Sustainable E-Commerce Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

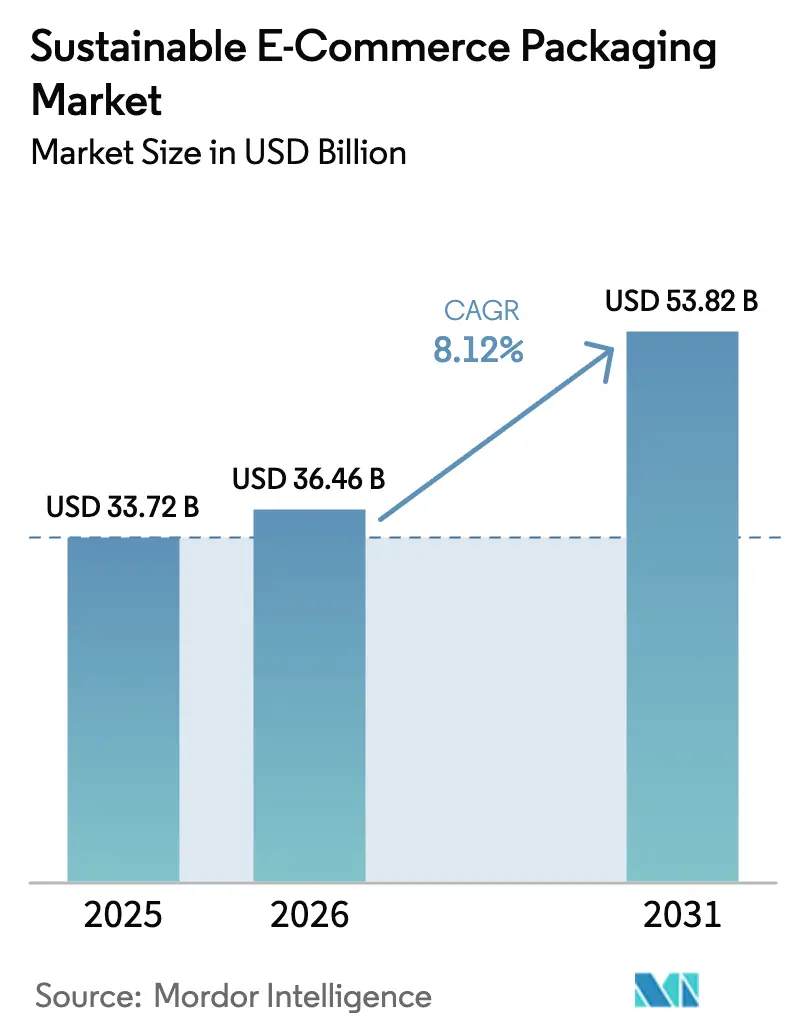

| Market Size (2026) | USD 36.46 Billion |

| Market Size (2031) | USD 53.82 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle East and Africa |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sustainable E-Commerce Packaging Market Analysis by Mordor Intelligence

The Sustainable E-Commerce Packaging Market size is projected to be USD 33.72 billion in 2025, USD 36.46 billion in 2026, and reach USD 53.82 billion by 2031, growing at a CAGR of 8.12% from 2026 to 2031.

Rising regulatory pressure on single-use plastics, surging online order volumes, and clear consumer preference for low-carbon materials are accelerating demand for sustainable solutions across last-mile delivery. Format optimization technologies that reduce dimensional weight fees, alongside expanding circular-economy business models, are broadening adoption beyond early movers. Consolidation among leading fiber-based players is improving global scale and R&D budgets, while AI-enabled right-sizing systems deliver measurable cost savings that reinforce payback arguments for brand owners.

Key Report Takeaways

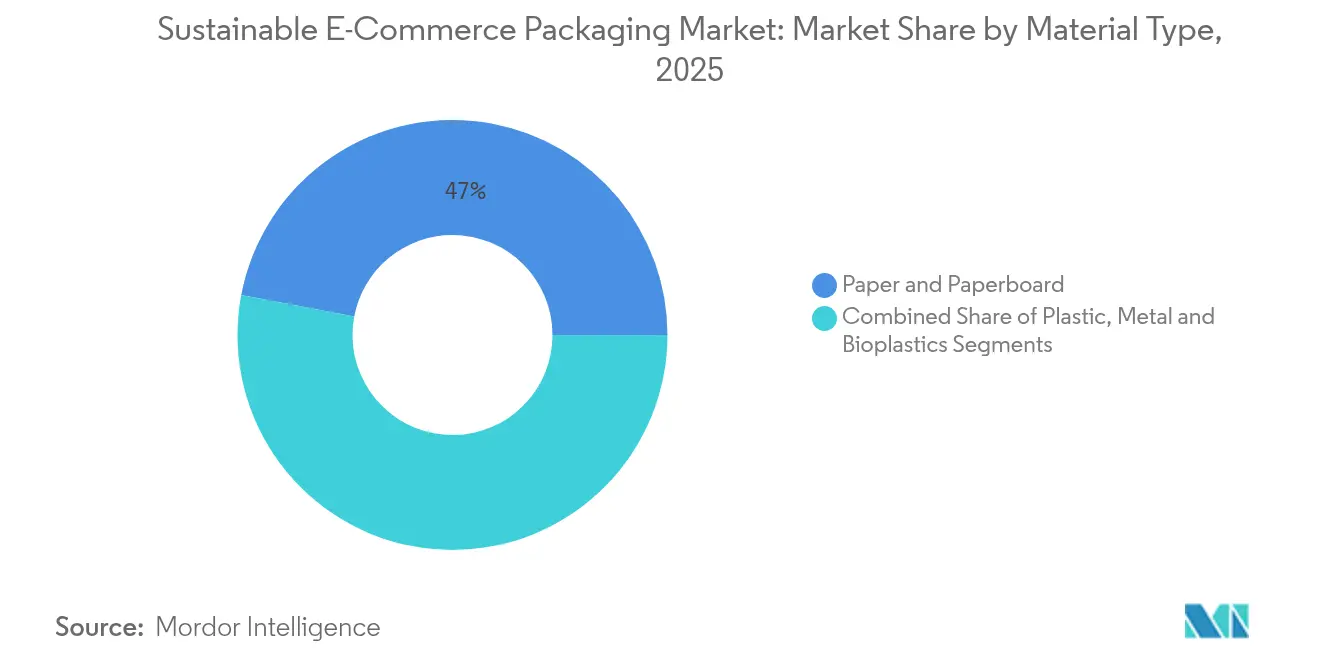

- By material type, paper and paperboard led with 47.02% of the sustainable e-commerce packaging market share in 2025, whereas bioplastics are forecast to expand at a 9.78% CAGR to 2031.

- By packaging format, corrugated boxes held 72.10% revenue share in 2025; mailers and envelopes are advancing at a 9.41% CAGR through 2031.

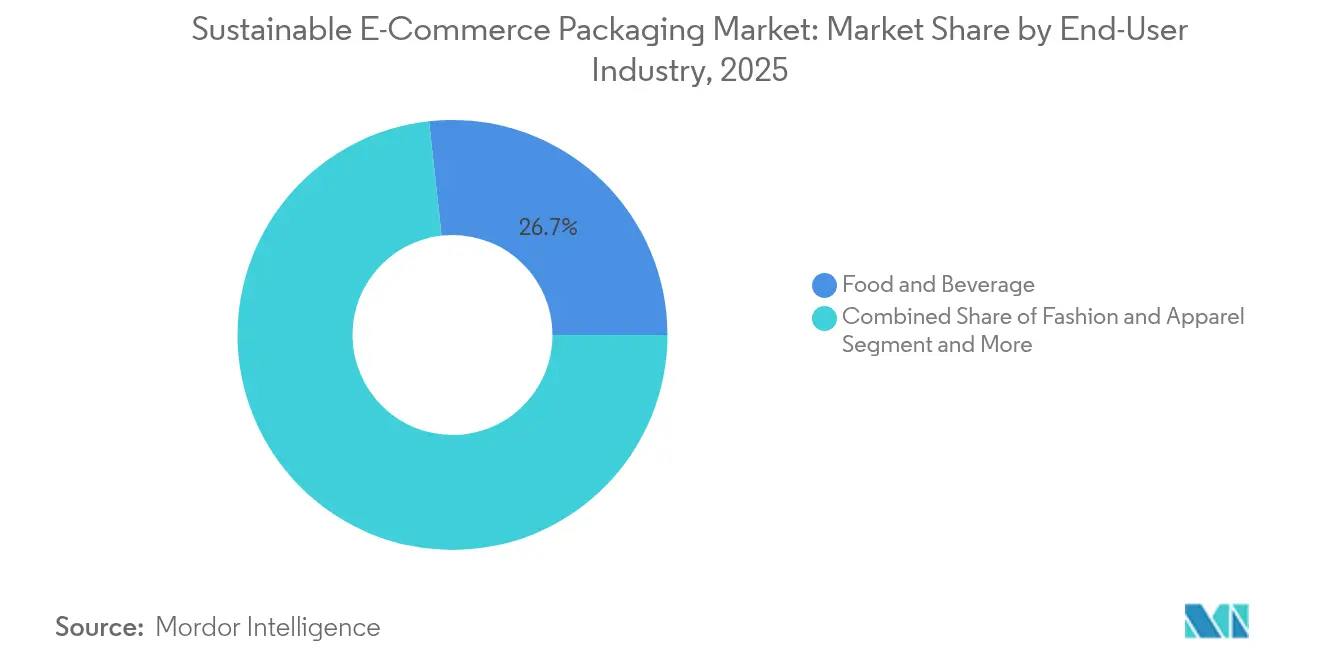

- By end-user industry, food and beverage accounted for 26.74% share of the sustainable e-commerce packaging market size in 2025, while pharmaceuticals record the fastest CAGR at 9.23% through 2031.

- By sustainable attribute, recyclable options dominated with 61.05% share in 2025; compostable solutions show the highest growth potential at 9.58% CAGR.

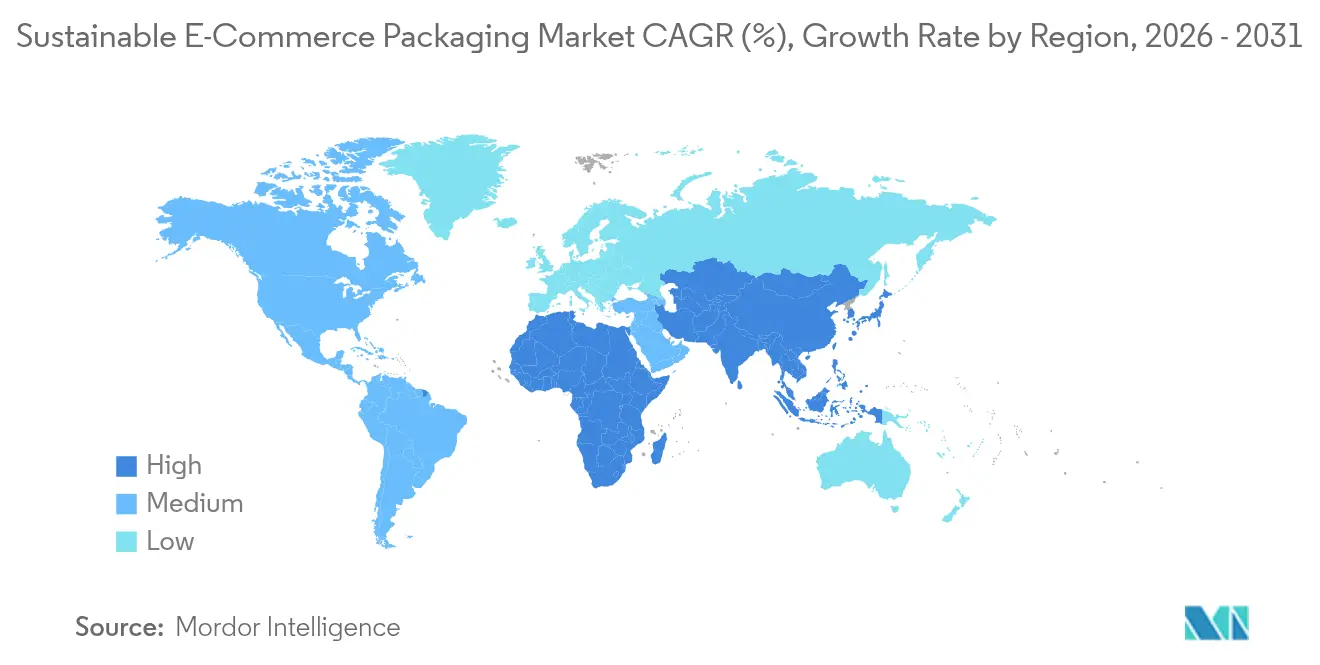

- By geography, Asia-Pacific captured 42.35% of the sustainable e-commerce packaging market share in 2025, yet Middle East and Africa is the fastest-growing geography at 9.66% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sustainable E-Commerce Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer preference for recyclable materials | +1.8% | EU, North America, Global | Medium term (2-4 years) |

| Surge in e-commerce order volumes | +2.1% | Asia-Pacific, Global | Short term (≤ 2 years) |

| Bans and eco-taxes on single-use plastics | +1.5% | EU core, North America, Asia-Pacific | Long term (≥ 4 years) |

| AI-driven right-sizing systems | +0.9% | North America, EU | Medium term (2-4 years) |

| Reusable packaging-as-a-service models | +0.7% | North America, EU | Long term (≥ 4 years) |

| Scope-3 carbon reporting mandates | +1.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift in consumer preference toward recyclable and eco-friendly materials

Brands that prove real environmental commitment now secure price premiums and deeper loyalty. Beauty and personal-care labels report that 61% of shoppers actively seek eco-aligned brands, prompting conversions to post-consumer-recycled (PCR) substrates and achieving carbon-footprint cuts of more than 40% versus virgin resin alternatives. PCR uptake therefore builds both revenue resilience and reputational equity. Retailers are extending PCR mandates to private-label ranges, making recyclability a minimum entry requirement across multiple online categories. Governments reinforce the trend via mandatory recycled-content thresholds that take effect in the European Union in 2025, raising baseline demand for compatible materials. The resulting pull-through effect speeds investment in next-generation fiber recovery systems, widening quality supply and lowering cost premiums. As conversion volumes climb, early adopters protect margin by locking multiyear PCR feedstock agreements.

Explosive growth in e-commerce order volumes and last-mile deliveries

Online spending outpaces store-based retail, lifting protective-packaging requirements across categories. Ranpak logged a 14.7% rise in void-fill volumes in Q3 2024, with net sales up 11.4% to USD 92.2 million [1]Ranpak Holdings, “Q3 2024 Investor Presentation,” ranpak.com. Amazon’s 96.7%-repulpable paper-padded mailer proves that fiber-based solutions can meet drop-test criteria and integrate into curbside streams. E-retailers subsequently accelerate plastic-to-paper shifts, capturing both cost efficiencies and sustainability gains. Volume-linked economies of scale widen price competitiveness for high-strength lightweight papers that resist puncture under automated handling. The trend raises demand for moisture-barrier coatings compatible with mainstream recycling processes, stimulating joint R&D between converters and chemical suppliers. As shipment frequency normalizes at a structurally higher base, packaging suppliers that guarantee consistent quality at scale consolidate preferred-supplier status.

AI-driven smart-box right-sizing systems reducing dimensional-weight fees

Algorithms that match product dimensions to optimal carton size in real time cut filler use and lower carrier surcharges. Ranpak’s Cut’it EVO platform trims carton height for as many as four lid options on a single line, delivering 15-25% material savings and sizable logistics cost cuts for early adopters. Retailers integrate dimension data into warehouse management systems, creating closed-loop feedback that continuously refines carton libraries. Reduced outbound volume improves truckfill rates and curbs greenhouse-gas emissions, strengthening performance against Scope-3 targets. Vendors now bundle AI software, vision systems, and service contracts, opening recurring-revenue streams that buffer cyclicality in substrate demand. As return-on-investment windows shorten to under 18 months, procurement teams elevate right-sizing to a top automation priority within omnichannel fulfillment upgrades.

Reusable packaging-as-a-service models gaining retailer adoption

Circular platforms supplying returnable mailers attract retailers eager to cut single-use waste and differentiate customer experience. The World Economic Forum names 2025 as a tipping point, given scaling pilots by apparel and grocery leaders [2]World Economic Forum, “Circularity in Packaging: 2025 Tipping Point,” weforum.org. Providers such as RePack manage reverse-logistics loops and cleaning operations, charging subscription fees that align profitability with reuse frequency. Consumer acceptance improves as drop-off networks expand and digital incentive programs gamify returns. Life-cycle assessments indicate that mailers achieve breakeven environmental benefit after three to five trips, depending on transport distance. Challenges persist in lost-asset rates and washing-facility capital costs, yet data-driven asset-tracking mitigates shrinkage risk. Retailers using pilot data to redesign fulfillment flows expect measurable cost parity with single-use formats once asset pools surpass critical scale thresholds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain volatility in fiber/polymer feedstocks | -1.1% | Global, import-dependent regions | Short term (≤ 2 years) |

| Barrier limitations of certain bio-based films | -0.8% | Global, food and pharma hubs | Medium term (2-4 years) |

| Cyber-security risks in connected packaging data | -0.3% | North America, EU | Long term (≥ 4 years) |

| Recycling-infrastructure gaps for multi-layer mailers | -0.6% | Developing markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-chain volatility and fluctuating fiber / polymer input costs

Containerboard prices have posted double-digit jumps since 2024, propelled by surging online demand and energy-cost spikes, straining converters’ margins. Bio-based resin supply is even tighter, with agricultural-commodity price swings feeding through to PLA and PHA cost structures. Large integrated producers mitigate exposure through captive forestry assets or multiyear buy-side contracts, but small converters face liquidity risk as working-capital needs inflate. Spot-price instability complicates forward-pricing for brand owners, delaying contract renewals and slowing new-format rollouts. Heightened price uncertainty therefore temporarily favors established incumbents that can underwrite hedging strategies until capacity additions ease feedstock tension.

Barrier-property limitations of certain bio-based films and coatings

Many compostable polymers fall short on moisture and oxygen barriers, limiting use in food and pharma shipments where shelf-life integrity is critical. Multilayer structures raise performance, yet introduce recycling challenges and extra cost. Nanocellulose coatings improve water vapor transmission rates, but commercial scale remains limited [3]PMC, “Nanocellulose Coatings for Bio-Based Films,” pubmed.ncbi.nlm.nih.gov. Brand owners must therefore weigh the reputational benefit of bio-based claims against potential spoilage risk. Hybrid solutions, such as starch-based liners combined with recyclable paper outers, emerge as interim fixes but add process complexity. Until material science closes the barrier gap at competitive cost, adoption in moisture-sensitive segments will lag more forgiving categories like apparel.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type : Bioplastics extend gains despite fiber dominance

Paper and paperboard accounted for 47.02% of the sustainable e-commerce packaging market in 2025 thanks to broad recyclability, cost advantages, and robust supply chains. Bioplastics register the fastest 9.78% CAGR to 2031 as sugarcane-derived PE, bark-based films, and algae coatings mature. The sustainable e-commerce packaging market size for bioplastics is projected to reach USD 9.32 billion by 2031, reflecting increased demand for higher barrier performance next to food and personal-care items. Fiber producers safeguard share by adding water-resistant dispersions that pass repulpability tests, while petrochemical incumbents invest in chemical-recycling back-loops to prolong the relevance of mono-material recyclables. Venture funding in protein-based films signals widening raw-material options poised to narrow price gaps with incumbent grades.

Cost differentials between kraft linerboard and PLA narrowed to under 20% in 2025, accelerating substitution in mailers that do not require high-clarity windows. Brands targeting carbon-neutral pledges lean on lifecycle-analysis data that position certified compostable films as a lower-emission choice when paired with industrial-compost access. Industrial procurement teams therefore split volumes across both fibers and emerging biopolymers to hedge technical and regulatory risk. Suppliers that can bundle both substrates within a single sourcing contract gain negotiating leverage and lock in throughput across economic cycles.

By Packaging Format : Mailers outpace boxes through right-sizing adoption

Corrugated boxes dominated at 72.10% of the sustainable e-commerce packaging market in 2025 on versatility, stacking strength, and a mature recycling stream. Mailers and envelopes, however, show a 9.41% CAGR on the strength of AI-assisted cartonization systems that eliminate void fill. The sustainable e-commerce packaging market size for mailers is forecast to hit USD 8.55 billion in 2031 as retailers deploy paper padded designs that meet fragile-item drop tests. Slim form factors benefit parcel hubs by lifting conveyor throughput and curbing trailer cube waste.

Retailers pair format diversification with SKU-level predictive analytics, ensuring the smallest feasible exterior is selected without compromising protective performance. Subscription-commerce brands prefer printed mailers that double as marketing real estate, accelerating adoption of digital-print lines that handle shorter runs economically. Boxes stay central for large consumer-electronics orders, yet box designs now integrate peel-and-seal closures and perforated returns strips to fit reverse-logistics workflows. Foam-in-place inserts give way to molded-pulp structures , cutting petroleum inputs and improving curbside recyclability.

By End-User Industry : Pharmaceutical demand accelerates under compliance pressure

Food and beverage held 26.74% of the sustainable e-commerce packaging market in 2025, driven by bulk grocery delivery and meal-kit services. Pharmaceutical shipments post a 9.23% CAGR through 2031 as regulators mandate higher recycled-content thresholds for cold-chain packaging. The sustainable e-commerce packaging market size for pharmaceuticals is forecast to exceed USD 5.95 billion by 2031, supported by fiber-based temperature-control boxes that replace EPS and reduce landfill burden. Beauty-and-personal-care sellers grow steadily as refill-ready packs and mono-material pumps reach commercial scale, fulfilling clean-beauty positioning.

Electronics brands continue searching for designs that balance ESD protection with recyclability; molded-pulp trays coated with antistatic layers gain pilot traction. Fashion houses test reusable garment bags that fold into prepaid return envelopes, cutting single-use polybag demand. Across industries, the convergence of e-grocery growth and prescription-drug home delivery raises performance expectations for fiber-based insulation, prompting investment in aerogel-liner scalability.

By Sustainable Attribute : Compostables gather momentum alongside recyclables

Recyclable solutions led with 61.05% share in 2025, anchored by mature curbside systems and rising EPR fees that reward recyclability. Compostables log a 9.58% CAGR as municipal organic-waste programs expand in Europe and selected North American cities. The sustainable e-commerce packaging market size tied to compostable formats is projected to touch USD 6.88 billion in 2031, aided by next-generation bio-resins that degrade in home composting within 90 days. Reusable attribute pilots expand among apparel and luxury sectors that value circular brand narratives. Biodegradable claims attract niche players targeting low-infrastructure regions, yet standardization challenges around certification and labeling slow mass uptake.

Brands increasingly adopt multi-attribute strategies, for example combining paper cores with compostable cushioning or employing reusable outer shells with recyclable inner liners. Regulators push clear “design for disassembly” guidelines in 2026, accelerating movement toward mono-material constructs that fit multiple end-of-life pathways.

Geography Analysis

Asia-Pacific accounted for 42.35% of the sustainable e-commerce packaging market in 2025, buoyed by China’s giant parcel volumes and India’s double-digit e-retail expansion. Several provincial governments in China have tied tax rebates to recycled-content thresholds, boosting demand for PCR linerboard among export-oriented sellers. Japanese converters pioneer smart-label technologies that integrate NFC tags, enabling authenticity checks and cold-chain alerts. Southeast Asian fulfillment hubs adopt paper-based insulated shippers to replace EPS, aligning with national plastic-waste roadmaps. The sustainable e-commerce packaging market size in Asia-Pacific is projected to surpass USD 23.6 billion by 2031, reflecting localized production of both fiber and bio-resin inputs.

Middle East and Africa posts the fastest 9.66% CAGR, lifted by Gulf-region omnichannel initiatives and Africa’s mobile-commerce surge. Saudi consumer surveys show willingness to pay up to 12% premiums for eco-friendly packaging, stimulating import substitution by regional converters installing high-throughput corrugators. The United Arab Emirates mandates 100% recyclability for e-commerce outer packs by 2026, propelling interest in lightweight kraft mailers. South Africa leverages comparatively robust collection infrastructure to pilot curbside separation of fiber-based insulated liners, positioning itself as a launchpad for sub-Saharan regional exports. Logistic free-zones in Kenya and Rwanda attract investment in automated mailer production lines that serve East-African cross-border trade.

North America and Europe remain mature but influential markets, shaping global standards through extended producer responsibility rules and plastic-tax rollouts. The European Union’s Packaging and Packaging Waste Regulation requires all e-commerce packs to be reusable or recyclable by 2030, spurring rapid design iterations among fiber specialists. United States brand owners anticipate nationwide EPR passage in at least eight additional states by 2027, integrating fee schedules into total-cost models. These regions continue to pilot high-complexity solutions such as fiber-based active-temperature shippers and cloud-connected track-and-trace labels that feed blockchain verification systems. Lessons learned feed into fast-growing emerging markets, accelerating global convergence toward proven circular-economy frameworks.

Competitive Landscape

Consolidation gathered pace in 2024–2025 after the USD 34 billion Smurfit Kappa-WestRock tie-up created the world’s largest fiber-based packaging supplier. International Paper reinforced scale by acquiring DS Smith for USD 7.2 billion, adding temperature-controlled fiber expertise. Top players now command deeper R&D budgets for compostable coatings and AI-enabled converting lines. The sustainable e-commerce packaging market therefore sees moderate concentration, yet room remains for specialists offering differentiated technology such as molded-pulp coolers or connected QR-based authenticity seals.

Strategic focus is shifting from mere production capacity to solutions that integrate materials, automation, and circular services. Amcor’s planned merger with Berry Global targets USD 650 million efficiency gains while pooling polymer science for mono-material recyclable films. Sealed Air commits to net-zero Scope 1 and 2 emissions by 2040, reporting a 54.6% cut already achieved, and embeds life-cycle assessment into new-product gating. Ranpak scales the Cut’it EVO right-sizing portfolio across Europe and Asia, adding on-line digital-print modules that convert packaging into marketing assets. Simultaneously, niche disruptors such as Returnity and RePack capture share with subscription-based reusable mailer pools that offload reverse-logistics management from retailers.

Technology partnerships intensify: converters sign joint-development agreements with bio-resin startups to secure intellectual property and speed time-to-market. Investors channel capital into nanocellulose-coated barrier papers, recognizing the premium available from food and pharma segments. Cyber-security expertise emerges as a differentiator for connected-pack providers that must safeguard consumer data while meeting Europe’s GDPR and the United States’ CCPA standards. Competitive advantage increasingly hinges on the ability to bundle substrate choice, automation know-how, and end-of-life strategy into a single contract that minimizes complexity for omnichannel retailers.

Sustainable E-Commerce Packaging Industry Leaders

Amcor PLC

Smurfit Kappa Group PLC

WestRock Company

DS Smith PLC

Mondi PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Mondi expanded its re/cycle MailerBAG production line in Poland to meet e-commerce demand for curbside-recyclable mailers.

- February 2025: Henkel introduced Technomelt E-COM G5 Eco Cool, a bio-based hot-melt adhesive optimized for automated e-commerce packaging.

- January 2025: DS Smith launched Tape Back, enabling two shipments with one glue strip and eliminating single-use plastic tear strips.

- December 2024: Movopack secured USD 2.5 million seed funding led by 360 Capital to scale circular e-commerce packaging.

Global Sustainable E-Commerce Packaging Market Report Scope

Based on current trends and market dynamics, the study tracks and analyzes the demand for sustainable e-commerce packaging within the end-user industry. The market numbers are derived by tracking the revenue generated by players providing sustainable e-commerce products across the end-user industries in the retail sector. The study provides a detailed breakdown of the various types of material across different geographies. This report analyzes the factors based on the prevalent base scenarios, key themes, and end-user vertical-related demand cycles.

The report covers sustainable e-commerce packaging companies. The market is segmented by material type (plastic, paper, and paper board metals), end user (fashion and apparel, consumer electronics, food and beverage, pharmaceuticals, personal care, and other end users), and geography (North America (United States and Canada), Europe (United Kingdom, Germany, France, Italy, Spain, and Rest of Europe), Asia-Pacific (China, India, Japan, Australia, and Rest of Asia-Pacific), Latin America (Brazil, Mexico, Argentina, and Rest of Latin America), Middle East and Africa (United Arab Emirates, Saudi Arabia, South Africa, and Rest of Middle East and Africa). The report offers market sizes and forecasts in value (USD) for all the above segments.

| Plastic |

| Paper and Paperboard |

| Metal |

| Bioplastics |

| Corrugated Boxes |

| Mailers and Envelopes |

| Pouches and Bags |

| Protective/Insulative Solutions |

| Fashion and Apparel |

| Consumer Electronics |

| Food and Beverage |

| Pharmaceuticals |

| Personal Care and Cosmetics |

| Recyclable |

| Compostable |

| Reusable |

| Biodegradable |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Material Type | Plastic | ||

| Paper and Paperboard | |||

| Metal | |||

| Bioplastics | |||

| By Packaging Format | Corrugated Boxes | ||

| Mailers and Envelopes | |||

| Pouches and Bags | |||

| Protective/Insulative Solutions | |||

| By End-User Industry | Fashion and Apparel | ||

| Consumer Electronics | |||

| Food and Beverage | |||

| Pharmaceuticals | |||

| Personal Care and Cosmetics | |||

| By Sustainable Attribute | Recyclable | ||

| Compostable | |||

| Reusable | |||

| Biodegradable | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the sustainable e-commerce packaging market?

The market stands at USD 36.46 billion in 2026 and is set to reach USD 53.82 billion by 2031.

How fast is the market expanding?

The sustainable e-commerce packaging market is growing at an 8.12% CAGR over the 2026-2031 period.

Which material segment is recording the quickest growth?

Bioplastics lead material growth with a 9.78% CAGR, driven by sugarcane- and bark-based resin innovations.

What geographic region holds the largest share?

Asia-Pacific commands 42.35% of global revenue, supported by high parcel volumes and government circular-economy policies.

Page last updated on: