Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

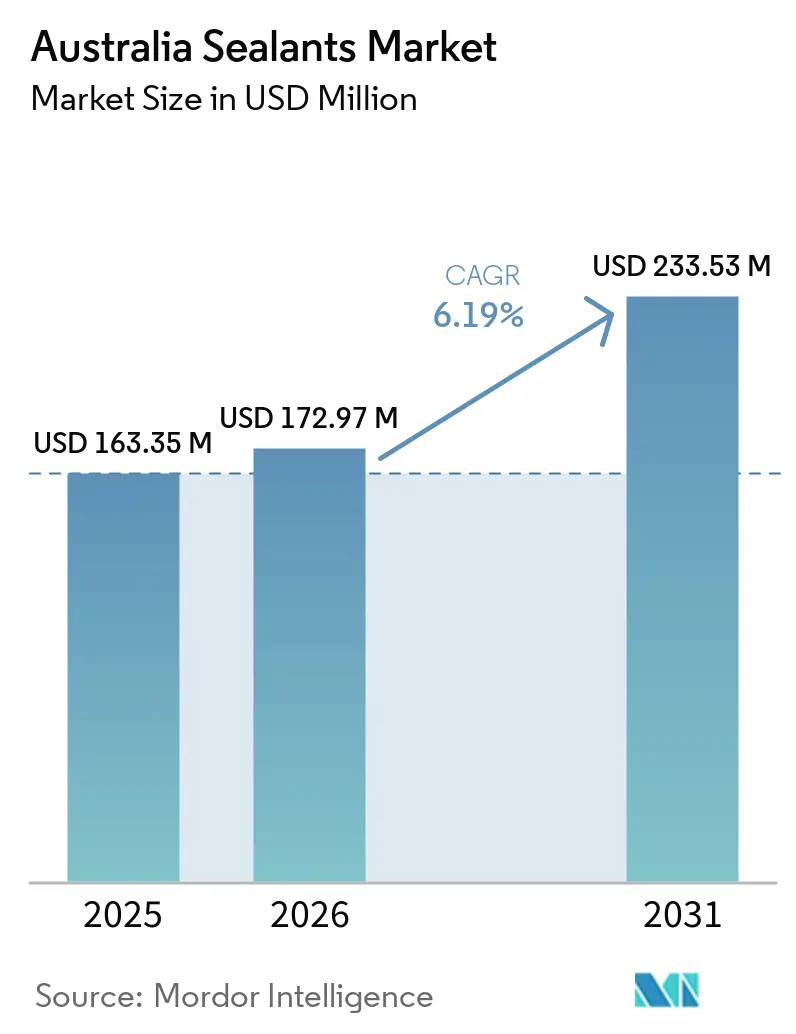

| Base Year Market Size (2025) | USD 163.35 Million |

| Market Size (2026) | USD 172.97 Million |

| Market Size (2031) | USD 233.53 Million |

| Growth Rate (2026 - 2031) | 6.19% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Sealants Market Analysis by Mordor Intelligence

The Australia Sealants Market size was valued at USD 163.35 million in 2025 and is estimated to grow from USD 172.97 million in 2026 to reach USD 233.53 million by 2031, at a CAGR of 6.19% during the forecast period (2026-2031). The market is shaped by advancements in public infrastructure projects, the enforcement of stricter 2025 NCC fire-safety and energy efficiency regulations, and the scaling of lithium-battery gigafactories. The market is also witnessing increased demand for environmentally friendly products, such as low-VOC and isocyanate-free sealants, driven by Green Star v2.0 standards. Furthermore, the development of offshore wind foundations in Gippsland highlights the growing focus on renewable energy infrastructure. Opportunities in the market are expanding, particularly in the area of EV battery-pack sealing, which is becoming increasingly critical as the electric vehicle industry grows. This segment requires innovative sealing solutions to ensure battery safety, enhance performance, and improve durability, presenting significant growth potential for market players. The competitive landscape remains moderately fragmented, with companies striving to leverage these opportunities and address the evolving needs of the market.

Key Report Takeaways

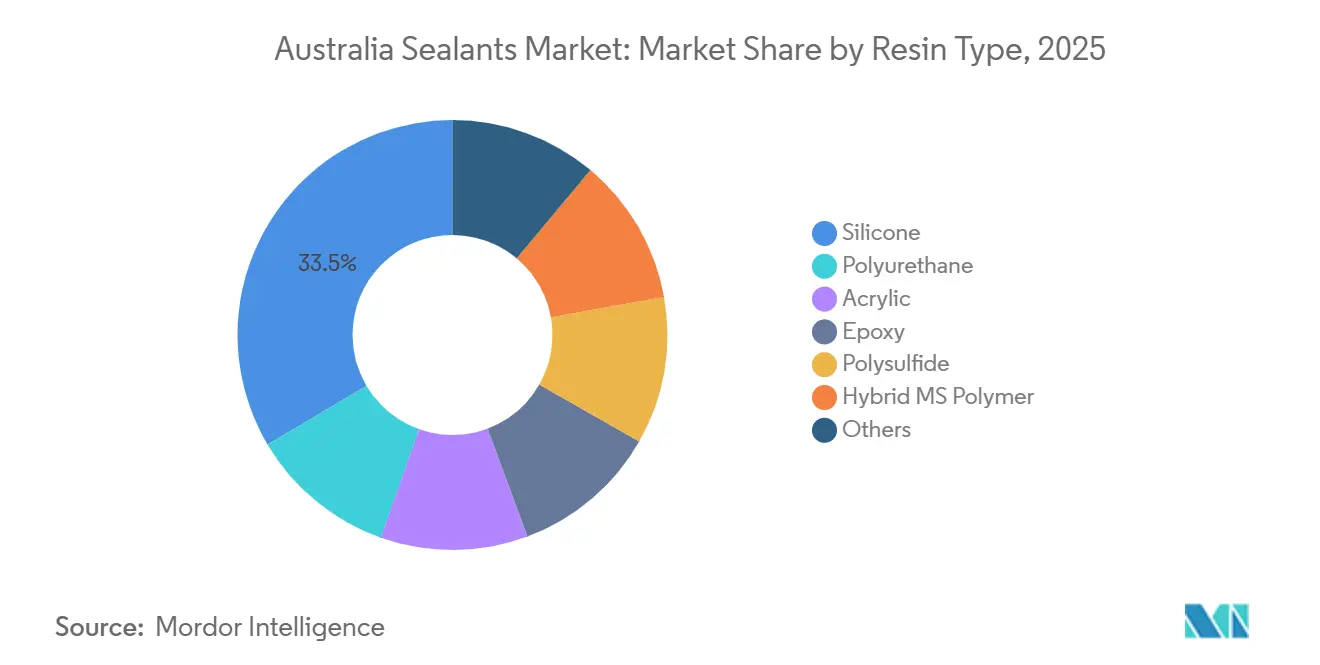

- By resin type, silicone held 33.50% of the Australia sealants market share in 2025, whereas hybrid MS polymer is on track to post the highest 7.02% CAGR through 2031 .

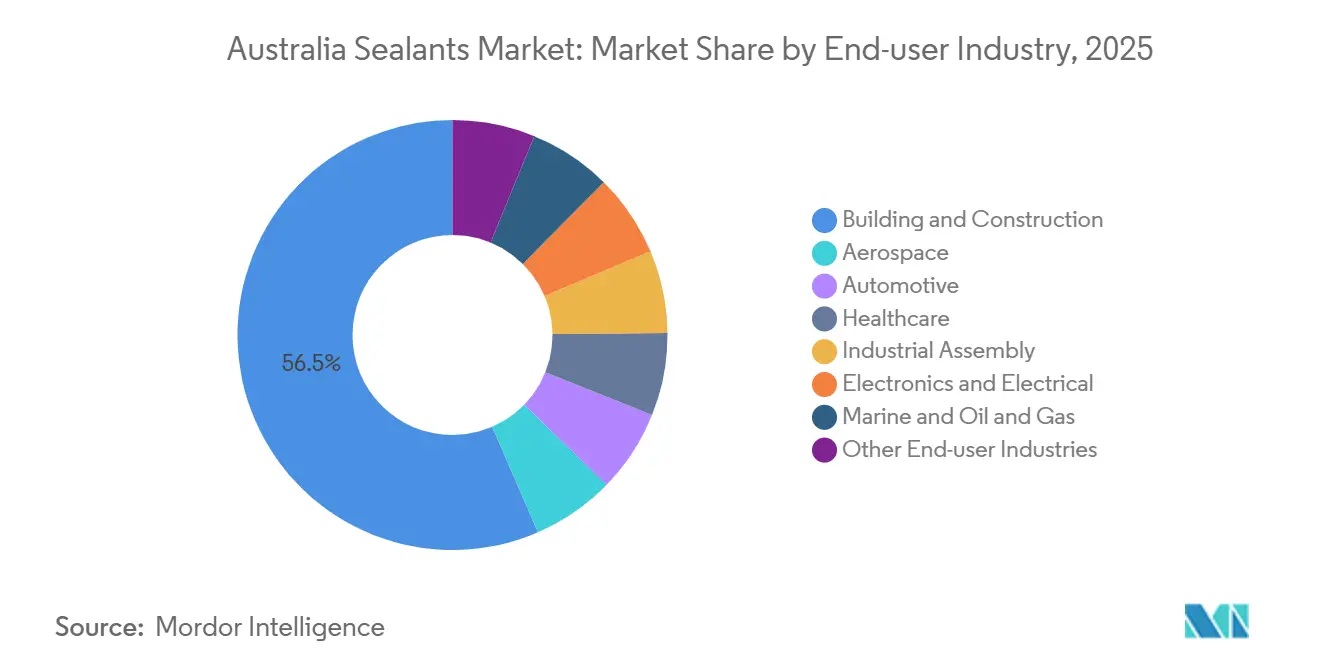

- By end-user industry, building and construction accounted for 56.50% of the Australia sealants market size in 2025, while the healthcare segment is projected to expand at a 7.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia Sealants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-billion public-infrastructure pipeline | +1.2% | National, NSW, VIC, QLD | Medium term (2-4 years) |

| Stricter 2025 NCC fire-safety and energy rules | +1.0% | National, climate zones 4-8 | Short term (≤ 2 years) |

| Scaling of lithium-battery gigafactories | +0.9% | NSW, VIC, SA | Medium term (2-4 years) |

| Low-VOC, isocyanate-free push from Green Star v2.0 | +0.7% | National urban projects | Long term (≥ 4 years) |

| Offshore-wind foundations in Gippsland | +0.5% | VIC, TAS | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Multi-Billion Public-Infrastructure Pipeline

Australia’s AUD 120 billion federal pipeline is redirecting sealant demand toward polyurethane and polysulfide joints able to withstand 30-year design lives in transport corridors, tunnels, and bridges[1]Infrastructure Australia, “Infrastructure Market Capacity 2025 Audit,” infrastructureaustralia.gov.au. Major undertakings such as Sydney Metro West and the Melbourne Airport Rail Link require fast-cure chemistries compatible with modular off-site fabrication timetables. Suppliers are co-locating technical teams at precast yards to troubleshoot adhesion before units ship, shortening commissioning cycles. Infrastructure Australia’s 2025 audit warned that 40% of scheduled projects face procurement delays from skilled-labor shortages, which is lifting demand for self-leveling sealants that reduce rework. The infrastructure wave therefore elevates the Australia sealants market as a strategic partner in project-delivery risk mitigation.

Stricter 2025 NCC Fire-Safety and Energy Rules Raise Performance Specs

NCC 2025 expands mandatory air-infiltration sealing and tightens smoke-spread limits, pushing specifiers toward intumescent silicone and low-modulus polyurethane products that pass AS 1530.4 tests[2]Australian Building Codes Board, “NCC 2025 Final Amendment,” abcb.gov.au. Part J5D7 now codifies the use of expanding foams, caulks or compressible strips at junctions once treated as discretionary, increasing installed volumes per building. Updated waterproofing provisions under public consultation add third-party certification requirements, which favor multinational formulators with accredited laboratories. Smaller regional brands lacking test infrastructure risk losing specification-driven share, accelerating consolidation inside the Australia sealants market.

Scaling of Lithium-Battery Gigafactories Needing Chemical-Resistant Joints

AGL’s Tomago and Recharge Industries’ Geelong cell plants have created a niche for sealants that survive electrolyte exposure and fire-suppression activation. Two-part polyurethane foams seal battery enclosures, while aluminum-oxide-filled thermal-interface materials achieve conductivities above 1.5 W/m·K in line with 3M technical briefs. Cure windows must align with automated dispensing cycles under 60 seconds, prompting co-development partnerships between formulators and cell makers. The Australia sealants market therefore, gains a high-margin, low-volume stream tied to the national battery-manufacturing roadmap.

Low-VOC / Isocyanate-Free Push from Green Star v2.0 Credits

The Green Building Council of Australia awards points for GECA-certified sealants capped at 95 g/L VOC and free of isocyanates and phthalates. Duram Resiflex Hybrid, launched in 2024, illustrates hybrid MS polymer appeal by offering over 400% elongation without residual monomer risk. Premium commercial developments increasingly mandate low-VOC specifications in tender documents, locking out non-certified suppliers from high-value contracts. This regulatory signal drives the Australia sealants market toward sustainable formulations while splitting supply chains between premium and cost-sensitive segments.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Silicone-polymer import-price volatility from NE-Asia | -0.8% | National | Short term (≤ 2 years) |

| Skilled-applicator shortage inflating costs and timelines | -0.6% | National, NSW, VIC metro | Medium term (2-4 years) |

| Advanced tapes and gaskets cannibalizing façade wet-sealant demand | -0.4% | National commercial construction | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Silicone-Polymer Import-Price Volatility from North-East Asia

Australia imports more than 70% of its silicone feedstock from China, Japan, and South Korea. Production curtailments in Shandong and Zhejiang during late 2025 tightened supply and lifted spot prices, compressing distributor margins because many construction contracts carry fixed pricing. With no local silicone-polymer capacity, distributors resort to inventory stockpiles that strain working capital. Smaller traders therefore exit the silicone category, curbing short-term growth for the Australia sealants market while potentially widening margins for remaining players once stability returns.

Skilled-Applicator Shortage Inflating Install Costs and Timelines

Master Builders Australia projects a construction labor deficit of up to 116,700 workers by 2027, with façade-sealing trades among the most undersupplied. Labor rates for qualified applicators in Sydney and Melbourne climbed 15% to 20% during 2025, raising installed costs and lengthening project schedules. Contractors increasingly specify self-leveling or fast-cure hybrids that demand less tooling skill, yet these products add 10% to 15% to material costs. The labor gap therefore erodes the cost advantage that once favored wet sealants, a structural drag on the Australia sealants market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Hybrid MS Polymer Gains Ground on Silicone

Hybrid MS polymer products are projected to expand at a 7.02% CAGR during 2026-2031, outpacing silicone and polyurethane as specifiers seek isocyanate-free, low-odor solutions that secure Green Star v2.0 points. The segment benefits from 60-minute skin times and paintability within four hours, attributes prized on fast-track projects. Silicone retained 33.50% of the Australia sealants market share in 2025 because its -50 °C to +250 °C service range is indispensable in façade, marine, and industrial settings. Sika Sikasil Marine and Sikaflex-295 UV illustrate continuous innovation to maintain competitive relevance. Polyurethane dominates high-movement joints in infrastructure and automotive because of superior adhesion to concrete, steel, and composites. Acrylic serves price-sensitive interior work, while polysulfide and epoxy maintain niche roles in fuel-resistant and chemical-resistant applications. Material science therefore re-orders priorities inside the Australia sealants market as sustainability, cure speed, and versatile adhesion define winning formulas.

Hybrid MS polymer’s rise aligns with NCC 2025 waterproofing consultations that direct specifiers to products validated under AS/NZS 4020 for potable-water contact. Duram Resiflex Hybrid delivers greater than 400% elongation without silicones or isocyanates, meeting these requirements while enabling same-day painting. Adheseal’s hybrid lineup cuts skin time versus solvent-based polyurethanes, reducing downtime on modular assemblies. The Australia sealants market size for hybrids will therefore swell rapidly in commercial towers, hospitals and cleanroom facilities, while silicone continues to anchor marine and high-temperature niches.

By End-User Industry: Healthcare Leads Growth, Construction Retains Scale

Building and construction represented 56.50% of 2025 demand because of the AUD 120 billion infrastructure program and NCC sealing mandates. Polyurethane and hybrid MS polymer jointing compounds dominate façades, precast panels and waterproofing membranes, with certified intumescent silicones joining fire-rated assemblies. Automotive and industrial assembly add momentum through EV battery-pack sealing at AGL’s Tomago and Recharge Industries’ Geelong plants, where thermal-interface materials and enclosure foams mitigate thermal-runaway risks.

Healthcare is forecast to register the fastest 7.31% CAGR to 2031, stimulated by Queensland’s Hospital Rescue Plan and the 600-bed New Coomera Hospital breaking ground in late-2026. Hospital projects specify antimicrobial silicones and GECA-certified hybrids compatible with indoor-air-quality objectives. Marine and oil-and-gas, tied to offshore-wind foundations in Gippsland, deploy IMO-approved polysulfide and polyurethane products for monopile interfaces. Electronics and electrical segments leverage high-fill TIMs from battery technologies to seal solar modules and power electronics. This diversity anchors long-term stability for the Australia sealants market size while concentrating above-average growth in healthcare.

Geography Analysis

New South Wales, Victoria, and Queensland collectively account for most of the national consumption, reflecting their dominance in construction, infrastructure, and manufacturing activity. Sydney Metro West and WestConnex in New South Wales drive polyurethane and hybrid MS polymer uptake in tunnel linings and bridge expansion joints. Victoria’s Melbourne Airport Rail Link and the Gippsland offshore-wind zone create marine-grade polyurethane and polysulfide demand for monopile foundations and offshore substations. Queensland’s Hospital Rescue Plan steers antimicrobial silicone and potable-water-compliant hybrids into new inpatient facilities such as the Coomera Hospital.

South Australia gains relevance through lithium-battery manufacturing clusters and renewable-energy assets, while Western Australia’s mining and LNG industries require chemical-resistant epoxies and high-temperature silicones for processing infrastructure. Tasmania’s offshore-wind and aquaculture activity sustains small yet high-specification demand for marine-grade sealants. The NCC 2025 energy-efficiency provisions apply more stringently to climate zones 4-8, encompassing Victoria, Tasmania and inland regions, thereby guiding product development toward cold-climate performance characteristics. This geographic divergence shapes formulation and distribution strategies across the Australia sealants market.

Competitive Landscape

The Australia sealants market is moderately fragmented, with global players using accredited labs and technical-service teams to win specification-intensive contracts. Sika’s 2026 digital partnership with Giatec embeds IoT sensors in concrete pours, letting contractors monitor curing and schedule joint sealing with predictive precision. Henkel’s March 2026 acquisition of ATP Adhesives enlarges its polyurethane and acrylic portfolio, signaling strategic consolidation.

White-space opportunities emerge in EV battery-pack sealing, where fire-resistant enclosure compounds command 30% to 50% price premiums. Temprotex’s F1ER intumescent coating, approved in January 2025 for SFI 54.1 fire protection, captures this niche. Evonik’s ORTEGOL DA 801 dispersant enables polyurethane TIMs with 90% filler loadings, easing thermal-conductivity bottlenecks. Competitive intensity remains heaviest in commodity polyurethane and acrylic lines for construction, while healthcare and battery segments offer margin headroom for technologically advanced entrants within the Australia sealants market.

Australia Sealants Industry Leaders

Henkel AG & Co. KGaA

Sika AG

Dow

RPM International Inc.

Fosroc, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Henkel completed its ATP Adhesives acquisition after Australian Competition and Consumer Commission clearance, expanding polyurethane and acrylic offerings for façade and industrial applications across Australia and New Zealand.

- March 2026: Sika formed a digital partnership with Giatec to integrate concrete-monitoring sensors into construction-materials contracts, enabling predictive maintenance for sealant installations in infrastructure projects.

Australia Sealants Market Report Scope

Sealants are elastomeric materials used to fill gaps, joints, or cracks, preventing water, air, dust, and fluid passage. Widely applied in construction and industrial sectors, they ensure waterproofing and structural flexibility in buildings, windows, automotive components, and appliances.

The Australia sealants market is segmented by resin type and end-user industry. By resin type, the market is segmented into silicone, polyurethane, acrylic, epoxy, polysulfide, hybrid MS polymer, and others. By end-user industry, the market is segmented into aerospace, automotive, building and construction, healthcare, industrial assembly, electronics and electrical, marine and oil and gas, and other end-user industries. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Resin Type

| Silicone |

| Polyurethane |

| Acrylic |

| Epoxy |

| Polysulfide |

| Hybrid MS Polymer |

| Others |

By End-user Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Healthcare |

| Industrial Assembly |

| Electronics and Electrical |

| Marine and Oil and Gas |

| Other End-user Industries |

| By Resin Type | Silicone |

| Polyurethane | |

| Acrylic | |

| Epoxy | |

| Polysulfide | |

| Hybrid MS Polymer | |

| Others | |

| By End-user Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Healthcare | |

| Industrial Assembly | |

| Electronics and Electrical | |

| Marine and Oil and Gas | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Automotive, Aerospace, Healthcare, and Others are the end-user industries considered under the sealants market.

- Product - All sealant products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Silicone, and Others are considered

- Technology - For the purpose of this study, One component and Two component sealant technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms