Medical Packaging Films Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.52 Billion |

| Market Size (2031) | USD 10.75 Billion |

| Growth Rate (2026 - 2031) | 4.76% CAGR |

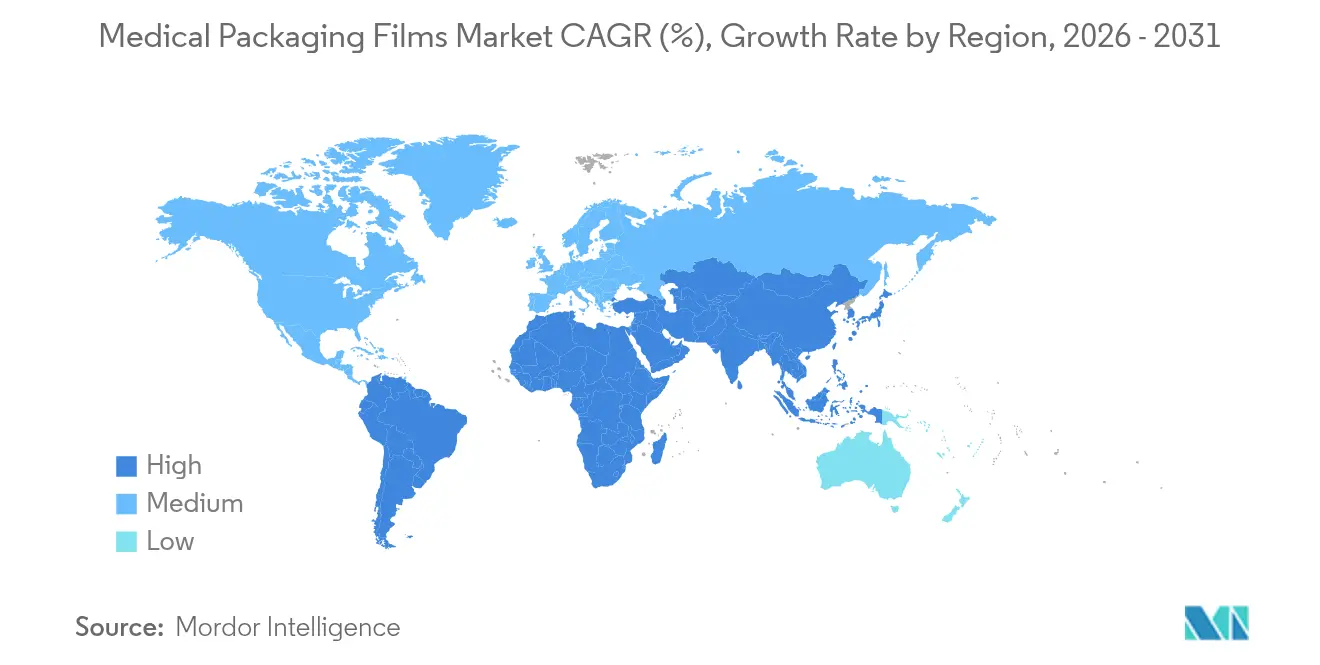

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Packaging Films Market Analysis by Mordor Intelligence

The medical packaging films market size is expected to grow from USD 8.13 billion in 2025 to USD 8.52 billion in 2026 and is forecast to reach USD 10.75 billion by 2031 at 4.76% CAGR over 2026-2031. Robust demand stems from serialization mandates, rapid biologics uptake, and aggressive sustainability targets that favor next-generation high-barrier and recyclable substrates. Manufacturers are shifting from single-function barriers to multi-layer structures that embed digital identifiers, time-temperature indicators, and post-consumer recycled content, thereby elevating both compliance and brand protection. Strategic consolidation, most notably Amcor’s USD 8.4 billion combination with Berry Global, is redefining scale advantages, while regional production shifts toward Asia-Pacific bring supply proximity and cost leverage. Volatile petroleum feedstock, however, still exerts pricing pressure, encouraging deeper vertical integration and diversified resin sourcing strategies.

Key Report Takeaways

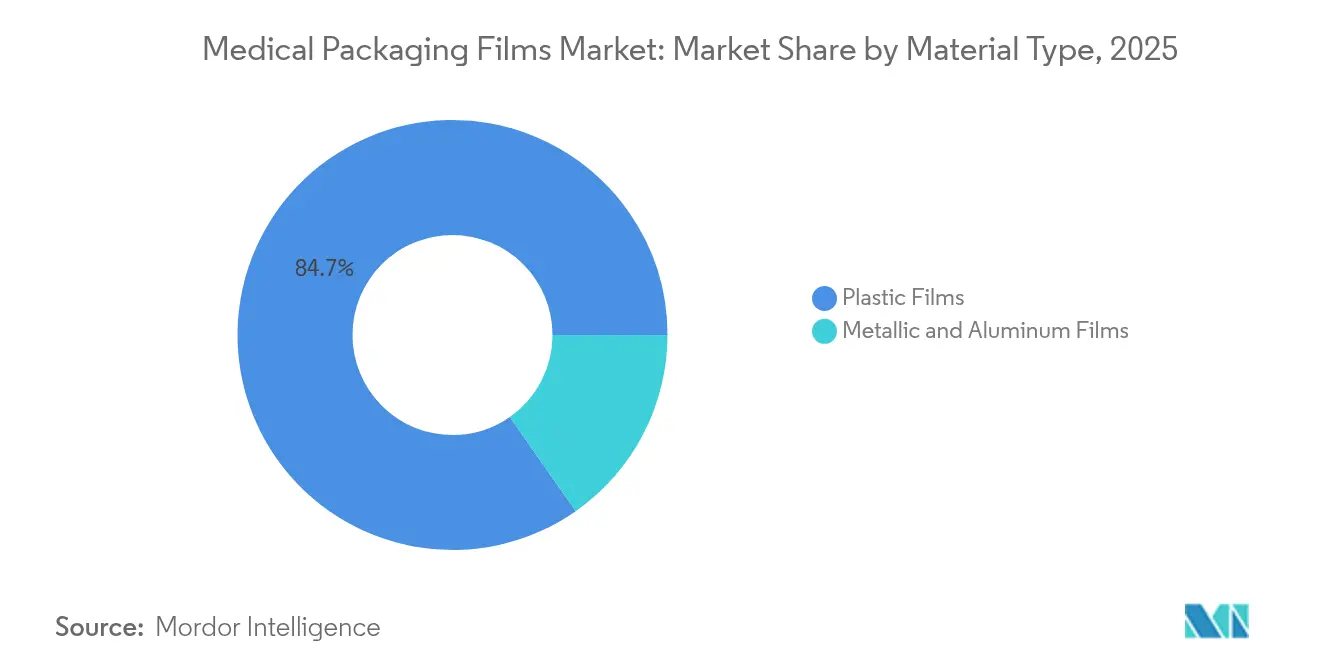

- By material type, plastic films led with 84.72% revenue share in 2025; bioplastics inside this cohort are growing the fastest at 7.12% CAGR through 2031.

- By product type, high-barrier films are expanding at 8.33% CAGR, while co-extruded and laminated films held 43.05% of the medical packaging films market share in 2025.

- By application, bags and pouches accounted for 43.29% of the medical packaging films market size in 2025; blister packs register the highest growth at 7.28% CAGR to 2031.

- By end-user, cast film extrusion commanded 35.08% share in 2025; blown film extrusion is set to expand at 6.86% CAGR from 2026 t0 2031.

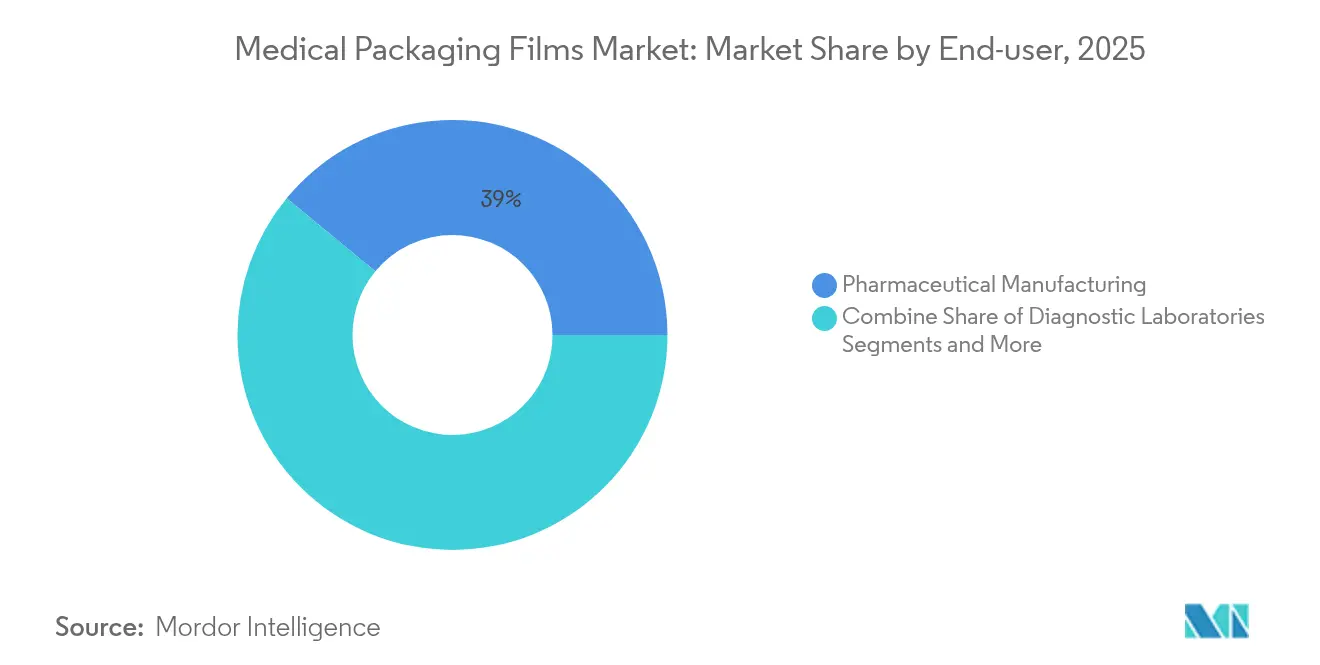

- By technology, pharmaceutical manufacturing held 39.02% share in 2025; home-healthcare kit assemblers represent the quickest riser at 6.86% CAGR.

- By geography, Asia-Pacific commanded 38.21% revenue share in 2025 and is projected to post a 6.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Packaging Films Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic diseases | +1.2% | North America, Europe, Global spread | Long term (≥ 4 years) |

| Sustainability push for bioplastics & recyclables | +0.8% | EU, North America, APAC | Medium term (2-4 years) |

| Pharmaceutical manufacturing expansion in APAC | +1.5% | Asia-Pacific, spill-over to MEA | Medium term (2-4 years) |

| Surge in home-based care & POC diagnostic kits | +0.9% | Early adoption in developed markets | Short term (≤ 2 years) |

| Digital serialization & smart anti-counterfeit films | +0.7% | Global compliance-driven | Short term (≤ 2 years) |

| Growth of 3D-printed personalized drug devices | +0.3% | North America, EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases

Growing noncommunicable disease incidence is transforming packaging from passive containment into active adherence tools. Calendar blister designs lowered HbA1c by 0.95% versus standard packs in diabetes trials, underscoring packaging’s clinical value. Aging demographics intensify polypharmacy, pushing drug makers to adopt unit-dose formats that synchronize with e-health platforms and smart pill reminders. Regulators now treat labeling and package configuration as integral to safe use, as reflected in successive FDA guidance updates.[1]U.S. Food and Drug Administration, “Guidance on Medical Device Patient Labeling,” fda.gov Consequently, film suppliers capable of certifying patient-centric designs secure long-term demand across the medical packaging films market.

Sustainability Push for Bioplastics and Recyclables

EU directives mandating minimum recycled content are accelerating biopolymer uptake. Avient’s Mevopur bio-based series cuts carbon footprints by 25% while maintaining ISO 10993 compliance. Amcor’s SureForm Pro ICE reduced overall plastic by 40% yet met drop-in recyclability thresholds across existing hospital streams. The challenge is sterilization resilience: autoclave and gamma cycles can degrade compostable resins, prompting alloyed formulations of PLA, PHA, and EVOH that preserve barrier integrity. Procurement teams in US health systems now assign environmental weighting in tenders, giving early movers in sustainable substrates a pricing premium within the medical packaging films market.

Pharmaceutical Manufacturing Expansion in Asia-Pacific

New GMP-compliant capacity in India, China, and the Philippines reconfigures global supply corridors. Zen Industrial Pharma Ecozone’s sterile injectables plant signals a strategic pivot that localizes packaging spend near fill-finish activity.[2]Philippine News Agency, “PEZA to host PH's first US-FDA certified pharma manufacturer,” pna.gov.phAmcor’s acquisition of Phoenix Flexibles in Gujarat embeds extrusion assets inside the pharmaceutical heartland, shrinking lead times and import dependencies. Harmonized PIC/S standards across ASEAN remove technical barriers, letting regional blister and pouch formats circulate freely. These dynamics lift the medical packaging films market’s center of gravity toward Asia-Pacific.

Surge in Home-Based Care and POC Diagnostic Kits

Remote-care protocols normalize self-administration and home testing, forcing packaging to balance sterility with intuitive opening features. FDA guidance on home-use devices highlights readability, tamper evidence, and waste disposal as critical design pillars. Dosepak fold-out cartons integrate calendar trays and NFC tags that prompt refills through mobile apps.[3]WestRock, “Dosepak Medication Adherence Packaging,” westrock.com Temperature-sensitive COVID-19 antigen kits adopt multi-layer film pouches embedding Evidencia’s one-degree-accuracy strip to safeguard efficacy across distribution. These innovations expand unit-dose and small-volume demand, sustaining rapid growth for the medical packaging films market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile petroleum-based polymer prices | -0.6% | Global, cost-sensitive regions | Short term (≤ 2 years) |

| High regulatory validation costs | -0.4% | Global, varying by region | Medium term (2-4 years) |

| Competition from paper-based sterile packs | -0.2% | Cost-sensitive applications | Medium term (2-4 years) |

| Weak recycling infrastructure for multilayer films | -0.3% | EU & North America regulatory hotspots | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Petroleum-Based Polymer Prices

Resin costs climbed 3-5 cents per pound in 2024 amid energy spikes, compressing margins for converters locked into medical-grade supply contracts. Smaller firms, lacking hedging leverage, face pass-through lags of up to six months, risking account attrition or line shutdowns. Strict change-control rules in healthcare impede rapid resin substitution, amplifying exposure versus general packaging segments. Larger players respond by forward-buying and co-locating extrusion near cracker complexes, yet this capital intensity widens the competitive gap in the medical packaging films market.

High Regulatory Validation Costs

ISO 13485 alignment and DSCSA serialization upgrades extend development cycles by 12-18 months and add USD 100,000-500,000 per new material for cytotoxicity and stability testing.[4]U.S. Food and Drug Administration, “Over-the-Counter Monograph Condition B001,” federalregister.gov Biologics blister solutions must also confirm extractables under drug-product contact conditions, doubling lab workloads. Small innovators often co-license resins through tolling deals with multinationals to defray expense, encouraging consolidation. As 2026 QMS rules take effect, access to in-house microbiology and accelerated-aging chambers becomes a decisive asset across the medical packaging films market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Plastic Films Dominate as Bioplastics Accelerate

Plastic films retained 84.72% share in 2025, and their internal shift toward bio-derivatives is propelling a 7.12% CAGR. Polyethylene grades, valued for sealability and gamma stability, underpin high-volume pharma pouches. EVOH-lined co-extrusions meet oxygen barrier thresholds for biologic vials shipped on dry ice. Within this mix, PLA/PHA blends are capturing pilot-scale orders from hospitals that target a 40% waste-footprint reduction. Metallic foils hold isolated niches where sub-0.05 cc/m²/day OTR is non-negotiable, such as transdermal patch liners. Additionallyy, medical packaging films industry participants invest in compatibilizer chemistries so multilayer off-cuts enter mechanical recycling without delaminating.

Further gains hinge on validating hot-water disintegration paths for hospital sterilants and aligning with EN 13432 compostability standards. Suppliers promoting cradle-to-cradle certifications gain procurement preference, though they must still pass 121 °C steam sterilization and 60 kGy e-beam cycles without tensile loss. Consequently, the next wave of the medical packaging films market will likely derive from hybrid structures that fuse conventional resins with bio-derived tie layers, balancing processability with end-of-life compliance.

By Product Type: High-Barrier Films Command Premium Growth

High-barrier films, currently 24.55% of revenue, will expand at 8.33% CAGR through 2031, outpacing the broader medical packaging films market. Demand tracks the proliferation of monoclonal antibodies that mandate oxygen transmission rates below 0.1 cc/m²/day. TekniPlex’s cleanroom-produced, seven-layer blown structures integrate EVOH and cyclic olefin polymers, extending cold-chain stability from 72 hours to 120 hours. Co-extruded and laminated films remain the volume backbone, controlling 43.05% share in 2025 thanks to format versatility that spans IV bags to diagnostic pouching. Nevertheless, price premiums for vapor-barrier upgrades yield outsized profitability, encouraging incumbents to retrofit lines with bubble-cage systems for ultra-thin EVOH placement.

Co-extruders also embed NFC circuits and thermochromic inks, merging a physical barrier with digital authentication. Looking forward, hydrogen-peroxide-resistant coatings will be essential as aseptic fill-finish lines pivot from steam to vaporized-plasma sterilants.

By Application: Blister Packs Lead Unit-Dose Revolution

Bags and pouches remained the single largest application at 43.29% of 2025 revenue, favored in IV solutions and wound-dressing kits. Yet blister packs are scaling faster, with 7.28% CAGR tied to chronic therapy regimens and tighter adherence protocols. Unit-dose compliance aligns with DSCSA lot-level traceability, so blister webs now carry serialized DataMatrix codes printable inline at 300 dpi. Diabetic antihyperglycemics migrate en masse to calendar blisters, supported by child-resistant push-through lidding.

Form-fill-seal sachets also grow on the back of rapid antigen and flu self-tests. Here, ultra-low-gauge laminated films cut basis weight by 18% while keeping MVTR under 0.3 g/m²/day. This portfolio breadth ensures the medical packaging films industry caters to both high-volume commodity and premium smart-pack use cases.

By End-User: Home Healthcare Assemblers Spur Design Shift

Pharmaceutical manufacturers occupied 39.02% of revenue in 2025 through entrenched purchase contracts and line-speed requirements exceeding 300 packs/min. However, home-healthcare kit providers post a 6.86% CAGR as payer models reimburse remote monitoring over inpatient stays. Kits for subcutaneous biologic autoinjectors demand tamper-evident, pictogram-rich pouches that seniors can open without scissors. Device OEMs, accounting for 18.32% share, require breathable Tyvek-film composites that pass EO sterilization yet block fiber shedding. Diagnostic labs rely on high-clarity PETG thermoforms for automated plate loading, a stable growth pocket at 4.22% CAGR.

Strategic interplay arises as pharma licensees bundle drug-device-delivery ecosystems, pressing converters to supply mixed portfolios spanning pre-fillable syringe lamination and autoinjector tray lidding. This complexity cements long-term multi-year sourcing arrangements across the medical packaging films market.

By Technology: Extrusion Platforms Embrace Circularity

Cast film extrusion commanded 35.08% of the medical packaging films market share in 2025, reflecting strong adoption for clear, peel-open pouches and lidding where gauge control and optical clarity matter. Hospitals favor the process because its flat-die geometry enables uniform thickness that supports high-speed form-fill-seal lines, while converters value the lower scrap rates that help offset resin volatility. Investments in inline digital printing now allow serialized codes to be applied during casting without secondary passes, enhancing compliance at minimal added cost. Energy-optimized chill-roll systems have trimmed power consumption by up to 12%, aligning with hospital group purchasing mandates for lower carbon products. These process upgrades reinforce cast film’s leadership yet still leave room for blended PCR content trials aimed at meeting 30% recycled-content targets by 2028.

Blown film extrusion is set to expand at a 6.66% CAGR from 2026 to 2031, making it the fastest-growing technology slice of the medical packaging films market size over the forecast window. The bubble process excels at multilayer structures that integrate EVOH or cyclic olefin barriers, which are essential for biologics shipped on dry ice. Recent double-bubble orientation lines have lifted puncture strength 15% while reducing basis weight 10%, a gain that satisfies both cold-chain integrity and sustainability criteria. Producers are pairing blown lines with near-infrared-detectable masterbatches so mono-material laminates sort cleanly into recycling streams. Real-time thickness monitoring driven by machine-learning algorithms holds variation within ±1 µm, cutting off-spec waste to under 1.5% and boosting overall equipment effectiveness. These advantages position blown film extrusion as the prime platform for future-ready smart and recyclable healthcare packaging solutions.

Geography Analysis

Asia-Pacific dominates the medical packaging films market with 38.21% revenue share in 2025 and the highest 6.11% CAGR to 2031. China’s biologics build-out and India’s generics push intensify demand for high-barrier lidding and thermoform webs. Government incentives such as India’s Production Linked Incentive scheme reimburse up to 5% of capital outlays on pharma-adjacent packaging plants, tilting fresh capacity toward Gujarat and Telangana. The Philippines’ FDA-certified ecozone illustrates a regional blueprint where co-located film converters slash logistics costs and expedite validation cycles. Japan sustains premium demand for ultra-cleanroom extrusion, while South Korea’s CDMO boom adds steady orders for serialized pouch laminate.

North America remains pivotal as DSCSA enforcement pushes universal serialization by November 2024. The region’s biologics weightings lift cold-chain pouch uptake, especially post-Amcor-Berry consolidation that clusters 11 extrusion sites across the US-Mexico border. Hospitals accelerating “sustainable purchasing” prefer PCR-infused PE/PP mono-materials, shaping converter R&D priorities. Canada’s national pharmacare plan, slated for 2027, is projected to widen access to chronic therapies, indirectly escalating blister demand and reinforcing the medical packaging films market trajectory.

Europe, although mature, enforces the world’s strictest eco-design statutes. Germany anchors high-value orders for PVdC-free barrier films, as regulators scrutinize chlorine-based substrates. France’s 2025 Extended Producer Responsibility amendment imposes escalating fees on unrecyclable formats, prompting a pivot to mono-material EVOH-PE. The UK’s post-Brexit MHRA serialization divergence necessitates dual coding on packs servicing both EU and UK channels, complicating line configurations. Southern Europe enjoys near-shore outsourcing from Northern pharma giants; Spanish blistering plants recorded 5.4% shipment gains in 2025.

Latin America shows nascent but fast-rising requirements as Brazil’s ANVISA finalizes RDC 680 for full aggregation by 2026. Multinational CDMOs invest in Mexico to service US demand under USMCA, blending cost savings with near-shoring resilience. The Gulf Cooperation Council is modernizing biologics fill-finish halls under Vision 2030, adding incremental high-barrier film imports until regional extrusion capacity scales. Collectively, these developments cement geography as a determinant of specification nuance across the medical packaging films market.

Competitive Landscape

The medical packaging films market is fragmented. The Amcor-Berry merger yields a portfolio exceeding USD 18 billion in combined sales, with anticipated synergies of USD 650 million by 2028. DuPont’s USD 313 million purchase of Donatelle bolsters access to precision molding, letting it bundle film, device, and tray into turnkey kits. TekniPlex doubled barrier-film capacity via its new Wisconsin site, featuring air-knife coating that achieves 0.05 cc/m²/day OTR at 80 micron thickness. SICPA leverages ink heritage to deploy modular L1-L3 serialization software, embedding covert markers into flexographic stations.

Strategic thrusts revolve around sustainability and smart functionality. Amcor pilots near-infrared sortable polyolefin laminates that mimic aluminum foil opacities yet remain mono-material. Avient commercializes color-stable, bio-based masterbatches that pass cytotoxicity and gamma sterilization. West Pharmaceutical Services reports 2.1% organic growth on the back of self-injection device popularity, pulling through multilayer pouch demand. White-space entrants from printed-electronics backgrounds unveil humidity-triggered RFID tags laminated between film layers, offering end-to-end cold-chain traceability for under USD 0.04 per dose.

Price competition remains measured because lengthy validation discourages frequent supplier switching. Nonetheless, resin volatility spurs dual-sourcing, so converters with global footprints and redundant ISO 13485 plants win RFQs. Patent races now target PVdC-free oxygen barriers and solvent-less bonding, expanding intellectual-property moats. As device-drug convergence deepens, platform contracts bundle film, tray, and sensor, favoring groups with multi-disciplinary engineering. Consequently, technological breadth, regulatory fluency, and lifecycle sustainability credentials define competitive edge in the medical packaging films market.

Medical Packaging Films Industry Leaders

Honeywell International Inc.

3M Company

Wipak Oy

Amcor Plc

DuPont de Nemours, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Avient launched Mevopur bio-based polymer masterbatches with 70–100% renewable content for medical film and blister applications and expanded healthcare TPU capacity in Asia.

- January 2025: PCI Pharma Services committed more than USD 365 million to enlarge drug-device combination packaging lines in Illinois and Ireland, adding high-barrier film pouching and cold-form blister capability.

- July 2024: DuPont acquired Donatelle Plastics for USD 313 million, gaining medical-grade injection molding and thermoforming expertise that complements its Tyvek sterile-packaging film portfolio.

- July 2024: Catalent finished a USD 25 million expansion of its Schorndorf, Germany site, installing new temperature-controlled film-pack lines for clinical supply of biologics.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the medical packaging films market as the total annual value of flexible, mono- and multi-layer plastic or metallic films converted into pouches, bags, lidding, blister webs, and overwraps that safeguard pharmaceuticals, diagnostic kits, and medical devices from manufacture to point of care.

Scope exclusion: Films destined for food, cosmetics, or industrial items, as well as rigid trays, paper, and foil-only solutions, are not counted.

Segmentation Overview

- By Material Type

- Plastic Films

- Polyethylene (LDPE, HDPE, LLDPE)

- Polypropylene

- Polyvinyl Chloride

- Polycarbonate

- Polyethylene Terephthalate

- Polyamide

- Ethylene Vinyl Alcohol Copolymer (EVOH)

- Bioplastics

- Metallic and Aluminum Films

- Plastic Films

- By Product Type

- Thermoformable Films

- Breathable and Porous Films

- High-Barrier Films

- Co-extruded and Laminated Films

- By Application

- Bags and Pouches

- Blister Packs

- Tubes and Form-Fill-Seal

- Lidding and Sachets/Stick Packs

- Diagnostic Strip and Pouch Laminates

- By End-user

- Pharmaceutical Manufacturing

- Medical Device Manufacturers

- Diagnostic Laboratories

- Hospitals and Clinics

- Home Healthcare Kit Assemblers

- By Technology

- Blown Film Extrusion

- Cast Film Extrusion

- Solvent / Extrusion Coating

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- GCC

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with film extruders, medical-device sterilizers, hospital supply managers, and regional regulators across North America, Europe, and Asia-Pacific enabled us to confirm barrier-spec preference shifts, validate average selling prices, and fine-tune replacement-rate assumptions that secondary data could only approximate.

Desk Research

We first mapped global demand drivers using open datasets such as WHO Health Expenditure, UN Comtrade film trade codes, U.S. FDA 510(k) clearances, and EU Eudamed registrations, which helped size treated-patient and device shipment pools. Industry associations, notably the Flexible Packaging Association and the Healthcare Plastics Recycling Council, offered adoption ratios, while company 10-Ks and investor decks revealed film pricing corridors. Paid intelligence from D&B Hoovers and Dow Jones Factiva supplied revenue splits and plant capacities. The sources named are illustrative; many additional publications informed data checks.

Market-Sizing & Forecasting

A hybrid top-down build (global pharmaceutical output and medical-device shipments reconstructed from production and trade data, then filtered through packaging intensity ratios) is cross-checked with selective bottom-up roll-ups of leading converter sales to ensure realism. Key variables include polymer price indices, chronic-disease prevalence, ISO 11607 sterilization method mix, blister-pack share in solid-dose drugs, and extrusion capacity utilization. Forecasts use multivariate regression blended with scenario analysis to reflect raw-material volatility and regulatory tightening. Where bottom-up gaps arise, for example in private-label converter volumes, we interpolate using median regional ASP×volume proxies anchored to verified customs records.

Data Validation & Update Cycle

Outputs pass variance screens against historical growth bands, peer benchmarks, and channel feedback, followed by a two-stage analyst review. The dataset refreshes annually; interim events such as resin price spikes or major M&A trigger expedited re-runs before any client delivery.

Why Mordor's Medical Packaging Films Baseline Commands Reliability

Published estimates diverge because firms choose different film types, conversion stages, and forecast cadences.

Our disciplined scoping and yearly refresh keep our baseline current and decision-ready.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.13 B (2025) | Mordor Intelligence | - |

| USD 7.8 B (2023) | Regional Consultancy A | Excludes barrier-coated PE and uses two-year-old base year |

| USD 9.36 B (2025) | Global Consultancy B | Blends volume and value, applies uniform 3% inflation uplift, limited primary checks |

These comparisons show that, by selecting the right scope and validating each assumption with market participants, Mordor Intelligence delivers a balanced, transparent baseline clients can trace and replicate.

Key Questions Answered in the Report

What is the current value of the medical packaging films market?

The market is worth USD 8.52 billion in 2026 and is projected to reach USD 10.75 billion by 2031.

Which technology segment is growing the fastest?

Blown film extrusion leads growth with a 6.66% CAGR for 2026-2031 as demand rises for multilayer, high-barrier structures.

Why is Asia-Pacific the most attractive region for suppliers?

Pharmaceutical capacity expansion in China, India, and the Philippines drives 38.21% of global revenue in 2025 and a 6.11% regional CAGR to 2031.

How are sustainability goals influencing material choices?

Hospitals and regulators now favor recyclable or bio-based films, prompting suppliers to launch PLA/PHA blends and PCR-rich polyolefins that still meet sterilization standards.

What role does serialization play in market growth?

FDA DSCSA requirements effective 2024 and EU Falsified Medicines rules fuel demand for films that can carry serialized barcodes and embedded NFC or RFID tags.

Page last updated on: