Food Container Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

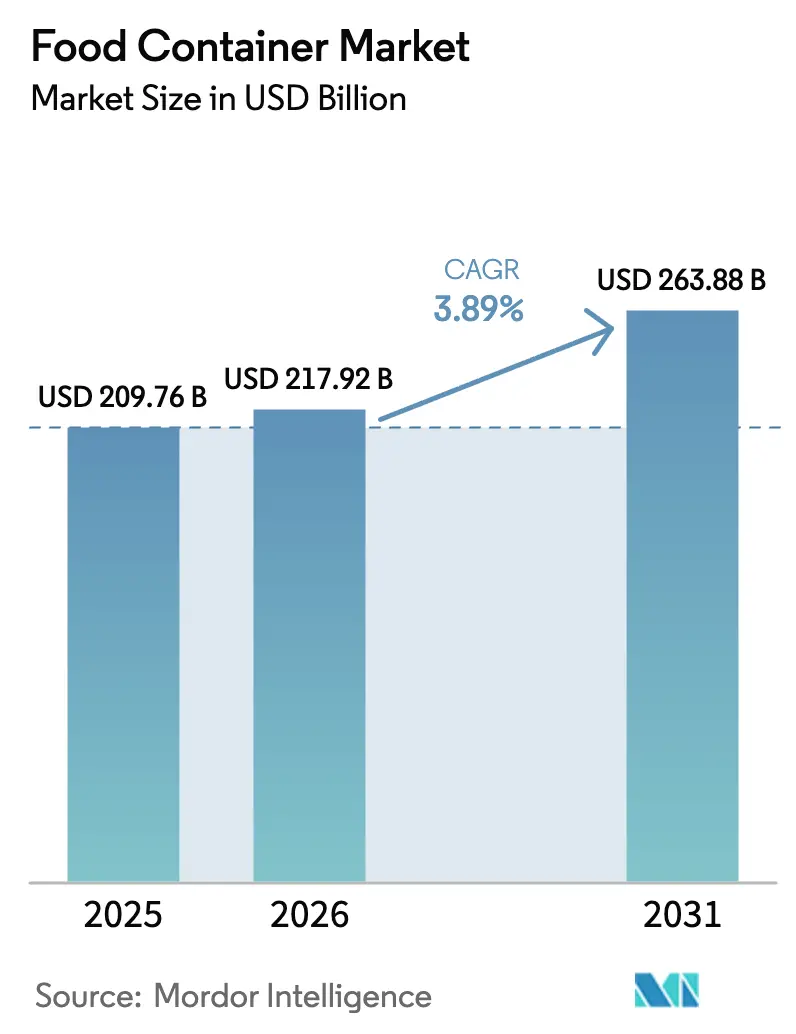

| Market Size (2026) | USD 217.92 Billion |

| Market Size (2031) | USD 263.88 Billion |

| Growth Rate (2026 - 2031) | 3.89% CAGR |

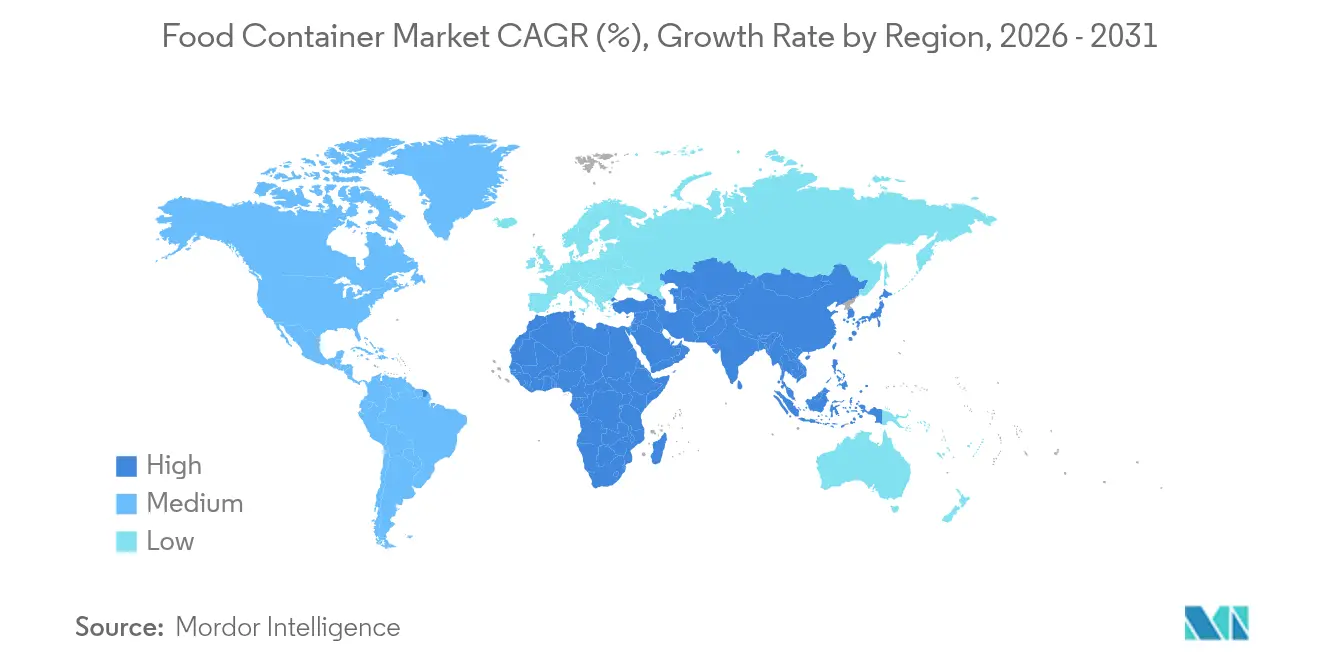

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Food Container Market Analysis by Mordor Intelligence

The food container market size in 2026 is estimated at USD 217.92 billion, growing from 2025 value of USD 209.76 billion with 2031 projections showing USD 263.88 billion, growing at 3.89% CAGR over 2026-2031. Growth is underpinned by urban lifestyle shifts that raise demand for packaged and convenience foods, the proliferation of e-commerce grocery and meal-kit services that require more protective yet lightweight formats, and steady investments in materials engineering that make recyclability and traceability technically and economically feasible. Larger converters defend margins through vertical integration, long-term resin and metal contracts, and global footprints that balance regional demand swings, while mid-sized firms differentiate through niche barrier technologies, smart-label integration, and paper-based alternatives. Asia-Pacific remains the fastest-expanding region, but regulatory frameworks in the European Union and North America now set the de-facto design rules for recycled content, mono-material structures, and chemical-migration thresholds. Meanwhile, the circular-economy push is accelerating substitution away from legacy single-use plastics and toward paperboard, metal, and hybrid formats, prompting incumbents to invest in bio-polymer capacity and post-consumer-resin (PCR) sourcing networks.

Key Report Takeaways

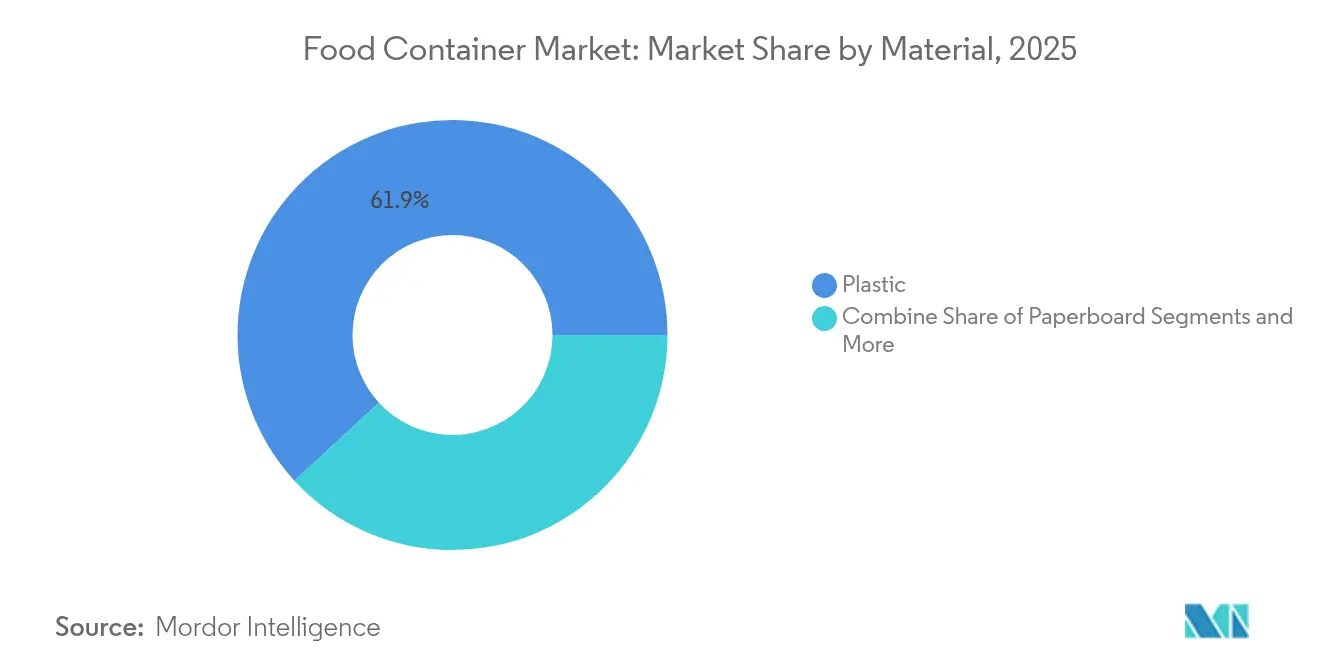

- By material, plastic retained 61.85% of food container market share in 2025, while paperboard is on track to grow at a 7.05% CAGR through 2031.

- By product type, flexible packaging led with a 53.75% revenue share in 2025, and is projected to expand at a 5.10% CAGR to 2031.

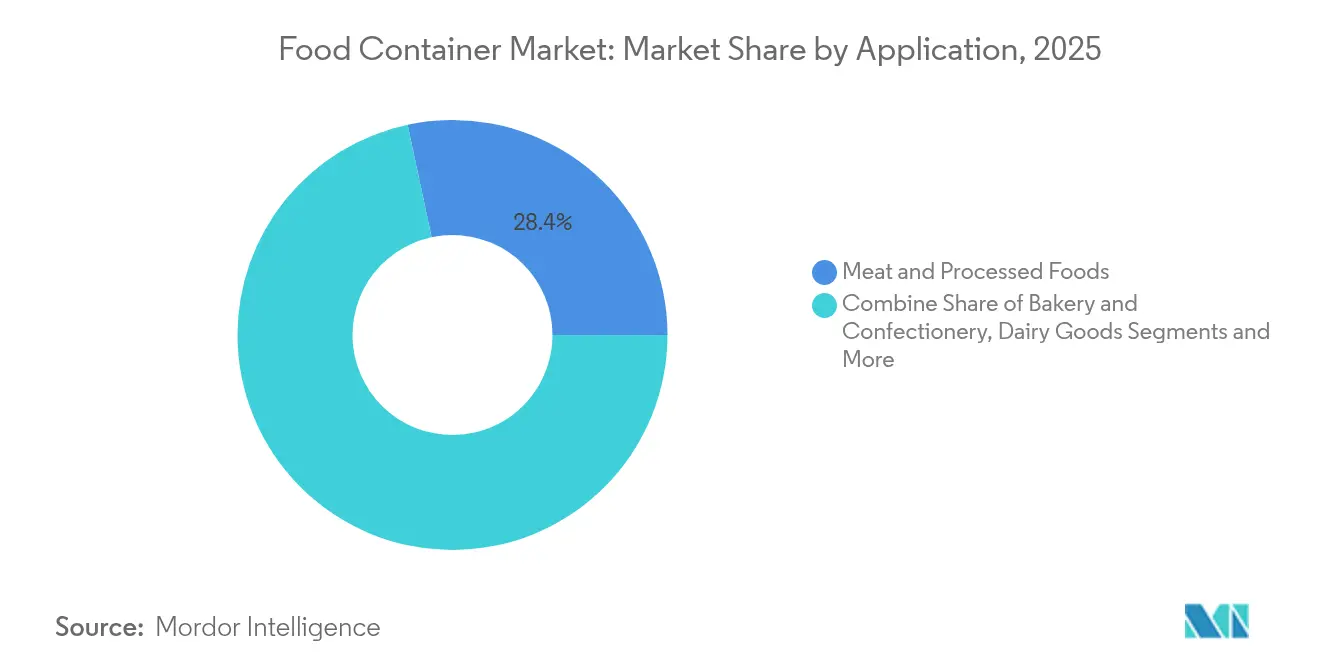

- By application, meat and processed foods accounted for a 28.35% share of the food container market size in 2025; ready meals are advancing at an 7.72% CAGR through 2031.

- By geography, Asia-Pacific commanded 38.62% of the food container market size in 2025 and is forecast to post a 7.61% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Food Container Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timelin |

|---|---|---|---|

| Rising packaged and convenience-food demand in emerging economies | +1.2% | Asia-Pacific core, spill-over to Latin America | Medium term (2-4 years) |

| Regulatory push and consumer demand for recyclable materials | +0.8% | Global, with EU and North America leading | Long term (≥ 4 years) |

| Expansion of e-commerce grocery and meal-kit channels | +0.7% | Global, concentrated in urban markets | Short term (≤ 2 years) |

| Extended-producer-responsibility fees spurring lightweight design | +0.5% | EU core, expanding to North America and APAC | Medium term (2-4 years) |

| Embedded freshness-sensing smart labels enabling premium pricing | +0.3% | North America and EU premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Packaged and Convenience-Food Demand in Emerging Economies

Rapid urbanization fosters a structural pivot toward processed and ready-to-eat products, lifting baseline volumes for the food container market in China, India, Indonesia, and Vietnam. China’s 2024 traceability rules oblige more sophisticated labeling, which in turn drives demand for multilayer films and interactive QR-coded packs that connect shoppers with provenance data. India’s middle-income households gravitate toward portion-controlled packs with extended shelf life, yet culturally anchored cooking practices still favor resealable formats over single-serve sachets. Suppliers benefit from multiyear volume visibility, but must localize printing, logistics, and post-consumer collection systems to align with city-level waste-segregation schemes. Growth momentum extends into Latin America where similar demographic trends unfold, albeit tempered by higher inflation and currency swings.

Regulatory Push and Consumer Demand for Recyclable Materials

The European Union’s Packaging and Packaging Waste Regulation, effective 2024, mandates minimum recycled-content thresholds and harmonized EPR fee structures, effectively rewriting the economics of material choice.[1]European Commission, “Packaging and Packaging Waste,” environment.ec.europa.euBrands that exceed the baseline gain market access advantages and reputational capital, while laggards shoulder steeper compliance costs. Parallel initiatives in the United States and Canada tighten limits on PFAS and other chemical migrants, compelling converters to accelerate material migration toward mono-PET and coated-paper solutions that balance barrier performance with recyclability. Surveys indicate that a majority of Generation Z shoppers now rank packaging sustainability among their top three purchase criteria, cementing the shift from niche to mainstream driver of the food container market.

Expansion of E-Commerce Grocery and Meal-Kit Channels

Direct-to-consumer grocery grew double digits in 2024 and is reshaping pack performance specifications: transit durability, leak-proof seals, and on-arrival shelf impact now carry equal weight with production cost. The U.S. meal-kit sector doubled packaging spend between 2022 and 2024, favoring lightweight pouches with integrated ice-pack compartments and QR-linked cooking instructions. Such designs reduce parcel weight, minimize spoilage, and enable the data capture that subscription algorithms depend on. Flexible formats see disproportionate share gains, but rigid trays with advanced insulation foams also benefit, especially for premium seafood and ready-meal lines. The channel likewise speeds adoption of smart time-temperature indicators, elevating barrier-film suppliers that can laminate electronic sensors at scale.

Extended-Producer-Responsibility Fees Spurring Lightweight Design

Germany’s revised EPR schedule pegs license fees to unit weight and material recyclability, making every gram saved a direct profit lever. Global brand owners replicate this accounting logic across portfolios, prompting engineering teams to thin-gauge lids, eliminate EVOH tie layers, and adopt mono-material pouches where seal-strength permits. Lightweighting compounds upstream cost volatility caused by fluctuating resin and aluminum premiums but ultimately dampens fee expense. Suppliers with in-house design services capture greater wallet share by offering finite-element simulation and lifecycle-assessment tools that convert EPR inputs into measurable ROI for customers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile raw-material prices for plastics and metals | -0.9% | Global, with emerging markets most affected | Short term (≤ 2 years) |

| Single-use-plastic bans across major economies | -0.6% | EU, North America, select APAC markets | Medium term (2-4 years) |

| PFAS / chemical-migration liabilities raising compliance costs | -0.4% | North America & EU core, expanding globally | Long term (≥ 4 years) |

| Shortage of food-grade PCR resin due to collection gaps | -0.3% | Global, with developed markets most constrained | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Raw-Material Prices for Plastics and Metals

Aluminum spot prices on the London Metal Exchange gyrated within a 26% band in 2024, squeezing can-makers whose raw input costs can exceed 60% of finished-pack value. [2]London Metal Exchange, “LME Aluminium,” lme.com Similarly, polyethylene and polypropylene resin contracts track Brent crude with a 3-month lag, confounding forecast accuracy for converters operating on quarterly customer pricing cycles. The food container market therefore rewards vertically integrated firms or those with hedging desks capable of locking in forward premiums. Smaller regional players, by contrast, battle margin erosion and occasionally cede share to private-label importers when currency depreciation amplifies resin spikes.

Single-Use-Plastic Bans Across Major Economies

The FDA expanded scrutiny of PFAS in 2025, disallowing certain coatings previously used in microwave popcorn bags and burger clamshells.[3]U.S. Food and Drug Administration, “Food Contact Substances,” fda.govIn parallel, EU directives forbid single-use plastic cutlery, plates, and expanded-polystyrene food containers, compelling brand owners to overhaul SKUs at speed. Dual supply chains often emerge because regulatory timelines differ across jurisdictions, undermining economies of scale and complicating raw-material planning. Companies that pre-emptively invested in paper-based or reusable systems gain shelf presence, but retrofit costs weigh heavily on late movers, dampening near-term cash flow.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Plastic Dominance Faces Sustainable Challengers

Plastic retained the largest slice of the food container market in 2025, holding 61.85% of volume thanks to low cost, formability, and well-established global supply chains. Within that, the food container market size for rigid PET bottles and HDPE tubs remained stable, while flexible multi-layer films captured incremental gains in snack and bakery packs. Yet, regulatory pressure and consumer eco-preferences are shifting momentum: paperboard, boosted by barrier-coating advances, is tracking a 7.05% CAGR to 2031, making it the fastest riser among major substrates. Notably, Braskem’s commercial launch of bio-circular polypropylene derived from used cooking oil signals that bio-plastics can now meet performance parity while cutting life-cycle emissions, a step change that larger brands are piloting at commercial scale.

Second-order implications include a scramble for food-grade PCR resin, whose collection shortfalls inflate premiums and hinder high-volume adoption in emerging markets. Metal packaging, leveraging infinite recyclability, enjoys a modest resurgence in premium ready-to-drink coffee and infant-formula tins, whereas glass trades share for value retention in gourmet sauces and functional beverages. Hybrid structures—paper cups with aqueous coatings or aluminum can ends on composite containers—appear increasingly in the food container market as converters balance performance, recyclability, and unit cost. Overall, the materials hierarchy is fluid, but clear winners combine circular attributes with drop-in processing compatibility and global regulatory acceptance.

By Product Type: Flexible Solutions Lead Innovation

Flexible formats captured 53.75% of 2025 revenue due to their low weight-to-product ratio, pouch-friendly e-commerce form factors, and gravure-printing aesthetics. Within this subset, mono-material PE and PP pouches outpaced traditional PET/PE laminates as brands chase recycle-ready certifications that unlock lower EPR fees. The segment’s 5.10% CAGR through 2031 is tied to nimble pack formats that marry convenience with source-reduction goals. Stand-up pouches for nuts, pet food, and liquid soups now incorporate spouts and laser scoring, expanding use cases and reinforcing flexible leadership in the food container market.

Rigid offerings, though slower, evolve via lightweighting and premiumization. Glass jars maintain brand heritage for sauces and spreads, while aluminum trays gain penetration in oven-ready meal kits that bank on quick-heat properties. Molded pulp bowls, championed by quick-service restaurants navigating single-use plastic bans, claim share in salads and grain bowls, albeit challenged by grease-resistance chemistry rules. To sustain relevance, rigid-pack manufacturers are embedding QR-coded lids and peel-off freshness films, offerings that align with the smart-pack trend sweeping the food container market.

By Application: Ready Meals Drive Growth Acceleration

Meat and processed foods remained the demand anchor in 2025, representing 28.35% of volume, rooted in stringent cold-chain and food-safety protocols that reward high-barrier laminates and metal cans. Yet the growth spotlight falls on ready meals and takeaway formats, which are advancing at an 7.72% CAGR through 2031 on the back of rising dual-income households, app-based food delivery, and consumer appetite for global cuisines. Microwaveable trays with vent-control films, self-heating bowls, and multi-compartment pouches tailored for ketogenic or plant-based diets illustrate how application needs dictate pack innovation.

In dairy, multi-layer PET cups with light-filtering additives extend shelf life for probiotic yogurt, while aseptic cartons press deeper into ambient-temperature distribution to trim energy use. Produce packaging experiments with breathable membranes and on-pack ethylene absorbers to limit spoilage, an approach supportive of zero-food-waste commitments from retailers. Bakery, confectionery, and grain-mill items focus on moisture regulation and tamper visibility, underscoring that each application cycle spawns its own micro-trends—and collectively they spread innovation across the broader food container market.

Geography Analysis

Asia-Pacific generated 38.62% of global revenues in 2025 and is forecast to expand at a 7.61% CAGR, extending its lead as urban migration, rising female workforce participation, and mobile-commerce uptake fuel new convenience-food consumption. China’s 2024 traceability code mandate positioned smart, multi-layer pouches as the default for chilled meat and poultry, pushing local converters to scale digital printing and variable-data serialization. India’s household-size fragmentation favors small pack units, and government-backed food-safety campaigns spur adoption of tamper-evident lids, benefiting regional plastic and paperboard mills positioned near megacities.

North America maintains robust share with a mature cold chain and consumers willing to pay sustainability premiums. The FDA’s heightened PFAS scrutiny reshapes coating portfolios, granting an edge to converters who already invested in fluorine-free barriers. E-grocery volumes, cemented by pandemic-era behavior, remain sticky; as a result, pouch and insulated-liner suppliers scale new capacity in the Midwest and Mexico to meet two-day delivery SLAs. Canada mirrors U.S. trends but layers carbon-pricing schemes that favor lightweight formats, while Mexico’s demand lifts corrugated and flexible suppliers aligning with burgeoning discount chains.

Europe is the crucible for circular-economy regulation. The 2024 Packaging and Packaging Waste Regulation codifies recycled-content targets and modulated EPR fees, accelerating design-for-recycling and PCR sourcing. Germany refined fee granularity, charging higher tariffs on multi-material packs, which spurred rapid mono-PET film substitution. The United Kingdom shadows EU rules but is piloting digital DRS (deposit-return scheme) to track pack units, offering data insights likely to diffuse globally. Southern European markets emphasize authenticity and premium cues, driving glass and decorated metal demand in olive oil, wine, and specialty preserves. Collectively, these regulatory and cultural factors influence pack design choices worldwide, as multinationals standardize to the toughest common denominator.

Competitive Landscape

The food container market is fragmented. Amcor’s pending merger with Berry Global would elevate the combined entity’s extrusion, molding, and film lamination scale, promising synergies in resin procurement and cold-chain logistics. Crown Holdings capitalizes on metal-can demand spikes by adding two high-speed lines in the U.S. Midwest, leveraging long-term aluminum supply contracts to buffer price swings. O-I Glass surpassed earnings expectations in Q1 2025, attributing gains to its “Fit to Win” cost-reduction roadmap that trimmed furnace downtime and improved cullet yields.

Strategic themes center on sustainability investments and smart-pack capabilities. Mondi’s EUR 200 million recycled-containerboard mill in Italy will add 420 kiloton capacity by 2027, reinforcing paperboard supply for European converters. Accredo Packaging’s 100% bio-based resin pouch, unveiled at Pack Expo 2024, shows how small innovators capture mindshare by aligning with carbon-neutral branding narratives. Meanwhile, Reynolds Consumer Products disclosed record 2024 profits despite resin swings, crediting price mix improvements and operational hedge strategies. Patent filings in bio-polymer blends and printed-electronics labels rose 18% year-on-year, signaling an arms race for intellectual property that can secure margin in an otherwise volume-centric arena.

Consolidation remains active but selective: acquisitions favor firms with differentiated barrier chemistries, PCR sourcing contracts, or data-enabled pack formats. Private-equity interest persists, yet valuations now hinge on demonstrable ESG metrics that align with lender sustainability-linked loan covenants. As regulatory latency narrows between the EU, U.S., and major APAC markets, supply-chain complexity rises, advantaging companies with global compliance teams and multi-regional production nodes capable of just-in-time SKU shifts. Over the next five years, the competitive frontier will likely center on who can operationalize closed-loop material flows and monetize pack-embedded data streams at scale.

Food Container Industry Leaders

Sonoco Products Company

Amcor PLC

Huhtamaki Oyj

Crown Holdings Inc.

Sealed Air Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: O-I Glass reported Q1 2025 adjusted earnings of USD 0.40 per share, generating USD 61 million in operational benefits under its “Fit to Win” program.

- February 2025: Mondi Group began construction of a EUR 200 million recycled-containerboard mill in Duino, Italy, targeting rising European demand for circular packaging.

- October 2024: Tupperware Brands reached a pact with secured lenders to form The New Tupperware Company, emphasizing a digital-first model in core North American markets.

- October 2024: Accredo Packaging launched the first 100% bio-based resin pouch at Pack Expo 2024, combining sugarcane feedstock with conventional performance.

- June 2024: Saica Group and Mondelēz International introduced recyclable paper-based multipack solutions for confectionery lines.

Global Food Container Market Report Scope

Food containers in diverse sizes, shapes, and materials cater to consumer needs, from storing dry goods and liquids to housing prepared meals. Premium containers are pivotal in prolonging food shelf life, ensuring ingredients remain fresh. Today's advanced containers often feature airtight seals, leak-proof designs, and specialized compartments designed to prevent spoilage by keeping foods distinct and separate. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The food container market is segmented by material (Plastic, Glass, Metal and Other Materials), by product type (Flexible Packaging (Pouches, Bags, Wraps and Other Product Types), Rigid Packaging (Bottles and Jars, Trays, Boxes, Cans and Other Product Types) and by geography (North America, Europe, Asia Pacific, South America and Middle East and Africa), The market sizing and forecasts are provided in terms of value (USD) for all the above segments.

| Plastic | Polyethylene (PE) | Low-Density Polyethylene (LDPE) |

| High-Density Polyethylene (HDPE) | ||

| Linear Low-Density Polyethylene (LLDPE) | ||

| Polypropylene (PP)? | ||

| Polyethylene Terephthalate (PET) | ||

| Other Plastics | ||

| Glass | ||

| Metal | ||

| Paperboard | ||

| Other Materials |

| Flexible Packaging | Pouches |

| Bags | |

| Wraps | |

| Other Flexible Packaging Types | |

| Rigid Packaging | Bottles and Jars |

| Trays | |

| Boxes | |

| Cans | |

| Cups and Tubs | |

| Clamshells | |

| Other Rigid Packaging Types |

| Bakery and Confectionery |

| Dairy Goods |

| Fruits and Vegetables |

| Grain-mill Products |

| Meat and Processed Foods |

| Ready Meals and Take-away |

| Sauces, Dressings and Spreads |

| Other Application |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Material | Plastic | Polyethylene (PE) | Low-Density Polyethylene (LDPE) |

| High-Density Polyethylene (HDPE) | |||

| Linear Low-Density Polyethylene (LLDPE) | |||

| Polypropylene (PP)? | |||

| Polyethylene Terephthalate (PET) | |||

| Other Plastics | |||

| Glass | |||

| Metal | |||

| Paperboard | |||

| Other Materials | |||

| By Product Type | Flexible Packaging | Pouches | |

| Bags | |||

| Wraps | |||

| Other Flexible Packaging Types | |||

| Rigid Packaging | Bottles and Jars | ||

| Trays | |||

| Boxes | |||

| Cans | |||

| Cups and Tubs | |||

| Clamshells | |||

| Other Rigid Packaging Types | |||

| By Application | Bakery and Confectionery | ||

| Dairy Goods | |||

| Fruits and Vegetables | |||

| Grain-mill Products | |||

| Meat and Processed Foods | |||

| Ready Meals and Take-away | |||

| Sauces, Dressings and Spreads | |||

| Other Application | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the food container market?

The food container market size reached USD 217.92 billion in 2026 and is projected to grow to USD 263.88 billion by 2031.

Which region dominates the food container market?

Asia-Pacific leads with a 38.62% share in 2025 and is forecast to expand at a 7.61% CAGR through 2031.

What material segment is growing the fastest?

Paperboard is the fastest-growing material, posting a 7.05% CAGR as regulatory and consumer sustainability preferences shift demand.

How are e-commerce and meal-kit services affecting packaging design?

They require lightweight, protective, and often smart-enabled packaging that withstands longer transit chains while providing real-time quality feedback.

What is driving the move toward recyclable and bio-based packaging?

EU and North American regulations mandate recycled-content thresholds, and consumers increasingly reward brands that invest in circular, low-carbon materials.

Are smart labels becoming mainstream in food packaging?

Adoption is rising, particularly in North America and Europe, as embedded sensors offer freshness monitoring and can justify premium pricing in high-value categories.

Page last updated on: