Flexitank Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

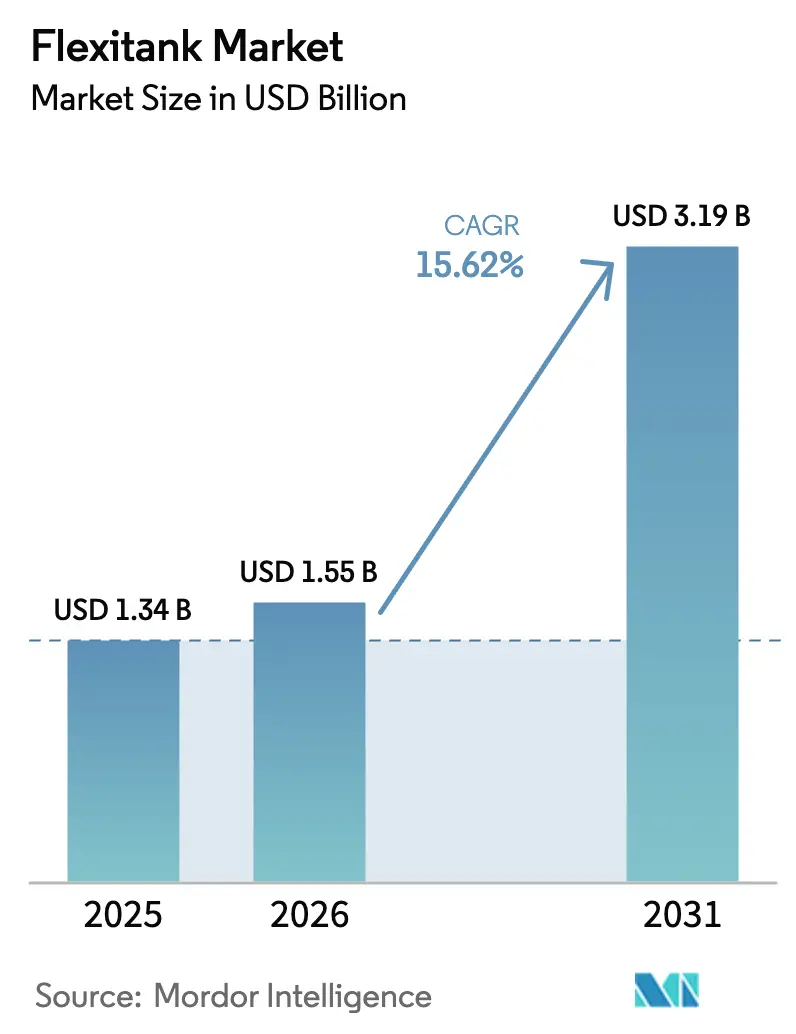

| Market Size (2026) | USD 1.55 Billion |

| Market Size (2031) | USD 3.19 Billion |

| Growth Rate (2026 - 2031) | 15.62% CAGR |

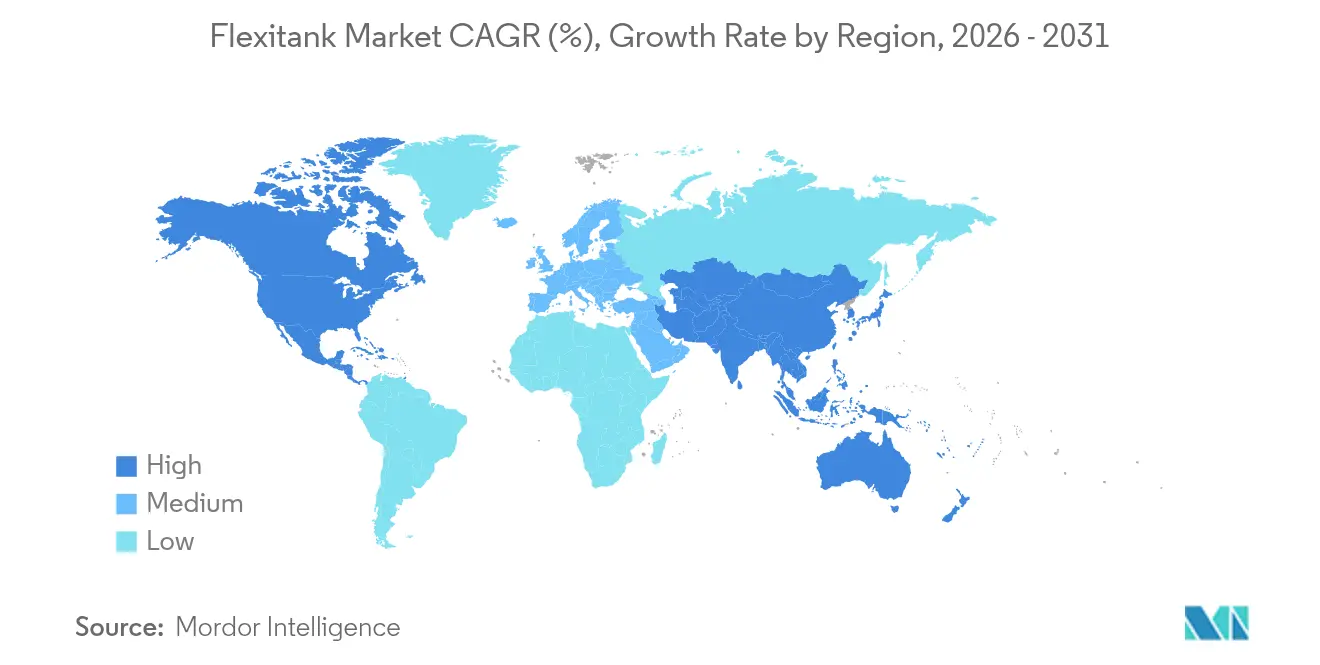

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flexitank Market Analysis by Mordor Intelligence

The flexitank market size in 2026 is estimated at USD 1.55 billion, growing from 2025 value of USD 1.34 billion with 2031 projections showing USD 3.19 billion, growing at 15.62% CAGR over 2026-2031. Growth gathers pace as shippers replace heavier ISO tanks and drums with lightweight bulk-liquid bags that help them curb freight bills, lower carbon levies, and avoid container repositioning charges. The International Maritime Organization (IMO) net-zero rules entering force in 2027 give weight-saving solutions a regulatory advantage, while steady port investments across emerging economies broaden the addressable customer base. Food-grade certification, barrier-film innovation, and temperature-controlled handling protocols continue to improve product integrity, supporting wider adoption in premium wine, edible oils, and pharmaceutical intermediates. Although more than 25 suppliers vie for contracts, service integration and material technology differentiate leaders that can demonstrate end-to-end quality management.

Key Report Takeaways

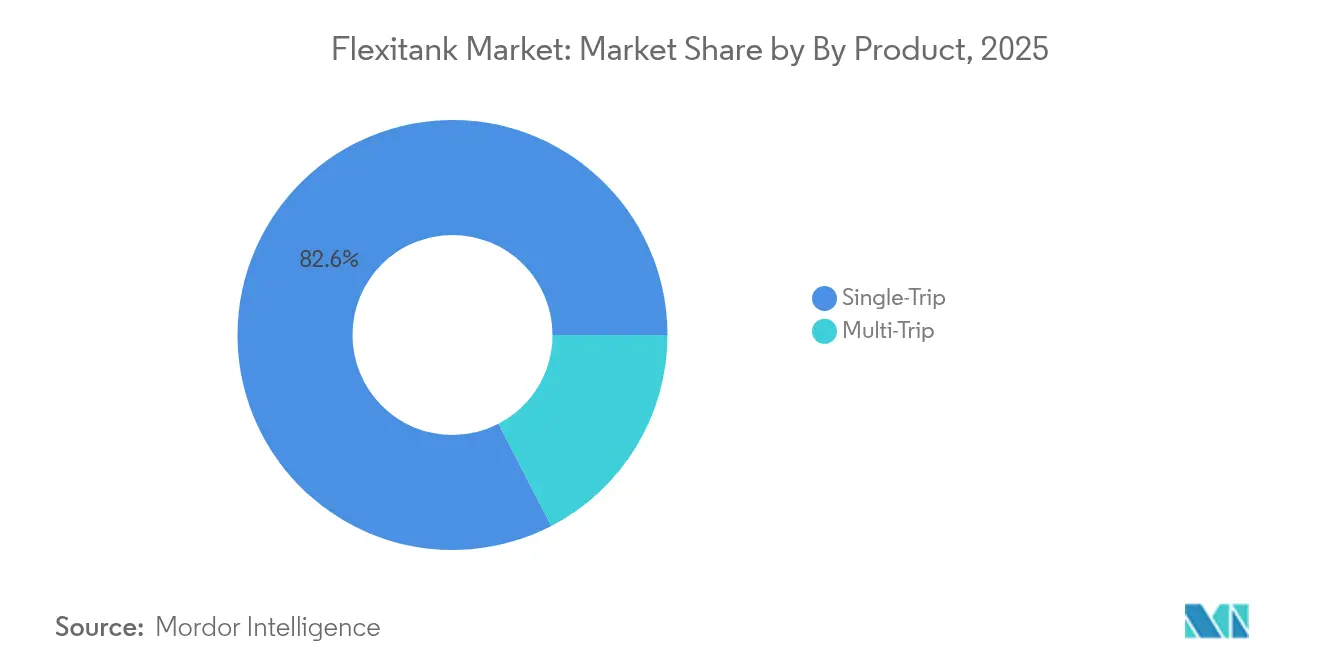

- By product type, single-trip bags led with 82.60% revenue share in 2025, while multi-trip variants are projected to expand at an 18.06% CAGR to 2031.

- By capacity, 24,001-26,000 liter units held 47.10% of the flexitank market size in 2025; >26,000 liter formats post the fastest growth at 16.85% CAGR through 2031.

- By material, polyethylene maintained 72.10% flexitank market share in 2025, whereas multi-layer composites are growing at 15.52% CAGR.

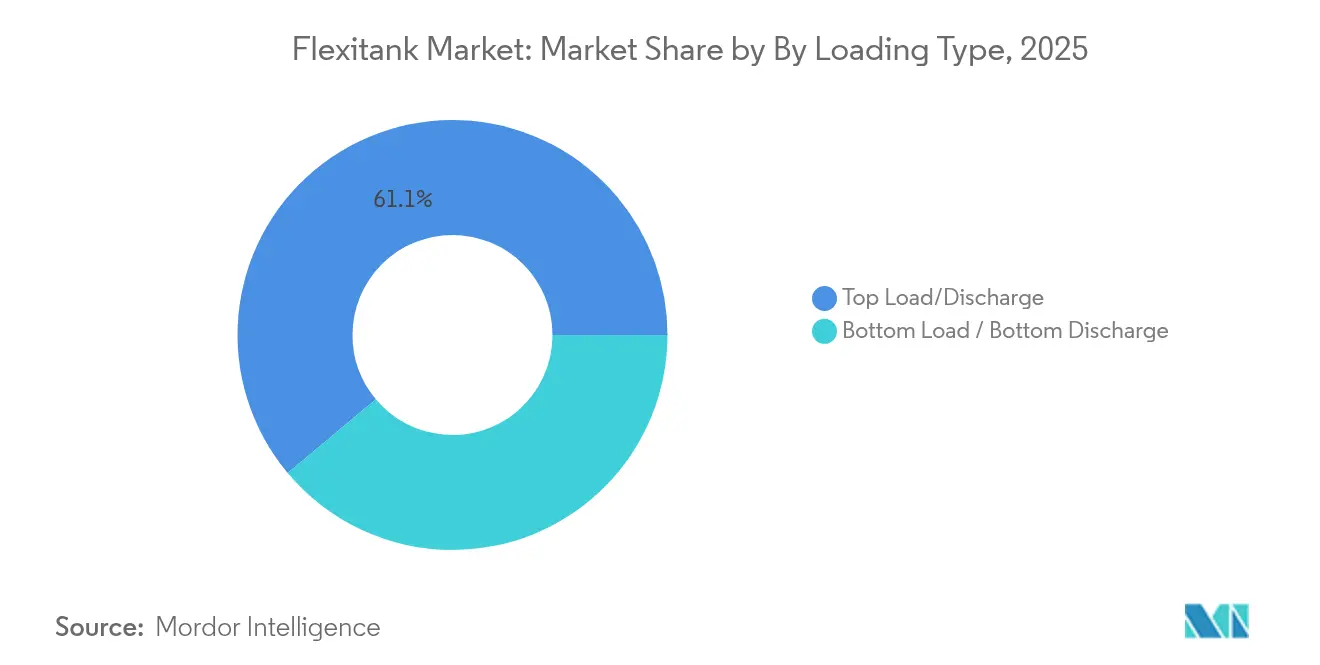

- By loading type, top-load/top-discharge designs retained 61.10% share of the flexitank market in 2025; bottom-discharge systems exhibit 17.25% CAGR.

- By end user, food and beverage applications accounted for 37.60% of the flexitank market size in 2025, with wine and spirits advancing at 19.10% CAGR.

- By geography, Asia-Pacific contributed 49.20% of global revenue in 2025, while Africa is forecast to record a 15.66% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Flexitank Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-effective alternative to ISO tanks and drums | +3.2% | Global, higher in cost-sensitive emerging markets | Medium term (2-4 years) |

| Rising demand for bulk transport of non-hazardous liquids | +2.8% | Asia-Pacific core; spill-over to MEA & South America | Long term (≥ 4 years) |

| Expansion of food-grade logistics in emerging markets | +2.1% | Africa, South America, ASEAN | Long term (≥ 4 years) |

| Lower container repositioning costs for shippers | +1.9% | Global, notably Asia-Europe and trans-Pacific | Medium term (2-4 years) |

| Surge in Southern-Hemisphere wine exports | +1.4% | South America, Australia, New Zealand | Short term (≤ 2 years) |

| IMO decarbonization rules favor lighter payloads | +2.3% | Global routes; EU and North America lead | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost-effective Alternative to ISO Tanks and Drums

Volatile container freight rates keep the economics of liquid logistics under scrutiny. Flexitanks lower total shipping costs by up to 30% because they remove tank-cleaning, storage, and backhaul charges while maximizing payload in standard 20-foot boxes Qingdao BLT Flexitank Solution Co., Ltd.. Their sterile, single-use build eliminates cross-contamination risk, a major pain point for kosher and halal cargo. Cost advantages are most pronounced in developing corridors where empty ISO tank repositioning can exceed ocean freight spend. Scale producers have therefore begun to embed flexitank shipping into annual tenders to stabilise landed costs and improve cash conversion cycles, Logistics IT.

Rising Demand for Bulk Transport of Non-Hazardous Liquids

Demand once centered on commodity chemicals now includes edible oils, liquid sweeteners, and specialty additives. Bulk shipping trims secondary packaging reduces handling labour, and cuts landfill waste, aligning with brand-owner sustainability targets. Olive-oil exporters in Spain and palm-oil shippers in Indonesia report double-digit volume shifts toward flexitank loading, citing FDA-approved film grades and compatibility with intermodal rail and short-sea services. Qingdao BLT Flexitank Solution Co., Ltd. Emerging export nations see particular benefit because bulk format lets them consolidate output into fewer sailings, smoothing seasonal capacity swings and improving working-capital turnover.

Expansion of Food-Grade Logistics in Emerging Markets

Africa and parts of South America are scaling food-processing clusters faster than cold-chain investments can keep pace. Food-grade flexitanks, produced from certified polyethylene and polypropylene films, fill the gap by giving exporters a compliant, sealed environment that meets EU and US import regulations. Container ship calls to African ports climbed 20% between 2018 and 2023, underscoring a wider logistics upgrade that now extends to inland depots United Nations Conference on Trade and Development. The Port of Banana project in the Democratic Republic of Congo alone is expected to unlock USD 1.12 billion in additional trade once operational, intensifying the need for safe, bulk-liquid options Health and Safety International.

IMO Decarbonization Rules Favor Lighter Container Payloads

The IMO net-zero framework mandates carbon-pricing and emissions ceilings starting 2027, covering vessels responsible for 85% of maritime CO₂, International Maritime Organization. Flexitanks, weighing less than 70 kilograms when empty, contrast sharply with a 3,600-kilogram steel ISO tank, allowing carriers to cut fuel consumption and shrink emissions‐fee exposure. Shippers that document such savings can apply them against Scope 3 targets, making flexitank adoption a straightforward route to meet the 40% CO₂ reduction milestone set for 2030 The Maritime Executive. Manufacturers are responding by publishing cradle-to-gate life-cycle assessments that quantify every kilogram of avoided CO₂, improving tender evaluations.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited awareness and trained operators in developing regions | -1.8% | Africa, parts of South America and ASEAN | Medium term (2-4 years) |

| Infrastructure constraints at secondary ports and depots | -1.4% | Secondary ports in emerging markets | Long term (≥ 4 years) |

| Scrutiny over single-use plastic disposal | -0.9% | EU, North America | Short term (≤ 2 years) |

| Insurance premium hikes after leakage claims | -0.7% | Global, higher in low-skill regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Awareness and Trained Operators in Developing Regions

Correct bag fitting, valve torque, and container lining procedures demand certified technicians, yet many secondary African and Latin American ports lack structured training pipelines. Mis-installation can spark spills that damage terminal floors and cargo, raising reluctance among local shippers. Manufacturers now roll out mobile academies and e-learning modules, but scaling competency fast enough to match market growth remains an open challenge.

Infrastructure Constraints at Secondary Ports and Depots

Smaller terminals often lack heated pumps, sterile hoses, or spill basins, lengthening discharge cycles and diminishing the economic edge that flexitank users expect. Temperature-sensitive cargo like cocoa butter or latex struggles when shore tanks cannot maintain viscosity or prevent crystallization. Gulf and Mediterranean investors—DP World and AD Ports among them—are funding berth-side pipelines and modular heating skids to close these gaps, yet roll-out timelines stretch across multiple budget cycles[2]Botho, “African Port Investments and Logistics Gaps,” botho.cloud.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Single-Trip Dominance Faces Multi-Trip Challenge

Single-trip designs maintained 82.60% of 2025 revenue, underscoring industry reliance on contamination-free shipping for food-grade flows. Multi-trip systems, however, are posting an 18.06% CAGR as ESG scorecards push brand owners to curb single-use plastics. These reusable variants integrate thicker films and RFID tags to verify cleaning history, answering procurement calls for life-cycle transparency. While single-trip bags keep their edge in premium olive oil, cocoa butter, and kosher syrups, tire sealant and industrial enzymes are migrating to multi-turn models as chemical compatibility matrices expand.Corporate climate pledges inside the European Green Deal reward returnable packaging, and shipper interest is now deep enough for service providers to run back-haul consolidation programs that achieve 60% reload rates. As a result, suppliers that marry efficient wash depots with digital asset tracking are grabbing share without price discounting, indicating the flexitank market is tilting toward a service-plus-product proposition.

By Capacity: Mid-Range Leadership with Large-Capacity Growth

Bags sized 24,001-26,000 L delivered 47.10% of 2025 billings and remain the logistical sweet spot for balancing container payload ceilings with port crane limits. Growing interest in 26,000 L-plus units mirrors commodity players’ need to squeeze every liter into scarce equipment amid red-hot freight rates. Tonnage restricted by IMO fuel-economy curves also prods operators to select a single mega-bag rather than multiple IBCs, reducing total container moves and associated emissions.Engineers are reinforcing wall structures and dome ends so that >26,000 L bags withstand at-sea sloshing without deformation, and early adopters have reported 15% fewer stuffing hours due to the switch. Nonetheless, mid-range bags keep favor in temperature-controlled cargo where insulation liners add kilograms that nibble at overall weight thresholds. The flexitank market continues to calibrate size optimization against regional axle-load statutes, leaving product managers to offer a wide spectrum rather than a monolithic capacity choice.

By Material: Polyethylene Dominance Challenged by Composite Innovation

Polyethylene films held 72.10% share in 2025 thanks to global resin availability, ease of welding, and robust food-contact certifications. Composite structures featuring EVOH or nylon barrier layers are growing 15.52% annually, cutting oxygen transmission by up to 50% and unlocking high-value wine, premium juice, and craft-beverage lanes. Jurisdictions piloting extended producer responsibility (EPR) rules now credit multilayer bags containing recycled or bio-based polymers, spurring R&D in dual-purpose sustainability and performance.Polypropylene liners sustain a niche in hot-fill edible oil and molten chocolate scenarios due to heat deflection temperatures above 100 °C, while proprietary elastomer blends are appearing in latex applications where polymer leaching matters. As composite recipes proliferate, certification agencies such as TÜV expand test protocols to cover flavor scalping and peroxide formation, ensuring safe entry into stringent Japanese and US beverage markets.

By Loading Type: Top Load Preference with Bottom Discharge Growth

Top load/top discharge configurations commanded 61.10% turnover in 2025 because they couple seamlessly with gravity-feed fillers common at edible-oil refineries. Bottom discharge variants, posting 17.25% CAGR, streamline unloading at inland depots where pump suction can be mounted directly onto a lower valve, cutting residual loss below 1% by volume. Recent valve redesigns embed anti-vacuum vents that accelerate discharge without risking cavitation, and rail operators laud the lower center of gravity that bottom valves provide.Nonetheless, ports with limited spill-containment trays hesitate to approve bottom fittings, and insurers sometimes insist on secondary pallet bunds before granting coverage. The flexitank market is responding with dual-valve hybrid systems that allow users to pick a discharge path based on terminal readiness, boosting bag versatility and asset utilization.

By End User: Food & Beverage Leadership with Wine and Spirits Acceleration

Food and beverage filled 37.60% of 2025 revenue as global diets leaned toward processed liquids in shelf-stable formats. Bulk orange concentrate, coconut water, and corn syrup each adopted flexitanks to evade glass breakage and lower CO₂ footprints compared with bottled shipping. Wine & spirits are rocketing at 19.10% CAGR because Southern Hemisphere vintners treat bulk shipping as a hedge against soaring glass and carton costs; EVOH-lined bags now preserve bouquet for voyages exceeding 40 days.Non-hazardous chemicals—lube stocks, surfactants, fertilizers—continue steady uptake, galvanized by 120% container rate spikes between 2023 and 2024 that made flexitanks’ payload advantage too large to ignore. Pharmaceutical intermediates represent a diffusion frontier requiring ISO 22000 and GDP audit trails, and suppliers investing early in pharma-grade validation could claim premium margins once volume scales.

Geography Analysis

Asia-Pacific accounted for 49.20% of global revenue in 2025, powered by China’s resin supply chain, India’s surging food-processing output, and dense intra-regional shipping routes. Korea and Japan underpin barrier-film R&D, feeding regional demand for high-performance bags. ASEAN producers of palm and coconut oils rely on flexitanks to bypass drum export tariffs and enjoy a 15% payload gain versus reconditioned IBCs, cementing APAC as the flexitank market’s anchor. Australia and New Zealand capitalize on counter-seasonal grape harvests to ship uncased wine to UK bottlers, aligning volume peaks with Northern Hemisphere off-season demand.

Africa is projected to post a 15.66% CAGR through 2031, the fastest globally, assisted by DP World and AD Ports-backed terminals in Tanzania and Congo that introduce deep-draft berths and food-grade stuffing sheds. Container calls on the continent rose 20% from 2018-2023, drawing edible-oil refiners and beverage mixers into regional export playbooks. New corridors reduce voyage legs to EU markets by four days on average, and shippers choosing flexitanks skirt return-container deficits that historically plagued northbound African lanes.

North America and Europe remain steady but opportunity-rich, as both regions codify plastic-waste levies encouraging multi-trip bag trials. IMO regulations entering force in 2027 will force North Atlantic carriers to itemize carbon fees, where flexitank’s lightweight edge can erase 2-4 t of CO₂ per 5,000 NM run. South America benefits from soaring demand for Argentine and Chilean bulk wine, plus Brazilian soy-oil and citrus concentrate flows heading to Asia, making the region a dependable volume contributor despite infrastructure heterogeneity.

Competitive Landscape

The flexitank market hosts over 25 active manufacturers, none exceeding a double-digit global share, yielding a low-concentration environment ripe for consolidation. Braid Logistics, JF Hillebrand, and HOYER differentiate through integrated shipping and value-added services such as inland drayage, while Asian producers like Qingdao BLT leverage cost leadership and regional factory proximity. Patent activity in multilayer oxygen-barrier films underscores material innovation as a durable moat; more than a dozen US and EU filings since 2024 target EVOH and polyamide co-extrusions that enhance shelf life for sensitive drinks.

Strategic moves include Kenan Advantage Group’s 2025 acquisition of M.C. Tank Transport, extending chemical hauling synergies into flexitank support fleets. Suppliers increasingly invest in digital telemetry—temperature and pressure sensors feeding voyage dashboards—giving shippers granular cargo assurance and a route to premium pricing. Regional service partners are also forming franchise models to cover installation and after-sales in under-served ports, indicating the industry is professionalizing its support ecosystem.

Consolidation prospects remain robust: smaller firms lacking capital for composite-film R&D or global depot networks represent acquisition targets for logistics majors seeking to cross-sell. Meanwhile, recyclers testing chemical depolymerization of used liners could create circular supply loops that shift bargaining power toward vertically integrated players owning both virgin and recycled feedstock channels.

Flexitank Industry Leaders

Braid Logistics UK

Hengxin Plastic Co. Ltd.

JF Hillebrand GROUP AG

SIA Flexitanks Ltd.

MY FlexiTank Industries Sdn Bhd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Qingdao BLT Flexitank Solution Co. launched FDA-compliant oil bags offering up to 30% logistics cost savings.

- April 2025: IMO approved net-zero rules for vessels over 5,000 GT, effective 2027, cementing carbon-price incentives for lightweight cargo systems.

- April 2025: Kenan Advantage Group completed the acquisition of M.C. Tank Transport, adding 100 tractors and 500 trailers to its chemical transport portfolio.

- January 2025: Liquitank Solutions announced advanced material upgrades aimed at heightened operational efficiency.

Global Flexitank Market Report Scope

Flexitanks, bulk liquid bladder pouches, enable shippers to maximize the liquid capacity of dry containers. Each flexitank can hold up to 24,000 liters and is crafted from multiple layers of flexible, durable plastic film, ensuring the safe storage of its liquid contents.

The flexitank market is segmented by product (single-trip, multi-trip), end-user (food, wine & spirits, chemicals and oil, pharmaceutical goods, others end users), geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Single-Trip |

| Multi-Trip |

| Less Than 24,000 L |

| 24,001-26,000 L |

| More Than 26,000 L |

| Polyethylene (PE) |

| Polypropylene (PP) |

| Multi-layer Composite |

| Top Load / Top Discharge |

| Bottom Load / Bottom Discharge |

| Food and Beverage |

| Chemicals |

| Wine and Spirits |

| Pharmaceutical Goods |

| Industrial Products (Lube Oils, Additives) |

| Agricultural Liquids |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Rest of Europe | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| By Product | Single-Trip | ||

| Multi-Trip | |||

| By Capacity | Less Than 24,000 L | ||

| 24,001-26,000 L | |||

| More Than 26,000 L | |||

| By Material | Polyethylene (PE) | ||

| Polypropylene (PP) | |||

| Multi-layer Composite | |||

| By Loading Type | Top Load / Top Discharge | ||

| Bottom Load / Bottom Discharge | |||

| By End User | Food and Beverage | ||

| Chemicals | |||

| Wine and Spirits | |||

| Pharmaceutical Goods | |||

| Industrial Products (Lube Oils, Additives) | |||

| Agricultural Liquids | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics | |||

| Rest of Europe | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

Key Questions Answered in the Report

What is the current flexitank market size?

The flexitank market size stands at USD 1.55 billion in 2026 and is projected to reach USD 3.19 billion by 2031.

How do IMO decarbonization rules affect flexitank demand?

The rules impose carbon costs that reward lighter payloads, making flexitanks a fuel-saving alternative to heavier ISO tanks and driving higher adoption.

Which region grows fastest in the flexitank market?

Africa leads with a forecast 15.66% CAGR through 2031, buoyed by new deep-water ports and expanding food-grade logistics.

Which end-use segment is expanding quickest?

Wine and spirits are increasing at a 19.10% CAGR as oxygen-barrier films now protect quality during long ocean voyages.

Why are multi-trip flexitanks gaining popularity?

Reusable bags align with ESG goals, lower life-cycle costs, and meet stricter single-use plastic regulations in Europe and North America.

Page last updated on: