Folding Carton In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

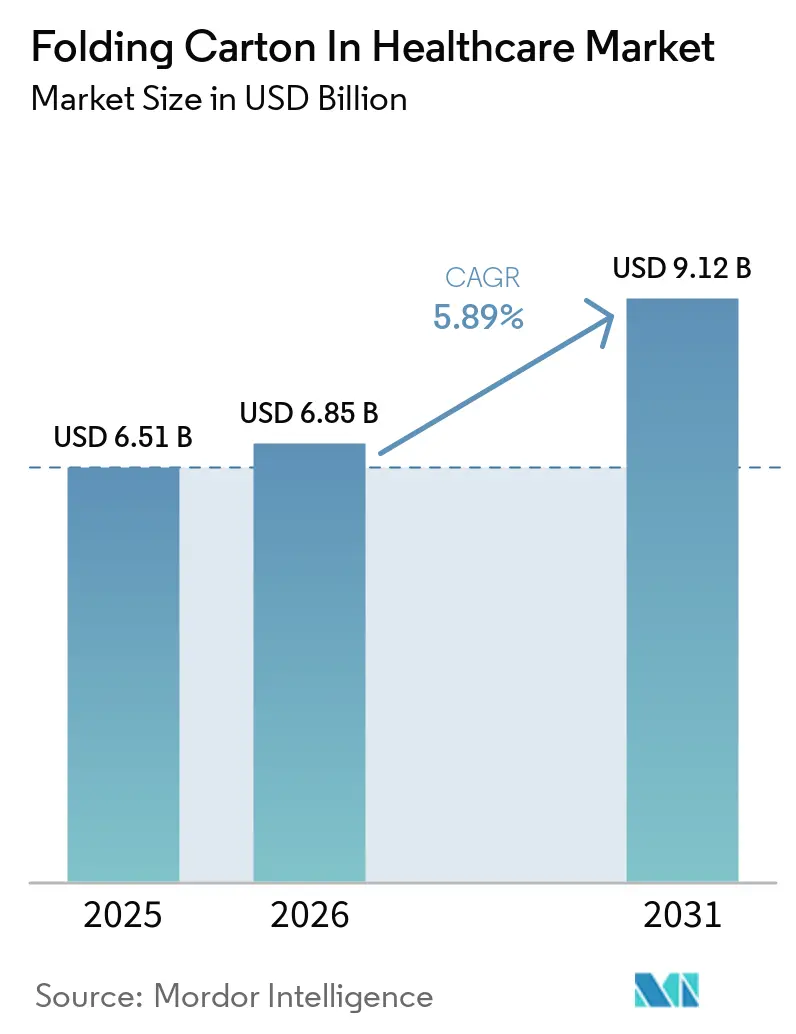

| Market Size (2026) | USD 6.85 Billion |

| Market Size (2031) | USD 9.12 Billion |

| Growth Rate (2026 - 2031) | 5.89% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Folding Carton In Healthcare Market Analysis by Mordor Intelligence

The folding carton in healthcare market size is expected to increase from USD 6.51 billion in 2025 to USD 6.85 billion in 2026 and reach USD 9.12 billion by 2031, growing at a CAGR of 5.89% over 2026-2031. Growth in the folding carton market for healthcare is being supported by serialization rules in the European Union and the United States, which are pushing drug makers to use larger, more precisely printed cartons with 2D DataMatrix codes and other identification details. The folding carton market in healthcare is also benefiting from the wider adoption of unit-dose formats for chronic-disease therapies, where child-resistant straight-tuck and reverse-tuck cartons are increasingly preferred for biologics and high-value small molecules. Regional demand remains uneven, with North America holding the largest share in 2025 while Asia-Pacific is set to post the fastest growth through 2031 as pharmaceutical production expands in India and China. Material and printing choices are shifting as buyers seek boards with stronger print performance, stronger sustainability credentials, and compatibility with shorter production runs that require variable data. Competition in the folding carton market for healthcare is tightening as integrated board producers use pulp access to protect margins, while specialized converters compete on pharmaceutical certifications, smart-packaging features, and the ability to serve emerging opportunities in veterinary medicines and medical devices.

Key Report Takeaways

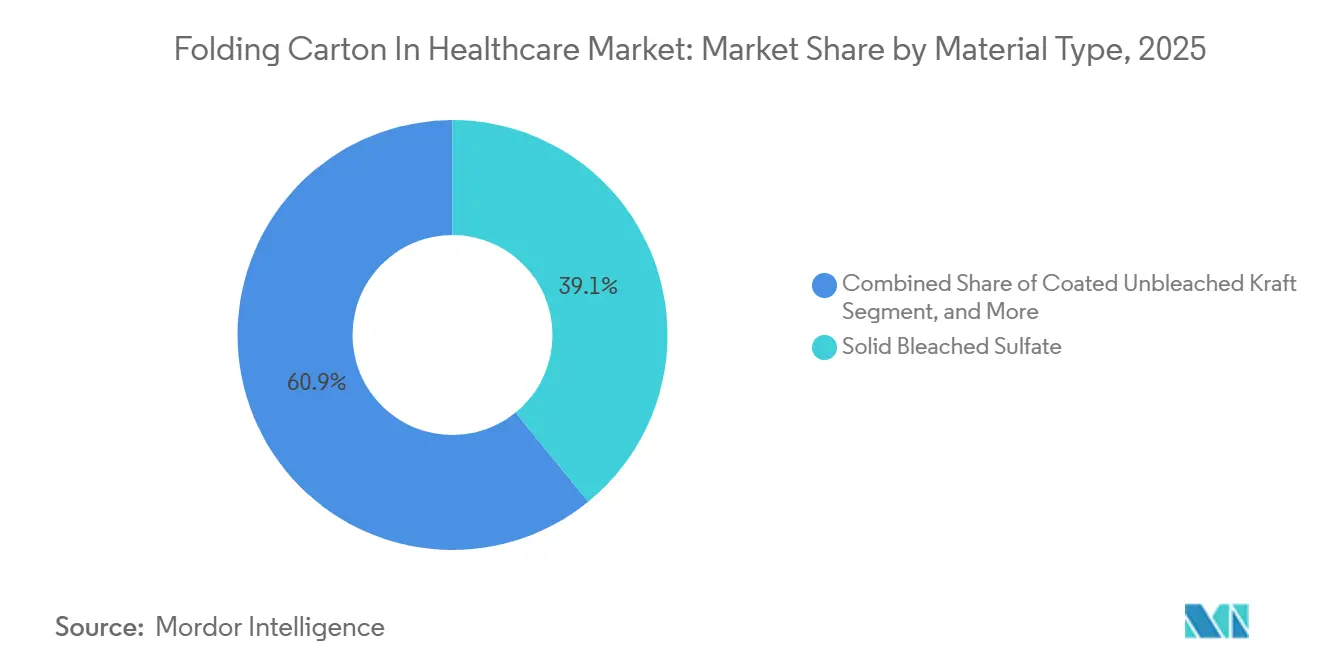

- By material type, solid bleached sulfate captured 39.13% of the folding carton in healthcare market share in 2025.

- By printing technology, the folding carton in healthcare market size for the digital printing segment is forecast to advance at a 6.78% CAGR through 2031.

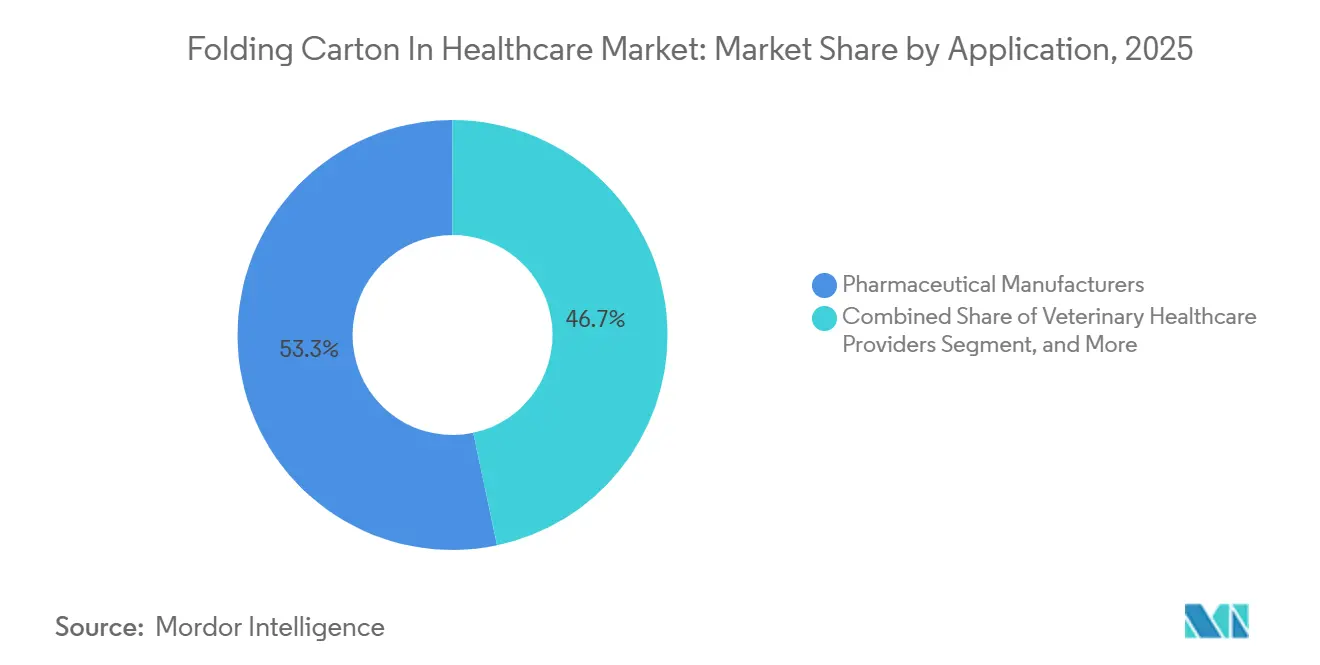

- By application, pharmaceutical manufacturers captured 53.32% of the folding carton in healthcare market share in 2025.

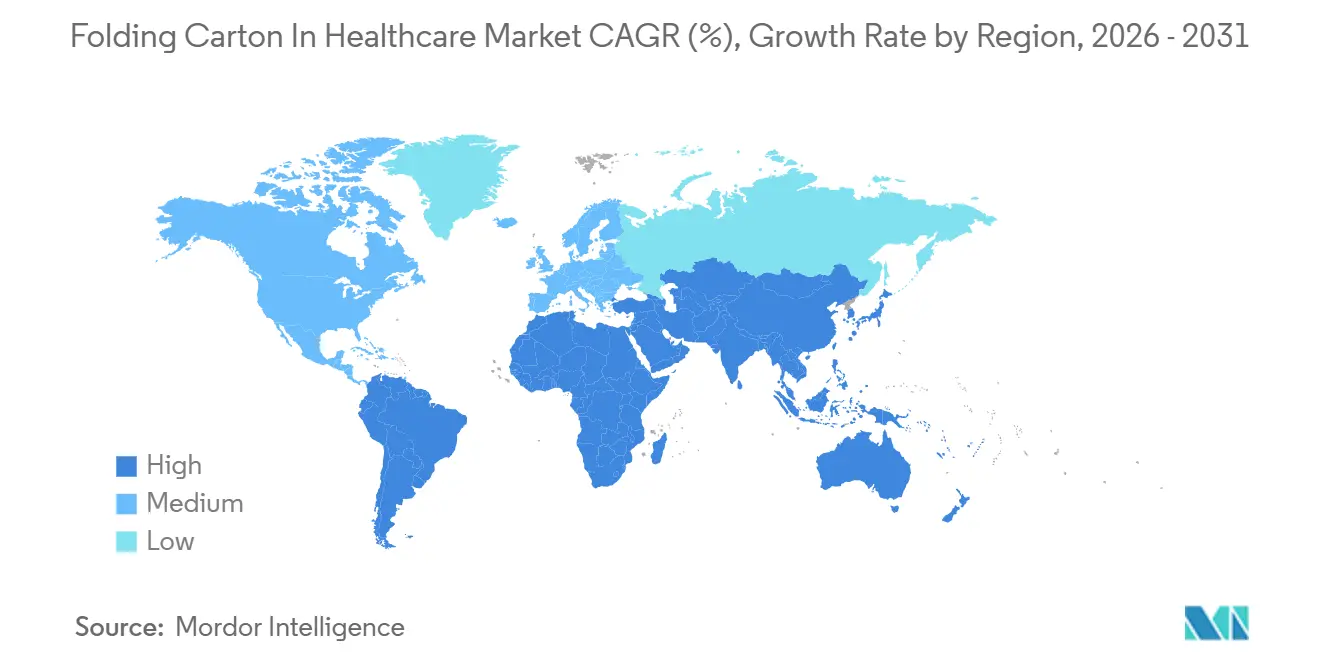

- By geography, the folding carton in healthcare market size for the Asia-Pacific segment is forecast to advance at a 6.57% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Folding Carton In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Child-Resistant Pharmaceutical Packaging | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Growth of Chronic Diseases Requiring Unit-Dose Treatments | +1.4% | Global, strongest in North America and Asia-Pacific | Long term (≥ 4 years) |

| Shift Toward Sustainable and Recyclable Paperboard | +1.0% | Europe and North America core, spillover to Asia-Pacific | Medium term (2-4 years) |

| Serialization Mandates Driving Larger Carton Real-Estate | +1.3% | North America, Europe, and emerging Asia-Pacific markets | Short term (≤ 2 years) |

| Adoption of Digital Printing for Personalized Medication Packs | +0.6% | North America and Europe, gradual adoption in Asia-Pacific | Medium term (2-4 years) |

| Integration of Smart Sensors and NFC Tags in Cartons | +0.5% | Europe and North America, pilot deployments in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth of Chronic Diseases Requiring Unit-Dose Treatments

The folding carton in healthcare market is seeing steady support from the rise in chronic diseases that require repeat dosing and tighter adherence controls. Unit-dose blister packs and calendar cartons are increasingly used for therapies in diabetes, cardiovascular care, and oncology because these formats make dosing schedules easier to follow and verify at dispensing points. Drug makers are therefore specifying carton structures that can hold 28-day and 90-day blister formats without losing crease strength after repeated opening and closing cycles. Lonza expanded capsule manufacturing capacity at its Rewari facility in India and its Suzhou facility in China, with both sites active in late 2024 and additional lines commissioned in Q3 2025, supporting the wider move toward unit-dose formats in Asia-Pacific. India’s pharmaceutical market was projected to rise from USD 61.36 billion in 2024 to USD 130 billion by 2033, while China’s market was projected to increase from USD 80.4 billion in 2024 to USD 126.6 billion by 2030, reinforcing long-term demand for folding cartons in the healthcare market. This demand is making volume growth in the folding carton market in healthcare less dependent on pricing cycles and more tied to treatment patterns and adherence-focused packaging design.

Serialization Mandates Driving Larger Carton Real Estate

The folding carton in healthcare market is also being pushed by serialization rules that require more carton space and better print accuracy. The European Union Falsified Medicines Directive has required a unique 2D DataMatrix code on prescription drug packs since 2019, while the U.S. Drug Supply Chain Security Act requires product identifiers, serial numbers, lot numbers, and expiration dates in machine-readable form. Commission Delegated Regulation 2016/161 specified a minimum 8-millimeter-by-8-millimeter DataMatrix area with a 1-millimeter quiet zone on all sides, which can consume 12% to 15% of usable carton surface on compact packs for single-dose vials and pre-filled syringes. As a result, converters in the folding carton market for healthcare are seeing increased demand for premium boards that can withstand sharp codes, prevent ink bleed, and remain flat during inspection and scanning. Amcor launched recycle-ready films at its Italian facility in March 2026 with serialization-compatible coatings that reduced a failure point linked to ink smudging during high-speed verification. The European Medicines Verification System now processes more than 40 million verification events each day, which keeps pressure on the folding carton in healthcare market to maintain tighter print tolerances and more reliable substrate performance.

Rising Demand for Child-Resistant Pharmaceutical Packaging

The folding carton market in healthcare is benefiting from tighter rules on child-resistant packaging across major drug markets. The U.S. Consumer Product Safety Commission requires that 85% of children under age 5 should not be able to open a package within 5 minutes, while 90% of adults aged 50 to 70 should be able to open and properly use it. Those dual requirements are pushing carton designers to incorporate push-through blister cards, peel-back seals, slide-lock features, and internal supports that prevent accidental puncture during shipping. ASTM D3475 also establishes classification standards for child-resistant packages, and these performance requirements favor stiffer substrates, such as solid bleached board, over white-lined chipboard in many healthcare applications. Nutraceutical brands are moving in the same direction after the FDA issued 27 warning letters in 2024 for unauthorized disease claims, which increased scrutiny around packaging safety and compliant presentation. This overlap between regulation and liability controls is helping child-resistant formats retain above-market momentum in the folding carton market for healthcare.

Shift Toward Sustainable and Recyclable Paperboard

The folding carton in healthcare market is also being reshaped by sustainability targets that now affect board grades, coatings, and supplier selection. The European Union’s Packaging and Packaging Waste Regulation set recycled-content targets of 25% for paperboard by 2030 and 50% by 2040, while also limiting structures that combine paperboard with polyethylene or polypropylene films in ways that hinder recycling. Metsä Board stated that fresh-fiber folding boxboard made from Nordic spruce can deliver 50% to 60% lower carbon emissions than coated unbleached kraftboard from mixed hardwood pulps, partly because longer fibers allow 15% to 20% lower basis weight without losing puncture resistance.[1]Metsä Board, “Life Cycle Assessment of Folding Boxboard Products,” Metsä Board, metsaboard.com Drug manufacturers are therefore requesting optical-brightener-agent-free grades that can move through municipal recycling streams and support carbon-accounting claims under ISO 14067. Stora Enso completed a 750,000-ton-per-annum consumer-board line at Oulu in 2025 and started first deliveries in Q2 2025, showing the scale of capacity investment needed to serve the folding carton in healthcare market with pharmaceutical-grade sustainable board. Water-based barrier coatings are moving forward as well, but moisture-sensitive biologics still limit how quickly the folding carton in healthcare market can replace older barrier systems in cold-chain distribution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Paperboard Prices | -0.8% | Global, with an acute impact in Europe and North America | Short term (≤ 2 years) |

| Competition from Flexible Packaging Alternatives | -0.6% | North America and Asia-Pacific, moderate in Europe | Medium term (2-4 years) |

| Carton Delamination With High-Moisture Biologic Drugs | -0.3% | Global, concentrated in tropical and subtropical regions | Medium term (2-4 years) |

| Supply-Chain Disruptions in Pharmaceutical-Grade Inks | -0.4% | Global, with regional bottlenecks in specialty pigments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in Paperboard Prices

The folding carton in healthcare market faces a clear restraint from unstable pulp and paperboard costs. Northern bleached softwood kraft pulp prices ranged from USD 1,050 to USD 1,350 per metric ton during 2024 and 2025, while energy swings in Scandinavian mills kept production costs under pressure. Solid bleached board and folding boxboard prices usually lag by 60 to 90 days, leaving converters exposed when they have fixed-price supply contracts with pharmaceutical customers. In the folding carton market for healthcare, that lag can compress margins at exactly the point when compliance, print quality, and certification costs are already high. Smaller regional converters are more exposed because they lack backward integration into pulp, and several European specialists lowered utilization to 70%-75% in H2 2025 as pulp prices rose above USD 1,300 per metric ton. Pharmaceutical buyers are responding by adopting dual sourcing and pulp-linked price clauses, which improve supply security but make folding cartons in the healthcare market more price-competitive and less favorable to smaller independent suppliers.

Competition from Flexible Packaging Alternatives

The folding carton in healthcare market is also facing competition from flexible packaging in applications where lower weight and shipping efficiency matter more than rigid structure. Stand-up pouches, stick packs, and sachets can reduce material weight by 60% to 80% compared with rigid paperboard formats, making them attractive for some nutraceutical and dietary supplement applications. The CDC reported that 57.6% of U.S. adults used dietary supplements in 2017-2018, and usage reached 74.3% among adults aged 60 and older, which helps explain why convenience-led packaging choices are gaining traction. Flexible-packaging suppliers are also developing recyclable mono-material polyethylene structures that align with the design-for-recycling direction of European policy, narrowing one of paperboard’s earlier advantages. Even so, child resistance, tamper evidence, and premium presentation still favor cartons in many regulated healthcare settings, so the folding carton in healthcare market remains stronger in higher-value pharmaceutical uses than in convenience-led supplement formats. This restraint is therefore forcing the folding carton in healthcare market to defend share through lighter board structures, hybrid formats, and clearer compliance-led differentiation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Solid Bleached Board Dominates, Folding Boxboard Gains

Solid bleached sulfate accounted for 43.28% share of the folding carton in healthcare market size in 2025, reflecting its strong opacity, high brightness, and reliable print performance on high-speed offset presses. Folding boxboard is projected to grow at a 7.06% CAGR through 2031, making it the fastest-growing material segment in the folding carton market for healthcare. Fresh-fiber grades are gaining ground because life-cycle assessments from Metsä Board showed carbon emissions 50% to 60% lower than those of coated unbleached kraftboard, while longer fibers also supported 15% to 20% basis-weight reductions without sacrificing puncture resistance. Coated unbleached kraftboard continues to serve outer shipping and secondary pack formats where structural strength matters more than premium printability. White-lined chipboard remains limited to more cost-sensitive nutraceutical applications where recycled content supports sustainability messaging and print requirements are less demanding.

In the healthcare industry, folding carton buyers are increasingly favoring boards that meet both compliance printing requirements and recyclability expectations. Stora Enso’s Oulu line, with first deliveries in Q2 2025, shows how suppliers are expanding pharmaceutical-grade consumer board capacity to meet this demand. The European Union’s Packaging and Packaging Waste Regulation is also pushing converters away from laminated paperboard structures that use polyethylene or polypropylene layers that reduce recyclability.[2]European Parliament, “Packaging and Packaging Waste Regulation (PPWR),” European Parliament, europarl.europa.eu Water-based barriers are becoming more relevant, but moisture-sensitive biologics still create a performance gap that supports continued use of traditional wax-coated or otherwise more protective grades in some cold-chain uses. That balance means the folding carton in healthcare market is moving toward cleaner and lighter substrates, but not at the expense of drug stability or distribution safety.

By Printing Technology: Offset Lithography Anchors, Digital Printing Surges

Lithography retained 48.37% of printing-technology revenue in 2025, which kept it as the leading print format in the folding carton in healthcare market because it delivers consistent color and reliable high-volume output. Digital printing is expected to expand at 6.78% CAGR through 2031, and that pace makes it the fastest-growing printing segment in the folding carton in healthcare market. Pharmaceutical companies are increasingly using digital systems for batch codes, expiry dates, and electronic leaflet QR codes on runs as short as 5,000 cartons, where plate costs make offset printing less attractive. Flexography continues to serve lower-cost nutraceutical applications, while gravure remains limited to ultra-high-volume runs, rare outside selected over-the-counter products and vitamin lines. The rising need for variable data is therefore widening the role of digital equipment even as offset remains the anchor for large pharmaceutical production runs.

Digital workflows are also becoming more important because serialization demands require consistent scanning and tighter control over data changes from batch to batch. The European Union’s serialization rules are keeping print resolution and code clarity at the center of converter investment decisions. Amcor’s March 2026 launch of serialization-compatible coatings in Italy addressed ink-smudge issues that had caused 3% to 5% rejection rates in earlier production runs, showing how print performance is now tied closely to substrate engineering. Schreiner Group is also advancing smart-packaging labels that combine NFC and RFID functions for authentication and warehouse tracking, which adds another layer of value to digital print workflows. As a result, the folding carton in healthcare market is treating printing technology less as a standalone process choice and more as part of a wider compliance, traceability, and patient-information system.

By Application: Pharmaceutical Manufacturers Lead, Nutraceuticals Accelerate

Pharmaceutical manufacturers held 53.32% of the folding carton in healthcare market share in 2025, making them the largest end-user group because prescription drugs, injectables, and biologics require child-resistant and tamper-evident secondary packs. Nutraceutical and dietary supplement firms are projected to grow at a 7.43% CAGR through 2031, the fastest pace among end-user groups in the folding carton in healthcare market. The FDA’s 27 warning letters issued in 2024 for unauthorized disease claims are reinforcing the move toward more compliant and more formal packaging among supplement brands. Medical device companies use folding cartons with integrated Tyvek peel-able lids to maintain sterile barriers during transport, although thermoformed trays still limit carton use in higher-value implant categories. Veterinary healthcare providers are also increasing demand for child-resistant cartons as regulatory harmonization progresses under European Medicines Agency guidelines for veterinary medicinal products.

Within the folding carton in healthcare industry, the pharmaceutical customer base is becoming more selective about supplier quality systems and batch handling capabilities. Personalized medicine and biologic therapies are increasing the need for smaller runs with variable data, which favors converters that combine regulatory discipline with digital printing. The top 10 global drug companies now source 60% to 70% of their folding-carton volumes from fewer than 5 converter partners, which raises the qualification bar for regional producers. That shift is making certification, print consistency, and audit readiness more important than simple price competition in the folding carton in healthcare market. Nutraceutical firms remain more fragmented and more cost sensitive, so premium pharmaceutical-grade cartons can still command 20% to 30% price premiums even when the underlying substrates are similar.

Geography Analysis

North America held 34.63% of the folding carton in healthcare market share in 2025, while Asia-Pacific is projected to record the fastest regional CAGR at 6.57% through 2031. North America’s position reflects the scale of U.S. pharmaceutical packaging demand and the continued use of bottle-and-carton systems across oral solid dosage categories. The region also remains central to the folding carton in healthcare market because child-resistant standards, serialization compliance, and premium print requirements are tightly enforced in mainstream drug distribution. Asia-Pacific is growing faster because pharmaceutical manufacturing is expanding, local capacity is increasing, and unit-dose formats are becoming more common in large population centers. India’s pharmaceutical market was projected to rise from USD 61.36 billion in 2024 to USD 130 billion by 2033, while China’s market was projected to increase from USD 80.4 billion in 2024 to USD 126.6 billion by 2030.

Lonza’s capacity additions at Rewari, India, and Suzhou, China, show how multinational suppliers are aligning production with the regional shift toward unit-dose packaging and better adherence formats.[3]Lonza Group, “Capsule Manufacturing Capacity Expansions - India and China,” Lonza Group Investor Presentation, lonza.com That matters for the folding carton in healthcare market because secondary packaging demand usually follows dosage-form output and localization of drug manufacturing. Europe remains a critical region even without the top revenue share because it combines strict serialization requirements with strong pressure for recyclable board structures and lower-impact packaging systems. The Falsified Medicines Directive and the Packaging and Packaging Waste Regulation are forcing pharmaceutical buyers in Europe to rethink board selection, print layout, and barrier design at the same time. This combination makes Europe one of the most regulation-shaped parts of the folding carton in healthcare market, especially for suppliers that want to sell premium sustainable substrates.

South America and the Middle East and Africa are expanding more slowly because local folding-carton capacity is limited and healthcare regulations remain more fragmented across countries. Imports from Europe and North America can add 15% to 25% to landed costs in these regions, which affects the competitiveness of locally supplied cartons versus other packaging options. India’s active pharmaceutical ingredient sector, valued at USD 13.5 billion in 2024 and growing at 7% CAGR since 2017, is reducing dependence on Chinese imports and opening room for domestic carton suppliers to move closer to pharmaceutical production hubs. The United States’ reshoring push, with an estimated USD 270 billion investment pool and India expected to capture 25% to 30% of that allocation, also supports packaging localization in Asia-Pacific. As those shifts continue, the folding carton in healthcare market is likely to become more regionally balanced in production, even if demand remains concentrated in North America, Europe, and the fastest-growing Asian pharmaceutical centers.

Competitive Landscape

The folding carton in healthcare market shows moderate concentration, with the top 5 global converters, Graphic Packaging, Smurfit WestRock, International Paper Company, and Mondi, holding a combined 35% to 40% of revenue. That leaves most of the folding carton in healthcare market spread across regional converters and some in-house packaging operations run by large pharmaceutical manufacturers. Scale matters, but the market is not consolidated enough for a few suppliers to control pricing or qualification standards on their own. Competition is therefore centered on pulp access, pharmaceutical certifications, print capability, and the ability to support regulated short runs as reliably as large commercial orders.

Integrated players are using upstream fiber access to protect margins and secure supply. Smurfit WestRock completed its acquisition of Ecuadorian containerboard assets in March 2026, giving it access to 500,000 tons of annual pulp capacity and strengthening backward integration amid raw-material volatility.[4]Smurfit WestRock plc, “Ecuador Acquisition and Merger Completion,” Smurfit WestRock plc Investor Relations, smurfitkappa.com Stora Enso’s Oulu expansion also strengthened the supply base for pharmaceutical-grade board and positioned the company to serve demand for optical-brightener-agent-free substrates. Pure-play converters such as Edelmann and AR Packaging compete differently, relying on ISO 15378 pharmaceutical-packaging certification and validated quality systems that help them win regulated work where clean-room discipline matters. This is why the folding carton in healthcare market rewards both scale and specialization, rather than favoring one model alone.

Technology is becoming another point of separation in the folding carton in healthcare market. Early adopters are combining digital printing with inline smart-label or NFC integration to meet demand for serialization-compliant variable-data runs and added authentication features. Sonoco announced a USD 30 million investment in adhesives and sealants capacity in July 2025, which supported higher-value closures and moisture-barrier features for healthcare packaging. Sonoco also divested its ThermoSafe temperature-controlled-packaging business for USD 1.2 billion in November 2025, reflecting a broader move toward portfolio focus and capital concentration on pharmaceutical-grade packaging assets. Opportunity areas remain strongest in veterinary medicine cartons and medical-device packs with sterile-barrier features, which means the folding carton in healthcare market still has room for specialists that can move quickly in tightly defined compliance-driven niches.

Folding Carton In Healthcare Industry Leaders

Smurfit WestRock plc

Graphic Packaging International LLC

Mayr-Melnhof Karton AG

International Paper Company

Mondi plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Amcor launched recycle-ready films at its Italian facility, incorporating serialization-compatible coatings that prevent ink smudging during high-speed verification and addressing quality-control failure modes that had caused 3% to 5% rejection rates in earlier flexographic production runs.

- March 2026: Smurfit WestRock completed the acquisition of Ecuadorian containerboard assets, securing access to 500,000 tons of annual pulp capacity and enabling backward integration that insulates folding-carton margins from spot-market volatility in northern bleached softwood kraft pulp prices.

- February 2026: Mayr-Melnhof announced that its Pharma and Healthcare Packaging division achieved a 25% profit increase in 2025, attributing the gain to its Fit-For-Future restructuring program that consolidated production into fewer, more automated facilities capable of running sleeve-carton formats at speeds exceeding 400 units per minute.

- November 2025: Sonoco divested its ThermoSafe temperature-controlled-packaging business for USD 1.2 billion, redirecting capital toward pharmaceutical-grade folding-carton capacity and value-added features such as tamper-evident closures and moisture-barrier coatings that command 15% to 25% price premiums.

Global Folding Carton In Healthcare Market Report Scope

The scope of this report focuses on the folding carton market within the healthcare sector. Folding cartons are paperboard-based packaging solutions that are pre-glued and folded flat for transportation and storage, then assembled into their final shape during use. These cartons are widely utilized in the healthcare industry for packaging pharmaceuticals, medical devices, and other healthcare-related products due to their lightweight, customizable, and eco-friendly nature.

The Folding Carton in Healthcare Market Report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and Other Material Types), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, Gravure Printing, and Other Printing Technologies), Application (Pharmaceutical Manufacturers, Medical Device Companies, Nutraceutical and Dietary Supplement Firms, Veterinary Healthcare Providers, and Other Applications), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solid Bleached Sulfate |

| Folding Boxboard |

| Coated Unbleached Kraft |

| White Line Chipboard |

| Other Material Types |

| Lithographic Printing |

| Flexographic Printing |

| Digital Printing |

| Gravure Printing |

| Other Printing Technologies |

| Pharmaceutical Manufacturers |

| Medical Device Companies |

| Nutraceutical and Dietary Supplement Firms |

| Veterinary Healthcare Providers |

| Other Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Material Type | Solid Bleached Sulfate | ||

| Folding Boxboard | |||

| Coated Unbleached Kraft | |||

| White Line Chipboard | |||

| Other Material Types | |||

| By Printing Technology | Lithographic Printing | ||

| Flexographic Printing | |||

| Digital Printing | |||

| Gravure Printing | |||

| Other Printing Technologies | |||

| By Application | Pharmaceutical Manufacturers | ||

| Medical Device Companies | |||

| Nutraceutical and Dietary Supplement Firms | |||

| Veterinary Healthcare Providers | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast size of the folding carton in healthcare market?

The folding carton in healthcare market was valued at USD 6.85 billion in 2026 and is projected to reach USD 9.12 billion by 2031 at a 5.89% CAGR.

Which region leads demand for folding cartons used in healthcare packaging?

North America led with 34.63% of revenue in 2025, supported by strong pharmaceutical packaging demand and strict compliance requirements.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is expected to post the fastest growth at 6.57% CAGR, driven by pharmaceutical expansion in India and China.

Which end-user group drives the largest share of demand?

Pharmaceutical manufacturers led with 53.32% share in 2025 because prescription drugs, injectables, and biologics require regulated secondary packaging.

What material is most used in healthcare folding cartons?

Solid bleached board held the largest material share at 43.28% in 2025 because it offers strong opacity, brightness, and print performance.

Which printing and packaging formats are gaining the most momentum?

Digital printing is the fastest-growing printing method at 6.78% CAGR, while sleeve cartons are the fastest-growing packaging format at 6.54% CAGR through 2031.

Page last updated on: