Food Packaging Films Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 45.99 Billion |

| Market Size (2031) | USD 57.25 Billion |

| Growth Rate (2026 - 2031) | 4.49% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Food Packaging Films Market Analysis by Mordor Intelligence

The Food Packaging Films Market size is expected to grow from USD 44.01 billion in 2025 to USD 45.99 billion in 2026 and is forecast to reach USD 57.25 billion by 2031 at 4.49% CAGR over 2026-2031. Sustained growth reflects rising urban populations, regulatory pressure for recyclable formats and advances in high-barrier film technologies that prolong shelf life and cut food waste. Polyethylene still dominates material selection, yet bioplastics and mono-material structures gain momentum as regional legislation tightens recycled-content targets and restricts multilayer constructions. Asia-Pacific leads demand thanks to large food-processing bases and cost-competitive capacity, while North America posts the fastest expansion on the back of e-commerce meal-kit adoption and ambitious circular-economy standards.

Key Report Takeaways

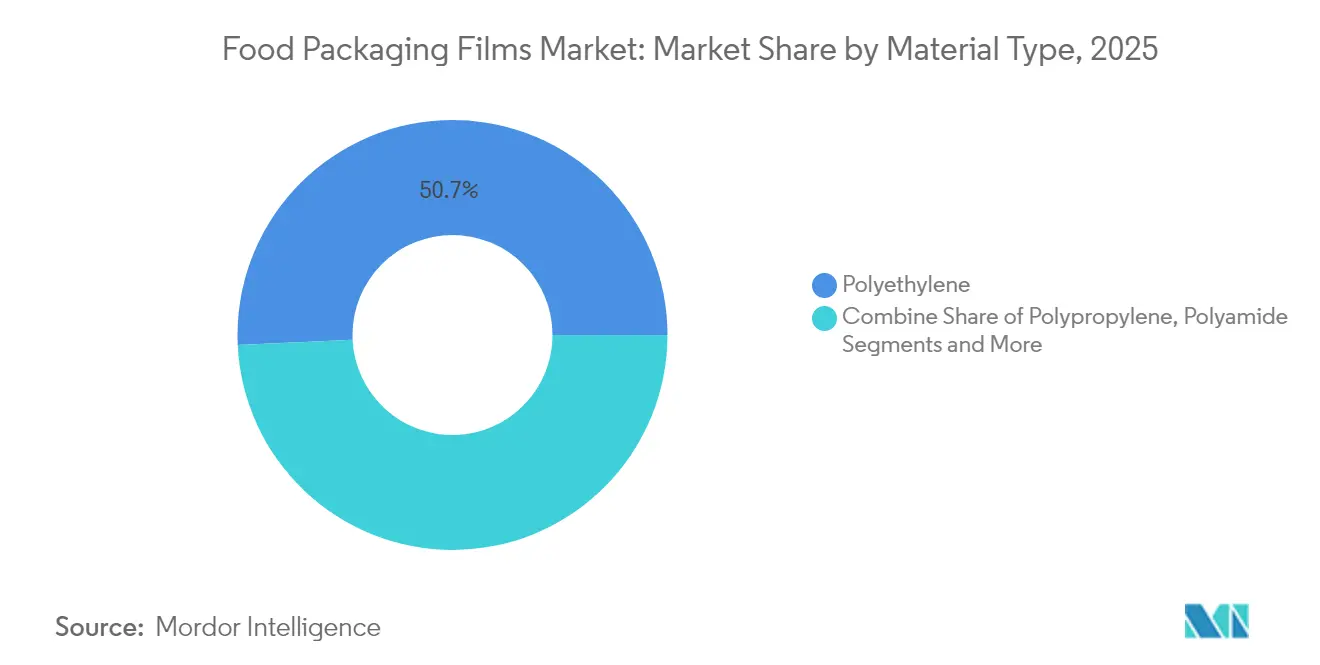

- By material type, polyethylene held 50.74% of the food packaging films market share in 2025, whereas bioplastics are projected to grow at a 6.33% CAGR to 2031.

- By packaging type, wraps and roll-stocks led with 28.35% revenue share in 2025; bags and pouches are forecast to expand at a 7.45% CAGR through 2031.

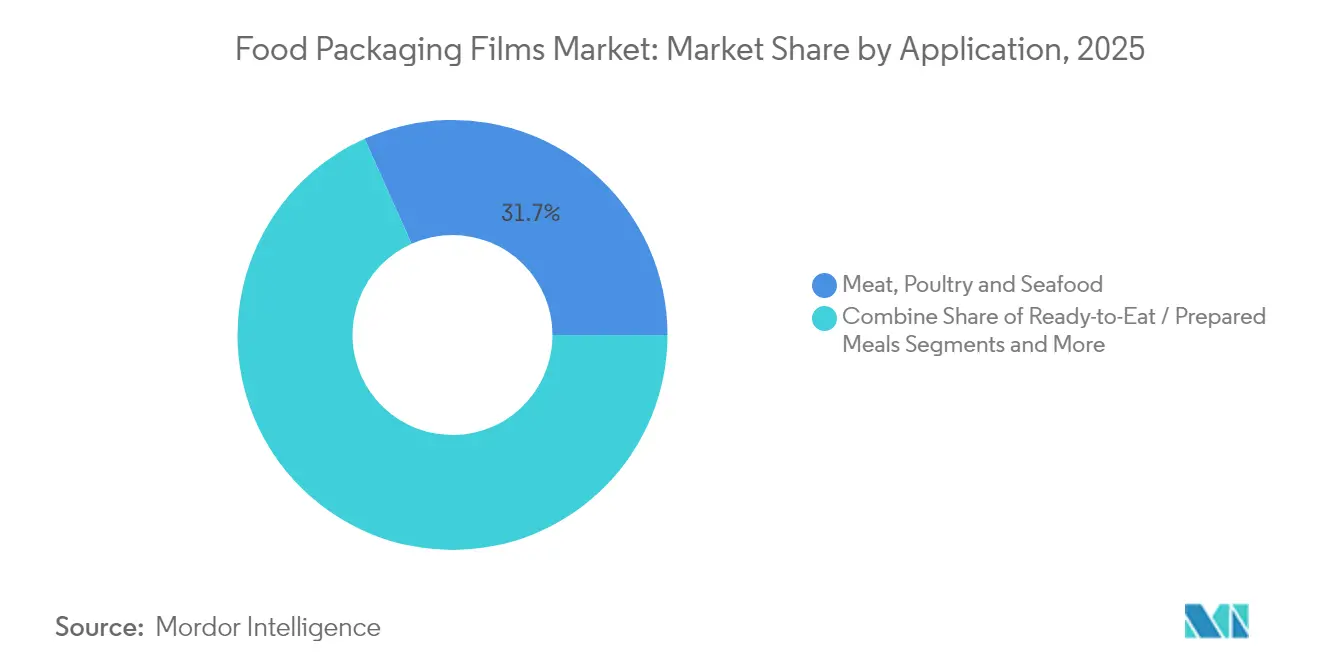

- By application, meat, poultry and seafood accounted for a 31.71% share of the food packaging films market size in 2025, while ready-to-eat meals are advancing at a 6.39% CAGR to 2031.

- By technology, biaxial orientation commanded 32.21% of the food packaging films market share in 2025 and is set to record the highest 7.05% CAGR by 2031.

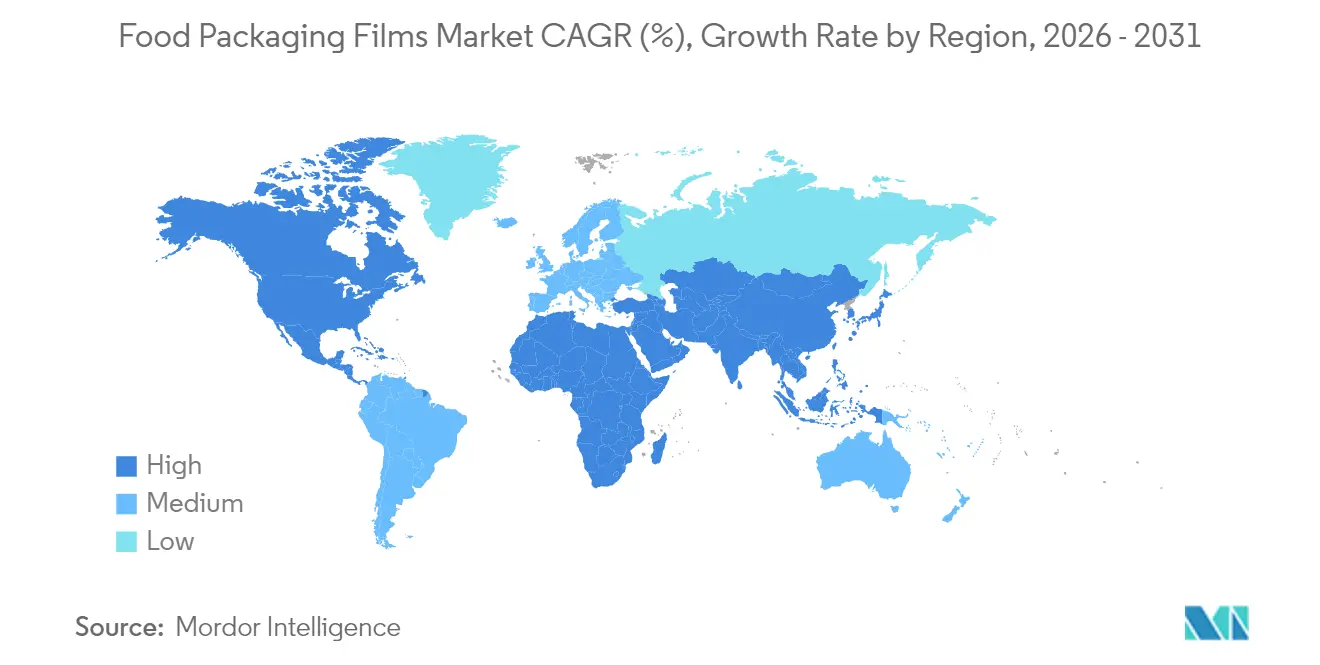

- By geography, Asia-Pacific represented 38.12% of global revenue in 2025; North America is projected to deliver the peak 6.18% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Food Packaging Films Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenience-ready meal boom in urban centres | +1.2% | Global, concentrated in North America & Asia-Pacific cities | Medium term (2-4 years) |

| Sustainability mandates for recyclable films | +0.9% | Europe & North America leading, Asia-Pacific catching up | Long term (≥ 4 years) |

| E-commerce meal-kit and grocery fulfilment | +0.8% | North America & Europe core, Asia-Pacific expanding | Short term (≤ 2 years) |

| High-barrier films for shelf-life extension | +0.7% | Global, premium in developed markets | Medium term (2-4 years) |

| Dark-store cold-chain micro-fulfilment | +0.4% | Urban hubs worldwide | Short term (≤ 2 years) |

| Chemical-recycling scale-up for PCR films | +0.6% | Europe leading, North America following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustainability mandates accelerating recyclable mono-material films

Legislation drives the food packaging films market toward structures that pass existing recycling tests without costly separation steps. The European Union now stipulates 30% recycled content in PET food packaging by 2030, rising to 50% by 2040, and bans PFAS above strict limits beginning 2026.[1]European Commission, “Regulation (EU) 2025/40 on Packaging and Packaging Waste,” eur-lex.europa.eu California’s SB 54 adds parallel pressure, requiring 25% cutbacks in single-use plastics and a 65% recycling rate by 2032. Klöckner Pentaplast answered with kp FlexiFlow films containing more than 93% PP or 95% PE while slashing weight by up to 75%.[2]Klöckner Pentaplast, “kp launches recyclable barrier flow-wrap films,” kpfilms.com

Surge in e-commerce meal-kit and grocery fulfilment packaging

Direct-to-consumer shipping exposes film to greater puncture risks and temperature swings than in-store retail. HelloFresh’s AI-driven pack optimisation accounts for weather patterns and trip length to minimise material without sacrificing product safety. Logistics models blending batch and zone picking cut fulfilment time and travelled distance, boosting demand for tear-resistant pouches compatible with automated loading lines.

Dark-store micro-fulfilment cold-chain growth

Thirty-minute urban delivery windows heighten requirements for insulation, condensation control and tamper evidence. Smart indicators embedded in films track temperature deviations, giving operators actionable freshness data during rapid dispatch cycles. As networks scale, suppliers look to low-density mono-PE laminates to simplify recycling while meeting compression-strength needs inside micro-hubs.

Chemical-recycling infrastructure scale-up unlocking PCR films

Axens, IFPEN and JEPLAN have commercialised Rewind PET, converting mixed waste into food-contact resins with virgin-like purity.[3]JEPLAN, “Rewind® PET Chemical Recycling Process Commercialisation,” jeplan.co.jp Nova Chemicals’ Indiana plant will deliver over 100 million lb of mechanically recycled PE annually for Amcor’s film portfolio. Lifecycle-assessment work shows super-critical-propane recycling of polypropylene emits only 0.32 kg CO₂ per kg of rPP—75% lower than solvent-antisolvent alternatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Petrochemical feedstock price volatility | -0.8% | Global, acute in import-dependent regions | Short term (≤ 2 years) |

| Tightening global single-use-plastic legislation | -0.6% | Europe & North America leading, spreading worldwide | Medium term (2-4 years) |

| Limited supply of food-grade high-barrier recycled resin | -0.4% | Global, notable in markets with strict mandates | Long term (≥ 4 years) |

| Rapid substitution by paper-based barrier laminates | -0.5% | Europe & North America core | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening global single-use-plastic legislation

South Australia expanded its plastics ban in September 2024 to include EPS food containers and thick carry bags, forcing rapid switchovers to alternative substrates. Similar restrictions in New South Wales remove plastic straws and integrated cutlery from packaged meals as of January 2025.[4]Environment Protection Authority, “Plastics bans and packaged food and drinks,” epa.nsw.gov.au

Limited supply of food-grade high-barrier recycled resins

Mechanical recycling struggles with post-consumer contamination that jeopardises food-contact approvals. FDA letters of no-objection remain scarce, pushing producers toward costlier chemical recycling until infrastructure scales.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Polyethylene retains scale while bioplastics outpace growth

Polyethylene generated 50.74% of 2025 revenue, underlining its unrivalled supply chain and processing versatility in the food packaging films market. The resin’s dominance stems from stable pricing, forgiving melt behaviour and compatibility with blown and cast processes. Even so, legislative momentum toward lower carbon footprints is steering procurement teams toward bioplastic grades that expand at a 6.33% CAGR. Producers are piloting sugarcane-based LDPE pouches that match seal integrity and clarity, each sequestering 43 g of CO₂ while fitting existing converting assets. Polypropylene remains a workhorse for oriented snack wraps thanks to inherent stiffness and moisture resistance, whereas PET benefits from rising access to PCR content through chemical-recycling breakthroughs. Limited-volume polyamide finds niches requiring toughness and puncture performance inside retort pouches.

Over the outlook, virgin polyolefins will still anchor sourcing, but the food packaging films industry sees a decisive tilt toward certified circular or bio-attributed alternatives in premium SKUs. As mechanical lines integrate deodorisation and extruders embrace low-temperature screws, film makers target 30% recycled inclusion without downgrading machinability. Brand pledges for 100% recyclable and 50% recycled packaging by 2030 further elevate demand for PCR-rich LLDPE blends across chilled and frozen sectors. Second-order effects include re-tooling extrusion dies to handle viscosity swings when switching between virgin and recycled streams, and revisiting corona-treatment protocols to maintain print adhesion on bio-based substrates.

By Packaging Type: Bags and pouches gain share on e-commerce momentum

Wraps and roll-stocks held 28.35% share in 2025 as continuous-form films power high-speed flow-wrap and thermoform-fill-seal lines in meat and dairy plants. Yet bags and pouches post the quickest 7.45% CAGR, mirroring meal-kit growth and the convenience orientation of single-serve portions. Their lightweight profile lowers dimensional weight, cutting courier surcharges and greenhouse-gas emissions per shipment critical for grocery platforms seeking carbon-neutral last-mile commitments. The food packaging films market size for bags and pouches is forecast to climb in tandem with quick-commerce adoption, aided by improvements in MDO-PE that deliver monomaterial-film stiffness comparable to PET laminations.

Lidding films stay resilient because MAP trays for fresh protein still require peelable, anti-fog top webs. Shrink films used for bulk cheese and poultry also preserve volume, although downgauging strategies are universal as resin costs fluctuate. In response, suppliers deploy digital twin simulation to optimise gusset geometry and zipper placement, driving both material savings and consumer convenience. As microwave-susceptor technologies evolve, retort-capable stand-up pouches continue to siphon share from rigid cans, especially in premium soup and rice entrées.

By Application: Ready-to-eat meals set the pace amid lifestyle shifts

Protein packaging remains the largest slice at 31.71% in 2025 as fresh and processed meat products demand stringent oxygen barriers and abuse resistance to traverse lengthening cold chains. Still, the ready-to-eat category grows 6.39% annually, propelled by hybrid work routines and appetites for refrigerated or shelf-stable meals that heat quickly. The food packaging films market size for ready-to-eat solutions benefits from oven-able paper-tray formats lined with PET-based films that seal hermetically and withstand 220 °C baking temperatures.

Dairy relies on high-clarity PA/PE multilayers for cheese vacuums, whereas bakery brands toggle between PP flow-wraps and emerging cellulose films that promise industrial compostability. Produce shippers test ethylene-scavenging sachets embedded within breathable LDPE bags to slow ripening. In niche segments such as infant nutrition, multilayer aluminium-oxide barriers hold firm due to regulatory conservatism, although research into nano-silica coatings hints at future displacement.

By Technology: Biaxial orientation sustains a commanding lead

Biaxially oriented lines contributed 32.21% of 2025 revenue and will advance at a 7.05% CAGR through 2031, reflecting the unmatched modulus, optical clarity and downgauging potential of BOPP and BOPET. Stretching in both machine and transverse directions aligns polymer chains, yielding films with balanced tear resistance and step-change gas-barrier performance indispensable for snack and dried-food markets. Cast-film capacity, while mature, finds growth in co-extruded structures for cheese shrink bags that require precise thickness profiles. Blown-film operators extend portfolio breadth via 9- and 11-layer air-ring systems, combining EVOH and mLLDPE to produce recyclable all-PE laminates suitable for high-humidity produce packs.

MDO-PE gains traction as printers demand smoother surfaces for high-definition graphics while maintaining mono-material recyclability. Adoption of digital process controls and infrared gauging has shrunk thickness tolerances below ±2 µm, permitting aggressive down-gauge targets without mechanical compromise. As energy costs rise, low-temperature extruders marketed under the EVO brand cut specific energy consumption by 20%, improving sustainability metrics and bolstering the cost competitiveness of multilayer blown film.

Geography Analysis

Asia-Pacific generated 38.12% of 2025 global revenue, underpinned by vast food-processing clusters in China and India and a proliferation of small and midsize converters servicing regional snack and noodle brands. Local resin integration, supportive export incentives and expanding cold-chain networks enable quick scaling of flexible-pack formats. Government subsidies for advanced extrusion lines in coastal provinces further cement regional leadership in thin-gauge, high-barrier BOPP export supply. Rising middle-class incomes stimulate demand for portion-controlled, branded goods, embedding growth for the food packaging films market across ASEAN.

North America, though smaller in share, is set to log a 6.18% CAGR through 2031—the fastest worldwide. Drivers include strict recyclability laws, robust e-commerce penetration and consumer readiness to pay premiums for verified PCR content. California’s SB 54 forces retailers to meet recycling-rate milestones, sparking investment in chemical recycling hubs and PCR-compatible mono-PE laminates. The food packaging films market share in North America is thus poised to expand within high-margin categories such as meal-kit liners and stand-up pouches for frozen entrées.Europe retains a strong foothold, benefiting from cohesive policy frameworks and technical know-how in solvent-less lamination and barrier-coating chemistries. The continent’s Packaging and Packaging Waste Regulation sets the world’s most ambitious recycled-content thresholds, accelerating deployment of high-barrier yet recyclable designs.

Eastern Europe contributes incremental capacity as multinationals relocate production closer to EU demand centres to mitigate supply-chain emissions and tariff exposure. Elsewhere, the Middle East and Africa tap oil-derivative feedstock advantages to court multinational fillers, and Latin America leverages agricultural export flows that require moisture-proof films for protein and produce shipments.

Competitive Landscape

The industry is Fragmented, with multibillion-dollar deals redefining scale economies and R&D breadth. Amcor’s USD 8.4 billion all-stock merger with Berry Global in April 2025 formed a packaging leader exceeding USD 24 billion in annual sales and unlocking USD 650 million in synergies through harmonised procurement and shared extrusion know-how. Toppan’s USD 1.8 billion purchase of Sonoco’s flexibles operation boosts its global footprint in retort-pouch and high-barrier roll-stock, while Mondi’s planned takeover of Schumacher’s Western European assets broadens capacity in corrugated-backed e-commerce sleeves.

Technology investments differentiate players: Amcor secured a European patent for AmFiber Performance Paper, a heat-seal coated paper with >80% fibre content delivering grease and moisture barriers suitable for confectionery wraps. Klöckner Pentaplast’s kp FlexiFlow range pioneers recyclable flow-wraps surpassing 90% mono-material content, meeting CEFLEX guidelines years ahead of schedule. Concurrently, converters strike supply contracts for high-purity rPE and rPP to safeguard availability against surging compliance demand; Amcor’s memorandum with Nova Chemicals exemplifies these tie-ups.

White-space entrants focus on paper-coated, cellulose-based or edible film solutions that target single-portion snacks and condiment sachets. Smart-pack start-ups embed NFC chips for freshness verification, courting premium grocers. Medium-size regional players aim to carve niches in PCR-rich meat casings or compostable produce bags, though capital-intensive barrier-film R&D limits their ability to match multinationals’ pace.

Food Packaging Films Industry Leaders

Amcor Plc

Mondi Group

Constantia Flexibles Group GmbH

Coveris Management GmbH

Sealed Air Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Amcor finalised its USD 8.4 billion combination with Berry Global, creating the world’s largest consumer and healthcare packaging supplier.

- February 2025: Mondi agreed to acquire Schumacher Packaging’s Western European assets to reinforce e-commerce corrugated supply.

- February 2025: The EU adopted Regulation (EU) 2025/40, obliging full recyclability by 2030 and 30% recycled content in PET food packaging.

- January 2025: Amcor signed an MoU with Nova Chemicals to purchase mechanically recycled PE resin for food-grade flexible films.

- December 2024: Toppan purchased Sonoco’s thermoformed and flexibles division for USD 1.8 billion, strengthening its retort-pouch portfolio.

- October 2024: Klöckner Pentaplast launched kp FlexiFlow recyclable barrier flow-wraps featuring 93% PP or 95% PE content.

Global Food Packaging Films Market Report Scope

The Food Packaging Films market study tracks the value consumption (USD) for packaging films in the food industry. The study provides a detailed assessment of the packaging film products based on the underlying factors related to the demand for packaging, end-products, and supply-side perspective. The analysis is based on the market insights captured through secondary research and the primaries. The market also covers the major factors impacting the growth of the Food Packaging Films in terms of drivers and restraints.

The Food Packaging Films Market is Segmented by Material (Polyethylene, Polypropylene, Polyethylene Terephthalate and Other Materials), and by Geography (North America (United States, Canada), Europe (Germany, United Kingdom, France, Italy, Rest of Europe), Asia-Pacific (China, India, Japan, Rest of Asia-Pacific), Latin America (Brazil, Mexico, Rest of Latin America), and Middle East and Africa (United Arab Emirates, Saudi Arabia, South Africa, Rest of Middle East and Africa ). The Market Sizes and Forecasts are Provided in Terms of Value (USD ) for all the Above Segments.

| Polyethylene (LDPE, LLDPE, HDPE) |

| Polypropylene (CPP, BOPP) |

| Polyethylene Terephthalate (BOPET) |

| Polyamide (BOPA) |

| Other Material Types |

| Wraps and Roll-Stocks |

| Bags and Pouches |

| Lidding Films |

| Other Packaging Type |

| Meat, Poultry and Seafood |

| Dairy and Cheese |

| Bakery and Confectionery |

| Fruits and Vegetables |

| Ready-to-Eat / Prepared Meals |

| Others Application |

| Blown Film Extrusion |

| Cast Film Extrusion |

| Biaxial Orientation (BOPP/BOPET) |

| Other Technology |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Nigeria | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Material Type | Polyethylene (LDPE, LLDPE, HDPE) | ||

| Polypropylene (CPP, BOPP) | |||

| Polyethylene Terephthalate (BOPET) | |||

| Polyamide (BOPA) | |||

| Other Material Types | |||

| By Packaging Type | Wraps and Roll-Stocks | ||

| Bags and Pouches | |||

| Lidding Films | |||

| Other Packaging Type | |||

| By Application | Meat, Poultry and Seafood | ||

| Dairy and Cheese | |||

| Bakery and Confectionery | |||

| Fruits and Vegetables | |||

| Ready-to-Eat / Prepared Meals | |||

| Others Application | |||

| By Technology | Blown Film Extrusion | ||

| Cast Film Extrusion | |||

| Biaxial Orientation (BOPP/BOPET) | |||

| Other Technology | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Nigeria | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the Food Packaging Films Market?

The market is valued at USD 45.99 billion in 2026 and is projected to reach USD 57.25 billion by 2031 based on a 4.49% CAGR.

Which region grows the fastest in Food Packaging Films Market?

North America shows the highest forecast CAGR at 6.18% through 2031, driven by strict recyclability laws and e-commerce demand.

Why are mono-material films gaining traction?

Regulations in Europe and US states require higher recycling rates and recycled content, favouring PE- or PP-rich structures that pass sortation tests without delamination.

Which application is expanding quicker than the overall market?

Ready-to-eat and prepared meals packaging is rising at a 6.39% CAGR, outpacing the broader market as urban consumers seek convenience.

How is industry consolidation affecting competition?

Mega-mergers such as Amcor–Berry Global yield economies of scale, larger PCR-resin supply contracts and broader R&D budgets, intensifying competitive barriers for smaller converters.

What technologies dominate future investment?

Biaxially oriented films remain the cornerstone due to high barrier performance, while chemical recycling and smart packaging sensors attract the most new capital for sustainability and traceability gains.

Page last updated on: