics Industry Leaders

Kuehne + Nagel International AG

DHL Group

DSV A/S

Swiss Post Ltd.

Galliker Transport AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Swiss Post rebranded its freight unit to “Swiss Post Cargo,” consolidating transport, warehousing, and distribution under one banner to reach CHF 2.5 billion revenue by 2027.

- February 2025: Kuehne + Nagel entered sustainability agreements with 14 airlines to fast-track sustainable aviation fuel usage targeting a 20% Scope 3 emissions cut by 2030.

- December 2024: DHL Group unveiled a CHF 200 million (USD 237.59 million) automation rollout, adding high-capacity sorters in Zurich, Basel, and Geneva.

- November 2024: Galliker Transport AG bought Camion Transport AG, enhancing its footprint in eastern Switzerland with 12 new depots.

Switzerland Freight And Logistics Market Report Scope

| Agriculture, Fishing, and Forestry |

| Construction |

| Manufacturing |

| Oil and Gas, Mining and Quarrying |

| Wholesale and Retail Trade |

| Others |

| Courier, Express, and Parcel (CEP) | By Destination Type | Domestic |

| International | ||

| Freight Forwarding | By Mode of Transport | Air |

| Sea and Inland Waterways | ||

| Others | ||

| Freight Transport | By Mode of Transport | Air |

| Pipelines | ||

| Rail | ||

| Road | ||

| Sea and Inland Waterways | ||

| Warehousing and Storage | By Temperature Control | Non-Temperature Controlled |

| Temperature Controlled | ||

| Other Services | ||

| By End User Industry | Agriculture, Fishing, and Forestry | ||

| Construction | |||

| Manufacturing | |||

| Oil and Gas, Mining and Quarrying | |||

| Wholesale and Retail Trade | |||

| Others | |||

| By Logistics Function | Courier, Express, and Parcel (CEP) | By Destination Type | Domestic |

| International | |||

| Freight Forwarding | By Mode of Transport | Air | |

| Sea and Inland Waterways | |||

| Others | |||

| Freight Transport | By Mode of Transport | Air | |

| Pipelines | |||

| Rail | |||

| Road | |||

| Sea and Inland Waterways | |||

| Warehousing and Storage | By Temperature Control | Non-Temperature Controlled | |

| Temperature Controlled | |||

| Other Services | |||

Key Questions Answered in the Report

How large is Switzerland’s freight and logistics sector in 2025?

The Switzerland freight and logistics market size is valued at USD 45.14 billion in 2025 and is projected to grow at a 3.55% CAGR to USD 53.75 billion by 2030.

Which logistics function is expanding the fastest?

Courier, express, and parcel services are forecast to advance at a 4.04% CAGR through 2030, driven by a sustained e-commerce boom.

What is the biggest restraint facing Swiss freight operators?

Acute driver shortages and high operating costs, compounded by the LSVA toll regime, subtract roughly 0.7 percentage points from expected market CAGR.

How will the 4-meter corridor affect rail freight?

Once completed in 2027-2028, the upgraded Alpine rail route will allow standard trailers to transit Switzerland, unlocking an extra 1.2 million t of annual rail cargo capacity.

Why is temperature-controlled warehousing gaining traction?

Strong growth in pharmaceuticals and food distribution is pushing temperature-controlled space at a 3.42% CAGR despite its current 8.24% share of total capacity.

What role does the Cargo Sous Terrain project play?

CST’s planned 500 km underground tunnel network, launching phase one by 2031, aims to move up to 40 million t of goods annually while easing urban congestion and labor shortages.

Page last updated on: